United States

Securities and Exchange Commission

Washington, D.C. 20549

FORM 20-F

(MarkOne)

¨

REGISTRATION STATEMENT PURSUANT TO SECTION 12(b) OR (g) OF THE SECURITIES EXCHANGE ACT OF 1934

OR

☒ ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934

For the fiscal year ended December 31, 2017

OR

¨

TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934

OR

¨

SHELL COMPANY REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934

Commission file number 1-37791

COCA-COLA EUROPEAN PARTNERS PLC

(Exact name of Registrant as specified in its charter)

England and Wales

(Jurisdiction of incorporation or organization)

Bakers Road, Uxbridge, UB8 1EZ, United Kingdom

(Address of principal executive offices)

Contact

(+44 (0)1895 231 313, Secretariat@ccep.com, Bakers Road, Uxbridge, UB8 1EZ, United Kingdom)

Securities registered or to be registered pursuant to Section 12(b) of the Act:

|

Title of each class

|

|

Name on each exchange on which registered

|

|

Ordinary Shares of €0.01 each

|

|

New York Stock Exchange

|

Securities registered or to be registered pursuant to Section 12(g) of the Act: None.

Securities for which there is a reporting obligation pursuant to Section 15(d) of the Act: None.

Indicate the number of outstanding shares of each of the issuer’s classes of capital or common stock as of the close of the period covered by the annual report: 484,586,428 Ordinary Shares of €0.01 each

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act Yes ☒ No ☐

If this Report is an annual or transition report, indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or 15(d) of the Securities Exchange Act of 1934 Yes ☐ No ☒

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days: Yes ☒ No ☐

Indicate by check mark whether the registrant has submitted electronically and posted on its corporate Web site, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T(§232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files). Yes ☒ No ☐

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, or an emerging growth company. See definition of large accelerated filer,"accelerated filer, and "emerging growth company" in Rule 12b-2 of the Exchange Act.

|

Large accelerated filer

|

☒

|

Accelerated filer

|

☐

|

Non-accelerated filer

|

☐

|

|

Emerging growth company

|

☐

|

||||

Indicate by check mark which basis of accounting the registrant has used to prepare the financial statements included in this filing.

|

U.S. GAAP

|

☐

|

International Financial Reporting Standards as issued by the International Accounting Standards Board

|

☒

|

Other

|

☐

|

If “Other” has been checked to the previous question indicate by check mark which financial statement item the registrant has elected to follow: Item 17 ☐ Item 18 ☐

If this is an annual report, indicated by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act). Yes ☐ No ☒

|

P a g e |

ii

|

|

TABLE OF CONTENTS

|

|||

|

INTRODUCTION

|

|||

|

AT A GLANCE

|

|||

|

STRATEGIC REPORT

|

|||

|

CHAIRMAN’S LETTER

|

|||

|

CEO’S LETTER

|

|||

|

STRATEGY

|

|||

|

PERFORMANCE INDICATORS

|

|||

|

BUSINESS MODEL

|

|||

|

BUSINESS AND FINANCIAL REVIEW

|

|||

|

SUSTAINABILITY

|

|||

|

PRINCIPAL RISKS

|

|||

|

RISK FACTORS

|

|||

|

VIABILITY STATEMENT

|

|||

|

GOVERNANCE AND DIRECTORS’ REPORT

|

|||

|

CHAIRMAN’S INTRODUCTION TO GOVERNANCE AND DIRECTORS’ REPORT

|

|||

|

BOARD OF DIRECTORS

|

|||

|

SENIOR MANAGEMENT

|

|||

|

CORPORATE GOVERNANCE REPORT

|

|||

|

NOMINATION COMMITTEE CHAIRMAN’S LETTER

|

|||

|

NOMINATION COMMITTEE REPORT

|

|||

|

AUDIT COMMITTEE CHAIRMAN’S LETTER

|

|||

|

AUDIT COMMITTEE REPORT

|

|||

|

DIRECTORS’ REMUNERATION REPORT

|

|||

|

STATEMENT FROM THE REMUNERATION COMMITTEE CHAIRMAN

|

|||

|

OVERVIEW OF THE REMUNERATION POLICY

|

|||

|

2017 REMUNERATION AT A GLANCE

|

|||

|

ANNUAL REPORT ON REMUNERATION

|

|||

|

DIRECTORS’ REPORT

|

|||

|

DIRECTORS’ RESPONSIBILITIES STATEMENT

|

|||

|

FINANCIAL STATEMENTS

|

|||

|

INDEPENDENT AUDITORS’ REPORTS

|

|||

|

CONSOLIDATED FINANCIAL STATEMENTS

|

|||

|

NOTES TO THE CONSOLIDATED FINANCIAL STATEMENTS

|

|||

|

COMPANY FINANCIAL STATEMENTS

|

|||

|

NOTES TO THE COMPANY FINANCIAL STATEMENTS

|

|||

|

OTHER INFORMATION

|

|||

|

OTHER GROUP INFORMATION

|

|||

|

FORM 20-F TABLE OF CROSS REFERENCES

|

|||

|

EXHIBITS

|

|||

|

GLOSSARY

|

|||

|

USEFUL ADDRESSES

|

|||

None of the websites referred to in this Annual Report on Form 20-F for the year ended 31 December 2017 (the Form 20-F), including where a link is provided, nor any of the information contained on such websites is incorporated by reference in the Form 20-F.

