|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

WASHINGTON, D.C. 20549

FORM 10-Q

|

☒ |

QUARTERLY REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

FOR THE QUARTERLY PERIOD ENDED SEPTEMBER 30, 2019

OR

|

☐ |

TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

FOR THE TRANSITION PERIOD FROM TO

Commission File Number: 000-55931

Blackstone Real Estate Income Trust, Inc.

(Exact name of Registrant as specified in its charter)

|

|

|

|

Maryland |

81-0696966 |

|

(State or other jurisdiction of incorporation or organization) 345 Park Avenue New York, NY (Address of principal executive offices) |

(I.R.S. Employer Identification No.)

10154 (Zip Code) |

Registrant’s telephone number, including area code: (212) 583-5000

Securities registered pursuant to Section 12(b) of the Act: None

|

Title of each class |

|

Trading Symbol(s) |

|

Name of each exchange on which registered |

|

|

|

|

|

|

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes ☒ No ☐

Indicate by check mark whether the registrant has submitted electronically every Interactive Data File required to be submitted pursuant to Rule 405 of Regulation S-T (§232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit such files). Yes ☒ No ☐

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, smaller reporting company, or an emerging growth company. See the definitions of “large accelerated filer,” “accelerated filer,” “smaller reporting company,” and “emerging growth company” in Rule 12b-2 of the Exchange Act.

|

Large accelerated filer |

|

☐ |

|

Accelerated filer |

|

☐ |

|

|

|

|

|

|||

|

Non-accelerated filer |

|

☒ |

|

Smaller reporting company |

|

☐ |

|

|

|

|

|

|

|

|

|

Emerging growth company |

|

☒ |

|

|

|

|

If an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided pursuant to Section 13(a) of the Exchange Act. Yes ☒ No ☐

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act). Yes ☐ No ☒

As of November 14, 2019, the issuer had the following shares outstanding: 499,191,747 shares of Class S common stock, 38,735,254 shares of Class T common stock, 78,041,510 shares of Class D common stock, and 408,084,624 shares of Class I common stock.

|

PART I. |

1 |

|

|

|

|

|

|

ITEM 1. |

1 |

|

|

|

|

|

|

|

Condensed Consolidated Financial Statements (Unaudited): |

|

|

|

|

|

|

|

Condensed Consolidated Balance Sheets as of September 30, 2019 and December 31, 2018 |

1 |

|

|

|

|

|

|

2 |

|

|

|

|

|

|

|

3 |

|

|

|

|

|

|

|

5 |

|

|

|

|

|

|

|

7 |

|

|

|

|

|

|

ITEM 2. |

MANAGEMENT’S DISCUSSION AND ANALYSIS OF FINANCIAL CONDITION AND RESULTS OF OPERATIONS |

30 |

|

|

|

|

|

ITEM 3. |

52 |

|

|

|

|

|

|

ITEM 4. |

52 |

|

|

|

|

|

|

PART II. |

53 |

|

|

|

|

|

|

ITEM 1. |

53 |

|

|

|

|

|

|

ITEM 1A. |

53 |

|

|

|

|

|

|

ITEM 2. |

54 |

|

|

|

|

|

|

ITEM 3. |

55 |

|

|

|

|

|

|

ITEM 4. |

55 |

|

|

|

|

|

|

ITEM 5. |

55 |

|

|

|

|

|

|

ITEM 6. |

56 |

|

|

|

|

|

|

57 |

||

PART I. FINANCIA L INFORMATION

Blackstone Real Estate Income Trust, Inc.

Condensed Consolidated Balance Sheets (Unaudited)

(in thousands, except share and per share data)

|

|

|

September 30, 2019 |

|

|

December 31, 2018 |

|

||

|

Assets |

|

|

|

|

|

|

|

|

|

Investments in real estate, net |

|

$ |

20,744,467 |

|

|

$ |

10,259,687 |

|

|

Investments in real estate-related securities and loans |

|

|

3,804,309 |

|

|

|

2,259,913 |

|

|

Cash and cash equivalents |

|

|

155,674 |

|

|

|

68,089 |

|

|

Restricted cash |

|

|

666,891 |

|

|

|

238,524 |

|

|

Other assets |

|

|

926,015 |

|

|

|

410,945 |

|

|

Total assets |

|

$ |

26,297,356 |

|

|

$ |

13,237,158 |

|

|

|

|

|

|

|

|

|

|

|

|

Liabilities and Equity |

|

|

|

|

|

|

|

|

|

Mortgage notes, term loans, and secured revolving credit facilities, net |

|

$ |

13,250,539 |

|

|

$ |

6,833,269 |

|

|

Repurchase agreements |

|

|

2,646,334 |

|

|

|

1,713,723 |

|

|

Unsecured revolving credit facilities |

|

|

— |

|

|

|

— |

|

|

Due to affiliates |

|

|

532,160 |

|

|

|

301,581 |

|

|

Accounts payable, accrued expenses, and other liabilities |

|

|

1,455,675 |

|

|

|

464,398 |

|

|

Total liabilities |

|

|

17,884,708 |

|

|

|

9,312,971 |

|

|

|

|

|

|

|

|

|

|

|

|

Commitments and contingencies |

|

|

— |

|

|

|

— |

|

|

Redeemable non-controlling interests |

|

|

8,996 |

|

|

|

9,233 |

|

|

|

|

|

|

|

|

|

|

|

|

Equity |

|

|

|

|

|

|

|

|

|

Preferred stock, $0.01 par value per share, 100,000,000 shares authorized; no shares issued and outstanding as of September 30, 2019 and December 31, 2018 |

|

|

— |

|

|

|

— |

|

|

Common stock — Class S shares, $0.01 par value per share, 1,000,000,000 shares authorized; 446,424,565 and 276,989,019 shares issued and outstanding as of September 30, 2019 and December 31, 2018, respectively |

|

|

4,464 |

|

|

|

2,770 |

|

|

Common stock — Class T shares, $0.01 par value per share, 500,000,000 shares authorized; 36,559,269 and 23,313,429 shares issued and outstanding as of September 30, 2019 and December 31, 2018, respectively |

|

|

366 |

|

|

|

233 |

|

|

Common stock — Class D shares, $0.01 par value per share, 500,000,000 shares authorized; 69,148,152 and 30,375,353 shares issued and outstanding as of September 30, 2019 and December 31, 2018, respectively |

|

|

691 |

|

|

|

304 |

|

|

Common stock — Class I shares, $0.01 par value per share, 1,000,000,000 shares authorized; 352,999,381 and 108,261,331 shares issued and outstanding as of September 30, 2019 and December 31, 2018, respectively |

|

|

3,530 |

|

|

|

1,083 |

|

|

Additional paid-in capital |

|

|

9,262,304 |

|

|

|

4,327,444 |

|

|

Accumulated deficit and cumulative distributions |

|

|

(1,087,923 |

) |

|

|

(587,548 |

) |

|

Total stockholders' equity |

|

|

8,183,432 |

|

|

|

3,744,286 |

|

|

Non-controlling interests attributable to third party joint ventures |

|

|

92,073 |

|

|

|

75,592 |

|

|

Non-controlling interests attributable to BREIT OP unitholders |

|

|

128,147 |

|

|

|

95,076 |

|

|

Total equity |

|

|

8,403,652 |

|

|

|

3,914,954 |

|

|

Total liabilities and equity |

|

$ |

26,297,356 |

|

|

$ |

13,237,158 |

|

See accompanying notes to condensed consolidated financial statements.

