Table of Contents

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

| (Mark One) | WASHINGTON, D.C. 20549 |

FORM 20-F

☐ REGISTRATION STATEMENT PURSUANT TO SECTION 12(b) OR (g) OF THE SECURITIES EXCHANGE ACT OF 1934

OR

X ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934

For the fiscal year ended: December 31, 2019

OR

☐ TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934

For the transition period from to

OR

☐ SHELL COMPANY REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934

Date of event requiring this shell company report

Commission file number: 001-32846

CRH public limited company

(Exact name of Registrant as specified in its charter)

Republic of Ireland

(Jurisdiction of incorporation or organisation)

Stonemason’s Way, Rathfarnham, Dublin 16, Ireland

(Address of principal executive offices)

Senan Murphy

Tel: +353 1 404 1000

mail@crh.com

Stonemason’s Way, Rathfarnham, Dublin 16, Ireland

(Name, Telephone, Email and/or Facsimile number and Address of Company Contact Person)

Securities registered or to be registered pursuant to Section 12(b) of the Act.

| Title of each class | Trading symbol(s) | Name of each exchange on which registered | ||

|

CRH plc |

||||

|

Ordinary Shares/Income Shares of € 0.34 each |

New York Stock Exchange* |

|||

| American Depositary Shares, each representing the right to receive one Ordinary Share | CRH | New York Stock Exchange | ||

| CRH America Inc. | ||||

| 5.750% Notes due 2021 guaranteed by CRH plc | CRH/21 | New York Stock Exchange | ||

–

| * |

Not for trading but only in connection with the registration of American Depositary Shares, pursuant to the requirements of the Securities and Exchange Commission. |

Securities registered or to be registered pursuant to Section 12(g) of the Act. None

Securities for which there is a reporting obligation pursuant to Section 15(d) of the Act. None

Indicate the number of outstanding shares of each of the issuer’s classes of capital or common stock as of the close of the period covered by the annual report.

|

Ordinary Shares/Income Shares of € 0.34 each ** |

799,640,338 |

|||

|

5% Cumulative Preference Shares of € 1.27 each |

50,000 | |||

|

7% ‘A’ Cumulative Preference Shares of € 1.27 each |

872,000 |

–

| ** |

Each Income Share is tied to an Ordinary Share and may only be transferred or otherwise dealt with in conjunction with such Ordinary Share. |

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. Yes X No ☐

If this report is an annual or transition report, indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or 15(d) of the Securities Exchange Act of 1934. Yes ☐ No X

Note – Checking the box above will not relieve any registrant required to file reports pursuant to Section 13 or 15(d) of the Securities Exchange Act of 1934 from their obligations under those Sections.

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes X No ☐

Indicate by check mark whether the registrant has submitted electronically every Interactive Data File required to be submitted pursuant to Rule 405 of Regulation S-T (§232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit such files). Yes X No ☐

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, or an emerging growth company. See definition of “large accelerated filer”, “accelerated filer”, and “emerging growth company” in Rule 12b-2 of the Exchange Act.

Large accelerated filer X Accelerated filer ☐ Non-accelerated filer ☐ Emerging Growth Company ☐

If an emerging growth company that prepares its financial statements in accordance with U.S. GAAP, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards† provided pursuant to Section 13(a) of the Exchange Act ☐

| † |

The term “new or revised financial accounting standard” refers to any update issued by the Financial Accounting Standards Board to its Accounting Standards Codification after April 5, 2012. |

Indicate by check mark which basis of accounting the registrant has used to prepare the financial statements included in this filing:

| U.S. GAAP ☐ | International Financial Reporting Standards as issued by the | Other ☐ | ||

| International Accounting Standards Board X |

If “Other” has been checked in response to the previous question, indicate by check mark which financial statement item the registrant has elected to follow. Item 17 ☐ Item 18 ☐

If this is an annual report, indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act). Yes ☐ No X

Table of Contents

[THIS PAGE INTENTIONALLY LEFT BLANK]

Table of Contents

|

2019 Annual Report and Form 20-F |

Table of Contents

|

|

||||||||||||||||||||

| Overview | Business Performance | Financial Statements | ||||||||||||||||||

| CRH at a glance | 2 | Business Overview | 32 | Independent Auditor’s Reports | 125 | |||||||||||||||

| Chairman’s Introduction | 4 | Finance Director’s Review | 33 | Consolidated Income Statements | 128 | |||||||||||||||

| Strategy Review | Segmental Reviews | 40 | Accounting Policies | 133 | ||||||||||||||||

| Why Invest in Us | 8 | Governance |

Notes on Consolidated

Financial Statements |

145 |

||||||||||||||||

| Our Executive Leadership | 9 | Board of Directors | 56 | |||||||||||||||||

| Chief Executive’s Review | 10 | Corporate Governance Report | 60 |

Supplementary

20-F Disclosures |

||||||||||||||||

| Market Backdrop | 12 | Directors’ Remuneration Report | 74 | 224 | ||||||||||||||||

| Strategy | 14 | Directors’ Report | 102 | Shareholder Information | 248 | |||||||||||||||

| Business Model | 16 | Other Information | 260 | |||||||||||||||||

| Measuring Performance | 18 | Cross Reference to Form 20-F | 267 | |||||||||||||||||

| Sustainability | 20 | Index | 270 | |||||||||||||||||

| Risk Governance | 26 | |||||||||||||||||||

|

Our Business

CRH is the leading building materials business in the world. Our global footprint spans 30 countries, employing c. 80,300 people at over 3,100 operating locations, serving customers across the breadth of the building materials spectrum. |

|

This document constitutes the Annual Report and Financial Statements in accordance with Irish and UK requirements and the Annual Report on Form 20-F in accordance with the US Securities Exchange Act of 1934, for CRH plc for the year ended 31 December 2019. A cross reference to Form 20-F requirements is included on page 267.

The Directors’ Statements (comprising the Statement of Directors’ Responsibilities, the Viability Statement and the Directors’ Compliance Statement on pages 104 to 106), the Principal Risks and Uncertainties (on pages 108 to 113), the Independent Auditor’s Report (on pages 116 to 124) |

and the Parent Company financial statements of CRH plc (on pages 216 to 221) do not form part of CRH’s Annual Report on Form 20-F as filed with the Securities and Exchange Commission (SEC).

Forward-Looking Statements

This document contains forward-looking statements, which by their nature involve risk and uncertainty. Please see Disclaimer/Forward-Looking Statements on page 103 for more information about these statements and certain factors that may cause them to prove inaccurate. |

|

View the Report on our website: www.crh.com/investors/annual-reports/ |

|

Ergon, part of CRH’s Europe Materials Division, supplied 10,300m² of hollow-core floor slabs and 289 concrete beams

and columns for the construction of a new 15,000m² plumbing and heating distribution centre in Merelbeke, Belgium. |

Table of Contents

|

CRH ANNUAL REPORT AND FORM 20-F I 2019

|

1

|

|

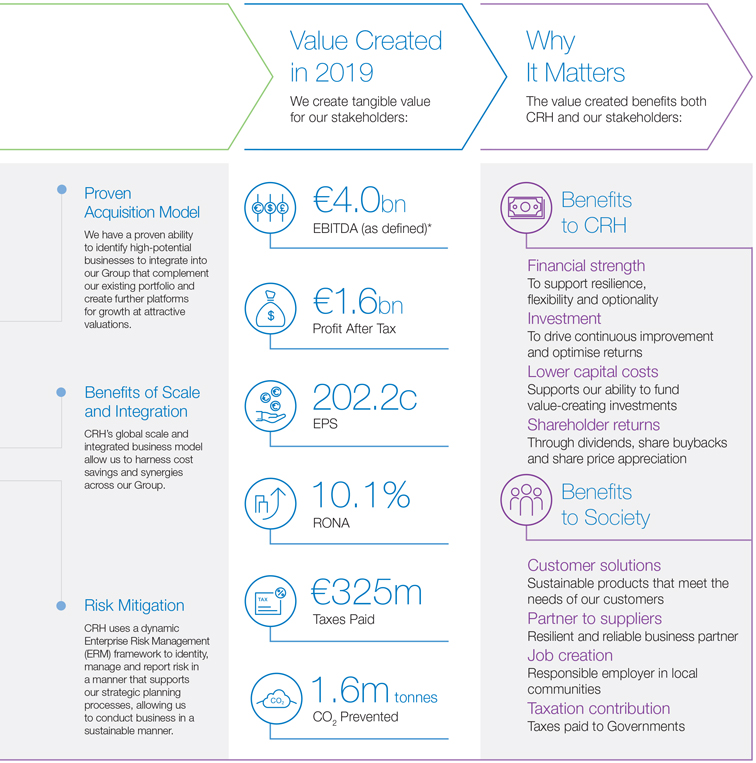

2019 Performance Highlights

During 2019 the Europe Distribution business was classified as discontinued operations under IFRS 5 Non-Current Assets Held for Sale and Discontinued Operations (refer to note 3 to the Consolidated Financial Statements for further information). Accordingly, all references to income statement data are on a continuing operations basis throughout the Overview, Strategy Review and Business Performance sections (pages 2 to 51), unless otherwise stated.

