As filed with the Securities and Exchange Commission on April 10, 2013

SECURITIES AND EXCHANGE COMMISSION

WASHINGTON, D.C. 20549

FORM 20-F

|

o

|

REGISTRATION STATEMENT PURSUANT TO SECTION 12(b) OR (g) OF THE SECURITIES EXCHANGE ACT OF 1934

|

OR

|

x

|

ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934

|

For the fiscal year ended December 31, 2012

OR

|

o

|

TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934

|

OR

|

o

|

SHELL COMPANY REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934

|

Commission file number: 001-12568

BBVA BANCO FRANCÉS S.A.

(Exact name of Registrant as specified in its charter)

BBVA FRENCH BANK

(Translation of Registrant’s name into English)

Republic of Argentina

(Jurisdiction of incorporation or organization)

Reconquista 199

Reconquista 199

(C1003ABB) Buenos Aires. Republic of Argentina

(Address of principal executive offices)

Adrián Bressani – 011-54-11-4346-4286 – abressani @bbvafrances.com.ar – Reconquista 281 3° (C1003ABE) Buenos Aires, Republic of Argentina

(Name, Telephone, E-mail and/or Facsimile number and Address of Company Contact Person)

Securities registered or to be registered pursuant to Section 12(b) of the Act:

|

Title of each class

|

Name of each exchange on which registered

|

|

|

American Depositary Shares, each representing the right to receive three ordinary shares, par value Ps.1.00 per share

|

New York Stock Exchange

|

|

|

Ordinary shares, par value Ps.1.00 per share

|

New York Stock Exchange*

|

|

*

|

The ordinary shares are not listed for trading, but are listed only in connection with the registration of the American Depositary Shares, pursuant to requirements of the New York Stock Exchange.

|

Securities registered or to be registered pursuant to Section 12(g) of the Act: None

Securities for which there is a reporting obligation pursuant to Section 15(d) of the Act: None

The number of outstanding shares of each of the classes of capital or common stock of the registrant

as of the close of the period covered by the annual report:

|

Title of class

|

Number of shares outstanding

|

|

|

Ordinary Shares, par value Ps.1.00 per share

|

536,877,850

|

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the

Securities Act

.

o

Yes

x

No

If this report is an annual or transition report, indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or 15(d) of the Securities Exchange Act of 1934.

o

Yes

x

No

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports)

,

and (2) has been subject to such filing requirements for the past 90 days:

x

Yes

o

No

Indicate by check mark whether the registrant has submitted electronically and posted on its corporate Web site, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T (§232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files).

o

Yes

o

No

Indicate by check mark if the registrant is a large accelerated filer, an accelerated filer, or a non-accelerated filer. See definition of “accelerated filer and large accelerated filer” in Rule 12b-2 of the Exchange Act. (Check one):

Large accelerated filer

o

Accelerated filer

x

Non-accelerated filer

o

Indicate by check mark which basis of accounting the registrant has used to prepare the financial statements included in this filing:

|

U.S. GAAP

o

|

International Financial Reporting Standards

by the International Accounting Standards o Board as issued |

Other

x

|

If “Other” has been checked in response to the previous question, indicate by check mark which financial statement item the registrant has elected to follow.

o

Item 17

x

Item 18

If this is an annual report, indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act).

o

Yes

x

No

|

|

Page

|

|

|

1

|

||

|

1

|

||

|

2

|

||

|

PART I

|

||

|

ITEM 1.

|

3

|

|

|

ITEM 2.

|

3

|

|

|

ITEM 3.

|

3

|

|

|

ITEM 4.

|

13

|

|

|

ITEM 4A.

|

104

|

|

|

ITEM 5.

|

105

|

|

|

ITEM 6.

|

134

|

|

|

ITEM 7.

|

146

|

|

|

ITEM 8.

|

148

|

|

|

ITEM 9.

|

148

|

|

|

ITEM 10.

|

152

|

|

|

ITEM 11.

|

162

|

|

|

ITEM 12.

|

167

|

|

|

PART II

|

||

|

ITEM 13.

|

169

|

|

|

ITEM 14.

|

169

|

|

|

ITEM 15.

|

169

|

|

|

ITEM 16A.

|

171

|

|

|

ITEM 16B.

|

171

|

|

|

ITEM 16C.

|

172

|

|

|

ITEM 16D.

|

172

|

|

|

ITEM 16E.

|

172

|

|

|

ITEM 16F.

|

172

|

|

|

ITEM 16G.

|

172

|

|

|

PART III

|

||

|

ITEM 17.

|

176

|

|

|

ITEM 18.

|

176

|

|

|

ITEM 19.

|

176

|

|

This Form 20-F contains words, such as “believe”

, “expect”, “estimate”, “intend”, “plan”, “may” and “anticipate” and similar expressions, that identify forward-looking statements, which reflect our views about future events and financial performance. Actual results could differ materially as a result of factors beyond our control, including but not limited to:

|

|

§

|

changes in general economic, business or political or other conditions in the Republic of Argentina (“Argentina”) or changes in general economic or business conditions in Latin America;

|

|

|

§

|

changes in capital markets in general that may affect policies or towards lending to Argentina or Argentine companies;

|

|

|

§

|

increased costs and decreased income related to macroeconomic variables such as exchange rates and the Consumer Price Index (“CPI”);

|

|

|

§

|

unanticipated increases in financing and other costs or the inability to obtain additional debt or equity financing on attractive terms; and

|

|

|

§

|

the factors discussed under

“Item 3. Key Information—D. Risk Factors”

.

|

Accordingly, readers are cautioned not to place undue reliance on these forward-looking statements, which speak only as of the date hereof. BBVA Francés undertakes no obligation to update or revise these forward-looking statements or to publicly release the results of any revisions to these forward-looking statements. The accompanying information in this annual report, including, without limitation, the information under

“Item 4. Information on the Company”

,

“Item 5. Operating and Financial Review and Prospects”

and

“Item 11. Quantitative and Qualitative Disclosures About Market Risk”

identifies important factors that could cause material differences between any forward-looking statements and actual results.

General

BBVA

Banco Francés S.A. (“BBVA Francés”)

is an Argentine bank and maintains its financial books and records in Argentine pesos and prepares its Consolidated Financial Statements in conformity with the accounting rules of the Banco Central de la República Argentina (the “Central Bank” or “BCRA”) related thereto (“Argentine Banking GAAP”), which differ in some respects from generally accepted accounting principles in Argentina (see Note 4 to our Consolidated Financial Statements) and the accounting principles in the United States (“U.S. GAAP”). See Note 22 to our Consolidated Financial Statements for a description of the principal differences between Argentine Banking GAAP and U.S. GAAP, as they relate to us, and a reconciliation to U.S. GAAP of net income and total stockholders’ equity. In this annual report, references to “$”, “U.S.$” and “dollars” are to United States dollars, references to “Ps.” or “pesos” are to Argentine pesos. Percentages and certain dollar and peso amounts have been rounded for ease of presentation. Unless otherwise stated, all market share and other industry information has been derived from information published by the Central Bank.

The Consolidated Financial Statements are presented in accordance with the guidelines of Technical Resolution Nr. 21 of the Argentine Federation of Economic Sciences Professional Association (Federación Argentina de Consejos Profesionales de Ciencias Económicas—“FACPCE”) and the disclosure standards set by the Central Bank.

The Bank presents its Consolidated Financial Statements in equivalents purchasing power. These Consolidated Financial Statements recognize the effects of the changes in the purchasing power of the currency through February 28, 2003, following the restatement method established by FACPCE Technical Resolution Nr. 6 (modified by Technical Resolution Nr. 19), using an adjustment rate derived from the Argentine internal Wholesale Price Index published by the National Institute of Statistics and Census (“INDEC”) of Argentina.

According to the above-mentioned method, the accounting measurements were restated by the purchasing power changes through August 31, 1995. As of that date, based on the prevailing economic stability conditions and according to the National Securities Commission (“CNV”) General Resolution Nr. 272 and Central Bank Communication “A” 2365, the accounting measures were not restated through December 31, 2001. In view of CNV General Resolution Nr. 415 and Central Bank Communication “A” 3702, the method was reinstated effective as of January 1, 2002, considering the previous accounting measures restated as of December 31, 2001.

