|

|

o |

REGISTRATION STATEMENT PURSUANT TO SECTION 12(b) OR (g) OF THE SECURITIES EXCHANGE ACT OF 1934

|

|

x

|

ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934

|

|

|

for the fiscal year ended December 31, 2011

|

|

o

|

TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934

|

|

|

for the transition period from ________________ to ________________

|

|

o

|

SHELL COMPANY REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934

|

|

|

Date of event requiring this shell company report

|

|

Title of each class

|

Name of each exchange on which registered

|

|

|

American Depositary Shares, each representing the right to receive 55 common shares, no par value, and 50 preferred shares, no par value, of Banco Santander (Brasil) S.A.

|

New York Stock Exchange

|

|

Large accelerated filer

x

|

Accelerated filer

o

|

Non-accelerated filer

o

|

|

US GAAP

o

|

International Financial Reporting Standards as

issued by the International Accounting Standards Board

x

|

Other

o

|

|

|

·

|

increases in defaults by our customers and in impairment losses;

|

|

|

·

|

decreases in deposits, customer loss or revenue loss;

|

|

|

·

|

increases in provisions for legal claims;

|

|

|

·

|

our ability to sustain or improve our performance;

|

|

|

·

|

changes in interest rates which may, among other effects, adversely affect margins;

|

|

|

·

|

competition in the banking, financial services, credit card services, insurance, asset management and related industries;

|

|

|

·

|

government regulation and tax matters;

|

|

|

·

|

adverse legal or regulatory disputes or proceedings;

|

|

|

·

|

credit, market and other risks of lending and investment activities;

|

|

|

·

|

decreases in our level of capitalization;

|

|

|

·

|

changes in market value of Brazilian securities, particularly Brazilian government securities;

|

|

|

·

|

changes in regional, national and international business and economic conditions and inflation;

|

|

|

·

|

the ongoing effects of recent volatility in global financial markets crisis; and

|

|

|

·

|

other risk factors as set forth under “Item 3. Key Information—D. Risk Factors”.

|

|

Directors and Senior Management

|

|

Advisers

|

|

Auditors

|

|

Offer Statistics

|

|

Method and Expected Timetable

|

|

Selected Financial Data

|

|

Santander Brasil

|

||||||||||||||||||||||||

|

For the year ended December 31,

|

||||||||||||||||||||||||

|

2011

|

2011

|

2010

|

2009

|

2008

|

2007

|

|||||||||||||||||||

|

(in millions of U.S.$, except as otherwise indicated)

(1)

|

(in millions of R$, except as otherwise indicated)

|

|||||||||||||||||||||||

|

Interest and similar income

|

27,581 | 51,736 | 40,909 | 39,343 | 23,768 | 13,197 | ||||||||||||||||||

|

Interest expense and similar charges

|

(12,706 | ) | (23,834 | ) | (16,814 | ) | (17,176 | ) | (12,330 | ) | (7,002 | ) | ||||||||||||

|

Net interest income

|

14,875 | 27,902 | 24,095 | 22,167 | 11,438 | 6,195 | ||||||||||||||||||

|

Income from equity instruments

|

50 | 94 | 52 | 30 | 37 | 36 | ||||||||||||||||||

|

Income from companies accounted for by the equity method

|

29 | 54 | 44 | 295 | 112 | 6 | ||||||||||||||||||

|

Fee and commission income

|

4,675 | 8,769 | 7,833 | 7,148 | 4,809 | 3,364 | ||||||||||||||||||

|

Fee and commission expense

|

(762 | ) | (1,430 | ) | (998 | ) | (910 | ) | (555 | ) | (266 | ) | ||||||||||||

|

Gains (losses) on financial assets and liabilities (net)

|

(61 | ) | (114 | ) | 1,458 | 2,716 | (1,286 | ) | 1,517 | |||||||||||||||

|

Exchange differences (net)

|

(65 | ) | (121 | ) | 417 | (51 | ) | 1,476 | 382 | |||||||||||||||

|

Other operating income (expenses)

|

(202 | ) | (379 | ) | (348 | ) | (115 | ) | (60 | ) | 133 | |||||||||||||

|

Total income

|

18,539 | 34,775 | 32,553 | 31,280 | 15,971 | 11,367 | ||||||||||||||||||

|

Administrative expenses

|

(6,596 | ) | (12,373 | ) | (11,231 | ) | (10,947 | ) | (7,185 | ) | (4,460 | ) | ||||||||||||

|

Depreciation and amortization

|

(779 | ) | (1,462 | ) | (1,237 | ) | (1,249 | ) | (846 | ) | (580 | ) | ||||||||||||

|

Provisions (net)

(2)

|

(1,632 | ) | (3,061 | ) | (1,974 | ) | (3,481 | ) | (1,230 | ) | (1,196 | ) | ||||||||||||

|

Impairment losses on financial assets (net)

(3)

|

(5,001 | ) | (9,382 | ) | (8,234 | ) | (9,966 | ) | (4,100 | ) | (2,160 | ) | ||||||||||||

|

Impairment losses on other assets (net)

|

(21 | ) | (39 | ) | (21 | ) | (901 | ) | (77 | ) | (298 | ) | ||||||||||||

|

Gains (losses) on disposal of assets not classified as non-current assets held for sale

|

3 | 5 | (59 | ) | 3,369 | 7 | 1 | |||||||||||||||||

|

Gains (losses) on non-current assets held for sale not classified as discontinued operations

|

238 | 447 | 199 | 32 | 9 | 13 | ||||||||||||||||||

|

Operating profit before tax

|

4,751 | 8,911 | 9,997 | 8,137 | 2,549 | 2,687 | ||||||||||||||||||

|

Income taxes

|

(616 | ) | (1,155 | ) | (2,614 | ) | (2,629 | ) | (170 | ) | (784 | ) | ||||||||||||

|

Profit for the year

|

4,135 | 7,756 | 7,383 | 5,508 | 2,379 | 1,903 | ||||||||||||||||||

|

Earnings per share

|

||||||||||||||||||||||||

|

Basic and diluted earnings per 1,000 shares

|

||||||||||||||||||||||||

|

Common shares (

reais

)

|

18.55 | 17.67 | 15.32 | 11.59 | 14.02 | |||||||||||||||||||

|

Preferred shares (

reais

)

|

20.41 | 19.44 | 16.85 | 12.75 | 15.43 | |||||||||||||||||||

|

Common shares (U.S. dollars)

(1)

|

9.89 | 10.61 | 9.19 | 6.69 | 8.41 | |||||||||||||||||||

|

Preferred shares (U.S. dollars)

(1)

|

10.88 | 11.67 | 10.11 | 7.65 | 9.26 | |||||||||||||||||||

|

Santander Brasil

|

||||||||||||||||||||||||

|

For the year ended December 31,

|

||||||||||||||||||||||||

|

2011

|

2011

|

2010

|

2009

|

2008

|

2007

|

|||||||||||||||||||

|

(in millions of U.S.$, except as otherwise indicated)

(1)

|

(in millions of R$, except as otherwise indicated)

|

|||||||||||||||||||||||

|

Dividends and interest on capital per 1,000 shares

(4)

|

||||||||||||||||||||||||

|

Common shares (

reais

)

|

7.61 | 8.47 | 4.11 | 4.26 | 16.30 | |||||||||||||||||||

|

Preferred shares (

reais

)

|

8.37 | 9.32 | 4.52 | 4.69 | 17.93 | |||||||||||||||||||

|

Common shares (U.S. dollars)

(1)

|

4.06 | 5.08 | 2.47 | 2.56 | 9.78 | |||||||||||||||||||

|

Preferred shares (U.S. dollars)

(1)

|

4.46 | 5.59 | 2.71 | 2.81 | 10.76 | |||||||||||||||||||

|

Weighted average shares outstanding (in thousands) – basic and diluted

|

||||||||||||||||||||||||

|

Common shares

|

212,841,732 | 212,841,732 | 183,650,861 | 104,926,194 | 69,383,705 | |||||||||||||||||||

|

Preferred shares

|

186,202,385 | 186,202,385 | 159,856,132 | 91,168,064 | 60,285,449 | |||||||||||||||||||

|

(1)

|

Translated for convenience only using the selling rate as reported by the Brazilian Central Bank at December 31, 2011 for

reais

into U.S. dollars of R$1.87 to U.S.$1.00.

|

|

(2)

|

Mainly provisions for legal obligations, tax and social security, labor and civil litigations.

|

|

(3)

|

Net provisions to the credit loss allowance less recovery of loans previously written off.

|

|

(4)

|

Includes dividends based on net income and dividends based on reserves.

|

|

Santander Brasil

|

||||||||||||||||||||||||

|

At December 31,

|

||||||||||||||||||||||||

|

2011

|

2011

|

2010

|

2009

|

2008

|

2007

|

|||||||||||||||||||

|

(in millions of U.S.$)