* EBITDA is defined as earnings before interest, taxes, depreciation, amortisation, asset impairment charges, profit on disposals and the Group’s share of equity accounted investments’ profit after tax. 1. Details of how non-GAAP measures are calculated are set out on pages 225 to 228. |

Table of Contents

Table of Contents

Table of Contents

| * |

EBITDA is defined as earnings before interest, taxes, depreciation, amortisation, asset impairment charges, profit on disposals and the Group’s share of equity accounted investments’ profit after tax. |

| 1. |

See cautionary statement regarding forward-looking statements on page 103. |

| 2. |

Net Debt/EBITDA (as defined)* is a non-GAAP measure as defined on page 227. The GAAP figures that are most directly comparable to the components of Net Debt/EBITDA (as defined)* include: interest-bearing loans and borrowings (2019: € 9,014 million; 2018: € 9,316 million) and profit after tax (2019: € 1,638 million; 2018: € 1,345 million). In line with the purpose of the metric, as set out on page 228, to “assess the Company’s level of indebtedness relative to its profitability and cash-generating capabilities”, the 2019 calculation is based on a continuing operations basis. For 2018, the Group net debt position includes debt related to operations discontinued in 2019 and therefore for comparability purposes the 2018 calculation uses EBITDA (as defined)* from continuing and discontinued operations. |

Table of Contents

Table of Contents

|

Inclusion and diversity is an important focus area for all CRH operating companies. Staker Parson Materials

& Construction, part of CRH’s Americas Materials Division, supports an inclusive and diverse environment at its operations in Ogden, Utah, where it employs 300 people. |

Table of Contents

| Strategy Review |

| Why Invest in Us | 8 | |||||||

| Our Executive Leadership | 9 | |||||||

| Chief Executive’s Review | 10 | |||||||

| Market Backdrop | 12 | |||||||

| Strategy | 14 | |||||||

| Business Model | 16 | |||||||

| Measuring Performance | 18 | |||||||

| Sustainability | 20 | |||||||

| Risk Governance | 26 | |||||||

Table of Contents

| 8 |

CRH ANNUAL REPORT AND FORM 20-F I 2019

|

| * |

EBITDA is defined as earnings before interest, taxes, depreciation, amortisation, asset impairment charges, profit on disposals and the Group’s share of equity accounted investments’ profit after tax. |

| 1. |

TSR represents the total accumulated value delivered to shareholders (via gross dividends reinvested and share appreciation). |

Table of Contents

|

CRH ANNUAL REPORT AND FORM 20-F I 2019

|

9

|

Table of Contents

| * |

EBITDA is defined as earnings before interest, taxes, depreciation, amortisation, asset impairment charges, profit on disposals and the Group’s share of equity accounted investments’ profit after tax. |

| 1. |

See cautionary statement regarding forward-looking statements on page 103. |

| 2. |

RONA is a non-GAAP measure as defined on page 226. The GAAP figures that are most directly comparable to the components of RONA include: Group operating profit (2019: € 2,494 million; 2018: € 2,071 million), total assets and total liabilities, respectively (2019: € 37,310 million and € 19,830 million respectively; 2018: € 35,173 million and € 18,619 million respectively). Details of how non-GAAP measures are calculated are set out on pages 225 to 228. |

Table of Contents

|

CRH ANNUAL REPORT AND FORM 20-F I 2019

|

11 |

Table of Contents

| 12 |

CRH ANNUAL REPORT AND FORM 20-F I 2019

|

Table of Contents

|

CRH ANNUAL REPORT AND FORM 20-F I 2019

|

13 |

Table of Contents

| 14 |

CRH ANNUAL REPORT AND FORM 20-F I 2019

|

Table of Contents

|

CRH ANNUAL REPORT AND FORM 20-F I 2019

|

15 |

Table of Contents

| 16 |

CRH ANNUAL REPORT AND FORM 20-F I 2019

|

Table of Contents

|

CRH ANNUAL REPORT AND FORM 20-F I 2019

|

17 |

Table of Contents

| 18 |

CRH ANNUAL REPORT AND FORM 20-F I 2019

|

Table of Contents

|

CRH ANNUAL REPORT AND FORM 20-F I 2019

|

19 |

Table of Contents

| 20 |

CRH ANNUAL REPORT AND FORM 20-F I 2019

|

Table of Contents

|

CRH ANNUAL REPORT AND FORM 20-F I 2019

|

21 |

Table of Contents

| 22 |

CRH ANNUAL REPORT AND FORM 20-F I 2019

|

Table of Contents

|

CRH ANNUAL REPORT AND FORM 20-F I 2019

|

23 |

Table of Contents

| 24 |

CRH ANNUAL REPORT AND FORM 20-F I 2019

|

Table of Contents

|

CRH ANNUAL REPORT AND FORM 20-F I 2019

|

25 |

Table of Contents

| 26 |

CRH ANNUAL REPORT AND FORM 20-F I 2019

|

Table of Contents

|

CRH ANNUAL REPORT AND FORM 20-F I 2019

|

27 |

Table of Contents

| 28 |

CRH ANNUAL REPORT AND FORM 20-F I 2019

|

Table of Contents

|

CRH ANNUAL REPORT AND FORM 20-F I 2019

|

29 |

Table of Contents

| The Joliette cement plant in Quebec, Canada, part of CRH’s Americas Materials Division, supplies more than ten types of cement to customers across Canada and the Northeastern US. The plant has 180 employees and has been in operation for more than 50 years. It is a pioneer in the use of Alternative Fuels and Raw Material (AFR) in the cement production process, with more than 30% of fossil fuels replaced by alternative fuels. |

Table of Contents

Table of Contents

| 32 |

CRH ANNUAL REPORT AND FORM 20-F I 2019

|

Table of Contents

Table of Contents

| 34 |

CRH ANNUAL REPORT AND FORM 20-F I 2019

|

Table of Contents

|

CRH ANNUAL REPORT AND FORM 20-F I 2019

|

35 |

Table of Contents

| 36 |

CRH ANNUAL REPORT AND FORM 20-F I 2019

|

Table of Contents

|

CRH ANNUAL REPORT AND FORM 20-F I 2019

|

37 |

Table of Contents

| Roadstone, part of CRH’s Europe Materials Division, developed over 4,500m³ of high-strength concrete for The Rose Fitzgerald Kennedy Bridge in Ireland, which opened in January 2020. The three-tower, 887m extrados bridge is the longest of its type in the world. Extending more than 230m over the River Barrow, and with a 36-metre clearance, it provides vital connectivity for surrounding communities and for shipping navigation to the Port of New Ross. |

Table of Contents

Table of Contents

| 40 |

CRH ANNUAL REPORT AND FORM 20-F I 2019

|

Table of Contents

|

CRH ANNUAL REPORT AND FORM 20-F I 2019

|

41 |

Table of Contents

| 42 |

CRH ANNUAL REPORT AND FORM 20-F I 2019

|

Table of Contents

|

CRH ANNUAL REPORT AND FORM 20-F I 2019

|

43 |

Table of Contents

| 44 |

CRH ANNUAL REPORT AND FORM 20-F I 2019

|

Table of Contents

|

CRH ANNUAL REPORT AND FORM 20-F I 2019

|

45 |

Table of Contents

| 46 |

CRH ANNUAL REPORT AND FORM 20-F I 2019

|

Table of Contents

|

CRH ANNUAL REPORT AND FORM 20-F I 2019

|

47 |

Table of Contents

| 48 |

CRH ANNUAL REPORT AND FORM 20-F I 2019

|

Table of Contents

|

CRH ANNUAL REPORT AND FORM 20-F I 2019

|

49 |

Table of Contents

| 50 |

CRH ANNUAL REPORT AND FORM 20-F I 2019

|

Table of Contents

|

CRH ANNUAL REPORT AND FORM 20-F I 2019

|

51 |

Table of Contents

| 52 |

CRH ANNUAL REPORT AND FORM 20-F I 2019

|

Table of Contents

|

Stradus, part of CRH’s Building Products Division, supplied c.1,000 Hydro Lineo XL grass tiles to pave the surroundings of an office complex in Doornik, Belgium. The lattice structure allows water to slowly drain away, keeping the surface free from water while not overloading drainage systems.

|

Table of Contents

HALFEN, part of CRH’s Building Products Division, supplied 200 panel anchors to affix the facade of

the new Pavilion 6 of the Paris Expo Porte de Versailles exhibition centre. The centre, which is Europe’s

largest conference venue, welcomes more than 7.5 million visitors and hosts 200 events each year.

