|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

QuickLinks -- Click here to rapidly navigate through this document

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

WASHINGTON, D.C. 20549

FORM 10-Q

QUARTERLY REPORT PURSUANT TO SECTION 13 OR 15(d) OF

THE SECURITIES EXCHANGE ACT OF 1934

For the quarterly period ended September 30, 2012

Commission file number 1-9924

Citigroup Inc.

(Exact name of registrant as specified in its charter)

|

Delaware

(State or other jurisdiction of incorporation or organization) |

52-1568099

(I.R.S. Employer Identification No.) |

|

|

399 Park Avenue, New York, NY (Address of principal executive offices) |

|

10022 (Zip code) |

|

(212) 559-1000 (Registrant's telephone number, including area code) |

||

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes ý No o

Indicate by check mark whether the registrant has submitted electronically and posted on its corporate Web site, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T (§232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files). Yes ý No o

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, or a smaller reporting company. See the definitions of "large accelerated filer," "accelerated filer" and "smaller reporting company" in Rule 12b-2 of the Exchange Act.

| Large accelerated filer ý | Accelerated filer o |

Non-accelerated filer

o

(Do not check if a smaller reporting company) |

Smaller reporting company o |

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act). Yes o No ý

Indicate the number of shares outstanding of each of the issuer's classes of common stock as of the latest practicable date:

Common stock outstanding as of September 30, 2012: 2,932,520,700

Available on the web at www.citigroup.com

CITIGROUP INC

THIRD QUARTER 2012—FORM 10-Q

|

OVERVIEW |

3 | |||

|

CITIGROUP SEGMENTS AND REGIONS |

4 |

|||

|

MANAGEMENT'S DISCUSSION AND ANALYSIS OF FINANCIAL CONDITION AND RESULTS OF OPERATIONS |

5 |

|||

|

Executive Summary |

5 |

|||

|

RESULTS OF OPERATIONS |

9 |

|||

|

Summary of Selected Financial Data |

9 |

|||

|

SEGMENT AND BUSINESS—INCOME (LOSS) AND REVENUES |

11 |

|||

|

CITICORP |

13 |

|||

|

Global Consumer Banking |

14 |

|||

|

North America Regional Consumer Banking |

15 |

|||

|

EMEA Regional Consumer Banking |

17 |

|||

|

Latin America Regional Consumer Banking |

19 |

|||

|

Asia Regional Consumer Banking |

21 |

|||

|

Institutional Clients Group |

23 |

|||

|

Securities and Banking |

25 |

|||

|

Transaction Services |

27 |

|||

|

CITI HOLDINGS |

29 |

|||

|

Brokerage and Asset Management |

30 |

|||

|

Local Consumer Lending |

31 |

|||

|

Special Asset Pool |

33 |

|||

|

CORPORATE/OTHER |

34 |

|||

|

BALANCE SHEET REVIEW |

35 |

|||

|

Segment Balance Sheet at September 30, 2012 |

38 |

|||

|

CAPITAL RESOURCES AND LIQUIDITY |

39 |

|||

|

Capital Resources |

39 |

|||

|

Funding and Liquidity |

44 |

|||

|

Off-Balance-Sheet Arrangements |

51 |

|||

|

MANAGING GLOBAL RISK |

51 |

|||

|

CREDIT RISK |

52 |

|||

|

Loans Outstanding |

52 |

|||

|

Details of Credit Loss Experience |

53 |

|||

|

Non-Accrual Loans and Assets, and Renegotiated Loans |

54 |

|||

|

North America Consumer Mortgage Lending |

58 |

|||

|

North America Cards |

71 |

|||

|

Consumer Loan Details |

72 |

|||

|

Corporate Loan Details |

74 |

|||

|

MARKET RISK |

76 |

|||

|

COUNTRY RISK |

87 |

|||

|

FAIR VALUE ADJUSTMENTS FOR DERIVATIVES AND STRUCTURED DEBT |

95 |

|||

|

CREDIT DERIVATIVES |

96 |

|||

|

INCOME TAXES |

98 |

|||

|

DISCLOSURE CONTROLS AND PROCEDURES |

99 |

|||

|

FORWARD-LOOKING STATEMENTS |

99 |

|||

|

FINANCIAL STATEMENTS AND NOTES—TABLE OF CONTENTS |

102 |

|||

|

CONSOLIDATED FINANCIAL STATEMENTS |

103 |

|||

|

NOTES TO CONSOLIDATED FINANCIAL STATEMENTS |

109 |

|||

|

LEGAL PROCEEDINGS |

232 |

|||

|

UNREGISTERED SALES OF EQUITY AND USE OF PROCEEDS |

233 |

2

Citigroup's history dates back to the founding of Citibank in 1812. Citigroup's original corporate predecessor was incorporated in 1988 under the laws of the State of Delaware. Following a series of transactions over a number of years, Citigroup Inc. was formed in 1998 upon the merger of Citicorp and Travelers Group Inc.

Citigroup is a global diversified financial services holding company whose businesses provide consumers, corporations, governments and institutions with a broad range of financial products and services. Citi has approximately 200 million customer accounts and does business in more than 160 countries and jurisdictions.

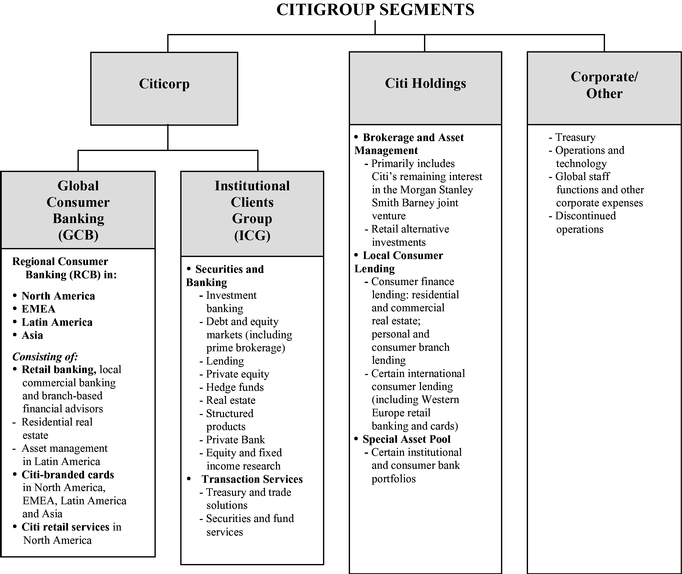

Citigroup currently operates, for management reporting purposes, via two primary business segments: Citicorp, consisting of Citi's Global Consumer Banking businesses and Institutional Clients Group ; and Citi Holdings, consisting of Brokerage and Asset Management, Local Consumer Lending and Special Asset Pool . For a further description of the business segments and the products and services they provide, see "Citigroup Segments" below, "Management's Discussion and Analysis of Financial Condition and Results of Operations" and Note 3 to the Consolidated Financial Statements.

Throughout this report, "Citigroup," "Citi" and "the Company" refer to Citigroup Inc. and its consolidated subsidiaries.

This Quarterly Report on Form 10-Q should be read in conjunction with Citigroup's Annual Report on Form 10-K for the year ended December 31, 2011 filed with the U.S. Securities and Exchange Commission (SEC) on February 24, 2012 (2011 Annual Report on Form 10-K) and Citigroup's Quarterly Reports on Form 10-Q for the quarters ended March 31, 2012 and June 30, 2012 filed with the SEC on May 4, 2012 (First Quarter Form 10-Q) and August 3, 2012 (Second Quarter Form 10-Q), respectively. Additional information about Citigroup is available on Citi's Web site at www.citigroup.com . Citigroup's recent annual reports on Form 10-K, quarterly reports on Form 10-Q, proxy statements, as well as other filings with SEC, are available free of charge through Citi's Web site by clicking on the "Investors" page and selecting "All SEC Filings." The SEC's Web site also contains current reports, information statements, and other information regarding Citi at www.sec.gov .

Within this Form 10-Q, please refer to the tables of contents on pages 2 and 102 for page references to Management's Discussion and Analysis of Financial Condition and Results of Operations and Notes to Consolidated Financial Statements, respectively.

Certain reclassifications have been made to the prior periods' financial statements to conform to the current period's presentation. For information on certain recent such classifications, including the transfer of the substantial majority of Citi's retail partner cards businesses (which is now referred to as Citi retail services) from Citi Holdings— Local Consumer Lending to Citicorp— North America Regional Consumer Banking, which was effective January 1, 2012, see Citi's Form 8-K furnished to the SEC on March 26, 2012.

3

As described above, Citigroup is managed pursuant to the following segments:

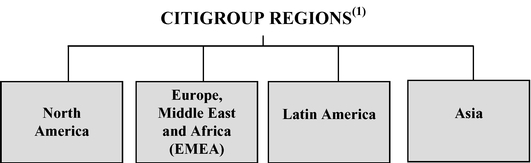

The following are the four regions in which Citigroup operates. The regional results are fully reflected in the segment results above.

- (1)

- North America includes the U.S., Canada and Puerto Rico, Latin America includes Mexico, and Asia includes Japan.

4

MANAGEMENT'S DISCUSSION AND ANALYSIS OF FINANCIAL CONDITION AND RESULTS OF OPERATIONS

THIRD QUARTER 2012 EXECUTIVE SUMMARY

On October 16, 2012, Citi announced that Vikram Pandit had resigned as Chief Executive Officer of Citigroup, effective after the close of business on October 15, 2012. Citi also announced that John Havens had resigned as President and Chief Operating Officer of Citigroup and as Chief Executive Officer of the Institutional Clients Group, effective as of the same time. In connection with the departure of Mr. Pandit, the Citigroup Board of Directors appointed Michael Corbat as Citi's new Chief Executive Officer.