(1)

|

(in millions of R$)

|

|||||||||||||||||||||||

|

Assets

|

||||||||||||||||||||||||

|

Cash and balances with the Brazilian Central Bank

|

35,152 | 65,938 | 56,800 | 27,269 | 23,700 | 22,277 | ||||||||||||||||||

|

Financial assets held for trading

|

15,941 | 29,901 | 24,821 | 20,116 | 19,986 | 12,293 | ||||||||||||||||||

|

Other financial assets at fair value through profit or loss

(2)

|

355 | 665 | 17,940 | 16,295 | 5,575 | 1,648 | ||||||||||||||||||

|

Available-for-sale financial assets

|

23,781 | 44,608 | 47,206 | 46,406 | 30,736 | 9,303 | ||||||||||||||||||

|

Loans and receivables

|

108,091 | 202,757 | 174,107 | 152,163 | 162,725 | 55,034 | ||||||||||||||||||

|

Hedging derivatives

|

43 | 81 | 116 | 163 | 106 | – | ||||||||||||||||||

|

Non-current assets held for sale

|

71 | 132 | 67 | 172 | 113 | 32 | ||||||||||||||||||

|

Investments in associates

|

225 | 422 | 371 | 419 | 634 | 55 | ||||||||||||||||||

|

Tangible assets

|

2,670 | 5,008 | 4,518 | 3,702 | 3,829 | 1,111 | ||||||||||||||||||

|

Intangible assets

|

16,758 | 31,435 | 31,963 | 31,618 | 30,995 | 1,799 | ||||||||||||||||||

|

Tax assets

|

8,663 | 16,250 | 14,842 | 15,779 | 12,920 | 4,223 | ||||||||||||||||||

|

Other assets

|

1,432 | 2,687 | 1,912 | 1,871 | 2,871 | 544 | ||||||||||||||||||

|

Total assets

|

213,182 | 399,886 | 374,663 | 315,973 | 294,190 | 108,319 | ||||||||||||||||||

|

Liabilities

|

||||||||||||||||||||||||

|

Financial liabilities held for trading

|

2,691 | 5,047 | 4,785 | 4,435 | 11,210 | 4,650 | ||||||||||||||||||

|

Other financial liabilities at fair value through profit or loss

|

– | – | – | 2 | 307 | 690 | ||||||||||||||||||

|

Financial liabilities at amortized cost

|

155,375 | 291,452 | 253,341 | 203,568 | 213,973 | 84,781 | ||||||||||||||||||

|

Deposits from the Brazilian Central Bank and deposits from credit institutions

|

27,469 | 51,527 | 42,392 | 21,196 | 26,510 | 18,217 | ||||||||||||||||||

|

Customer deposits

|

93,013 | 174,474 | 167,949 | 149,440 | 155,495 | 55,147 | ||||||||||||||||||

|

Marketable debt securities

|

20,573 | 38,590 | 20,087 | 11,439 | 12,086 | 2,806 | ||||||||||||||||||

|

Subordinated liabilities

|

5,815 | 10,908 | 9,695 | 11,305 | 9,197 | 4,210 | ||||||||||||||||||

|

Other financial liabilities

|

8,504 | 15,952 | 13,218 | 10,188 | 10,685 | 4,401 | ||||||||||||||||||

|

Hedging derivatives

|

19 | 36 | – | 10 | 265 | – | ||||||||||||||||||

|

Liabilities for insurance contracts

|

– | – | 19,643 | 15,527 | – | – | ||||||||||||||||||

|

Provisions

(3)

|

5,073 | 9,515 | 9,395 | 9,480 | 8,915 | 4,816 | ||||||||||||||||||

|

Santander Brasil

|

||||||||||||||||||||||||

|

At December 31,

|

||||||||||||||||||||||||

|

2011

|

2011

|

2010

|

2009

|

2008

|

2007

|

|||||||||||||||||||

|

(in millions of U.S.$)

(1)

|

(in millions of R$)

|

|||||||||||||||||||||||

|

Tax liabilities

|

6,331 | 11,876 | 10,530 | 9,457 | 6,156 | 1,719 | ||||||||||||||||||

|

Other liabilities

|

2,094 | 3,928 | 3,605 | 4,228 | 3,527 | 1,454 | ||||||||||||||||||

|

Total liabilities

|

171,582 | 321,854 | 301,299 | 246,707 | 244,353 | 98,111 | ||||||||||||||||||

|

Shareholders’ equity

|

41,073 | 77,045 | 72,572 | 68,706 | 49,318 | 8,671 | ||||||||||||||||||

|

Valuation adjustments

|

516 | 968 | 784 | 559 | 514 | 1,537 | ||||||||||||||||||

|

Non-controlling interests

|

10 | 19 | 8 | 1 | 5 | – | ||||||||||||||||||

|

Total equity

|

41,599 | 78,032 | 73,364 | 69,266 | 49,837 | 10,208 | ||||||||||||||||||

|

Total liabilities and equity

|

213,182 | 399,886 | 374,663 | 315,973 | 294,190 | 108,319 | ||||||||||||||||||

|

Average assets

|

210,429 | 394,722 | 341,285 | 298,174 | 163,621 | 100,243 | ||||||||||||||||||

|

Average interest-bearing liabilities

|

130,316 | 244,446 | 198,456 | 184,332 | 109,455 | 69,204 | ||||||||||||||||||

|

Average shareholders’ equity

|

40,365 | 75,716 | 71,875 | 56,192 | 23,110 | 10,521 | ||||||||||||||||||

|

(1)

|

Translated for convenience only using the selling rate as reported by the Brazilian Central Bank at December 31, 2011 for

reais

into U.S. dollars of R$1.87 to U.S.$1.00.

|

|

(2)

|

In 2010 and 2009, this item includes Investment fund units of Guarantors of Benefit Plans—PGBL/VGBL, in the amount of R$17,426 million and R$14,184 million, respectively, related to the liabilities for insurance contracts held by Santander Seguros, which were no longer included in the scope of consolidation in 2011, following the sale of Santander Seguros. See “Item 4. Information on the Company—A. History and Development of the Company—Important Events—Sale of Santander Seguros”.

|

|

(3)

|

Mainly legal obligations, tax and social security, labor and civil litigation.

|

|

At and for the year ended December 31,

|

||||||||||||||||||||

|

2011

|

2010

|

2009

|

2008

|

2007

|

||||||||||||||||

|

Profitability and performance

|

||||||||||||||||||||

|

Net yield

(1)

|

8.6 | % | 8.8 | % | 9.7 | % | 8.6 | % | 7.2 | % | ||||||||||

|

Return on average total assets

|

2.0 | % | 2.2 | % | 1.8 | % | 1.5 | % | 1.9 | % | ||||||||||

|

Return on average shareholders’ equity

|

10.2 | % | 10.3 | % | 9.8 | % | 10.3 | % | 18.1 | % | ||||||||||

|

Adjusted return on average shareholders’ equity

(2)

|

16.2 | % | 16.9 | % | 19.3 | % | 16.8 | % | 18.1 | % | ||||||||||

|

Capital adequacy

|

||||||||||||||||||||

|

Average shareholders’ equity as a percentage of average total assets

|

19.2 | % | 21.1 | % | 18.8 | % | 14.1 | % | 10.5 | % | ||||||||||

|

Average shareholders’ equity excluding goodwill as a percentage of average total assets excluding goodwill

(2)

|

13.0 | % | 13.9 | % | 10.5 | % | 9.2 | % | 10.5 | % | ||||||||||

|

Basel capital adequacy ratio

(3)

|

19.9 | % | 22.1 | % | 25.6 | % | 14.7 | % | 14.2 | % | ||||||||||

|

Asset quality

|

||||||||||||||||||||

|

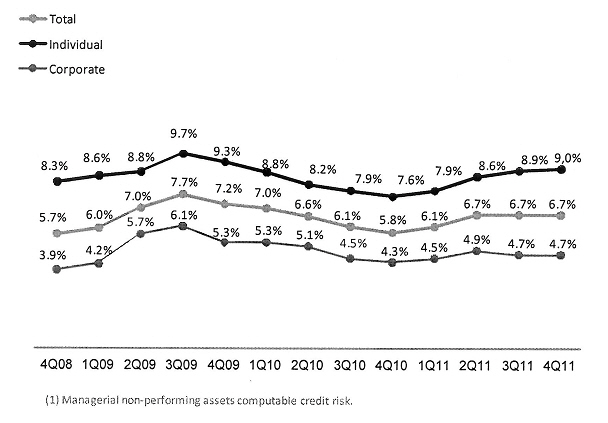

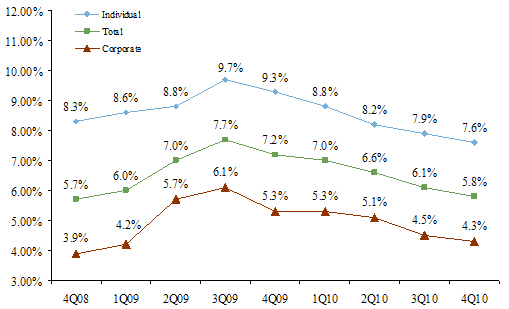

Non-performing assets as a percentage of total loans

(4)

|

6.7 | % | 5.8 | % | 7.2 | % | 5.4 | % | 4.1 | % | ||||||||||

|

Non-performing assets as a percentage of total assets

(4)

|

3.3 | % | 2.7 | % | 3.1 | % | 2.6 | % | 2.2 | % | ||||||||||

|

Non-performing assets as a percentage of computable credit risk

(4)(5)