Table of Contents

|

Governance

|

|

|||||||||||

| 56 - 113 | Board of Directors | 56 | ||||||||||

| Corporate Governance Report | 60 | |||||||||||

| Directors’ Remuneration Report | 74 | |||||||||||

| Directors’ Report | 102 | |||||||||||

Table of Contents

Table of Contents

|

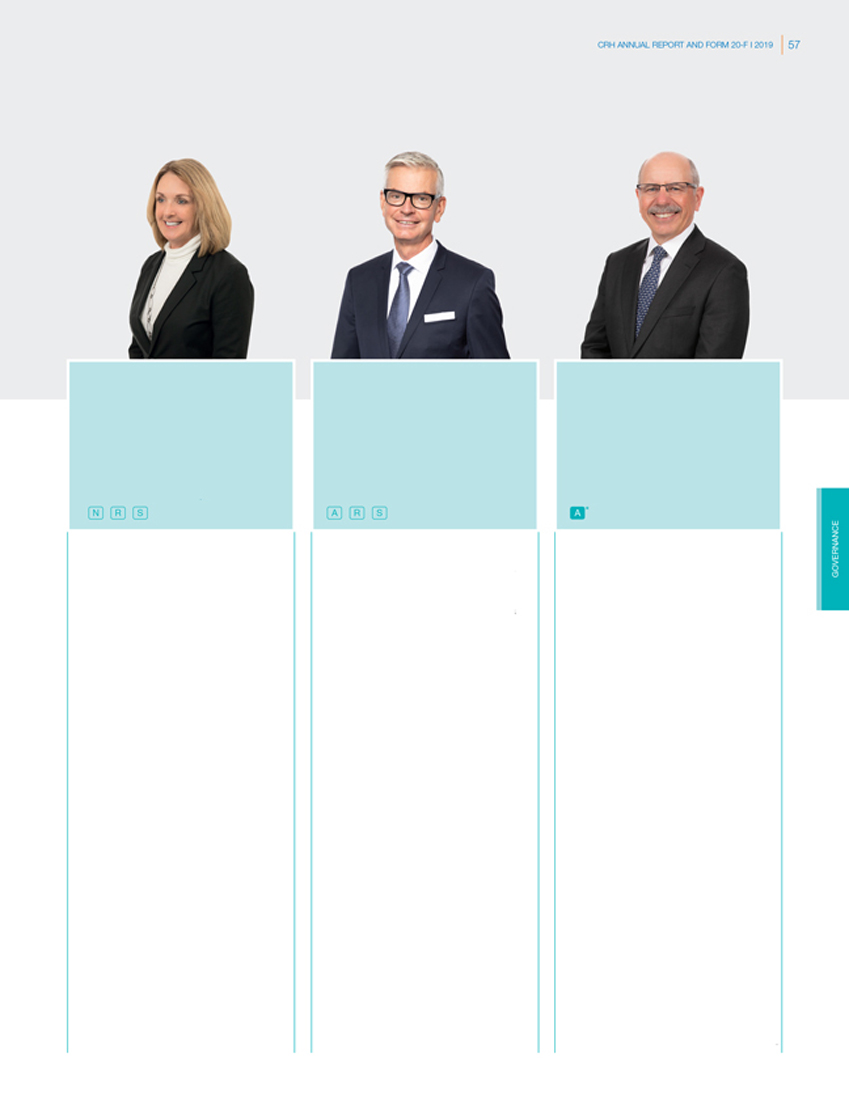

Gillian L. Platt |

Johan Karlström |

Shaun Kelly |

||||||||||

|

Senior Independent Director |

Non-executive Director |

Non-executive Director |

||||||||||

|

Appointed to the Board: January 2017 |

Appointed to the Board: September 2019 |

Appointed to the Board: December 2019 |

||||||||||

|

Nationality: Canadian Age: 66 |

Nationality: Swedish Age: 63 |

Nationality: Dual United States and Irish |

||||||||||

|

Committee membership:

|

Committee membership:

|

Age: 60 Committee membership:

|

||||||||||

|

Skills and experience:

During the course of her executive career, Gillian has held a number of senior leadership positions in a variety of industries, geographies and roles including human resources, corporate affairs and strategy. Most recently she was Executive Vice President and Chief Human Resources Officer at Finning International, Inc. (the world’s largest Caterpillar equipment dealer) with global responsibility for human resources, talent development and communications. She previously held senior executive roles at Aviva, the multinational insurance company, as Executive Vice President Human Resources and Executive Vice President Strategy and Corporate Development.

Qualifications: Bachelor of Arts from the University of Western Ontario and a Masters of Education from the University of Toronto.

External appointments:

Listed: Non-executive Director and Chair of the Management Resources & Compensation Committee of Interfor Corporation, a Canadian listed company, which is one of the world’s largest providers of lumber.

Non-listed: Not applicable. |

Skills and experience:

Johan was President and Chief Executive Officer of Skanska AB, a leading multinational construction and project development company until 2017. Over a thirty-year career with Skanska, he held a variety of leadership roles in Europe and America, before becoming President and Chief Executive in 2008. He also served as President and Chief Executive Officer of BPA (now Bravida), a listed mechanical and installation group from 1996 to 2000.

Qualifications: Masters degree in Engineering from the KTH Royal Institute of Technology, Sweden.

External appointments:

Listed: Non-executive Director of Sandvik AB.

Non-listed: Not applicable. |

Skills and experience:

Shaun was until September 2019, the Global Chief Operating Officer of KPMG International, where he was responsible for the execution of the firm’s global strategy and for the delivery of various global initiatives. Over a thirty-year career with KPMG, the majority of which was spent in the US, he held a variety of senior leadership positions, including Partner in Charge, US Transaction Services (2001-2005), Vice Chair and Head of US Tax (2005 to 2010) and Vice Chair Operations and Chief Operating Officer Americas (2010 to 2015), before his appointment as Global Chief Operating Officer in 2015.

Qualifications: Fellow of Chartered Accountants Ireland and a US Certified Public Accountant. Shaun also holds a Bachelor of Commerce and Diploma in Professional Accounting from University College Dublin and an honorary doctorate from Queen’s University Belfast.

External appointments:

Listed: Not applicable.

Non-listed: Shaun holds a number of non-profit board memberships.

*Audit Committee Financial Expert as determined by the Board. |

||||||||||

Table of Contents

| Board of Directors - continued | ||||||||||||

|

Patrick J. Kennedy |

Heather Ann McSharry |

Mary K. Rhinehart |

||||||||||

|

Non-executive Director |

Non-executive Director |

Non-executive Director |

||||||||||

|

Appointed to the Board: January 2015 |

Appointed to the Board: February 2012 |

Appointed to the Board: October 2018 |

||||||||||

|

Nationality: Irish Age: 66 |

Nationality: Irish Age: 58 |

Nationality: United States Age: 61 |

||||||||||

|

Committee membership: |

Committee membership: |

Committee membership: |

||||||||||

|

Skills and experience:

Pat was Chairman of the Executive Board of Directors of SHV Holdings (SHV), a large family-owned Dutch multinational company with a diverse portfolio of businesses, including the production and distribution of energy, the provision of industrial services, heavy lifting and transport solutions, cash and carry wholesale and the provision of private equity. During a 32 year career with SHV, he held various leadership roles across SHV’s diverse portfolio of businesses, while living in various parts of the world, and was a member of the Executive Board of SHV from 2001, before becoming Executive Chairman in 2006. He retired from SHV in mid-2014.

Qualifications: BComm, MBS.

External appointments:

Listed: Not applicable.

Non-listed: Member of the Supervisory Board of SHV Holdings N.V. |

Skills and experience:

Heather Ann is a former Managing Director Ireland of Reckitt Benckiser and Boots Healthcare and was previously a non-executive Director of Bank of Ireland plc and IDA Ireland.

Qualifications: BComm, MBS.

External appointments:

Listed: Non-executive Director of Greencore Group plc, Jazz Pharmaceuticals plc and Uniphar Group plc.

Non-listed: Director of the Institute of Directors in Ireland. |

Skills and experience:

Mary is Chairman, Chief Executive Officer and President of Johns Manville Corporation, a Berkshire Hathaway company, which is a leading global manufacturer of premium-quality building products and engineered specialty materials. Over nearly 40 years with Johns Manville she has held a wide range of global leadership roles, encompassing responsibility for business management and strategic business development and was also Chief Financial Officer. Mary was until recently a non-executive Director of Ply Gem Holdings Inc., a leader in exterior building products in North America, and lead Director of CoBiz Financial Inc.

Qualifications: Bachelor’s degree in Finance from the University of Colorado; MBA from the University of Denver.

External appointments:

Listed: Not applicable.

Non-listed: Chairman, Chief Executive Officer and President of Johns Manville Corporation and member of the Board of Trustees of the University of Denver.

*Audit Committee Financial Expert as determined by the Board. |

||||||||||

Table of Contents

|

|

||||||||||||

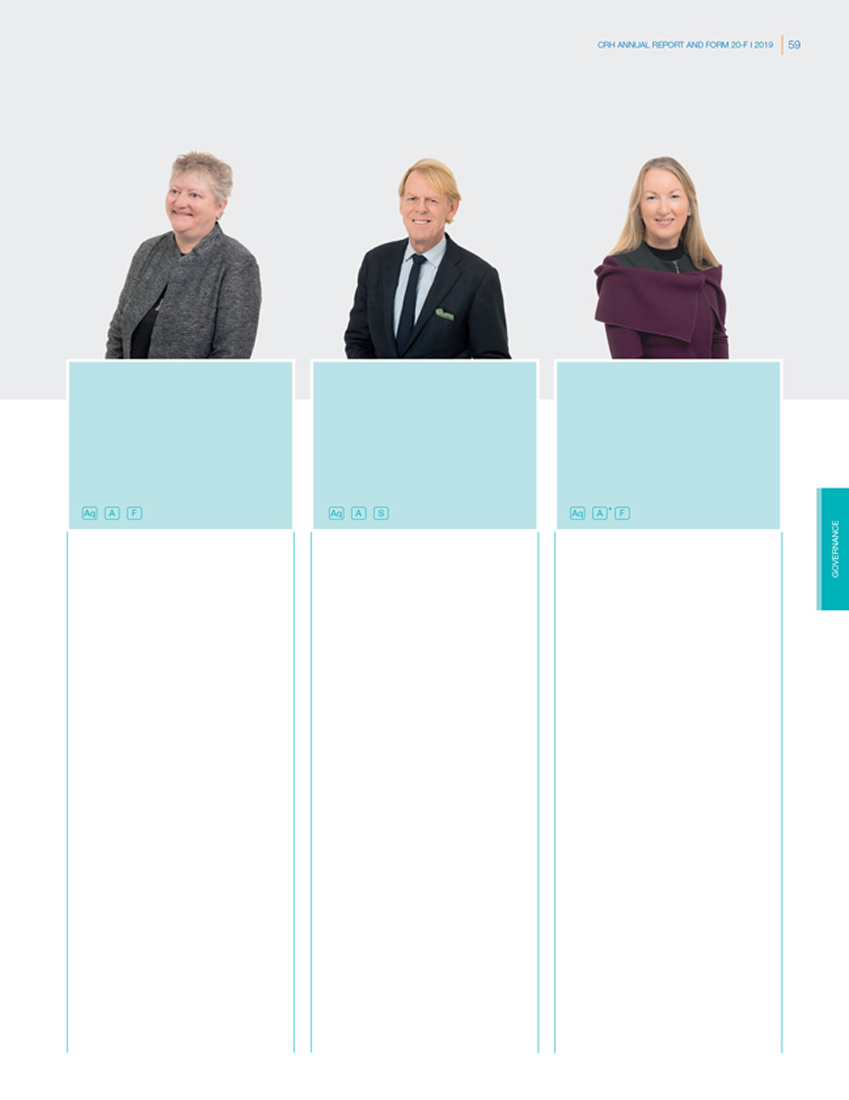

|

Lucinda J. Riches |

Henk Th. Rottinghuis |

Siobhán Talbot |

||||||||||

|

Non-executive Director |

Non-executive Director |

Non-executive Director |

||||||||||

|

Appointed to the Board: March 2015 |

Appointed to the Board: February 2014 |

Appointed to the Board: December 2018 |

||||||||||

|

Nationality: British Age: 58 |

Nationality: Dutch Age: 64 |

Nationality: Irish Age: 56 |

||||||||||

|

Committee membership: |

Committee membership: |

Committee membership: |

||||||||||

|

Skills and experience:

Lucinda spent the majority of her career in investment banking, including 21 years in UBS Investment Bank and its predecessor firms where she worked until 2007. She held senior management positions in the UK and the US, including Global Head and Chairman of UBS’ Equity Capital Markets Group and Vice Chairman of the Investment Banking Division.

