Table of Contents

As filed with the Securities and Exchange Commission on April 25, 2014

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 20-F

ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d)

OF THE SECURITIES EXCHANGE ACT OF 1934

For the fiscal year ended December 31, 2013

Commission file number 001-15266

BANCO DE CHILE

(Exact name of Registrant as specified in its charter)

BANK OF CHILE

(Translation of Registrant’s name into English)

REPUBLIC OF CHILE

(Jurisdiction of incorporation or organization)

Banco de Chile

Paseo Ahumada 251

Santiago, Chile

(562) 2637-1111

(Address of principal executive offices)

Pedro Samhan E.

Banco de Chile

Paseo Ahumada 251

Santiago, Chile

Telephone: (562) 653-5150

Facsimile: (562) 653-5156

(Name, telephone, e-mail and/or facsimile number and address of company contact person)

Securities registered or to be registered pursuant to Section 12(b) of the Act:

|

Title of each class |

Name of each exchange on which registered |

|

| American Depositary Shares, each representing 600 shares of common stock, without nominal (par) value (“ADSs”) | New York Stock Exchange | |

| Shares of common stock, without nominal (par) value |

New York Stock Exchange (for listing purposes only) |

|

Securities registered or to be registered pursuant to Section 12(g) of the Act:

None

(Title of Class)

Securities for which there is a reporting obligation pursuant to Section 15(d) of the Act:

None

(Title of Class)

Indicate the number of outstanding shares of each of the issuer’s classes of capital or common stock as of the close of the period covered by the annual report:

Shares of common stock : 93,175,043,991

Indicate by check mark if the registrant is a well-known seasoned issuer , as defined in Rule 405 of the Securities Act. Yes x No ¨

If this report is an annual or transition report, indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or 15(d) of the Securities Exchange Act of 1934. Yes ¨ No x

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes x No ¨

Indicate by check mark whether the registrant has submitted electronically and posted on its corporate Web site, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files). Yes ¨ No ¨

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, or a non-accelerated filer. See definition of “accelerated filer and large accelerated filer” in Rule 12b-2 of the Exchange Act. (Check one):

Large accelerated filer x Accelerated filer ¨ Non-accelerated filer ¨

Indicate by check mark which basis of accounting the registrant has used to prepare the financial statements included in this filing:

|

U.S. GAAP ¨ |

IFRS x | Other ¨ |

If “Other” has been checked in response to the previous question, indicate by check mark which financial statement item the registrant has elected to follow. ¨ Item 17 ¨ Item 18

If this is an annual report, indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act). Yes ¨ No x

Table of Contents

| 1 | ||||||

|

Item 1 |

1 | |||||

|

Item 2 |

1 | |||||

|

Item 3 |

1 | |||||

|

Item 4 |

14 | |||||

|

Item 5 |

94 | |||||

|

Item 6 |

133 | |||||

|

Item 7 |

149 | |||||

|

Item 8 |

156 | |||||

|

Item 9 |

160 | |||||

|

Item 10 |

163 | |||||

|

Item 11 |

181 | |||||

|

Item 12 |

181 | |||||

|

Item 12A |

181 | |||||

|

Item 12B |

181 | |||||

|

Item 12C |

181 | |||||

|

Item 12D |

181 | |||||

| 183 | ||||||

|

Item 13 |

183 | |||||

|

Item 14 |

Material Modifications to the Rights of Security Holders and Use of Proceeds |

183 | ||||

|

Item 15 |

183 | |||||

|

Item 16A |

184 | |||||

|

Item 16B |

184 | |||||

|

Item 16C |

184 | |||||

|

Item 16D |

185 | |||||

i

Table of Contents

|

Item 16E |

Purchases of Equity Securities by the Issuer and Affiliated Purchasers |

185 | ||||

|

Item 16F |

185 | |||||

|

Item 16G |

185 | |||||

| 188 | ||||||

|

Item 17 |

188 | |||||

|

Item 18 |

188 | |||||

|

Item 19 |

188 | |||||

ii

Table of Contents

FORWARD-LOOKING STATEMENTS

This annual report on Form 20-F contains “forward-looking statements” within the meaning of Section 27A of the Securities Act of 1933, as amended (the “Securities Act”), Section 21E of the Securities Exchange Act of 1934, as amended (the “Exchange Act”), and the safe harbor provisions of the Private Securities Litigation Reform Act of 1995. Although we have based these forward-looking statements on our expectations and projections about future events, it is possible that actual results may differ materially from our expectations. In many cases, we include a discussion of the factors that are most likely to cause forward-looking statements to differ from actual results together with the forward-looking statements themselves. These statements appear throughout this annual report, including, without limitation, under “Item 4. Information on the Company” and “Item 5. Operating and Financial Review and Prospects.” Examples of such forward-looking statements include:

| • |

projections of operating revenues, net income (loss), net income (loss) per share, capital expenditures, dividends, capital structure or other financial items or ratios; |

| • |

statements of our plans, objectives or goals, including those related to anticipated trends, competition and regulation; |

| • |

statements about market risks, including interest rate risk and foreign exchange risk; |

| • |

statements about our future economic performance or that of Chile or other countries in which we operate; and |

| • |

statements of assumptions underlying such statements. |

Words such as “believe,” “anticipate,” “plan,” “aims,” “seeks,” “expect,” “intend,” “target,” “objective,” “estimate,” “project,” “potential,” “predict,” “forecast,” “guideline,” “could,” “may,” “will,” “should” and similar expressions are intended to identify forward-looking statements but are not the exclusive means of identifying such statements. These statements may relate to (i) our asset growth and financing plans, (ii) trends affecting our financial condition or results of operations and (iii) the impact of competition and regulations, but are not limited to such topics. Forward-looking statements are not guarantees of future performance and involve risks and uncertainties, and actual results may differ materially from those described in such forward-looking statements included in this annual report as a result of various factors (including, without limitation, the actions of competitors, future global economic conditions, market conditions, foreign exchange rates and operating and financial risks), many of which are beyond our control. The occurrence of any such factors not currently expected by us could significantly alter the results set forth in these statements.

Factors that could cause actual results to differ materially and adversely include, but are not limited to:

| • |

changes in general economic, business, political or other conditions in Chile, or changes in general economic or business conditions in Latin America, the United States, Europe or Asia; |

| • |

changes in capital markets in general that may affect policies or attitudes towards lending to Chile or Chilean companies; |

| • |

increased costs; |

| • |

increased competition and changes in competition or pricing environments, including the effect of new technological developments; |

| • |

unanticipated increases in financing and other costs or the inability to obtain additional debt or equity financing on attractive terms; |

| • |

natural disasters; |

| • |

the effect of tax laws on our business; and |

| • |

the factors discussed under “—Risk Factors.” |

You should not place undue reliance on forward-looking statements, which speak only as of the date that they were made. This cautionary statement should be considered in connection with any written or oral forward-looking statements that we may issue in the future. We do not undertake any obligation to publicly release any revisions to such forward-looking statements after the filing of this annual report to reflect later events or circumstances or to reflect the occurrence of unanticipated events.

iii

Table of Contents

THE MERGER

On January 1, 2008, Banco de Chile (the “Bank”) merged with Citibank Chile in a transaction in which Banco de Chile was the surviving corporate entity. As used in this annual report, unless the context otherwise requires, references to “Banco de Chile” relating to any date or period prior to January 1, 2008 (the effective date of the merger) are to Banco de Chile as it existed prior to the consummation of the merger, and such references relating to any date or period on or after January 1, 2008 are to Banco de Chile after the consummation of the merger.

PRESENTATION OF FINANCIAL INFORMATION

We prepare our audited consolidated financial statements in Chilean pesos and in accordance with International Financial Reporting Standards in effect from time to time as issued by the International Accounting Standards Board (“IFRS”). Unless otherwise specified, all financial information herein is in IFRS.