|

6.0 | % | 5.1 | % | 6.2 | % | 4.7 | % | 3.2 | % | ||||||||||

|

Allowance for credit losses as a percentage of non-performing assets

(4)

|

85.5 | % | 98.3 | % | 101.7 | % | 105.8 | % | 107.5 | % | ||||||||||

|

Allowance for credit losses as a percentage of total loans

|

5.7 | % | 5.8 | % | 7.2 | % | 5.4 | % | 4.4 | % | ||||||||||

|

Net loan charge-offs as a percentage of total loans

|

4.7 | % | 6.2 | % | 6.2 | % | 2.3 | % | 4.7 | % | ||||||||||

|

Non-performing assets as a percentage of shareholders’ equity

(4)

|

17.0 | % | 12.9 | % | 14.4 | % | 15.7 | % | 24.1 | % | ||||||||||

|

At and for the year ended December 31,

|

||||||||||||||||||||

|

2011

|

2010

|

2009

|

2008

|

2007

|

||||||||||||||||

|

Non-performing assets as a percentage of shareholders’ equity excluding goodwill

(2)(4)

|

26.2 | % | 21.1 | % | 24.5 | % | 35.4 | % | 24.1 | % | ||||||||||

|

Liquidity

|

||||||||||||||||||||

|

Total loans, net as a percentage of total funding

|

66.4 | % | 63.0 | % | 66.4 | % | 66.0 | % | 60.7 | % | ||||||||||

|

Deposits as a percentage of total funding

|

82.0 | % | 87.6 | % | 88.2 | % | 89.5 | % | 91.3 | % | ||||||||||

|

Other Information

|

||||||||||||||||||||

|

Efficiency

|

||||||||||||||||||||

|

Efficiency ratio

(6)

|

35.6 | % | 34.5 | % | 35.0 | % | 45.0 | % | 39.2 | % | ||||||||||

|

(1)

|

Net yield is defined as net interest income (including dividends on equity securities) divided by average interest earning assets.

|

|

(2)

|

“Adjusted return on average shareholders’ equity”, “Average shareholders’ equity excluding goodwill as a percentage of average total assets excluding goodwill” and “Non-performing assets as a percentage of shareholders’ equity excluding goodwill” are non-GAAP financial measurements which adjust “Return on average shareholders’ equity”, “Average shareholders’ equity as a percentage of average total assets” and “Non-performing assets as a percentage of shareholders’ equity”, to exclude the R$27 billion goodwill arising from the acquisition of Banco Real in 2008.

|

|

At and for the year ended December 31,

|

||||||||||||||||

|

2011

|

2010

|

2009

|

2008

|

|||||||||||||

|

(in millions of R$, except as otherwise indicated)

|

||||||||||||||||

|

Return on average shareholders’ equity:

|

||||||||||||||||

|

Consolidated profit for the year

|

7,756 | 7,383 | 5,508 | 2,379 | ||||||||||||

|

Average shareholders’ equity

|

75,716 | 71,875 | 56,192 | 23,110 | ||||||||||||

|

Return on average shareholders’ equity

|

10.2 | % | 10.3 | % | 9.8 | % | 10.3 | % | ||||||||

|

Adjusted return on average shareholders’ equity:

|

||||||||||||||||

|

Consolidated profit for the year

|

7,756 | 7,383 | 5,508 | 2,379 | ||||||||||||

|

Average shareholders’ equity

|

75,716 | 71,875 | 56,192 | 23,110 | ||||||||||||

|

Average goodwill

|

27,975 | 28,312 | 27,714 | 8,925 | ||||||||||||

|

Average shareholders’ equity excluding goodwill

|

47,741 | 43,562 | 28,478 | 14,185 | ||||||||||||

|

Adjusted return on average shareholders’ equity

|

16.2 | % | 16.9 | % | 19.3 | % | 16.8 | % | ||||||||

|

Average shareholders’ equity as a percentage of average total assets:

|

||||||||||||||||

|

Average shareholders’ equity

|

75,716 | 71,875 | 56,192 | 23,110 | ||||||||||||

|

Average total assets

|

394,722 | 341,284 | 298,173 | 163,621 | ||||||||||||

|

Average shareholders’ equity as a percentage of average total assets

|

19.2 | % | 21.1 | % | 18.8 | % | 14.1 | % | ||||||||

|

Average shareholders’ equity excluding goodwill as a percentage of average total assets excluding goodwill:

|

||||||||||||||||

|

Average shareholders’ equity

|

75,716 | 71,875 | 56,192 | 23,110 | ||||||||||||

|

Average goodwill

|

27,975 | 28,312 | 27,714 | 8,925 | ||||||||||||

|

Average shareholders’ equity excluding goodwill

|

47,741 | 43,562 | 28,478 | 14,185 | ||||||||||||

|

Average total assets

|

394,722 | 341,284 | 298,173 | 163,621 | ||||||||||||

|

Average goodwill

|

27,975 | 28,312 | 27,714 | 8,925 | ||||||||||||

|

Average total assets excluding goodwill

|

366,746 | 312,972 | 270,460 | 154,696 | ||||||||||||

|

Average shareholders’ equity excluding goodwill as a percentage of average total assets excluding goodwill

|

13.0 | % | 13.9 | % | 10.5 | % | 9.2 | % | ||||||||

|

At and for the year ended December 31,

|

||||||||||||||||

|

2011

|

2010

|

2009

|

2008

|

|||||||||||||

|

(in millions of R$, except as otherwise indicated)

|

||||||||||||||||

|

Non-performing assets as a percentage of shareholders’ equity:

|

||||||||||||||||

|

Non-performing assets

|

13,073 | 9,349 | 9,900 | 7,730 | ||||||||||||

|

Shareholders’ equity

|

77,045 | 72,572 | 68,706 | 49,318 | ||||||||||||

|

Non-performing assets as a percentage of shareholders’ equity

|

17.0 | % | 12.9 | % | 14.4 | % | 15.7 | % | ||||||||

|

Non-performing assets as a percentage of shareholders’ equity excluding goodwill:

|

||||||||||||||||

|

Non-performing assets

|

13,073 | 9,349 | 9,900 | 7,730 | ||||||||||||

|

Shareholders’ equity

|

77,045 | 72,572 | 68,706 | 49,318 | ||||||||||||

|

Goodwill

|

27,218 | 28,312 | 28,312 | 27,488 | ||||||||||||

|

Shareholders’ equity excluding goodwill

|

49,827 | 44,259 | 40,394 | 21,829 | ||||||||||||

|

Non-performing assets as a percentage of shareholders’ equity excluding goodwill

|

26.2 | % | 21.1 | % | 24.5 | % | 35.4 | % | ||||||||

|

(3)

|

In July 2008, new regulatory capital measurement rules, which implement the Basel II standardized approach, went into effect in Brazil, including a new methodology for credit risk and operational risk measurement, analysis and management. As a result, our capital adequacy ratios as of any date after July 2008 are not comparable to our capital ratios as of any prior date. Our Basel capital adequacy ratios are calculated excluding goodwill, in accordance with the Basel II standardized approach (provided by the “International Convergence of Capital Measurement and Capital Standards—A Revised Framework Comprehensive Version” issued by the Basel Committee on Banking Supervision from the Bank for International Settlements). In December 2010, the Brazilian Central Bank issued the Circular 3,515 that introduced the rule weight of 150% for lending operations over 24 months, allowing some exceptions given the type of operation, maturity and guarantees. In November 2011, the Circular 3,515 was revoked and the Brazilian Central Bank issued the Circular 3,563 that required the application of 150% ask weight for financing vehicles, risk weight reduction for payroll loans originated up to July 2011 from 150% to 75% or 100%, and raised the risk weight to 300% for payroll and personal loans that have no specific purpose and a term over 60 months, originated as from November 14, 2011.

|

|

(4)

|

Non-performing assets include all credits past due by more than 90 days and other doubtful credits. For further information see “Item 4. Information on the Company—Selected Statistical Information—Impaired Assets”.

|

|

(5)

|

Computable credit risk is the sum of the face amounts of loans and leases (including non-performing assets), guarantees and documentary credits.