Qualifications: Masters in Philosophy, Politics and Economics and a Masters in Political Science.

External appointments:

Listed: Non-executive Director of Ashtead Group plc, Greencoat UK Wind plc and ICG Enterprise Trust plc.

Non-listed: Non-executive Director of the British Standards Institution. |

Skills and experience:

Henk has a background in distribution, wholesale and logistics. Until 2010, he was Chief Executive Officer at Pon Holdings B.V., a large, privately held international company which is focused on the supply and distribution of passenger cars and trucks, and equipment for the construction and marine sectors. He was also a member of the Supervisory Boards of the Royal Bank of Scotland N.V., the food-retail group Detailresult Groep, the retail group Blokker Holding B.V. and Chairman of the Supervisory Board of Stork Technical Services B.V.

Qualifications: Masters degree in Dutch Law; PMD Harvard Business School.

External appointments:

Listed: Not applicable.

Non-listed: Chairman of Koole Terminals B.V. Henk also holds several non-profit board memberships. |

Skills and experience:

Siobhán is Group Managing Director of Glanbia plc, a global nutrition company with operations in 32 countries, a position she has held since 2013. She has been a member of the Glanbia Board since 2009 and was previously Finance Director, a role which encompassed responsibility for Glanbia’s strategic planning. Prior to joining Glanbia, she worked with PricewaterhouseCoopers in Dublin and Sydney.

Qualifications: Fellow of Chartered Accountants Ireland; Bachelor of Commerce; Diploma in Professional Accounting from University College Dublin.

External appointments:

Listed: Group Managing Director of Glanbia plc.

Non-listed: Director of the Irish Business Employers Confederation (IBEC).

*Audit Committee Financial Expert as determined by the Board. |

||||||||||

Table of Contents

| 1. |

The Governance Appendix is published in conjunction with the Directors’ Report in compliance with Section 1373 of the Companies Act 2014. For the purposes of Section 1373(2) of the Companies Act 2014, the Governance Appendix and the risk management disclosures on pages 26 to 29 and 108 to 113 form part of, and are incorporated by reference into, this Corporate Governance Report. |

The primary (premium) listing of CRH plc is on the LSE, with the listing on Euronext Dublin characterised as secondary. For this reason, CRH plc is not subject to the same ongoing listing requirements as would apply to an Irish company with a primary listing on Euronext Dublin. For further information, shareholders should consult their financial adviser. Further details on the Group’s listing arrangements, including its premium listing on the LSE, are set out on page 72.

Table of Contents

|

CRH ANNUAL REPORT AND FORM 20-F I 2019

|

61 |

Table of Contents

| 62 |

CRH ANNUAL REPORT AND FORM 20-F I 2019

|

Table of Contents

|

CRH ANNUAL REPORT AND FORM 20-F I 2019

|

63 |

Table of Contents

| 1. |

The Board has determined that all of the non-executive Directors on the Audit Committee are independent according to the requirements of Rule 10A.3 of the rules of the Securities and Exchange Commission (SEC) and Provision 10 of the 2018 Code. |

| 2. |

A copy of Section 404 of the Sarbanes Oxley Act 2002 can be obtained from the SEC’s website, www.sec.gov. |

Table of Contents

|

CRH ANNUAL REPORT AND FORM 20-F I 2019

|

65 |

Table of Contents

| 66 |

CRH ANNUAL REPORT AND FORM 20-F I 2019

|

Table of Contents

|

CRH ANNUAL REPORT AND FORM 20-F I 2019

|

67 |

Table of Contents

Table of Contents

|

CRH ANNUAL REPORT AND FORM 20-F I 2019

|

69 |

Table of Contents

| 70 |

CRH ANNUAL REPORT AND FORM 20-F I 2019

|

Table of Contents

|

CRH ANNUAL REPORT AND FORM 20-F I 2019

|

71 |

Table of Contents

| 72 |

CRH ANNUAL REPORT AND FORM 20-F I 2019

|

Table of Contents

|

CRH ANNUAL REPORT AND FORM 20-F I 2019

|

73 |

Table of Contents

Table of Contents

|

CRH ANNUAL REPORT AND FORM 20-F I 2019

|

75 |

Table of Contents

| 76 |

CRH ANNUAL REPORT AND FORM 20-F I 2019

|

Table of Contents

|

CRH ANNUAL REPORT AND FORM 20-F I 2019

|

77 |

Table of Contents

| 78 |

CRH ANNUAL REPORT AND FORM 20-F I 2019

|

Table of Contents

|

CRH ANNUAL REPORT AND FORM 20-F I 2019

|

79 |

Table of Contents

| 80 |

CRH ANNUAL REPORT AND FORM 20-F I 2019

|

Table of Contents

|

CRH ANNUAL REPORT AND FORM 20-F I 2019

|

81 |

Table of Contents

| 82 |

CRH ANNUAL REPORT AND FORM 20-F I 2019

|

Table of Contents

|

CRH ANNUAL REPORT AND FORM 20-F I 2019

|

83 |

Table of Contents

| 84 |

CRH ANNUAL REPORT AND FORM 20-F I 2019

|

Table of Contents

|

CRH ANNUAL REPORT AND FORM 20-F I 2019

|

85 |

Table of Contents

| 86 |

CRH ANNUAL REPORT AND FORM 20-F I 2019

|

Table of Contents

|

CRH is a leading provider of structural concrete to the Danish market. In 2019, CRH Denmark, part of our Europe Materials Division, supplied 15,000m² of materials to the ‘Karré 31’ project in the town of Holbaek, north-east of Copenhagen. Products included hollow-core floor slabs, walls and facades for the 17-story apartment building. |

Table of Contents

| 88 |

CRH ANNUAL REPORT AND FORM 20-F I 2019

|

Table of Contents

|

CRH ANNUAL REPORT AND FORM 20-F I 2019

|

89 |

Table of Contents

| 90 |

CRH ANNUAL REPORT AND FORM 20-F I 2019

|

Table of Contents

|

CRH ANNUAL REPORT AND FORM 20-F I 2019

|

91 |

Table of Contents

| 92 |

CRH ANNUAL REPORT AND FORM 20-F I 2019

|

Table of Contents

|

CRH ANNUAL REPORT AND FORM 20-F I 2019

|

93 |

Table of Contents

| 94 |

CRH ANNUAL REPORT AND FORM 20-F I 2019

|

Table of Contents

|

CRH ANNUAL REPORT AND FORM 20-F I 2019

|

95 |

Table of Contents

| 96 |

CRH ANNUAL REPORT AND FORM 20-F I 2019

|

Table of Contents

|

CRH ANNUAL REPORT AND FORM 20-F I 2019

|

97 |

Table of Contents

| 98 |

CRH ANNUAL REPORT AND FORM 20-F I 2019

|

Table of Contents

|

CRH ANNUAL REPORT AND FORM 20-F I 2019

|

99 |

Table of Contents

| 100 |

CRH ANNUAL REPORT AND FORM 20-F I 2019

|

Table of Contents

|

Part of CRH’s Americas Materials Division and in operation since January 2005, Texas Materials’ plant at Seward Junction, located in the Greater Austin metropolitan area, includes a rail terminal to facilitate delivery of aggregates from the company’s nearby quarry in Marble Falls. The rail terminal was expanded in 2016 to help meet strong demand in what is the fastest growing large city in the US. |

Table of Contents

| 102 |

CRH ANNUAL REPORT AND FORM 20-F I 2019

|

Table of Contents

|

CRH ANNUAL REPORT AND FORM 20-F I 2019

|

103 |

Table of Contents

| 104 |

CRH ANNUAL REPORT AND FORM 20-F I 2019

|

Table of Contents

|

CRH ANNUAL REPORT AND FORM 20-F I 2019

|

105 |

Table of Contents

| 106 |

CRH ANNUAL REPORT AND FORM 20-F I 2019

|

Table of Contents

| In July 2019, OPTERRA, part of CRH’s Europe Materials Division and one of the leading cement producers in Germany, officially inaugurated a new exhaust gas purification system at its Karsdorf cement plant near Leipzig. The new filter technology, which includes a state-of-the-art AUTONOX ® Low Dust System installed on the existing kilns, enables the factory to comply with new limits for dust, ammonia and nitrogen oxide emissions. |

Table of Contents

| 108 |

CRH ANNUAL REPORT AND FORM 20-F I 2019

|

Table of Contents

|

CRH ANNUAL REPORT AND FORM 20-F I 2019

|

109 |

Table of Contents

| 110 |

CRH ANNUAL REPORT AND FORM 20-F I 2019

|

Table of Contents

|

CRH ANNUAL REPORT AND FORM 20-F I 2019

|

111 |

Table of Contents

| 112 |

CRH ANNUAL REPORT AND FORM 20-F I 2019

|

Table of Contents

|

CRH ANNUAL REPORT AND FORM 20-F I 2019

|

113 |

Table of Contents

Oldcastle Infrastructure, part of CRH’s Building Products Division, is supplying 2.1 miles of pre-fabricated concrete

box culverts to a storm water drainage project in downtown Tampa, Florida. The project will reduce flooding and

provide enhanced safety for pedestrians and vehicles. Construction is expected to be completed in 2021.