|

|

P a g e |

1

|

Welcome to the Coca-Cola European Partners plc 2017 Annual Report

DELIGHTING CUSTOMERS AND CONSUMERS

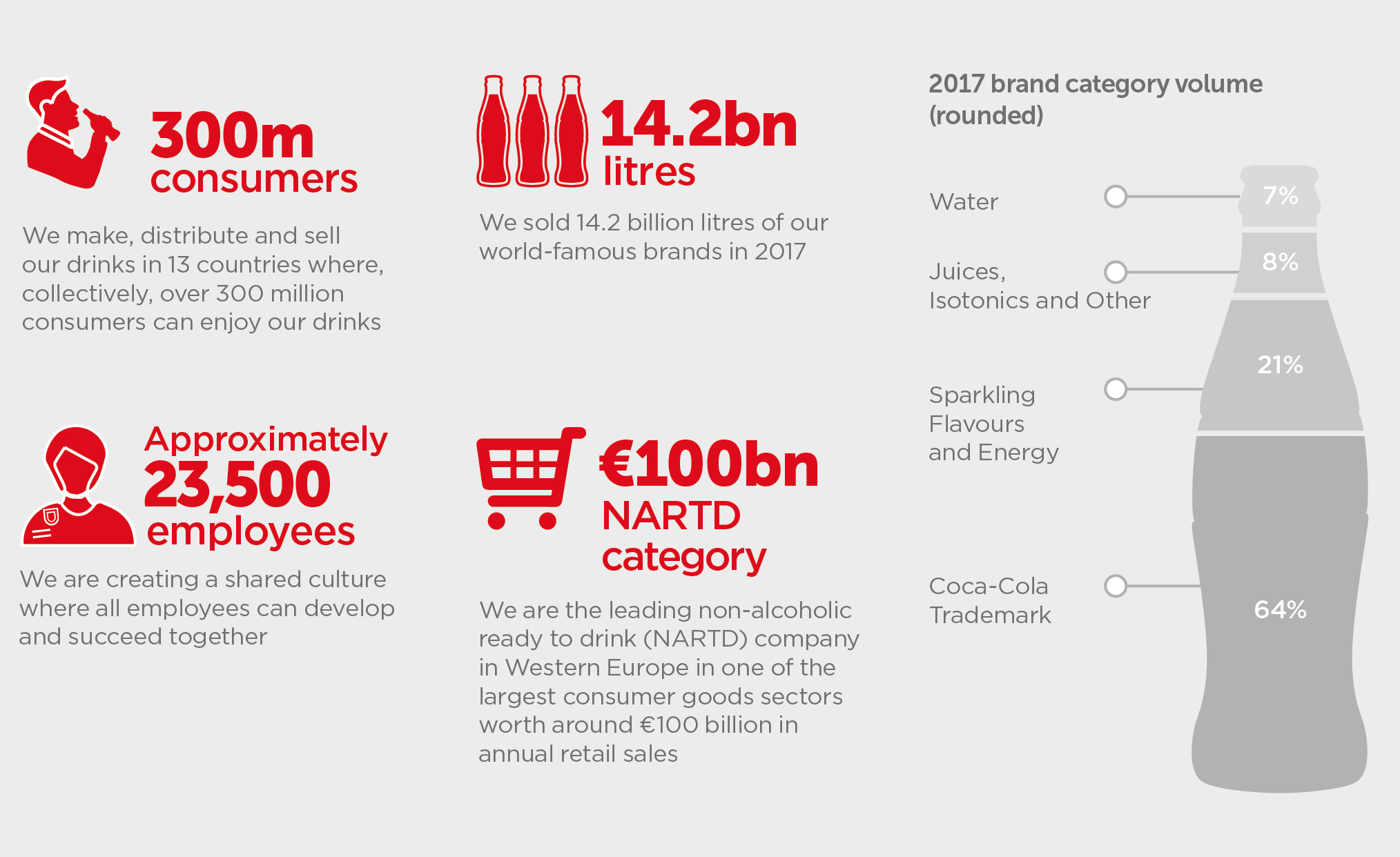

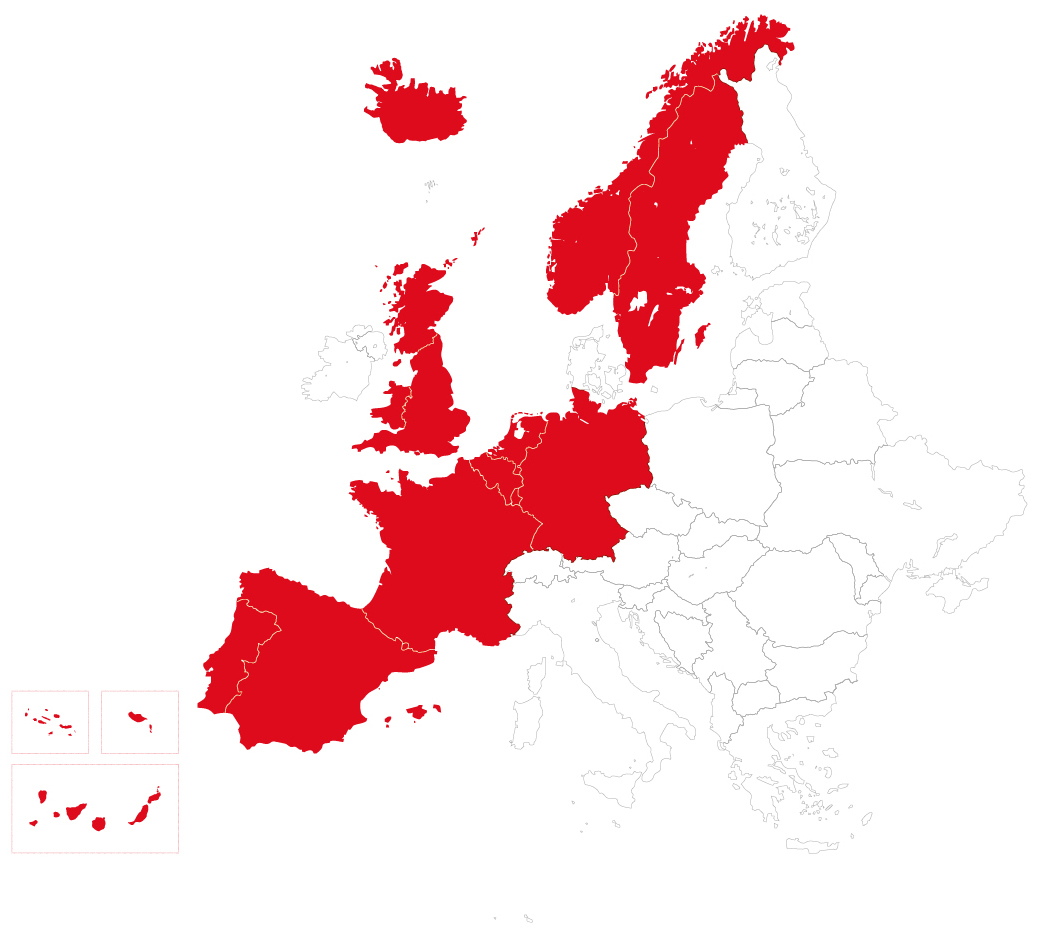

Coca-Cola European Partners is a leading consumer goods company and the world’s largest independent Coca-Cola bottler by revenue, operating in 13 countries and employing around 23,500 people. We are proud of our strong heritage in Western Europe and, as Coca-Cola European Partners, we are establishing a compelling track record and platform for profitable growth through our combined experience, scale and reach.

Over 300 million people can enjoy our drinks in Western Europe and, working together with The Coca-Cola Company, we are leading the way in our markets, offering consumers a greater choice of drinks with reduced or no sugar, holding ourselves accountable for our packaging and expanding the contribution we make to society. We are taking action on sustainability to build a better future, for people and for the planet. We work closely with customers to understand their needs and priorities and develop tailored strategies to deliver shared value.

In our first 18 months, we have become a leading consumer goods company capable of delivering long-term growth, and we are on a journey to be the world’s most sustainable and valuable Coca-Cola bottler creating increased shareholder value.

|

|

P a g e |

2

|

GREAT BEVERAGES, SERVICE AND PEOPLE

We are the world’s largest independent Coca-Cola bottler and one of Europe’s leading consumer goods companies

At our core, we provide customers and consumers with great beverages and great service, creating shared and sustainable value.

We look at our business through two lenses: consumer categories and customer channels.

In each category, we are meeting changing consumer preferences by expanding our offering and re-shaping our portfolio to offer a wider range of drinks including more low/no-sugar brands and more innovative packages.

In each channel, we are collaborating with customers to drive joint value creation through unparalleled execution, having the right product available at the right price across more outlets and occasions.

We are focused on delivering world-class customer service to existing customers and expanding the range of customers we serve. This will include building new relationships in the e-commerce and leisure channels and with institutions.

|

|

P a g e |

3

|

Achieving sustainable growth

Our goal is to deliver long-term and sustainable growth and create shared value. To do this, we are:

|

•

|

Investing in our existing portfolio and launching new brands with scale and impact to offer a drink for every taste and occasion

|

|

•

|

Working closely with existing and new customers to reach more consumers in more outlets

|

|

•

|

Improving our route to market so our products are more available and visible to consumers

|

Our growth culture

Focus on customers & front line

We do everything we can to help the front line team develop our business and delight our customers.

Passion for growth

We show our determination to grow the business, take accountability and develop ourselves.

Listening & caring

We listen to what our colleagues, customers, consumers and communities tell us – seeking to understand and take the right actions.

Empowered to win together

We work together to win, encouraging diverse ideas and supporting people at every level to make decisions.

Execute with speed & agility

We move quickly, find ways to remove barriers and make things happen.

Our relationship with The Coca-Cola Company (TCCC)

Over the last year we have strengthened our relationship with TCCC, developing a shared long-term plan to create value and a joint sustainability action plan for Western Europe.

TCCC makes and sells concentrates, beverage bases and syrups to bottling operations, owns the brands and is responsible for consumer brand marketing. We license these brands and purchase the concentrate to sell, make and distribute the packaged beverages to our customers and vending partners, who then retail our products to consumers. We work closely with our customers to execute localised strategies based on a vision for growth that is shared with TCCC.

|

|

P a g e |

6

|

CHAIRMAN’S LETTER

I am proud of what we have achieved in our first 18 months. We have delivered consistent profitable growth and shared value for Coca-Cola European Partners (CCEP), our customers, partners, employees and shareholders.

In 2017, CCEP has established itself as a leading consumer goods company and made great progress in setting the foundations for long-term sustainable growth.

Western Europe remains a dynamic market, with ongoing political, social and economic changes. 2017 has ushered in new governments in some of the countries in which we operate, increased governance requirements for businesses, and, in our own industry, an evolved retail landscape through customer mergers, increased regulation and changes in shoppers’ habits.

While our business is realistic about these challenges, CCEP is well positioned to take advantage of the opportunities that come with change.

Footprint for growth

We have made clear choices about CCEP’s strategy and operating model, putting the customer at the heart of everything we do and focusing on the front line where we can have the greatest impact in the market.

We have increased investment in key areas of the business. This includes putting the best coolers in the right places so consumers can enjoy our drinks wherever they are. Our production and distribution network has also been improved to support our growing range of products.

We continued to invest in our sales force to make sure it remains a powerful competitive strength, particularly through harnessing new technology. We have improved our route to market so our products are more visible and available and deepened relationships with world class customer management.

We are working closely with our partners, particularly The Coca-Cola Company, to be a total beverage company, offering consumers a drink for every occasion including low and no-sugar options. Last year, this included the launch of new brands, such as Royal Bliss, as well as innovations that helped grow existing strong brands, like trademark Coca-Cola, Fanta and Monster. In premium water and tea, we introduced new brands and will expand existing brands geographically, including Honest and GLACÉAU Smartwater.