By Communication “A” 3921 of the Central Bank and General Resolution Nr. 441/03 of the CNV, in compliance with Decree Nr. 664/03 of the Federal Executive, application of the restatement method to Consolidated Financial Statements in equivalent purchasing power has been suspended as of March 1, 2003. Accordingly, BBVA Banco Francés S.A. applied the mentioned restatement method until February 28, 2003.

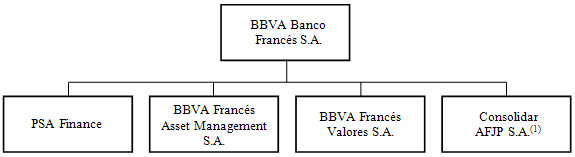

Unless otherwise indicated, financial information contained in this annual report reflects the consolidation of the following subsidiaries at and for the fiscal years indicated below:

|

|

December 31,

|

||

|

Entity

|

2012

|

2011

|

2010

|

|

PSA Finance Argentina Compañía Financiera S.A.

|

X

|

X

|

X

|

|

Consolidar AFJP S.A. (undergoing liquidation proceedings)

|

X

|

X

|

X

|

|

Consolidar Cía. de Seguros de Retiro S.A.

(1)

|

X

|

||

|

BBVA Francés Valores Sociedad de Bolsa S.A.

|

X

|

X

|

X

|

|

BBVA Francés Asset Management S.A. Sociedad Gerente de Fondos Comunes de Inversión

|

X

|

X

|

X

|

|

(1)

|

See Note 1.4 to the Consolidated Financial Statements.

|

On January 7, 2002, Argentina abandoned the peso-dollar parity introduced in April 1991 under Law Nr. 23,928 (the “Convertibility Law”). Following the initial devaluation and the setting of an official rate exchange at Ps.1.4 per U.S.$1.00, the peso was allowed to float, and as of April 5, 2013 traded at approximately Ps.5.1370 per U.S.$1.00. See

“

Item 3. Key Information—

Exchange Rates”

for information regarding the evolution of rates of exchange since fiscal year 2008.

As used in this Form 20-F, “BBVA Francés”, the “Bank”, the “Company” and terms such as “we”, “us” and “our” mean BBVA Banco Francés S.A. and its consolidated subsidiaries unless the context otherwise requires.

- PART I -

Not applicable.

Not applicable.

Not applicable.

|

A.

|

Selected Financial Data

|

The information in this section has been selected from the Consolidated Financial Statements as of the dates and for the fiscal years indicated. This information should be read in conjunction with, and is qualified in its entirety by reference to,

“Risk Factors”

, the Consolidated Financial Statements and the related notes. The selected financial data for the fiscal years ended December 31, 2012, 2011, 2010, 2009 and 2008 are derived from the Consolidated Financial Statements. For information concerning the preparation and presentation of the Consolidated Financial Statements, see

“Presentation of Financial Information”

.

See

“D. Risk Factors—Factors Related to Argentina”

, and

“Risk Factors—Factors Related to BBVA Francés”

.

|

For the fiscal year ended December 31,

|

||||||||||||||||||||

|

2012

|

2011 (11) | 2010 | 2009 | 2008 | ||||||||||||||||

|

(in thousands of pesos)

(1)

|

||||||||||||||||||||

|

CONSOLIDATED INCOME STATEMENT

|

||||||||||||||||||||

|

Amounts in accordance with Argentine Banking GAAP

|

||||||||||||||||||||

|

Financial income

|

5,705,193 | 3,565,030 | 3,298,259 | 3,039,470 | 1,946,432 | |||||||||||||||

|

Financial expenses

|

(2,061,131 | ) | (1,355,698 | ) | (814,673 | ) | (975,431 | ) | (1,212,738 | ) | ||||||||||

|

Gross intermediation margin

|

3,644,062 | 2,209,332 | 2,483,586 | 2,064,039 | 733,694 | |||||||||||||||

|

Provision for loan losses

|

(256,259 | ) | (132,663 | ) | (179,353 | ) | (245,966 | ) | (36,708 | ) | ||||||||||

|

Service charge income

|

2,530,197 | 1,957,724 | 1,485,442 | 1,204,703 | 981,891 | |||||||||||||||

|

Service charge expenses

|

(683,730 | ) | (519,630 | ) | (406,347 | ) | (279,691 | ) | (234,328 | ) | ||||||||||

|

Operating expenses

|

(3,039,731 | ) | (2,279,500 | ) | (1,969,461 | ) | (1,562,326 | ) | (1,149,778 | ) | ||||||||||

|

Net other (expenses) / income

|

(26,400 | ) | 254,845 | 38,867 | (44,063 | ) | 67,776 | |||||||||||||

|

Income before income tax

|

2,168,139 | 1,490,108 | 1,452,734 | 1,136,696 | 362,547 | |||||||||||||||

|

Income tax

|

(864,625 | ) | (549,992 | ) | (272,923 | ) | (362,439 | ) | (23,695 | ) | ||||||||||

|

Net income

|

1,303,514 | 940,116 | 1,179,811 | 774,257 | 338,852 | |||||||||||||||

|

Net (loss) / income on minority interests in subsidiaries

|

(37,874 | ) | 6,783 | (16,538 | ) | (17,851 | ) | (8,589 | ) | |||||||||||

|

Final consolidated income from continued operations

|

1,265,640 | 946,899 | 1,163,273 | 756,406 | 330,263 | |||||||||||||||

|

Final consolidated (loss) / income from discontinued operations

|

(1,961 | ) | 58,678 | 34,906 | (37,944 | ) | (8,753 | ) | ||||||||||||

|

Final consolidated income

|

1,263,679 | 1,005,577 | 1,198,179 | 718,462 | 321,510 | |||||||||||||||

|

Net operating revenue

(3)

|

5,490,529 | 3,647,426 | 3,562,681 | 2,989,051 | 1,481,257 | |||||||||||||||

|

Net operating income

(4)

|

2,194,539 | 1,235,263 | 1,413,867 | 1,180,759 | 294,771 | |||||||||||||||

|

Net income per ordinary shares from continued operations

(2) (9)

|

2.36 | 1.76 | 2.17 | 1.55 | 0.70 | |||||||||||||||

|

Net income per ADS from continued operations

(2) (9)

|

7.08 | 5.28 | 6.51 | 4.65 | 2.10 | |||||||||||||||

|

Net income per ordinary shares

(2) (9)

|

2.35 | 1.87 | 2.23 | 1.47 | 0.68 | |||||||||||||||

|

Net income per ADS

(2) (9)

|

7.05 | 5.61 | 6.69 | 4.41 | 2.04 | |||||||||||||||

|

Declared dividends per ordinary share

(9) (10)

|

— | — | 1.49899 | 0.98439 | 0.21215 | |||||||||||||||

|

Declared dividends per ADS

(9) (10)

|

— | — | 4.49697 | 2.95317 | 0.63645 | |||||||||||||||

|

Net operating income per ordinary shares

(2) (9)

|

4.09 | 2.30 | 2.64 | 2.42 | 0.63 | |||||||||||||||

|

Net operating income per ADS

(2) (9)

|

12.27 | 6.90 | 7.92 | 7.26 | 1.89 | |||||||||||||||

|

Average ordinary shares outstanding (000s) primary

(9)

|

536,878 | 536,620 | 536,361 | 487,611 | 471,361 | |||||||||||||||

|

Amounts in accordance with U.S. GAAP:

|

||||||||||||||||||||

|

Net income

|

1,541,104 | 698,807 | 804,101 | 1,029,755 | 910,294 | |||||||||||||||

|

Net income per ordinary share

(2) (9)

|

2.87 | 1.30 | 1.50 | 2.11 | 1.87 | |||||||||||||||

|

Net income per ADS

(2) (9)

|

8.61 | 3.90 | 4.50 | 6.33 | 5.61 | |||||||||||||||

|

Average ordinary shares outstanding (000s) primary

(9)