Until and including our consolidated financial statements included in our annual report on Form 20-F for the year ended December 31, 2008, we prepared our audited consolidated financial statements in accordance with generally accepted accounting principles in Chile as supplemented by the applicable rules of the Superintendencia de Bancos e Instituciones Financieras de Chile (the “SBIF”) (“Chilean GAAP”), with reconciliations to generally accepted accounting principles in the United States (“U.S. GAAP”). As required by IFRS 1— First Time Adoption of International Financial Reporting Standards , our financial position as of December 31, 2008 and our results of operations for the year ended December 31, 2008 were restated in accordance with IFRS 1 for comparative purposes. Reconciliations and a description of the transition to IFRS, and the effects on our assets, liabilities, equity, net income and cash flows are presented in Note 5 to our audited consolidated financial statements included in our annual report on Form 20-F for the year ended December 31, 2009 filed with the Securities and Exchange Commission (the “SEC”) on June 29, 2010. Unless otherwise indicated, the financial information included in this annual report with respect to 2009, 2010, 2011, 2012 and 2013 has been derived from financial statements that have been prepared in accordance with IFRS. See Note 2(a) to our audited consolidated financial statements as of and for the year ended December 31, 2013 appearing elsewhere in this annual report. IFRS differs in certain significant respects from Chilean GAAP. As a result, our financial information presented under IFRS is not directly comparable to any of our financial information presented under Chilean GAAP. Accordingly, readers should avoid such comparison.

Since adopting IFRS, we are no longer required to reconcile our financial statements to U.S. GAAP.

For comparison purposes and as a result of changes in certain accounting policies, some line items in our consolidated statement of income and balance sheet have been reclassified for the years ended December 31, 2011 and 2012. For more information, see “Item 5. Operating and Financial Review and Prospects—Critical Accounting Policies—New Standards Adopted in 2013”, as well as Notes 2(aj), 3 and 4 to our audited consolidated financial statements as of and for the year ended December 31, 2013 appearing elsewhere in this annual report.

In this annual report, references to “$,” “U.S.$,” “U.S. dollars” and “dollars” are to United States dollars, references to “pesos” or “Ch$” are to Chilean pesos (see Note 2(u) to our audited consolidated financial statements as of and for the year ended December 31, 2013 appearing elsewhere in this annual report), and references to “UF” are to “Unidades de Fomento.” The UF is an inflation indexed Chilean monetary unit of account with a value in Chilean pesos that is linked to and adjusted daily to reflect changes in the Consumer Price Index (“CPI”) of the Instituto Nacional de Estadísticas (the “Chilean National Statistics Institute”). As of December 31, 2013, one UF equaled Ch$23,309.56.

This annual report contains translations of certain Chilean peso amounts into U.S. dollars at specified rates solely for your convenience. These translations should not be construed as representations that the Chilean peso amounts actually represent such U.S. dollar amounts, were converted from U.S. dollars at the rate indicated in our audited consolidated financial statements as of and for the year ended December 31, 2013 or could be converted into U.S. dollars at the rate indicated. Until November 30, 2011, Banco de Chile applied the observed exchange rate reported by the Banco Central de Chile (the “Central Bank”) in order to translate its financial statements from Chilean pesos to U.S. dollars. However, beginning December 1, 2011, Banco de Chile adopted the exchange rate of accounting representation, or spot exchange rate, for such matters. This is also described in “Item 3. Key Information—Selected Financial Data—Exchange Rates.” Thus, unless otherwise indicated, the U.S. dollar amounts have been translated from Chilean pesos based on the exchange rate of accounting representation as of December 31, 2013 as determined by our Treasury and Money Market Operations segment, on a daily basis, based on the average of the daily closing bid and offer rates reported by Bloomberg for the Santiago Stock Exchange. The exchange rate of accounting representation on April 15, 2014 was Ch$549.66 = U.S. $1.00. As of the same date, the observed exchange rate was Ch$549.04 = U.S.$ 1.00.

iv

Table of Contents

The Federal Reserve Bank of New York does not report a noon buying rate for Chilean pesos.

Unless otherwise specified, all references in this annual report to total loans are to loans to customers before deducting allowances for loan losses, and they do not include loans to banks or contingent loans. In addition, all market share data and financial indicators for the Chilean banking system as compared to Banco de Chile’s financial information presented in this annual report are based on information published periodically by the SBIF which is published under Chilean GAAP and prepared on a consolidated basis.

In this annual report, “total past-due loans” are the loan installments that are 90 or more days overdue and the remaining outstanding balance of such loan (principal and interests) overdue. See “Item 4. Information on the Company—Selected Statistical Information—Classification of Loan Portfolio Based on the Borrower’s Payment Performance.”

According to Chilean regulations and for the purposes of this annual report, regulatory capital (“Regulatory Capital”) consists of:

| • |

basic capital, which is composed of our paid-in capital, reserves and retained earnings, excluding capital attributable to subsidiaries and foreign branches (“Basic Capital”); and |

| • |

supplementary capital, which is composed of the following: (i) our subordinated bonds, considered at issue price (reduced by 20% for each year during the period commencing six years prior to maturity), but not exceeding 50% of our Basic Capital; plus (ii) our voluntary allowances for loan losses (up to 1.25% of risk-weighted assets to the extent voluntary allowances exceed those that banks are required to maintain by law or regulation); minus (iii) our goodwill and unconsolidated investments in companies (“Supplementary Capital”). |

Certain figures included in this annual report and in our audited consolidated financial statements as of and for the year ended December 31, 2013 have been rounded for ease of presentation. Percentage figures included in this annual report have not in all cases been calculated on the basis of such rounded figures but on the basis of such amounts prior to rounding. For this reason, percentage amounts in this annual report may vary slightly from those obtained by performing the same calculations using the figures in our audited consolidated financial statements as of and for the year ended December 31, 2013. Certain other amounts that appear in this annual report may similarly not sum due to rounding.

Inflation figures are those reported by the Chilean National Statistics Institute, unless otherwise stated herein or required by the context.

MACRO-ECONOMIC AND MARKET DATA

In this annual report, all macro-economic data relating to the Chilean economy is based on information published by the Central Bank. All market share data, financial indicators and other data relating to the Chilean financial system are based on information published periodically by the SBIF, which is published under Chilean GAAP and prepared on a consolidated basis.

v

Table of Contents

| Item 1 | Identity of Directors, Senior Management and Advisors |

Not Applicable.

| Item 2 | Offer Statistics and Expected Timetable |

Not Applicable.

| Item 3 | Key Information |

SELECTED FINANCIAL DATA

The following tables present historical financial information about us as of the dates and for each of the periods indicated. The following tables should be read in conjunction with, and are qualified in their entirety by reference to, our audited consolidated financial statements as of and for the year ended December 31, 2013 appearing elsewhere in this annual report. The financial information for the years ended December 31, 2009, 2010, 2011, 2012 and 2013 is presented under IFRS.

Our audited consolidated financial statements have been prepared in accordance with IFRS for the years ended December 31, 2009, 2010, 2011, 2012 and 2013.

| For the Year Ended December 31, | ||||||||||||||||||||||||

| 2009 | 2010 | 2011 | 2012 | 2013 | 2013 | |||||||||||||||||||

| (in millions of Ch$, except share and per share data) |

(in thousands of

U.S.$) (1) |

|||||||||||||||||||||||

|

IFRS: |

||||||||||||||||||||||||

|

CONSOLIDATED STATEMENT OF INCOME DATA |

||||||||||||||||||||||||

|

Interest revenue |

Ch$ | 900,407 | Ch$ | 1,092,003 | Ch$ | 1,501,684 | Ch$ | 1,672,766 | Ch$ | 1,765,942 | U.S$ | 3,359,092 | ||||||||||||

|

Interest expense |

(222,883 | ) | (324,377 | ) | (624,209 | ) | (708,629 | ) | (704,371 | ) | (1,339,822 | ) | ||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||

|

Net interest income |

677,524 | 767,626 | 877,475 | 964,137 | 1,061,571 | 2,019,270 | ||||||||||||||||||

|

Net fees and commissions income |

246,053 | 277,566 | 290,108 | 287,272 | 287,093 | 546,095 | ||||||||||||||||||

|

Net financial operating income |

(138,179 | ) | 17,163 | 58,101 | 16,199 | 32,672 | 62,147 | |||||||||||||||||

|

Foreign exchange transactions, net |

220,999 | 63,762 | (7,973 | ) | 35,136 | 71,457 | 135,922 | |||||||||||||||||

|

Other operating income |

22,190 | 23,584 | 24,735 | 20,887 | 25,884 | 49,235 | ||||||||||||||||||

|

Provisions for loan losses |

(241,345 | ) | (157,651 | ) | (146,925 | ) | (166,420 | ) | (221,653 | ) | (421,618 | ) | ||||||||||||