Table of Contents

| Financials |

Table of Contents

|

116 |

CRH ANNUAL REPORT AND FORM 20-F | 2019 |

Table of Contents

|

CRH ANNUAL REPORT AND FORM 20-F | 2019 |

117 |

Table of Contents

|

118 |

CRH ANNUAL REPORT AND FORM 20-F | 2019 |

[THIS PAGE INTENTIONALLY LEFT BLANK]

Table of Contents

|

CRH ANNUAL REPORT AND FORM 20-F | 2019 |

119 |

Table of Contents

|

120 |

CRH ANNUAL REPORT AND FORM 20-F | 2019 |

[THIS PAGE INTENTIONALLY LEFT BLANK]

Table of Contents

|

CRH ANNUAL REPORT AND FORM 20-F | 2019 |

121 |

Table of Contents

|

122 |

CRH ANNUAL REPORT AND FORM 20-F | 2019 |

[THIS PAGE INTENTIONALLY LEFT BLANK]

Table of Contents

|

CRH ANNUAL REPORT AND FORM 20-F | 2019 |

123 |

Table of Contents

|

124 |

CRH ANNUAL REPORT AND FORM 20-F | 2019 |

[THIS PAGE INTENTIONALLY LEFT BLANK]

Table of Contents

Table of Contents

|

126 |

CRH ANNUAL REPORT AND FORM 20-F | 2019 |

Independent Auditor’s US Reports - continued

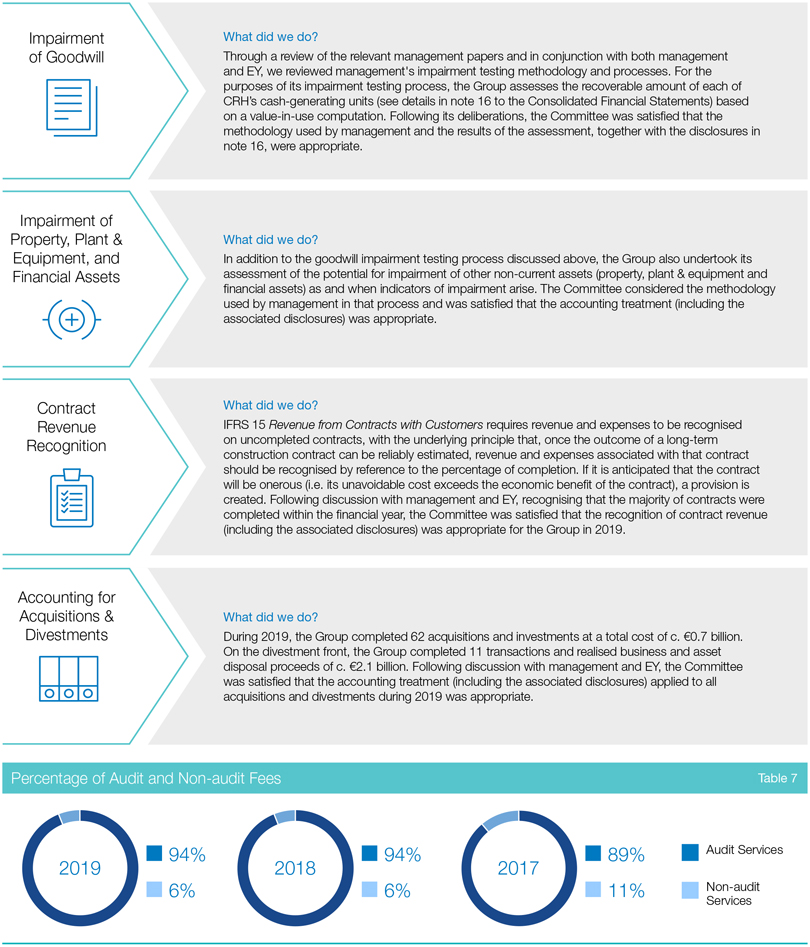

| estimates and performed sensitivity analysis of significant assumptions to evaluate the change in the fair value of the CGUs resulting from changes in these assumptions. We involved valuation specialists to assist in our evaluation of the valuation methodology and comparison of key inputs to external market data (principally risk-free rates, country risk premium and inflation rates) used by management in calculating discount rates. | ||

| We also evaluated management’s disclosures in respect of impairment testing. | ||

| Assessment of the carrying value of property, plant and equipment and financial assets | ||

|

Description of the Matter |

At 31 December 2019, the Company’s carrying value of property, plant and equipment (PP&E) and financial assets was € 17.4 billion and € 0.7 billion respectively. As discussed in notes 15 and 17 of the financial statements, the carrying values of PP&E and financial assets are reviewed for indicators of impairment at each reporting date and are subject to impairment testing when events or changes in circumstances indicate that the carrying values may not be recoverable. For an asset that does not generate largely independent cash inflows, the recoverable amount is determined by reference to the CGU to which the asset belongs. | |

| Auditing management’s impairment test is complex and judgemental due to the significant estimation required in determining the fair value of the CGUs. In particular,judgemental aspects include assumptions of future profitability, revenue growth, margins and forecast cash flows, and the selection of appropriate discount rates. | ||

|

How We Addressed the Matter in Our Audit |

We obtained an understanding, evaluated the design and tested the operating effectiveness of controls over the Company’s impairment review process. For example, we tested controls over the Company’s review of significant assumptions, including future profitability, revenue growth, margins and forecast cash flows, and the selection of appropriate discount rates, among others. | |

| To test the estimated fair value of the Company CGUs where indicators of impairment existed, we performed audit procedures that included, among others, evaluation of the internal and external indicators of impairment used within the Company’s assessment, assessing fair values methodologies and testing the significant assumptions discussed above and the underlying data used by the Company in its analysis. We compared the significant assumptions used by management to external economic forecasts and construction activity measures, the Company’s historical results, and evaluated whether changes in the Company’s business would affect the significant assumptions. We assessed the historical accuracy of management’s estimates and performed sensitivity analysis of significant assumptions to evaluate the change in the fair value of the reporting units resulting from changes in these assumptions. We involved valuation specialists to assist in our evaluation of the valuation methodology and comparison of key inputs to external market data (principally risk-free rates, country risk premium and inflation rates) used by management in calculating discount rates. | ||

| Revenue recognition for construction contracts | ||

|

Description of the Matter |

At 31 December 2019, the Company’s revenue for construction contracts was € 5.9 billion. As discussed in note 1 of the financial statements, revenue yet to be recognised from fixed-price long-term construction contracts, primarily within the Europe Materials and Americas Materials businesses, amounted to € 1.9 billion at 31 December 2019. The majority of the Company’s construction contracts have a maturity within one year. | |

| Auditing management’s revenue recognition for construction contracts is complex and judgemental as such recognition is materially affected by changes in assumptions regarding the determination of the stage of completion, the timing of revenue recognition and the calculation under the percentage-of-completion method. In particular, judgemental aspects include assumptions of the estimated materials, hours, and other costs required to fulfil contractual performance obligations. | ||

|

How We Addressed the Matter in Our Audit |

We obtained an understanding, evaluated the design and tested the operating effectiveness of controls over the Company’s revenue recognition for construction contracts process. For example, we tested controls over the Company’s process for evaluating the estimated contract value, estimated and actual costs upon completion, including the estimation of units of measurement, and the amount of profit or loss to be recognised in accordance with IFRS 15. | |

| To test the revenue recognised by the Company, we performed audit procedures that included, among others, testing a sample of contracts and evaluating the original executed contract including any change orders. For these contracts, we tested key components of the cost to complete estimates and actual costs to date, including vouching materials, hours, and subcontractor costs to source documentation, and conducted interviews with and inspected questionnaires prepared by project personnel. We recalculated revenues recognised and assessed compliance with IFRS 15. In addition, our audit procedures included performing a retrospective review of estimated profit and costs to complete and enquiring of key personnel regarding adjustments for job costing and potential contract losses. | ||

ERNST & YOUNG

We have served as the Company’s auditor since 1988.

Dublin, Ireland

27 February 2020

Table of Contents

|

CRH ANNUAL REPORT AND FORM 20-F | 2019 |

127 |

Table of Contents

|

128 |

CRH ANNUAL REPORT AND FORM 20-F | 2019 |

for the financial year ended 31 December 2019

|

2019 € m |

Restated (i)

€ m |

Restated (i)

€ m |

||||||||||||

|

Notes |

||||||||||||||

|

1,2 |

Revenue |

25,129 | 23,241 | 21,653 | ||||||||||

|

4 |

Cost of sales |

(16,846) | (15,572) | (14,275) | ||||||||||

|

Gross profit |

8,283 | 7,669 | 7,378 | |||||||||||

|

4 |

Operating costs |

(5,789) | (5,598) | (5,451) | ||||||||||

|

2,5,7,8 |

Group operating profit |

2,494 | 2,071 | 1,927 | ||||||||||

|

2,6 |

(Loss)/profit on disposals |

(1) | (27) | 54 | ||||||||||

|

Profit before finance costs |

2,493 | 2,044 | 1,981 | |||||||||||

|

10 |

Finance costs |

(346) | (339) | (301) | ||||||||||

|

10 |

Finance income |

20 | 34 | 12 | ||||||||||

|

10 |

Other financial expense |

(112) | (46) | (59) | ||||||||||

|

11 |

Share of equity accounted investments’ profit |

60 | 48 | 52 | ||||||||||

|

2 |

Profit before tax from continuing operations |

2,115 | 1,741 | 1,685 | ||||||||||

|

12 |

Income tax expense |

(477) | (396) | (12) | ||||||||||

| Group profit for the financial year from continuing operations | 1,638 | 1,345 | 1,673 | |||||||||||

|

3 |

Profit after tax for the financial year from discontinued operations | 310 | 1,176 | 246 | ||||||||||

| Group profit for the financial year | 1,948 | 2,521 | 1,919 | |||||||||||

|

Profit attributable to: |

||||||||||||||

|

Equity holders of the Company |

||||||||||||||

|

From continuing operations |

1,620 | 1,342 | 1,650 | |||||||||||

|

From discontinued operations |

309 | 1,175 | 245 | |||||||||||

|

Non-controlling interests |

||||||||||||||

|

From continuing operations |

18 | 3 | 23 | |||||||||||

|

From discontinued operations |

1 | 1 | 1 | |||||||||||

|

Group profit for the financial year |

1,948 | 2,521 | 1,919 | |||||||||||

|

14 |

Basic earnings per Ordinary Share |

240.7c | 302.4c | 226.8c | ||||||||||

|

14 |

Diluted earnings per Ordinary Share |

238.8c | 300.9c | 225.4c | ||||||||||

|

14 |

Basic earnings per Ordinary Share from continuing operations | 202.2c | 161.2c | 197.4c | ||||||||||

|

14 |

Diluted earnings per Ordinary Share from continuing operations | 200.6c | 160.4c | 196.2c | ||||||||||

| (i) |

Restated to show the results of our former Europe Distribution segment in discontinued operations. See note 3 for further details. |