|

536,878 | 536,620 | 536,361 | 487,611 | 487,611 | |||||||||||||||

|

CONSOLIDATED BALANCE SHEET

|

||||||||||||||||||||

|

Amounts in accordance with Argentine Banking GAAP

|

||||||||||||||||||||

|

Cash and due from banks

|

8,614,889 | 6,353,428 | 5,691,806 | 5,255,412 | 4,243,080 | |||||||||||||||

|

Government and private securities

|

4,101,846 | 5,565,029 | 7,495,382 | 7,214,232 | 5,233,660 | |||||||||||||||

|

Loans, net of allowances

|

28,493,431 | 22,697,031 | 16,699,852 | 11,751,889 | 12,507,489 | |||||||||||||||

|

Other assets

|

3,574,413 | 4,390,157 | 2,693,206 | 2,170,060 | 3,841,236 | |||||||||||||||

|

Total assets

|

44,784,579 | 39,005,645 | 32,580,246 | 26,391,593 | 25,825,465 | |||||||||||||||

|

Deposits

|

34,165,053 | 29,165,704 | 22,461,307 | 18,334,845 | 17,079,203 | |||||||||||||||

|

Other liabilities and minority interest in subsidiaries

|

5,487,590 | 5,971,684 | 6,372,024 | 5,130,276 | 6,670,238 | |||||||||||||||

|

Total liabilities and minority interest in subsidiaries

|

39,652,643 | 35,137,388 | 28,833,331 | 23,465,121 | 23,749,441 | |||||||||||||||

|

Capital stock

|

536,878 | 536,878 | 536,361 | 536,361 | 471,361 | |||||||||||||||

|

Issuance premiums

|

182,511 | 182,511 | 175,132 | 175,132 | 175,132 | |||||||||||||||

|

Adjustments to stockholders’ equity

|

312,979 | 312,979 | 312,979 | 312,979 | 312,979 | |||||||||||||||

|

Retained earnings

|

2,835,889 | 1,042,021 | 802,385 | 658,693 | 594,391 | |||||||||||||||

|

Unrealized valuation difference

|

— | — | 88,131 | (14,133 | ) | (181,119 | ) | |||||||||||||

|

Unappropriated earnings

|

1,263,679 | 1,793,868 | 1,831,927 | 1,257,440 | 703,280 | |||||||||||||||

|

Total stockholders’ equity

|

5,131,936 | 3,868,257 | 3,746,915 | 2,926,472 | 2,076,024 | |||||||||||||||

|

For the fiscal year ended December 31,

|

||||||||||||||||||||

|

2012

|

2011 (11) | 2010 | 2009 | 2008 | ||||||||||||||||

|

(in thousands of pesos)

(1)

|

||||||||||||||||||||

|

Amounts in accordance with U.S. GAAP

|

||||||||||||||||||||

|

Total assets

|

47,552,013 | 40,367,604 | 33,448,725 | 27,760,274 | 27,199,899 | |||||||||||||||

|

Total stockholders’ equity

|

5,535,611 | 4,003,440 | 4,500,072 | 3,696,499 | 2,225,579 | |||||||||||||||

|

SELECTED RATIOS IN ACCORDANCE WITH ARGENTINE BANKING GAAP

|

||||||||||||||||||||

|

Profitability and Performance

|

||||||||||||||||||||

|

Return on average total assets

(5)

|

3.27% | 2.65% | 3.95% | 2.90% | 1.38% | |||||||||||||||

|

Return on average stockholders’ equity

(6)

|

28.51% | 24.87% | 34.86% | 30.24% | 15.98% | |||||||||||||||

|

Services charge income as a percentage of operating expenses

|

83.24% | 85.88% | 75.42% | 77.11% | 85.40% | |||||||||||||||

|

Operating expenses as a percentage of average total assets

(7)

|

7.86% | 6.37% | 6.68% | 5.98% | 4.81% | |||||||||||||||

|

Capital

|

||||||||||||||||||||

|

Stockholders’ equity as a percentage of total assets

|

11.46% | 9.92% | 11.50% | 11.09% | 8.04% | |||||||||||||||

|

Total liabilities as a multiple of stockholders’ equity

|

7.73x | 9.08x | 7.70x | 8.02x | 11.44x | |||||||||||||||

|

Credit Quality

|

||||||||||||||||||||

|

Allowances for doubtful loans as a percentage of total loans

|

1.81% | 1.91% | 2.32% | 2.79% | 1.55% | |||||||||||||||

|

Non-performing loans as a percentage of gross loans

(8)

|

0.65% | 0.45% | 0.47% | 1.00% | 0.87% | |||||||||||||||

|

Allowances for doubtful loans as a percentage of non-performing loans

(8)

|

278.79% | 422.14% | 492.96% | 277.93% | 177.50% | |||||||||||||||

|

(1)

|

Except net income per-ordinary share and net income per-ADS data and financial ratios.

|

|

(2)

|

Assumes average ordinary shares outstanding in each period. The cash dividend amounts do not reflect any deduction for certain charges that are taken with regards to the “American Depositary Receipts”.

|

|

(3)

|

Includes: financial income, financial expenses, service charge income and service charge expenses.

|

|

(4)

|

Includes: financial income, financial expenses, provision for loan losses, services charge income, service charge expenses and operating expenses.

|

|

(5)

|

Net income as a percentage of average total assets, computed as the average of fiscal-year-beginning and fiscal-year-ending balances.

|

|

(6)

|

Net income as a percentage of average stockholders’ equity, computed as the average of fiscal-year-beginning and fiscal-year-ending balances.

|

|

(7)

|

Operating expenses as a percentage of average total assets, computed as the average of fiscal-year-beginning and fiscal-year-ending balances.

|

|

(8)

|

Non-performing loans include all loans to borrowers classified as “Problem”, “Medium Risk”, “High Risk of Insolvency”, “High Risk”, “Irrecoverable” and “Irrecoverable for Technical Decision” according to the Central Bank’s loan classification system as well as all loans contractually past due 90 days or more. See “

|

|

(9)

|

The average ordinary shares outstanding was computed as the average of the previous twelve months.

|

|

(10)

|

For the fiscal years ended December 31, 2012 and 2011, the Bank decided not to declare and distribute dividends as result of the issuance of Communications “A” 5272 and 5273 of the Central Bank (see

“Item 8. Financial Information—Dividends”)

. For the fiscal years ended December 31, 2010 and 2009, the dividends were paid totally in cash. For the fiscal year ended December 31, 2008 the dividends paid in 2009 were Ps.35 million in cash and Ps.65 million through the issue of new shares.

|

|

(11)

|

See Note 3.3 to our Consolidated Financial Statements.

|

Declared Dividends

The table below shows the declared dividends paid on each ordinary share and the equivalent of those dividends expressed in terms of dividends per American Depositary Share, each representing three ordinary shares (the “ADSs”), in each case adjusted for all stock dividends during the relevant periods. The Central Bank requires that we maintain 20% of our net income in legal reserves.

|

Decla

red

Dividends

Per Ordinary Share

(6)

|

Declared Dividends

Per ADS

(6)

|

|||||||||||||||

|

Ps.

(1)

|

U.S.$

|

Ps.

(1)

|

U.S.$

|

|||||||||||||

|

December 31, 2012

(2)

|

— | — | — | — | ||||||||||||

|

December 31, 2011

(2)

|

— | — | — | — | ||||||||||||

|

December 31, 2010

(2) (5)

|

1.49899 | 0.36994 | 4.49697 | 1.10981 | ||||||||||||

|

December 31, 2009

(2) (4)

|

0.89492 | 0.23054 | 2.68476 | 0.69163 | ||||||||||||

|

December 31, 2008

(2) (3)

|

0.21215 | 0.05747 | 0.63645 | 0.17240 | ||||||||||||

| ____________________ | ||||||||||||||||

|

|

(1)

|

Historical values.

|

|

|

(2)

|

On April 2002, the Central Bank suspended the payment of dividends by Argentine financial institutions. Since June 2, 2004 the Central Bank makes some exceptions to the suspension of profits distributions and may pre-authorize dividend payments under certain conditions. See

“Item 8. Financial Information—Dividends”

.

|

|

|

(3)

|

Based upon the reference exchange rate quoted by Central Bank at March 26, 2009.

|

|

|

(4)

|

Based upon the reference exchange rate quoted by Central Bank at April 29, 2010.

|

|

|

(5)

|

Based upon the reference exchange rate quoted by Central Bank at March 31, 2011.