Sustainable future

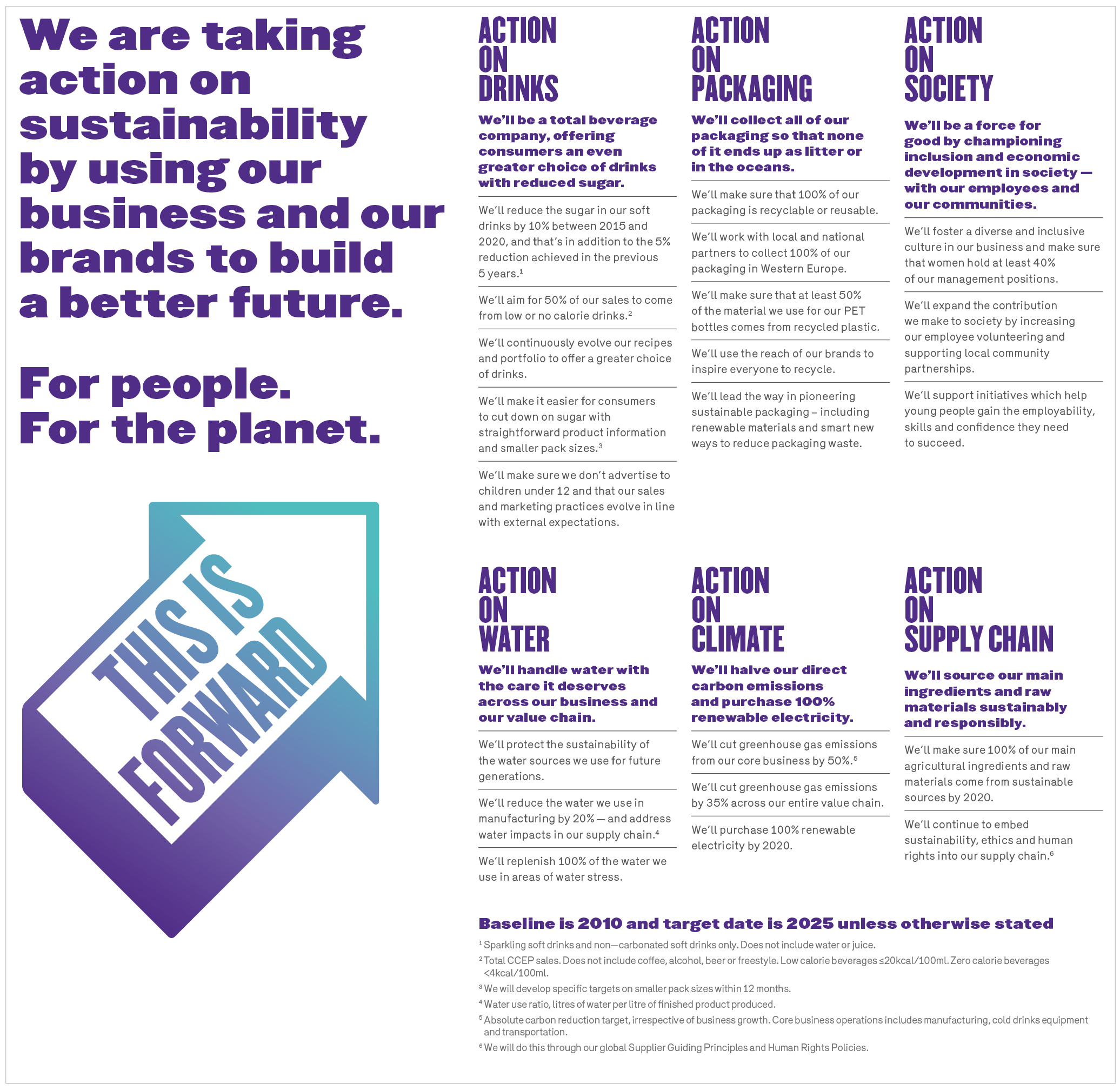

We are also working hard with our partners to make and sell our brands in a responsible and sustainable way. In November, CCEP and The Coca-Cola Company in Western Europe launched an ambitious new sustainability action plan, This is Forward. You can read the plan in full at www.ccep.com/pages/thisisforward. I am proud of the plan which sets out a clear direction of how we intend to work together, using the strength of our businesses and our brands to build a better future.

The plan is based on three priority actions on drinks, packaging and society, which are underpinned by three supporting actions that are core to our business operations: climate, water and supply chain. There are 21 goals, each one identified and developed in the context of the global challenges that face our communities, our society and our business today.

While ambitious, our action plan builds upon 10 years of focused work on sustainability across Western Europe. Importantly, our sustainability action plan, is the result of listening to our stakeholders - including governments, Non-Governmental Organisations, customers, suppliers - as well as thousands of consumers and employees, to ensure we deliver the changes that matter most to all of us.

|

|

P a g e |

7

|

Strength in people

CCEP’s employees continue a proud legacy in Western Europe and combine expert, local knowledge with a passion for our brands and business. I am grateful for their dedication and all they do every day to serve our customers and communities.

I would also like to thank my fellow Directors who have brought their wisdom and leadership to bear on all aspects of our business. I would particularly like to express my gratitude to Francisco Ruiz de la Torre Esporrín and Sandy Douglas, both of whom are stepping down to dedicate more time to their other roles. Francisco brought a fresh perspective and Sandy a wealth of experience of the Coca-Cola system, particularly drawing from the North American bottling business. I am pleased to welcome Álvaro Gómez-Trénor Aguilar and Francisco Crespo Benítez to the Board.

With the Board, I have had the opportunity to visit plants and markets in Spain, Great Britain and Germany. I have also enjoyed taking part in an Accelerate Performance programme for all our leaders, which has been designed to embed our new culture and strategy with company leaders. I have also been on the panel at major diversity network events in Great Britain and France. I have been consistently impressed with the quality and engagement of our people and the progress we are making together.

We are committed to being a company where people are proud to work and where success is strengthened through mutual growth. I believe we have the right team in place to do this. Under the leadership of Damian Gammell and his executive team, we are creating a culture that is agile and flexible, and values diversity and inclusion.

Finally, I would like to thank all of our shareholders for their support. 2018 will build on the strong progress we have made as CCEP. We will continue to listen to and work closely with all our partners and stakeholders to ensure we can accelerate our performance and the value we create together.

Sol Daurella

Chairman

“I am proud of what we have achieved in our first 18 months. We have delivered consistent profitable growth and shared value for CCEP, our customers, partners, employees and shareholders.”

|

|

P a g e |

8

|

CEO’S LETTER

This is an exciting time to be a leader in the non-alcoholic ready to drink category in Western Europe. The demand for innovation in great tasting drinks, packages and brands has never been greater, and Coca-Cola European Partners (CCEP) is ready to meet the consumer challenges and opportunities.

Our goal is clear: to work closely with new and existing customers to make even more great beverages available to more consumers, creating long-term sustainable and profitable growth. We made good progress in 2017, delivering comparable revenue growth of 1.5%.

With the creation of CCEP, we are uniquely positioned to do this through our local footprint and unrivalled sales force. We are able to operate with scale across 13 countries where we make, sell and distribute our products. At the same time, we support a wide range of customer outlets across Western Europe.

Our success is built on three fundamental elements: our portfolio of great brands, the great service and execution we provide to our customers, and our great people who make this happen every day.

A drink for every taste and occasion

Together with our partners at The Coca-Cola Company, our goal is to create a portfolio of beverages that caters for every taste and occasion. We are delivering on this through innovation and growth in leading brands, including Coca-Cola trademark brands, while also bringing new beverages to market.

2017 demonstrates this strategy is creating value. Coca-Cola Zero Sugar continues to be popular with consumers, with volume growth of approximately 15% in 2017. We are also giving consumers more choice across a range of popular brands by introducing new flavours, low or no-sugar variants, and contemporary and sustainable packaging in a variety of sizes.

In May 2017, we relaunched Fanta with a new logo, new recipe and new bottle. We built on a successful launch with a fun and engaging Halloween campaign, limited edition packaging and in-store execution. Sparkling flavours and energy grew 4% in volume in 2017, driven in part by Fanta’s success.

Our presence in energy and emerging drinks segments, such as ready to drink tea, is also growing. Monster, supported by the exciting partnership with Lewis Hamilton, contributed to 16% volume growth in energy in the final quarter of 2017. We also are increasing our presence in adult sparkling drinks, with the launch of Royal Bliss in Spain, the Finley brand in several markets, and the relaunch of Schweppes in Great Britain.

In 2018, we will continue this strategy, supporting the growth of our core brands and further new product development, including the expansion of the Honest and GLACÉAU Smartwater brands in our markets, and the launch of Fuze tea and AdeZ - a plant based smoothie with nuts, seeds and fruit.

Winning with customers

Our focus on value creation starts with our customers, who we put at the heart of every aspect of our business. CCEP will be known for world class customer management and we have a relentless focus on great execution store by store and street by street.

At the forefront of this is our 6,000 strong sales force, which now visits 12 outlets a day on average. In 2017, our focus has been on empowering our sales force to create more value from each visit, through new technology and merchandising. We placed an additional 138,000 coolers into more outlets and increased our coverage of important channels outside grocery, including hotels, restaurants, cafes, institutions and offices.

|

|

P a g e |

9

|

This will continue in 2018, as will efforts to improve our route to market, by working more closely with wholesalers and other partners to better support the growth of all our customers. We are also working with new digital platforms, such as online ordering and customer portals, to improve service and availability.

Delivering sustainable growth

I am confident that the people who work for CCEP and the entrepreneurial culture that is emerging will accelerate our performance. We have invested in developing the capabilities and behaviours that are fundamental to our future success. Our focus is on instilling agile ways of working, creating an environment where people are empowered to win together, and inspiring a passion for growth.

Our stakeholders also have big expectations of how we do business and we are holding ourselves accountable for the impact we have on society. Together with The Coca-Cola Company in Western Europe, our new sustainability action plan advances the progress we are making to reduce sugar in our drinks, recover and recycle our packaging, and be a force for good in our communities.