|

|

(6)

|

Efficiency ratio is defined as administrative expenses divided by total income. Our calculation for the efficiency ratio disclosed herein differs from another, with similar name, used by us in our quarterly managerial reports, due to an adjustment made in those quarterly reports in light of the results of the hedge of the investment in the Cayman Islands branch, which is included in our total income. The adjustment, which impacts the line items income tax, gains (losses) on financial assets and liabilities and exchange rate differences, does not affect net profit. Our management believes that the adjusted efficiency ratio provides a more consistent framework for evaluating and conducting business, as a result of excluding from our revenues the effect of the volatility caused by possible gains and losses on our hedging strategies for tax purposes. For example, in 2011, the effects of the devaluation of the

real

against the U.S. dollar impacted our hedging of the investments held in our Cayman Islands branch generating losses of R$1,646 million recorded under “gains/losses on

|

|

At and for the years ended December 31,

|

||||||||||||||||||||

|

2011

|

2010

|

2009

|

2008

|

2007

|

||||||||||||||||

|

(in millions of R$, except as otherwise indicated)

|

||||||||||||||||||||

|

Efficiency ratio

|

||||||||||||||||||||

|

Administrative expenses

|

12,373 | 11,231 | 10,947 | 7,185 | 4,460 | |||||||||||||||

|

Total income

|

34,775 | 32,553 | 31,280 | 15,971 | 11,367 | |||||||||||||||

|

of which:

|

||||||||||||||||||||

|

Gains (losses) on financial assets and liabilities (net)

|

(235 | ) | 1,875 | 2,665 | 190 | 1,899 | ||||||||||||||

|

Efficiency ratio

|

35.6 | % | 34.5 | % | 35.0 | % | 45.0 | % | 39.2 | % | ||||||||||

|

Total Income

|

34,775 | 32,553 | 31,280 | 15,971 | 11,367 | |||||||||||||||

|

Income tax including effects of Cayman tax hedge

|

1,646 | 272 | 1,146 | – | – | |||||||||||||||

|

Total income excluding effects of Cayman tax hedge

|

36,421 | 32,281 | 30,134 | 15,971 | 11,367 | |||||||||||||||

|

Administrative expenses

|

12,373 | 11,231 | 10,947 | 7,185 | 4,460 | |||||||||||||||

|

Total income excluding effects of Cayman tax hedge

|

36,421 | 32,281 | 30,134 | 15,971 | 11,367 | |||||||||||||||

|

of which:

|

||||||||||||||||||||

|

Gains (losses) on financial assets and liabilities (net) excluding effects of Cayman tax hedge

|

1,411 | 1,603 | 1,519 | 190 | 1,899 | |||||||||||||||

|

Efficiency ratio adjusted for effects of Cayman tax hedge

|

34.0 | % | 34.8 | % | 36.3 | % | 45.0 | % | 39.2 | % | ||||||||||

|

Period-end

|

Average

(1)

|

Low

|

High

|

|||||||||||||

|

(per U.S. dollar)

|

||||||||||||||||

|

Year:

|

||||||||||||||||

|

2007

|

1.77 | 1.95 | 1.73 | 2.15 | ||||||||||||

|

2008

|

2.33 | 1.84 | 1.56 | 2.50 | ||||||||||||

|

2009

|

1.74 | 1.99 | 1.70 | 2.42 | ||||||||||||

|

2010

|

1.66 | 1.76 | 1.65 | 1.88 | ||||||||||||

|

2011

|

1.87 | 1.67 | 1.53 | 1.90 | ||||||||||||

|

Period-end

|

Average

(1)

|

Low

|

High

|

|||||||||||||

|

(per U.S. dollar)

|

||||||||||||||||

|

Month Ended:

|

||||||||||||||||

|

October 2011

|

1.69 | 1.77 | 1.69 | 1.89 | ||||||||||||

|

November 2011

|

1.81 | 1.79 | 1.73 | 1.89 | ||||||||||||

|

December 2011

|

1.87 | 1.84 | 1.78 | 1.88 | ||||||||||||

|

January 2012

|

1.74 | 1.79 | 1.74 | 1.87 | ||||||||||||

|

February 2012

|

1.71 | 1.72 | 1.70 | 1.74 | ||||||||||||

|

March 2012 (through March 29)

|

1.83 | 1.79 | 1.72 | 1.83 | ||||||||||||

|

(1)

|

Represents the average of the exchange rates on the closing of each business day during the period.

|

|

|

|

Reasons for the Offer and Use of Proceeds

|

|

Risk Factors

|

|

|

·

|

interest rates;

|

|

|

·

|

exchange rates and controls and restrictions on the movement of capital out of Brazil (such as those briefly imposed in 1989 and early 1990);

|

|

|

·

|

currency fluctuations;

|

|

|

·

|

inflation;

|

|

|

·

|

liquidity of the domestic capital and lending markets; and

|

|

|

·

|

tax and regulatory policies.

|

|

|

·

|

minimum capital requirements;

|

|

|

·

|

compulsory deposit and/or reserve requirements;

|

|

|

·

|

requirements for investments in fixed rate assets;

|

|

|

·

|

lending limits and other credit restrictions, including compulsory allocations;

|

|

|

·

|

limits and other restrictions on fees;

|

|

|

·

|

limits on the amount of interest banks can charge or the period for capitalizing interest;

|

|

|

·

|

accounting and statistical requirements; and

|

|

|

·

|

other requirements or limitations in the context of the global financial crisis.

|

|

|

·

|

limiting our ability to increase our customer base and expand our operations;

|

|

|

·

|

reducing our profit margins on the banking, insurance, leasing and other services and products we offer; and

|

|

|

·

|

increasing competition for investment opportunities.

|

|

|

·

|

elect a majority of our directors that appoint our executive officers, set our management policies and exercise overall control over our company and subsidiaries;

|

|

|

·

|

agree to sell or otherwise transfer its controlling stake in our company; and

|

|

|

·

|

determine the outcome of substantially all actions requiring shareholder approval, including transactions with related parties, corporate reorganizations, acquisitions and dispositions of assets, and dividends.

|

|

History and Development of the Company

|

|

Business Overview

|

|

|

·

|

leverage the Santander Group’s global information systems platform, reducing our technology development costs, providing operational synergies with the Santander Group and enhancing our ability to provide international products and services to our customers;

|

|

|

·

|

access the Santander Group’s multinational client base;

|

|

|

·

|

take advantage of the Santander Group’s global presence, in particular in other countries in Latin America, to offer international solutions for our Brazilian corporate customers’ financial needs as they expand their operations globally;

|

|

|

·

|

selectively replicate or adapt the Santander Group’s successful product offerings from other countries in Brazil;

|

|

|

·

|

benefit from the Santander Group’s operational expertise in areas such as internal controls and risk management, which practices have been developed in response to a wide range of market conditions across the world and which we believe will enhance our ability to expand our business within desired risk limits;

|

|

|

·

|

leverage the Santander Group’s experience with integrations to maximize and accelerate the generation of synergies from any future acquisitions; and

|

|

|

·

|

benefit from the Santander Group’s management training and development which is composed of a combination of in-house training and development with access to managerial expertise in other Santander Group units outside Brazil.

|

|

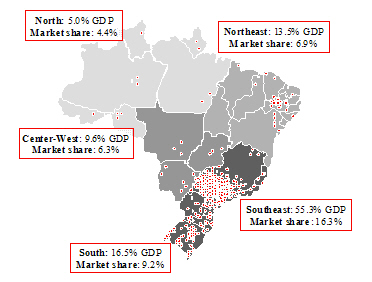

At November 30, 2011

Market share (%)

|

||||

|

Payroll/individual loans

|

11.9 | |||

|

Individual loans

|

19.2 | |||

|

Payroll

|

7.8 | |||

|

Auto leasing/CDC

|

15.0 | |||

|

Credit cards

|

11.8 | |||

|

Branches*

|

12.4 | |||

|

Southeast*

|

16.2 | |||

|

South*

|

9.3 | |||

|

|

·

|

Full consolidation of the operational databases;

|

|

|

·

|

Leverage the fact that we are a well prepared bank with products and services that suit different segments;

|

|

|

·

|

Aggressively reposition the bank within target markets;

|

|

|

·

|

Improve our strategic position and relationships with clients and other markets;

|

|

|

·

|

Value our brand

|

|

Commercial Banking

|

Global Wholesale Banking

|

Asset Management and Insurance

|

||

|

·

Retail banking

– Individuals

– SMEs

·

Enterprises with annual gross revenues in excess of R$30 million but less than R$250 million

·

Corporations with annual gross revenues in excess of R$250 million (other than global corporate clients)

·

Consumer finance

|

·

Global corporate clients, or GB&M

·

Treasury

|

·

Asset management

·

Insurance brokerage

|

|

For the year ended December 31,

|

||||||||||||||||||||||||

|

2011

|

2010

|

2009

|

2011

|

2010

|

2009

|

|||||||||||||||||||

|

Net interest income

|

Profit before tax

|

|||||||||||||||||||||||

|

(in millions of R$)

|

||||||||||||||||||||||||

|

Commercial Banking

|

24,971 | 21,301 | 20,091 | 5,128 | 6,347 | 4,898 | ||||||||||||||||||

|

Global Wholesale Banking

|

2,589 | 2,501 | 1,943 | 2,947 | 2,818 | 2,689 | ||||||||||||||||||

|

Asset Management and Insurance

|

342 | 292 | 133 | 835 | 832 | 550 | ||||||||||||||||||

|

Total

|

27,902 | 24,095 | 22,167 | 8,911 | 9,997 | 8,137 | ||||||||||||||||||

|

|

·

|

Private banking

: We seek to provide our private banking customers personal service from a highly trained team in exclusive offices, with the objective of providing privacy and individualized service.

|

|

|

·

|

High-income customers

: Our model includes differentiated areas in our regular branches (Van Gogh area) and is based on personal relationships with our account managers.

|

|

|

·

|

Mid-income customers

: We use a multi-channel service model, supported by our account managers. We provide differentiated services to customers we view as upwardly mobile.