1

Blackstone Real Estate Income Trust, Inc.

Condensed Consolidated Statements of Operations (Unaudited)

(in thousands, except share and per share data)

|

|

Three Months Ended September 30, |

|

|

Nine Months Ended September 30, |

|

||||||||||

|

|

2019 |

|

|

2018 |

|

|

2019 |

|

|

2018 |

|

||||

|

Revenues |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Rental revenue |

$ |

290,453 |

|

|

$ |

152,838 |

|

|

$ |

750,322 |

|

|

$ |

366,213 |

|

|

Hotel revenue |

|

132,036 |

|

|

|

40,000 |

|

|

|

301,653 |

|

|

|

79,017 |

|

|

Other revenue |

|

15,544 |

|

|

|

7,324 |

|

|

|

37,457 |

|

|

|

16,842 |

|

|

Total revenues |

|

438,033 |

|

|

|

200,162 |

|

|

|

1,089,432 |

|

|

|

462,072 |

|

|

Expenses |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Rental property operating |

|

121,591 |

|

|

|

63,783 |

|

|

|

310,613 |

|

|

|

153,853 |

|

|

Hotel operating |

|

89,951 |

|

|

|

26,822 |

|

|

|

204,468 |

|

|

|

51,958 |

|

|

General and administrative |

|

4,548 |

|

|

|

3,027 |

|

|

|

12,607 |

|

|

|

7,973 |

|

|

Management fee |

|

29,858 |

|

|

|

11,823 |

|

|

|

69,522 |

|

|

|

28,073 |

|

|

Performance participation allocation |

|

56,322 |

|

|

|

12,447 |

|

|

|

106,383 |

|

|

|

29,796 |

|

|

Depreciation and amortization |

|

204,653 |

|

|

|

103,758 |

|

|

|

505,986 |

|

|

|

262,708 |

|

|

Total expenses |

|

506,923 |

|

|

|

221,660 |

|

|

|

1,209,579 |

|

|

|

534,361 |

|

|

Other income (expense) |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Income from real estate-related securities and loans |

|

52,568 |

|

|

|

28,647 |

|

|

|

166,035 |

|

|

|

59,279 |

|

|

Gain on disposition of real estate |

|

6,481 |

|

|

|

— |

|

|

|

36,167 |

|

|

|

— |

|

|

Interest income |

|

1,763 |

|

|

|

82 |

|

|

|

2,260 |

|

|

|

280 |

|

|

Interest expense |

|

(116,037 |

) |

|

|

(65,711 |

) |

|

|

(310,903 |

) |

|

|

(146,943 |

) |

|

Other income (expense) |

|

(2,379 |

) |

|

|

(283 |

) |

|

|

(2,786 |

) |

|

|

(672 |

) |

|

Total other income (expense) |

|

(57,604 |

) |

|

|

(37,265 |

) |

|

|

(109,227 |

) |

|

|

(88,056 |

) |

|

Net loss |

$ |

(126,494 |

) |

|

$ |

(58,763 |

) |

|

$ |

(229,374 |

) |

|

$ |

(160,345 |

) |

|

Net loss attributable to non-controlling interests in third party joint ventures |

$ |

1,305 |

|

|

$ |

433 |

|

|

$ |

4,311 |

|

|

$ |

3,054 |

|

|

Net loss attributable to non-controlling interests in BREIT OP |

|

2,018 |

|

|

|

663 |

|

|

|

4,342 |

|

|

|

1,594 |

|

|

Net loss attributable to BREIT stockholders |

$ |

(123,171 |

) |

|

$ |

(57,667 |

) |

|

$ |

(220,721 |

) |

|

$ |

(155,697 |

) |

|

Net loss per share of common stock — basic and diluted |

$ |

(0.15 |

) |

|

$ |

(0.17 |

) |

|

$ |

(0.34 |

) |

|

$ |

(0.57 |

) |

|

Weighted-average shares of common stock outstanding, basic and diluted |

|

819,055,389 |

|

|

|

342,351,542 |

|

|

|

647,729,961 |

|

|

|

274,226,898 |

|

See accompanying notes to condensed consolidated financial statements.

2

Blackstone Real Estate Income Trust, Inc.

Condensed Consolidated Statements of Changes in Equity (Unaudited)

(in thousands, except per share data)