Our performance in 2017 demonstrates that we are making the right strategic choices. We delivered against all key metrics set out in our financial framework to generate profitable growth and create value for shareholders. This is made possible by our close alignment with The Coca-Cola Company and the support from our experienced leadership team and Board of Directors.

With a solid strategy for long-term growth and a great team, our focus for 2018 is to maintain this momentum, continuing to give customers and consumers the great service and great beverages they want.

Thank you for investing in CCEP. I look forward to continuing our journey with you in 2018.

Damian Gammell

Chief Executive Officer

“Our success is built on three fundamental elements: our portfolio of great brands, the great service and execution we provide to our customers, and our great people who make this happen.”

|

|

P a g e |

10

|

STRATEGY

We are making clear choices to increase our focus on the customer and expand our portfolio to become a total beverage company. This is central to our journey to becoming a great company and the world’s best bottler and key to our ultimate objective: long-term and sustainable growth.

Great beverages

We are committed to delivering sustainable revenue growth from our Coca-Cola trademark drinks, through new flavours, mini cans and premium glass bottles. In 2017 we relaunched Fanta with a new logo, a new recipe and new flavours and we will do the same for Sprite in 2018. We will also continue to expand our portfolio into new categories, launching products - like Fuze and AdeZ - with scale and impact.

Great service

We work closely with existing customers, creating long-term plans for shared value creation. At the same time, we will continue to grow the number of customers and outlets we reach so our great products are always within reach of consumers. That also means improving our route to market by working with wholesalers and developing new ways of bringing our products to the consumer.

Great people

Central to achieving our ambitions is the creation of a culture and environment that empowers everyone in our business to be successful. We will harness efficiencies and share best practice across Coca-Cola European Partners but we are locally led and will always cater for the specific demands of our markets.

We will move quickly and focus on progress over perfection. We will encourage diverse ideas and support people in every part of the business to make decisions. We will listen to what customers, consumers, colleagues and communities tell us so we can take the right actions.

Action on sustainability

This is Forward is our sustainability action plan and a critical part of our long-term business strategy. It has been developed jointly with The Coca-Cola Company in Western Europe. It sets out how we will grow our business in a responsible and sustainable way and how we intend to play a meaningful role in helping to address many of the key societal issues that people are most concerned about. We have made bold leadership commitments on drinks, packaging and society and supporting commitments on water, supply chain and climate.

|

|

P a g e |

11

|

PERFORMANCE INDICATORS

Tracking our performance in 2017

|

Revenue*

|

||||

|

€11.1 billion

|

||||

|

Operating profit*

|

Free cash flow*

|

Diluted earnings per share*

|

||

|

€1.5 billion

on a comparable basis

|

€1.0 billion

|

€2.12

on a comparable basis

|

||

|

Lost time incident rate

|

Water use ratio

|

Energy use ratio

|

||

|

1.23

Calculations based upon number of lost time incidents in 2017 per 100 full time equivalent employees.

|

1.61

litres of water used/litre of product produced

Calculations based upon total water usage of our manufacturing sites, based upon site invoice data, divided by the total number of litres produced in 2017.

|

0.32

MJ/litre of product produced

Calculations based upon total energy usage of our manufacturing sites, based upon monthly site invoice and meter data, divided by the total number of litres of product produced in 2017.

|

||

*Refer to page 21 for a reconciliation of GAAP to non-GAAP figures

|

|

P a g e |

12

|

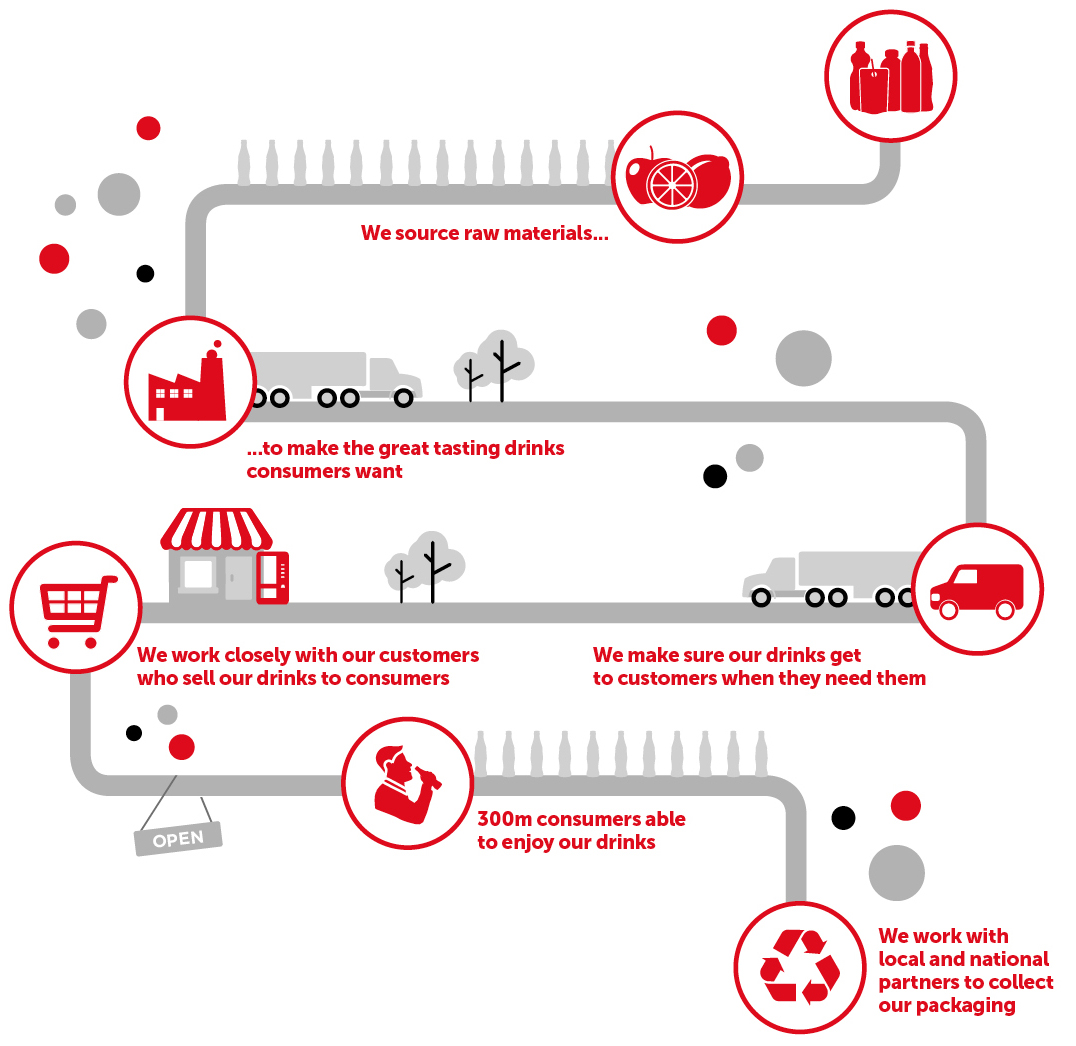

BUSINESS MODEL

We create long-term and sustainable value by making, distributing and selling the world’s most loved drinks and delivering excellent service to our customers. Our success is made possible by our culture and the passion and commitment of our employees.

|

|

P a g e |

13

|

We source raw materials...

We use raw materials such as water, sugar beet, coffee, juices and syrup to make our drinks.

We also rely on packaging materials like PET, pulp and paper to make our packaging.

We require all our suppliers to meet our strict targets around

workplace policies and practices, health and safety, ethics and human rights, environmental protection and business integrity.

As part of our sustainability action plan we’ll make sure 100% of our main agricultural ingredients and raw materials come from sustainable sources by 2020.

...to make the great tasting drinks consumers want

Our manufacturing sites make and bottle our wide range of drinks. We are constantly improving our manufacturing facilities and investing in new technologies to make them more efficient and safer for our employees. 93% of the drinks we sell are produced and marketed in the country in which they are consumed.

We make sure our drinks get to customers when they need them

Working with logistics partners and our own logistics and distribution teams to get our products to customers in the most efficient and sustainable way possible.

We work closely with our customers who sell our drinks to consumers

We work with a huge range of customers – from small local shops to sports stadiums and your favourite bar – so consumers can enjoy one of our great products wherever they are and whenever they want. We also provide coolers and vending machines so people can find our drinks on the go. We work closely with large retail chains, like supermarkets and wholesalers.

We work with local and national partners to collect our packaging

Although all of our bottles and cans are 100% recyclable – they don’t always end up being recycled.

We are determined to do more and lead the way towards a circular economy where 100% of our packaging can be collected, reused or recycled, and where none of it ends up as litter or in the oceans.

The resources and relationships we rely on

Our customers

We strive to be our customers’ preferred partner and create value together through our response to changing consumer and shopper preferences and retail trends. We are uniquely close to our customers, with thousands of our employees calling on our customers every day. Our operating model is customer-centric and focused on the front line, and we aim to deliver the strongest execution and reach a broad range of outlets in the marketplace, all the while making it easier to do business with us.