|

|

|

·

|

Low-income customers

: Our emphasis is on serving customers through alternative channels. In our branches, these customers are served under a standardized model through pools of managers, with a sales-oriented approach. Differentiated services are offered to customers we view as upwardly mobile.

|

|

|

·

|

SMEs

: For medium-sized enterprises, our model is centered on a relationship with the account manager while for small-sized enterprises, we rely more on multi-channel distribution. Special platforms are used to offer differentiated services to clients with a high earnings potential.

|

|

|

·

|

current accounts, saving accounts and time deposits;

|

|

|

·

|

loans to individual customers, including consumer finance, personal loans and payroll loans;

|

|

|

·

|

credit cards;

|

|

|

·

|

loans to SMEs;

|

|

|

·

|

agricultural loans;

|

|

|

·

|

mortgages;

|

|

|

·

|

leasing;

|

|

|

·

|

insurance and asset management products;

|

|

|

·

|

private retirement plans; and

|

|

|

·

|

cash management services for SMEs.

|

|

|

·

|

current accounts (also referred to as demand deposits), which do not bear interest;

|

|

|

·

|

traditional savings accounts, which currently earn the Brazilian reference rate for savings accounts (

taxa referencial

) plus 0.5% per month, as set by the federal government; and

|

|

|

·

|

time deposits, also known as certificates of bank deposits, or “CDBs”, which are highly liquid and earn interest at a fixed or floating rate.

|

|

At December 31,

|

||||||||||||

|

2011

|

2010

|

2009

|

||||||||||

|

(in millions of R$)

|

||||||||||||

|

Customer deposits

|

||||||||||||

|

Current accounts

|

13,561 | 16,132 | 15,140 | |||||||||

|

Savings accounts

|

23,293 | 30,303 | 25,216 | |||||||||

|

Time deposits

|

83,942 | 68,916 | 74,634 | |||||||||

|

Repurchase Agreements

|

53,678 | 52,598 | 34,450 | |||||||||

|

Total customer deposits

|

174,474 | 167,949 | 149,440 | |||||||||

|

Deposits from the Brazilian Central Bank and credit institutions

|

||||||||||||

|

Time deposits

|

27,023 | 28,867 | 20,838 | |||||||||

|

Demand deposits

|

133 | 344 | 195 | |||||||||

|

Repurchase Agreements

|

24,371 | 13,180 | 164 | |||||||||

|

Total

|

51,527 | 42,391 | 21,197 | |||||||||

|

At December 31,

|

Change, at December 31, 2011 vs. December 31, 2010

|

|||||||||||||||||||

|

2011

|

2010

|

2009

|

R$ million

|

%

|

||||||||||||||||

|

(in millions of R$)

|

||||||||||||||||||||

|

Individuals

|

63,413 | 50,981 | 43,200 | 12,432 | 24.4 | |||||||||||||||

|

Consumer finance

|

30,459 | 26,969 | 25,101 | 3,490 | 12.9 | |||||||||||||||

|

Small and Medium Enterprises

(1)

|

47,940 | 38,178 | 31,448 | 9,762 | 25.6 | |||||||||||||||

|

Corporations

(2)

|

52,373 | 44,431 | 38,645 | 7,942 | 17.9 | |||||||||||||||

|

Total

|

194,184 | 160,558 | 138,394 | 33,626 | 20.9 | |||||||||||||||

|

(1)

|

Companies with annual gross revenues of up to R$250 million.

|

|

(2)

|

Companies with annual gross revenues exceeding R$250 million, including our global corporate clients.

|

|

At December 31,

|

Change, at December 31, 2011 vs. December 31, 2010

|

|||||||||||||||||||

|

2011

|

2010

|

2009

|

R$ million

|

%

|

||||||||||||||||

|

(in millions of R$)

|

||||||||||||||||||||

|

Leasing/Auto Loans

(1)

|

2,277 | 2,471 | 2,121 | (194 | ) | (7.9 | ) | |||||||||||||

|

Credit cards

|

14,144 | 10,760 | 8,472 | 3,384 | 31.5 | |||||||||||||||

|

Payroll loans

(2)

|

12,248 | 9,600 | 7,864 | 2,648 | 27.6 | |||||||||||||||

|

Mortgages

|

10,018 | 6,698 | 5,226 | 3,320 | 49.6 | |||||||||||||||

|

Agricultural Loans

|

2,492 | 2,817 | 3,073 | (325 | ) | (11.5 | ) | |||||||||||||

|

Personal loans/Other

|

22,234 | 18,635 | 16,445 | 3,599 | 19.3 | |||||||||||||||

|

Total

|

63,413 | 50,981 | 43,200 | 12,432 | 24.4 | |||||||||||||||

|

(1)

|

Including the loans to individuals in the consumer finance segment, the auto loan portfolio totaled R$27,556 million in the fourth quarter of 2011, R$24,173 million in the fourth quarter of 2010, and R$22,575 million in the fourth quarter of 2009.

|

|

(2)

|

Including Payroll Loan acquired portfolio, Payroll loans totaled R$15,142 million in the fourth quarter of 2011, R$13,800 million in the fourth quarter of 2010 and R$10,084 million in the fourth quarter of 2009.

|

|

At December 31,

|

Change, December 31, 2011 vs. December 31, 2010

|

|||||||||||||||||||

|

2011

|

2010

|

2009

|

R$ million

|

%

|

||||||||||||||||

|

(in millions of R$)

|

||||||||||||||||||||

|

Agricultural lending

|

117 | 112 | 156 | 5 | 4.3 | |||||||||||||||

|

Working capital loans

|

16,776 | 12,442 | 9,138 | 4,324 | 34.8 | |||||||||||||||

|

Buyer financing

|

85 | 38 | 31 | 47 | 123.0 | |||||||||||||||

|

Vendor financing

|

3 | 2 | 10 | 1 | 37.2 | |||||||||||||||

|

Discounted receivables

|

740 | 533 | 428 | 207 | 38.8 | |||||||||||||||

|

Comex

|

302 | 202 | 201 | 100 | 49.4 | |||||||||||||||

|

Overdraft facility

|

4,029 | 3,647 | 3,084 | 381 | 10.5 | |||||||||||||||

|

Refinancing

|

3,189 | 2,793 | 3,169 | 396 | 14.2 | |||||||||||||||

|

Resolution 2,770

|

38 | 58 | 115 | (20 | ) | (35.1 | ) | |||||||||||||

|

Account overdraft loans

|

2,638 | 1,798 | 1,341 | 839 | 46.7 | |||||||||||||||

|

CDC/leasing

(1)

|

2,323 | 2,551 | 2,466 | (228 | ) | (8.9 | ) | |||||||||||||

|

Other

(2)

|

2,191 | 2,141 | 2,072 | 50 | 2.3 | |||||||||||||||

|

Total

(3)

|

32,419 | 26,318 | 22,210 | 6,102 | 23.2 | |||||||||||||||

|

(1)

|

Does not include Consumer Finance.

|

|

(2)

|

Includes credit cards, mortgage finance products and other products.

|

|

(3)

|

Includes small and medium companies with annual gross revenues of up to R$30 million.

|

|

|

·

|

“

Crédito Rural

” and “CPR” (

Cédula de Crédito Rural)

are

products to finance working capital. Basically, CPR is an advanced sale of future production in what essentially amounts to a futures contract. We are the main private bank to offer these products which provide credit based on future revenues and may be used to provide funds to buy agribusiness inputs and to cover storage and sales expenses. Loans are usually secured by mortgages on crops and equipment.

|

|

|

·

|

We act as an agent to lend funds provided by BNDES through government agricultural programs to fund machinery and equipment, fixed assets and permanent plantations such as sugar cane fields, orange groves and coffee plantations.

|

|

|

·

|

We also provide products to fund low carbon agricultural activities in order to stimulate sustainable activities that will increase the share of production with a low environmental impact.

|

|

|

·

|

Global Transaction Banking, which includes cash management, local loans and bank guarantees, trade finance, global custody and securities services and guarantees (both trade and non-trade) and trade services;

|

|

|

·

|

Credit Markets, which includes origination units, distribution of structured credit and debt products, debt capital markets, project finance and asset and capital structuring;

|

|

|

·

|

Corporate Finance, which includes mergers and acquisitions and equity capital markets;

|

|

|

·

|

Equities, which includes equity derivatives, exchange traded derivatives, cash equities and equity research;

|

|

|

·

|

Rates, which offer our customers derivative products, foreign exchange transactions (including for individuals) and other financial products and structures;

|

|

|

·

|

Market Making, which is responsible for the pricing of client deals originated by the sales force from our corporate, institutional, private banking and retail operations; and

|

|

|

·

|

Proprietary Trading, which is responsible for the management of our proprietary books and the establishment of a relevant presence as a leading liquidity provider across all local markets.

