|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

UNITED STATES

|

|

SECURITIES AND EXCHANGE COMMISSION

|

|

Washington, D.C. 20549

|

|

FORM 10-K

|

|

☒

|

ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934

|

|

For the fiscal year ended

December 31, 2014

|

|

|

☐

|

TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934

|

|

For the transition period from _________to________

|

|

|

Commission File Number:

001-36448

|

|

|

Bankwell Financial Group, Inc.

|

|

|

(Exact Name of Registrant as specified in its Charter)

|

|

|

Connecticut

|

20-8251355

|

|

|

(State or other jurisdiction of

|

(I.R.S. Employer

|

|

|

Incorporation or organization)

|

Identification No.)

|

|

220 Elm Street

|

|

New Canaan, Connecticut 06840

|

|

(203) 652-0166

|

|

(Address, including zip code, and telephone number, including area code, of registrant’s principal executive offices)

|

|

Large

accelerated filer ☐

|

Accelerated filer

þ

|

|

|

Non-accelerated

filer ☐ (Do not check if a smaller reporting company)

|

Smaller

reporting company ☐

|

|

|

1

|

||

|

25

|

||

|

39

|

||

|

39

|

||

|

39

|

||

|

39

|

||

|

39

|

||

|

41

|

||

|

45

|

||

|

79

|

||

|

83

|

||

|

144

|

||

|

144

|

||

|

145

|

||

|

145

|

||

|

145

|

||

|

145

|

||

|

145

|

||

|

145

|

||

|

146

|

||

|

147

|

|

●

|

local, regional and national business or economic conditions may differ from those expected;

|

|

|

●

|

we are subject to credit risk and could incur losses in our loan portfolio;

|

|

|

●

|

our allowance for loan losses may not be adequate to absorb loan losses;

|

|

|

●

|

changes in real estate values could also increase our credit risk;

|

|

|

●

|

we could experience changes in our key management personnel;

|

|

|

●

|

we may not be able to successfully execute our management team’s strategic initiatives;

|

|

|

●

|

our ability to successfully execute our growth initiatives such as branch openings and acquisitions;

|

|

|

●

|

volatility and direction of market interest rates;

|

|

|

●

|

increased competition within our market area may limit our growth and profitability;

|

|

|

●

|

economic, market, operational, liquidity, credit and interest rate risks associated with our business;

|

|

|

●

|

the effects of and changes in trade, monetary and fiscal policies and laws, including the Federal Reserve Board’s interest rate policies;

|

|

|

●

|

changes in accounting policies and practices, as may be adopted by regulatory agencies, the Public Accounting Oversight Board or the Financial Accounting Standards Board;

|

|

|

●

|

changes in law and regulatory requirements (including those concerning taxes, banking, securities and insurance);

|

|

|

●

|

further governmental intervention in the U.S. financial system; and

|

|

|

●

|

difficulties and delays in integrating Quinnipiac Bank and Trust Company.

|

| 1 |

| 2 |

|

●

|

Responsive, Customer-Centric Products and Services and a Community Focus.

We offer a broad array of products and services which we customize to allow us to focus on building long-term relationships with our customers through high-quality, responsive and personal customer service. By focusing on the entire customer relationship, we build the trust of our customers which leads to long-term relationships and generates our organic growth. In addition, we are committed to meeting the needs of the communities that we serve. Our employees are involved in many civic and community organizations which we support through sponsorships. As a result, customers and potential customers within our market know about us and frequently interact with our employees which allows us to develop long-term customer relationships without extensive advertising.

|

|

|

●

|

Strategic Acquisitions.

To complement our organic growth, we focus on strategic acquisitions in or around our existing markets that further our objectives. We believe there are many banking institutions that continue to face credit challenges, capital constraints and liquidity issues and that lack the scale and management expertise to manage the increasing regulatory burden and will likely need to partner with an institution like ours. On March 31, 2014, we entered into a merger agreement with Quinnipiac. Quinnipiac had one branch located in Hamden, Connecticut and a second branch in the neighboring town of North Haven. The transaction closed on October 1, 2014 and Quinnipiac merged with and into Bankwell Bank. As we evaluate potential acquisitions, we will continue to seek acquisitions that provide meaningful financial benefits, long-term organic growth opportunities and expense reductions, without compromising our risk profile.

|

|

|

●

|

Utilization of Efficient and Scalable Infrastructure.

We employ a systematic and calculated approach to increasing our profitability and improving our efficiencies. We recently upgraded our operating infrastructure particularly in the areas of technology, data processing, compliance and personnel. We believe that our scalable infrastructure provides us with an efficient operating platform from which to grow in the near term, and without incurring significant incremental noninterest expenses, while continuing to deliver our high-quality, responsive customer service, which will enhance our ability to grow and increase our returns.

|

|

|

●

|

Disciplined Focus on Risk Management.

Effective risk management is a key component of our strong corporate culture. We use our strong risk management infrastructure to monitor our existing loan and investment securities portfolios, support operational decision-making and improve our ability to generate earning assets with strong credit quality. To maintain our strong credit quality, we use a comprehensive underwriting process and we seek to maintain a diversified loan portfolio and a conservative investment securities portfolio. Board-approved policies contain approval authorities, as appropriate, and are reviewed at least annually. We have a Risk Management Steering Committee comprised of executive officers who oversee new business initiatives and other activities that warrant oversight of risk and related mitigants. Internal review procedures are performed regarding anti-money laundering and consumer compliance requirements. Our Chief Risk Officer reports directly to the Chair of our Audit Committee.

|

| 3 |

|

●

|

Our

Market.

Our current market has been defined as the greater Fairfield County area, which is part of the second most

affluent metropolitan statistical area in the United States, the Bridgeport-Stamford-Norwalk, Connecticut MSA, according to

the U.S. Department of Commerce. In addition, our current market has expanded to New Haven County Connecticut with the

acquisition of Quinnipiac. The Stamford market area includes numerous affluent suburban communities of professionals who work

and commute into New York City, approximately 50 miles from our headquarters, and many small to mid-sized businesses which

support these communities. Fairfield County is the wealthiest county in Connecticut, with a 2009 – 2013 median household

income of $82,283 according to estimates from United States Census Bureau. We believe that this market has economic and

competitive dynamics that are favorable to executing our growth strategy.

|

|

|

●

|

Experienced and Respected Management Team with a Proven and Successful Track Record.

Our executive management team, is comprised of seasoned professionals with significant banking experience, a history of high performance at local financial institutions and success in identifying, acquiring and integrating financial institutions. Our senior management team includes Christopher Gruseke, Chief Executive Officer (since February 2015) Heidi S. DeWyngaert, Executive Vice President, Chief Lending Officer (ten years with us), Ernest J. Verrico, Sr., Executive Vice President, Chief Financial Officer (five years with us), Gail E.D. Brathwaite, Executive Vice President, Chief Operating Officer (two years with us), Diane Knetzger, Senior Vice President, Director of Marketing (ten years with us), Christine A. Chivily, Senior Vice President and Chief Credit Officer (two years with us) and Michele Johnson, Senior Vice President and Chief Risk Officer (six years with us).

|

|

|

●

|

Dedicated Board of Directors with Strong Community Involvement.

Our board of directors is comprised of a group of local business leaders who understand the need for strong community banks that focus on serving the financial needs of their customers. One of our directors, Frederick R. Afragola was instrumental in our organization and growth. Mr. Afragola was the Chief Executive Officer and President of The Bank of New Canaan from its opening in 2002 until his retirement in 2008 and played an integral role in building our foundation and guiding our growth. The interests of our executive management team and directors are aligned with those of our shareholders through common stock ownership. By capitalizing on the close community ties and business relationships of our executive management team and directors, we are positioned to continue taking advantage of the market opportunity present in our primary market.

|

|

|

●

|

Strong Capital Position.

At December 31, 2014, we had a 10.47% tangible common equity ratio, and the Bank had a 11.12% tier 1 leverage ratio and a 12.47% tier 1 risk-based ratio. Our ability to attract capital has facilitated our growth and is an integral component to the execution of our business plan.

|

|

|

●

|

Scalable Operating Platform.