As disclosed in connection with the announcements, these senior management changes are not expected to alter the overall strategy of Citigroup going forward, which is to continue to:

- •

-

enhance Citi's position as a leading global bank for both institutions and individuals, by building on its unique global

network, deep emerging markets expertise, client relationships and product expertise;

- •

-

position Citi to seize the opportunities provided by current trends (globalization, digitization, urbanization and the

rise of the emerging market consumer) for the benefit of clients;

- •

-

further its commitment to responsible finance and the basics of banking;

- •

-

strengthen Citi's performance—including gaining market share with clients, making Citi more efficient and

productive, and building upon its history of innovation; and

- •

- wind down Citi Holdings as soon as practicable, in an economically rational manner.

In addition, on October 29 and 30, 2012, the metropolitan New York City region and New Jersey suffered severe damage from Hurricane Sandy. Citi continues to assess the impact on Citi's facilities and customers in the affected areas and what impact, if any, the storm could have on its results of operations for the fourth quarter of 2012.

Citigroup

Citigroup reported third quarter of 2012 net income of $468 million, or $0.15 per diluted share. Citi's reported net income declined from $3.8 billion in the third quarter of 2011. Results for the third quarter of 2012 included a pre-tax loss of $4.7 billion ($2.9 billion after-tax) from the previously announced sale of a 14% interest and other-than-temporary impairment of the carrying value of Citi's remaining 35% interest in the Morgan Stanley Smith Barney (MSSB) joint venture recorded in Citi Holdings— Brokerage and Asset Management . (For additional information on the agreement entered into with Morgan Stanley regarding MSSB on September 11, 2012 and the impact of that agreement on third quarter of 2012 results, see Citigroup's Form 8-K filed with the SEC on September 11, 2012 and Note 11 to the Consolidated Financial Statements below.)

In addition, third quarter results included credit valuation adjustment on derivatives (excluding monolines), net of hedges (CVA) and debt valuation adjustment on Citi's fair value option debt (DVA) of pre-tax negative $776 million (negative $485 million after-tax) as Citi's credit spreads tightened during the quarter, compared to pretax positive $1.9 billion (positive $1.2 billion after-tax in the third quarter of 2011. The vast majority of this CVA/DVA was recorded in Securities and Banking . Results for the third quarter of 2012 also included a $582 million tax benefit related to the resolution of certain tax audit items, recorded in the Corporate/Other segment.

Excluding CVA/DVA, the loss on MSSB and the tax items described above, Citi earned $3.3 billion, or $1.06 per diluted share, compared to $0.84 per diluted share in the prior-year period. The year-over-year increase in earnings per share, excluding CVA/DVA, the loss on MSSB and the tax items, primarily reflected higher Citicorp revenues, as well as year-over-year declines in both expenses and credit costs.

Citi's revenues, net of interest expense, were $14.0 billion in the third quarter of 2012, down 33% versus the prior-year period. Excluding CVA/DVA and the loss on MSSB, revenues were $19.4 billion, up 3% from the third quarter of 2011, as revenues in Citicorp rose 5% from the prior-year period while revenues continued to decline in Citi Holdings. Net interest revenues of $11.9 billion were 2% lower than the prior-year period, largely due to continued declining loan balances in Local Consumer Lending in Citi Holdings and ongoing spread compression in GCB and Transaction Services in Citicorp (as used throughout this Form 10-Q, spread compression refers to the reduction in net interest revenue as a percentage of loans or deposits, as applicable, as driven by either lower yields on interest-earning assets or higher costs to fund such assets (or a combination thereof)). Excluding CVA/DVA and the impact of MSSB, non-interest revenues were $7.5 billion, up 11% from the prior-year period, principally driven by higher mortgage revenues in North America RCB and higher revenues in Securities and Banking , partially offset by a lower contribution from MSSB and lower private equity marks in Brokerage and Asset Management within Citi Holdings.

Operating Expenses

Citigroup expenses decreased 2% versus the prior-year period to $12.2 billion. In the third quarter of 2012, Citi continued to incur elevated legal and related costs ($528 million) and repositioning charges ($95 million) compared to $274 million of legal and related costs and $208 million of repositioning charges in the prior-year period. Excluding these items, as well as the impact of foreign exchange translation into U.S. dollars for reporting purposes (as used throughout this Form 10-Q, FX translation), which lowered reported expenses by approximately $0.3 billion in the third quarter of 2012 as compared to the prior-year period, operating expenses declined slightly to $11.6 billion versus $11.7 billion in the

5

prior-year period. Citi expects to continue to incur elevated legal and related expenses and repositioning costs in the fourth quarter of 2012.

Citicorp's expenses were $10.3 billion, down 2% from the prior-year period, as efficiency savings more than offset investments and volume-related increases.

Citi Holdings expenses were down 21% year-over-year to $1.2 billion, principally due to the continued decline in assets and thus lower operating expenses.

Credit Costs

Citi's total provisions for credit losses and for benefits and claims of $2.7 billion declined 20% from the prior-year period. Net credit losses of $4.0 billion were down 12% from the third quarter of 2011. Net credit losses in the third quarter of 2012 included approximately $635 million of incremental mortgage charge-offs in Local Consumer Lending within Citi Holdings required by new industry guidance from the Office of the Comptroller of the Currency (OCC) regarding the treatment of mortgage loans where the borrower has gone through Chapter 7 bankruptcy (see Note 1 to the Consolidated Financial Statements). The vast majority of the charge-offs were related to loans which were current. Excluding the charge-offs related to the new OCC guidance, net credit losses would have declined to $3.3 billion or by 26% from the prior-year period.

Consumer net credit losses declined 9% to $3.9 billion, as the continued credit improvement in North America Citi-branded cards and Citi retail services in Citicorp were partially offset by the increase in net credit losses in Local Consumer Lending within Citi Holdings related to the new OCC guidance mentioned above. Corporate net credit losses decreased 57% year-over-year to $117 million, driven primarily by continued credit improvement in the Special Asset Pool in Citi Holdings.

The net release of allowance for loan losses and unfunded lending commitments was $1.5 billion in the third quarter of 2012, 6% higher than the third quarter of 2011. The increase in the net reserve release was due to an approximately $600 million reserve release related to loans impacted by the new OCC guidance described above. Excluding the reserve release related to loans impacted by the new OCC guidance, the net reserve release would have been $909 million, 36% lower than the prior-year period.

Of the $1.5 billion net reserve release, $696 million was attributable to Citicorp compared to an $887 million release in the prior-year period. The decline in the Citicorp reserve release year-over-year mostly reflected a lower reserve release in North America RCB , partially offset by a net reserve release in the Corporate portfolio. The $813 million net reserve release in Citi Holdings was up from $535 million in the prior-year period, due primarily to the release associated with loans impacted by the new OCC guidance mentioned above. $1.3 billion of the $1.5 billion net reserve release related to Consumer, with the remainder in Corporate.

Capital and Loan Loss Reserve Positions

Citigroup's Tier 1 Capital and Tier 1 Common ratios were 13.9% and 12.7% as of September 30, 2012, respectively, compared to 13.5% and 11.7% in the prior-year period. Citi's estimated Tier 1 Common ratio under Basel III was 8.6% at the end of the third quarter of 2012, up from an estimated 7.9% as of the end of the second quarter of 2012. Citi's estimated Basel III Tier 1 Common ratio is a non-GAAP financial measure. For additional information on Citi's estimated Basel III Tier 1 Common Capital and Tier 1 Common ratio, including the calculation of these measures, see "Capital Resources and Liquidity—Capital Resources" below.

Citigroup's total allowance for loan losses was $25.9 billion at quarter end, or 4.0% of total loans, compared to $32.1 billion, or 5.1%, at the end of the prior-year period. The decline in the total allowance for loan losses reflected continued asset sales in Citi Holdings, consistent with Citi's strategy to reduce these assets in an economically rational manner, lower non-accrual loans, and overall continued improvement in the credit quality of the loan portfolios.

The Consumer allowance for loan losses was $23.1 billion, or 5.7% of total Consumer loans, at quarter-end, compared to $28.9 billion, or 6.8% of total loans, at September 30, 2011. Total non-accrual assets declined 5% to $12.7 billion compared to the third quarter of 2011. Corporate non-accrual loans declined 42% to $2.4 billion. Consumer non-accrual loans increased $1.9 billion, or 25%, to $9.8 billion versus the prior-year period, predominantly reflecting the new OCC guidance mentioned above which added $1.5 billion to Consumer non-accrual loans (of which approximately $1.3 billion were current).

Citicorp

Citicorp net income decreased 18% from the prior-year period to $4.1 billion. The decrease largely reflected the negative CVA/DVA versus positive CVA/DVA in the prior-year period. CVA/DVA, recorded in Securities and Banking , was a negative $799 million in the third quarter of 2012, compared to positive $1.9 billion in the prior-year period. Excluding CVA/DVA, Citicorp net income increased 20% from the prior-year period to $4.6 billion driven by a 5% increase in revenues, a 2% decline in operating expenses and a 14% decline in provisions for credit losses and for benefits and claims.

Excluding CVA/DVA, Citicorp revenues were $18.4 billion, up 5% versus the third quarter of 2011. GCB revenues of $10.2 billion were up 2% versus the prior-year period. North America RCB revenues grew 6% to $5.4 billion driven by higher mortgage revenues, partially offset by lower cards revenues as consumers continued to deleverage in the face of ongoing macroeconomic uncertainty. For additional information on the results of operations of North America RCB for the third quarter of 2012, see " Global Consumer Banking—North America Regional Consumer Banking " below.