|

|

|

(6)

|

For the fiscal years ended December 31, 2012 and 2011, the Bank decided not to declare and distribute dividends as result of the issuance of Communications “A” 5272 and 5273 of the Central Bank (see

“Item 8. Financial Information—Dividends”)

. For the fiscal years ended December 31, 2010 and 2009 the dividends were paid totally in cash. For the fiscal year ended December 31, 2008 the dividends paid in 2009 were Ps.35 million in cash and Ps.65 million through the issue of new shares. For the fiscal years ended December 31, 2010 and 2009 the number of outstanding shares were 536,361,306, respectively, and for the fiscal year ended December 31, 2008 the number of outstanding shares were 471,361,306. Declared dividends per ordinary share are calculated taking into account dividends paid over the outstanding shares at the end of each fiscal year.

|

Exchange Rates

The following table shows the annual high, low, average and year-end free exchange rate for U.S.$1.00 for the periods indicated. The Federal Reserve Bank of New York does not report a noon buying rate for pesos.

|

High

(1)

|

Low

(1)

|

Average

(2)

|

||||||||||

|

Year /Period

|

(in pesos per U.S.$1.00)

|

|||||||||||

|

March 2013

|

5.1223 | 5.0475 | 5.0840 | |||||||||

|

February 2013

|

5.0448 | 4.9825 | 5.0111 | |||||||||

|

January 2013

|

4.9768 | 4.9228 | 4.9486 | |||||||||

|

2012

|

4.9173 | 3.9715 | 4.5502 | |||||||||

|

December 2012

|

4.9173 | 4.8398 | 4.8800 | |||||||||

|

November 2012

|

4.8338 | 4.7700 | 4.7974 | |||||||||

|

October 2012

|

4.7655 | 4.6992 | 4.7299 | |||||||||

|

2011

|

4.3035 | 3.9715 | 4.1302 | |||||||||

|

2010

|

3.9857 | 3.7942 | 3.9127 | |||||||||

|

2009

|

3.8545 | 3.4497 | 3.7301 | |||||||||

|

2008

|

3.4537 | 3.0128 | 3.1614 | |||||||||

| ________________________ | ||||||||||||

|

|

(1)

|

Source: BCRA.

|

|

|

(2)

|

The average of monthly average rates during the period.

|

The exchange rate on April 5, 2013 was Ps.5.1370 = U.S.$1.00.

Fluctuations in the exchange rate between pesos and dollars affect the dollar equivalent of the peso price of the ordinary shares on the Buenos Aires Stock Exchange (Bolsa de Comercio de Buenos Aires — the “BCBA”) and as a result, would most likely affect the market price of the ADSs. Fluctuations in exchange rates also affect dividend income measured in dollars. The Bank of New York Mellon, as depositary for the ADSs is required, subject to the terms of the deposit agreement, to convert pesos to dollars at the prevailing exchange rate at the time of making any dividend payments or other distributions. The following table shows the rate of devaluation of the peso vis-à-vis the dollar, the rate of exchange (number of pesos per dollar prevailing in the Argentine foreign exchange market) and the rate of inflation for wholesale prices for fiscal year ended December 31, 2012 and for the four most recent

fiscal years. Since the repeal of the Convertibility Law in January 2002, the peso has devalued approximately 413.70% vis-à-vis the dollar.

|

December 31,

|

||||||||||||||||||||

|

2012

|

2011

|

2010

|

2009

|

2008

|

||||||||||||||||

|

Devaluation Rate

|

14.27% | 8.23% | 4.72% | 9.93% | 9.61% | |||||||||||||||

|

Exchange Rate

|

4.9173 | 4.3032 | 3.9758 | 3.7967 | 3.4537 | |||||||||||||||

|

Inflation Rate

(1)

|

13.13% | 12.67% | 14.56% | 10.26% | 8.98% | |||||||||||||||

| _____________________ | ||||||||||||||||||||

|

|

(1)

|

The inflation rate presented is the general WPI published by the INDEC.

|

|

B.

|

Capitalization and indebtedness

|

Not applicable.

|

C.

|

Reasons for the offer and use of proceeds

|

Not applicable.

|

D.

|

Risk Factors

|

Factors Related to Argentina

Overview

We are an Argentine corporation (sociedad anónima) and substantially all of our operations, properties and customers are located in Argentina. Accordingly, the quality of our assets, our financial condition and our results of operations depend primarily on macroeconomic and political conditions prevailing in Argentina. In 2001, the Argentine economy suffered a severe economic and political crisis (“the Argentine Crisis”), but was able to recover during Nestor Kirchner’s term as President, which ended in 2007. Kirchner was succeeded by Cristina Fernández de Kirchner, who was reelected for another four year term on October 23, 2011. The global financial crisis since 2008 (the “Global Financial Crisis”) led to lower growth and a moderate rise in unemployment, but did not affect the stability of Argentina’s financial system (see

Item 4. Information on the Company—Recent Political and Economic Developments in Argentina – Macroeconomic Environment

).

Although the economic policies implemented by the Kirchner administrations have succeeded in the short- and mid-term, there still remain issues to be resolved, such as:

|

|

§

|

contracts with privatized public utilities, and the elimination of subsidies to the energy and gas companies that could affect consumption levels;

|

|

|

§

|

increasing inflation affecting competiveness and economic growth;

|

|

|

§

|

availability of long-term fixed interest rate loans;

|

|

|

§

|

high commodity prices have had a favourable impact on economic activities in recent years, but are very volatile and out of the Government’s scope of control;

|

|

|

§

|

recent measures implemented by the Government to control imports led to the imposition of barriers to Argentine exports to trading parties and had a negative impact on economic activities during 2012;

|

|

|

§

|

the Government has issued several measures that have limited the access to the purchase of foreign currency, which has caused certain uncertainty especially to dollar-denominated deposit holders; and

|

|

|

§

|

a significant intervention by the Government in the private sector, including through the expropriation of YPF, the country’s largest oil and gas company.

|

High inflation rate expectations could negatively affect the Argentine economy in general, including access to the long-term financing market.

In the event of an acceleration of inflation rates, Argentine exports could lose competitiveness in international markets and private consumption could decline, causing a negative effect on economic activity and employment. Moreover, a high inflation rate could undermine confidence in the Argentine financial system in general, and this would negatively affect the business volume of banks, including BBVA Francés, and could potentially hinder the interest margin of long-term and fixed interest rates loans, although currently these loans are not a significant part of the Bank assets.

There exists a discrepancy between statistical data published by National Institute for Statistics and Census (“INDEC”) referring to the CPI (consumer price index) for the Greater Buenos Aires area (the “CPI-GBA”), CPI indexes corresponding to the different Argentine regions/provinces and private estimates. This generates uncertainty about the country’s actual inflation rate and does not contribute to anchor inflation expectations. It is to be noted that assets indexed by Coeficiente de Estabilización de Referencia (“CER”) are adjusted according to the CPI-GBA.

Impositions of sanctions on Argentina by international organizations such as the declaration of censure recently issued by the International Monetary Fund (IMF) against Argentina due to the inaccuracy of certain official data reported, could negatively affect Argentina’s access to international financial markets.

Following several warnings about the quality of the official data reported by Argentina to the IMF regarding the CPI-GBA, the gross domestic product (the “GDP”) and the non-implementation of remedial measures to produce accurate inflation and growth related statistics, the IMF issued on February 1, 2013 a declaration of censure against Argentina “in connection with its breach of obligations to the IMF under the Articles of Agreement”. This is the first sanction imposed by the IMF to Argentina, but this is not an economic fine. Argentina must adopt remedial measures to address the inaccuracy of the mentioned indices without further delay, and no later than September 29, 2013. After that, the Managing Director is required to report to the Executive Board by November 13, 2013 on the status of Argentina’s implementation of the above mentioned remedial measures. If the Managing Director considers that Argentina failed to implement any of the actions called for in the declaration of censure within the specified timeframe, the Managing Director may issue a complaint to the Executive Board and recommend that the Executive Board declare the member ineligible to use the general resources of the IMF. The Executive Board will again review this issue and will decide on this ineligibility, and it may inform that the member’s persistence in its failure to fulfill its obligations following the declaration of ineligibility may result in the issuance of a complaint for the suspension of the member’s voting and related rights.