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Non- |

|

|

Non- |

|

|

|

|

|

||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

controlling |

|

|

controlling |

|

|

|

|

|

||

|

|

|

Par Value |

|

|

|

|

|

|

Accumulated |

|

|

|

|

|

|

Interests |

|

|

Interests |

|

|

|

|

|

||||||||||||||||

|

|

|

Common |

|

|

Common |

|

|

Common |

|

|

Common |

|

|

Additional |

|

|

Deficit and |

|

|

Total |

|

|

Attributable |

|

|

Attributable |

|

|

|

|

|

|||||||||

|

|

|

Stock |

|

|

Stock |

|

|

Stock |

|

|

Stock |

|

|

Paid-in |

|

|

Cumulative |

|

|

Stockholders' |

|

|

to Third Party |

|

|

to BREIT OP |

|

|

Total |

|

||||||||||

|

|

|

Class S |

|

|

Class T |

|

|

Class D |

|

|

Class I |

|

|

Capital |

|

|

Distributions |

|

|

Equity |

|

|

Joint Ventures |

|

|

Unitholders |

|

|

Equity |

|

||||||||||

|

Balance at June 30, 2019 |

|

$ |

3,812 |

|

|

$ |

319 |

|

|

$ |

529 |

|

|

$ |

2,286 |

|

|

$ |

6,969,300 |

|

|

$ |

(845,511 |

) |

|

$ |

6,130,735 |

|

|

$ |

113,725 |

|

|

$ |

131,915 |

|

|

$ |

6,376,375 |

|

|

Common stock issued |

|

|

638 |

|

|

|

45 |

|

|

|

160 |

|

|

|

1,251 |

|

|

|

2,342,048 |

|

|

|

— |

|

|

|

2,344,142 |

|

|

|

— |

|

|

|

— |

|

|

|

2,344,142 |

|

|

Offering costs |

|

|

— |

|

|

|

— |

|

|

|

— |

|

|

|

— |

|

|

|

(59,354 |

) |

|

|

— |

|

|

|

(59,354 |

) |

|

|

— |

|

|

|

— |

|

|

|

(59,354 |

) |

|

Distribution reinvestment |

|

|

32 |

|

|

|

3 |

|

|

|

4 |

|

|

|

21 |

|

|

|

67,817 |

|

|

|

— |

|

|

|

67,877 |

|

|

|

— |

|

|

|

— |

|

|

|

67,877 |

|

|

Common stock/units repurchased |

|

|

(18 |

) |

|

|

(1 |

) |

|

|

(2 |

) |

|

|

(29 |

) |

|

|

(55,172 |

) |

|

|

— |

|

|

|

(55,222 |

) |

|

|

— |

|

|

|

(648 |

) |

|

|

(55,870 |

) |

|

Amortization of compensation awards |

|

|

— |

|

|

|

— |

|

|

|

— |

|

|

|

1 |

|

|

|

99 |

|

|

|

— |

|

|

|

100 |

|

|

|

— |

|

|

|

500 |

|

|

|

600 |

|

|

Net loss ($732 allocated to redeemable non-controlling interests) |

|

|

— |

|

|

|

— |

|

|

|

— |

|

|

|

— |

|

|

|

— |

|

|

|

(123,171 |

) |

|

|

(123,171 |

) |

|

|

(625 |

) |

|

|

(1,966 |

) |

|

|

(125,762 |

) |

|

Distributions declared on common stock ($0.1594 gross per share) |

|

|

— |

|

|

|

— |

|

|

|

— |

|

|

|

— |

|

|

|

— |

|

|

|

(119,241 |

) |

|

|

(119,241 |

) |

|

|

— |

|

|

|

— |

|

|

|

(119,241 |

) |

|

Contributions from non-controlling interests |

|

|

— |

|

|

|

— |

|

|

|

— |

|

|

|

— |

|

|

|

— |

|

|

|

— |

|

|

|

— |

|

|

|

1,995 |

|

|

|

425 |

|

|

|

2,420 |

|

|

Distributions to non-controlling interests |

|

|

— |

|

|

|

— |

|

|

|

— |

|

|

|

— |

|

|

|

— |

|

|

|

— |

|

|

|

— |

|

|

|

(23,022 |

) |

|

|

(2,079 |

) |

|

|

(25,101 |

) |

|

Allocation to redeemable non-controlling interests |

|

|

— |

|

|

|

— |

|

|

|

— |

|

|

|

— |

|

|

|

(2,434 |

) |

|

|

— |

|

|

|

(2,434 |

) |

|

|

— |

|

|

|

— |

|

|

|

(2,434 |

) |

|

Balance at September 30, 2019 |

|

$ |

4,464 |

|

|

$ |

366 |

|

|

$ |

691 |

|

|

$ |

3,530 |

|

|

$ |

9,262,304 |

|

|

$ |

(1,087,923 |

) |

|

$ |

8,183,432 |

|

|

$ |

92,073 |

|

|

$ |

128,147 |

|

|

$ |

8,403,652 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Non- |

|

|

Non- |

|

|

|

|

|

||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

controlling |

|

|

controlling |

|

|

|

|

|

||

|

|

|

Par Value |

|

|

|

|

|

|

Accumulated |

|

|

|

|

|

|

Interests |

|

|

Interests |

|

|

|

|

|

||||||||||||||||

|

|

|

Common |

|

|

Common |

|

|

Common |

|

|

Common |

|

|

Additional |

|

|

Deficit and |

|

|

Total |

|

|

Attributable |

|

|

Attributable |

|

|

|

|

|

|||||||||

|

|

|

Stock |

|

|

Stock |

|

|

Stock |

|

|

Stock |

|

|

Paid-in |

|

|

Cumulative |

|

|

Stockholders' |

|

|

to Third Party |

|

|

to BREIT OP |

|

|

Total |

|

||||||||||

|

|

|

Class S |

|

|

Class T |

|

|

Class D |

|

|

Class I |

|

|

Capital |

|

|

Distributions |

|

|

Equity |

|

|

Joint Ventures |

|

|

Unitholders |

|

|

Equity |

|

||||||||||

|

Balance at December 31, 2018 |

|

$ |

2,770 |

|

|

$ |

233 |

|

|

$ |

304 |

|

|

$ |

1,083 |

|

|

$ |

4,327,444 |

|

|

$ |

(587,548 |

) |

|

$ |

3,744,286 |

|

|

$ |

75,592 |

|

|

$ |

95,076 |

|

|

$ |

3,914,954 |

|

|

Common stock issued |

|

|

1,662 |

|

|

|

134 |

|

|

|

381 |

|

|

|

2,482 |

|

|

|

5,150,713 |

|

|

|

— |

|

|

|

5,155,372 |

|

|

|

— |

|

|

|

— |

|

|

|

5,155,372 |

|

|

Offering costs |

|

|

— |

|

|

|

— |

|

|

|

— |

|

|

|

— |

|

|

|

(213,228 |

) |

|

|

— |

|

|

|

(213,228 |

) |

|

|

— |

|

|

|

— |

|

|

|

(213,228 |

) |

|

Distribution reinvestment |

|

|

84 |

|

|

|

7 |

|

|

|

9 |

|

|

|

46 |

|

|

|

161,625 |

|

|

|

— |

|

|

|

161,771 |

|

|

|

— |

|

|

|

— |

|

|

|

161,771 |

|

|

Common stock/units repurchased |

|

|

(52 |

) |

|

|

(8 |

) |

|

|

(3 |

) |

|

|

(84 |

) |

|

|

(160,672 |

) |

|

|

— |

|

|

|

(160,819 |

) |

|

|

— |

|

|

|

(718 |

) |

|

|

(161,537 |

) |

|

Amortization of compensation awards |

|

|

— |

|

|

|

— |

|

|

|

— |

|

|

|

3 |

|

|

|

297 |

|

|

|

— |

|

|

|

300 |

|

|

|

— |

|

|

|

1,500 |

|

|

|

1,800 |

|

|

Net loss ($1,083 allocated to redeemable non-controlling interests) |

|

|

— |

|

|

|

— |

|

|

|

— |

|

|

|

— |

|

|

|

— |

|

|

|

(220,721 |

) |

|

|

(220,721 |

) |

|

|

(3,631 |

) |

|

|

(3,939 |

) |

|

|

(228,291 |

) |

|

Distributions declared on common stock ($0.4764 gross per share) |

|

|

— |

|

|

|

— |

|

|

|

— |

|

|

|

— |

|

|

|

— |

|

|

|

(279,654 |

) |

|

|

(279,654 |

) |

|

|

— |

|

|

|

— |

|

|

|

(279,654 |

) |

|

Contributions from non-controlling interests |

|

|

— |

|

|

|

— |

|

|

|

— |

|

|

|

— |

|

|

|

— |

|

|

|

— |

|

|

|

— |

|

|

|

47,938 |

|

|

|

41,888 |

|

|

|

89,826 |

|

|

Distributions to non-controlling interests |

|

|

— |

|

|

|

— |

|

|

|

— |

|

|

|

— |

|

|

|

— |

|

|

|

— |

|

|

|

— |

|

|

|

(27,826 |

) |

|

|

(5,660 |

) |

|

|

(33,486 |

) |

|

Allocation to redeemable non-controlling interests |

|

|

— |

|

|

|

— |

|

|

|

— |

|

|

|

— |

|

|

|

(3,875 |

) |

|

|

— |

|

|

|

(3,875 |

) |

|

|

— |

|

|

|

— |

|

|

|

(3,875 |

) |

|

Balance at September 30, 2019 |

|

$ |

4,464 |

|

|

$ |

366 |

|

|

$ |

691 |

|

|

$ |

3,530 |

|

|

$ |

9,262,304 |

|

|

$ |

(1,087,923 |

) |

|

$ |

8,183,432 |

|

|

$ |

92,073 |

|

|

$ |

128,147 |

|

|

$ |

8,403,652 |

|

See accompanying notes to condensed consolidated financial statements.

3

Blackstone Real Estate Income Trust, Inc.

Condensed Consolidated Statements of Changes in Equity (Unaudited)

(in thousands, except per share data)