|

Total operating expenses |

(485,947 | ) | (529,969 | ) | (595,000 | ) | (612,934 | ) | (619,530 | ) | (1,178,440 | ) | ||||||||||||

|

Income attributable to associates |

840 | 1,609 | 3,054 | (468 | ) | 1,780 | 3,386 | |||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||

|

Income before income taxes |

302,135 | 463,690 | 503,575 | 543,809 | 639,274 | 1,215,997 | ||||||||||||||||||

|

Income taxes |

(40,389 | ) | (46,425 | ) | (65,431 | ) | (63,928 | ) | (89,085 | ) | (169,453 | ) | ||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||

|

Net income from continued operations, net of taxes |

261,746 | 417,265 | 438,144 | 479,881 | 550,189 | 1,046,544 | ||||||||||||||||||

|

Net income from discontinued operations, net of taxes |

||||||||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||

|

Net income for the year |

Ch$ | 261,746 | Ch$ | 417,265 | Ch$ | 438,144 | Ch$ | 479,881 | Ch$ | 550,189 | U.S.$ | 1,046,544 | ||||||||||||

|

Attributable to: |

||||||||||||||||||||||||

|

Equity holders of the parent |

261,744 | 417,264 | 438,143 | 479,880 | 550,188 | 1,046,542 | ||||||||||||||||||

|

Non-controlling interest |

2 | 1 | 1 | 1 | 1 | 2 | ||||||||||||||||||

|

Earnings per share (2) |

3.06 | 4.86 | 4.91 | 5.37 | 5.92 | 0.011 | ||||||||||||||||||

|

Earnings per ADS |

1,837.16 | 2,916.22 | 2,944.35 | 3,222.57 | 3,549.93 | 6.75 | ||||||||||||||||||

|

Dividends per share (3) |

2.72 | 3.50 | 3.38 | 3.41 | 3.90 | 0.007 | ||||||||||||||||||

|

Weighted average number of shares (in millions) |

85,484.08 | 85,850.51 | 89,285.13 | 89,347.56 | 92,991.45 | |||||||||||||||||||

(See footnotes below)

1

Table of Contents

| As of December 31, | ||||||||||||||||||||||||

| 2009 | 2010 | 2011 | 2012 | 2013 | 2013 | |||||||||||||||||||

| (in millions of Ch$, except share and per share data) |

(in thousands of

U.S.$) (1) |

|||||||||||||||||||||||

|

IFRS: |

||||||||||||||||||||||||

|

CONSOLIDATED STATEMENT OF FINANCIAL POSITION DATA |

||||||||||||||||||||||||

|

Cash and due from banks |

Ch$ | 727,553 | Ch$ | 772,329 | Ch$ | 881,146 | Ch$ | 684,925 | Ch$ | 873,308 | U.S.$ | 1,661,166 | ||||||||||||

|

Transactions in the course of collection |

526,051 | 429,756 | 373,639 | 310,077 | 300,026 | 570,695 | ||||||||||||||||||

|

Financial assets held-for-trading |

351,590 | 279,765 | 269,861 | 159,682 | 326,921 | 621,854 | ||||||||||||||||||

|

Cash collateral on securities borrowed and reverse repurchase agreements |

79,401 | 82,787 | 47,981 | 35,100 | 82,422 | 156,779 | ||||||||||||||||||

|

Derivative instruments |

565,986 | 488,354 | 381,055 | 326,083 | 374,687 | 712,712 | ||||||||||||||||||

|

Loans and advances to banks |

448,981 | 349,588 | 648,425 | 1,343,322 | 1,062,056 | 2,020,193 | ||||||||||||||||||

|

Loans to customers, net |

12,879,155 | 14,029,968 | 17,023,756 | 18,383,958 | 20,441,472 | 38,882,812 | ||||||||||||||||||

|

Financial assets available-for-sale |

1,267,774 | 1,157,105 | 1,471,120 | 1,272,316 | 1,681,883 | 3,199,199 | ||||||||||||||||||

|

Investments in other companies |

10,494 | 11,072 | 13,196 | 11,674 | 14,407 | 27,404 | ||||||||||||||||||

|

Intangible assets |

88,182 | 88,463 | 81,026 | 75,610 | 72,223 | 137,379 | ||||||||||||||||||

|

Property and equipment |

205,847 | 204,352 | 207,888 | 205,189 | 197,578 | 375,824 | ||||||||||||||||||

|

Investment properties |

17,840 | 17,459 | 17,079 | 16,698 | 16,317 | 31,037 | ||||||||||||||||||

|

Current tax assets |

— | 3,363 | — | — | — | — | ||||||||||||||||||

|

Deferred tax assets, net |

49,733 | 57,678 | 60,025 | 55,801 | 56,421 | 107,321 | ||||||||||||||||||

|

Other assets |

282,872 | 304,425 | 279,804 | 317,765 | 373,987 | 711,381 | ||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||

|

Total assets |

Ch$ | 17,501,459 | Ch$ | 18,276,464 | Ch$ | 21,756,001 | Ch$ | 23,198,200 | Ch$ | 25,873,708 | U.S.$ | 49,215,756 | ||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||

|

Current accounts and other demand deposits |

3,718,076 | 4,446,181 | 4,895,426 | 5,470,971 | 5,984,332 | 11,383,116 | ||||||||||||||||||

|

Transactions in the course of payment |

325,056 | 208,750 | 155,424 | 72,684 | 51,898 | 98,718 | ||||||||||||||||||

|

Cash collateral on securities lent and repurchase agreements |

308,028 | 81,755 | 223,202 | 226,396 | 256,766 | 488,408 | ||||||||||||||||||

|

Saving accounts and time deposits |

7,427,481 | 7,697,968 | 9,282,324 | 9,612,950 | 10,402,725 | 19,787,577 | ||||||||||||||||||

|

Derivative instruments |

538,240 | 528,445 | 429,913 | 380,322 | 426,110 | 810,527 | ||||||||||||||||||

|

Borrowings from financial institutions |

1,368,226 | 1,281,372 | 1,690,939 | 1,108,681 | 989,465 | 1,882,114 | ||||||||||||||||||

|

Debt issued |

1,587,998 | 1,764,165 | 2,388,341 | 3,273,933 | 4,366,960 | 8,306,627 | ||||||||||||||||||

|

Other financial obligations |

176,150 | 179,160 | 184,785 | 162,123 | 210,926 | 401,214 | ||||||||||||||||||

|

Currents tax liabilities |

39,018 | — | 3,095 | 23,189 | 7,131 | 13,564 | ||||||||||||||||||

|

Deferred tax liabilities, net |

— | — | — | — | — | — | ||||||||||||||||||

|

Provisions |

88,607 | 114,685 | 131,344 | 141,839 | 154,650 | 294,168 | ||||||||||||||||||

|

Employee benefits |

43,202 | 55,433 | 60,634 | 64,545 | 67,944 | 129,240 | ||||||||||||||||||

|

Other liabilities |

280,392 | 224,225 | 269,905 | 305,105 | 275,762 | 524,539 | ||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||

|

Total liabilities |

Ch$ | 15,900,474 | Ch$ | 16,582,139 | Ch$ | 19,715,332 | Ch$ | 20,842,738 | Ch$ | 23,194,669 | U.S.$ | 44,119,812 | ||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||

|

Total equity |

1,600,985 | 1,694,325 | 2,040,669 | 2,355,462 | 2,679,039 | 5,095,944 | ||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||

|

Total liabilities and equity |

Ch$ | 17,501,459 | Ch$ | 18,276,464 | Ch$ | 21,756,001 | Ch$ | 23,198,200 | Ch$ | 25,873,708 | U.S.$ | 49,215,756 | ||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||

(See footnotes below)