International GCB revenues (consisting of Asia RCB , Latin America RCB and EMEA RCB ) declined 2% year-over-year to $4.8 billion. International GCB revenues were

6

negatively impacted by FX translation as the U.S. dollar generally strengthened in the third quarter of 2012 against local currencies in which Citi generates revenues. Excluding the impact of FX translation, international GCB revenues rose 3% year-over-year, driven by 7% revenue growth in each of Latin America RCB and EMEA RCB , partially offset by a 2% decline in Asia RCB revenues.(1) In Asia RCB , the revenue decline reflected the continued impact of several factors, including spread compression in several countries within the region, lower revenues in Japan and regulatory actions to limit the availability of consumer credit in certain countries, particularly Korea. For additional information on the results of operations of Asia RCB for the third quarter of 2012, see " Global Consumer Banking—Asia Regional Consumer Banking " below.

In North America RCB , average deposits of $154 billion grew 6% year-over-year and average retail loans of $41 billion grew 17%, while average card loans of $108 billion declined 4% and card purchase sales of $58 billion were roughly flat due to the deleveraging related to ongoing macroeconomic uncertainty, as referenced above. Excluding the impact of FX translation, international GCB average deposits grew 4% year-over-year, average retail loans increased 11%, average card loans grew 7% year-over-year and international card purchase sales increased 7%. Growth in these metrics year-over-year reflected continued execution of Citi's strategy to grow its core businesses in Citicorp, particularly in emerging markets such as Latin America .

Securities and Banking revenues were $4.8 billion in the third quarter of 2012, down 29% year-over-year. Excluding the impact of CVA/DVA, Securities and Banking revenues were $5.6 billion, or 15% higher than the prior-year period. Fixed income markets revenues of $3.7 billion in the third quarter of 2012, excluding CVA/DVA,(2) increased 63% from the prior-year period, reflecting significantly higher trading revenues in credit-related and securitized products, as well as a strong performance in rates and currencies, driven by improved market conditions. Equity markets revenues of $510 million in the third quarter of 2012, excluding CVA/DVA, were 76% above the prior-year period driven by improved derivatives performance as well as the absence of proprietary trading losses in the prior-year period, partially offset by lower cash equity volumes.

Investment banking revenues rose 26% from the prior-year period to $926 million, reflecting higher revenues in debt underwriting, equity underwriting and advisory services. Lending revenues of $194 million were down 81% from the prior-year period, reflecting $252 million in losses on hedges related to accrual loans as credit spreads tightened during the third quarter 2012 (compared to a $702 million gain in the prior-year period as spreads widened). Excluding the mark-to-market impact of loan hedges related to accrual loans, lending revenues rose 35% year-over-year to $445 million reflecting higher lending volumes and improved spreads. Private Bank revenues of $590 million increased 8% from the prior-year period, excluding CVA/DVA, driven primarily by growth in North America lending and deposits.

Transaction Services revenues were $2.7 billion, down 2% from the prior-year period, but up 1% excluding the impact of FX translation, as growth in Treasury and Trade Solutions offset a decline in Securities and Fund Services .(3) Excluding the impact of FX translation, Treasury and Trade Solutions revenues were up 4%, reflecting strong growth in average deposits and trade loans, partially offset by ongoing spread compression given the low interest rate environment. Securities and Fund Services revenues were down 8% excluding the impact of FX translation, mostly reflecting lower settlement volumes.

Citicorp end of period loans increased for the seventh consecutive quarter, up 11% year-over-year to $537 billion, with 5% growth in Consumer loans, primarily in Asia and Latin America, and 19% growth in Corporate loans.

Citi Holdings

Citi Holdings net loss was $3.6 billion in the third quarter of 2012 compared to a $1.2 billion loss reported in the third quarter of 2011. The increase in the net loss year-over-year was driven by the $4.7 billion pre-tax ($2.9 billion after-tax) loss on MSSB mentioned above. Excluding the loss on MSSB and CVA/DVA,(4) Citi Holdings net loss improved to $679 million, from a $1.3 billion loss in the prior-year period, as revenue declines were more than offset by lower operating expenses and lower credit costs, all reflecting the continued decline in Citi Holdings assets, consistent with Citi's strategy. In addition, the net loss in the third quarter of 2012 also reflected a tax benefit of approximately $200 million related to the sale of certain assets in the Special Asset Pool .

Citi Holdings revenues decreased to a negative $3.7 billion from $1.1 billion in the prior-year period. Excluding CVA/DVA and the loss on MSSB, Citi Holdings revenues were $971 million in the third quarter compared to $1.1 billion in the prior-year period. Special Asset Pool revenues, excluding CVA/DVA, were a negative $13 million in the third quarter 2012, compared to a negative $277 million in the prior-year period, largely due to lower funding costs as well as an improvement in asset marks. Local Consumer Lending revenues of $1.1 billion declined 15% from the prior-year period primarily due to the 26% decline in average assets. Brokerage and Asset Management revenues, excluding the loss on MSSB, were $(120) million, compared to $55 million in the prior-year period, reflecting a lower equity contribution from MSSB as well as lower asset marks. Net interest revenues declined 14% year-over-year to $668 million, largely driven by continued declining loan balances in Local Consumer Lending . Non-interest revenues, excluding MSSB

- (1)

-

For

the impact of FX translation on the third quarter of 2012 results of operations for each of

EMEA RCB

,

Latin America RCB

and

Asia

RCB

, see the table accompanying the discussion of each respective business'

results of operations under "

Global Consumer Banking

" below.

- (2)

-

For

the summary of CVA/DVA by business within

Securities and Banking

for the third quarter of 2012 and

comparable periods, see "Citicorp—

Institutional Clients Group

."

- (3)

-

For

the impact of FX translation on the third quarter of 2012 results of operations for

Transaction

Services

, see the table accompanying the discussion under "

Institutional Clients

Group

—

Transaction Services

" below.

- (4)

- CVA/DVA in Citi Holdings, recorded in the Special Asset Pool , was a positive $23 million in the third quarter of 2012, compared to a positive $50 million in the prior-year period.

7

and CVA/DVA, were essentially flat at $303 million versus the prior-year period, reflecting the lower equity contribution from MSSB in Brokerage and Asset Management offset by the improvement in asset marks within the Special Asset Pool .

Citi Holdings assets declined 31% year-over-year to $171 billion as of the end of the third quarter of 2012. At the end of the third quarter of 2012, Citi Holdings assets comprised approximately 9% of total Citigroup GAAP assets and 16% of risk-weighted assets (as defined under current regulatory guidelines). Local Consumer Lending continued to represent the largest segment within Citi Holdings, with $134 billion of assets as of the end of the third quarter, of which approximately 70% consisted of mortgages in North America real estate lending.

8

SUMMARY OF SELECTED FINANCIAL DATA—Page 1

|

|

|||||||||||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

|

Citigroup Inc. and Consolidated Subsidiaries

|

|||||||||||||||||||

|

|

|

Third Quarter |

|

|

|

Nine Months |

|

|

|

||||||||||

|

|

%

Change |

%

Change |

|||||||||||||||||

| In millions of dollars, except per-share amounts and ratios | 2012 | 2011 | 2012 | 2011 | |||||||||||||||

|

Net interest revenue |

$ | 11,913 | $ | 12,114 | (2 | )% | $ | 35,453 | $ | 36,364 | (3 | )% | |||||||

|

Non-interest revenue |

2,038 | 8,717 | (77 | ) | 16,546 | 24,815 | (33 | ) | |||||||||||

|

Revenues, net of interest expense |

$ | 13,951 | $ | 20,831 | (33 | )% | $ | 51,999 | $ | 61,179 | (15 | )% | |||||||

|

Operating expenses |

12,220 | 12,460 | (2 | ) | 36,673 | 37,722 | (3 | ) | |||||||||||

|

Provisions for credit losses and for benefits and claims |

2,695 | 3,351 | (20 | ) | 8,520 | 9,922 | (14 | ) | |||||||||||

|

Income (loss) from continuing operations before income taxes |

$ | (964 | ) | $ | 5,020 | NM | $ | 6,806 | $ | 13,535 | (50 | )% | |||||||

|

Income taxes (benefits) |

(1,488 | ) | 1,278 | NM | 233 | 3,430 | (93 | ) | |||||||||||

|

Income from continuing operations |

$ | 524 | $ | 3,742 | (86 | )% | $ | 6,573 | $ | 10,105 | (35 | )% | |||||||

|

Income (loss) from discontinued operations, net of taxes(1) |

(31 | ) | 1 | NM | (37 | ) | 112 | NM | |||||||||||

|

Net income before attribution of noncontrolling interests |

$ | 493 | $ | 3,743 | (87 | )% | $ | 6,536 | $ | 10,217 | (36 | )% | |||||||

|

Net income (loss) attributable to noncontrolling interests |

25 | (28 | ) | NM | 191 | 106 | 80 | ||||||||||||

|

Citigroup's net income |

$ | 468 | $ | 3,771 | (88 | )% | $ | 6,345 | $ | 10,111 | (37 | )% | |||||||

|

Less: |

|||||||||||||||||||

|

Preferred dividends—Basic |

$ | 4 | $ | 4 | — | % | $ | 17 | $ | 17 | — | % | |||||||

|

Dividends and undistributed earnings allocated to employee restricted and deferred shares that contain nonforfeitable rights to dividends, applicable to Basic EPS |

11 | 70 | (84 | ) | 138 | 164 | (16 | ) | |||||||||||

|

Income allocated to unrestricted common shareholders for Basic EPS |

$ | 453 | $ | 3,697 | (88 | )% | $ | 6,190 | $ | 9,930 | (38 | )% | |||||||

|

Add: Interest expense, net of tax, on convertible securities and adjustment of undistributed earnings allocated to employee restricted and deferred shares that contain nonforfeitable rights to dividends, applicable to diluted EPS |

2 | 6 | (67 | ) | 10 | 12 | (17 | ) | |||||||||||

|

Income allocated to unrestricted common shareholders for diluted EPS |

$ | 455 | $ | 3,703 | (88 | )% | $ | 6,200 | $ | 9,942 | (38 | )% | |||||||

|

Earnings per share(2) |

|||||||||||||||||||

|

Basic |

|||||||||||||||||||

|

Income from continuing operations |

$ | 0.17 | $ | 1.27 | (87 | )% | $ | 2.13 | $ | 3.38 | (37 | )% | |||||||

|

Net income |

0.15 | 1.27 | (88 | ) | 2.12 | 3.41 | (38 | ) | |||||||||||

|

Diluted |

|||||||||||||||||||

|

Income from continuing operations |

$ | 0.16 | $ | 1.23 | (87 | )% | $ | 2.07 | $ | 3.28 | (37 | )% | |||||||

|

Net income |

0.15 | 1.23 | (88 | ) | 2.06 | 3.32 | (38 | ) | |||||||||||

|

Dividends declared per common share |

0.01 | 0.01 | — | 0.03 | 0.02 | 50 | |||||||||||||

Statement continues on the next page, including notes to the table.