The imposition of further sanctions could eventually result, in the long term, in Argentina’s exclusion from the IMF. Were Argentina excluded as a member of the IMF, Argentine companies such as BBVA Francés, could suffer adverse consequences, either by jeopardizing their access to international financial markets or by having to pay increasing interest rates in order to obtain financing. Furthermore, it could also negatively affect foreign investments in Argentina. These adverse effects, however, could be mitigated by the fact that Argentina has not requested to the IMF any kind of financings since 2005.

A considerable decrease in the public sector balance could negatively affect the Argentine economy, and access to international financial markets.

Commencing in 2005, public expenditure began to increase more than public revenues. Thus, the primary fiscal surplus of the central public non-financial sector fell from 3.9% of GDP in 2004 to 0.3% of GDP in 2011. During 2012 there was a primary fiscal deficit of Ps.4.37 billion, while the operational fiscal deficit was Ps.55.56 billion representing a 81.2% of increase as compared to the deficit of the prior year. Moreover, the primary fiscal balance could be negatively affected in the future if public expenditure continues to increase at a rate higher than revenues due to subsidies to lower-income sectors, social security benefits, financial assistance to provinces with financial problems, increased spending on public works and subsidies to the energy and transportation sectors.

A further deterioration in fiscal accounts could negatively affect the Government’s ability to access the long-term financial markets and could in turn result in more limited access to such markets by Argentine companies. BBVA Francés could therefore be adversely affected by such limitation.

A recent decision by a U.S. District Judge requiring Argentina to pay 100% of the principal and interest in arrears due to certain holders of bonds issued by Argentina and even subjecting the paying agent to injunction, could, if ratified by the NY Court of Appeals, result in Argentina’s default on its payment obligations, negatively affecting its access to international financial markets.

The plaintiffs in this case are holders of sovereign bonds issued by the Argentine Republic pursuant to a Fiscal Agency Agreement prior to Argentina’s default on its payments obligations (“FAA Bonds”). The plaintiffs bonds are in default, and are the subject of federal court judgements which are unsatisfied.

In 2005 and again in 2012, Argentina made exchange offers to the holders of FAA Bonds, pursuant to which bondholders who tendered their FAA Bonds received new Bonds (“Exchange Bonds”). As the result of the two exchange offers, approximately 91% of the FAA Bonds were tendered, and the Exchange Bonds are currently held by Argentina. The plaintiff’s FAA Bonds were not tendered in the exchange offer.

Argentina has stated that it does not intend to make further payments on the plaintiffs´ unexchanged FAA Bonds. Further, Argentina adopted legislation, referred to as the Lock Law, that prohibited the Argentine state from making any payment on pay the unexchanged FAA Bonds.

The plaintiffs applied to the United States District Court for the Southern District of New York for a determination that Argentina’s conduct in making full payment on the Exchange Bonds while making no payments on the FAA Bonds constituted a breach of the Pari Passu Clause (equal treatment of all bondholders) included in the FAA Bonds. The matter was referred to Judge Thomas Griesa, who has been assigned to hear all matters arising out of Argentina’s 2001 default. In a series of rulings running from December 2011 through October 2012, Judge Griesa held that Argentina breached the Pari Passu Clause by lowering the rank of the FAA Bonds in violation of the said clause, by making payments under the Exchange Bonds, while persisting on its refusal to satisfy its payment obligations currently due under the terms of the plaintiffs’ FAA Bonds.

The Second U.S. Circuit Court of Appeals initially ratified Griesa’s interpretation and asked the Judge to specify a formula for payments to the plaintiff. The formula, which was announced in November 2012, implied paying 100% of the capital and interest in arrears due on the bonds under litigation. Furthermore, it included the agent of payment Bank of New York Mellon (“BoNY”) in the injunction, meaning that funds paid to BoNY for payment to the exchange bondholders are potentially available for payment instead to the plaintiffs. This interpretation constituted the worst possible scenario for Argentina, and the market reacted with an extensive sale-off of Argentine sovereign bonds and a skyrocketing price for Argentine credit default swaps.

After an appeal by Argentina against the decision, the NY Appeals Court placed a stay on Griesa’s decision and is currently reviewing it. It should be noted, however, that “pari passu” provision (or equal treatment of all bondholders) is not subject to review and, thus, holdout bondholders have the right to eventually receive payments from Argentine under their bonds. Only the formula that results in 100% of such payments being required is subject to review.

On February 27, 2013 a hearing was held by the Second U.S. Circuit Court of Appeals where the parties exposed their arguments. After the hearing the Court requested Argentina to state in writing on or before March 29, 2013, the precise terms of any alternate payment formula and schedule to which it is willing to commit.

The legal process will therefore continue during the 2013, but a negative ruling for Argentina cannot be discarded, which could lead to a default in the payment of Argentina’s obligations currently being serviced. The macroeconomic impact of an unfavourable ruling could lead to a further financial isolation of Argentina, and companies, such as BBVA Francés, and a denial from accessing to international markets in order to obtain financing.

A series of restrictions in the foreign exchange markets recently imposed by the Argentine Government could have a material adverse effect on the results and the solvency of the financial system.

The Argentine Government has issued since October 2011 until the present date, a series of measures restricting the access of private sectors to the foreign exchange markets.

Decree Nr. 1722 was issued in October 2011 eliminating a prior exception for oil and mining companies and thus requiring these companies to settle in the foreign exchange market all their export receipts.

Moreover, the National Insurance Bureau, issued in October 2011, Resolution Nr. 36,162 imposing the obligation for insurance companies to have all their investments and liquid assets allocated in Argentina.

In addition, as from January 2012, the National Tax Bureau must be notified in advance and approve all import operations. This restriction contributed to a decrease in imports (with a negative impact on industrial activities using imports and spare parts) which led to a decrease in the volume of trade financing and negatively impacted our business. Limitations on foreign currency purchases resulted in a decrease in the volume of foreign trade commissions in foreign currency sales.

Finally, Communication “A” 5318, dated July 5, 2012, forbid the purchase of foreign currency by local individuals and companies, except for the purchase of foreign currency for tourism purposes.

The new regulations issued during 2012 regarding the access to foreign currencies led to a 46% withdrawal of dollar denominated deposits in of private sector as of December 31, 2012. A more detailed explanation of said measures is included in

“Item 10. Additional Information — Exchange Controls”.

These restrictions resulting in a withdrawal of dollar denominated deposits, led in turn to a contraction in dollar denominated loans related export finance (the lending capacity in foreign currencies are provided by Bank deposits in foreign currencies), which could have a material adverse effect on the Argentine financial system, including BBVA Francés, our result of operations and financial condition.

Government measures designed to exercise greater control over funds entering the country may disrupt our ability to access the international capital markets.

Argentina’s executive branch enacted Decree Nr. 616/05 to regulate funds coming into and flowing out of Argentina in order to maintain stability and support the economic recovery of the country. These measures require that 30% of the funds remitted to Argentina must be deposited in an account with a local financial institution as a U.S. dollar deposit for one year, without accruing interest. Financial sector and non-financial private sector inflows originated from foreign financial borrowings that are invested in non-financial assets and must be fully repaid (principal and interest) within 24 months from the date of the borrowing are not subject to the foregoing deposit requirement. These measures may adversely affect the Argentine entities’, including BBVA Francés, ability to access the international capital markets and to effectively invest the funds raised in any such financing, which could materially adversely affect Argentine entities’ financial condition and results of operations.

Conditions in the global financial markets and economy have yet to normalize and may materially adversely affect the Bank´s business and profitability.

The outlook for the global economy over the near- to medium-term remains challenging as the global financial system has yet to fully stabilize. Results of operations in the past have been, and in the future may continue to be, materially affected by many factors of a global nature, including political, economic and market conditions; the availability and cost of capital; the liquidity of global markets; the level and volatility of equity prices, commodity prices and interest rates; currency values and other market indexes; technological changes and events; the availability and cost of credit; inflation, the stability and solvency of financial institutions and other companies; investor sentiment and confidence in the financial markets; or a combination of these factors.