Our employees

Our success depends on our people – growth for our business goes hand in hand with growth for our employees. We respect each other and support a workplace where people with different perspectives belong, are heard and have equal opportunity. We build the engagement and development of our employees into our business plans, enabling a diverse and local workforce that contributes to the communities where we operate. We also make long-term investments in technology and facilities that equip our people for success.

Our franchisors

We conduct our business primarily under agreements with The Coca-Cola Company and a limited number of other franchisors. These agreements generally give us the exclusive right to sell, distribute and, in most cases, make beverages in approved packaging in specified territories. We have shared long-term growth plans that enable us to create value together.

Our suppliers

Our suppliers are critical partners for our business. We believe collaboration and innovation throughout our supply chain are essential in advancing our sustainable growth. We work with a network of about 19,000 suppliers across our markets, covering commodities and services such as ingredients, packaging, energy, equipment, building and facilities, fleet and logistics services, sales and marketing services, IT and telecoms, general administration and professional services.

Our communities

We recognise the economic, social and environmental impact our business has on our communities, and we seek to make a positive contribution to society building on our strong local heritage and presence. Continued success is critical for the people who work for us and the communities in which we operate. We work with them to find solutions and create opportunities for the future.

|

|

P a g e |

14

|

BUSINESS AND FINANCIAL REVIEW

Our business

Coca-Cola European Partners plc (CCEP) is the largest independent Coca-Cola bottler by revenue, operating in 13 countries and employing around 23,500 people. We are proud of our strong heritage in Western Europe, and as CCEP, we are establishing a compelling track record and platform for profitable growth through our combined experience, scale and reach.

CCEP was created on 28 May 2016 through the Merger of Coca-Cola Enterprises, Inc., (CCE), Coca-Cola Erfrischungsgetränke A.G. (CCEG) and Coca-Cola Iberian Partners, S.L.U. (CCIP). CCEP is a publicly traded UK domiciled company listed on Euronext Amsterdam, New York Stock Exchange, Euronext London and the continuous market of the Spanish Stock exchange (ticker symbol: CCE).

Over 300 million people can enjoy our drinks in Western Europe, and working together with The Coca-Cola Company, we are leading the way in our markets, offering consumers a greater choice of drinks with reduced or no sugar, holding ourselves accountable for our packaging and expanding the contribution we make to society. We are taking action on sustainability by using our business to build a better future, for people and for the planet. We work closely with customers to understand their needs and priorities and develop tailored strategies to deliver shared value.

In our first 18 months, we have become a leading consumer goods company capable of delivering long-term growth, and we are on a journey to be the world’s most sustainable and valuable Coca-Cola bottler creating increased shareholder value.

Note regarding the presentation of non-GAAP financial information

We use certain alternative performance measures (non-GAAP performance measures) to make financial, operating and planning decisions and to evaluate and report performance. We believe these measures provide useful information to investors, and as such, where clearly identified, we have included certain alternative performance measures in this document to allow investors to better analyse our business performance and allow for greater comparability. To do so, where indicated, we have given effect to the Merger as if it had occurred at the beginning of 2016, thereby including the financial results of CCE, CCEG (Germany) and CCIP (Iberia) along with other adjustments as described below. We have also excluded items affecting the comparability of period-over-period financial performance as described in the tables below.

The alternative performance measures included herein should be read in conjunction with and do not replace the directly reconcilable GAAP measure.

Additionally, we provide certain forward-looking non-GAAP financial Information, which management uses for planning and measuring performance. We are not able to reconcile forward looking non-GAAP measures to reported measures without unreasonable efforts because it is not possible to predict with a reasonable degree of certainty the actual impact or exact timing of items that may impact comparability throughout 2018.

For purposes of this document, the following terms are defined:

‘

As reported

’ includes the financial results of CCE only, as the accounting predecessor, for all periods prior to 27 May 2016 and combined CCEP (CCE, Germany and Iberia) for the period from 28 May 2016 for all periods presented after that date.

‘

Comparable

’ represents results excluding items impacting comparability during the periods presented. Items impacting comparability include restructuring charges, merger and integration related costs, out of period mark-to-market impact of hedges, litigation provisions and net tax items relating to rate and law changes. Such items are excluded from our comparable results in order to provide a better understanding of business performance and allow for greater comparability. Additionally, for periods prior to 27 May 2016, comparable includes the results of CCE, Germany and Iberia as if the Merger had occurred at the beginning of 2016 along with acquisition accounting and the additional debt financing costs incurred by CCEP in connection with the Merger. Comparable volume is also adjusted for selling days.

‘

Fx-neutral

’ represents the comparable results excluding the impact of foreign exchange rate changes during the periods presented. Foreign exchange impact is calculated by recasting current year results at prior year exchange rates.

‘

Free cash flow

’ is defined as net cash flows from operations, less capital expenditures and interest paid, plus proceeds from capital disposals. Management utilises free cash flow as a measure of the Group’s cash generation from operating activities, taking into account investments in property, plant and equipment and non-discretionary interest payments.

|

|

P a g e |

15

|

‘

Adjusted EBITDA

’ is defined as profit after tax plus taxes, net finance costs, non-operating items, depreciation, amortisation and adjusted for items impacting comparability. Management utilises Adjusted EBITDA and the ratio of net debt to Adjusted EBITDA to evaluate operating performance in the context of the Group’s targeted financial leverage.

|

Key financial measures

(A)

Unaudited, fx impact calculated by recasting current year results at prior year rates

|

Year Ended 31 December 2017

|

|||||||||||||||||

|

€ million

|

% change vs. prior year

|

|||||||||||||||||

|

As Reported

|

Comparable

|

Fx-Impact

|

|

As Reported

|

|

Comparable

|

|

Fx-Impact

|

|

Comparable fx‑neutral

|

|

|||||||

|

Revenue

|

11,062

|

11,055

|

(142

|

)

|

21.0

|

%

|

1.5

|

%

|

(1.5

|

)%

|

3.0

|

%

|

||||||

|

Cost of sales

|

6,772

|

6,739

|

(85

|

)

|

21.5

|

%

|

2.0

|

%

|

(1.5

|

)%

|

3.5

|

%

|

||||||

|

Operating expenses

|

3,030

|

2,838

|

(31

|

)

|

12.5

|

%

|

(2.5

|

)%

|

(1.0

|

)%

|

(1.5

|

)%

|

||||||

|

Operating profit

|

1,260

|

1,478

|

(26

|

)

|

48.0

|

%

|

9.0

|

%

|

(1.5

|

)%

|

10.5

|

%

|

||||||

|

Profit after taxes

|

688

|

1,035

|

(19

|

)

|

25.5

|

%

|

13.0

|

%

|

(2.0

|

)%

|

15.0

|

%

|

||||||

|

Diluted earnings per share (€)

|

1.41

|

2.12

|

(0.04

|

)

|

(0.5

|

)%

|

13.0

|

%

|

(2.0

|

)%

|

15.0

|

%

|

||||||

(A)

See page 21 for reconciliation of As Reported to Comparable financial information

Financial highlights

|

•

|

Full-year diluted earnings per share were €1.41 on a reported basis or €2.12 on a comparable basis, including a negative currency translation impact of €0.04.

|

|

•

|

Full-year reported revenue totalled €11.1 billion, up 21.0%, or up 3.0% on a comparable and fx-neutral basis. Volume was up 0.5% on a comparable basis.

|

|

•

|

Full-year reported operating profit totalled €1.3 billion, or €1.5 billion on a comparable basis, up 9.0%, or up 10.5% on a comparable and fx-neutral basis.

|

|

•

|

Net cash flows from operating activities were €1.6 billion. Full-year free cash flow was €1.0 billion.

*

|

|

•

|

We remain on track to achieve pre-tax savings of €315 million to €340 million through synergies by mid-2019.

|

*

Refer to page 19 for a reconciliation between net cash flows from operating activities and free cash flow.

Operational review

In our first full year as Coca-Cola European Partners, we have started to realise the growth opportunities created by the Merger and, importantly, exceeded our initial guidance for revenue, operating profit, diluted earnings per share, and free cash flow. Our strong performance in 2017 enabled us to accelerate investment behind our brand portfolio, our field sales teams, our route-to-market and our digital capabilities. We are confident of making further progress, underpinned by a number of exciting growth opportunities ahead of us and continued investments in our business.

Key operating factors for the year included solid revenue growth driven by revenue per case growth coupled with 0.5% volume growth. Operating margins improved as we maintained gross margin and as we continue to realise post-Merger synergy benefits. We benefited from growth in our sugar-free portfolio, a strong innovation pipeline and a focus on driving joint value for our customers across all channels.

Full-year 2017 diluted earnings per share were €1.41 on a reported basis, or €2.12 on a comparable basis. Currency translation had a negative impact of €0.04 on comparable diluted earnings per share for the year ended 31 December 2017. Full-year reported operating profit totalled €1.3 billion, up 48.0%, driven by the inclusion of Germany, Iberia and Iceland. Comparable operating profit was €1.5 billion, up 9.0%, or up 10.5% on a comparable and fx-neutral basis.