9

SUMMARY OF SELECTED FINANCIAL DATA—Page 2

|

Citigroup Inc. and Consolidated Subsidiaries

|

|||||||||||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

|

|

Third Quarter |

|

Nine Months |

|

|||||||||||||||

|

|

%

Change |

%

Change |

|||||||||||||||||

| In millions of dollars, except per-share amounts, ratios and direct staff | 2012 | 2011 | 2012 | 2011 | |||||||||||||||

|

At September 30: |

|||||||||||||||||||

|

Total assets |

$ | 1,931,346 | $ | 1,935,992 | — | % | |||||||||||||

|

Total deposits |

944,644 | 851,281 | 11 | ||||||||||||||||

|

Long - term debt |

271,862 | 333,824 | (19 | ) | |||||||||||||||

|

Trust preferred securities (included in long-term debt) |

10,560 | 16,089 | (34 | ) | |||||||||||||||

|

Citigroup common stockholders' equity |

186,465 | 177,060 | 5 | ||||||||||||||||

|

Total Citigroup stockholders' equity |

186,777 | 177,372 | 5 | ||||||||||||||||

|

Direct staff (in thousands) |

261 | 267 | (2 | ) | |||||||||||||||

|

Ratios |

|||||||||||||||||||

|

Return on average common stockholders' equity(3) |

0.99 | % | 8.44 | % | 4.61 | % | 7.82 | % | |||||||||||

|

Return on average total stockholders' equity(3) |

1.00 | 8.43 | 4.61 | 7.82 | |||||||||||||||

|

Tier 1 Common(4) |

12.73 | % | 11.71 | % | |||||||||||||||

|

Tier 1 Capital |

13.92 | 13.45 | |||||||||||||||||

|

Total Capital |

17.12 | 16.89 | |||||||||||||||||

|

Leverage(5) |

7.39 | 7.01 | |||||||||||||||||

|

Citigroup common stockholders' equity to assets |

9.65 | % | 9.15 | % | |||||||||||||||

|

Total Citigroup stockholders' equity to assets |

9.67 | 9.16 | |||||||||||||||||

|

Dividend payout ratio(6) |

0.07 | 0.01 | |||||||||||||||||

|

Book value per common share(2) |

$ | 63.59 | $ | 60.56 | |||||||||||||||

|

Ratio of earnings to fixed charges and preferred stock dividends |

0.81x | 1.81x | 1.41x | 1.71x | |||||||||||||||

- (1)

-

Discontinued

operations in 2012 includes definitive agreements executed by Citi to transition a carve-out of its liquid strategies business

within Citi Capital Advisors to certain employees responsible for managing those operations. Discontinued operations in 2011 primarily reflect the sale of the Egg Banking PLC credit card

business. See Note 2 to the Consolidated Financial Statements.

- (2)

-

All

per share amounts and Citigroup shares outstanding for all periods reflect Citigroup's 1-for-10 reverse stock split, which was

effective May 6, 2011.

- (3)

-

The

return on average common stockholders' equity is calculated using net income less preferred stock dividends divided by average common stockholders'

equity. The return on average total Citigroup stockholders' equity is calculated using net income divided by average Citigroup stockholders' equity.

- (4)

-

As

currently defined by the U.S. banking regulators, the Tier 1 Common ratio represents Tier 1 Capital less non-common elements,

including qualifying perpetual preferred stock, qualifying noncontrolling interests in subsidiaries and qualifying trust preferred securities divided by risk-weighted assets.

- (5)

-

The

leverage ratio represents Tier 1 Capital divided by quarterly adjusted average total assets.

- (6)

- Dividends declared per common share as a percentage of net income per diluted share.

10

SEGMENT AND BUSINESS—INCOME (LOSS) AND REVENUES

The following tables show the income (loss) and revenues for Citigroup on a segment and business view:

|

|

Third Quarter |

|

Nine Months |

|

|||||||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

|

|

%

Change |

%

Change |

|||||||||||||||||

| In millions of dollars | 2012 | 2011 | 2012 | 2011 | |||||||||||||||

|

Income (loss) from continuing operations |

|||||||||||||||||||

|

CITICORP |

|||||||||||||||||||

|

Global Consumer Banking |

|||||||||||||||||||

|

North America |

$ | 1,300 | $ | 1,103 | 18 | % | $ | 3,813 | $ | 3,151 | 21 | % | |||||||

|

EMEA |

10 | 9 | 11 | 20 | 99 | (80 | ) | ||||||||||||

|

Latin America |

405 | 339 | 19 | 1,109 | 1,208 | (8 | ) | ||||||||||||

|

Asia |

449 | 562 | (20 | ) | 1,400 | 1,494 | (6 | ) | |||||||||||

|

Total |

$ | 2,164 | $ | 2,013 | 8 | % | $ | 6,342 | $ | 5,952 | 7 | % | |||||||

|

Securities and Banking |

|||||||||||||||||||

|

North America |

$ | 232 | 674 | (66 | )% | $ | 848 | $ | 1,485 | (43 | )% | ||||||||

|

EMEA |

346 | 735 | (53 | ) | 1,223 | 1,840 | (34 | ) | |||||||||||

|

Latin America |

363 | 207 | 75 | 1,030 | 776 | 33 | |||||||||||||

|

Asia |

190 | 526 | (64 | ) | 747 | 946 | (21 | ) | |||||||||||

|

Total |

$ | 1,131 | $ | 2,142 | (47 | )% | $ | 3,848 | $ | 5,047 | (24 | )% | |||||||

|

Transaction Services |

|||||||||||||||||||

|

North America |

$ | 120 | $ | 112 | 7 | % | $ | 370 | $ | 347 | 7 | % | |||||||

|

EMEA |

283 | 286 | (1 | ) | 930 | 847 | 10 | ||||||||||||

|

Latin America |

157 | 168 | (7 | ) | 520 | 500 | 4 | ||||||||||||

|

Asia |

286 | 316 | (9 | ) | 862 | 888 | (3 | ) | |||||||||||

|

Total |

$ | 846 | $ | 882 | (4 | )% | $ | 2,682 | $ | 2,582 | 4 | % | |||||||

|

Institutional Clients Group |

$ | 1,977 | $ | 3,024 | (35 | )% | $ | 6,530 | $ | 7,629 | (14 | )% | |||||||

|

Total Citicorp |

$ | 4,141 | $ | 5,037 | (18 | )% | $ | 12,872 | $ | 13,581 | (5 | )% | |||||||

|

Corporate/Other |

$ | (55 | ) | $ | (74 | ) | 26 | $ | (794 | ) | $ | (687 | ) | (16 | )% | ||||

|

Total Citicorp and Corporate/Other |

$ | 4,086 | $ | 4,963 | (18 | )% | $ | 12,078 | $ | 12,894 | (6 | )% | |||||||

|

CITI HOLDINGS |

|||||||||||||||||||

|

Brokerage and Asset Management |

$ | (3,018 | ) | $ | (83 | ) | NM | $ | (3,178 | ) | $ | (193 | ) | NM | |||||

|

Local Consumer Lending |

(694 | ) | (1,011 | ) | 31 | % | (2,148 | ) | (3,209 | ) | 33 | % | |||||||

|

Special Asset Pool |

150 | (127 | ) | NM | (179 | ) | 613 | NM | |||||||||||

|

Total Citi Holdings |

$ | (3,562 | ) | $ | (1,221 | ) | NM | $ | (5,505 | ) | $ | (2,789 | ) | (97 | )% | ||||

|

Income from continuing operations |

$ | 524 | $ | 3,742 | (86 | )% | $ | 6,573 | $ | 10,105 | (35 | )% | |||||||

|

Discontinued operations |

$ | (31 | ) | $ | 1 | NM | $ | (37 | ) | 112 | NM | ||||||||

|

Net income attributable to noncontrolling interests |

25 | (28 | ) | NM | 191 | 106 | 80 | % | |||||||||||

|

Citigroup's net income |

$ | 468 | $ | 3,771 | (88 | )% | $ | 6,345 | $ | 10,111 | (37 | )% | |||||||

NM Not meaningful

11

|

|

Third Quarter |

|

Nine Months |

|

|||||||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

|

|

%

Change |

%

Change |

|||||||||||||||||

| In millions of dollars | 2012 | 2011 | 2012 | 2011 | |||||||||||||||

|

CITICORP |

|||||||||||||||||||

|

Global Consumer Banking |

|||||||||||||||||||

|

North America |

$ | 5,402 | $ | 5,100 | 6 | % | $ | 15,735 | $ | 14,992 | 5 | % | |||||||

|

EMEA |

381 | 379 | 1 | 1,125 | 1,210 | (7 | ) | ||||||||||||

|

Latin America |

2,419 | 2,417 | — | 7,182 | 7,119 | 1 | |||||||||||||

|

Asia |

1,978 | 2,067 | (4 | ) | 5,923 | 5,989 | (1 | ) | |||||||||||

|

Total |

$ | 10,180 | $ | 9,963 | 2 | % | $ | 29,965 | $ | 29,310 | 2 | % | |||||||

|

Securities and Banking |

|||||||||||||||||||

|

North America |

$ | 1,439 | $ | 2,445 | (41 | )% | $ | 4,713 | $ | 6,898 | (32 | )% | |||||||

|

EMEA |

1,511 | 2,299 | (34 | ) | 5,074 | 6,002 | (15 | ) | |||||||||||

|

Latin America |

802 | 521 | 54 | 2,314 | 1,791 | 29 | |||||||||||||

|

Asia |

1,018 | 1,460 | (30 | ) | 3,349 | 3,538 | (5 | ) | |||||||||||

|

Total |

$ | 4,770 | $ | 6,725 | (29 | )% | $ | 15,450 | $ | 18,229 | (15 | )% | |||||||

|

Transaction Services |

|||||||||||||||||||

|

North America |

$ | 623 | $ | 620 | — | $ | 1,929 | $ | 1,839 | 5 | % | ||||||||

|

EMEA |

867 | 893 | (3 | )% | 2,691 | 2,628 | 2 | ||||||||||||

|

Latin America |

447 | 444 | 1 | 1,353 | 1,300 | 4 | |||||||||||||

|

Asia |

721 | 759 | (5 | ) | 2,235 | 2,188 | 2 | ||||||||||||

|

Total |

$ | 2,658 | $ | 2,716 | (2 | )% | $ | 8,208 | $ | 7,955 | 3 | % | |||||||

|

Institutional Clients Group |

$ | 7,428 | $ | 9,441 | (21 | )% | $ | 23,658 | $ | 26,184 | (10 | )% | |||||||

|

Total Citicorp |

$ | 17,608 | $ | 19,404 | (9 | )% | $ | 53,623 | $ | 55,494 | (3 | )% | |||||||

|

Corporate/Other |

$ | 33 | $ | 300 | (89 | )% | $ | 268 | $ | 502 | (47 | )% | |||||||

|

Total Citicorp and Corporate/Other |

$ | 17,641 | $ | 19,704 | (10 | )% | $ | 53,891 | $ | 55,996 | (4 | )% | |||||||

|

CITI HOLDINGS |

|||||||||||||||||||

|

Brokerage and Asset Management |

$ | (4,804 | ) | $ | 55 | NM | $ | (4,763 | ) | $ | 239 | NM | |||||||

|

Local Consumer Lending |

1,104 | 1,299 | (15 | )% | 3,361 | 4,163 | (19 | )% | |||||||||||

|

Special Asset Pool |

10 | (227 | ) | NM | (490 | ) | 781 | NM | |||||||||||

|

Total Citi Holdings |

$ | (3,690 | ) | $ | 1,127 | NM | $ | (1,892 | ) | $ | 5,183 | NM | |||||||

|

Total Citigroup net revenues |

$ | 13,951 | $ | 20,831 | (33 | )% | $ | 51,999 | $ | 61,179 | (15 | )% | |||||||

NM Not meaningful

12

Citicorp is Citigroup's global bank for consumers and businesses and represents Citi's core franchises. Citicorp is focused on providing best-in-class products and services to customers and leveraging Citigroup's unparalleled global network, including many of the world's emerging economies. Citicorp is physically present in approximately 100 countries, many for over 100 years, and offers services in over 160 countries and jurisdictions. Citi believes this global network provides a strong foundation for servicing the broad financial services needs of its large multinational clients and for meeting the needs of retail, private banking, commercial, public sector and institutional clients around the world. At September 30, 2012, Citicorp had approximately $1.5 trillion of assets and $875 billion of deposits, representing approximately 75% of Citi's total assets and approximately 92% of its deposits.

Citicorp consists of the following businesses: Global Consumer Banking (which consists of Citi's Regional Consumer Banking in North America, EMEA, Latin America and Asia ) and Institutional Clients Group (which includes Securities and Banking and Transaction Services ).

|

|

Third Quarter |

|

Nine Months |

|

|||||||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

|

|

%

Change |

%

Change |

|||||||||||||||||

| In millions of dollars except as otherwise noted | 2012 | 2011 | 2012 | 2011 | |||||||||||||||

|

Net interest revenue |

$ | 11,381 | $ | 11,363 | — | $ | 33,647 | $ | 33,585 | — | |||||||||

|

Non-interest revenue |

6,227 | 8,041 | (23 | )% | 19,976 | 21,909 | (9 | )% | |||||||||||

|

Total revenues, net of interest expense |

$ | 17,608 | $ | 19,404 | (9 | )% | $ | 53,623 | $ | 55,494 | (3 | )% | |||||||

|

Provisions for credit losses and for benefits and claims |

|||||||||||||||||||

|

Net credit losses |

$ | 2,173 | $ | 2,632 | (17 | )% | $ | 6,639 | $ | 8,864 | (25 | )% | |||||||

|

Credit reserve build (release) |

(671 | ) | (932 | ) | 28 | (1,988 | ) | (4,134 | ) | 52 | |||||||||

|

Provision for loan losses |

$ | 1,502 | $ | 1,700 | (12 | )% | $ | 4,651 | $ | 4,730 | (2 | )% | |||||||

|

Provision for benefits and claims |

65 | 56 | 16 | 173 | 147 | 18 | |||||||||||||

|

Provision for unfunded lending commitments |

(25 | ) | 45 | NM | (11 | ) | 44 | NM | |||||||||||

|

Total provisions for credit losses and for benefits and claims |

$ | 1,542 | $ | 1,801 | (14 | )% | $ | 4,813 | $ | 4,921 | (2 | )% | |||||||

|

Total operating expenses |

$ | 10,266 | $ | 10,427 | (2 | )% | $ | 30,871 | $ | 31,332 | (1 | )% | |||||||

|

Income from continuing operations before taxes |

$ | 5,800 | $ | 7,176 | (19 | )% | $ | 17,939 | $ | 19,241 | (7 | )% | |||||||

|

Provisions for income taxes |

1,659 | 2,139 | (22 | ) | 5,067 | 5,660 | (10 | ) | |||||||||||

|

Income from continuing operations |

$ | 4,141 | $ | 5,037 | (18 | )% | $ | 12,872 | $ | 13,581 | (5 | )% | |||||||

|

Net income attributable to noncontrolling interests |

17 | 6 | NM | 108 | 29 | NM | |||||||||||||

|

Citicorp's net income |

$ | 4,124 | $ | 5,031 | (18 | )% | $ | 12,764 | $ | 13,552 | (6 | )% | |||||||

|

Balance sheet data (in billions of dollars) |

|||||||||||||||||||

|

Total end of period (EOP) assets |

$ | 1,458 | $ | 1,406 | 4 | % | |||||||||||||

|

Average assets |

1,432 | 1,423 | 1 | $ | 1,420 | $ | 1,404 | 1 | % | ||||||||||

|

Total EOP loans |

537 | 483 | 11 | ||||||||||||||||

|

Total EOP deposits |

875 | 779 | 12 | ||||||||||||||||

NM Not meaningful

13

Global Consumer Banking (GCB) consists of Citigroup's four geographical Regional Consumer Banking (RCB) businesses that provide traditional banking services to retail customers through retail banking, commercial banking, Citi-branded cards and Citi retail services. GCB is a globally diversified business with 4,069 branches in 39 countries around the world. For the three months ended September 30, 2012, GCB had $388 billion of average assets and $324 billion of average deposits.

|

|

Third Quarter |

|

Nine Months |

|

|||||||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

|

|

%

Change |

%

Change |

|||||||||||||||||

| In millions of dollars except as otherwise noted | 2012 | 2011 | 2012 | 2011 | |||||||||||||||