2

Table of Contents

| As of December 31, | ||||||||||||||||||||

| 2009 | 2010 | 2011 | 2012 | 2013 | ||||||||||||||||

|

IFRS: |

||||||||||||||||||||

|

CONSOLIDATED RATIOS |

||||||||||||||||||||

|

Profitability and Performance |

||||||||||||||||||||

|

Net interest margin (4) |

4.48 | % | 4.87 | % | 4.80 | % | 4.68 | % | 4.67 | % | ||||||||||

|

Return on average total assets (5) |

1.51 | 2.37 | 2.16 | 2.14 | 2.25 | |||||||||||||||

|

Return on average equity (6) |

16.85 | 24.98 | 22.61 | 21.71 | 20.67 | |||||||||||||||

|

Capital |

||||||||||||||||||||

|

Average equity as a percentage of average total assets |

8.99 | 9.50 | 9.53 | 9.85 | 10.90 | |||||||||||||||

|

Bank regulatory capital as a percentage of minimum regulatory capital |

234.93 | 232.92 | 245.53 | 269.50 | 274.26 | |||||||||||||||

|

Ratio of liabilities to regulatory capital (7) |

11.87 | 12.98 | 12.30 | 11.11 | 10.90 | |||||||||||||||

|

Credit Quality |

||||||||||||||||||||

|

Substandard loans as a percentage of total loans (8) |

5.81 | 5.46 | 2.87 | 3.31 | 3.48 | |||||||||||||||

|

Allowances for loan losses as a percentage of substandard loans (8) |

40.71 | 44.33 | 72.58 | 62.42 | 60.52 | |||||||||||||||

|

Provision for loan losses as a percentage of average loans |

1.89 | 1.16 | 0.92 | 0.92 | 1.12 | |||||||||||||||

|

Allowances for loan losses as a percentage of total loans |

2.37 | 2.42 | 2.09 | 2.07 | 2.10 | |||||||||||||||

|

Operating Ratios |

||||||||||||||||||||

|

Operating expenses/operating revenue |

47.24 | 46.10 | 47.89 | 46.31 | 41.90 | |||||||||||||||

|

Operating expenses/average total assets |

2.81 | % | 3.01 | % | 2.93 | % | 2.73 | % | 2.54 | % | ||||||||||

| (1) | Translations of Chilean peso amounts into U.S. dollars are based on the exchange rate of accounting representation, or the spot exchange rate, which is determined on a daily basis by our Treasury, based on the average of the daily closing bid and offer rates reported by Bloomberg for the Santiago Stock Exchange. Thus, amounts stated in U.S. dollars as of and for the fiscal year ended December 31, 2013 have been translated from Chilean pesos based on the spot exchange rate of Ch$525.72 to U.S.$1.00 as of December 31, 2013. |

| (2) | Earnings per share data have been calculated by dividing net income by the weighted average number of shares outstanding during the year. |

| (3) | Dividends per share data are calculated by dividing the amount of the dividend paid during each year by the previous year’s number of shares outstanding. |

| (4) | Annualized net interest income divided by average interest earning assets. The average balances for interest earning assets, including interest and readjustments, have been calculated on the basis of our daily balances and on the basis of monthly balances for our subsidiaries. Net interest margin does not include the interest earned on trading securities, which is accounted for under Other Income (Loss), Net. |

| (5) | Annualized net income (loss) divided by average total assets. The average balances for total assets have been calculated on the basis of our daily balances and on the basis of monthly balances for our subsidiaries. |

| (6) | Annualized net income (loss) divided by average equity. The average balances for equity have been calculated on the basis of our daily balances. |

| (7) | Total liabilities divided by bank regulatory capital. |

| (8) | See “Item 4. Information on the Company—Selected Statistical Information—Analysis of Substandard Loans and Total Past Due.” |

3

Table of Contents

Exchange Rates

As a general matter, prior to 1989, Chilean law permitted the purchase and sale of foreign currency only in those cases explicitly authorized by the Central Bank. The Ley Orgánica Constitucional del Banco Central de Chile 18,840 (the “Central Bank Act”) liberalized the rules governing the purchase and sale of foreign currency. The Central Bank Act empowers the Central Bank to determine that certain purchases and sales of foreign currency specified by law must be carried out in the Mercado Cambiario Formal (the “Formal Exchange Market”). The Formal Exchange Market is composed of banks and other entities so authorized by the Central Bank. The observed exchange rate for any given day equals the average exchange rate of the transactions conducted in the Formal Exchange Market on the immediately preceding banking day, as certified by the Central Bank. Even though the Central Bank is authorized to carry out its transactions at the rates it sets, it generally uses the spot rate for its transactions. Authorized transactions by other banks are generally carried out at the spot rate.

Purchases and sales of foreign exchange are not required to be conducted in the Formal Exchange Market and therefore may be carried out in the Mercado Cambiario Informal (the “Informal Exchange Market”). There are no price limits imposed on transactions executed in the Informal Exchange Market. On December 30, 2013 (the last trading date of the year), the average exchange rate in the Informal Exchange Market was Ch$526.20 per U.S.$1.00, or 0.5% higher than the observed exchange rate of Ch$523.76 per U.S.$1.00 reported by the Central Bank on the same date.

The following table sets forth the annual low, high, average and period-end observed exchange rate for U.S. dollars for each year beginning in 2009, and the last six complete months, as reported by the Central Bank:

| Daily Observed Exchange Rate Ch$ per U.S.$(1) | ||||||||||||||||

|

Year |

Low (2) | High (2) | Average (3) | Period End (4) | ||||||||||||

| (in Ch$) | ||||||||||||||||

|

2009 |

491.09 | 643.87 | 559.61 | 506.43 | ||||||||||||

|

2010 |

468.37 | 549.17 | 510.25 | 468.37 | ||||||||||||

|

2011 |

455.91 | 533.74 | 483.67 | 521.46 | ||||||||||||

|

2012 |

469.65 | 519.69 | 486.49 | 478.60 | ||||||||||||

|

2013 |

466.50 | 533.95 | 495.35 | 523.76 | ||||||||||||

|

October 2013 |

493.36 | 508.58 | 500.81 | 508.58 | ||||||||||||

|

November 2013 |

507.64 | 528.19 | 519.25 | 528.19 | ||||||||||||

|

December 2013 |

523.76 | 533.95 | 529.45 | 523.76 | ||||||||||||

|

2014 (through April 15) |

524.61 | 573.24 | 551.48 | 549.04 | ||||||||||||

|

January 2014 |

524.61 | 550.53 | 537.03 | 547.22 | ||||||||||||

|

February 2014 |

546.94 | 563.32 | 554.41 | 563.32 | ||||||||||||

|

March 2014 |

550.53 | 573.24 | 563.84 | 550.53 | ||||||||||||

|

April 2014 (through April 15) |

544.96 | 555.97 | 550.65 | 549.04 | ||||||||||||

Source: Central Bank.

| (1) | Figures are expressed in nominal terms. |

| (2) | Exchange rates are the actual low and high, on a day-by-day basis for each period. |

| (3) | For full years, the average of monthly average rates during the year. For full months, the daily average during the month. |

| (4) | As reported by the Central Bank on the first business day of the following period. |

The observed exchange rate on April 15, 2014 was Ch$549.04 = U.S.$1.00. The Federal Reserve Bank of New York does not report a noon buying rate for Chilean pesos.

Until November 30, 2011, Banco de Chile applied the observed exchange rate as reported by the Central Bank in order to translate its financial statements from Chilean pesos to U.S. dollars. However, beginning December 1, 2011, Banco de Chile adopted the exchange rate of accounting representation, or spot exchange rate, for such matters. The exchange rate of accounting representation is determined on a daily basis by our Treasury based on the average of the daily closing bid and offer rates reported by Bloomberg for the Santiago Stock Exchange.

4

Table of Contents

RISK FACTORS

The risks and uncertainties described below are not the only ones that we face. Additional risks and uncertainties that we do not know about or that we currently think are immaterial may also impair our business operations. Any of the following risks, if they actually occur, could materially and adversely affect our business, results of operations, prospects and financial condition.

We are also subject to market risks that are presented both in this subsection and in Note 42 to our audited consolidated financial statements as of and for the year ended December 31, 2013 appearing elsewhere in this annual report.

Risks Relating to our Operations and the Chilean Banking Industry

The growth of our loan portfolio may expose us to increased loan losses.