|

|

At December 31, 2011

|

||||

|

Branches

|

2,355 | |||

|

PABs (on-site service units)

|

1,420 | |||

|

ATMs

|

18,419 | |||

|

At December 31,

|

Change, At December 31, 2011 vs. December 31, 2010

|

|||||||||||||||||||

|

2011

|

2010

|

2009

|

# |

%

|

||||||||||||||||

|

Central West

|

93 | 86 | 72 | 7 | 8 | |||||||||||||||

|

Northeast

|

196 | 183 | 176 | 13 | 7 | |||||||||||||||

|

North

|

36 | 31 | 31 | 5 | 16 | |||||||||||||||

|

Southeast

|

1,707 | 1,606 | 1,533 | 101 | 6 | |||||||||||||||

|

South

|

323 | 295 | 279 | 28 | 9 | |||||||||||||||

|

Total

|

2,355 | 2,201 | 2,091 | 154 | 7 | |||||||||||||||

|

At December 31,

|

Change, December 31, 2011 vs. December 31, 2010

|

|||||||||||||||||||

|

2011

|

2010

|

2009

|

# |

%

|

||||||||||||||||

|

Central West

|

98 | 100 | 101 | (2 | ) | (2 | ) | |||||||||||||

|

Northeast

|

130 | 159 | 159 | (29 | ) | (18 | ) | |||||||||||||

|

North

|

53 | 59 | 59 | (6 | ) | (10 | ) | |||||||||||||

|

Southeast

|

970 | 1,001 | 1,018 | (31 | ) | (3 | ) | |||||||||||||

|

South

|

169 | 176 | 177 | (7 | ) | (4 | ) | |||||||||||||

|

Total

|

1,420 | 1,495 | 1,514 | (75 | ) | (5 | ) | |||||||||||||

|

At December 31,

|

Change, December 31, 2011 vs. December 31, 2010

|

|||||||||||||||||||

|

2011

|

2010

|

2009

|

# |

%

|

||||||||||||||||

|

Central West

|

759 | 746 | 714 | 13 | 1.7 | |||||||||||||||

|

Northeast

|

1,666 | 1,683 | 1,647 | (17 | ) | (1.0 | ) | |||||||||||||

|

North

|

393 | 398 | 390 | (5 | ) | (1.3 | ) | |||||||||||||

|

Southeast

|

13,406 | 13,407 | 13,336 | (1 | ) | 0.0 | ||||||||||||||

|

South

|

2,195 | 2,078 | 2,041 | 117 | 5.6 | |||||||||||||||

|

Total

|

18,419 | 18,312 | 18,128 | 107 | 0.6 | |||||||||||||||

|

At December 31,

|

Change, December 31, 2011 vs. December 31, 2010

|

|||||||||||||||||||

|

2011

|

2010

|

2009

|

# |

%

|

||||||||||||||||

|

Number of individual customers (in thousands)

|

2,525 | 2,436 | 2,216 | 89 | 3.7 | |||||||||||||||

|

PAS

(1)

|

3,631 | 4,150 | 3,976 | (519 | ) | (12.5 | ) | |||||||||||||

|

Headcount

|

6,588 | 6,882 | 6,516 | (294 | ) | (4.3 | ) | |||||||||||||

|

Percentage of using customers per month

|

27 | % | 29 | % | 27 | % | ||||||||||||||

|

(1)

|

Work stations set up for call center activities.

|

|

At December 31,

|

Change, December 31, 2011 vs. December 31, 2010

|

|||||||||||||||||||

|

2011

|

2010

|

2009

|

# |

%

|

||||||||||||||||

|

Number of individual customers (in thousands)

|

2,448 | 2,025 | 1,790 | 423 | 20.9 | |||||||||||||||

|

Percentage of using customers

|

28 | % | 23 | % | 22 | % | ||||||||||||||

|

|

·

|

consolidation of our operational base;

|

|

|

·

|

leverage our full range of products and services in all business segments;

|

|

|

·

|

strategic repositioning in markets of interest with favorable growth prospects;

|

|

|

·

|

improve our strategic positioning and relationships with clients in other markets; and

|

|

|

·

|

increase our brand value.

|

|

|

·

|

Data Centers

. We currently have data centers in two locations. Our security environment entails an authentication and authorization system based on mainframe infrastructure, a secure internal network protected by a complex set of firewalls, continuous monitoring of incoming traffic and protection of work stations with anti-virus software. We are currently building a latest generation technology, research and data processing center, in the city of Campinas, State of São Paulo.

|

|

|

·

|

Data Communications

. Our data communications infrastructure has been upgraded to provide for faster broadband speeds at all of our branches.

|

|

|

·

|

Call Centers

. In addition to customer service, our call centers perform recovery and sales activities.

|

|

|

·

|

Branches/ATMs

. The integration of our retail operations was implemented in two steps. The first step, completed in February 2011, was the full integration of all clients and channels excluding cash management operations. The second step was the integration of cash management operations, which was completed in March 2011. In 2012, we expect to open 100 to 120 new branches and we expect to replace 4,000 ATMs (more than 20% of our total ATMs).

|

|

|

·

|

End-user systems

. We maintained the end-user systems, with the goal of standardizing hardware and operating systems at all workstations for all employees.

|

|

|

·

|

to contribute towards developing the future professional citizen giving the student, through practice in the community, the opportunity to work systematically with the knowledge acquired at the university;

|

|

|

·

|

to make the knowledge of the institution of higher education available to low-income communities , contributing towards improving their living conditions; and

|

|

|

·

|

to support university extension courses, encouraging knowledge sharing and integration into the community.

|

|

At December 31,

|

||||||||||||||||||||||||||||||||||||

|

2011

|

2010

|

2009

|

||||||||||||||||||||||||||||||||||

|

Average Balance

|

Interest

|

Average Rate

|

Average Balance

|

Interest

|

Average Rate

|

Average Balance

|

Interest

|

Average Rate

|

||||||||||||||||||||||||||||

|

(in millions of R$, except percentages)

|

||||||||||||||||||||||||||||||||||||

|

Assets and Interest Income

|

||||||||||||||||||||||||||||||||||||

|

Cash and balances with the Brazilian Central Bank

|

55,100 | 6,297 | 11.4 | % | 37,421 | 3,590 | 9.6 | % | 17,879 | 1,667 | 9.3 | % | ||||||||||||||||||||||||

|

Loans and amounts due from credit institutions

|

19,017 | 1,219 | 6.4 | % | 22,815 | 1,398 | 6.1 | % | 31,122 | 2,901 | 9.3 | % | ||||||||||||||||||||||||

|

Loans and advances to customers

|

163,046 | 35,398 | 21.7 | % | 137,046 | 29,290 | 21.4 | % | 126,712 | 29,470 | 23.3 | % | ||||||||||||||||||||||||

|

Debt instruments

|

68,770 | 8,084 | 11.8 | % | 57,830 | 6,442 | 11.1 | % | 45,530 | 5,202 | 11.4 | % | ||||||||||||||||||||||||

|

Other interest-earning assets

|

– | 738 | – | – | 189 | – | – | 103 | – | |||||||||||||||||||||||||||

|

Total interest-earning assets

|

305,934 | 51,736 | 16.9 | % | 255,112 | 40,909 | 16.0 | % | 221,243 | 39,343 | 17.8 | % | ||||||||||||||||||||||||

|

Equity instruments

|

17,324 | 94 | 0.5 | % | 19,684 | 52 | 0.3 | % | 7,746 | 30 | 0.4 | % | ||||||||||||||||||||||||

|

Investments in associates

|

402 | – | – | 421 | – | – | 506 | – | – | |||||||||||||||||||||||||||

|

Total earning assets

|

323,660 | 51,830 | 16.0 | % | 275,217 | 40,961 | 14.9 | % | 229,495 | 39,373 | 17.2 | % | ||||||||||||||||||||||||

|

At December 31,

|

||||||||||||||||||||||||||||||||||||

|

2011

|

2010

|

2009

|

||||||||||||||||||||||||||||||||||

|

Average Balance

|

Interest

|

Average Rate

|

Average Balance

|

Interest

|

Average Rate

|

Average Balance

|

Interest

|

Average Rate

|

||||||||||||||||||||||||||||

|

(in millions of R$, except percentages)

|

||||||||||||||||||||||||||||||||||||

|

Cash and balances with the Brazilian Central Bank

|

6,830 | – | – | 6,549 | – | – | 6,250 | – | – | |||||||||||||||||||||||||||

|

Loans and amounts due from credit institutions

|

3,082 | – | – | 1,064 | – | – | 3,152 | – | – | |||||||||||||||||||||||||||

|

Impairment losses

|

(10,359 | ) | – | – | (9,119 | ) | – | – | (8,765 | ) | – | – | ||||||||||||||||||||||||

|

Other assets

|

35,089 | – | – | 31,889 | – | – | 33,007 | – | – | |||||||||||||||||||||||||||

|

Tangible assets

|

4,647 | – | – | 4,025 | – | – | 3,690 | – | – | |||||||||||||||||||||||||||

|

Intangible assets

|

31,772 | – | – | 31,660 | – | – | 31,345 | – | – | |||||||||||||||||||||||||||

|

Total average assets

|

394,722 | 51,830 | 13.1 | % | 341,285 | 40,961 | 12.0 | % | 298,174 | 39,373 | 13.2 | % | ||||||||||||||||||||||||

|

Liabilities and Interest Expense

|

||||||||||||||||||||||||||||||||||||

|

Deposits from the Brazilian Central Bank and Deposits from credit institutions

|

41,670 | 2,006 | 4.8 | % | 35,274 | 1,147 | 3.3 | % | 22,319 | 1,208 | 5.4 | % | ||||||||||||||||||||||||