We provide banking technology, including remote deposit capture, internet banking and mobile banking, to provide our customers with maximum flexibility and create a scalable platform to accommodate our future growth aspirations. We believe that our advanced technology combined with responsive and personal service provides our customers with a superior banking experience.

|

| 4 |

| 5 |

|

At December 31,

|

||||||||||||||||||||||||

|

2014

|

2013

|

2012

|

||||||||||||||||||||||

|

Percent of

|

Percent of

|

Percent of

|

||||||||||||||||||||||

|

Loan

|

Loan

|

Loan

|

||||||||||||||||||||||

|

(In thousands)

|

Amount

|

Portfolio

|

Amount

|

Portfolio

|

Amount

|

Portfolio

|

||||||||||||||||||

|

Real estate loans:

|

||||||||||||||||||||||||

|

Residential

|

$ | 175,031 | 18.83 | % | $ | 155,874 | 24.66 | % | $ | 144,288 | 27.22 | % | ||||||||||||

|

Commercial

|

521,181 | 56.06 | 316,533 | 50.08 | 284,763 | 53.72 | ||||||||||||||||||

|

Construction

|

63,229 | 6.80 | 51,545 | 8.16 | 33,148 | 6.26 | ||||||||||||||||||

|

Home equity

|

18,166 | 1.95 | 13,892 | 2.20 | 11,030 | 2.08 | ||||||||||||||||||

| 777,607 | 83.64 | 537,844 | 85.10 | 473,229 | 89.28 | |||||||||||||||||||

|

Commercial business

|

149,259 | 16.05 | 93,566 | 14.80 | 56,764 | 10.71 | ||||||||||||||||||

|

Consumer

|

2,896 | 0.31 | 602 | 0.10 | 57 | 0.01 | ||||||||||||||||||

|

Total loans

|

$ | 929,762 | 100.00 | % | $ | 632,012 | 100.00 | % | $ | 530,050 | 100.00 | % | ||||||||||||

| 6 |

|

At December 31,

|

||||||||||||||||

| 2011 | 2010 | |||||||||||||||

|

Percent of

|

Percent of

|

|||||||||||||||

|

Loan

|

Loan

|

|||||||||||||||

|

(In thousands)

|

Amount

|

Portfolio

|

Amount

|

Portfolio

|

||||||||||||

|

Real estate loans:

|

||||||||||||||||

|

Residential

|

$ | 104,754 | 28.37 | % | $ | 104,053 | 36.08 | % | ||||||||

|

Commercial

|

173,951 | 47.10 | 111,271 | 38.58 | ||||||||||||

|

Construction

|

40,422 | 10.95 | 38,072 | 13.20 | ||||||||||||

|

Home equity

|

14,815 | 4.01 | 16,657 | 5.77 | ||||||||||||

| 333,942 | 90.43 | 270,053 | 93.63 | |||||||||||||

|

Commercial business

|

35,041 | 9.49 | 17,713 | 6.14 | ||||||||||||

|

Consumer

|

311 | 0.08 | 659 | 0.23 | ||||||||||||

|

Total loans

|

$ | 369,294 | 100.00 | % | $ | 288,425 | 100.00 | % | ||||||||

| 7 |

| 8 |

| 9 |

| 10 |

| 11 |

| 12 |

| 13 |

| 14 |

| 15 |

| 16 |

| 17 |

| 18 |

| 19 |

|

|

●

|

Truth-In-Savings Act, requiring certain disclosures for consumer deposit accounts;

|

|

|

●

|

Right to Financial Privacy Act, which imposes a duty to maintain confidentiality of consumer financial records and prescribes procedures for complying with administrative subpoenas of financial records;

|

|

|

●

|

Electronic Funds Transfer Act and Regulation E issued by the Federal Reserve to implement that act, which govern automatic deposits to and withdrawals from deposit accounts and customers’ rights and liabilities arising from the use of automated teller machines and other electronic banking services; and

|

|

|

●

|

Rules and regulations of the various federal banking agencies charged with the responsibility of implementing these federal laws.

|

|

|

●

|

A lending test, to evaluate the bank’s record of making loans in its assessment areas;

|

|

|

●

|

An investment test, to evaluate the bank’s record of investing in community development projects, affordable housing, and programs benefiting low or moderate income individuals and businesses; and

|

|

|

●

|

A service test, to evaluate the bank’s delivery of services through its branches, ATMs, and other offices.

|

| 20 |

|

|

●

|

Federal Truth-In-Lending Act, governing disclosures of credit terms to consumer borrowers;

|

|

|

●

|

Home Mortgage Disclosure Act of 1975, requiring financial institutions to provide information to enable the public and public officials to determine whether a financial institution is fulfilling its obligation to help meet the housing needs of the community it serves;

|

|

|

●

|

Equal Credit Opportunity Act, prohibiting discrimination on the basis of race, creed, or other prohibited factors in extending credit;

|

|

|

●

|

Fair Credit Reporting Act of 1978, governing the use of consumer credit reports and the provision of information to credit reporting agencies;

|

|

|

●

|

Fair Debt Collection Act, governing the manner in which consumer debts may be collected by collection agencies;

|

|

|

●

|

Real Estate Settlement Procedures Act, governing closing costs and settlement procedures and disclosures to consumers related thereto;

|

|

|

●

|

Servicemembers Civil Relief Act of 2004, governing the repayment terms of, and property rights underlying, secured obligations of persons in military service; and

|

|

|

●

|

Rules and regulations of the various federal agencies charged with the responsibility of implementing these federal laws.

|

| 21 |

| 22 |

| 23 |

| 24 |

| 25 |

| 26 |

| 27 |

| 28 |

|

|

●

|

Our ability to build and maintain long-term customer relationships while ensuring high ethical standards and safe and sound banking practices;

|

|

|

●

|

The scope, relevance and pricing of products and services that we offer;

|

|

|

●

|

Customer satisfaction with our products and personalized services;

|

|

|

●

|

Industry and general economic trends; and

|

|

|

●

|

Our ability to keep pace with technological advances and to invest in new technology.

|

| 29 |

|

|

●

|

incurring time and expense associated with identifying and evaluating potential acquisitions and negotiating potential transactions, resulting in our attention being diverted from the operation of our existing business;

|

|

|

●

|

using inaccurate estimates and judgments to evaluate credit, operations, management and market risks with respect to the target institution or assets;

|

| 30 |

|

|

●

|

intense competition from other banking organizations and other inquirers for acquisitions;

|

|

|

●

|

potential exposure to unknown or contingent liabilities of banks and businesses we acquire;

|

|

|

●

|

the time and expense required to integrate the operations and personnel of the combined businesses;

|

|

|

●

|

experiencing higher operating expenses relative to operating income from the new operations;

|

|

|

●

|

creating an adverse short-term effect on our results of operations;

|

|

|

●

|

losing key employees and customers as a result of an acquisition that is poorly received;

|

|

|

●

|

significant problems relating to the conversion of the financial and customer data of the entity;

|

|

|

●

|

inconsistencies in standards, controls, procedures and policies that adversely affect our ability to maintain relationships with clients, customers, depositors and employees or to achieve the anticipated benefits of the acquisition;

|

|

|

●

|

diversion of our management’s attention and resources;

|

|

|

●

|

integration of acquired customers into our financial and customer product systems; or

|

|

|

●

|

risks of impairment to goodwill or other than temporary impairment.

|

| 31 |

| 32 |

| 33 |

| 34 |

| 35 |

| 36 |

| 37 |

| 38 |

| 39 |

|

December 31, 2014

|

December 31, 2013

|

|||||||||||||||||||||||

|

Cash

|

Cash | |||||||||||||||||||||||

|

Sales Price

|

Dividends |

Sales Price

|

Dividends | |||||||||||||||||||||

|

Quarter Ended

|

High

|

Low

|

Declared

|

High

|

Low

|

Declared

|

||||||||||||||||||

|

March 31

|

$ | 22.00 | $ | 18.80 | $ | - | $ | 22.00 | $ | 13.50 | $ | - | ||||||||||||

|

June 30

|

17.40 | 16.55 | - | 23.00 | 20.00 | - | ||||||||||||||||||

|

September 30

|

18.99 | 18.75 | - | 23.00 | 19.00 | - | ||||||||||||||||||

|

December 31

|

21.00 | 20.60 | - | 22.00 | 19.00 | - | ||||||||||||||||||

| 40 |

|

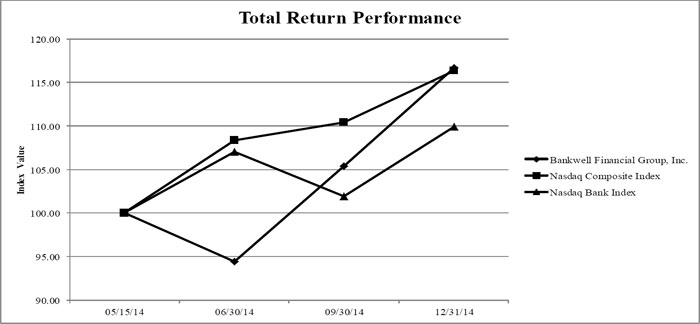

Index

|

05/15/14

|

06/30/14

|

09/30/14

|

12/31/14

|

|

Bankwell Financial Group, Inc.

|

100.00

|

94.44

|

105.39

|

116.67

|

|

Nasdaq Composite Index

|

100.00

|

108.33

|

110.42

|

116.39

|

|

Nasdaq Bank Index

|

100.00

|

107.01

|

101.91

|

109.89

|

| 41 |

| At or For the Years Ended December 31, | ||||||||||||||||||||

|

(Dollars in thousands, except per share data)

|

2014

|

2013

|

2012

|

2011

|

2010

|

|||||||||||||||

|

Statements of Income:

|

||||||||||||||||||||

|

Interest income

|

$ | 35,589 | $ | 28,092 | $ | 24,397 | $ | 20,587 | $ | 16,877 | ||||||||||

|

Interest expense

|

3,929 | 2,765 | 3,192 | 2,870 | 3,209 | |||||||||||||||

|

Net interest income

|

31,660 | 25,327 | 21,205 | 17,717 | 13,668 | |||||||||||||||

|

Provision for loan losses

|

2,152 | 585 | 1,821 | 1,049 | 1,311 | |||||||||||||||

|

Net interest income after provision for loan losses

|

29,508 | 24,742 | 19,384 | 16,668 | 12,357 | |||||||||||||||

|

Noninterest income

|

3,041 | 4,723 | 345 | 1,134 | 1,695 | |||||||||||||||

|

Noninterest expense

|

25,812 | 22,120 | 17,858 | 14,601 | 13,331 | |||||||||||||||

|

Income before income tax

|

6,737 | 7,345 | 1,871 | 3,201 | 721 | |||||||||||||||

|

Income tax expense

|

2,169 | 2,184 | 657 | 997 | 214 | |||||||||||||||

|

Net income

|

4,568 | 5,161 | 1,214 | 2,204 | 507 | |||||||||||||||

|

Net income attributable to common shareholders

|

$ | 4,458 | $ | 5,050 | $ | 1,082 | $ | 1,998 | $ | 246 | ||||||||||

|

Per Share Data:

|

||||||||||||||||||||

|

Basic earnings per share

|

$ | 0.78 | $ | 1.46 | $ | 0.39 | $ | 0.72 | $ | 0.10 | ||||||||||

|

Diluted earnings per share

|

0.78 | 1.44 | 0.38 | 0.71 | 0.09 | |||||||||||||||

|

Book value per share (end of period) (a)

|

16.84 | 15.58 | 14.50 | 13.85 | 12.81 | |||||||||||||||

|

Tangible book value per share (end of period) (a) (b)

|

16.35 | 15.46 | 14.50 | 13.85 | 12.81 | |||||||||||||||

|

Shares outstanding (end of period) (a)

|

7,019,620 | 3,754,253 | 2,797,200 | 2,758,200 | 2,756,200 | |||||||||||||||

|

Weighted average shares outstanding - basic

|

5,577,942 | 3,395,779 | 2,767,850 | 2,757,000 | 2,531,000 | |||||||||||||||

|

Weighted average shares outstanding - diluted

|

5,605,512 | 3,451,393 | 2,864,700 | 2,811,000 | 2,588,000 | |||||||||||||||

|

Performance Ratios:

|

||||||||||||||||||||

|

Return on average assets (c)

|

0.52 | % | 0.77 | % | 0.22 | % | 0.50 | % | 0.14 | % | ||||||||||

|

Return on average common shareholders’ equity

|

5.13 | % | 9.68 | % | 2.73 | % | 6.70 | % | 0.75 | % | ||||||||||

|

Return on average shareholders’ equity (c)

|

4.66 | % | 8.17 | % | 2.40 | % | 5.03 | % | 1.33 | % | ||||||||||

|

Average shareholders’ equity to average assets

|

11.14 | % | 9.32 | % | 9.34 | % | 10.01 | % | 10.37 | % | ||||||||||

|

Net interest margin

|

3.84 | % | 3.94 | % | 4.11 | % | 4.27 | % | 4.12 | % | ||||||||||

|

Efficiency ratio (b)

|

69.09 | % | 75.71 | % | 82.76 | % | 78.50 | % | 84.93 | % | ||||||||||

|

Asset Quality Ratios:

|

||||||||||||||||||||

|

Total past due loans to total loans (d)

|

0.86 | % | 0.73 | % | 0.75 | % | 1.01 | % | 0.79 | % | ||||||||||

|

Nonperforming loans to total loans (d)

|

0.36 | % | 0.16 | % | 0.75 | % | 1.01 | % | 0.79 | % | ||||||||||

|

Nonperforming assets to total assets (e)

|

0.39 | % | 0.23 | % | 0.81 | % | 0.78 | % | 0.57 | % | ||||||||||

|

Allowance for loan losses to nonperforming loans

|

323.02 | % | 835.69 | % | 200.84 | % | 171.88 | % | 239.23 | % | ||||||||||

|

Allowance for loan losses to total loans (d)

|

1.17 | % | 1.33 | % | 1.50 | % | 1.74 | % | 1.87 | % | ||||||||||

|

Net

(recoveries) charge-off’s to average loans (d)

|

(0.05 | ) % | 0.03 | % | 0.07 | % | 0.02 | % | 0.09 | % | ||||||||||

|

Statements of Financial Condition:

|

||||||||||||||||||||

|

Total assets

|

$ | 1,099,531 | $ | 779,618 | $ | 610,016 | $ | 477,355 | $ | 395,708 | ||||||||||

|

Gross portfolio loans (d)

|

929,762 | 632,012 | 530,050 | 369,294 | 288,425 | |||||||||||||||

|

Investment securities

|

76,463 | 42,413 | 46,412 | 94,972 | 58,152 | |||||||||||||||

|

Deposits

|

835,439 | 661,545 | 462,081 | 367,115 | 309,137 | |||||||||||||||

|

Borrowings

|

129,000 | 44,000 | 91,000 | 58,000 | 44,000 | |||||||||||||||

|

Total equity

|

129,210 | 69,485 | 51,534 | 49,188 | 40,354 | |||||||||||||||

|

Capital Ratios:

|

||||||||||||||||||||

|

Tier 1 capital to average assets (f)

|

||||||||||||||||||||

|

Bankwell Bank

|

11.12 | % | 7.91 | % | - | % | - | % | - | % | ||||||||||

|

The Bank of New Canaan

|

- | % | - | % | 7.88 | % | 8.71 | % | 8.15 | % | ||||||||||

|

The Bank of Fairfield

|

- | % | - | % | 8.39 | % | 11.30 | % | 13.25 | % | ||||||||||

|

Tier 1 capital to risk-weighted assets (f)

|

||||||||||||||||||||

|

Bankwell Bank

|

12.47 | % | 9.49 | % | - | % | - | % | - | % | ||||||||||

|

The Bank of New Canaan

|

- | % | - | % | 9.09 | % | 11.07 | % | 11.86 | % | ||||||||||

|

The Bank of Fairfield

|

- | % | - | % | 10.80 | % | 13.66 | % | 16.41 | % | ||||||||||

|

Total capital to risk-weighted assets (f)

|

||||||||||||||||||||

|

Bankwell Bank

|

13.55 | % | 10.74 | % | - | % | - | % | - | % | ||||||||||

|

The Bank of New Canaan

|

- | % | - | % | 10.34 | % | 12.33 | % | 13.12 | % | ||||||||||

|

The Bank of Fairfield

|

- | % | - | % | 12.05 | % | 14.91 | % | 17.10 | % | ||||||||||

|

Total shareholders’ equity to total assets

|

11.75 | % | 8.91 | % | 8.45 | % | 10.30 | % | 10.20 | % | ||||||||||

|

Tangible common equity ratio (b)

|

10.47 | % | 7.45 | % | 6.65 | % | 8.00 | % | 8.93 | % | ||||||||||

| (a) |

Excludes preferred stock and unvested restricted stock awards

|

| (b) |

This measure is not a measure recognized under GAAP and is therefore considered to be a non-GAAP financial measure. See “Non-GAAP Financial M easures” for a description of this measure and a reconciliation of this measure to its most directly comparable GAAP measure.

|

| (c) |

Calculated based on net income before preferred stock dividends

|

| (d) | Calculated using the principal amounts outstanding on loans |

| (e) |

Nonperforming assets consist of nonperforming loans and other real estate owned

|

| (f) |

Represents bank ratios. During 2013, The Bank of New Canaan and The Bank of Fairfield were merged into Bankwell Bank.

|

| 42 |

| 43 |

|

Years Ended December 31,

|

||||||||||||

|

2014

|

2013

|

2012

|

||||||||||

|

Efficiency Ratio

|

||||||||||||

|

Noninterest expense

|

$ | 25,812 | $ | 22,120 | $ | 17,858 | ||||||

|

Less: foreclosed real estate expenses

|

36 | 8 | 9 | |||||||||

|

Less: merger and acquisition expenses

|

1,801 | 908 | - | |||||||||

|

Adjusted noninterest expense (numerator)

|

$ | 23,975 | $ | 21,204 | $ | 17,849 | ||||||

|

Net interest income

|

$ | 31,660 | $ | 25,327 | $ | 21,205 | ||||||

|

Noninterest income

|

3,041 | 4,723 | 345 | |||||||||

|

Less: gains (losses) on sales of securities

|

- | 648 | (18 | ) | ||||||||

|

Less: gains on sale of foreclosed real estate

|

- | 64 | - | |||||||||

|

Less: gain on bargain purchase

|

- | 1,333 | - | |||||||||

|

Adjusted operating revenue (denominator)