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Non- |

|

|

Non- |

|

|

|

|

|

||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

controlling |

|

|

controlling |

|

|

|

|

|

||

|

|

|

Par Value |

|

|

|

|

|

|

Accumulated |

|

|

|

|

|

|

Interests |

|

|

Interests |

|

|

|

|

|

||||||||||||||||

|

|

|

Common |

|

|

Common |

|

|

Common |

|

|

Common |

|

|

Additional |

|

|

Deficit and |

|

|

Total |

|

|

Attributable |

|

|

Attributable |

|

|

|

|

|

|||||||||

|

|

|

Stock |

|

|

Stock |

|

|

Stock |

|

|

Stock |

|

|

Paid-in |

|

|

Cumulative |

|

|

Stockholders' |

|

|

to Third Party |

|

|

to BREIT OP |

|

|

Total |

|

||||||||||

|

|

|

Class S |

|

|

Class T |

|

|

Class D |

|

|

Class I |

|

|

Capital |

|

|

Distributions |

|

|

Equity |

|

|

Joint Ventures |

|

|

Unitholders |

|

|

Equity |

|

||||||||||

|

Balance at June 30, 2018 |

|

$ |

1,986 |

|

|

$ |

149 |

|

|

$ |

168 |

|

|

$ |

667 |

|

|

$ |

2,884,242 |

|

|

$ |

(297,090 |

) |

|

$ |

2,590,122 |

|

|

$ |

30,965 |

|

|

$ |

— |

|

|

$ |

2,621,087 |

|

|

Common stock issued |

|

|

377 |

|

|

|

42 |

|

|

|

73 |

|

|

|

207 |

|

|

|

754,860 |

|

|

|

— |

|

|

|

755,559 |

|

|

|

— |

|

|

|

— |

|

|

|

755,559 |

|

|

Offering costs |

|

|

— |

|

|

|

— |

|

|

|

— |

|

|

|

— |

|

|

|

(47,436 |

) |

|

|

— |

|

|

|

(47,436 |

) |

|

|

— |

|

|

|

— |

|

|

|

(47,436 |

) |

|

Distribution reinvestment |

|

|

17 |

|

|

|

1 |

|

|

|

3 |

|

|

|

6 |

|

|

|

28,370 |

|

|

|

— |

|

|

|

28,397 |

|

|

|

— |

|

|

|

— |

|

|

|

28,397 |

|

|

Common stock repurchased |

|

|

(7 |

) |

|

|

— |

|

|

|

(2 |

) |

|

|

(9 |

) |

|

|

(19,471 |

) |

|

|

— |

|

|

|

(19,489 |

) |

|

|

— |

|

|

|

— |

|

|

|

(19,489 |

) |

|

Amortization of restricted stock grant |

|

|

— |

|

|

|

— |

|

|

|

— |

|

|

|

— |

|

|

|

62 |

|

|

|

— |

|

|

|

62 |

|

|

|

— |

|

|

|

— |

|

|

|

62 |

|

|

Net loss ($164 allocated to redeemable non-controlling interest) |

|

|

— |

|

|

|

— |

|

|

|

— |

|

|

|

— |

|

|

|

— |

|

|

|

(57,667 |

) |

|

|

(57,667 |

) |

|

|

(124 |

) |

|

|

(808 |

) |

|

|

(58,599 |

) |

|

Distributions declared on common stock ($0.1581 gross per share) |

|

|

— |

|

|

|

— |

|

|

|

— |

|

|

|

— |

|

|

|

— |

|

|

|

(48,454 |

) |

|

|

(48,454 |

) |

|

|

— |

|

|

|

— |

|

|

|

(48,454 |

) |

|

Contributions from non-controlling interests |

|

|

— |

|

|

|

— |

|

|

|

— |

|

|

|

— |

|

|

|

— |

|

|

|

— |

|

|

|

— |

|

|

|

18,942 |

|

|

|

50,000 |

|

|

|

68,942 |

|

|

Acquired non-controlling interests |

|

|

— |

|

|

|

— |

|

|

|

— |

|

|

|

— |

|

|

|

— |

|

|

|

— |

|

|

|

— |

|

|

|

12,802 |

|

|

|

— |

|

|

|

12,802 |

|

|

Distributions to non-controlling interests |

|

|

— |

|

|

|

— |

|

|

|

— |

|

|

|

— |

|

|

|

— |

|

|

|

— |

|

|

|

— |

|

|

|

(620 |

) |

|

|

(368 |

) |

|

|

(988 |

) |

|

Allocation to redeemable non-controlling interest |

|

|

— |

|

|

|

— |

|

|

|

— |

|

|

|

— |

|

|

|

(370 |

) |

|

|

— |

|

|

|

(370 |

) |

|

|

— |

|

|

|

— |

|

|

|

(370 |

) |

|

Balance at September 30, 2018 |

|

$ |

2,373 |

|

|

$ |

192 |

|

|

$ |

242 |

|

|

$ |

871 |

|

|

$ |

3,600,257 |

|

|

$ |

(403,211 |

) |

|

$ |

3,200,724 |

|

|

$ |

61,965 |

|

|

$ |

48,824 |

|

|

$ |

3,311,513 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Non- |

|

|

Non- |

|

|

|

|

|

||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

controlling |

|

|

controlling |

|

|

|

|

|

||

|

|

|

Par Value |

|

|

|

|

|

|

Accumulated |

|

|

|

|

|

|

Interests |

|

|

Interests |

|

|

|

|

|

||||||||||||||||

|

|

|

Common |

|

|

Common |

|

|

Common |

|

|

Common |

|

|

Additional |

|

|

Deficit and |

|

|

Total |

|

|

Attributable |

|

|

Attributable |

|

|

|

|

|

|||||||||

|

|

|

Stock |

|

|

Stock |

|

|

Stock |

|

|

Stock |

|

|

Paid-in |

|

|

Cumulative |

|

|

Stockholders' |

|

|

to Third Party |