During the last five years, our total loan portfolio has grown at a compounded average growth rate of 8.8%. The expansion in our loan portfolio has been primarily fostered by the expansion in residential mortgage and consumer loans, and, to a lesser extent, due to the growth posted in commercial loans. The enlargement of our loan portfolio is in line with our strategic priorities, although we recognize our focus on the retail banking segment may expose us to higher levels of loan losses and may require us to establish higher levels of allowances for loan losses. For the year ended December 31, 2013, our loan portfolio amounted to Ch$20,880,770 million, which represents an 11.2% annual increase as compared to the Ch$18,771,761 million that we recorded as of December 31, 2012. Similarly, our allowances for loans losses increased 13.3% from Ch$387,803 million in 2012 to Ch$439,298 million in 2013. As a result, our ratio of allowances for loan losses to total loans slightly increased over that period, from 2.07% in 2012 to 2.10% in 2013.

Our loan portfolio may not continue to grow at the same or similar rate.

We cannot assure you that our loan portfolio will continue to grow at the same rates as it has in the past. The Chilean financial industry’s aggregate loan portfolio has grown significantly over the last five years, which has been fostered by a general effort of its participants to broaden their value offerings and increase banking penetration of lower and middle income segments, as well as small and medium-sized companies. These efforts have been also supported by the robustness and growth of the Chilean economy over the last decade. However, a slowdown or negative GDP growth rates, as well as a change in the behavior of banking customers, could adversely affect the growth rate of our loan portfolio and our credit quality indicators and, accordingly, lead us to increase our requirements of allowances for loan losses. For more information, see “Item 4. Information on the Company—Regulation and Supervision” and “Item 4. Information on the Company—Selected Statistical Information.”

Restrictions imposed by banking regulations may restrict our operations and thereby adversely affect our financial condition and results of operations.

We are subject to regulation by the SBIF. In addition, we are subject to regulation by the Central Bank with respect to certain matters, including interest rates and foreign exchange transactions. See “Item 4. Information on the Company—Regulation and Supervision.”

Pursuant to the Ley General de Bancos (the “General Banking Law”) all Chilean banks may, subject to the approval of the SBIF, engage in certain non-banking businesses approved by the law. The SBIF’s approval will depend on the risk of the activity and the strength of the bank. Further, the General Banking Law applies to the Chilean banking system a modified version of the capital adequacy guidelines issued by the Basel Committee on Banking Regulation and Supervisory Practices (the “Basel Committee”) and limits the discretion of the SBIF to deny new banking licenses.

In addition, in recent years the Chilean government has focused on consumer protection matters. Accordingly, between 2010 and 2013, a number of legal and administrative regulations have been enacted, amended and revoked in order to reinforce consumer protection in all relevant aspects of the financial relationship between consumers and financial institutions. We cannot assure that there will not be new regulations and restrictions on this matter. See “Item 4. Information on the Company—Regulation and Supervision.”

5

Table of Contents

There can be no assurance that regulators will not impose more restrictive limitations in the future on the activities of banks, including us, than those that are currently in effect. Any such change could have a material adverse effect on our results of operations or financial condition in a fashion that we cannot determine in advance.

Regarding Basel III, it is important to note that the SBIF has suggested that these guidelines may be implemented in Chile in the future, which could impose new requirements for all Chilean banks, including us. Similarly, the Chilean Central Bank has announced that it is working on developing new liquidity standards for local banks. Since neither the SBIF nor the Central Bank has provided any indication as to when and how these guidelines will be implemented or even presented to the market, we do not expect they will affect our profitability or results of operations in 2014. Nevertheless, we cannot assure you that these guidelines will not affect our financial performance in the future, if adopted.

As for credit risk provisioning matters, on December 18, 2013 the SBIF published for comments a set of amendments to the regulations on allowances for loan losses and credit risk matters. These amendments propose a standard model for calculating allowances for loan losses associated with residential mortgage loans only, although the SBIF announced that an approach will be proposed for consumer and commercial loans in the future. As for residential mortgage loans, the amendments are intended to introduce a standard model for determining allowances for loan losses that includes past-due behavior and loan-to-value ratios. Similarly, the proposed amendments establish specific guidelines regarding the treatment of collateral when calculating provisions for loan losses and provisioning factoring loans. In addition, on February 13, 2014 the SBIF published for comments a new regulation that aims to establish minimum requirements to be met by any bank in order to use internal models for calculating allowances for loan losses. These requirements have to do with both banks (capital adequacy, management qualification, and satisfactory evaluation by the SBIF) and their credit risk management system (ad hoc organizational structure, quality assurance, etc.). Even though this proposal is at an initial stage of analysis, we cannot assure you that it will not materially affect our results of operations or financial condition in the future, if adopted.

Increased competition and industry consolidation may adversely affect our operations.

The Chilean market for financial services is highly competitive. We compete with other Chilean and foreign banks, with Banco del Estado de Chile, which is government-owned, and with large department stores that grant consumer loans to a large portion of the Chilean population, especially in the low and middle-income segments. In addition, the retail market (which encompasses individuals and small and medium-sized companies) has become the target market of several banks. Accordingly, competition within this market is increasing as banks are continuously incorporating new and tailored products, while they strive to improve service quality. As a result, net interest margins (after provisions for loan losses) in these sub-segments are likely to decline over time.

We also face competition from non-bank competitors in some of our credit products, especially credit cards and consumer loans. In these markets, competition from non-banking companies like large department stores, private compensation funds, and saving and credit cooperatives has become increasingly significant. In addition, we face competition from other types of competitors, such as leasing, factoring and automobile financing companies (especially in credit products), as well as mutual funds, pension funds and insurance companies within the market for savings products and mortgage loans. Currently, banks continue to be the main suppliers of leasing, factoring and mutual funds, and the insurance sales business is experiencing fast growth. However, we cannot assure you that this trend will continue in the future. See “Item 4. Information on the Company—Business Overview—Competition.”

In the past, increasing competition within the Chilean banking industry has been accompanied by a consolidation wave. We expect that both of these trends will continue and result in the creation of larger and stronger financial groups offering a wide range of products and services and targeting most of the segments in the Chilean banking market. These trends may adversely affect us because they may increase the interest rates we pay to attract depositors and decrease the interest rates we charge our customers for loans, resulting in a decrease of the net interest margins we are able to generate.

6

Table of Contents

Our exposure to certain segments of the retail market could lead to higher levels of total past-due loans and subsequent charge-offs.

Although we historically focused on banking for the wholesale market and high-income individuals, an increasing portion of our retail banking segment consists of small and medium-sized companies (approximately 7.7% of our total loan book as of December 31, 2013, including companies with annual sales of up to Ch$1,600 million) and, to a lesser extent, of lower-income individuals (approximately 3.8% of our total loan book as of December 31, 2013, including individuals with monthly incomes ranging from Ch$170,000 to Ch$500,000). Our strategy aims to increase lending and banking penetration by providing multiple value propositions to attract additional retail customers. These customers are likely to be more severely affected by adverse developments in the Chilean economy than large corporations and high-income individuals. Consequently, in the future we may be exposed to higher levels of total past-due loans and subsequent write-offs, which could result in materially higher allowances for loan losses and adversely affect our results of operations.

As of December 31, 2013 our total past-due loans (loans overdue 90 days or more) reached Ch$236,730 million, which represented a 30.2% annual increase as compared to the figure recorded in 2012. Also, as of December 31, 2013 our total past-due loans were composed of 79.1% of retail banking past-due loans (consumer and residential mortgage loans to individuals, as well as commercial loans to small and medium sized companies) and 20.9% of wholesale banking past-due loans (commercial loans to large companies and corporations). During the prior fiscal year, our past-due portfolio encompassed 77.3% of retail banking past-due loans and 22.7% wholesale banking past-due credits.

The annual increase in the amount of past-due loans had mainly to do with greater balances of past-due loans associated with SMEs and, to a lesser extent individual banking. This trend of higher delinquency was in line with an economic cycle that showed some signs of slowdown in 2013, after three years of sustained growth, with annual GPD expansion rates above 5.0%. Even though we have tightened the whole credit process, from assessment to collection, we cannot assure you this trend will not continue if global or local economic conditions deteriorate in the future.

For more information, see “Item 4. Information on the Company—Business Overview—Principal Business Activities.”

One of our affiliates may be obligated to sell shares of our stock in the public market if we do not pay sufficient dividends.