|

Customer deposits

|

161,159 | 16,494 | 10.2 | % | 139,825 | 12,774 | 9.1 | % | 139,917 | 13,164 | 9.4 | % | ||||||||||||||||||||||||

|

Marketable debt securities

|

31,330 | 3,227 | 10.3 | % | 13,404 | 1,213 | 9.0 | % | 11,420 | 1,048 | 9.2 | % | ||||||||||||||||||||||||

|

Subordinated liabilities

|

10,288 | 1,213 | 11.8 | % | 9,953 | 999 | 10.0 | % | 10,676 | 1,077 | 10.1 | % | ||||||||||||||||||||||||

|

Other interest-bearing liabilities

|

– | 893 | – | – | 682 | – | – | 679 | – | |||||||||||||||||||||||||||

|

Total interest-bearing liabilities

|

244,446 | 23,834 | 9.8 | % | 198,456 | 16,815 | 8.5 | % | 184,332 | 17,176 | 9.3 | % | ||||||||||||||||||||||||

|

Deposits from credit institutions

|

321 | – | – | 196 | – | – | 100 | – | – | |||||||||||||||||||||||||||

|

Customer deposits – demand deposits

|

13,648 | – | – | 14,287 | – | – | 13,000 | – | – | |||||||||||||||||||||||||||

|

Other liabilities

|

60,579 | – | – | 56,467 | – | – | 44,546 | – | – | |||||||||||||||||||||||||||

|

Non-controlling interests

|

11 | – | – | 4 | – | – | 4 | – | – | |||||||||||||||||||||||||||

|

Equity

|

75,716 | – | – | 71,875 | – | – | 56,192 | – | – | |||||||||||||||||||||||||||

|

Total average liabilities and equity

|

394,722 | 23,834 | 6.0 | % | 341,285 | 16,815 | 4.9 | % | 298,174 | 17,176 | 5.8 | % | ||||||||||||||||||||||||

|

For the years ended 2011/2010

|

For the years ended 2010/2009

|

|||||||||||||||||||||||

|

Increase (decrease) due to changes in

|

||||||||||||||||||||||||

|

Volume

|

Rate

|

Net change

|

Volume

|

Rate

|

Net change

|

|||||||||||||||||||

|

Interest and Similar Income

|

(In millions of R$)

|

|||||||||||||||||||||||

|

Interest-earning assets

|

||||||||||||||||||||||||

|

Cash and balances with the Brazilian Central Bank

|

1,927 | 781 | 2,708 | 1,873 | 50 | 1,923 | ||||||||||||||||||

|

Loans and amounts due from credit institutions

|

(241 | ) | 63 | (179 | ) | (658 | ) | (845 | ) | (1,503 | ) | |||||||||||||

|

Loans and advances to customers

|

5,638 | 470 | 6,108 | 2,306 | (2,485 | ) | (179 | ) | ||||||||||||||||

|

Debt instruments

|

1,271 | 371 | 1,642 | 1,373 | (133 | ) | 1,240 | |||||||||||||||||

|

Other interest-earning assets

|

549 | – | 549 | 86 | – | 86 | ||||||||||||||||||

|

Total interest-earning assets

|

9,143 | 1,684 | 10,827 | 4,980 | (3,413 | ) | 1,567 | |||||||||||||||||

|

Investments in associates

|

(7 | ) | 49 | 42 | 34 | (12 | ) | 22 | ||||||||||||||||

|

Total earning assets

|

9,136 | 1,733 | 10,869 | 5,014 | (3,425 | ) | 1,589 | |||||||||||||||||

|

For the years ended 2011/2010

|

For the years ended 2010/2009

|

|||||||||||||||||||||||

|

Increase (decrease) due to changes in

|

||||||||||||||||||||||||

|

Volume

|

Rate

|

Net change

|

Volume

|

Rate

|

Net change

|

|||||||||||||||||||

|

(in millions of R$)

|

||||||||||||||||||||||||

|

Interest Expense and Similar Charges

|

||||||||||||||||||||||||

|

Interest-bearing liabilities

|

||||||||||||||||||||||||

|

Deposits from the Brazilian Central Bank and Deposits from credit institutions

|

238 | 622 | 859 | 563 | (624 | ) | (61 | ) | ||||||||||||||||

|

Customer deposits

|

2,080 | 1,641 | 3,721 | (9 | ) | (382 | ) | (391 | ) | |||||||||||||||

|

Marketable debt securities

|

1,825 | 189 | 2,014 | 180 | (14 | ) | 166 | |||||||||||||||||

|

Subordinated liabilities

|

35 | 179 | 214 | (73 | ) | (4 | ) | (77 | ) | |||||||||||||||

|

Other interest-bearing liabilities

|

212 | – | 212 | 1 | – | 1 | ||||||||||||||||||

|

Total interest-bearing liabilities

|

4,390 | 2,631 | 7,020 | 662 | (1,024 | ) | (362 | ) | ||||||||||||||||

|

For the year ended December 31,

|

||||||||||||

|

2011

|

2010

|

2009

|

||||||||||

|

(in millions of R$, except percentages)

|

||||||||||||

|

Average earning assets

|

323,660 | 275,217 | 229,495 | |||||||||

|

Interest and dividends on equity securities

(1)

|

51,830 | 40,961 | 39,373 | |||||||||

|

Net interest income

|

27,902 | 24,095 | 22,167 | |||||||||

|

Gross yield

(2)

|

16.0 | % | 14.9 | % | 17.2 | % | ||||||

|

Net yield

(3)

|

8.6 | % | 8.8 | % | 9.7 | % | ||||||

|

Yield spread

(4)

|

6.3 | % | 6.4 | % | 7.8 | % | ||||||

|

(1)

|

Dividends on equity securities include dividends from companies accounted for by the equity method.

|

|

(2)

|

Gross yield is the quotient of interest and dividends on equity securities divided by average earning assets.

|

|

(3)

|

Net yield is the quotient of net interest income divided by average earning assets.

|

|

(4)

|

Yield spread is the difference between gross yield on earning assets and the average cost of interest-bearing liabilities.

|

|

For the year ended December 31,

|

||||||||||||

|

2011

|

2010

|

2009

|

||||||||||

|

ROA: Return on average total assets

|

2.0 | % | 2.2 | % | 1.8 | % | ||||||

|

ROE: Return on average shareholders’ equity

|

10.2 | % | 10.3 | % | 9.8 | % | ||||||

|

Average shareholders’ equity as a percentage of average total assets

|

19.2 | % | 21.1 | % | 18.8 | % | ||||||

|

Payout

(1)

|

41.0 | % | 47.9 | % | 26.8 | % | ||||||

|

(1)

|

Divided payout ratio (dividends declared per share divided by net income per share).

|

|

For the year ended December 31,

|

||||||||||||

|

2011

|

2010

|

2009

|

||||||||||

|

Cash and balances with the Brazilian Central Bank

|

18.0 | % | 14.7 | % | 8.1 | % | ||||||

|

Loans and amounts due from credit institutions

|

6.2 | % | 8.9 | % | 14.1 | % | ||||||

|

Loans and advances to customers

|

53.3 | % | 53.7 | % | 57.2 | % | ||||||

|

Debt instruments

|

22.5 | % | 22.7 | % | 20.6 | % | ||||||

|

Total interest-earning assets

|

100.0 | % | 100.0 | % | 100.0 | % | ||||||

|

At December 31,

|

||||||||||||

|

2011

|

2010

|

2009

|

||||||||||

|

(in millions of R$)

|

||||||||||||

|

Time deposits

|

7,136 | 9,110 | 9,945 | |||||||||

|

Reverse repurchase agreements

|

1,040 | 600 | 6,160 | |||||||||

|

Escrow deposits

|

6,869 | 7,317 | 6,192 | |||||||||

|

Cash and Foreign currency investments

|

4,247 | 5,827 | 3,493 | |||||||||

|

Other accounts

|

459 | 144 | 412 | |||||||||

|

Total

|

19,751 | 22,998 | 26,202 | |||||||||

|

At December 31,

|

||||||||||||

|

2011

|

2010

|

2009

|

||||||||||

|

(in millions of R$)

|

||||||||||||

|

Debt securities

|

||||||||||||

|

Government securities—Brazil

|

56,833 | 55,444 | 53,620 | |||||||||

|

Government securities—other countries

|

– | 379 | 366 | |||||||||

|

Other debt securities

|

12,058 | 6,433 | 3,554 | |||||||||

|

Total domestic

|

68,891 | 62,256 | 57,540 | |||||||||

|

Less-allowance for credit losses

|

– | – | (30 | ) | ||||||||

|

Total debt securities

|

68,891 | 62,256 | 57,510 | |||||||||

|

Equity securities

|

||||||||||||

|

Shares of Brazilian companies

|

1,002 | 1,153 | 1,471 | |||||||||

|

Shares of foreign companies

|

1 | 1 | 68 | |||||||||

|

Investment fund units and shares

(1)

|

1,128 | 21,282 | 16,453 | |||||||||

|

Total equity securities

|

2,131 | 22,436 | 17,992 | |||||||||

|

Total investment securities

|

71,022 | 84,692 | 75,502 | |||||||||

|

(1)

|

In 2010 and 2009, includes Investment fund units Guarantors of Benefit Plans—PGBL/VGBL, related to the liabilities for insurance contracts. For further details see Note 3a to our audited consolidated financial statements.