While there are additional signs of global recovery, it is not yet certain whether the global recovery will continue or reverse. The economic impact of a worsening global financial scenario in Argentina in general, and in the Bank, in particular, will be limited given the isolation of Argentina in the international capital markets and the low level of foreign investment in the country. If there is, however, a significant drop in commodity prices and a contraction in external demand which affects domestic economic growth and private consumption the Bank’s business could be adversely affected.

As a consequence of Financial Action Task Force’s (“FATF”) evaluation report on Anti-Money Laundering and Combating Financing of Terrorism, Argentina has to implement measures in order to comply with FATF´s recommendations. In the event these measures are not correctly addressed, Argentina could find difficulties in obtaining financing and attracting direct foreign investments.

In October 2010, FATF issued a report on Anti-Money Laundering and Combating the Financing of Terrorism in Argentina, stating that since the last evaluation, finalized in June 2004, Argentina has not made adequate progress in addressing a number of deficiencies identified at the time.

Moreover, in February 2011, Argentina, represented by the Minister of Justice, attended the FATF Plenary in Paris, in order to present a preliminary action plan. Notwithstanding that, FATF has granted an extension until June 2011 to work closely with Argentina and will consider its next steps in the context of the enhanced follow-up process.

During the last semester of 2011, Argentina issued a series of new laws regarding financial and economic crimes together with market manipulation, that were considered an important progress in Argentina’s action plan.

Despite Argentina having remediated five out of the six key material deficiencies identified by the report issued by FATF on Anti-Money Laundering and Combating the Financing of Terrorism, it still has a pending action plan for the total fulfilment of all recommendations set forth in such report. Non-compliance with such report could limit the Bank’s access to foreign financial markets.

Factors Related to BBVA Francés

The short term structure of the deposit base of the Argentine financial system, including the Bank, could lead to a reduction in liquidity levels and limit the long-term expansion of financial intermediation.

After the Argentine Crisis, the volume of financial activity regarding deposits and loans was severely reduced.

Between 2003 and 2007, a gradual and increasing recovery of deposits levels took place. But because of the Global Financial crisis, these levels were reduced during 2008 and further improved during the last semester of 2009, 2010, 2011 and 2012.

Such recovery resulted in an improvement of the liquidity of the financial system.

Notwithstanding that, liquidity problems are not totally overcome. Because most of the deposits in the Argentine financial system are demand deposits and time deposits (which have terms of less than 90 days), the financial system could be exposed to other risks, such as: (i) term mismatch for entities that decided to enter into long term loans; (ii) sudden interest rates increases; (iii) and certain limitations to the expansion of long term loans due to deposit volatility.

This could increase the risk of low liquidity levels and increased funding cost in the event of a withdrawal of significant portions of the deposit base of the financial system, including BBVA Francés.

The instability of the regulatory framework, in particular the regulatory framework affecting financial entities, could have a material adverse effect in financial entities activities, such as the Bank.

Since the beginning of Cristina Kirchner’s second term as President, a series of new regulations have been issued, mainly regulating the foreign exchange market and new capital requirements for financial institutions.

In this regard, Communications “A” 5272 and 5273 of the Central Bank, dated February 1, 2012, increased the capital requirements for financial institutions carrying out activities in Argentina. These Communications require certain minimum capital levels in order to support operational risks and the distribution of dividends, and an additional capital buffer equivalent to 75% of the total capital requirements.

The Central Bank has stated that these new requirements are based on the credit risk measure required by Basel II.

It must be stressed that the Bank, taking into consideration the new capital requirements for operational risks, still has an excess of capital as of December 31, 2012 with respect to the minimum capital requirements of the Communications, of Ps. 1,231 million. Not withstanding that, as a consequence of the additional 75% capital buffer requirement, the Bank will not distribute dividends to its shareholders during the present fiscal year. The amount of the shortfall that prohibits us from distributing dividends to ours shareholders, as required by the BCRA, amounts to Ps.1.3 billion. The Bank is legally entitled to pay dividends because there is no regulation that prohibits the payment of dividends. Not withstanding that, the Central Bank has recently imposed new capital requirements and an additional buffer, making impossible for us the payment of dividends in this fiscal year and the previous one. We cannot state what will happen in the future. For more information about dividends see

“Item 10. Additional Information — D. Exchange Controls — Transfer of Corporate Bonds”.

Moreover, a new law was approved by the Congress introducing amendments to the Central Bank ´s charter. The principal issues addressed by this bill are the use of Central Bank’s reserves for the cancellation of public debt together with the implementation of polices by the Central Bank in order to interfere in the fixing of interest rates, and terms of loans to financial institutions.

The Central Bank issued two Communications, “A” 5319 and “A” 5380 dated July 5, 2012 and December 21, 2012 respectively, whereby it is mandatory for banks to grant credit lines for productive purposes. The Government's intention is to increase investments, although it should be noted that an increase in the demand for these loans could in turn lower the demand of other types of loans. BBVA Francés used approximately Ps.1,300 million in 2012 for these type of loans; and for the first semester of 2013 there is a requirement to use approximately Ps.1,373 million.

On November 29, 2012, the Argentine Congress passed the new “Securities Law”, which modifies the public offer regime set forth by Law Nr.17, 811, as amended. One of the most significant amendments introduced by the Securities Law refers to the powers of the CNV. The incorporation of Section 20 raises concern in the market, especially among listed companies, since it entitles the

CNV to (i) appoint supervisors with powers of veto of the resolutions adopted by the board of directors of the companies and (ii) disqualify the board of directors of the companies for a period of 180 days when, as determined by the CNV, the interests of the minority shareholders and/or security holders are infringed.

The absence of a stable regulatory framework could result in significant limits to the financial institutions’ decisions, such as the Bank, regarding asset allocation, that could cause uncertainty with respect to the future financial activities and result of operations.

Argentine corporate disclosure, governance and accounting standards may require the Bank to provide different information than would be required under U.S. standards. This difference could influence foreign investors decisions to invest in Argentine securities and could therefore limit the Bank’s access to international markets.

The securities laws of Argentina that govern publicly listed companies such as the Bank impose disclosure requirements that are more limited than those in the United States. The Argentine securities markets are not as highly regulated and supervised as the U.S. securities markets. There are also important differences between accounting and financial reporting standards applicable to financial institutions in Argentina and to those in the U.S. As a result, financial statements and reported earnings of Argentine financial institutions generally differ from those reported based on U.S. accounting and reporting standards. See

“Item 5. Operating and Financial Review and Prospects—U.S. and Argentine Banking GAAP Reconciliation”

for a description of the principal differences between Argentine banking GAAP and U.S. GAAP and how they affect our financial statements and the reconciliation to U.S. GAAP of net income and total stockholders’ equity for the periods ended and as of the dates therein indicated.

Accordingly, the information available about the Bank will not be the same as the information available about a U.S. company. The difference in the disclosure requirements between Argentine corporate, governance and accounting standards and U.S. GAAP, could influence foreign investors decisions to invest in Argentine securities and could therefore limit the Bank’s access to international financial markets.

Lawsuits brought against us outside Argentina, the enforcement of foreign judgments and complaints based on foreign legal concepts may be unsuccessful.

We are a commercial bank organized under the laws of Argentina. Most of our shareholders, directors, members of the supervisory committee, and officers and certain experts named herein reside outside the United States (principally in Argentina). Substantially all of our assets are located outside the United States. If any shareholder were to bring a lawsuit against our directors, officers or experts in the United States, it may be difficult for them to effect service of legal process within the United States upon these persons or to enforce a judgment against them in the United States courts based upon the civil liability provisions of the United States federal securities laws, due to specific requirements of Argentine law regarding procedural law issues and principles of public policy.

Because we are a financial institution, any insolvency proceeding against us would be subject to the powers of and intervention by the Central Bank, which may limit remedies otherwise available and extend the duration of the proceedings.

Under Argentine law, the liquidation and commencement of bankruptcy proceedings against financial institutions, until their banking license has been revoked by the Central Bank, may only be commenced by the Central Bank. If BBVA Francés were unable to pay its debts as they come due, the Central Bank would intervene and revoke its banking license, and file a bankruptcy petition before a commercial court. If the Central Bank intervenes, the reorganization proceeding could take longer and it is likely that the shareholders’ remedies would be restricted. During any such process, the Central Bank would have to consider its interests as a regulator and could well prioritize the claims of other creditors and third parties against the Bank. As a result of any such intervention, the shareholders may realize substantially less on the claims than they would in a bankruptcy proceeding in Argentina, the United States or any other country.