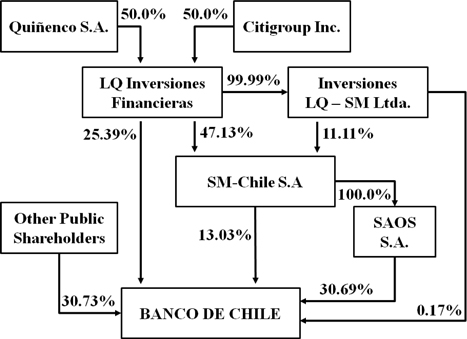

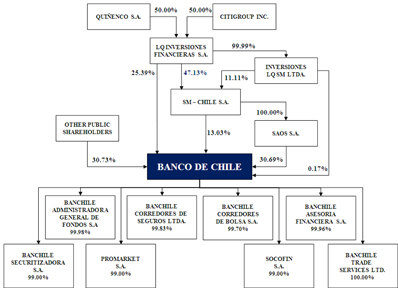

As of December 31, 2013, Sociedad Administradora de la Obligación Subordinada S.A . (“SAOS”), our affiliate, held 30.69% of our shares as a consequence of our 1996 reorganization. This reorganization was due in part to the 1989 repurchase by the Central Bank of certain non-performing loans that we had previously sold to the Central Bank and later exchanged for subordinated debt without a fixed term. For more information, see “Item 4. Information on the Company—History and Development of the Bank—History—The 1982-1983 Economic Crisis and the Central Bank Subordinated Debt.”

In exchange for assuming the Central Bank debt, SAOS received from SM-Chile S.A. (“SM-Chile”), the holding company that controls us and SAOS, a stake of 63.6% of our shares as collateral for this debt. Dividends received from us are the sole source of SAOS’s revenues, which—in turn—must be used to repay this debt. To the extent distributed dividends are not sufficient to pay the amount due on this debt, SAOS is permitted to maintain a cumulative deficit balance with the Central Bank that SAOS commits to pay with future dividends. If this cumulative deficit balance exceeds 20% of our paid-in capital and reserves, the Central Bank may require SAOS to sell a sufficient number of our shares to pay the entire amount of the accumulated deficit. As of March 31, 2014, SAOS maintained a surplus with the Central Bank of Ch$373,556 million, equivalent to a 16.9% of our paid-in capital and reserves as of the same date.

7

Table of Contents

Furthermore, if our shareholders decide to retain and capitalize all or part of our annual net income in order to finance our future growth and to distribute stock dividends, the Central Bank may require us to pay in cash to SAOS the portion of net income corresponding to its stake in our shares. If we distribute stock dividends and the Central Bank does not require us to pay that portion in cash, the shares received by SAOS must be sold by SAOS within the following 12 months. SM-Chile shareholders will have a right of first refusal with respect to that sale.

If SAOS is required to sell shares of our stock for any of the aforementioned circumstances in the public market, that sale could adversely affect the prevailing market price of our stock.

The results of our operations are affected by inflation and interest rate volatility.

The results of our operations depend to a great extent on our net interest income, which represented 71.8% of our total operating revenues in 2013. Changes in inflation and nominal interest rates could affect the interest rates earned on our interest-earning assets differently from the interest rates paid on our interest-bearing liabilities, resulting in a reduction in our net income. Inflation and interest rates are highly sensitive to several factors beyond our control, including the Central Bank’s monetary policy, deregulation of the Chilean financial sector, domestic and international economic and political conditions, among other factors. Any volatility in interest rates could have a material adverse effect on our financial condition and results of operations.

The average annual short-term nominal interest rate in Chile for 90 to 360 day deposits received by Chilean financial institutions was 5.61% in 2011, 5.90% in 2012 and 5.20% in 2013. The average long-term nominal interest rate based on the interest rate of the Central Bank’s five-year bonds was 5.67% in 2011, 5.26% in 2012 and 5.14% in 2013.

Inflation in Chile has been moderate in recent years, especially in comparison with periods of high inflation in the 1980s and 1990s. High levels of inflation in Chile could adversely affect the Chilean economy, the consumers’ purchase power and, indirectly, our results of operations. The annual rate of inflation (as measured by annual changes in the CPI and as reported by the Chilean National Institute of Statistics) during the last five years and the first three months of 2014 was:

|

Year |

Inflation

(CPI Variation) |

|||

|

2008 |

7.1 | % | ||

|

2009 |

(1.4 | ) | ||

|

2010 |

3.0 | |||

|

2011 |

4.4 | |||

|

2012 |

1.5 | |||

|

2013 |

3.0 | |||

|

2014 (through March 31) |

1.5 | % | ||

Source: Chilean National Institute of Statistics

Although we benefit from a higher than expected inflation rate in Chile due to the structure of our assets and liabilities (we have a significant net asset position indexed to the inflation rate), significant changes in inflation with respect to current levels could adversely affect our results of operations and, therefore, the value of both our shares and ADSs.

For more information, see “Item 5. Operating and Financial Review and Prospects—Operating Results—Overview—Inflation” and “Item 5. Operating and Financial Review and Prospects—Operating Results—Overview—Interest Rates.”

Operational problems or errors can have a material adverse impact on our business, financial condition and results of operations.

As all large financial institutions, we are exposed to many operational risks, including the risk of fraud by employees and outsiders, failure to obtain proper internal authorizations, failure to properly document transactions, equipment failures, errors made by employees and natural disasters, such as earthquakes or tsunamis. Although we maintain a system of operational controls composed of world-class human and technological resources, as well as comprehensive contingency plans, there can be no assurance that operational problems or errors will not occur and that their occurrence will not have a material adverse impact on us.

8

Table of Contents

Cybersecurity events could negatively affect our reputation or results of operations and may result in litigation.

We have access to large amounts of confidential financial information and control substantial financial assets belonging to our customers as well as to us. In addition, we provide our customers with continuous remote access to their accounts and the possibility of transferring substantial financial assets by electronic means. Accordingly, cybersecurity is a material risk for us.

We depend on a variety of internet-based data processing, communication, and information exchange platforms and networks. Thus, we cannot assure you that all of our systems are entirely free from vulnerability. Additionally, we enter into contracts with several third-parties to provide the business, data and communication services we offer to our customers. If information security is breached, or if one of our employees breaches compliance procedures, information could be lost or misappropriated, which may affect our results of operations, damage others or result in potential litigation. Cybersecurity incidents, such as computer break-ins, phishing, identity theft and other disruptions could negatively affect the security of information stored in and transmitted through our computer systems and network infrastructure, which may result in significant liability to us in excess of insurance coverage, and may cause existing and potential customers to refrain from doing business with us. Although we, with the help of service providers, intend to continuously implement security technology devices and establish operational procedures to prevent such damage, we cannot assure you that these security measures will be successful.

Exposure to European sovereign debt or related instruments and future turmoil and destabilization related thereto could negatively affect our business.

Although emerging markets were less impacted by the global financial crisis of 2008 and showed a quick recovery, concerns about the possibility of a recession in developed countries cannot be ruled out yet, especially due to the fiscal condition of certain European economies (such as Greece, Italy, Ireland, Portugal and Spain, also called PIIGS economies). Debt levels and fiscal unreliability of these countries have resulted in uncertainty regarding the outlook for the global economy and a potential contagion to other economies linked to these countries. Although developed countries are gradually overcoming the troubles associated with the financial turmoil of 2008 and the subsequent instability of PIIGS countries, we cannot dismiss concerns regarding future volatility.

Likewise, we are unable to determine and predict the effects that this situation could have on the GDP growth of Chile’s main commercial partners and the entire world. Also, these factors could translate into a slowdown in the local economy that could affect the decision making processes of individuals and companies regarding consumption and investment. All of these factors could adversely affect the demand for credits in the Chilean Banking industry. We cannot assure you that these developments will not occur or that they will not affect our results of operations or financial condition.

As of December 31, 2013 we had a total exposure to PIIGS economies of Ch$18,751 million (U.S.$35.7 million), which represents 0.07% of our total assets as of the same date. This exposure was concentrated in only two economies, Italy and Spain, and it was related to contingent credits, such as standby letter of credits in favor of us as well as third parties. As of the same date, we had no additional exposure to PIIGS countries, in any type of instrument, such as financial assets available-for-sale, assets held for trading, derivatives, commercial loans, credit lines, confirming export letters of credits, etc.