|

|

to BREIT OP |

|

|

Total |

|

||||||||||

|

|

|

Class S |

|

|

Class T |

|

|

Class D |

|

|

Class I |

|

|

Capital |

|

|

Distributions |

|

|

Equity |

|

|

Joint Ventures |

|

|

Unitholders |

|

|

Equity |

|

||||||||||

|

Balance at December 31, 2017 |

|

$ |

1,301 |

|

|

$ |

56 |

|

|

$ |

40 |

|

|

$ |

307 |

|

|

$ |

1,616,720 |

|

|

$ |

(132,633 |

) |

|

$ |

1,485,791 |

|

|

$ |

23,848 |

|

|

$ |

— |

|

|

$ |

1,509,639 |

|

|

Common stock issued |

|

|

1,045 |

|

|

|

134 |

|

|

|

201 |

|

|

|

560 |

|

|

|

2,080,278 |

|

|

|

— |

|

|

|

2,082,218 |

|

|

|

— |

|

|

|

— |

|

|

|

2,082,218 |

|

|

Offering costs |

|

|

— |

|

|

|

— |

|

|

|

— |

|

|

|

— |

|

|

|

(131,288 |

) |

|

|

— |

|

|

|

(131,288 |

) |

|

|

— |

|

|

|

— |

|

|

|

(131,288 |

) |

|

Distribution reinvestment |

|

|

42 |

|

|

|

2 |

|

|

|

3 |

|

|

|

15 |

|

|

|

66,836 |

|

|

|

— |

|

|

|

66,898 |

|

|

|

— |

|

|

|

— |

|

|

|

66,898 |

|

|

Common stock repurchased |

|

|

(15 |

) |

|

|

— |

|

|

|

(2 |

) |

|

|

(11 |

) |

|

|

(30,575 |

) |

|

|

— |

|

|

|

(30,603 |

) |

|

|

— |

|

|

|

— |

|

|

|

(30,603 |

) |

|

Amortization of restricted stock grant |

|

|

— |

|

|

|

— |

|

|

|

— |

|

|

|

— |

|

|

|

112 |

|

|

|

— |

|

|

|

112 |

|

|

|

— |

|

|

|

— |

|

|

|

112 |

|

|

Net loss ($786 allocated to redeemable non-controlling interest) |

|

|

— |

|

|

|

— |

|

|

|

— |

|

|

|

— |

|

|

|

— |

|

|

|

(155,697 |

) |

|

|

(155,697 |

) |

|

|

(3,054 |

) |

|

|

(808 |

) |

|

|

(159,559 |

) |

|

Distributions declared on common stock ($0.4699 gross per share) |

|

|

— |

|

|

|

— |

|

|

|

— |

|

|

|

— |

|

|

|

— |

|

|

|

(114,881 |

) |

|

|

(114,881 |

) |

|

|

— |

|

|

|

— |

|

|

|

(114,881 |

) |

|

Contributions from non-controlling interests |

|

|

— |

|

|

|

— |

|

|

|

— |

|

|

|

— |

|

|

|

— |

|

|

|

— |

|

|

|

— |

|

|

|

30,216 |

|

|

|

50,000 |

|

|

|

80,216 |

|

|

Acquired non-controlling interests |

|

|

— |

|

|

|

— |

|

|

|

— |

|

|

|

— |

|

|

|

— |

|

|

|

— |

|

|

|

— |

|

|

|

12,802 |

|

|

|

— |

|

|

|

12,802 |

|

|

Distributions to non-controlling interests |

|

|

— |

|

|

|

— |

|

|

|

— |

|

|

|

— |

|

|

|

— |

|

|

|

— |

|

|

|

— |

|

|

|

(1,847 |

) |

|

|

(368 |

) |

|

|

(2,215 |

) |

|

Allocation to redeemable non-controlling interest |

|

|

— |

|

|

|

— |

|

|

|

— |

|

|

|

— |

|

|

|

(1,826 |

) |

|

|

— |

|

|

|

(1,826 |

) |

|

|

— |

|

|

|

— |

|

|

|

(1,826 |

) |

|

Balance at September 30, 2018 |

|

$ |

2,373 |

|

|

$ |

192 |

|

|

$ |

242 |

|

|

$ |

871 |

|

|

$ |

3,600,257 |

|

|

$ |

(403,211 |

) |

|

$ |

3,200,724 |

|

|

$ |

61,965 |

|

|

$ |

48,824 |

|

|

$ |

3,311,513 |

|

See accompanying notes to condensed consolidated financial statements.

4

Blackstone Real Estate Income Trust, Inc.

Condensed Consolidated Statements of Cash Flows (Unaudited)

(in thousands)

|

|

|

Nine Months Ended September 30, |

|

|||||

|

|

|

2019 |

|

|

2018 |

|

||

|

Cash flows from operating activities: |

|

|

|

|

|

|

|

|

|

Net loss |

|

$ |

(229,374 |

) |

|

$ |

(160,345 |

) |

|

Adjustments to reconcile net loss to net cash provided by operating activities: |

|

|

|

|

|

|

|

|

|

Management fee |

|

|

69,522 |

|

|

|

28,073 |

|

|

Performance participation allocation |

|

|

106,383 |

|

|

|

29,796 |

|

|

Depreciation and amortization |

|

|

505,986 |

|

|

|

262,708 |

|

|

Gain on disposition of real estate |

|

|

(36,167 |

) |

|

|

— |

|

|

Unrealized gain on changes in fair value of financial instruments |

|

|

(53,025 |

) |

|

|

(8,761 |

) |

|

Other items |

|

|

7,131 |

|

|

|

(880 |

) |

|

Change in assets and liabilities: |

|

|

|

|

|

|

|

|

|

(Increase) / decrease in other assets |

|

|

(95,832 |

) |

|

|

(53,117 |

) |

|

Increase / (decrease) in due to affiliates |

|

|

4,802 |

|

|

|

234 |

|

|

Increase / (decrease) in accounts payable, accrued expenses, and other liabilities |