Revenue

Full-year 2017 reported revenue totalled €11.1 billion, up 21.0%, or up 3.0% on a comparable and fx-neutral basis. Revenue per unit case grew 2.5% on a comparable and fx-neutral basis and volume increased 0.5% on a comparable basis.

|

|

P a g e |

16

|

|

Revenue

In millions of €, except per case data which is calculated prior to rounding

|

Year ended

|

||||||||

|

31 December 2017

|

|

31 December 2016

|

|

% Change

|

|

||||

|

As reported

|

11,062

|

|

9,133

|

|

21.0

|

%

|

|||

|

Adjust: Total items impacting comparability

(A)

|

(7

|

)

|

1,732

|

|

(100.5

|

)%

|

|||

|

Comparable

|

11,055

|

|

10,865

|

|

1.5

|

%

|

|||

|

Adjust: Impact of fx changes

|

142

|

|

n/a

|

|

(1.5

|

)%

|

|||

|

Comparable & fx-neutral

|

11,197

|

|

10,865

|

|

3.0

|

%

|

|||

|

Revenue per unit case

|

4.46

|

|

4.35

|

|

2.5

|

%

|

|||

|

(A)

|

Amounts include items impacting comparability during the periods presented. Additionally, for periods prior to 27 May 2016, amounts include the results of Germany and Iberia as if the Merger had occurred at the beginning of the presented period.

|

On a territory basis for full-year 2017, Iberia revenues were up 3.0%, and revenue in Germany was up 2.5%. Revenue in Great Britain grew 4.5% on an fx-neutral basis, and on a reported basis, revenue declined 2.5%, driven by a decline of the British pound versus the euro. Revenue in France was up 0.5% for the year, and revenue in the Northern European territories (Belgium, Luxembourg, the Netherlands, Norway, Sweden and Iceland) was up 4.5%, led by Belgium/Luxembourg and the Netherlands.

|

Year ended

|

||||||||||

|

Revenue by geography

Comparable

|

31 December 2017

% of Total

|

|

31 December 2016

% of Total

|

|

Revenue % Change

|

|

||||

|

Spain/Portugal/Andorra

(A)

|

24.5

|

%

|

24.0

|

%

|

3.0

|

%

|

||||

|

Germany

|

20.0

|

%

|

20.0

|

%

|

2.5

|

%

|

||||

|

Great Britain

|

18.5

|

%

|

19.0

|

%

|

(2.5

|

)%

|

||||

|

France/Monaco

|

16.5

|

%

|

16.5

|

%

|

0.5

|

%

|

||||

|

Belgium/Luxembourg/Netherlands

|

13.0

|

%

|

13.0

|

%

|

2.0

|

%

|

||||

|

Norway

|

3.5

|

%

|

4.0

|

%

|

1.5

|

%

|

||||

|

Sweden

|

3.0

|

%

|

3.0

|

%

|

1.0

|

%

|

||||

|

Iceland

(B)

|

1.0

|

%

|

0.5

|

%

|

150.5

|

%

|

||||

|

Total

|

100.0

|

%

|

100.0

|

%

|

1.5

|

%

|

||||

|

(A)

|

Spain/Portugal/Andorra is also referred to as Iberia.

|

|

(B)

|

Iceland was acquired in July 2016.

|

|

Comparable volume - selling day shift

In millions of unit cases, prior period volume recast using current year selling days

(A)

|

Year ended

|

||||||||

|

31 December 2017

|

|

31 December 2016

|

|

% Change

|

|

||||

|

Volume

|

2,510

|

|

2,502

|

|

0.5%

|

|

|||

|

Impact of selling day shift

|

n/a

|

|

(7

|

)

|

n/a

|

|

|||

|

Pro forma comparable volume

|

2,510

|

|

2,495

|

|

0.5

|

%

|

|||

|

(A)

|

A unit case equals approximately 5.678 litres or 24 8-ounce servings, a typical volume measure used in our industry.

|

On a brand basis for full-year 2017, volume for sparkling brands was up 0.5%. Coca-Cola trademark brands decreased 0.5%, with growth of approximately 15.0% in Coca-Cola Zero Sugar offset by declines in other trademark brands. Sparkling flavours and energy grew 4.0% with continued strong growth in energy and solid growth in Fanta, Vio and Royal Bliss. Still brands increased 1.0%,with increases in juice, isotonics and other of 2.5% being offset by water brands being down 1.5%.

|

Year ended

|

||||||||||

|

Comparable volume by brand category

Adjusted for selling day shift

|

31 December 2017

% of Total

|

|

31 December 2016

% of Total

|

|

% Change

|

|

||||

|

Sparkling

|

85.0

|

%

|

85.5

|

%

|

0.5

|

%

|

||||

|

Coca-Cola trademark

|

63.5

|

%

|

64.5

|

%

|

(0.5

|

)%

|

||||

|

Sparkling flavours and energy

|

21.5

|

%

|

21.0

|

%

|

4.0

|

%

|

||||

|

Stills

|

15.0

|

%

|

14.5

|

%

|

1.0

|

%

|

||||

|

Juice, isotonics and other

|

8.0

|

%

|

7.5

|

%

|

2.5

|

%

|

||||

|

Water

|

7.0

|

%

|

7.0

|

%

|

(1.5

|

)%

|

||||

|

Total

|

100.0

|

%

|

100.0

|

%

|

0.5

|

%

|

||||

|

|

P a g e |

17

|

Cost of sales

Full-year 2017 reported cost of sales were €6.8 billion, up 21.5%, driven by the inclusion of Germany, Iberia and Iceland. Comparable cost of sales was €6.7 billion, up 2.0%, or up 3.5% on a comparable and fx-neutral basis. Full-year cost of sales per unit case increased 3.0% on a comparable and fx-neutral basis, driven by channel, brand and package mix, and manufacturing costs, as well as year-over-year cost increases in key inputs, principally concentrate and sweetener. This was partially offset by benefits from our synergy programmes.

|

Cost of sales

In millions of €, except per case data which is calculated prior to rounding

|

Year ended

|

||||||||

|

31 December 2017

|

|

31 December 2016

|

|

% Change

|

|

||||

|

As reported

|

6,772

|

|

5,584

|

|

21.5

|

%

|

|||

|

Adjust: Total items impacting comparability

(A)

|

(33

|

)

|

1,011

|

|

(103.5

|

)%

|

|||

|

Comparable

|

6,739

|

|

6,595

|

|

2.0

|

%

|

|||

|

Adjust: Impact of fx changes

|

85

|

|

n/a

|

|

(1.5

|

)%

|

|||

|

Comparable & fx-neutral

|

6,824

|

|

6,595

|

|

3.5

|

%

|

|||

|

Cost of sales per unit case

|

2.72

|

|

2.64

|

|

3.0

|

%

|

|||

|

(A)

|

Amounts include items impacting comparability during the periods presented. Additionally, for periods prior to 27 May 2016, amounts include the results of Germany and Iberia as if the Merger had occurred at the beginning of the presented period.

|

Operating expenses

Full-year 2017 reported operating expenses were €3.0 billion, up 12.5%, driven by the inclusion of Germany, Iberia and Iceland. Comparable operating expenses were €2.8 billion, down 2.5%, or down 1.5% on a comparable and fx-neutral basis, primarily driven by synergy benefits and a continued focus on managing expenses.

|

Operating expenses

In millions of € except % change

|

Year ended

|

||||||||

|

31 December 2017

|

|

31 December 2016

|

|

% Change

|

|

||||

|

As reported

|

3,030

|

|

2,698

|

|

12.5

|

%

|

|||

|

Adjust: Total items impacting comparability

(A)

|

(192

|

)

|

213

|

|

(190.0

|

)%

|

|||

|

Comparable

|

2,838

|

|

2,911

|

|

(2.5

|

)%

|

|||

|

Adjust: Impact of fx changes

|

31

|

|

n/a

|

|

(1.0

|

)%

|

|||

|

Comparable & fx-neutral

|

2,869

|

|

2,911

|

|

(1.5

|

)%

|

|||

|

(A)

|

Amounts include items impacting comparability during the periods presented. Additionally, for periods prior to 27 May 2016, amounts include the results of Germany and Iberia as if the Merger had occurred at the beginning of the presented period.

|

Restructuring and synergy programme

During the full-year 2017, we recognised restructuring charges totalling €235 million. These charges principally related to proposed restructuring activities under our Integration and Synergy Programme including those related to supply chain improvements such as network optimisation, productivity initiatives, continued facility rationalisation in Germany, end to end supply chain organisational design, and cold drink operational practices and facilities. Our proposed restructuring activities also include the transfer of Germany and Iberia transactional related activities to our shared services centre in Sofia, Bulgaria, streamlining of our HR organisation, and other central function initiatives. Since the Merger we have recognised restructuring charges totalling €495 million.

We remain on track to achieve pre-tax run rate savings of €315 million to €340 million through synergies by mid-2019. Since the Merger, we have achieved €155 million in synergies and expect to have realised approximately 75% of our total target by year-end 2018. Restructuring cash costs to achieve these synergies are expected to be approximately 2 1/4 times expected savings and includes cash costs associated with pre-transaction close accruals.