|

|

At December 31, 2011

|

||||||||||||||||||||||||

|

Maturing within 1 year

|

Maturing between 1 and 5 years

|

Maturing between 5 and 10 years

|

Maturing after 10 years

|

Total

|

Average Yield

|

|||||||||||||||||||

|

(in millions of R$)

|

||||||||||||||||||||||||

|

Debt Securities

|

||||||||||||||||||||||||

|

Government securities—Brazil

|

10,196 | 35,009 | 9,041 | 2,587 | 56,833 | 11.7 | % | |||||||||||||||||

|

Other debt securities

|

4,080 | 3,347 | 4,615 | 16 | 12,058 | 11.8 | % | |||||||||||||||||

|

Total debt investment securities

|

14,276 | 38,356 | 13,656 | 2,603 | 68,891 | 11.0 | % | |||||||||||||||||

|

At December 31,

|

||||||||||||||||||||

|

2011

|

2010

|

2009

|

2008

|

2007

|

||||||||||||||||

|

(in millions of R$)

|

||||||||||||||||||||

|

Commercial, financial and industrial

(1)

|

94,922 | 78,101 | 66,601 | 76,407 | 32,879 | |||||||||||||||

|

Real estate-construction

(2)

|

6,280 | 5,392 | 3,828 | 2,469 | 301 | |||||||||||||||

|

Real estate-mortgage

(3)

|

10,018 | 6,698 | 5,226 | 4,472 | 1,692 | |||||||||||||||

|

Installment loans to individuals

(4)

|

76,459 | 60,251 | 49,103 | 46,857 | 16,178 | |||||||||||||||

|

Lease financing

(5)

|

6,506 | 10,116 | 13,636 | 12,444 | 402 | |||||||||||||||

|

Loans and advances to customers, gross

(6)

|

194,184 | 160,558 | 138,394 | 142,649 | 51,452 | |||||||||||||||

|

Impairment losses

|

(11,118 | ) | (9,192 | ) | (10,070 | ) | (8,181 | ) | (2,249 | ) | ||||||||||

|

Loans and advances to customers, net

|

183,066 | 151,366 | 128,324 | 134,468 | 49,203 | |||||||||||||||

|

(1)

|

Includes primarily loans to small and medium-size businesses, or SMEs in our Commercial Banking segment, and to Global Banking & Markets, or GB&M, corporate and business enterprise customers in our Wholesale Global Banking segment. The principal products offered to SMEs in this category include revolving loans, overdraft facilities, installment loans, working capital and equipment finance loans. Credit approval for SMEs is based on customer income, business activity, collateral coverage and internal and external credit scoring tools. Collateral on commercial, financial and industrial lending to SMEs generally includes receivables, liens, pledges, guarantees and mortgages, with coverage generally ranging from 100% to 150% of the loan value depending on the risk profile of the loan. Our Wholesale Global Banking customers are offered a range of loan products ranging from typical corporate banking products (installment loans, working capital and equipment finance loans) to more sophisticated products (derivative and capital markets transactions). As Wholesale Global Banking customers tend to be larger businesses, credit approval is based on customer credit quality as evaluated by a specialized teams of risk analysts taking account of, among other things, business revenues and credit history of each customer. Underwriting policies for this category of loans to our Wholesale Global Banking customers are focused on the type of guarantee or collateral provided. Certain loans (BNDES products) are generally secured by liens on financed machinery and equipment, though guarantees may also be provided as additional security.

|

|

(2)

|

Includes construction loans made principally to real estate developers that are SMEs and corporate customers in our Wholesale Global Banking Segment. Credit approval is carried out by a specialized team of risk analysts which follows a specific set of underwriting standards and analysis of each customer based on, among other things, business revenues and credit history. Loans in this category are generally secured by mortgages and receivables, though guarantees may also be provided as additional security.

|

|

(3)

|

Includes loans on residential real estate to individuals. Credit approval policies in this category are determined by reference to the type of lending product being offered, the type and location of the real estate, the revenue or income of the business or customer, respectively, requesting the loan and internal and external credit scoring information. All loans granted under this category are secured by the financed real estate. Loan-to-value ratios for loans in this category are generally limited to 80% and the average loan to value ratio for new loans is approximately between 50% and 60%.

|

|

(4)

|

Consists primarily of unsecured personal installment loans (including loans the payments for which are automatically deducted from a customer’s payroll), revolving loans, overdraft facilities, consumer finance

|

|

(5)

|

Includes primarily automobile leases and loans to individuals. Credit approval is based both on an automatic scoring model using external credit scores and on evaluation by our branch personnel following our risk management policies. The vehicle financed acts as collateral for the particular loan granted.

|

|

(6)

|

Includes the debit balances (financial assets) of all the credit and loans granted by us, including money market operations through central counterparties, except for credit of any nature in the name of credit institutions or those represented by securities.

|

|

Maturity

|

||||||||||||||||||||||||||||||||

|

Less than one year

|

One to five years

|

Over five years

|

Total

|

|||||||||||||||||||||||||||||

|

Balance

|

% of Total

|

Balance

|

% of Total

|

Balance

|

% of Total

|

Balance

|

% of Total

|

|||||||||||||||||||||||||

|

(in millions of R$, except percentages)

|

||||||||||||||||||||||||||||||||

|

Commercial, financial and industrial

|

58,952 | 51.5 | % | 32,901 | 46.1 | % | 3,069 | 36.9 | % | 94,922 | 48.9 | % | ||||||||||||||||||||

|

Real estate

|

5,683 | 5.0 | % | 6,036 | 8.5 | % | 4,579 | 55.1 | % | 16,298 | 8.4 | % | ||||||||||||||||||||

|

Installment loans to individuals

|

46,200 | 40.4 | % | 29,600 | 41.4 | % | 658 | 8.0 | % | 76,459 | 39.4 | % | ||||||||||||||||||||

|

Lease financing

|

3,614 | 3.1 | % | 2,890 | 4.0 | % | 3 | 0.0 | % | 6,506 | 3.3 | % | ||||||||||||||||||||

|

Loans and advances to customers, gross

|

114,449 | 100.0 | % | 71,427 | 100.0 | % | 8,308 | 100 | % | 194,184 | 100.0 | % | ||||||||||||||||||||

|

Fixed and variable rate loans having a maturity of more than one year

|

||||

|

(in millions of R$)

|

||||

|

Fixed rate

|

50,824 | |||

|

Variable rate

|

28,912 | |||

|

Total

|

79,736 | |||

|

At December 31,

|

||||||||||||||||||||||||

|

2011

|

2010

|

2009

|

||||||||||||||||||||||

|

Balance

|

% of Total Assets

|

Balance

|

% of Total Assets

|

Balance

|

% of Total Assets

|

|||||||||||||||||||

|

(in millions of R$, except percentages)

|

||||||||||||||||||||||||

|

OECD countries

(1)

|

||||||||||||||||||||||||

|

Austria

|

366 | 0.1 | % | 379 | 0.1 | % | 571 | 0.2 | % | |||||||||||||||

|

Spain

|

256 | 0.1 | % | 954 | 0.3 | % | 1,289 | 0.4 | % | |||||||||||||||

|

United States

|

8,305 | 2.1 | % | 1,630 | 0.4 | % | 2,383 | 0.8 | % | |||||||||||||||

|

Netherlands

|

5,675 | 1.4 | % | 3,825 | 1.0 | % | – | – | ||||||||||||||||

|

Other OECD countries

(2)

|

583 | 0.1 | % | 227 | 0.1 | % | 673 | 0.2 | % | |||||||||||||||

|

Total OECD

|

15,186 | 3.8 | % | 7,015 | 1.9 | % | 4,916 | 1.6 | % | |||||||||||||||

|

Non-OECD countries

|

||||||||||||||||||||||||

|

Latin American countries

(2)

|

60 | – | 66 | – | 79 | – | ||||||||||||||||||

|

Cayman Islands

|

4,081 | 1.0 | % | 4,175 | 1.1 | % | 3,615 | 1.1 | % | |||||||||||||||

|

Other

(2)

|

354 | 0.1 | % | 135 | – | 258 | 0.1 | % | ||||||||||||||||

|

Total non-OECD

|

4,495 | 1.1 | % | 4,376 | 1.2 | % | 3,952 | 1.2 | % | |||||||||||||||

|

Total

|

19,681 | 4.9 | % | 11,391 | 3.0 | % | 8,868 | 2.8 | % | |||||||||||||||

|

(1)

|

The Organization for Economic Cooperation and Development.

|

|

(2)

|

Aggregate outstandings in any single country in this category do not exceed 0.75% of our total assets.

|

|

Government

|

Banks and Other Financial Institutions

|

Commercial and Industrial

|

Other Loans

|

Total

|

||||||||||||||||

|

(in millions of R$)

|

||||||||||||||||||||

|

2009

|

||||||||||||||||||||

|

United States