9

Table of Contents

Risks Relating to our ADSs

Our principal shareholders may have interests that differ from those of our other shareholders and their significant share ownership may have an adverse effect on the future market price of our ADSs and shares.

As of April 15, 2014, LQ Inversiones Financieras S.A. (“LQIF”), a holding company beneficially owned by Quiñenco S.A. and Citigroup Chile S.A., holds directly and indirectly approximately 51.22% of the voting rights of our shares. These principal shareholders are in a position to elect a majority of the members of our board of directors, direct our management and control all matters decided by a shareholder vote, including the approval of fundamental corporate transactions.

Actions by our principal shareholders with respect to the disposition of the shares or ADSs they beneficially own, or the perception that such actions may occur, may adversely affect the trading price of our shares on the various stock exchanges on which they are listed and, consequently, the market price of the ADSs.

There may be a lack of liquidity and a limited market for our shares and ADSs.

While our ADSs have been listed on the New York Stock Exchange (the “NYSE”) since the first quarter of 2002, there can be no assurance that an active trading market for our ADSs will be sustained. During 2013, a daily average of 16,121 of our American Depositary Receipts (“ADRs”) were traded on the NYSE, according to data provided by Bloomberg. Although our shares are traded on the Santiago Stock Exchange, the Valparaiso Stock Exchange and the Chilean Electronic Stock Exchange, the market for our shares in Chile is small and somewhat illiquid. As of April 15, 2014 approximately 24.80% of our outstanding shares were held by shareholders other than our principal shareholders, including LQIF, SM-Chile, SAOS and Ergas Group.

If an ADS holder withdraws the underlying shares from the ADR facility, the small size of the market, its limited liquidity, as well as our concentrated ownership, may impair the ability of the ADS holder to sell the shares in the Chilean market in the amount and at the price and time such holder desires, and could increase the volatility of the price of our ADSs.

You may be unable to exercise preemptive rights.

The Ley Sobre Sociedades Anónimas No. 18,046 (the “Chilean Corporations Law”) and the Reglamento de Sociedades Anónimas (the “Chilean Corporations Regulations”) require that whenever we issue new common stock for cash, we grant preemptive rights to all of our shareholders (including holders of ADSs) to purchase a sufficient number of shares to maintain their existing ownership percentage. Such an offering would not be possible unless a registration statement under the Securities Act were effective with respect to such rights and common stock or an exemption from the registration requirements thereunder were available.

We may elect not to make a registration statement available with respect to the preemptive rights and the common stock, in which case you may not be able to exercise your preemptive rights. If a registration statement is not filed, the depositary will sell such holders’ preemptive rights and distribute the proceeds thereof if a premium can be recognized over the cost of any such sale.

Developments in international financial markets may adversely affect the market price of the ADSs and shares.

The market price of our ADSs and shares may be adversely affected by volatility in international financial markets and adverse global economic conditions. The market for Chilean securities and the Chilean economy as a whole are, to diverse extents, influenced by economic and market conditions in the United States, Europe and certain emerging market countries, especially Asian countries, and also economic as well as political developments in Latin American countries. Although economic conditions are different in each country, investors’ reactions to specific issues in one country can affect the financial markets in others, including Chile. Therefore, unfavorable developments in other countries—especially in developed economies and Chile’s main commercial partners—may adversely affect the market price of our ADSs and shares.

10

Table of Contents

In particular, since August 2007, there has been significant volatility in worldwide financial markets due to consequences from the announcement, by several U.S. banks and financial institutions, of significant write-downs related to their exposure to mortgage-backed securities and other financial instruments. This situation, also known as the subprime crisis, translated into several and significant government bail-outs for important banks worldwide, bankruptcy for some others and an active M&A market in the financial industry intended to maintain the confidence of investors and customers, as well as avoiding bank runs. Although the Chilean economy was not directly exposed to the U.S. housing credit market and —historically— we have not directly held any assets related to such financial instruments, the subprime crisis impacted the Chilean economy by the end of 2008, including banking activity. Currently, the U.S. economy seems to be overcoming the effects of the subprime crisis, as evidenced by recovering mid-term growth rates, employment and consumption, while the Federal Reserve is tapering the expansionary monetary policy it has used for the past several years. However, we cannot assure you that these past developments will not repeat in the future or that any future developments in international markets could not affect us, including our results of operations and consequently the market price of our ADSs and shares.

Financial deterioration in certain European countries was another indirect effect of the subprime crisis that occurred in the United States. Although our exposure to European sovereign debt is not significant, we cannot assure you that volatility in global financial markets due to the uncertainty regarding the Eurozone fiscal condition will not continue and affect the Chilean economy and consequently our financial condition and results of operations. Accordingly, the price of our ADS could be adversely affected by a new financial turmoil in the Eurozone, political issues, a slower than expected recovery, or a deterioration in healthier economies, such as Germany, that could translate into increasing volatility and uncertainty all over the world.

In the past, Chile has imposed controls on foreign investment and repatriation of investments that affected investments in, and earnings from, our ADSs.

Equity investments held in Chile by non-Chilean residents have historically been subject to various exchange control regulations that restrict the repatriation of investments and earnings therefrom. In April 2001, the Central Bank eliminated most of the regulations affecting foreign investors, although they still have to provide the Central Bank with information related to equity investments and must conduct such operations within the Formal Exchange Market. Additional Chilean restrictions applicable to holders of our ADSs, the disposition of the shares underlying them, the repatriation of the proceeds from such disposition or the payment of dividends may be imposed in the future, and we can neither determine in advance nor advise you as to when or how those restrictions could impact you, if imposed.

If for any reason, including changes in Chilean law, the depositary for our ADSs were unable to convert Chilean pesos to U.S. dollars, investors would receive dividends and other distributions, if any, in Chilean pesos.

We are required to withhold 35% from any dividends we pay to you.

ADS holders are entitled to receive dividends on the underlying shares to the same extent as the holders of shares. Dividends received by ADS holders will be paid net of foreign currency exchange fees and expenses of the depositary and will be subject to Chilean withholding tax of 35% of the dividend, which we will withhold and pay to the Chilean tax authorities. Any dividend distributions made in property (other than common stock) will be subject to the same Chilean tax rules as cash dividends. For more information, see “Item 10. Additional Information—Taxation—Chilean Tax Considerations.”

Risks Relating to Chile

Our growth and profitability depend on the level of economic activity in Chile.

Our core business and transactions are with customers doing business in Chile. Accordingly, our ability to grow our business volumes and results of operations, as well as enhance our financial condition, in general, depends on the dynamism of the Chilean economy and specific macroeconomic variables such as inflation, unemployment, consumption and investment. The global financial crisis of 2008 that dramatically affected the economic growth in developed countries also affected the Chilean economy by the end of 2008 and during the first three quarters of 2009. This translated into a subsequent slowdown in the local banking industry due to

11

Table of Contents

lower levels of consumption and deteriorated credit quality in loan portfolios prompted by increasing unemployment and financial stress experienced by certain economic sectors. Conversely, between 2010 and 2012 the local economy and the banking industry evidenced a significant upturn, fostered by real GDP growth that averaged 5.7% per year, mainly as a result of the recovery in consumption and investment, as well as higher fiscal spending associated with the reconstruction process after a significant earthquake. In 2013, the Chilean economy entered into a moderate slowdown by recording a 4.1% GDP expansion. The lower dynamism was caused by an important slowdown in investment which posted a slight 0.4% annual growth, principally owing to postponed projects in the mining and energy sectors, as well as companies waiting for better economic signals. On the other hand, consumption remained strong by growing 5.4% in 2013. In line with the economic cycle, banking activity decreased as compared to 2012 in spite of maintaining attractive figures in loan growth and profitability. Although Chilean economic growth continues to be above the average of comparable countries and the world, we cannot assure you that the local economy will continue expanding in the future or developments in, or affecting, the Chilean economy and the local banking industry will not materially and adversely affect us, our business, financial condition or results of operations. For more information, see “Item 5. Operating and Financial Review and Prospects—Operating Results—Overview”.

Currency fluctuations could adversely affect the value of our ADSs and any distributions on the ADSs.