US tax reform

The US Tax Cuts and Jobs Act (the US Tax Act) was enacted on 22 December 2017 and represents a significant change to the US tax code. While CCEP is a UK listed and tax resident entity, it has a number of subsidiaries outside the UK, including a US incorporated holding company that is wholly owned by Coca-Cola European Partners plc. Based on the applicable provisions of the US Tax Act, during the fourth quarter of 2017, we recorded a non-recurring book tax expense of €320 million, which included an estimated book tax expense of approximately €125 million related to the transition from a worldwide to territorial tax system and a reduction in deferred tax assets of approximately €195 million primarily due to the elimination of foreign tax credits. We do not currently expect an increase in cash taxes as a result of any provision of the US Tax Act and while we continue to assess the situation, at this stage, we do not anticipate any impact on our effective tax rate going forward.

|

|

P a g e |

18

|

Financial position

|

In millions of €

|

As at

|

|||||

|

31 December 2017

|

|

31 December 2016

|

|

|||

|

Assets

|

||||||

|

Non-current assets

|

14,880

|

|

15,143

|

|

||

|

Current assets

|

3,314

|

|

3,425

|

|

||

|

Total assets

|

18,194

|

|

18,568

|

|

||

|

Liabilities

|

||||||

|

Non-current liabilities

|

8,222

|

|

8,355

|

|

||

|

Current liabilities

|

3,287

|

|

3,752

|

|

||

|

Total liabilities

|

11,509

|

|

12,107

|

|

||

|

Total equity

|

6,685

|

|

6,461

|

|

||

|

Total equity and liabilities

|

18,194

|

|

18,568

|

|

||

Total non-current assets decreased €263 million, or 1.5%, from €15.1 billion at 31 December 2016 to €14.9 billion at 31 December 2017. This change was partially driven by a decrease in deferred tax assets of €218 million mainly related to US tax law changes enacted prior to year-end. Property, plant and equipment reduced by €156 million which was offset by increases in intangible assets and goodwill of €40 million and €93 million, respectively, relating primarily to the finalisation of acquisition accounting for Germany and Iberia and currency effects during the period.

Total current assets decreased €111 million, or 3.0%, from €3.4 billion at 31 December 2016 to €3.3 billion at 31 December 2017. This change was primarily driven by a decrease of €23 million in inventories and €128 million in trade accounts receivable resulting from working capital initiatives.

Total non-current liabilities decreased by €133 million, or 1.5%, from €8.4 billion at 31 December 2016 to €8.2 billion at 31 December 2017. This change was mainly driven by a reduction of €116 million in employee benefit liabilities primarily due to the actual return on underlying assets exceeding actuarial estimates, a reduction in non-current borrowings of €88 million reflecting early repayments on a term loan of €300 million, foreign exchange movements on our US denominated debt and issuance of €350 million floating-rate notes, offset by an increase in our derivative liabilities of €92 million, relating to US denominated debt.

Total current liabilities decreased €465 million, or 12.5%, from €3.8 billion at 31 December 2016 to €3.3 billion at 31 December 2017. This change was primarily driven by the repayment of €300 million Eurobond notes in November 2017 and €500 million floating rate notes in December 2017, offset by commercial paper issuances of €250 million. This reduction was offset by an increase in trade and other payables of €115 million, primarily due to working capital initiatives.

Liquidity and capital management

Liquidity

Liquidity risk is actively managed to ensure we have sufficient funds to satisfy our commitments as they fall due. Our sources of capital include, but are not limited to, cash flows from operations, public and private issuances of debt securities and bank borrowings. We believe our operating cash flow, cash on hand and available short-term and long-term capital resources are sufficient to fund our working capital requirements, scheduled borrowing payments, interest payments, capital expenditures, benefit plan contributions, income tax obligations and dividends to shareholders. Counterparties and instruments used to hold cash and cash equivalents are continuously assessed, with a focus on preservation of capital and liquidity.

We have amounts available for borrowing under a €1.5 billion multi-currency credit facility with a syndicate of 10 banks. This credit facility matures in 2021 and is for general corporate purposes and supporting our working capital needs. Based on information that is currently available, there is no indication that the financial institutions participating in this facility would be unable to fulfil their commitments to CCEP as at the date of this report. Our current credit facility contains no financial covenants that would impact our liquidity or access to capital. As at 31 December 2017, we had no amounts drawn under this credit facility.

Free cash flow generation was strong during 2017, with €1.0 billion generated in the year. This reflects our dedicated efforts to improve working capital where we have improved our total cash conversion cycle by over 10 days and have achieved over €250 million of working capital benefits throughout 2017. We also maintained our prudent capex approach and continued to challenge ourselves when managing restructuring costs.

|

|

P a g e |

19

|

|

Free cash flow

(A)

In millions of €

|

Year Ended

|

||

|

31 December 2017

|

|

||

|

Net cash flows from operating activities

|

1,623

|

|

|

|

Less: Purchases of property, plant and equipment

|

(484

|

)

|

|

|

Less: Purchases of capitalised software

|

(36

|

)

|

|

|

Less: Interest paid

|

(94

|

)

|

|

|

Add: Disposals of property, plant and equipment

|

32

|

|

|

|

Free cash flow

|

1,041

|

|

|

|

(A)

|

Free cash flow is defined as net cash flows from operations, less capital expenditures and interest paid, plus proceeds from capital disposals.

|

Capital management

The primary objective of our capital management strategy is to ensure strong credit ratings and to maintain appropriate capital ratios in order to support our business and maximise shareholder value. Our credit ratings are periodically reviewed by rating agencies. Currently, our long-term ratings from Moody’s and Standard & Poor’s (S&P) are A3 and BBB+ respectively. The ratings outlook from Moody’s and S&P are stable. Changes in the operating results, cash flows or financial position could impact the ratings assigned by the various rating agencies. We regularly assess debt and equity capital levels against our stated policy for capital structure. Our capital structure is managed and, as appropriate, adjusted in light of changes in economic conditions and our financial policy.

|

Net debt

In millions of €

|

As at

|

Credit Ratings

|

|||||

|

31 December 2017

|

|

As of 14 March 2018

|

Moody’s

|

Standard & Poor’s

|

|||

|

Total borrowings

|

5,748

|

|

Long-term rating

|

A3

|

BBB+

|

||

|

Add: Fx impact of non-EUR borrowings

|

66

|

|

Outlook

|

Stable

|

Stable

|

||

|

Adjusted total borrowings

|

5,814

|

|

Note: Our credit ratings can be materially influenced by a number of factors including, but not limited to, acquisitions, investment decisions and working capital management activities of TCCC and/or changes in the credit rating of TCCC.

|

||||

|

Less: Cash and cash equivalents

|

(360

|

)

|

|||||

|

Net debt

|

5,454

|

|

|||||

The ratio of net debt to Adjusted EBITDA is used by investors, analysts and credit rating agencies to analyse our operating performance in the context of targeted financial leverage, and as such, we provide a reconciliation of this measure. Net debt enables investors to see the economic effect of total borrowings, related foreign exchange impact and cash and cash equivalents in total and is calculated as being the net of cash and cash equivalents and currency adjusted borrowings. Adjusted EBITDA is calculated as EBITDA, before adding back items impacting the comparability of year-over-year financial performance.

Adjusted EBITDA does not reflect our cash expenditures, or future requirements for capital expenditures or contractual commitments. Further, Adjusted EBITDA does not reflect changes in, or cash requirements for, our working capital needs, and although depreciation and amortisation are non-cash charges, the assets being depreciated and amortised are likely to be replaced in the future and Adjusted EBITDA does not reflect cash requirements for such replacements.

|

|

P a g e |

20

|

|

Adjusted EBITDA

In millions of €

|

Year Ended

|

||

|

31 December 2017

|

|

||

|

Reported profit after tax

|

688

|

|

|

|

Taxes

|

471

|

|

|

|

Finance costs, net

|

100

|

|

|

|

Non-operating items

|

1

|

|

|

|

Reported operating profit

|

1,260

|

|

|

|

Depreciation and amortisation

|

490

|

|

|

|

Reported EBITDA

|

1,750

|

|

|

|

Items impacting comparability:

|

|||

|

Merger effects

(A)

|

(20

|

)

|

|

|

Mark-to-market effects

(B)

|

(6

|

)

|

|

|

Restructuring Charges

(C)

|

218

|

|

|

|

Merger and Integration Related Costs

(D)

|

4

|

|

|

|

Litigation provision

(E)

|

5

|

|

|

|

Adjusted EBITDA

|

1,951

|

|

|

|

Net debt to EBITDA

|

3.1

|

||

|

Net debt to Adjusted EBITDA

|

2.8

|

||

|

(A)

|

Adjustments to reflect Germany and Iberia financial results as if the Merger had occurred at the beginning of each period (if applicable), the impact of acquisition accounting including final fair values of the acquired inventory, property, plant, and equipment and intangibles from Germany and Iberia, final acquisition accounting related adjustments and associated impact on depreciation and amortisation expense, and additional debt financing cost incurred by CCEP in connection with the Merger.

|

|

(B)

|

Amounts represent the net out-of-period mark-to-market impact of non-designated commodity hedges.

|

|

(C)

|

Amounts represent restructuring charges related to business transformation activities, excluding accelerated depreciation included in the depreciation and amortisation line.

|

|

(D)

|

Amounts represent costs associated with the Merger to form CCEP.

|

|

(E)

|

Amount represents a provision recorded for ongoing litigation.

|

Dividends

In March 2017, the Board increased our quarterly dividend by more than 20% to €0.21 per share. For the full year 2017, our dividend per share represented approximately 40% of our comparable diluted earnings per share. In February 2018, the Board declared a further increase in the quarterly dividend to €0.26 per share, equivalent to an annualised dividend of €1.04 per share. This is in line with our commitment to deliver long-term value to shareholders.