|

$ | 34,701 | $ | 28,005 | $ | 21,568 | ||||||

|

Efficiency ratio

|

69.09 | % | 75.71 | % | 82.76 | % | ||||||

|

Tangible Common Equity and

|

||||||||||||

|

Tangible Common Equity/Tangible Assets

|

||||||||||||

|

Total shareholders' equity

|

$ | 129,210 | $ | 69,485 | $ | 51,534 | ||||||

|

Less: preferred stock

|

10,980 | 10,980 | 10,980 | |||||||||

|

Common shareholders' equity

|

118,230 | 58,505 | 40,554 | |||||||||

|

Less: Intangible assets

|

3,437 | 481 | - | |||||||||

|

Tangible Common shareholders' equity

|

$ | 114,793 | $ | 58,024 | $ | 40,554 | ||||||

|

Total assets

|

$ | 1,099,531 | $ | 779,618 | $ | 610,016 | ||||||

|

Less: Intangible assets

|

3,437 | 481 | - | |||||||||

|

Tangible assets

|

$ | 1,096,094 | $ | 779,137 | $ | 610,016 | ||||||

|

Tangible common shareholders' equity to tangible assets

|

10.47 | % | 7.45 | % | 6.65 | % | ||||||

|

Tangible Book Value per Share

|

||||||||||||

|

Total shareholders' equity

|

$ | 129,210 | $ | 69,485 | $ | 51,534 | ||||||

|

Less: preferred stock

|

10,980 | 10,980 | 10,980 | |||||||||

|

Common shareholders' equity

|

118,230 | 58,505 | 40,554 | |||||||||

|

Less: Intangible assets

|

3,437 | 481 | - | |||||||||

|

Tangible common shareholders' equity

|

$ | 114,793 | $ | 58,024 | $ | 40,554 | ||||||

|

Common shares issued

|

7,185,482 | 3,876,393 | 2,846,700 | |||||||||

|

Less: shares of unvested restricted stock

|

165,862 | 122,140 | 49,500 | |||||||||

|

Common shares outstanding

|

7,019,620 | 3,754,253 | 2,797,200 | |||||||||

|

Book value per share

|

$ | 16.84 | $ | 15.58 | $ | 14.50 | ||||||

|

Less: effects of intangible assets

|

0.49 | 0.12 | - | |||||||||

|

Tangible Book Value per Common Share

|

$ | 16.35 | $ | 15.46 | $ | 14.50 | ||||||

|

Total Revenue

|

||||||||||||

|

Net Interest income

|

$ | 31,660 | $ | 25,327 | $ | 21,205 | ||||||

|

Add: noninterest income

|

3,041 | 4,723 | 345 | |||||||||

|

Total Revenue

|

34,701 | 30,050 | 21,550 | |||||||||

|

Noninterest income as a percentage of total revenue

|

8.76 | % | 15.72 | % | 1.60 | % | ||||||

|

Return on Average Common Shareholders' Equity

|

||||||||||||

|

Net Income Attributable to Common Shareholders

|

$ | 4,458 | $ | 5,050 | $ | 1,082 | ||||||

|

Total average shareholders' equity

|

$ | 97,921 | $ | 63,142 | $ | 50,572 | ||||||

|

Less: average preferred stock

|

10,980 | 10,980 | 10,980 | |||||||||

|

Average common shareholders' equity

|

$ | 86,941 | $ | 52,162 | $ | 39,592 | ||||||

|

Return on Average Common Shareholders' Equity

|

5.13 | % | 9.68 | % | 2.73 | % | ||||||

| 44 |

| ● | Responsive, customer-centric products and services and a community focus; | |

| ● | Strategic acquisitions; | |

| ● | Utilization of efficient and scalable infrastructure; | |

| ● | Disciplined focus on risk management; and | |

| ● | Organic growth. |

| 45 |

| 46 |

|

Key Financial Measures (a)

|

||||||||||||

|

At or For the Years Ended December 31,

|

||||||||||||

|

(Dollars in thousands, except per share data)

|

2014

|

2013

|

2012

|

|||||||||

|

Selected balance sheet measures:

|

||||||||||||

|

Total assets

|

$ | 1,099,531 | $ | 779,618 | $ | 610,016 | ||||||

|

Gross portfolio loans (b)

|

929,762 | 632,012 | 530,050 | |||||||||

|

Deposits

|

835,439 | 661,545 | 462,081 | |||||||||

|

Borrowings

|

129,000 | 44,000 | 91,000 | |||||||||

|

Total equity

|

129,210 | 69,485 | 51,534 | |||||||||

|

|

||||||||||||

|

Total revenue (c)

|

34,701 | 30,050 | 21,550 | |||||||||

|

Net interest income before provision for loan losses

|

31,660 | 25,327 | 21,205 | |||||||||

|

Income before income tax

|

6,737 | 7,345 | 1,871 | |||||||||

|

Net income

|

4,568 | 5,161 | 1,214 | |||||||||

|

Basic earnings per share

|

0.78 | 1.46 | 0.39 | |||||||||

|

Diluted earnings per share

|

0.78 | 1.44 | 0.38 | |||||||||

|

Other financial measures and ratios:

|

||||||||||||

|

Return on average assets (d)

|

0.52 | % | 0.77 | % | 0.22 | % | ||||||

|

Return on average common shareholders' equity

|

5.13 | % | 9.68 | % | 2.73 | % | ||||||

|

Net interest margin

|

3.84 | % | 3.94 | % | 4.11 | % | ||||||

|

Efficiency ratio (c)

|

69.09 | % | 75.71 | % | 82.76 | % | ||||||

|

Tangible book value per share (end of period) (c) (e)

|

$ | 16.35 | $ | 15.46 | $ | 14.50 | ||||||

|

Net (recoveries) charge-off's to average loans (b)

|

(0.05 | )% | 0.03 | % | 0.07 | % | ||||||

|

Nonperforming assets to total assets (f)

|

0.39 | % | 0.23 | % | 0.81 | % | ||||||

|

Allowance for loan losses to nonperforming loans

|

323.02 | % | 835.69 | % | 200.84 | % | ||||||

|

Allowance for loan losses to total loans (b)

|

1.17 | % | 1.33 | % | 1.50 | % | ||||||

| (a) | We have derived the selected balance sheet measures as of December 31, 2014 and 2013 and the selected statement of income measures for the years ended December 31, 2014, 2013 and 2012 from our audited consolidated financial statements included elsewhere in this annual report. We have derived the selected balance sheet measures as of December 31, 2012 from our audited consolidated statement of financial condition not included in this annual report. Average balances have been computed using daily averages. Our historical results may not be indicative of our results for any future period. |

| (b) | Calculated using the principal amounts outstanding on loans. |

| (c) | This measure is not a measure recognized under GAAP and is therefore considered to be a non-GAAP financial measure. See "Non-GAAP Financial Measures" for a description of this measure and a reconciliation of this measure to its most directly comparable GAAP measure. |

| (d) | Calculated based on net income before preferred stock dividends. |

| (e) | Excludes preferred stock and unvested restricted stock awards. |

| (f) | Nonperforming assets consist of nonperforming loans and other real estate owned. |

| 47 |

| 48 |

| 49 |

| 50 |

2014 Earnings Overview

| 51 |

| 52 |

| 53 |

| 54 |

| Years Ended December 31, | ||||||||||||||||||||||||||||||||||||

| 2014 | 2013 | 2012 | ||||||||||||||||||||||||||||||||||

|

Average

|

Yield /

|

Average

|

Yield /

|

Average

|

Yield /

|

|||||||||||||||||||||||||||||||

|

(Dollars in thousands)

|

Balance

|

Interest

|

Rate

|

Balance

|

Interest

|

Rate

|

Balance

|

Interest

|

Rate

|

|||||||||||||||||||||||||||

|

Assets:

|

||||||||||||||||||||||||||||||||||||

|

Cash and Fed funds sold

|

$ | 49,152 | $ | 127 | 0.26 | % | $ | 35,599 | $ | 84 | 0.24 | % | $ | 16,933 | $ | 35 | 0.21 | % | ||||||||||||||||||

|

Securities (1)

|

61,398 | 2,424 | 3.95 | 40,932 | 1,766 | 4.31 | 56,321 | 2,366 | 4.20 | |||||||||||||||||||||||||||

|

Loans:

|

||||||||||||||||||||||||||||||||||||

|

Commercial real estate

|

378,345 | 18,515 | 4.83 | 299,142 | 15,124 | 5.06 | 236,934 | 12,919 | 5.45 | |||||||||||||||||||||||||||

|

Residential real estate

|

164,598 | 5,911 | 3.59 | 152,498 | 5,577 | 3.66 | 119,960 | 4,826 | 4.02 | |||||||||||||||||||||||||||

|

Construction (2)

|

49,212 | 2,300 | 4.61 | 38,073 | 1,763 | 4.63 | 34,177 | 1,752 | 5.13 | |||||||||||||||||||||||||||

|

Commercial business

|

109,121 | 5,496 | 4.97 | 69,252 | 3,699 | 5.34 | 44,220 | 2,370 | 5.36 | |||||||||||||||||||||||||||

|

Home equity

|

14,529 | 564 | 3.88 | 11,287 | 423 | 3.74 | 12,789 | 465 | 3.64 | |||||||||||||||||||||||||||

|

Consumer

|

1,270 | 81 | 6.35 | 308 | 18 | 5.98 | 80 | 10 | 12.50 | |||||||||||||||||||||||||||

|

Acquired Loan Portfolio Non accrual loans (net of mark)

|

2,707 | 545 | 20.14 | - | - | - | - | - | - | |||||||||||||||||||||||||||

|

Total loans

|

719,782 | 33,412 | 4.59 | 570,560 | 26,604 | 4.66 | 448,160 | 22,342 | 4.99 | |||||||||||||||||||||||||||

|

Federal Home Loan Bank stock

|

5,078 | 73 | 1.45 | 4,624 | 17 | 0.36 | 3,615 | 18 | 0.49 | |||||||||||||||||||||||||||

|

Total earning assets

|

835,410 | $ | 36,036 | 4.25 | % | 651,715 | $ | 28,471 | 4.37 | % | 525,029 | $ | 24,761 | 4.72 | % | |||||||||||||||||||||

|

Other assets

|

43,535 | 17,782 | 16,297 | |||||||||||||||||||||||||||||||||

|

Total assets

|

$ | 878,945 | $ | 669,497 | $ | 541,326 | ||||||||||||||||||||||||||||||

|

Liabilities and shareholders’ equity:

|

||||||||||||||||||||||||||||||||||||

|

Interest -bearing liabilities:

|

||||||||||||||||||||||||||||||||||||

|

NOW

|

$ | 53,041 | 58 | 0.11 | % | $ | 40,554 | 49 | 0.12 | % | $ | 31,490 | 45 | 0.14 | % | |||||||||||||||||||||