The special rules that govern the priority of different stakeholders of financial institutions in Argentina, which give priority to depositors with respect to most other creditors, may negatively affect other stakeholders in case of judicial liquidation or bankruptcy of the Bank.

Argentine Law Nr. 24,485, in force since April 18, 1995 and as amended by Law Nr. 25,089, provides that in case of judicial liquidation or bankruptcy of the Bank, all depositors, irrespective of the type, amount or currency of their deposits, will have general and absolute preferential rights with respect to all other creditors, except for certain labor credits and credits secured with pledge or mortgage, to be paid with 100% of the funds deriving from the liquidation of the Bank’s assets. In addition, depositors of any kind of deposits have special preferential rights over the remaining creditors of the Bank, except for certain labor credits, to be paid with (i) any of the Bank’s funds which may be held by the Central Bank as total reserves, (ii) any remaining funds of the Bank in existence as

of the date on which the Bank’s license is revoked, or (iii) any funds derived from the compulsory transfer of certain assets of the Bank according to instructions of the Central Bank, in the following order of priority: (a) deposits made by legal entities up to Ps.5,000 per entity, or its equivalent in foreign currency, (b) deposits for terms exceeding 90 days and (c) all other deposits on a pro rata basis.

Volatility of credit ratings in Argentina could affect the volatility of the Bank’s credit ratings, and therefore limit the Bank’s access to international financial markets.

The Bank’s credit ratings are based on those of Argentina's sovereign rating, which has fluctuated considerably since the Argentine Crisis. As a result, the Bank’s ratings have also fluctuated in this period, although they have tended to be higher than the sovereign rating. These fluctuations impact our costs of funding and collateral obligations and our ability to access international markets. Continued volatility of, or a decrease in, Argentina’s sovereign rating could affect our business.

Factors Related to BBVA Francés’ Subsidiaries

|

§

|

Consolidar AFJP S.A.

|

As a consequence of the social security reform, the loss of its corporate purpose and its liquidation, labor lawsuits were filed against Consolidar AFJP claiming additional payment amounts. Adverse rulings for Consolidar AFJP´ in such lawsuits could result in severance payment obligations for considerable amounts, which could have a material adverse effect on the financial condition of the company.

Consolidar AFJP S.A. (“Consolidar AFJP” or “AFJP”) was a privately owned pension fund managing company whose purpose was the administration of retirement contributions from affiliates and the corresponding grant of old age, disability and death pensions. On December 4, 2008, the Federal Government enacted Law Nr. 26,425 to implement social security reform, by which the National State assumed once again the coverage of contingencies in cases of old age, disability and death. Certain matters deriving from Law Nr. 26,425 that remain pending, such as possible indemnity in favor of AFJP in the amount of its corporate capital arising from the loss of its corporate business purpose. Notwithstanding this, on December 7, 2010, Consolidar AFJP filed a claim against the Federal Government and the Ministry of Labor and Social Security, requesting compensation for the losses suffered by the company and its shareholders, as a result of the aforementioned social security reform.

Moreover, as a consequence of the social security reform and the loss of corporate business purpose, on December 28, 2009, in a Shareholders’ Extraordinary Meeting of AFJP, the shareholders decided to terminate the corporate existence of the company and liquidate it. Until the present date, the liquidation process is still pending.

During 2012, 22 legal labor actions were filed against AFJP claiming differences in severance payment amounts. AFJP has estimated this contingency and raised the corresponding allowances. Adverse rulings against Consolidar AFJP could result in severance payments by the company of considerable amounts, which could have a material adverse effect on the financial condition of the company, and therefore in the result of liquidation process for BBVA Francés as its shareholder which owns a 53.89% interest in the company.

RECENT POLITICAL AND ECONOMIC DEVELOPMENTS IN ARGENTINA

Macroeconomic Environment

Impaired by factors such as the draught, a lower growth in Brazil and the impact of increasing restrictions in the foreign exchange market, the Argentine economy underwent a strong deceleration in 2012, following the dynamic trends which had prevailed in 2011. After an 8.9% increase in 2011, the GDP grew only 1.9% in 2012. Such a low increase was mainly due to a poor performance in real terms of investment, which fell by 4.2% in 2012 with respect to 2011, as well as to a decrease in exports (-4.5%). Private consumption, instead, provided some support to the GDP with a 3.6% increase in 2012, favored by public consumption that showed a 6% increase in real terms. The braking effect on the GDP was somewhat softened by the decrease of imports, which fell by 2% in 2012.

This poor economic performance reflected itself on the labor market, negatively affecting the generation of employment. Thus, in 2012 the employment rate, and the total number of employees over total population, fell slightly to around 42.9% of the total population against the 43% of 2011, but the decrease in the labor supply (as the labor force participation rate fell to 46.2% of the total

population in 2012) prevented a rise in the unemployment rate, which remained at 7.2% for 2012 as compared to the 7.2% average rate for 2011. This less dynamic tendency in the labor market did not reflect itself on the behavior of salaries, which at December 2012 accumulated an increase of 24.8% over those at December 2011 for registered private workers and of 24.5% in the general index, which is an average of the total wages of the economy, including both private and public sector, as well informal workers. The salaries of public servant showed an accumulated rise of 17% for the year, whereas the accumulated increase for workers of the “informal” sector is estimated at 29%.

In spite of a less dynamic economic activity, inflation measured as per the CPI-GBA reached 10.8% in terms of year-over-year variation as at December 31, 2012, showing an acceleration as compared to the 9.5% rate of the previous year. Such increase was mainly due to the Food and Beverages chapter which increased from a 7.6% hike in December 2011 to 9.9% in December 2012. The Housing chapter also had a 10.5% increase (against 6.4% the previous year) after price adjustments in the power and gas rates, whereas the prices of Transport were accelerated by increases in bus, railway and subway fares due to the cancellation of public subsidies.

The fiscal policy remained expansive, and in 2012 there was a primary fiscal deficit of Ps.4,374 million, compared to a surplus of Ps.4,921 million in 2011 as a result of a 29% increase of primary public spending in the period, above the 26.6% increase in total income. Among the expenditures, the increases in remunerations (29%), social security benefits (39%) and other current expenditures (56%) stood out, whereas the items with increases under the average included transfers to the private sector (15%), capital spending (15.5%) and transfers to the provinces (3%). The income side was supported by the social security contributions which increased by 30.5% year over year in 2012 and the non-tax and capital income, including Central Bank transfers and income of the Argentine Social Security Administration (“ANSES”) which grew by 25% in the year. Total income tax increased by 25.9%, mainly due to an increase in the income tax collection (27.5%). VAT collection had a 23.5% increase and the foreign trade taxes grew a bare 13.3%, affected by the fall in exports and imports. If the payment of interest is taken into account, the Federal Government had an operating deficit of Ps.55,564 million in 2012, 81.2% higher than the Ps.30,663 million recorded the previous year.

The foreign exchange market and the foreign sector were affected by profound regulatory changes, by means of which the Government sought to ensure a level of foreign reserves large enough to face the payment of debt denominated in foreign currency and avoid a further depreciation of the peso. Restrictions to the movements in current accounts started with a requirement of prior authorization by the Commerce Secretariat/Federal Tax Authority (Administración General de Ingresos Públicos or “AFIP”) for imports, and a limitation of access to the purchase of foreign exchange by companies for the purpose of transferring profits and dividends abroad. In the case of banks, an “additional capital reserve buffer” was established, increasing the requirement in force from 30% to 75%.

Later on, limits were also imposed on tourist spending by establishing a system of prior information to the AFIP for the purchase of foreign currency when traveling abroad, plus increasingly stringent administrative hindrances and, finally, by applying a 15% surcharge (deductible from Income Tax) on all credit card purchases made abroad.