|

|

93,940 |

|

|

|

81,340 |

|

|

Net cash provided by operating activities |

|

|

373,366 |

|

|

|

179,048 |

|

|

Cash flows from investing activities: |

|

|

|

|

|

|

|

|

|

Acquisitions of real estate |

|

|

(9,827,563 |

) |

|

|

(5,693,880 |

) |

|

Capital improvements to real estate |

|

|

(135,645 |

) |

|

|

(59,071 |

) |

|

Proceeds from disposition of real estate |

|

|

74,568 |

|

|

|

— |

|

|

Pre-acquisition costs |

|

|

(9,991 |

) |

|

|

— |

|

|

Purchase of real estate-related securities and loans |

|

|

(1,623,503 |

) |

|

|

(1,227,708 |

) |

|

Proceeds from settlement of real estate-related securities and loans |

|

|

329,445 |

|

|

|

124,396 |

|

|

Net cash used in investing activities |

|

|

(11,192,689 |

) |

|

|

(6,856,263 |

) |

|

Cash flows from financing activities: |

|

|

|

|

|

|

|

|

|

Proceeds from issuance of common stock |

|

|

4,913,617 |

|

|

|

1,948,928 |

|

|

Offering costs paid |

|

|

(53,548 |

) |

|

|

(31,316 |

) |

|

Subscriptions received in advance |

|

|

560,444 |

|

|

|

180,425 |

|

|

Repurchase of common stock |

|

|

(82,878 |

) |

|

|

(11,691 |

) |

|

Repurchase of management fee shares |

|

|

(72,711 |

) |

|

|

(7,568 |

) |

|

Redemption of redeemable non-controlling interest |

|

|

(35,435 |

) |

|

|

(8,400 |

) |

|

Redemption of affiliate service provider incentive compensation awards |

|

|

(718 |

) |

|

|

— |

|

|

Borrowings from mortgage notes, term loans, and secured revolving credit facilities |

|

|

10,036,847 |

|

|

|

5,632,422 |

|

|

Repayments from mortgage notes, term loans, and secured revolving credit facilities |

|

|

(4,692,644 |

) |

|

|

(1,737,931 |

) |

|

Borrowings under repurchase agreements |

|

|

1,152,366 |

|

|

|

954,892 |

|

|

Settlement of repurchase agreements |

|

|

(219,755 |

) |

|

|

(96,025 |

) |

|

Borrowings from affiliate line of credit |

|

|

1,883,000 |

|

|

|

1,135,900 |

|

|

Repayments on affiliate line of credit |

|

|

(1,883,000 |

) |

|

|

(1,141,150 |

) |

|

Borrowings from unsecured credit facilities |

|

|

240,000 |

|

|

|

— |

|

|

Repayments on unsecured credit facilities |

|

|

(240,000 |

) |

|

|

— |

|

|

Payment of deferred financing costs |

|

|

(94,726 |

) |

|

|

(39,468 |

) |

|

Contributions from non-controlling interests |

|

|

50,400 |

|

|

|

80,216 |

|

|

Distributions to non-controlling interests |

|

|

(31,325 |

) |

|

|

(2,776 |

) |

|

Distributions |

|

|

(94,659 |

) |

|

|

(38,075 |

) |

|

Net cash provided by financing activities |

|

|

11,335,275 |

|

|

|

6,818,383 |

|

|

Net change in cash and cash equivalents and restricted cash |

|

|

515,952 |

|

|

|

141,168 |

|

|

Cash and cash equivalents and restricted cash, beginning of period |

|

|

306,613 |

|

|

|

157,729 |

|

|

Cash and cash equivalents and restricted cash, end of period |

|

$ |

822,565 |

|

|

$ |

298,897 |

|

|

Reconciliation of cash and cash equivalents and restricted cash to the condensed consolidated balance sheets: |

|

|

|

|

|

|

|

|

|

Cash and cash equivalents |

|

$ |

155,674 |

|

|

$ |

75,529 |

|

|

Restricted cash |

|

|

666,891 |

|

|

|

223,368 |

|

|

Total cash and cash equivalents and restricted cash |

|

$ |

822,565 |

|

|

$ |

298,897 |

|

5

|

|

|

|

|

|

|

|

|

|

|

Assumption of mortgage notes in conjunction with acquisitions of real estate |

|

$ |

1,146,823 |

|

|

$ |

197,290 |

|

|

Assumption of other liabilities in conjunction with acquisitions of real estate |

|

$ |

66,629 |

|

|

$ |

51,094 |

|

|

Issuance of BREIT OP units as consideration for acquisitions of real estate |

|

$ |

36,749 |

|

|

$ |

— |

|

|

Recognition of financing lease liability |

|

$ |

56,008 |

|

|

$ |

— |

|

|

Assumed operating ground lease liabilities |

|

$ |

47,393 |

|

|

$ |

— |

|

|

Accrued pre-acquisition costs |

|

$ |

868 |

|

|

$ |

61 |

|

|

Contributions from non-controlling interests |

|

$ |

2,520 |

|

|

$ |

— |

|

|

Accrued capital expenditures and acquisition related costs |

|

$ |

7,187 |

|

|

$ |

3,985 |

|

|

Accrued distributions |

|

$ |

23,380 |

|

|

$ |

9,952 |

|

|

Accrued stockholder servicing fee due to affiliate |

|

$ |

160,604 |

|

|

$ |

101,124 |

|

|

Redeemable non-controlling interest issued as settlement of performance participation allocation |

|

$ |

37,484 |

|

|

$ |

16,974 |

|

|

Exchange of redeemable non-controlling interest for Class I shares |

|

$ |

11,620 |

|

|

$ |

— |

|

|

Allocation to redeemable non-controlling interest |

|

$ |

3,875 |

|

|

$ |

1,826 |

|

|

Distribution reinvestment |

|

$ |

161,771 |

|

|

$ |

66,899 |

|

|

Accrued common stock repurchases |

|

$ |

5,330 |

|

|

$ |

11,344 |

|

|

Acquired non-controlling interests |

|

$ |

— |

|

|

$ |

12,802 |

|

|

Issuance of BREIT OP units as settlement of affiliate incentive compensation awards |

|

$ |

4,714 |

|

|

$ |

— |

|

|

Payable for real estate-related securities |

|

$ |

185,074 |

|

|

$ |

— |

|

See accompanying notes to condensed consolidated financial statements.

6

Blackstone Real Estate Income Trust, Inc.

Notes to Condensed Consolidated Financial Statements

(Unaudited)

1. Organization and Business Purpose

Blackstone Real Estate Income Trust, Inc. (“BREIT” or the “Company”) invests primarily in stabilized income-oriented commercial real estate in the United States and, to a lesser extent, in real estate-related securities and loans. The Company is the sole general partner of BREIT Operating Partnership, L.P., a Delaware limited partnership (“BREIT OP”). BREIT Special Limited Partner L.P. (the “Special Limited Partner”), a wholly-owned subsidiary of The Blackstone Group Inc. (together with its affiliates, “Blackstone”), owns a special limited partner interest in BREIT OP. Substantially all of the Company’s business is conducted through BREIT OP. The Company and BREIT OP are externally managed by BX REIT Advisors L.L.C. (the “Adviser”). The Adviser is part of the real estate group of Blackstone, a leading global investment manager, which serves as our sponsor. The Company was formed on November 16, 2015 as a Maryland corporation and qualifies as a real estate investment trust (“REIT”) for U.S. federal income tax purposes.