Looking forward

For 2018, we expect revenue growth in a low single-digit range, with both operating profit and earnings per share growth of between 6% and 7%. Each of these growth figures is on a comparable and fx-neutral basis when compared to 2017 comparable results. This revenue growth guidance excludes the accounting impact of incremental soft drinks industry taxes. These taxes are expected to add approximately 2% to 3% to revenue growth and approximately 4% to cost of goods growth. At recent rates, currency translation would have a negligible impact on 2018 full-year diluted earnings per share.

We expect 2018 free cash flow* in the range of €850 million to €900 million, including the expected benefit from improved working capital offset by the impact of restructuring and integration costs. Capital expenditures are expected to be approximately €525 million to €575 million, including approximately €75 million of capital expenditures related to synergies. Weighted-average cost of debt is expected to be approximately 2%. The comparable effective tax rate for 2018 is expected to be approximately 25%.

We remain on track to achieve pre-tax run-rate savings of €315 million to €340 million through synergies by mid-2019. Further, we expect to have realised approximately 75% of the target by year-end 2018. Restructuring cash costs to achieve these synergies are expected to be approximately 2 1/4 times expected savings and includes cash costs associated with pre-transaction close accruals. Given these factors, currency exchange rates, and our outlook for 2018, we expect year-end net debt to Adjusted EBITDA* for 2018 to be towards the low-end of our target range of 2.5 to 3 times. As a result, during 2018, we expect to continue to evaluate returning incremental cash to shareholders.

*Refer to note regarding the presentation of non-GAAP financial information.

|

|

P a g e |

21

|

Supplementary financial information – income statement full year

The following provides a summary reconciliation of CCEP’s reported and comparable results for the full year ended 31 December 2017 and 31 December 2016:

|

Full-year 2017

Unaudited, in millions of € except per share data which is calculated prior to rounding

|

As Reported

|

|

Items Impacting Comparability

|

Comparable

|

|

|||||||||||||

|

Merger effects

(A)

|

Mark-to-market effects

(B)

|

Restructuring charges

(C)

|

Merger and integration related costs

(D)

|

Litigation provision

(E)

|

Net tax items

(F)

|

CCEP

|

|

|||||||||||

|

Revenue

|

11,062

|

|

(7

|

)

|

—

|

|

—

|

|

—

|

|

—

|

|

—

|

|

11,055

|

|

||

|

Cost of sales

|

6,772

|

|

27

|

|

6

|

|

(66

|

)

|

—

|

|

—

|

|

—

|

|

6,739

|

|

||

|

Gross profit

|

4,290

|

|

(34

|

)

|

(6

|

)

|

66

|

|

—

|

|

—

|

|

—

|

|

4,316

|

|

||

|

Operating expenses

|

3,030

|

|

(14

|

)

|

—

|

|

(169

|

)

|

(4

|

)

|

(5

|

)

|

—

|

|

2,838

|

|

||

|

Operating profit

|

1,260

|

|

(20

|

)

|

(6

|

)

|

235

|

|

4

|

|

5

|

|

—

|

|

1,478

|

|

||

|

Total finance costs, net

|

100

|

|

—

|

|

—

|

|

—

|

|

—

|

|

(1

|

)

|

—

|

|

99

|

|

||

|

Non-operating items

|

1

|

|

—

|

|

—

|

|

—

|

|

—

|

|

—

|

|

—

|

|

1

|

|

||

|

Profit before taxes

|

1,159

|

|

(20

|

)

|

(6

|

)

|

235

|

|

4

|

|

6

|

|

—

|

|

1,378

|

|

||

|

Taxes

|

471

|

|

(4

|

)

|

(2

|

)

|

70

|

|

1

|

|

1

|

|

(194

|

)

|

343

|

|

||

|

Profit after taxes

|

688

|

|

(16

|

)

|

(4

|

)

|

165

|

|

3

|

|

5

|

|

194

|

|

1,035

|

|

||

|

Diluted earnings per share (€)

|

1.41

|

|

2.12

|

|

||||||||||||||

|

Diluted shares outstanding

|

489

|

|

||||||||||||||||

|

Full-year 2016

Unaudited, in millions € except per share data which is calculated prior to rounding

|

As Reported

|

|

Items Impacting Comparability

|

Comparable

|

|

|||||||||||

|

Merger effects

(A)

|

Mark-to-market effects

(B)

|

Restructuring charges

(C)

|

Merger and integration related costs

(D)

|

Net tax items

(F)

|

CCEP

|

|

||||||||||

|

Revenue

|

9,133

|

|

1,732

|

|

—

|

|

—

|

|

—

|

|

—

|

|

10,865

|

|

||

|

Cost of sales

|

5,584

|

|

1,006

|

|

18

|

|

(13

|

)

|

—

|

|

—

|

|

6,595

|

|

||

|

Gross profit

|

3,549

|

|

726

|

|

(18

|

)

|

13

|

|

—

|

|

—

|

|

4,270

|

|

||

|

Operating expenses

|

2,698

|

|

911

|

|

17

|

|

(547

|

)

|

(168

|

)

|

—

|

|

2,911

|

|

||

|

Operating profit

|

851

|

|

(185

|

)

|

(35

|

)

|

560

|

|

168

|

|

—

|

|

1,359

|

|

||

|

Total finance costs, net

|

123

|

|

12

|

|

—

|

|

—

|

|

(5

|

)

|

—

|

|

130

|

|

||

|

Non-operating items

|

9

|

|

(1

|

)

|

—

|

|

—

|

|

—

|

|

—

|

|

8

|

|

||

|

Profit before taxes

|

719

|

|

(196

|

)

|

(35

|

)

|

560

|

|

173

|

|

—

|

|

1,221

|

|

||

|

Taxes

|

170

|

|

(29

|

)

|

(9

|

)

|

156

|

|

39

|

|

(23

|

)

|

304

|

|

||

|

Profit after taxes

|

549

|

|

(167

|

)

|

(26

|

)

|

404

|

|

134

|

|

23

|

|

917

|

|

||

|

Diluted earnings per share (€)

|

1.42

|

|

1.88

|

|

||||||||||||

|

Reported diluted shares outstanding

|

385

|

|

||||||||||||||

|

Adjust: Capital structure share impact related to the Merger

|

103

|

|

||||||||||||||

|

Comparable diluted shares outstanding

|

488

|

|

||||||||||||||

|

(A)

|

Adjustments to reflect Germany and Iberia financial results as if the Merger had occurred at the beginning of each period (if applicable), the impact of acquisition accounting including final fair values of the acquired inventory, property, plant, and equipment and intangibles from Germany and Iberia, final acquisition accounting related adjustments and associated impact on depreciation and amortisation expense, and additional debt financing cost incurred by CCEP in connection with the Merger.

|

|

(B)

|

Amounts represent the net out-of-period mark-to-market impact of non-designated commodity hedges.

|

|

(C)

|

Amounts represent restructuring charges related to business transformation activities.

|

|

(D)

|

Amounts represent costs associated with the Merger to form CCEP.

|

|

(E)

|

Amount represents a provision recorded for ongoing litigation.

|

|

(F)

|

Amounts represent the deferred tax impact related to income tax rate and law changes. The amount in 2017 principally represents the net book tax impact of US tax reform.

|

|

|

P a g e |

22

|

SUSTAINABILITY

Action on sustainability

In 2017, together with The Coca-Cola Company in Western Europe, we launched This is Forward - our joint sustainability action plan. This is Forward builds upon many years of work in sustainability and is a critical part of Coca-Cola European Partners’ (CCEP) long-term business strategy. It sets out how we will grow our business in a responsible and sustainable way and how we intend to play a meaningful role in addressing key societal issues.

This is Forward has been developed following extensive consultation with over 100 of our key stakeholders - including governments, Non-Governmental Organisations (NGOs), customers, suppliers, as well as 12,000 consumers across six countries and over 1,000 of our own employees.

Our plan outlines the actions that we are taking on major societal issues - including health and nutrition, packaging and economic development; as well as continuing to address climate change and water scarcity and drive sustainability within our supply chain.

Reporting and transparency

Being accountable and transparent is central to the way in which we operate. We report our progress against our sustainability action plan in our annual Stakeholder Progress Report, which will be published in May 2018, and will be available at https://www.ccep.com/pages/thisisforward. Our Stakeholder Progress Report is being produced in accordance with the GRI Standards: Core Option.

The following are some of the highlights of our progress in 2017:

Action on Drinks