As a consequence, the foreign trade balance had a U.S.$12,690 billion surplus in 2012, around 26.7% higher than the previous year, but with a fall in trade volumes. The country’s exports, affected by the draught which reduced grain crops, amounted to U.S.$81,205 billion, which implies a decrease of 3.3%, since the 5% fall in volumes sold to the rest of the world was scarcely compensated by a 0.7% hike in prices. Imports, in the meantime, amounted to U.S.$68,205 billion and decreased 7.3% in the year, owing to a 6.7% reduction in the volumes imported and a variation of only 0.3% in prices.

In addition, throughout 2012, the control measures on capital movements, which had started at the end of October 2011 with the requirement of prior AFIP authorization for the purchase of foreign currency by residents, were intensified. The restrictions became more and more stringent up to a point in July when the purchase of foreign currency for hoarding purposes was totally prohibited. These measures succeeded in restricting the outflow of private capitals (Formation of Net External Assets) which amounted to U.S.$3,570 billion in the first nine months of the year as compared to U.S.$18,245 billion in the same period of 2011.

With private demand strongly limited by the new regulations, the Central Bank became the main actor in the foreign exchange market. It continued to apply its managed flotation policy in order to moderate exchange rate volatility, even if permitting an acceleration of the monthly rate of devaluation of the peso during the second half of the year. Over the last six months of 2012 the monthly devaluation reached an average rate of 1.4% as compared to 0.8% in the first half of the year and 0.6% in 2011. Thus the exchange rate increased to 4.92 pesos per U.S. dollar at the end of 2012 (a 14% increase for the year) reaching an average of 4.88 per U.S. dollar in December 2012 (a 14% increase from the average for December 2011).

Monetary Policy

The monetary policy remained expansionary in 2012, with a growth of Ps.84,430 billion in the monetary base over the year, which implies a 38% increase (as compared to 35% in 2011). This resulted from a high rate of monetization of the foreign currency originated in the foreign trade surplus (the Central Bank purchased U.S.$9,200 billion in the foreign exchange market during the year, totaling Ps.41,086 billion), and from the monetary expansion required for financing the public sector, which amounted to Ps.47,495 in the year. The international reserves as at December 31, 2012 amounted to U.S.$43,290 billion, with a net loss of U.S.$3,086 billion as compared to the balance at the end of 2011. This result was mainly due to the fact that the above-mentioned interventions of the BCRA on the foreign exchange market were more than compensated by the creation of the ‘Non-indebtedness’ Fund applied in order to cover the national public debt commitments in foreign currency.

During the first quarter of the year the Central Bank charter was changed to broaden its functions and ensure monetary and financial stability. The Central Bank must now promote employment and economic development with social equality. Following the implementation of this amendment, the board of directors of the BCRA will determine the level of reserves required for compliance with the foreign exchange policy, thus eliminating the requirement that such reserves must cover 100% of the monetary base and so expanding their availability to face payment commitments of the public debt in foreign currency. Moreover, an automatic mechanism was stipulated for the granting automatic advances of funds to the National Treasury and the limit for these loans was raised from 10% to 20% of all fiscal income. As regards specifically to the financial sector, changes were made to the scheme of integration of liquidity requirements, in the sense that such integration may only be constituted by sight deposits with the Central Bank. As compensation for such measure, a reduction was granted in the required cash reserve in pesos according to the proportion of credit to small and medium-sized companies with respect to the total loans granted to the private sector by each financial institution, applicable since December.

Meanwhile, the total “M2” monetary aggregate grew by 38% in the year-over-year variation, as compared to a 30% increase in December 2011 and with a 31% increase in the private “M2”, which excludes public sector deposits. In addition, the Badlar interest rate for private banks, which had increased to an average of 19% in December 2011 when the first foreign exchange restrictions were implemented, progressively decreased in the first half of 2012 to an average of 11.7% in May, and since then it reverted its tendency to achieve a level of 15% in the last quarter of the year, to close 2012 at a 15.4% rate.

The private sector’s deposits in pesos grew by 41% in 2012, whereas those denominated in dollars experienced a 35% decrease. As for the total deposits of the public sector, they had an expansion of 27% in the same period.

Consistent with a lower economic activity, the total of loans to the private sector in pesos increased by 41%, showing a deceleration with respect to the growth recorded in 2011 (48%). The loans in foreign currency showed the opposite behavior, with a fall of 42% as compared to an increase of 27% last year. This was a consequence of the restrictions imposed on the foreign exchange market, which caused an outflow of deposits in dollars and therefore a fall in foreign exchange loans, partially compensated by an increase of the lines in pesos.

In July 2012, making use of its powers to “orientate the credit” as detailed in the new charter, the Central Bank established the “line of credits for productive investment”, according to which the system’s largest financial entities and those which are financial agents of the State must devote a minimum of 5% of their deposits in pesos from the private sector as at that date to finance the purchase of capital goods or the construction of production installations. The line contemplates a maximum interest rate of 15% and a term of not less than 36 months for repayment, and on top of that stipulates that half of the total amount must be granted to Micro, Small and Medium-size Companies (“MiPyMES”). For 2013 the line was expanded by another 5% of the private sector’s deposits in pesos as of November 2012. Given this situation, corporate loans in pesos increased by 47% in the year-over-year variation for 2012, whereas the growth in consumer loans did not exceed 34%.

A.

HISTORY AND DEVELOPMENT OF THE COMPANY

BBVA Francés, an Argentine corporation (a “sociedad anónima” or “S.A.”), was duly incorporated under the name Banco Francés del Río de la Plata S.A. on October 14, 1886. We have our registered office in Argentina, Reconquista 199, C1003ABB, Buenos Aires, telephone number 54-11-4346-4000. Our agent in the United States for U.S. federal securities law purposes is CT Corporation System, currently with offices at 111 Eighth Avenue, New York, New York 10011.

Our original by-laws (“Estatutos”) were approved on November 20, 1886, by a decree recorded in the Public Registry of Commerce of Buenos Aires City on December 6, 1886, under Number 1065 on Folio 359, Book 5, Volume “A” of National By-laws. Our by-laws, including all amendments introduced to this date, were recorded in the Public Registry of Commerce (the Governmental regulatory agency of corporations). The last amendment was recorded on August 2, 2010, under N° 13.784 Book 50 of Corporations

(“sociedades anónimas”). Pursuant to current corporate by-laws, the Bank will terminate its activities on December 31, 2080, unless this term is extended by the shareholders. On March 5, 1998 the Public Registry of Commerce registered the change from Banco Francés del Río de la Plata S.A. to Banco Francés S.A. At the ordinary and extraordinary shareholders’ meeting held on April 27, 2000, a resolution was passed to change our name to BBVA Banco Francés S.A. On October 4, 2000, the Public Registry of Commerce registered the change from Banco Francés S.A. to BBVA Banco Francés S.A., and the amendment to our by-laws reflected the name change.

We are supervised by the Central Bank of Argentina, an entity that establishes valuation and accounting criteria, the rules on liquidity and capital requirements as well as the informative systems of Argentine financial institutions. We are also subject to inspections by the Central Bank, based on which we are assigned a “rating”. See

“Item 4. Information on the Company—The Argentine Banking System and its Regulatory Framework”

.

On August 11, 1997, we acquired 71.75% of the capital stock of Banco de Crédito Argentino S.A. (“Banco de Crédito”). We completed this merger of the two banks by final registration with the Public Registry of Commerce on March 5, 1998. To effect the merger, BBVA Francés issued 14,174,432 ordinary shares to the existing shareholders of Banco de Crédito through a capital increase.

As a result of the acquisition of Banco de Crédito, we gained control of Consolidar Compañía de Seguros de Retiro S.A., Consolidar Compañía de Seguros de Vida S.A. and Consolidar Administradora de Fondos de Jubilaciones y Pensiones S.A. (together the “Consolidar entities” or the “Consolidar Group”), and also acquired control of Crédito Argentino Sociedad de Bolsa S.A. which was liquidated in 2000.

On November 5, 1999, we and Banco Bilbao Vizcaya (today Banco Bilbao Vizcaya Argentaria S.A. or “BBVA”), executed a share purchase agreement, pursuant to which we acquired 99.99% of the shares of Corp Banca S.A., an Argentine bank, and 99.99% of Atuel Fideicomisos S.A., a trust company. On November 22, 1999, as part of a corporate reorganization, all assets and liabilities of Corp Banca S.A. were transferred to us, with full integration of operations and systems.