The Chilean Government’s economic policies and any future changes in the value of the Chilean peso with respect to the U.S. dollar could affect the dollar value of our common stock and our ADSs. Given the floating exchange rate regime that exists in Chile, the Chilean peso has been subject to large fluctuations in the past and could continue this trend in the future. According to information published by the Chilean Central Bank, between December 31, 2012 and December 31, 2013, the value of the U.S. dollar relative to the Chilean peso increased by approximately 9.4%, as compared to the decrease of 8.2% recorded in the period from December 31, 2011 to December 31, 2012. See “Item 3. Key Information—Exchange rates.”

Chilean trading in the shares underlying our ADSs is conducted in Chilean pesos. Cash dividends associated with our shares of common stock are received in Chilean pesos by the depositary, which then converts such amounts to U.S. dollars at the then-prevailing exchange rate for making payments in respect of our ADSs. If the value of the U.S. dollar increases relative to the Chilean peso, the dollar value of our ADSs and any distributions to be received from the depositary will decrease. In addition, the depositary will incur customary currency conversion costs (to be borne by the holders of our ADSs) in connection with the conversion and subsequent distribution of dividends or other payments. For more information, see “Item 10. Additional Information—Exchange Controls.”

Our results of operations may be affected by fluctuations in the exchange rates between the Chilean peso and the U.S. dollar despite our policy and Chilean regulations related to the general avoidance of material exchange rate mismatches. In order to reduce the effect of exchange rate mismatches we enter into foreign exchange derivative transactions that hedge our exposure. As of December 31, 2013, our foreign currency-denominated assets and Chilean peso-denominated assets, which contain repayment terms linked to changes in foreign currency exchange rates, were exceeded by our foreign currency-denominated liabilities and Chilean peso-denominated liabilities, which contain repayment terms linked to changes in foreign currency exchange rates, by an amount of Ch$781 million, or 0.04% of our paid-in capital and reserves.

We may decide to change our policy regarding exchange rate mismatches. Regulations that limit such mismatches may also be amended or eliminated by regulatory institutions. Higher exchange rate mismatches will increase our exposure to the devaluation of the Chilean peso, and any such devaluation may impair our capacity to service foreign-currency obligations and may, therefore, materially and adversely affect us, our financial condition and results of operations. Additionally, the economic policies of the Chilean Government and any future fluctuations of the Chilean peso with respect to the U.S. dollar could adversely affect our financial condition and results of operations.

12

Table of Contents

Chile has corporate disclosure standards different from those you may be familiar with in the United States.

Chilean disclosure requirements for publicly listed companies differ from those in the United States in some significant aspects. In addition, although Chilean law imposes restrictions on insider trading and price manipulation, the Chilean securities markets are not as highly regulated and closely supervised as the U.S. securities markets. Accordingly, the information about us available to you will not be the same as the information available to shareholders of a U.S. company. For more information, see “Item 16G. Corporate Governance.”

Chilean law provides shareholders with fewer and less well-defined rights.

Our corporate affairs are governed by our estatutos (bylaws) and the laws of Chile. Under such laws, our shareholders may have fewer or less well-defined rights than they might have as shareholders of a corporation incorporated in a U.S. jurisdiction. For example, our shareholders would not be entitled to appraisal rights in the event of a merger or other business combination undertaken by us.

A Potential Tax Reform in Chile may Increase our Tax Burden

A new administration assumed control of the Chilean government in March 2014. The new president has recently announced and sent to the Chilean congress a tax reform bill intended to finance improvements to the Chilean educational system, among other matters. The bill contemplates a gradual increase in the statutory corporate income tax rate, from the current 20.0% to a maximum of 25.0%, over a four-year period. In addition, the proposed bill includes changes in personal taxation for dividends-related taxes affecting both local and foreign investors, from a basis on cash dividends to a basis on accrued earnings of companies held as an investment. Similarly, the bill proposes a reduction in the tax rate for the upper income bracket, in the case of individuals, from 40.0% to 35.0%. As a result, the announced tax reform could adversely affect our results of operations, costs and profitability in the future. However, since the reform has not been yet passed in the congress, we cannot yet accurately estimate its potential effects on our operations. For more information, see “Item 10. Additional Information—Taxation—Chilean Tax Considerations—Tax Reform Proposal, by Presidential message N°24-362 (April 1 , 2014).”

13

Table of Contents

| Item 4 | Information on the Company |

History and Development of the Bank

Overview

We were founded in 1893, and we have been, for much of our history, among the largest and most profitable Chilean banks in terms of return on assets and equity in Chile. Our core business is commercial banking in Chile, providing traditional banking products and specialized financial services to our diversified customer base of individuals and companies.

Our legal name is Banco de Chile and we are organized as a banking corporation under the laws of Chile and were licensed by the SBIF to operate as a commercial bank on September 17, 1996. Our main executive offices are located at Paseo Ahumada 251, Santiago, Chile, our telephone number is +56 (2) 2637-1111 and our website is www.bancochile.cl . Our representative in the United States is Puglisi & Associates, with offices at 850 Library Avenue, Suite 204, Newark, Delaware 19711.

We are a full-service financial institution that provides, directly and indirectly through our subsidiaries and affiliates, a wide variety of lending and non-lending products and services to all segments of the Chilean financial market, providing powerful and differentiated value offerings to our customers. Our business is not materially affected by seasonality.

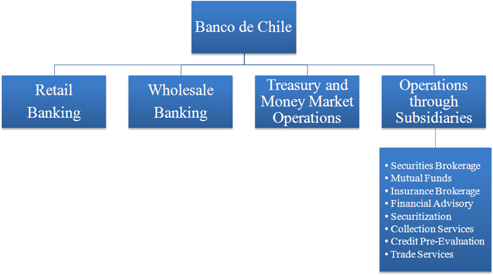

We organize our operations and deliver our services to our customers through the following four principal business segments:

| (i) | retail banking; |

| (ii) | wholesale banking; |

| (iii) | treasury and money markets; and |

| (iv) | subsidiaries. |

We provide our retail customers with credit cards, residential mortgage loans and consumer loans, as well as traditional deposit services, such as current accounts, demand deposits, savings accounts and time deposits. Our retail customers are composed of micro, small and medium sized companies that we serve by providing them with short and long term loans, as well as diverse deposit solution, in order to satisfy their needs. Our banking services for wholesale customers include commercial loans (which include factoring and leasing), foreign trade, capital markets services, cash management and non-lending services, such as payroll and payment services, as well as a wide range of treasury, financial advisory and risk management products.

In 2008, we supplemented our products and services and enhanced our value offerings by entering into a strategic partnership with Citigroup Inc., as a result of our merger with Citibank Chile.

As of December 31, 2013, we also offered international banking services through our Trade Services subsidiary in Hong Kong, our representative office in Beijing, and a worldwide network of correspondent banks.

In addition to our traditional banking operations, our subsidiaries and affiliates permit us to offer a variety of non-banking but specialized financial services including securities brokerage, mutual funds management, investment banking, insurance brokerage, securitization, collection and credit pre-evaluation services.

According to the SBIF, as of December 31, 2013 and excluding the operations of subsidiaries abroad, we were the second largest bank in Chile in terms of total loans with a market share of 19.1%, the largest provider of commercial loans with a market share of 19.5%, the second largest provider of consumer loans with a market share of 20.9% and the second largest privately owned bank in terms of residential mortgage loans with a market share of

14

Table of Contents

17.4%. Also, as published by the SBIF, we were the largest bank in terms of net income with a market share of 26.8% and the first bank in terms of current account balances held by individuals with a market share of 30.2%, both as of December 31, 2013. Lastly, according to the Chilean Association of Mutual Funds, as of December 31, 2013 we were the largest provider of mutual funds management with a market share of 21.3%.

As of December 31, 2013 we had:

| • |

total assets of Ch$25,873,708 million (approximately U.S.$49,216 million); |

| • |

total loans of Ch$20,880,770 million (approximately U.S.$39,718 million), before deducting allowances for loan losses; |

| • |

total deposits of Ch$16,387,057 million (approximately U.S.$ 31,171 million), of which Ch$5,984,332 million (approximately U.S.$ 11,383 million) correspond to current account and demand deposits; |

| • |