Table of Contents

Table of Contents

|

130 |

CRH ANNUAL REPORT AND FORM 20-F | 2019 |

as at 31 December 2019

|

2019 € m |

2018 € m |

|||||||||

|

Notes |

||||||||||

|

ASSETS |

||||||||||

|

Non-current assets |

||||||||||

|

15 |

Property, plant and equipment |

17,424 | 15,761 | |||||||

|

16 |

Intangible assets |

8,434 | 8,433 | |||||||

|

17 |

Investments accounted for using the equity method |

690 | 1,163 | |||||||

|

17 |

Other financial assets |

12 | 23 | |||||||

|

19 |

Other receivables |

317 | 181 | |||||||

|

27 |

Derivative financial instruments |

76 | 30 | |||||||

|

29 |

Deferred income tax assets |

67 | 71 | |||||||

|

Total non-current assets |

27,020 | 25,662 | ||||||||

|

Current assets |

||||||||||

|

18 |

Inventories |

2,742 | 3,061 | |||||||

|

19 |

Trade and other receivables |

3,767 | 4,074 | |||||||

|

Current income tax recoverable |

20 | 15 | ||||||||

|

27 |

Derivative financial instruments |

6 | 15 | |||||||

|

25 |

Cash and cash equivalents |

3,755 | 2,346 | |||||||

|

Total current assets |

10,290 | 9,511 | ||||||||

|

Total assets |

37,310 | 35,173 | ||||||||

|

EQUITY |

||||||||||

|

Capital and reserves attributable to the Company’s equity holders |

||||||||||

|

31 |

Equity share capital |

272 | 287 | |||||||

|

31 |

Preference share capital |

1 | 1 | |||||||

|

31 |

Share premium account |

6,534 | 6,534 | |||||||

|

31 |

Treasury Shares and own shares |

(325) | (792) | |||||||

|

Other reserves |

326 | 296 | ||||||||

|

Foreign currency translation reserve |

210 | (109) | ||||||||

|

Retained income |

9,922 | 9,812 | ||||||||

|

Capital and reserves attributable to the Company’s equity holders |

16,940 | 16,029 | ||||||||

|

33 |

Non-controlling interests |

540 | 525 | |||||||

|

Total equity |

17,480 | 16,554 | ||||||||

|

LIABILITIES |

||||||||||

|

Non-current liabilities |

||||||||||

|

22 |

Lease liabilities |

1,240 | - | |||||||

|

26 |

Interest-bearing loans and borrowings |

8,199 | 8,698 | |||||||

|

27 |

Derivative financial instruments |

1 | 18 | |||||||

|

29 |

Deferred income tax liabilities |

2,338 | 2,209 | |||||||

|

20 |

Other payables |

485 | 472 | |||||||

|

30 |

Retirement benefit obligations |

427 | 424 | |||||||

|

28 |

Provisions for liabilities |

760 | 719 | |||||||

|

Total non-current liabilities |

13,450 | 12,540 | ||||||||

|

Current liabilities |

||||||||||

|

22 |

Lease liabilities |

271 | - | |||||||

|

20 |

Trade and other payables |

4,376 | 4,609 | |||||||

|

Current income tax liabilities |

503 | 443 | ||||||||

|

26 |

Interest-bearing loans and borrowings |

815 | 618 | |||||||

|

27 |

Derivative financial instruments |

16 | 41 | |||||||

|

28 |

Provisions for liabilities |

399 | 368 | |||||||

|

Total current liabilities |

6,380 | 6,079 | ||||||||

|

Total liabilities |

19,830 | 18,619 | ||||||||

|

Total equity and liabilities |

37,310 | 35,173 | ||||||||

|

R. Boucher, A. Manifold, Directors |

||||||||||

Table of Contents

Table of Contents

|

132 |

CRH ANNUAL REPORT AND FORM 20-F | 2019 |

Consolidated Statement of Cash Flows

for the financial year ended 31 December 2019

|

2019 € m |

2018 € m |

2017 € m |

||||||||||||

|

Notes |

||||||||||||||

|

Cash flows from operating activities |

||||||||||||||

|

Profit before tax from continuing operations |

2,115 | 1,741 | 1,685 | |||||||||||

|

3 |

Profit before tax from discontinued operations |

333 | 1,679 | 328 | ||||||||||

|

Profit before tax |

2,448 | 3,420 | 2,013 | |||||||||||

|

10 |

Finance costs (net) |

445 | 351 | 349 | ||||||||||

|

11 |

Share of equity accounted investments’ profit |

(72) | (60) | (65) | ||||||||||

|

6 |

Profit on disposals |

(226) | (1,539) | (59) | ||||||||||

|

Group operating profit |

2,595 | 2,172 | 2,238 | |||||||||||

|

15,22 |

Depreciation charge |

1,538 | 1,071 | 1,006 | ||||||||||

|

16 |

Amortisation of intangible assets |

59 | 61 | 66 | ||||||||||

|

15,16 |

Impairment charge |

8 | 56 | - | ||||||||||

|

9 |

Share-based payment expense |

77 | 67 | 65 | ||||||||||

|

Other (primarily pension payments) |

(3) | (67) | (186) | |||||||||||

|

21 |

Net movement on working capital and provisions |

(64) | (463) | (209) | ||||||||||

|

Cash generated from operations |

4,210 | 2,897 | 2,980 | |||||||||||

|

Interest paid (including leases) (i) |

(419) | (335) | (317) | |||||||||||

|

Corporation tax paid |

(325) | (663) | (474) | |||||||||||

|

Net cash inflow from operating activities |

3,466 | 1,899 | 2,189 | |||||||||||

|

Cash flows from investing activities |

||||||||||||||

|

6 |

Proceeds from disposals (net of cash disposed and deferred proceeds) |

2,096 | 3,009 | 222 | ||||||||||

|

Interest received |

20 | 34 | 11 | |||||||||||

|

17 |

Dividends received from equity accounted investments |

35 | 48 | 31 | ||||||||||

|

15 |

Purchase of property, plant and equipment |

(1,229) | (1,121) | (1,044) | ||||||||||

|

32 |

Acquisition of subsidiaries (net of cash acquired) |

(650) | (3,505) | (1,841) | ||||||||||

|

17 |

Other investments and advances |

(29) | (2) | (11) | ||||||||||

|

21 |

Deferred and contingent acquisition consideration paid |

(48) | (55) | (53) | ||||||||||

|

Net cash inflow/(outflow) from investing activities |

195 | (1,592) | (2,685) | |||||||||||

|

Cash flows from financing activities |

||||||||||||||

|

31 |

Proceeds from issue of shares (net) |

- | 11 | 42 | ||||||||||

|

Proceeds from exercise of share options |

20 | 7 | - | |||||||||||

|

Transactions involving non-controlling interests |

(19) | - | (37) | |||||||||||

|

23 |

Increase in interest-bearing loans and borrowings |

91 | 1,434 | 1,010 | ||||||||||

|

23 |

Net cash flow arising from derivative financial instruments |

(36) | 6 | 169 | ||||||||||

|

10 |

Premium paid on early debt redemption |

- | - | (18) | ||||||||||

|

23 |

Repayment of interest-bearing loans, borrowings and finance leases (ii) |

(572) | (246) | (343) | ||||||||||

|

22 |

Repayment of lease liabilities (iii) |

(317) | - | - | ||||||||||

|

31 |

Treasury Shares/own shares purchased |

(852) | (792) | (3) | ||||||||||

|

13 |

Dividends paid to equity holders of the Company |

(584) | (521) | (469) | ||||||||||

|

13 |

Dividends paid to non-controlling interests |

(10) | (12) | (8) | ||||||||||

|

Net cash (outflow)/inflow from financing activities |

(2,279) | (113) | 343 | |||||||||||

|

Increase/(decrease) in cash and cash equivalents |

1,382 | 194 | (153) | |||||||||||

|

Reconciliation of opening to closing cash and cash equivalents |

||||||||||||||

|

Cash and cash equivalents at 1 January |

2,346 | 2,135 | 2,449 | |||||||||||

|

Translation adjustment |

27 | 17 | (161) | |||||||||||

|

Increase/(decrease) in cash and cash equivalents |

1,382 | 194 | (153) | |||||||||||

|

25 |

Cash and cash equivalents at 31 December |

3,755 | 2,346 | 2,135 | ||||||||||

| (i) |

Leases include finance leases previously capitalised under IAS 17 Leases in 2018 and 2017 and all capitalised leases included as lease liabilities under IFRS 16 Leases in 2019. |

| (ii) |

Finance leases as previously capitalised under IAS 17 in 2018 and 2017. |

| (iii) |

Repayment of lease liabilities capitalised under IFRS 16 in 2019 amounted to € 386 million, of which € 69 million related to interest paid which is presented in cash flows from operating activities. |