|

Net interest revenue |

$ | 7,395 | $ | 7,515 | (2 | )% | $ | 21,965 | $ | 22,258 | (1 | )% | |||||||

|

Non-interest revenue |

2,785 | 2,448 | 14 | % | 8,000 | 7,052 | 13 | ||||||||||||

|

Total revenues, net of interest expense |

$ | 10,180 | $ | 9,963 | 2 | % | $ | 29,965 | $ | 29,310 | 2 | % | |||||||

|

Total operating expenses |

$ | 5,389 | $ | 5,382 | — | $ | 15,912 | $ | 15,830 | 1 | % | ||||||||

|

Net credit losses |

$ | 2,030 | $ | 2,545 | (20 | )% | $ | 6,432 | $ | 8,417 | (24 | )% | |||||||

|

Credit reserve build (release) |

(522 | ) | (964 | ) | 46 | (1,984 | ) | (3,716 | ) | 47 | |||||||||

|

Provisions for unfunded lending commitments |

1 | — | — | — | 3 | (100 | ) | ||||||||||||

|

Provision for benefits and claims |

65 | 56 | 16 | 173 | 147 | 18 | |||||||||||||

|

Provisions for credit losses and for benefits and claims |

$ | 1,574 | $ | 1,637 | (4 | )% | $ | 4,621 | $ | 4,851 | (5 | )% | |||||||

|

Income from continuing operations before taxes |

$ | 3,217 | $ | 2,944 | 9 | % | $ | 9,432 | $ | 8,629 | 9 | % | |||||||

|

Income taxes |

1,053 | 931 | 13 | 3,090 | 2,677 | 15 | |||||||||||||

|

Income from continuing operations |

$ | 2,164 | $ | 2,013 | 8 | % | $ | 6,342 | $ | 5,952 | 7 | % | |||||||

|

Net income (loss) attributable to noncontrolling interests |

3 | 1 | NM | 3 | 2 | 50 | |||||||||||||

|

Net income |

$ | 2,161 | $ | 2,012 | 7 | % | $ | 6,339 | $ | 5,950 | 7 | % | |||||||

|

Average assets (in billions of dollars) |

$ | 388 | $ | 380 | 2 | % | $ | 384 | $ | 375 | 2 | % | |||||||

|

Return on assets |

2.22 | % | 2.10 | % | — | 2.21 | % | 2.12 | % | ||||||||||

|

Total EOP assets |

$ | 395 | $ | 377 | 5 | ||||||||||||||

|

Average deposits (in billions of dollars) |

324 | 315 | 3 | 320 | 314 | 2 | % | ||||||||||||

|

Net credit losses as a percentage of average loans |

2.83 | % | 3.64 | % | |||||||||||||||

|

Revenue by business |

|||||||||||||||||||

|

Retail banking |

$ | 4,597 | $ | 4,173 | 10 | % | $ | 13,509 | $ | 12,250 | 10 | % | |||||||

|

Cards(1) |

5,583 | 5,790 | (4 | ) | 16,456 | 17,060 | (4 | ) | |||||||||||

|

Total |

$ | 10,180 | $ | 9,963 | 2 | % | $ | 29,965 | $ | 29,310 | 2 | % | |||||||

|

Income from continuing operations by business |

|||||||||||||||||||

|

Retail banking |

$ | 789 | $ | 628 | 26 | % | $ | 2,389 | $ | 1,938 | 23 | % | |||||||

|

Cards(1) |

1,375 | 1,385 | (1 | ) | 3,953 | 4,014 | (2 | ) | |||||||||||

|

Total |

$ | 2,164 | $ | 2,013 | 8 | % | $ | 6,342 | $ | 5,952 | 7 | % | |||||||

|

Foreign Currency (FX) Translation Impact |

|||||||||||||||||||

|

Total revenue—as reported |

$ | 10,180 | $ | 9,963 | 2 | % | $ | 29,965 | $ | 29,310 | 2 | % | |||||||

|

Impact of FX translation(2) |

— | (217 | ) | — | (735 | ) | |||||||||||||

|

Total revenues—ex-FX |

$ | 10,180 | $ | 9,746 | 4 | % | $ | 29,965 | $ | 28,507 | 5 | % | |||||||

|

Total operating expenses—as reported |

$ | 5,389 | $ | 5,382 | — | $ | 15,912 | $ | 15,830 | 1 | % | ||||||||

|

Impact of FX translation(2) |

— | (145 | ) | — | (478 | ) | |||||||||||||

|

Total operating expenses—ex-FX |

$ | 5,389 | $ | 5,237 | 3 | % | $ | 15,912 | $ | 15,298 | 4 | % | |||||||

|

Total provisions for LLR & PBC—as reported |

$ | 1,574 | $ | 1,637 | (4 | )% | $ | 4,621 | $ | 4,851 | (5 | )% | |||||||

|

Impact of FX translation(2) |

— | (51 | ) | — | (141 | ) | |||||||||||||

|

Total provisions for LLR & PBC—ex-FX |

$ | 1,574 | $ | 1,586 | (1 | )% | $ | 4,621 | $ | 4,692 | (2 | )% | |||||||

- (1)

-

Includes

both Citi-branded cards and Citi retail services.

- (2)

-

Reflects

the impact of foreign exchange (FX) translation into U.S. dollars at the current exchange rate for all periods presented.

- NM

- Not meaningful

14

NORTH AMERICA REGIONAL CONSUMER BANKING

North America Regional Consumer Banking (NA RCB) provides traditional banking and Citi-branded card and Citi retail service to retail customers and small to mid-size businesses in the U.S. NA RCB's 1,017 retail bank branches and 12.5 million customer accounts, as of September 30, 2012, are largely concentrated in the greater metropolitan areas of New York, Los Angeles, San Francisco, Chicago, Miami, Washington, D.C., Boston, Philadelphia, Dallas, Houston, San Antonio and Austin. At September 30, 2012, NA RCB had $41.5 billion of retail banking loans and $156.8 billion of deposits. In addition, NA RCB had 102.4 million Citi-branded and Citi retail services credit card accounts, with $108.8 billion in outstanding card loan balances.

|

|

Third Quarter |

|

Nine Months |

|

|||||||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

|

|

%

Change |

%

Change |

|||||||||||||||||

| In millions of dollars, except as otherwise noted | 2012 | 2011 | 2012 | 2011 | |||||||||||||||

|

Net interest revenue |

$ | 4,183 | $ | 4,268 | (2 | )% | $ | 12,343 | $ | 12,666 | (3 | )% | |||||||

|

Non-interest revenue |

1,219 | 832 | 47 | 3,392 | 2,326 | 46 | |||||||||||||

|

Total revenues, net of interest expense |

$ | 5,402 | $ | 5,100 | 6 | % | $ | 15,735 | $ | 14,992 | 5 | % | |||||||

|

Total operating expenses |

$ | 2,465 | $ | 2,409 | 2 | $ | 7,257 | $ | 7,018 | 3 | % | ||||||||

|

Net credit losses |

$ | 1,351 | $ | 1,854 | (27 | )% | $ | 4,491 | $ | 6,362 | (29 | )% | |||||||

|

Credit reserve build (release) |

(519 | ) | (955 | ) | 46 | (2,174 | ) | (3,396 | ) | 36 | |||||||||

|

Provisions for benefits and claims |

1 | (1 | ) | NM | 1 | (2 | ) | NM | |||||||||||

|

Provision for unfunded lending commitments |

19 | 18 | 6 | 52 | 49 | 6 | |||||||||||||

|

Provisions for credit losses and for benefits and claims |

$ | 852 | $ | 916 | (7 | )% | $ | 2,370 | $ | 3,013 | (21 | )% | |||||||

|

Income from continuing operations before taxes |

$ | 2,085 | $ | 1,775 | 17 | % | $ | 6,108 | $ | 4,961 | 23 | % | |||||||

|

Income taxes |

785 | 672 | 17 | 2,295 | 1,810 | 27 | |||||||||||||

|

Income from continuing operations |

$ | 1,300 | $ | 1,103 | 18 | % | $ | 3,813 | $ | 3,151 | 21 | % | |||||||

|

Net income attributable to noncontrolling interests |

1 | — | — | 1 | — | — | |||||||||||||

|

Net income |

$ | 1,299 | $ | 1,103 | 18 | % | $ | 3,812 | $ | 3,151 | 21 | % | |||||||

|

Average assets (in billions of dollars) |

$ | 173 | $ | 167 | 4 | % | $ | 171 | $ | 163 | 5 | % | |||||||

|

Average deposits (in billions of dollars) |

154 | 145 | 6 | 152 | 144 | 5 | |||||||||||||

|

Net credit losses as a percentage of average loans |

3.60 | % | 4.99 | % | |||||||||||||||

|

Revenue by business |

|||||||||||||||||||

|

Retail banking |

$ | 1,736 | $ | 1,282 | 35 | % | $ | 5,011 | $ | 3,721 | 35 | % | |||||||

|

Citi-branded cards |

2,111 | 2,192 | (4 | ) | 6,189 | 6,569 | (6 | ) | |||||||||||

|

Citi retail services |

1,555 | 1,626 | (4 | ) | 4,535 | 4,702 | (4 | ) | |||||||||||

|

Total |

$ | 5,402 | $ | 5,100 | 6 | % | $ | 15,735 | $ | 14,992 | 5 | % | |||||||

|

Income from continuing operations by business |

|||||||||||||||||||

|

Retail banking |

$ | 340 | $ | 118 | NM | $ | 1,006 | $ | 299 | NM | |||||||||

|

Citi-branded cards |

571 | 577 | (1 | )% | 1,606 | 1,650 | (3 | )% | |||||||||||

|

Citi retail services |

389 | 408 | (5 | ) | 1,201 | 1,202 | — | ||||||||||||

|

Total |

$ | 1,300 | $ | 1,103 | 18 | % | $ | 3,813 | $ | 3,151 | 21 | % | |||||||

NM Not meaningful

15

Net income increased 18%, mainly driven by higher gains on sale of mortgages.

Revenues increased 6% driven by a 47% increase in non-interest revenues from higher gains on sale of mortgages, partly offset by a 2% decline in net interest revenues, mostly due to cards. Revenue from the retail banking business excluding mortgages was essentially flat, as volume growth and improved mix in the deposit and lending portfolios was offset by significant spread compression. The higher gains on sale of mortgages were driven by continued high levels of mortgage refinancing activity, which Citi currently expects will continue into 2013.

With respect to cards, revenues declined 4%. In Citi-branded cards, both average loans and net interest margin declined year-over-year, reflecting continued increased payment rates resulting from consumer deleveraging and the impact of the look-back provisions of The Credit Card Accountability Responsibility and Disclosure Act (CARD Act).(5) In Citi retail services, net interest revenues improved but were offset by declining non-interest revenues, driven by improving credit and the resulting impact on contractual partner payments. On a sequential basis (third quarter of 2012 compared to second quarter of 2012), cards revenues grew 5%, with flat average loans and improved net interest margin. Despite the improvement quarter-over-quarter, Citi expects cards revenues could continue to be negatively impacted by higher payment rates for consumers, reflecting ongoing economic uncertainty and deleveraging as well as Citi's shift to higher credit quality borrowers.