|

Money market

|

182,676 | 836 | 0.46 | 116,323 | 498 | 0.45 | 90,342 | 612 | 0.68 | |||||||||||||||||||||||||||

|

Savings

|

91,058 | 302 | 0.33 | 117,388 | 543 | 0.46 | 102,641 | 846 | 0.82 | |||||||||||||||||||||||||||

|

Time

|

238,710 | 2,099 | 0.88 | 158,996 | 1,143 | 0.72 | 122,350 | 864 | 0.71 | |||||||||||||||||||||||||||

|

Total interest-bearing deposits

|

565,485 | 3,295 | 0.58 | 433,261 | 2,233 | 0.43 | 346,823 | 2,367 | 0.56 | |||||||||||||||||||||||||||

|

Borrowed Money

|

65,953 | 634 | 0.96 | 69,912 | 532 | 0.73 | 61,836 | 825 | 1.33 | |||||||||||||||||||||||||||

|

Total interest bearing liabilities

|

631,438 | $ | 3,929 | 0.62 | % | 503,173 | $ | 2,765 | 0.47 | % | 408,659 | $ | 3,192 | 0.66 | % | |||||||||||||||||||||

|

Noninterest-bearing deposits

|

136,748 | 96,009 | 78,453 | |||||||||||||||||||||||||||||||||

|

Other liabilities

|

12,838 | 7,173 | 3,642 | |||||||||||||||||||||||||||||||||

|

Total Liabilities

|

781,024 | 606,355 | 490,754 | |||||||||||||||||||||||||||||||||

|

Shareholders’ equity

|

97,921 | 63,142 | 50,572 | |||||||||||||||||||||||||||||||||

|

Total liabilities and shareholders’

equity

|

$ | 878,945 | $ | 669,497 | $ | 541,326 | ||||||||||||||||||||||||||||||

|

Net interest income (3)

|

$ | 32,107 | $ | 25,706 | $ | 21,569 | ||||||||||||||||||||||||||||||

|

Interest rate spread

|

3.63 | % | 3.90 | % | 4.06 | % | ||||||||||||||||||||||||||||||

|

Net interest margin (4)

|

3.84 | % | 3.94 | % | 4.11 | % | ||||||||||||||||||||||||||||||

|

(1)

|

Average balances and yields for securities are based on amortized cost

|

|

|

(2)

|

Includes commercial and residential real estate construction loans

|

|

|

(3)

|

The adjustment for securities and loans taxable equivalency was $447 thousand, $379 thousand and $364 thousand, respectively, for the years ended December 31, 2014, 2013 and 2012.

|

|

|

(4)

|

Net interest income as a percentage of total earning assets

|

|

| 55 |

| Year Ended | Year Ended | |||||||||||||||||||||||

|

December 31, 2014 vs 2013

|

December 31, 2013 vs 2012

|

|||||||||||||||||||||||

|

Increase (Decrease)

|

Increase (Decrease)

|

|||||||||||||||||||||||

|

(In thousands)

|

Volume

|

Rate

|

Total

|

Volume

|

Rate

|

Total

|

||||||||||||||||||

|

Interest and dividend income:

|

||||||||||||||||||||||||

|

Cash and Fed funds sold

|

$ | 35 | $ | 9 | $ | 44 | $ | 44 | $ | 5 | $ | 49 | ||||||||||||

|

Securities

|

818 | (161 | ) | 657 | (662 | ) | 62 | (600 | ) | |||||||||||||||

|

Loans:

|

||||||||||||||||||||||||

|

Commercial real estate

|

3,904 | (513 | ) | 3,391 | 3,198 | (993 | ) | 2,205 | ||||||||||||||||

|

Residential real estate

|

436 | (102 | ) | 334 | 1,220 | (469 | ) | 751 | ||||||||||||||||

|

Construction

|

520 | 17 | 537 | 189 | (178 | ) | 11 | |||||||||||||||||

|

Commercial business

|

2,026 | (229 | ) | 1,797 | 1,337 | (8 | ) | 1,329 | ||||||||||||||||

|

Home equity

|

125 | 16 | 141 | (56 | ) | 14 | (42 | ) | ||||||||||||||||

|

Consumer

|

61 | 1 | 62 | 16 | (8 | ) | 8 | |||||||||||||||||

|

Acquired Non accrual loans (net of mark)

|

545 | - | 545 | - | - | - | ||||||||||||||||||

|

Total loans

|

7,617 | (810 | ) | 6,807 | 5,904 | (1,642 | ) | 4,262 | ||||||||||||||||

|

Federal Home Loan Bank stock

|

2 | 55 | 57 | 4 | (5 | ) | (1 | ) | ||||||||||||||||

|

Total change in interest and

dividend income

|

8,472 | (907 | ) | 7,565 | 5,290 | (1,580 | ) | 3,710 | ||||||||||||||||

|

Interest expense:

|

||||||||||||||||||||||||

|

Deposits:

|

||||||||||||||||||||||||

|

NOW

|

14 | (5 | ) | 9 | 12 | (8 | ) | 4 | ||||||||||||||||

|

Money market

|

303 | 35 | 338 | 148 | (262 | ) | (114 | ) | ||||||||||||||||

|

Savings

|

(106 | ) | (135 | ) | (241 | ) | 108 | (411 | ) | (303 | ) | |||||||||||||

|

Time

|

662 | 294 | 956 | 263 | 16 | 279 | ||||||||||||||||||

|

Total deposits

|

873 | 189 | 1,062 | 531 | (665 | ) | (134 | ) | ||||||||||||||||

|

Borrowed Money

|

(30 | ) | 132 | 102 | 97 | (390 | ) | (293 | ) | |||||||||||||||

|

Total change in interest expense

|

843 | 321 | 1,164 | 628 | (1,055 | ) | (427 | ) | ||||||||||||||||

|

Change in net interest income

|

$ | 7,629 | $ | (1,228 | ) | $ | 6,401 | $ | 4,662 | $ | (525 | ) | $ | 4,137 | ||||||||||

| 56 |

| Years Ended | 2014/2013 | 2013/2012 | ||||||||||||||||||||||||||

| December 31, |

Change

|

Change

|

||||||||||||||||||||||||||

|

(Dollars in thousands)

|

2014

|

2013

|

2012

|

$ | % | $ | % | |||||||||||||||||||||

|

Gains and fees from sales of loans

|

$ | 1,313 | $ | 2,020 | $ | 18 | $ | (707 | ) | (35 | ) % | $ | 2,002 | 11,122 | % | |||||||||||||

|

Service charges and fees

|

643 | 416 | 314 | 227 | 55 | 102 | 32 | |||||||||||||||||||||

|

Bank owned life insurance

|

497 | 31 | - | 466 | 1,503 | 31 | 100 | |||||||||||||||||||||

|

Net gain on sale of available for sale securities

|

- | 648 | (18 | ) | (648 | ) | (100 | ) | 666 | 3,700 | ||||||||||||||||||

|

Gain (loss) on sale of foreclosed

real estate, net

|

- | 64 | - | (64 | ) | (100 | ) | 64 | 100 | |||||||||||||||||||

|

Gain on bargain purchase

|

- | 1,333 | - | (1,333 | ) | (100 | ) | 1,333 | 100 | |||||||||||||||||||

|

Other

|

588 | 211 | 31 | 377 | 179 | 180 | 581 | |||||||||||||||||||||

|

Total noninterest income

|

$ | 3,041 | $ | 4,723 | $ | 345 | $ | (1,682 | ) | (36 | ) % | $ | 4,378 | 1,269 | % | |||||||||||||

| 57 |

| 58 |

| Years Ended | 2014/2013 | 2013/2012 | ||||||||||||||||||||||||||

| December 31, |

Change

|

Change

|

||||||||||||||||||||||||||

|

(Dollars in thousands)

|

2014

|

2013

|

2012

|

$ | % | $ | % | |||||||||||||||||||||

|

Salaries and employee benefits

|

$ | 13,534 | $ | 11,578 | $ | 9,451 | $ | 1,956 | 17 | % | $ | 2,127 | 23 | % | ||||||||||||||

|

Occupancy and equipment

|

4,422 | 3,420 | 3,004 | 1,002 | 29 | 416 | 14 | |||||||||||||||||||||

|

Merger and acquisition related expenses

|

1,801 | 908 | - | 893 | 98 | 908 | 100 | |||||||||||||||||||||

|

Data processing

|

1,289 | 1,349 | 1,209 | (60 | ) | (4 | ) | 140 | 12 | |||||||||||||||||||

|

Professional services

|

1,194 | 1,595 | 1,546 | (401 | ) | (25 | ) | 49 | 3 | |||||||||||||||||||

|

Marketing

|

674 | 927 | 333 | (253 | ) | (27 | ) | 594 | 178 | |||||||||||||||||||

|

Director fees

|

650 | 330 | 381 | 320 | 97 | (51 | ) | (13 | ) | |||||||||||||||||||

|

FDIC insurance

|

488 | 333 | 365 | 155 | 47 | (32 | ) | (9 | ) | |||||||||||||||||||

|

Amortization of intangibles

|

133 | 18 | - | 115 | 639 | 18 | 100 | |||||||||||||||||||||

|

Foreclosed real estate

|

36 | 8 | 9 | 28 | 350 | (1 | ) | (11 | ) | |||||||||||||||||||

|

Other

|

1,591 | 1,654 | 1,560 | (63 | ) | (4 | ) | 94 | 6 | |||||||||||||||||||

|

Total noninterest expense

|

$ | 25,812 | $ | 22,120 | $ | 17,858 | $ | 3,692 | 17 | % | $ | 4,262 | 24 | % | ||||||||||||||