As of September 30, 2019, the Company had received net proceeds of $9.8 billion from selling shares in the Offering, as defined below, and unregistered share of the Company’s common stock. The Company had registered with the Securities and Exchange Commission (the “SEC”) an offering of up to $5.0 billion in shares of common stock (the “Initial Offering”) and accepted gross offering proceeds of $4.9 billion during the period January 1, 2017 to January 1, 2019. The Company subsequently registered with the SEC a follow-on offering of up to $12.0 billion in shares of common stock, consisting of up to $10.0 billion in shares in its primary offering and up to $2.0 billion in shares pursuant to its distribution reinvestment plan (the “Current Offering” and with the Initial Offering, the “Offering”). The Company intends to sell any combination of four classes of shares of its common stock, with a dollar value up to the maximum aggregate amount of the Current Offering. The share classes have different upfront selling commissions, dealer manager fees and ongoing stockholder servicing fees. The Company intends to continue selling shares on a monthly basis.

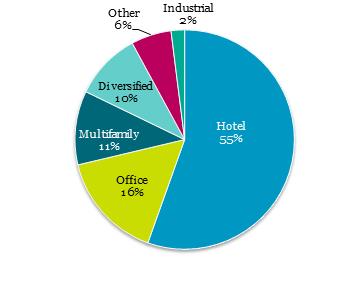

As of September 30, 2019, the Company owned 1,022 properties and had 182 positions in real estate-related securities and loans. The Company currently operates in six reportable segments: Multifamily, Industrial, Hotel, Retail and Other Properties, and Real Estate-Related Securities and Loans. Multifamily includes various forms of rental housing including apartments, student housing and manufactured housing. Other Properties includes self-storage properties. Financial results by segment are reported in Note 13 — Segment Reporting.

2. Summary of Significant Accounting Policies

Basis of Presentation

The accompanying unaudited condensed consolidated financial statements have been prepared in accordance with accounting principles generally accepted in the United States of America (“GAAP”) for interim financial information and the instructions to Form 10-Q and Rule 10-01 of Regulation S-X. The condensed consolidated financial statements, including the condensed notes thereto, are unaudited and exclude some of the disclosures required in audited financial statements. Management believes it has made all necessary adjustments, consisting of only normal recurring items, so that the condensed consolidated financial statements are presented fairly and that estimates made in preparing its condensed consolidated financial statements are reasonable and prudent. The accompanying unaudited condensed consolidated interim financial statements should be read in conjunction with the audited consolidated financial statements included in the Company’s Annual Report on Form 10-K for the fiscal year ended December 31, 2018 filed with the SEC.

Certain amounts in the Company’s prior period condensed consolidated financial statements have been reclassified to conform to the current period presentation. The Company has chosen to aggregate certain financial statement line items in the Company’s condensed consolidated statements of operations. Such reclassifications had no effect on total revenues or net loss on the condensed consolidated statements of operations.

The accompanying condensed consolidated financial statements include the accounts of the Company, the Company’s subsidiaries and joint ventures in which the Company has a controlling interest. For consolidated joint ventures, the non-controlling partner’s share of the assets, liabilities and operations of the joint ventures is included in non-controlling interests as equity of the Company. The non-controlling partner’s interest is generally computed as the joint venture partner’s ownership percentage. All intercompany balances and transactions have been eliminated in consolidation.

7

The Company consolidates partially owned entities in which it has a controlling financial interest. In determ ining whether the Company has a controlling financial interest in a partially owned entity and the requirement to consolidate the accounts of that entity, the Company considers whether the entity is a variable interest entity (“VIE”) and whether it is the primary beneficiary. The Company is the primary beneficiary of a VIE when it has (i) the power to direct the most significant activities impacting the economic performance of the VIE and (ii) the obligation to absorb losses or receive benefits significant to the VIE. BREIT OP and each of the Company’s joint ventures are considered to be a VIE. The Company consolidates these entities because it has the ability to direct the most significant activities of the entities such as purchases, dispositions, financin gs, budgets, and overall operating plans.

As of September 30, 2019, the total assets and liabilities of the Company’s consolidated VIEs, excluding BREIT OP, were $4.7 billion and $3.3 billion, respectively, compared to $2.8 billion and $1.9 billion as of December 31, 2018. Such amounts are included on the Company’s Condensed Consolidated Balance Sheets.

The preparation of the financial statements in conformity with GAAP requires management to make estimates and assumptions that affect the reported amounts of assets and liabilities and disclosures of contingent assets and liabilities at the date of the balance sheet. Actual results could differ from those estimates.

Fair Value Option

The Company elected the fair value option (“FVO”) for its investments in term loans. Unrealized gains and losses on the value of financial instruments for which the FVO has been elected are recorded as a component of net income or loss. The Company records any unrealized gains or losses on its investments in term loans as a component of Income from Real Estate-Related Securities and Loans on the Condensed Consolidated Statements of Operations.

Fair Value Measurements

Under normal market conditions, the fair value of an investment is the amount that would be received to sell an asset or transfer a liability in an orderly transaction between market participants at the measurement date (i.e., the exit price). Additionally, there is a hierarchal framework that prioritizes and ranks the level of market price observability used in measuring investments at fair value. Market price observability is impacted by a number of factors, including the type of investment and the characteristics specific to the investment and the state of the marketplace, including the existence and transparency of transactions between market participants. Investments with readily available actively quoted prices or for which fair value can be measured from actively quoted prices generally will have a higher degree of market price observability and a lesser degree of judgment used in measuring fair value.

Investments measured and reported at fair value are classified and disclosed in one of the following levels within the fair value hierarchy:

Level 1 — quoted prices are available in active markets for identical investments as of the measurement date. The Company does not adjust the quoted price for these investments.

Level 2 — quoted prices are available in markets that are not active or model inputs are based on inputs that are either directly or indirectly observable as of the measurement date.

Level 3 — pricing inputs are unobservable and include instances where there is minimal, if any, market activity for the investment. These inputs require significant judgment or estimation by management or third parties when determining fair value and generally represent anything that does not meet the criteria of Levels 1 and 2. Due to the inherent uncertainty of these estimates, these values may differ materially from the values that would have been used had a ready market for these investments existed.

As of September 30, 2019 and December 31, 2018, the Company’s $3.8 billion and $2.3 billion, respectively, of investments in real estate-related securities and loans were classified as Level 2.

Valuation

The Company’s investments in real estate-related securities and loans are reported at fair value. As of September 30, 2019, the Company’s investments in real estate-related securities and loans consisted of commercial mortgage-backed securities (“CMBS”) and residential mortgage-backed securities (“RMBS”), which are mortgage-related fixed income securities, corporate bonds, and term loans of real estate-related companies. The Company generally determines the fair value of its real estate-related securities and loans by utilizing third-party pricing service providers and broker-dealer quotations on the basis of last available bid price.