Table of Contents

Table of Contents

|

134 |

CRH ANNUAL REPORT AND FORM 20-F | 2019 |

Accounting Policies - continued

Primary statement line item / financial metric

|

As at 1 January 2019

€ m |

||||||

| Consolidated Balance Sheet | ||||||

|

Property, plant and equipment (i) (ii) |

+1,939 | |||||

| Lease liabilities; net debt (i) (ii) | +1,954 | |||||

|

For the year ended

31 December 2019 € m |

||||||

| Consolidated Income Statement | ||||||

|

Depreciation (i) |

+334 | |||||

|

Finance costs |

+69 | |||||

|

EPS (i) (iii) |

-3c | |||||

| Consolidated Statement of Cash Flows | ||||||

|

Net cash flow from operating activities |

+317 | |||||

| Net cash flow from financing activities | -317 | |||||

| (i) |

The operating profit and depreciation impact of IFRS 16 on discontinued operations included above are + € 4 million and + € 63 million respectively for the year ended 31 December 2019. The right-of-use asset and discounted lease liability related to discontinued operations are € 398 million as at 1 January 2019. |

| (ii) |

The impact of the adoption of IFRS 16 on property, plant and equipment and net debt is net of existing finance leases ( € 23 million at 31 December 2018) which have been recorded as part of the right-of-use assets and lease liabilities at their previous carrying amounts on 1 January 2019. |

| (iii) |

The impact of the adoption of IFRS 16 on operating profit for the year ended 31 December 2019 is € 0.05 billion and has been calculated based only on the portfolio of leases which existed at 1 January 2019. |

A reconciliation of the operating lease commitment previously reported under IAS 17 to the discounted lease liability as at 1 January 2019 under IFRS 16 is as follows:

|

As at 1 January 2019

€ m |

||||

|

Operating lease commitment under IAS 17 |

1,911 | |||

|

Lease extensions beyond break date |

632 | |||

|

Leases that are cancellable at any time |

35 | |||

|

Existing IAS 17 finance leases (i) |

23 | |||

|

Other lease payments not included in discounted lease liability under IFRS 16 (ii) |

(108) | |||

|

Undiscounted lease liability under IFRS 16 |

2,493 | |||

|

Less impact of discounting |

(516) | |||

|

Discounted lease liability under IFRS 16 |

1,977 | |||

| (i) |

Existing IAS 17 finance leases are presented at discounted amounts as the impact of discounting on these leases is not considered material. |

| (ii) |

Other lease payments not included in the discounted lease liability under IFRS 16 include payments related to short-term and low-value leases which were included in the operating lease commitment under IAS 17 but are exempt from capitalisation under IFRS 16. |

Table of Contents

|

CRH ANNUAL REPORT AND FORM 20-F | 2019 |

135 |

Table of Contents

|

136 |

CRH ANNUAL REPORT AND FORM 20-F | 2019 |

Accounting Policies - continued

Table of Contents

|

CRH ANNUAL REPORT AND FORM 20-F | 2019 |

137 |

Table of Contents

|

138 |

CRH ANNUAL REPORT AND FORM 20-F | 2019 |

Accounting Policies - continued

Table of Contents

|

CRH ANNUAL REPORT AND FORM 20-F | 2019 |

139 |

Table of Contents

|

140 |

CRH ANNUAL REPORT AND FORM 20-F | 2019 |

Accounting Policies - continued

Table of Contents

|

CRH ANNUAL REPORT AND FORM 20-F | 2019 |

141 |

Table of Contents

|

142 |

CRH ANNUAL REPORT AND FORM 20-F | 2019 |

Accounting Policies - continued

Table of Contents

|

CRH ANNUAL REPORT AND FORM 20-F | 2019 |

143 |

Table of Contents

|

144 |

CRH ANNUAL REPORT AND FORM 20-F | 2019 |

Accounting Policies - continued

The principal exchange rates used for the translation of results, cash flows and balance sheets into euro were as follows:

| Average | Year-end | |||||||||||||||||||||||

| euro 1 = | 2019 | 2018 | 2017 | 2019 | 2018 | |||||||||||||||||||

|

Brazilian Real |

4.4134 | 4.3085 | 3.6054 | 4.5157 | 4.4440 | |||||||||||||||||||

|

Canadian Dollar |

1.4855 | 1.5294 | 1.4647 | 1.4598 | 1.5605 | |||||||||||||||||||

|

Chinese Renminbi |

7.7355 | 7.8081 | 7.6290 | 7.8205 | 7.8751 | |||||||||||||||||||

|

Hungarian Forint |

325.2967 | 318.8897 | 309.1933 | 330.5300 | 320.9800 | |||||||||||||||||||

|

Indian Rupee |

78.8361 | 80.7332 | 73.5324 | 80.1870 | 79.7298 | |||||||||||||||||||

|

Philippine Peso |

57.9851 | 62.2101 | 56.9734 | 56.9000 | 60.1130 | |||||||||||||||||||

|

Polish Zloty |

4.2976 | 4.2615 | 4.2570 | 4.2568 | 4.3014 | |||||||||||||||||||

|

Pound Sterling |

0.8778 | 0.8847 | 0.8767 | 0.8508 | 0.8945 | |||||||||||||||||||

|

Romanian Leu |

4.7453 | 4.6540 | 4.5688 | 4.7830 | 4.6635 | |||||||||||||||||||

|

Serbian Dinar |

117.8377 | 118.2302 | 121.3232 | 117.8237 | 118.3157 | |||||||||||||||||||

|

Swiss Franc |

1.1124 | 1.1550 | 1.1117 | 1.0854 | 1.1269 | |||||||||||||||||||

|

Ukrainian Hryvnia |

28.8881 | 32.0987 | 30.0341 | 26.7377 | 31.6900 | |||||||||||||||||||

|

US Dollar |

1.1195 | 1.1810 | 1.1297 | 1.1234 | 1.1450 | |||||||||||||||||||

Table of Contents

Table of Contents

|

146 |

CRH ANNUAL REPORT AND FORM 20-F | 2019 |

1. Revenue - continued

|

Year ended 31 December |

||||||||||||||||||||||||||||||||||||

|

Americas

Materials (iii) 2019 |

Europe

Materials (iii) 2019 |

Building

Products 2019 |

Total

2019 |

Americas

Materials (iii) 2018 |

Europe

Materials (iii) 2018 |

Building

Products 2018 |

Total

2018 |

|||||||||||||||||||||||||||||

| Principal activities and products | € m | € m | € m | € m | € m | € m | € m | € m | ||||||||||||||||||||||||||||

|

Continuing operations |

||||||||||||||||||||||||||||||||||||

|

Cement, lime and cement products |

1,222 | 2,646 | - | 3,868 | 810 | 2,506 | - | 3,316 | ||||||||||||||||||||||||||||

|

Aggregates, asphalt and readymixed products |

5,046 | 3,061 | - | 8,107 | 4,330 | 2,919 | - | 7,249 | ||||||||||||||||||||||||||||

|

Construction contract activities* |

4,117 | 1,609 | 165 | 5,891 | 3,811 | 1,542 | 240 | 5,593 | ||||||||||||||||||||||||||||

|

Architectural products |

- | 955 | 2,664 | 3,619 | - | 903 | 2,597 | 3,500 | ||||||||||||||||||||||||||||

|

Infrastructure products |

- | 223 | 1,239 | 1,462 | - | 172 | 1,080 | 1,252 | ||||||||||||||||||||||||||||

|

Construction accessories |

- | - | 590 | 590 | - | - | 593 | 593 | ||||||||||||||||||||||||||||

| Architectural glass and glazing systems and wholesale hardware distribution | - | - | 1,592 | 1,592 | - | - | 1,431 | 1,431 | ||||||||||||||||||||||||||||

|

DIY |

- | - | - | - | - | - | 307 | 307 | ||||||||||||||||||||||||||||

|

Total Group from continuing operations |

10,385 | 8,494 | 6,250 | 25,129 | 8,951 | 8,042 | 6,248 | 23,241 | ||||||||||||||||||||||||||||

|

Discontinued operations |

||||||||||||||||||||||||||||||||||||

| Exterior and interior products - Americas Distribution | - | 7 | ||||||||||||||||||||||||||||||||||

| General Builders Merchants, DIY Germany and Sanitary, Heating & Plumbing - Europe Distribution | 3,177 | 3,549 | ||||||||||||||||||||||||||||||||||

|

Total Group |

28,306 | 26,797 | ||||||||||||||||||||||||||||||||||

| (iii) |

Americas Materials and Europe Materials both operate vertically integrated businesses, which are founded in resource-backed cement and aggregates assets and which support the manufacture and supply of aggregates, asphalt, cement, readymixed and precast concrete and landscaping products. Accordingly, for the purpose of disaggregation of revenue we have included certain products together, as this is how management review and evaluate this business line. |

|

* Revenue principally recognised over time. Construction contracts are generally completed within the same financial reporting year. |