As previously disclosed, as part of its U.S. Citi-branded cards business, Citi (through Citibank, N.A.) issues a co-branded credit card product with American Airlines, the Citi/AAdvantage card. As has been widely-reported, AMR Corporation and certain of its subsidiaries, including American Airlines, Inc. (collectively, AMR), filed voluntary petitions for reorganization under Chapter 11 of the U.S. Bankruptcy Code in November 2011. To date, the ongoing AMR bankruptcy has not had a material impact on the results of operations for U.S. Citi-branded cards, NA RCB , Citicorp or Citi as a whole. However, it is not certain what the outcome of the bankruptcy process will be or whether the impact could be material to the results of operations or financial condition of U.S. Citi-branded cards over time.

Expenses increased 2%, largely due to the higher retail channel mortgage volumes and higher cards network-related expense, partially offset by lower advertising and marketing, reengineering saves and lower repositioning costs.

Provisions decreased 7%, primarily due to lower net credit losses in the cards portfolio partly offset by continued lower loan loss reserve releases ($519 million in the third quarter of 2012 compared to $955 million in the prior-year period). Citi currently expects NA RCB net credit losses could continue to improve slightly from third quarter of 2012 levels, while loan loss reserve releases will likely continue to decline, as delinquency trends have largely stabilized in the cards businesses.

Year-to-date, NA RCB has experienced similar trends to those described above. Net income increased 21% driven by higher non-interest revenue and improvements in credit costs, partially offset by lower net interest revenue and higher expenses.

Revenues increased 5% mainly due to the higher non-interest revenue from the gains on sale of mortgages, partially offset by lower net interest revenue in the cards and retail banking businesses. Net interest revenue was down 3% driven primarily by margin pressure and lower volumes in cards, with average loans lower by 3%. Cards net interest margin was negatively impacted by the look-back provision of the CARD Act, as described above. Revenue from the retail banking business excluding mortgages was down 2% due to spread compression, partially offset by the impact of volume growth and improved product mix.

Expenses increased 3%, primarily driven by higher legal reserves related to the interchange litigation as previously disclosed, and the higher retail channel mortgage volumes and cards network-related expense described above, partially offset by ongoing savings initiatives.

Provisions decreased 21%, largely due to a net credit loss decline of 29%, substantially all of which related to cards (cards net credit losses were down $1.8 billion, or 30%, from the prior year-to-date period). The decline in net credit losses was partially offset by a decrease in loan loss reserve releases of $1.2 billion.

.

- (5)

- The CARD Act requires a review be done once every six months for card accounts where the annual percentage rate (APR) has been increased since January 1, 2009 to assess whether changes in credit risk, market conditions or other factors merit a future decline in APR.

16

EMEA REGIONAL CONSUMER BANKING

EMEA Regional Consumer Banking (EMEA RCB) provides traditional banking and Citi-branded card services to retail customers and small to mid-size businesses, primarily in Central and Eastern Europe, the Middle East and Africa. The countries in which EMEA RCB has the largest presence are Poland, Turkey, Russia and the United Arab Emirates. At September 30, 2012, EMEA RCB had 234 retail bank branches with 3.9 million customer accounts, $4.9 billion in retail banking loans and $12.9 billion in deposits. In addition, the business had 2.5 million Citi-branded card accounts with $2.9 billion in outstanding card loan balances.

|

|

Third Quarter |

|

Nine Months |

|

|||||||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

|

|

%

Change |

%

Change |

|||||||||||||||||

| In millions of dollars, except as otherwise noted | 2012 | 2011 | 2012 | 2011 | |||||||||||||||

|

Net interest revenue |

$ | 257 | $ | 233 | 10 | % | $ | 775 | $ | 723 | 7 | % | |||||||

|

Non-interest revenue |

124 | 146 | (15 | ) | 350 | 487 | (28 | ) | |||||||||||

|

Total revenues, net of interest expense |

$ | 381 | $ | 379 | 1 | % | $ | 1,125 | $ | 1,210 | (7 | )% | |||||||

|

Total operating expenses |

$ | 335 | $ | 344 | (3 | )% | $ | 1,032 | $ | 1,017 | 1 | % | |||||||

|

Net credit losses |

$ | 29 | $ | 49 | (41 | )% | $ | 72 | $ | 144 | (50 | )% | |||||||

|

Credit reserve build (release) |

2 | (32 | ) | NM | (16 | ) | $ | (121 | ) | 87 | |||||||||

|

Provision for unfunded lending commitments |

— | 1 | (100 | ) | (1 | ) | 5 | NM | |||||||||||

|

Provisions for credit losses |

$ | 31 | $ | 18 | 72 | $ | 55 | $ | 28 | 96 | |||||||||

|

Income from continuing operations before taxes |

$ | 15 | $ | 17 | (12 | )% | $ | 38 | $ | 165 | (77 | )% | |||||||

|

Income taxes |

5 | 8 | (38 | ) | 18 | 66 | (73 | ) | |||||||||||

|

Income from continuing operations |

$ | 10 | $ | 9 | 11 | % | $ | 20 | $ | 99 | (80 | )% | |||||||

|

Net income attributable to noncontrolling interests |

2 | 1 | 100 | 4 | 3 | 33 | |||||||||||||

|

Net income |

$ | 8 | $ | 8 | — | $ | 16 | $ | 96 | (83 | )% | ||||||||

|

Average assets (in billions of dollars) |

$ | 9 | $ | 10 | (10 | )% | $ | 9 | $ | 10 | (10 | )% | |||||||

|

Return on assets |

0.35 | % | 0.32 | % | 0.24 | % | 1.28 | % | |||||||||||

|

Average deposits (in billions of dollars) |

12.7 | 12.4 | 2 | 12.5 | 12.6 | (1 | ) | ||||||||||||

|

Net credit losses as a percentage of average loans |

1.54 | % | 2.70 | % | |||||||||||||||

|

Revenue by business |

|||||||||||||||||||

|

Retail banking |

$ | 223 | $ | 215 | 4 | % | $ | 659 | $ | 691 | (5 | )% | |||||||

|

Citi-branded cards |

158 | 164 | (4 | ) | 466 | 519 | (10 | ) | |||||||||||

|

Total |

$ | 381 | $ | 379 | 1 | % | $ | 1,125 | $ | 1,210 | (7 | )% | |||||||

|

Income (loss) from continuing operations by business |

|||||||||||||||||||

|

Retail banking |

$ | (12 | ) | $ | (21 | ) | 43 | % | $ | (40 | ) | $ | (19 | ) | NM | ||||

|

Citi-branded cards |

22 | 30 | (27 | ) | 60 | 118 | (49 | )% | |||||||||||

|

Total |

$ | 10 | $ | 9 | 11 | % | $ | 20 | $ | 99 | (80 | )% | |||||||

|

Foreign Currency (FX) Translation Impact |

|||||||||||||||||||

|

Total revenue—as reported |

$ | 381 | $ | 379 | 1 | % | $ | 1,125 | $ | 1,210 | (7 | )% | |||||||

|

Impact of FX translation(1) |

— | (23 | ) | — | (80 | ) | |||||||||||||

|

Total revenues—ex-FX |

$ | 381 | $ | 356 | 7 | % | $ | 1,125 | $ | 1,130 | — | % | |||||||

|

Total operating expenses—as reported |

$ | 335 | $ | 344 | (3 | )% | $ | 1,032 | $ | 1,017 | 1 | % | |||||||

|

Impact of FX translation(1) |

— | (20 | ) | — | (67 | ) | |||||||||||||

|

Total operating expenses—ex-FX |

$ | 335 | $ | 324 | 3 | % | $ | 1,032 | $ | 950 | 9 | % | |||||||

|

Provisions for credit loans—as reported |

$ | 31 | $ | 18 | 72 | % | $ | 55 | $ | 28 | 96 | % | |||||||

|

Impact of FX translation(1) |

— | (1 | ) | — | (1 | ) | |||||||||||||

|

Provisions for credit loans—ex-FX |

$ | 31 | $ | 17 | 82 | % | $ | 55 | $ | 27 | 104 | % | |||||||

|

Net income—as reported |

$ | 8 | $ | 8 | — | % | $ | 16 | $ | 96 | (83 | )% | |||||||

|

Impact of FX translation(1) |

— | (3 | ) | — | — | (14 | ) | — | |||||||||||

|

Net income—ex-FX |

$ | 8 | $ | 5 | 60 | % | $ | 16 | $ | 82 | (80 | )% | |||||||

- (1)

- Reflects the impact of foreign exchange (FX) translation into U.S. dollars at the current exchange rate for all periods presented.

NM Not meaningful

17

The discussion of the results of operations for EMEA RCB below excludes the impact of FX translation for all periods presented. Presentation of the results of operations, excluding the impact of FX translation, are non-GAAP financial measures. Citi believes the presentation of EMEA RCB's results excluding the impact of FX translation is a more meaningful depiction of the underlying fundamentals of the business. For a reconciliation of certain of these metrics to the reported results, see the table above.

Net income increased 60%, mainly due to higher revenues, partially offset by higher expenses and provisions.

Revenues were up 7%, primarily driven by underlying growth across the products, partly offset by the absence of Akbank, Citi's equity investment in Turkey, which was moved to Corporate/Other in the first quarter of 2012. Net interest revenue was up 18% driven by the absence of Akbank investment funding costs in the current quarter and growth in average deposits of 9%, average retail loans of 18% and average cards loans of 7%, partially offset by spread compression. Interest rate caps on credit cards, particularly in Turkey, and the continued liquidation of a higher yielding non-strategic retail banking portfolio were the main contributors to the lower spreads. Non-interest revenue decreased 12%, mainly reflecting the absence of Akbank, partly offset by higher investment income and cards fees. Year-over-year, cards purchase sales grew 11%, investment sales grew 17% and retail new loan volume grew 23%.