8

In determining the fair value of a particular investment, pricing service providers may use broker-dealer quotations, reported trades or valuation estimates from their interna l pricing models to determine the reported price. The pricing service providers’ internal models for securities such as real estate-related securities and loans generally consider the attributes applicable to a particular class of the security (e.g., credi t rating, seniority), current market data, and estimated cash flows for each class and incorporate deal collateral performance such as prepayment speeds and default rates, as available.

As of September 30, 2019, the fair value of the Company’s mortgage notes, term loans, secured and unsecured revolving credit facilities, repurchase agreements, and affiliate line of credit was approximately $71.8 million above carrying value. Fair value of the Company’s indebtedness is estimated by modeling the cash flows required by the Company’s debt agreements and discounting them back to the present value using the appropriate discount rate. Additionally, the Company considers current market rates and conditions by evaluating similar borrowing agreements with comparable loan-to-value ratios and credit profiles. The inputs used in determining the fair value of the Company’s indebtedness are considered Level 3.

Stock-Based Compensation

The Company’s stock-based compensation consists of incentive compensation awards issued to certain employees of affiliate portfolio company service providers. Such awards vest over the life of the awards and stock-based compensation expense is recognized for these awards in net income on a straight-line basis over the applicable vesting period of the award, based on the value of the awards at grant. Refer to Note 11 for additional information.

Recent Accounting Pronouncements

On January 1, 2019, the Company adopted Accounting Standards Update 2016-02 (“ASU 2016-02”), “Leases,” and all related amendments (codified in Accounting Standards Codification Topic 842 (“Topic 842”)). Certain of the Company’s investments in real estate are subject to ground leases, for which lease liabilities and corresponding right-of-use (“ROU”) assets were recognized as a result of adoption. The Company calculated the amount of the lease liabilities and ROU assets by taking the present value of the remaining lease payments, and adjusted the ROU assets for any existing straight-line ground rent liabilities and acquired ground lease intangibles. The Company’s estimated incremental borrowing rate of a loan with a similar term as the corresponding ground leases was used as the discount rate, which was determined to be approximately 7.0%. Considerable judgment and assumptions were required to estimate the Company’s incremental borrowing rate which was determined by considering the Company’s credit quality, ground lease duration, and debt yields observed in the market.

Three of the Company’s existing ground leases were classified as operating leases, and upon adoption the Company recognized operating lease liabilities and corresponding ROU assets of $31.3 million. The Company’s existing below-market ground lease intangible asset of $4.5 million, above-market ground lease intangible liability of $4.6 million, and straight-line ground rent liability of $1.2 million were reclassified as of January 1, 2019 to be presented net of the operating ROU assets. In addition, the Company’s existing prepaid ground lease intangible asset of $15.7 million was reclassified as of January 1, 2019 to be presented along with the operating ROU assets.

The lease liabilities are included as a component of Accounts Payable, Accrued Expenses, and Other Liabilities and the related ROU assets are recorded as a component of Investments in Real Estate, Net on the Company’s Condensed Consolidated Balance Sheet. Refer to Note 3, Note 9 and Note 12 for additional information.

In transition, the Company elected the package of practical expedients to not reassess (i) whether existing arrangements are or contain a lease, (ii) the classification of an operating or financing lease in a period prior to adoption, and (iii) any initial direct costs for existing leases. Additionally, the Company elected to not use hindsight and carried forward its lease term assumptions when adopting Topic 842 and did not recognize lease liabilities and lease assets for leases with a term of 12 months or less. The Company applied ASU 2016-02 as of the effective date of January 1, 2019, and there was no impact to retained earnings as a result of the Company’s adoption.

9

The adoption of ASU 2016-02 for leases in which the Company is lessor did not have a material impact on the Company’s condensed consolidated financial statements. The Company elected to not separate non-lease components from lease components and presented lease related revenues as a single line item, net of bad debt expense on the Company’s Condensed Consolidated Statement of Operations. Prior to the adoption of ASU 2016-02, the Company separated lease related revenue between “rental revenue” and “tenant re imbursement income” and bad debt expense as a component of “rental property operating” expense. As a result of adoption, the Company reclassified the prior period balances of “tenant reimbursement income” to “rental revenue” to conform to the current perio d presentation. The Company did not reclassify the prior period balance of bad debt expense on its condensed consolidated statement of operations. The operating lease income presented in “rental revenue” for the three and nine months ended September 30, 20 18 includes $18.3 million and $42.9 million, respectively, previously classified as “tenant reimbursement income,” which was determined under the standard in effect prior to the Company’s adoption of ASU 2016-02. Refer to Note 12 for additional information .

3. Investments in Real Estate

Investments in real estate, net consisted of the following ($ in thousands):

|

|

|

September 30, 2019 |

|

|

December 31, 2018 |

|

||

|

Building and building improvements |

|

$ |

17,107,025 |

|

|

$ |

8,389,864 |

|

|

Land and land improvements |

|

|

3,793,031 |

|

|

|

1,961,977 |

|

|

Furniture, fixtures and equipment |

|

|

286,501 |

|

|

|

182,418 |

|

|

Right of use asset - operating leases (1) |

|

|

110,764 |

|

|

|

— |

|

|

Right of use asset - financing leases (1) |

|

|

56,008 |

|

|

|

— |

|

|

Total |

|

|

21,353,329 |

|

|

|

10,534,259 |

|

|

Accumulated depreciation and amortization |

|

|

(608,862 |

) |

|

|

(274,572 |

) |

|

Investments in real estate, net |

|

$ |

20,744,467 |

|

|

$ |

10,259,687 |

|

|

(1) |

Refer to Note 12 for additional details on the Company’s leases. |

During the nine months ended September 30, 2019, the Company acquired interests in 38 real estate investments for $11.1 billion, which were comprised of 440 industrial, 61 multifamily, 25 hotel, two retail and 21 self-storage properties categorized as other.

10

The following table provides further details of the properties acquired during the nine months ended September 30, 2019 ($ in thousands):

|

|

|

Ownership |

|

|

Number of |

|

|

|

|

|

|

Acquisition |

|

Purchase |

|

|||

|

Investment |

|

Interest (1) |

|

|

Properties |

|

|

Location |

|

Segment |

|

Date |

|

Price (2) |

|

|||

|

4500 Westport Drive |

|

100% |

|

|

|

1 |

|

|

Harrisburg, PA |

|

Industrial |

|

Jan. 2019 |

|

$ |

11,975 |

|

|

|

Roman Multifamily Portfolio |

|

100% |

|

|

|

14 |

|

|

Various (3) |

|

Multifamily |

|

Feb. 2019 |

|

|

857,540 |

|

|

|

Gilbert Heritage Apartments |

|

90% |

|

|

|

1 |

|

|

Phoenix, AZ |

|

Multifamily |

|

Feb. 2019 |

|

|

60,984 |

|

|

|

Courtyard Kona |

|

100% |

|

|

|

1 |

|

|

Kailua-Kona, HI |

|

Hotel |

|

March 2019 |

|

|

105,587 |

|