| 59 |

| 60 |

| 61 |

|

(In thousands)

|

2014

|

2013

|

Change

|

|||||||||||||||||

|

Total

|

%

|

Total

|

%

|

|||||||||||||||||

|

Real estate loans:

|

||||||||||||||||||||

|

Residential

|

$ | 175,031 | 18.83 | % | $ | 155,874 | 24.66 | % | $ | 19,157 | ||||||||||

|

Commercial

|

521,181 | 56.06 | 316,533 | 50.08 | 204,648 | |||||||||||||||

|

Construction

|

63,229 | 6.80 | 51,545 | 8.16 | 11,684 | |||||||||||||||

|

Home equity

|

18,166 | 1.95 | 13,892 | 2.20 | 4,274 | |||||||||||||||

| 777,607 | 83.64 | 537,844 | 85.10 | 239,763 | ||||||||||||||||

|

Commercial business

|

149,259 | 16.05 | 93,566 | 14.80 | 55,693 | |||||||||||||||

|

Consumer

|

2,896 | 0.31 | 602 | 0.10 | 2,294 | |||||||||||||||

|

Total loans

|

$ | 929,762 | 100.00 | % | $ | 632,012 | 100.00 | % | $ | 297,750 | ||||||||||

| 62 |

| December 31, 2014 | ||||||||||||||||

|

Commercial

|

Commercial |

Commercial

|

||||||||||||||

|

(In thousands)

|

Real Estate

|

Construction

|

Business

|

Total

|

||||||||||||

|

Amounts due:

|

||||||||||||||||

|

One Year or less

|

$ | 15,694 | $ | 13,322 | $ | 25,918 | $ | 54,934 | ||||||||

|

After one year:

|

||||||||||||||||

|

One to five years

|

100,506 | 13,224 | 58,834 | 172,564 | ||||||||||||

|

Over five years

|

404,981 | 22,335 | 64,507 | 491,823 | ||||||||||||

|

Total due after one year

|

505,487 | 35,559 | 123,341 | 664,387 | ||||||||||||

|

Total

|

$ | 521,181 | $ | 48,881 | $ | 149,259 | $ | 719,321 | ||||||||

| 63 |

|

December 31, 2014

|

||||||||||||

|

Adjustable

|

Fixed Interest

|

|||||||||||

|

(In thousands)

|

Interest Rate

|

Rate

|

Total

|

|||||||||

|

Commercial Real Estate

|

$ | 209,905 | $ | 295,582 | $ | 505,487 | ||||||

|

Construction

|

3,359 | 32,200 | 35,559 | |||||||||

|

Commercial Business

|

45,484 | 77,857 | 123,341 | |||||||||

|

Total loans due after one year

|

$ | 258,748 | $ | 405,639 | $ | 664,387 | ||||||

| 64 |

| At December 31, | ||||||||||||||||||||

|

(In thousands)

|

2014

|

2013

|

2012

|

2011

|

2010

|

|||||||||||||||

|

Nonaccrual loans:

|

||||||||||||||||||||

|

Real estate loans:

|

||||||||||||||||||||

|

Residential

|

$ | - | $ | 1,003 | $ | 2,137 | $ | 2,166 | $ | 974 | ||||||||||

|

Commercial

|

3,220 | - | 1,817 | 307 | - | |||||||||||||||

|

Construction

|

- | - | - | 1,175 | 1,300 | |||||||||||||||

|

Home equity

|

- | - | - | 90 | - | |||||||||||||||

|

Commercial business

|

142 | - | - | - | - | |||||||||||||||

|

Total non accrual loans

|

3,362 | 1,003 | 3,954 | 3,738 | 2,274 | |||||||||||||||

|

Property acquired through foreclosure

or repossession, net

|

950 | 829 | 962 | - | - | |||||||||||||||

|

Total nonperforming assets

|

$ | 4,312 | $ | 1,832 | $ | 4,916 | $ | 3,738 | $ | 2,274 | ||||||||||

|

Nonperforming assets to total assets

|

0.39 | % | 0.23 | % | 0.81 | % | 0.78 | % | 0.57 | % | ||||||||||

|

Nonaccrual loans to total loans

|

0.36 | % | 0.16 | % | 0.75 | % | 1.01 | % | 0.79 | % | ||||||||||

|

Total past due loans to total loans

|

0.86 | % | 0.73 | % | 0.75 | % | 1.01 | % | 0.79 | % | ||||||||||

|

Accruing loans 90 days or more past due

|

$ | 1,998 | $ | 3,620 | $ | - | $ | - | $ | - | ||||||||||

| 65 |

| 66 |

|

31-60 Days

|

61-90 Days

|

Greater Than

|

Total Past

|

|||||||||||||

|

(In thousands)

|

Past Due

|

Past Due

|

90 Days

|

Due

|

||||||||||||

|

As of December 31, 2014

|

||||||||||||||||

|

Originated Loans

|

||||||||||||||||

|

Residential real estate

|

$ | - | $ | - | $ | - | $ | - | ||||||||

|

Commercial real estate

|

- | - | 3,436 | 3,436 | ||||||||||||

|

Commercial business

|

- | - | - | - | ||||||||||||

|

Consumer

|

- | - | - | - | ||||||||||||

|

Total originated loans

|

- | - | 3,436 | 3,436 | ||||||||||||

|

Acquired Loans

|

||||||||||||||||

|

Residential real estate

|

339 | - | 294 | 633 | ||||||||||||

|

Commercial real estate

|

685 | 677 | 836 | 2,198 | ||||||||||||

|

Construction

|

- | - | 835 | 835 | ||||||||||||

|

Home Equity

|

- | 40 | - | 40 | ||||||||||||

|

Commercial business

|

178 | 386 | 305 | 869 | ||||||||||||

|

Consumer

|

3 | - | - | 3 | ||||||||||||

|

Total acquired loans

|

1,205 | 1,103 | 2,270 | 4,578 | ||||||||||||

|

Total loans

|

$ | 1,205 | $ | 1,103 | $ | 5,706 | $ | 8,014 | ||||||||

|

As of December 31, 2013

|

||||||||||||||||

|

Originated Loans

|

||||||||||||||||

|

Residential real estate

|

$ | - | $ | - | $ | 1,003 | $ | 1,003 | ||||||||

|

Total originated loans

|

- | - | 1,003 | 1,003 | ||||||||||||

|

Acquired Loans

|

||||||||||||||||

|

Commercial real estate

|

- | - | 797 | 797 | ||||||||||||

|

Construction

|

- | - | 2,508 | 2,508 | ||||||||||||

|

Commercial business

|

- | - | 315 | 315 | ||||||||||||

|

Total acquired loans

|

- | - | 3,620 | 3,620 | ||||||||||||

|

Total loans

|

$ | - | $ | - | $ | 4,623 | $ | 4,623 | ||||||||

| 67 |

| December 31, | ||||||||||||||||||||

|

(In thousands)

|

2014

|

2013

|

2012

|

2011

|

2010

|

|||||||||||||||

|

Accruing troubled debt restructured loans:

|

||||||||||||||||||||

|

Residential real estate

|

$ | 1,965 | $ | 864 | $ | 864 | $ | - | $ | - | ||||||||||

|

Commercial real estate

|

216 | - | 194 | 203 | 2,218 | |||||||||||||||

|

Construction

|

- | - | - | - | 1,415 | |||||||||||||||

|

Home equity

|

92 | 97 | - | - | - | |||||||||||||||

|

Commercial business

|

1,338 | 642 | 794 | 57 | - | |||||||||||||||

|

Accruing troubled debt restructured loans

|

3,611 | 1,603 | 1,852 | 260 | 3,633 | |||||||||||||||

|

Nonaccrual troubled debt restructured loans:

|

||||||||||||||||||||

|

Commercial real estate

|

- | - | - | - | - | |||||||||||||||

|

Nonaccrual troubled debt restructured loans

|

- | - | - | - | - | |||||||||||||||

|

Total troubled debt restructured loans

|

$ | 3,611 | $ | 1,603 | $ | 1,852 | $ | 260 | $ | 3,633 | ||||||||||

| 68 |

| 69 |

| December 31, | ||||||||||||||||||||

|

(Dollars in thousands)

|

2014

|

2013

|

2012

|

2011

|

2010

|

|||||||||||||||

|

Balance at beginning of period

|

$ | 8,382 | $ | 7,941 | $ | 6,425 | $ | 5,440 | $ | 4,380 | ||||||||||

|

Charge-offs:

|

||||||||||||||||||||

|

Residential real estate

|

- | - | (261 | ) | - | - | ||||||||||||||

|

Commercial real estate

|

- | (166 | ) | - | - | - | ||||||||||||||

|

Construction

|

(100 | ) | - | (60 | ) | (84 | ) | (254 | ) | |||||||||||

|

Home equity

|

- | - | - | - | - | |||||||||||||||

|

Consumer

|

(3 | ) | (4 | ) | (5 | ) | - | (6 | ) | |||||||||||

|

Total charge-offs

|

(103 | ) | (170 | ) | (326 | ) | (84 | ) | (260 | ) | ||||||||||

|

Recoveries:

|

||||||||||||||||||||

|

Consumer

|

425 | 26 | 21 | 20 | 9 | |||||||||||||||

|

Commercial Business

|

4 | - | - | - | - | |||||||||||||||

|

Total recoveries

|

429 | 26 | 21 | 20 | 9 | |||||||||||||||

|

Net (recoveries) charge-offs

|

(326 | ) | 144 | 305 | 64 | 251 | ||||||||||||||

|

Provision charged to earnings

|

2,152 | 585 | 1,821 | 1,049 | 1,311 | |||||||||||||||

|

Balance at end of period

|

$ | 10,860 | $ | 8,382 | $ | 7,941 | $ | 6,425 | $ | 5,440 | ||||||||||

|

Net (recoveries) charge-offs to average loans

|

(0.05 | )% | 0.03 | % | 0.07 | % | 0.02 | % | 0.09 | % | ||||||||||

|

Allowance for loan losses to total loans

|

1.17 | % | 1.33 | % | 1.50 | % | 1.74 | % | 1.87 | % | ||||||||||

| 70 |

| At December 31, | ||||||||||||||||||||||||

|

2014

|

2013

|

2012

|

||||||||||||||||||||||

|

Percent of

|

Percent of

|

Percent of

|

||||||||||||||||||||||

|

Loan

|

Loan

|

Loan

|

||||||||||||||||||||||

|

(Dollars in thousands)

|

Amount

|

Portfolio

|

Amount

|

Portfolio

|

Amount

|

Portfolio

|

||||||||||||||||||

|

Residential real estate

|

$ | 1,431 | 18.83 | % | $ | 1,310 | 24.66 | % | $ | 1,230 | 27.22 | % | ||||||||||||

|

Commercial real estate

|

5,480 | 56.06 | 3,616 | 49.96 | 3,842 | 53.73 | ||||||||||||||||||

|

Construction

|

1,102 | 6.80 | 1,032 | 8.15 | 929 | 6.25 | ||||||||||||||||||

|

Home equity

|

205 | 1.95 | 190 | 2.14 | 220 | 2.08 | ||||||||||||||||||

|

Commercial business

|

2,638 | 16.05 | 2,225 | 14.96 | 1,718 | 10.71 | ||||||||||||||||||

|

Consumer

|

4 | 0.31 | 9 | 0.13 | 2 | 0.01 | ||||||||||||||||||

|

Unallocated

|

- | - | - | - | - | - | ||||||||||||||||||

|

Total allowance for loan losses

|

$ | 10,860 | 100.00 | % | $ | 8,382 | 100.00 | % | $ | 7,941 | 100.00 | % | ||||||||||||

| At December 31, | ||||||||||||||||

|

2011

|

2010

|

|||||||||||||||

|

Percent of

|

Percent of

|

|||||||||||||||

|

Loan

|

Loan

|

|||||||||||||||

|

(Dollars in thousands)

|

Amount

|

Portfolio

|

Amount

|

Portfolio

|

||||||||||||

|

Residential real estate

|

$ | 1,290 | 28.37 | % | $ | 1,053 | 36.08 | % | ||||||||

|

Commercial real estate

|

2,519 | 47.10 | 1,806 | 38.58 | ||||||||||||

|

Construction

|

1,007 | 10.95 | 951 | 13.20 | ||||||||||||

|

Home equity

|

274 | 4.01 | 313 | 5.77 | ||||||||||||

|

Commercial business

|

1,317 | 9.49 | 744 | 6.14 | ||||||||||||

|

Consumer

|

11 | 0.08 | 20 | 0.23 | ||||||||||||

|

Unallocated

|

7 | - | 553 | - | ||||||||||||

|

Total allowance for loan losses

|

$ | 6,425 | 100.00 | % | $ | 5,440 | 100.00 | % | ||||||||

| 71 |

| December 31, | ||||||||||||||||||||||||

|

2014

|

2013

|

2012

|

||||||||||||||||||||||

|

Amortized

|

Fair

|

Amortized

|

Fair

|

Amortized

|

Fair

|

|||||||||||||||||||

|

(In thousands)

|

Cost

|

Value

|

Cost

|

Value

|

Cost

|

Value

|

||||||||||||||||||

|

Securities available for sale:

|

||||||||||||||||||||||||

|

U.S Government and agency obligations

|

$ | 24,554 | $ | 24,418 | $ | 5,997 | $ | 5,688 | $ | 5,997 | $ | 6,005 | ||||||||||||

|

State agency and municipal obligations

|

17,797 | 18,584 | 11,605 | 12,132 | 17,036 | 18,531 | ||||||||||||||||||

|

Corporate bonds

|

16,035 | 16,325 | 9,166 | 9,566 | 13,681 | 14,556 | ||||||||||||||||||

|

Government mortgage-backed securities

|

5,567 | 5,682 | 1,133 | 1,211 | 1,872 | 1,966 | ||||||||||||||||||

|

Total securities available for sale

|

$ | 63,953 | $ | 65,009 | $ | 27,901 | $ | 28,597 | $ | 38,586 | $ | 41,058 | ||||||||||||

|

Securities held to maturity:

|

||||||||||||||||||||||||

|

U.S Government and agency obligations

|

$ | 1,010 | $ | 1,010 | $ | 1,021 | $ | 1,019 | $ | - | $ | - | ||||||||||||

|

State agency and municipal obligations

|

9,179 | 9,179 | 11,461 | 11,461 | 3,903 | 3,903 | ||||||||||||||||||

|

Corporate bonds

|

1,000 | 985 | 1,000 | 973 | 1,000 | 904 | ||||||||||||||||||

|

Government mortgage-backed securities

|

265 | 296 | 334 | 362 | 451 | 485 | ||||||||||||||||||

|

Total securities held to maturity

|

$ | 11,454 | $ | 11,470 | $ | 13,816 | $ | 13,815 | $ | 5,354 | $ | 5,292 | ||||||||||||

| 72 |

|

At December 31, 2014

|

Due Within 1 Year

|

Due 1 - 5 Years

|

Due 5 - 10 Years

|

Due After 10 Years

|

||||||||||||||||||||||||||||

|

(In thousands)

|

Amortized Cost

|

Yield

|

Amortized Cost

|

Yield

|

Amortized Cost

|

Yield

|

Amortized Cost

|

Yield

|

||||||||||||||||||||||||

|

Securities available for sale:

|

||||||||||||||||||||||||||||||||

|

U.S Government and agency obligations

|

$ | 497 | 2.24 | % | $ | 3,998 | 1.43 | % | $ | 17,055 | 2.50 | % | $ | 3,004 | 2.56 | % | ||||||||||||||||

|

State agency and municipal obligations

|

- | - | - | - | 9,297 | 3.13 | 8,500 | 3.83 | ||||||||||||||||||||||||

|

Corporate bonds

|

5,764 | 1.77 | 4,150 | 4.26 | 6,121 | 2.38 | - | - | ||||||||||||||||||||||||

|

Government mortgage-backed securities

|

- | - | 99 | 2.64 | - | - | 5,468 | 2.36 | ||||||||||||||||||||||||

|

Total securities available for sale

|

$ | 6,261 | 1.81 | % | $ | 8,247 | 2.87 | % | $ | 32,473 | 2.66 | % | $ | 16,972 | 3.13 | % | ||||||||||||||||

|

Securities held to maturity:

|

||||||||||||||||||||||||||||||||

|

U.S Government and agency obligations

|

$ | 1,010 | 0.27 | % | $ | - | - | % | $ | - | - | % | $ | - | - | % | ||||||||||||||||

|

State agency and municipal obligations

|

- | - | - | - | - | - | 9,179 | 4.50 | ||||||||||||||||||||||||

|

Corporate bonds

|

- | - | - | - | 1,000 | 2.69 | - | - | ||||||||||||||||||||||||

|

Government mortgage-backed securities

|

- | - | - | - | - | - | 265 | 5.06 | ||||||||||||||||||||||||

|

Total securities held to maturity

|

$ | 1,010 | 0.27 | % | $ | - | - | % | $ | 1,000 | 2.69 | % | $ | 9,444 | 4.52 | % | ||||||||||||||||

|

At December 31, 2013

|

Due Within 1 Year

|

Due 1 - 5 Years

|

Due 5 - 10 Years

|

Due After 10 Years

|

||||||||||||||||||||||||||||

|

(In thousands)

|

Amortized Cost

|

Yield

|

Amortized Cost

|

Yield

|

Amortized Cost

|

Yield

|

Amortized Cost

|

Yield

|

||||||||||||||||||||||||

|

Securities available for sale:

|

||||||||||||||||||||||||||||||||

|

U.S Government and agency obligations

|

$ | - | - | % | $ | 1,000 | 1.29 | % | $ | 4,997 | 1.51 | % | $ | - | - | % | ||||||||||||||||

|

State agency and municipal obligations

|

- | - | - | - | 3,125 | 4.07 | 8,480 | 4.20 | ||||||||||||||||||||||||

|

Corporate bonds

|

- | - | 9,166 | 4.28 | - | - | - | - | ||||||||||||||||||||||||

|

Government mortgage-backed securities

|

- | - | - | - | - | - | 1,133 | 5.23 | ||||||||||||||||||||||||

|

Total securities available for sale

|

$ | - | - | % | $ | 10,166 | 3.99 | % | $ | 8,122 | 2.49 | % | $ | 9,613 | 4.32 | % | ||||||||||||||||

|

Securities held to maturity:

|

||||||||||||||||||||||||||||||||

|

U.S Government and agency obligations

|

$ | - | - | % | $ | 1,021 | 1.38 | % | $ | - | - | % | $ | - | - | % | ||||||||||||||||

|

State agency and municipal obligations

|

- | - | - | - | - | - | 11,461 | 4.50 | ||||||||||||||||||||||||

|

Corporate bonds

|

- | - | - | - | 1,000 | 2.90 | - | - | ||||||||||||||||||||||||

|

Government mortgage-backed securities

|

- | - | - | - | - | - | 334 | 5.50 | ||||||||||||||||||||||||

|

Total securities held to maturity

|

$ | - | - | % | $ | 1,021 | 1.38 | % | $ | 1,000 | 2.90 | % | $ | 11,795 | 4.53 | % | ||||||||||||||||

| 73 |

|

At December 31,

|

||||||||||||||||||||||||

|

2014

|

2013

|

|||||||||||||||||||||||

|

Weighted

|

Weighted

|

|||||||||||||||||||||||

|

Average

|

Average

|

|||||||||||||||||||||||

|

(Dollars in thousands)

|

Amount

|

Percent

|

Rate

|

Amount

|

Percent

|

Rate

|

||||||||||||||||||

|

Noninterest-bearing demand

|

$ | 166,030 | 19.87 | % | - | % | $ | 118,618 | 17.93 | % | - | % | ||||||||||||

|

NOW

|

60,321 | 7.22 | 0.11 | 73,652 | 11.13 | 0.12 | ||||||||||||||||||

|

Money Market

|

216,180 | 25.88 | 0.46 | 164,579 | 24.88 | 0.45 | ||||||||||||||||||

|

Savings

|

84,457 | 10.11 | 0.33 | 107,692 | 16.28 | 0.46 | ||||||||||||||||||

|

Time

|

308,451 | 36.92 | 0.88 | 197,004 | 29.78 | 0.72 | ||||||||||||||||||

|

Total Deposits

|

$ | 835,439 | 100.00 | % | 0.58 | % | $ | 661,545 | 100.00 | % | 0.43 | % | ||||||||||||

| 74 |

|

2012

|

||||||||||||

|

Weighted

|

||||||||||||

|

Average

|

||||||||||||

|

(Dollars in thousands)

|

Amount

|

Percent

|

Rate

|

|||||||||

|

Noninterest-bearing demand

|

$ | 78,120 | 16.91 | % | - | % | ||||||

|

NOW

|

33,722 | 7.30 | 0.14 | |||||||||

|

Money Market

|

94,090 | 20.36 | 0.68 | |||||||||

|

Savings

|

136,101 | 29.45 | 0.82 | |||||||||

|

Time

|

120,048 | 25.98 | 0.71 | |||||||||

|

Total Deposits

|

$ | 462,081 | 100.00 | % | 0.56 | % | ||||||

|

December 31,

|

||||||||

|

(Dollars in

thousands)

|

2014

|

2013

|

||||||

|

Maturing:

|

||||||||

|

Within 3

months

|

$ | 47,918 | $ | 71,221 | ||||

|

After 3 but within 6 months

|

49,511 | 22,236 | ||||||

|

After 6

months but within 1 year

|

92,502 | 40,204 | ||||||

|

After 1 year

|

49,885 | 17,152 | ||||||

|

Total

|

$ | 239,816 | $ | 150,813 | ||||

| 75 |

|

(Dollars in

thousands)

|

Year Ended December 31, | |||||||||||

|

As of and for

the period ending:

|

2014

|

2013

|

2012

|

|||||||||

|

Average

amount outstanding during the period

|

$ | 37,129 | $ | 39,167 | $ | 29,250 | ||||||

|

Amount outstanding at end of period

|

107,000 | 12,000 | 51,000 | |||||||||

|

Highest

month end balance during the period

|

107,000 | 60,000 | 51,000 | |||||||||

|

Weighted

average interest rate at end of period

|

0.26 | % | 0.41 | % | 0.21 | % | ||||||

|

Weighted

average interest rate during the period

|

0.23 | % | 0.28 | % | 0.23 | % | ||||||

|

Notional

|

Fair

|

||||||||||||||||

|

(Dollars in thousands)

|

Amount

|

Maturity

|

Received

|

Paid

|

Value

|

||||||||||||

|

Cash flow hedge:

|

|||||||||||||||||

|

Interest rate swap on FHLB advance

|

$ | 25,000 |

4.7 years

|

0.26 | % | 1.62 | % | $ | (73 | ) | |||||||

|

Interest rate swap on forward -starting FHLB advance

|

$ | 25,000 |

5.0 years

|

0.26 | % | 1.83 | % | $ | (113 | ) | |||||||

| 76 |

| 77 |

|

(in thousands)

|

Payments Due by Period

|

|||||||||||||||||||

|

Less Than

|

1-3 | 4-5 |

After

|

|||||||||||||||||

|

Contractual Obligations:

|

Total

|

1 Year

|

Years

|

Years

|

5 Years

|

|||||||||||||||

|

FHLB advances

|

$ | 129,000 | $ | 109,000 | $ | 20,000 | $ | - | $ | - | ||||||||||

|

Operating lease agreements

|

9,286 | 1,788 | 2,926 | 1,636 | 2,936 | |||||||||||||||

|

Time deposits with stated maturity dates

|

308,451 | 244,674 | 44,119 | 19,658 | - | |||||||||||||||

|

Total contractual obligations

|

$ | 446,737 | $ | 355,462 | $ | 67,045 | $ | 21,294 | $ | 2,936 | ||||||||||

| 78 |

|

As of December 31, 2014

|

||||||||||||||||||||

|

(in thousands)

|

Amount of Commitment Expiration per Period | |||||||||||||||||||

|

Less Than

|

1-3 | 4-5 |

After

|

|||||||||||||||||

|

Other Commitments:

|

Total

|

1 Year

|

Years

|

Years

|

5 Years

|

|||||||||||||||

|

Loan Commitments

|

$ | 83,013 | $ | 52,370 | $ | 14,791 | $ | 2,556 | $ | 13,296 | ||||||||||

|

Undisbursed construction loans

|

61,095 | 9,218 | 11,104 | - | 40,773 | |||||||||||||||

|

Unused home equity lines of credit

|

12,340 | 138 | 799 | 781 | 10,622 | |||||||||||||||

|

Total other commitments

|

$ | 156,448 | $ | 61,726 | $ | 26,694 | $ | 3,337 | $ | 64,691 | ||||||||||

|

As of December 31, 2013

|

||||||||||||||||||||

|

(in thousands)

|

Amount of Commitment Expiration per Period | |||||||||||||||||||

|

Less Than

|

1-3 | 4-5 |

After

|

|||||||||||||||||

|

Other Commitments:

|

Total

|

1 Year

|

Years

|

Years

|

5 Years

|

|||||||||||||||

|

Loan Commitments

|

$ | 61,633 | $ | 35,236 | $ | 7,528 | $ | 5,267 | $ | 13,602 | ||||||||||

|

Undisbursed construction loans

|

44,670 | 7,613 | 6,600 | - | 30,457 | |||||||||||||||

|

Unused home equity lines of credit

|

11,575 | 143 | 823 | 1,061 | 9,548 | |||||||||||||||

|

Total other commitments

|

$ | 117,878 | $ | 42,992 | $ | 14,951 | $ | 6,328 | $ | 53,607 | ||||||||||

| 79 |

|

Parallel Ramp

|

Estimated Percent Change

|

|||||||

|

in Net Interest Income

|

||||||||

|

At December 31,

|

||||||||

|

Rate Changes (basis points)

|

2014

|

2013

|

||||||

|

-100

|

(0.95 | )% | (0.73 | )% | ||||

|

+200

|

(4.00 | ) | (3.63 | ) | ||||

|

Parallel Shock

|

Estimated Percent Change

|

|||||||

|

in Net Interest Income

|

||||||||

|

At December 31,

|

||||||||

|

Rate Changes (basis points)

|

2014 | 2013 | ||||||

|

-100

|

(3.26 | )% | (1.97 | )% | ||||

|

+100

|

(3.07 | ) | (3.18 | ) | ||||

|

+200

|

(5.61 | ) | (5.93 | ) | ||||

|

+300

|

(9.00 | ) | (10.20 | ) | ||||

| 80 |

|

Parallel Shock

|

Estimated Percent Change

|

|||||||

|

in Economic Value of Equity

|

||||||||

|

At December 31,

|

||||||||

|

Rate Changes (basis points)

|

2014

|

2013

|

||||||

|

-100

|

(0.50 | )% | (4.30 | )% | ||||

|

+100

|

(8.50 | ) | (9.30 | ) | ||||

|

+200

|

(18.20 | ) | (20.10 | ) | ||||

|

+300

|

(26.90 | ) | (29.20 | ) | ||||

| 81 |

| 82 |

|

The financial statements and supplementary data required by this item are presented in the order shown below:

|

||

|

Report of Independent Registered Public Accounting Firm

|

||

|

Consolidated Balance Sheets as of December 31, 2014 and 2013

|

||

|

Consolidated Statements of Income for the years ended December 31, 2014, 2013 and 2012

|

||

|

Consolidated Statements of Comprehensive Income for the years ended December 31, 2014, 2013 and 2012

|

||

|

Consolidated Statements of Shareholders’ Equity for the years ended December 31, 2014, 2013 and 2012

|

||

|