Expenses grew by 3% due to the impact of continued investment spending focused on account acquisition and repositioning charges in Poland and Pakistan.

Provisions increased 82%, due to lower loan loss reserve releases, partially offset by lower net credit losses. Net credit losses continued to improve, declining 35% due to the ongoing improvement in credit quality and the move towards lower risk customers. Citi believes that net credit losses in EMEA RCB have largely stabilized and the loan loss reserve releases could continue to decline or stabilize and thus, overall, provisions could negatively impact the operating results of EMEA RCB in the near term.

Year-to-date, EMEA RCB has experienced similar trends to those described above. Net income declined by 80%, primarily due to lower revenues and higher operating expenses and credit costs.

Revenues were flat, as continued growth in the underlying business was offset by the absence of Akbank since the first quarter of 2012 as described above. Net interest revenue was up 16% driven by the absence of the Akbank investment funding costs as well as growth in deposits and retail loans of 5% and 14% respectively, partially offset by spread compression. Similar to the year-over-year discussion above, interest rate caps on credit cards, particularly in Turkey, and the continued liquidation of a higher yielding non-strategic retail banking portfolio were the main contributors to the lower spreads. Non-interest revenue decreased 24%, mainly reflecting the absence of Akbank. Period-over-period, cards purchase sales grew 17% and retail new loan volume grew 29%.

Expenses increased 9% due to the impact of investment spending and repositioning charges in Poland, Central Europe and Pakistan as well as increased volumes.

Provisions increased $28 million due to lower loan loss reserve releases, partially offset by lower net credit losses of $61 million. Net credit losses continued to improve, declining 43% due to the ongoing improvement in credit quality and a benefit from sale of written-off portfolios in Turkey, Poland and Hungary.

18

LATIN AMERICA REGIONAL CONSUMER BANKING

Latin America Regional Consumer Banking (Latin America RCB) provides traditional banking and Citi-branded card services to retail customers and small to mid-size businesses, with the largest presence in Mexico and Brazil. Latin America RCB includes branch networks throughout Latin America as well as Banco Nacional de Mexico, or Banamex, Mexico's second-largest bank, with over 1,700 branches. At September 30, 2012, Latin America RCB had 2,200 retail branches, with 32.1 million customer accounts, $27.5 billion in retail banking loans and $47.3 billion in deposits. In addition, the business had 13.0 million Citi-branded card accounts with $14.2 billion in outstanding loan balances.

|

|

Third Quarter |

|

Nine Months |

|

|||||||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

|

|

%

Change |

%

Change |

|||||||||||||||||

| In millions of dollars, except as otherwise noted | 2012 | 2011 | 2012 | 2011 | |||||||||||||||

|

Net interest revenue |

$ | 1,687 | $ | 1,654 | 2 | % | $ | 4,970 | $ | 4,836 | 3 | % | |||||||

|

Non-interest revenue |

732 | 763 | (4 | ) | 2,212 | 2,283 | (3 | ) | |||||||||||

|

Total revenues, net of interest expense |

$ | 2,419 | $ | 2,417 | — | $ | 7,182 | $ | 7,119 | 1 | % | ||||||||

|

Total operating expenses |

$ | 1,387 | $ | 1,487 | (7 | )% | $ | 4,114 | $ | 4,348 | (5 | )% | |||||||

|

Net credit losses |

$ | 433 | $ | 406 | 7 | % | $ | 1,263 | $ | 1,238 | 2 | % | |||||||

|

Credit reserve build (release) |

29 | 63 | (54 | ) | 262 | (105 | ) | NM | |||||||||||

|

Provision for benefits and claims |

46 | 38 | 21 | 121 | 98 | 23 | |||||||||||||

|

Provisions for loan losses and for benefits and claims (LLR & PBC) |

$ | 508 | $ | 507 | — | $ | 1,646 | $ | 1,231 | 34 | % | ||||||||

|

Income from continuing operations before taxes |

$ | 524 | $ | 423 | 24 | % | $ | 1,422 | $ | 1,540 | (8 | )% | |||||||

|

Income taxes |

119 | 84 | 42 | 313 | 332 | (6 | ) | ||||||||||||

|

Income from continuing operations |

$ | 405 | $ | 339 | 19 | % | $ | 1,109 | $ | 1,208 | (8 | )% | |||||||

|

Net income (loss) attributable to noncontrolling interests |

— | — | — | (2 | ) | (1 | ) | (100 | )% | ||||||||||

|

Net income |

$ | 405 | $ | 339 | 19 | % | $ | 1,111 | $ | 1,209 | (8 | )% | |||||||

|

Average assets (in billions of dollars) |

$ | 79 | $ | 80 | (1 | )% | $ | 79 | $ | 80 | — | ||||||||

|

Return on assets |

2.04 | % | 1.68 | % | 1.88 | % | 2.02 | % | |||||||||||

|

Average deposits (in billions of dollars) |

44.6 | 45.5 | — | 44.9 | 46.2 | (3 | ) | ||||||||||||

|

Net credit losses as a percentage of average loans |

4.25 | % | 4.43 | % | |||||||||||||||

|

Revenue by business |

|||||||||||||||||||

|

Retail banking |

$ | 1,452 | $ | 1,394 | 4 | % | $ | 4,278 | $ | 4,125 | 4 | % | |||||||

|

Citi-branded cards |

967 | 1,023 | (5 | ) | 2,904 | 2,994 | (3 | ) | |||||||||||

|

Total |

$ | 2,419 | $ | 2,417 | — | $ | 7,182 | $ | 7,119 | 1 | % | ||||||||

|

Income from continuing operations by business |

|||||||||||||||||||

|

Retail banking |

$ | 214 | $ | 169 | 27 | % | $ | 639 | $ | 700 | (9 | )% | |||||||

|

Citi-branded cards |

191 | 170 | 12 | 470 | 508 | (7 | ) | ||||||||||||

|

Total |

$ | 405 | $ | 339 | 19 | % | $ | 1,109 | $ | 1,208 | (8 | )% | |||||||

|

Foreign Currency (FX) Translation Impact |

|||||||||||||||||||

|

Total revenue—as reported |

$ | 2,419 | $ | 2,417 | — | % | $ | 7,182 | $ | 7,119 | 1 | % | |||||||

|

Impact of FX translation(1) |

— | (151 | ) | — | (536 | ) | |||||||||||||

|

Total revenues—ex-FX |

$ | 2,419 | $ | 2,266 | 7 | % | $ | 7,182 | $ | 6,583 | 9 | % | |||||||

|

Total operating expenses—as reported |

$ | 1,387 | $ | 1,487 | (7 | )% | $ | 4,114 | $ | 4,348 | (5 | )% | |||||||

|

Impact of FX translation(1) |

— | (101 | ) | — | (346 | ) | |||||||||||||

|

Total operating expenses—ex-FX |

$ | 1,387 | $ | 1,386 | — | % | $ | 4,114 | $ | 4,002 | 3 | % | |||||||

|

Provisions for LLR & PBC—as reported |

$ | 508 | $ | 507 | — | % | $ | 1,646 | $ | 1,231 | 34 | % | |||||||

|

Impact of FX translation(1) |

— | (47 | ) | — | (130 | ) | |||||||||||||

|

Provisions for LLR & PBC—ex-FX |

$ | 508 | $ | 460 | 10 | % | $ | 1,646 | $ | 1,101 | 50 | % | |||||||

|

Net income—as reported |

$ | 405 | $ | 339 | 19 | % | $ | 1,111 | $ | 1,209 | (8 | )% | |||||||

|

Impact of FX translation(1) |

— | (9 | ) | — | — | (69 | ) | — | |||||||||||

|

Net income—ex-FX |

$ | 405 | $ | 330 | 23 | % | $ | 1,111 | $ | 1,140 | (3 | )% | |||||||

- (1)

- Reflects the impact of foreign exchange (FX) translation into U.S. dollars at the current exchange rate for all periods presented.

NM Not meaningful

19

The discussion of the results of operations for Latin America RCB below excludes the impact of FX translation for all periods presented. Presentation of the results of operations, excluding the impact of FX translation, are non-GAAP financial measures. Citi believes the presentation of Latin America RCB's results excluding the impact of FX translation is a more meaningful depiction of the underlying fundamentals of the business. For a reconciliation of certain of these metrics to the reported results, see the table above.

Net income increased 23%, mainly driven by higher revenues, partially offset by higher credit costs.

Revenues were up 7%, primarily due to loan growth across the region, particularly in Mexico. The business experienced increased demand for a number of different loans, predominantly personal installment loans and credit cards. Net interest revenue increased 8% due to growth in loans and deposits, partially offset by continued spread compression from higher credit quality customers. Average loans increased in both retail banking and cards, by 27% and 13%, respectively, and deposits grew by 4%. Non-interest revenue increased 3%, primarily due to increased business volumes in Citi's private pension fund and insurance businesses.

Expenses were flat, as higher volume-related expenses were offset by lower advertising and increased efficiency saves.

Provisions increased 10% due to higher net credit losses resulting from the growing loan portfolio, in particular personal loans.

Year-to-date, Latin America RCB has experienced similar trends to those described above. Net income declined 3% as increased credit provisions were mostly offset by higher revenues.

Revenues increased 9% primarily due to higher volumes, mostly in Mexico personal loans and cards. This increase in volumes, which was partly offset by spread compression, resulted in net interest revenue increasing 10%. Non-interest revenue was up 5%, primarily due to the increased business volumes in Citi's pension fund and insurance businesses.

Expenses increased 3% primarily due to higher volumes, account acquisition and sales incentives, partially offset by reengineering actions.

Provisions increased 50% mainly as a result of loan loss reserve builds driven by the loan growth.

20

ASIA REGIONAL CONSUMER BANKING