Table of Contents

|

CRH ANNUAL REPORT AND FORM 20-F | 2019 |

147 |

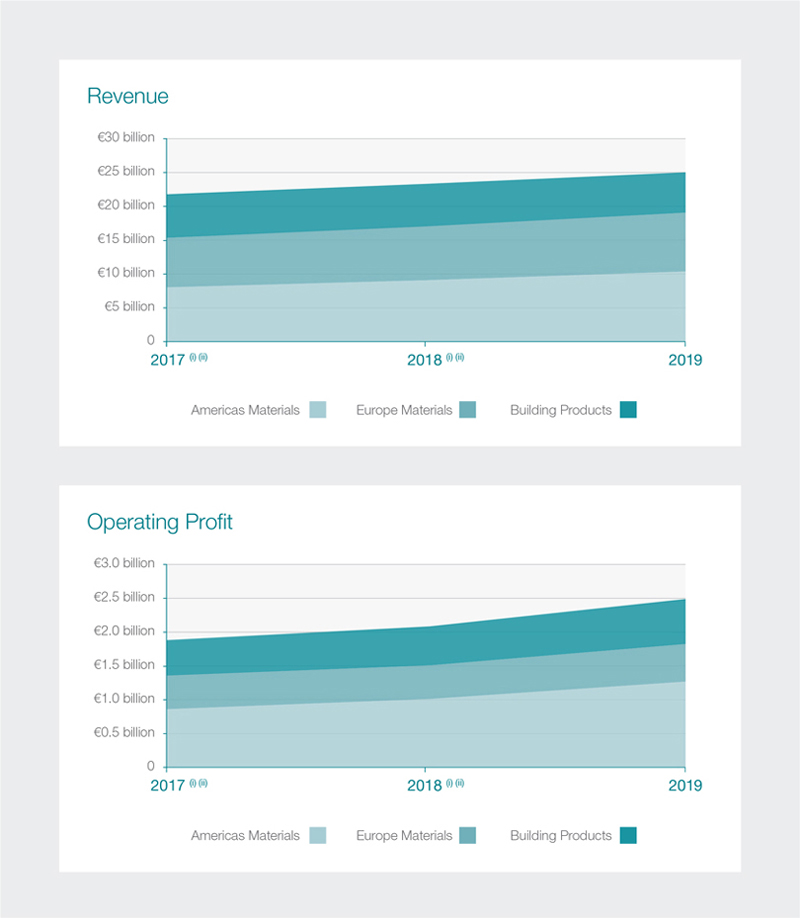

2. Segment Information

|

* EBITDA is defined as earnings before interest, taxes, depreciation, amortisation, asset impairment charges, profit on disposals and the Group’s share of equity accounted investments’ profit after tax. |

Table of Contents

|

148 |

CRH ANNUAL REPORT AND FORM 20-F | 2019 |

2. Segment Information - continued

A. Operating segments disclosures - Consolidated Income Statement data

| Year ended 31 December | ||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Revenue |

Group EBITDA

(as defined)* |

Depreciation,

amortisation and impairment |

Group

operating profit |

|||||||||||||||||||||||||||||||||||||||||||||||||||

|

2019

€ m |

2018

€ m |

2017

€ m |

2019

€ m |

2018

€ m |

2017

€ m |

2019

€ m |

2018

€ m |

2017

€ m |

2019

€ m |

2018

€ m |

2017

€ m |

|||||||||||||||||||||||||||||||||||||||||||

|

Continuing operations |

||||||||||||||||||||||||||||||||||||||||||||||||||||||

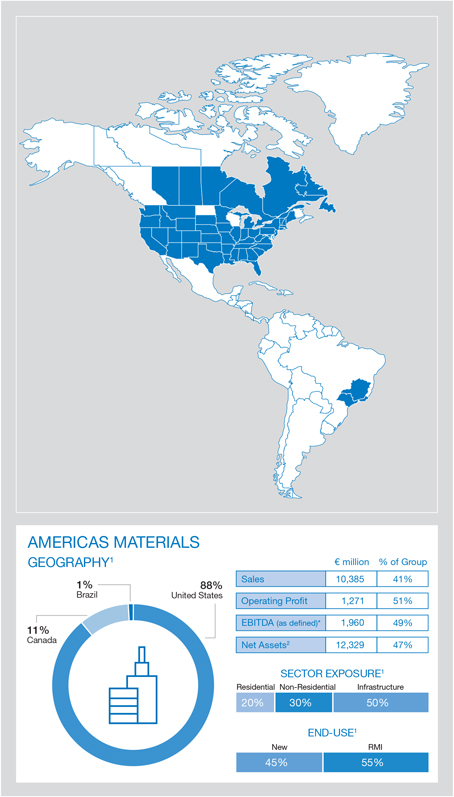

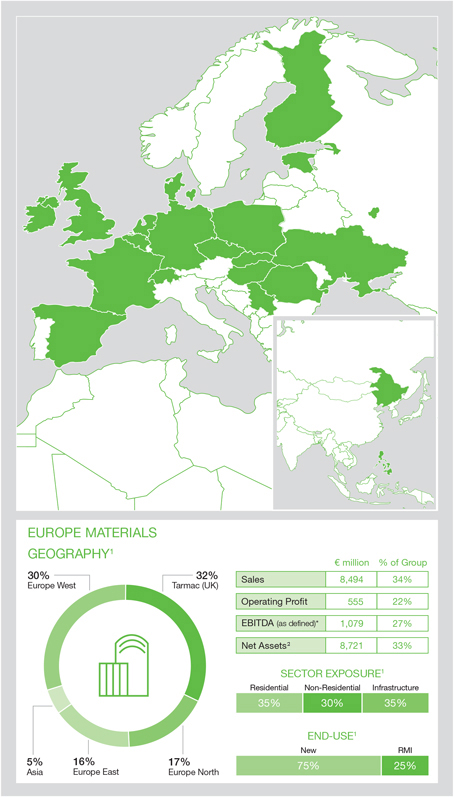

|

Americas Materials |

10,385 | 8,951 | 7,970 | 1,960 | 1,493 | 1,270 | 689 | 484 | 412 | 1,271 | 1,009 | 858 | ||||||||||||||||||||||||||||||||||||||||||

|

Europe Materials |

8,494 | 8,042 | 7,338 | 1,079 | 936 | 891 | 524 | 449 | 398 | 555 | 487 | 493 | ||||||||||||||||||||||||||||||||||||||||||

|

Building Products |

6,250 | 6,248 | 6,345 | 961 | 787 | 769 | 293 | 212 | 193 | 668 | 575 | 576 | ||||||||||||||||||||||||||||||||||||||||||

|

Total Group from continuing operations |

25,129 | 23,241 | 21,653 | 4,000 | 3,216 | 2,930 | 1,506 | 1,145 | 1,003 | 2,494 | 2,071 | 1,927 | ||||||||||||||||||||||||||||||||||||||||||

|

Discontinued operations |

||||||||||||||||||||||||||||||||||||||||||||||||||||||

|

Americas Distribution |

- | 7 | 2,343 | - | (5) | 164 | - | - | 21 | - | (5) | 143 | ||||||||||||||||||||||||||||||||||||||||||

|

Europe Distribution |

3,177 | 3,549 | 3,567 | 200 | 149 | 216 | 99 | 43 | 48 | 101 | 106 | 168 | ||||||||||||||||||||||||||||||||||||||||||

|

Total Group |

28,306 | 26,797 | 27,563 | 4,200 | 3,360 | 3,310 | 1,605 | 1,188 | 1,072 | 2,595 | 2,172 | 2,238 | ||||||||||||||||||||||||||||||||||||||||||

|

Group operating profit from continuing operations |

|

2,494 | 2,071 | 1,927 | ||||||||||||||||||||||||||||||||||||||||||||||||||

|

(Loss)/profit on disposals (i) |

(1) | (27) | 54 | |||||||||||||||||||||||||||||||||||||||||||||||||||

|

Finance costs less income |

(326) | (305) | (289) | |||||||||||||||||||||||||||||||||||||||||||||||||||

|

Other financial expense |

(112) | (46) | (59) | |||||||||||||||||||||||||||||||||||||||||||||||||||

|

Share of equity accounted investments’ profit (ii) |

|

60 | 48 | 52 | ||||||||||||||||||||||||||||||||||||||||||||||||||

|

Profit before tax from continuing operations |

|

2,115 | 1,741 | 1,685 | ||||||||||||||||||||||||||||||||||||||||||||||||||

|

(i) (Loss)/profit on

disposals (note 6) |

(ii) Share of equity

accounted investments’ profit (note 11) |

|||||||||||||||||||||||||||||||||||||||||

|

Americas Materials |

2 | 44 | 29 | 38 | 25 | 32 | ||||||||||||||||||||||||||||||||||||

|

Europe Materials |

(131) | 7 | 19 | 13 | 18 | 18 | ||||||||||||||||||||||||||||||||||||

|

Building Products |

128 | (78) | 6 | 9 | 5 | 2 | ||||||||||||||||||||||||||||||||||||

|

Total Group from continuing operations |

(1) | (27) | 54 | 60 | 48 | 52 | ||||||||||||||||||||||||||||||||||||

|

* EBITDA is defined as earnings before interest, taxes, depreciation, amortisation, asset impairment charges, profit on disposals and the Group’s share of equity accounted investments’ profit after tax. |

Table of Contents

|

CRH ANNUAL REPORT AND FORM 20-F | 2019 |

149 |

Table of Contents

|

150 |

CRH ANNUAL REPORT AND FORM 20-F | 2019 |

2. Segment Information - continued

D. Information about geographical areas

The non-current assets (as defined in IFRS 8) attributable to the country of domicile and all foreign countries of operation, for which revenue exceeds 10% of total external Group revenue, are set out below.

| As at 31 December | ||||||||

| Non-current assets* | ||||||||

| 2019 | 2018 | |||||||

| € m | € m | |||||||

|

Republic of Ireland (country of domicile) |

506 | 495 | ||||||

|

United Kingdom |

2,772 | 2,461 | ||||||

|

United States |

14,259 | 12,925 | ||||||

|

Other |

9,011 | 9,476 | ||||||

|

Total Group |

26,548 | 25,357 | ||||||

3. Assets Held for Sale and Discontinued Operations

A. Profit on disposal of discontinued operations

In October 2019, the Group completed the divestment of its Europe Distribution business, formerly part of our Building Products segment. With the exception of our Europe Distribution business, no other businesses divested in 2019 are considered to be either separate major lines of business or geographical areas of operation and therefore do not constitute discontinued operations as defined in IFRS 5 Non-Current Assets Held for Sale and Discontinued Operations .

In January 2018, the Group completed the divestment of its 100% holding in Allied Building Products, the trading name of our former Americas Distribution segment, which was considered a discontinued operation in 2018 and was classified accordingly.

Assets and liabilities that met the IFRS 5 criteria at 31 December 2019 have not been separately disclosed as held for sale as they were not considered material in the context of the Group.

The table overleaf sets out the proceeds and related profit recognised on divestment which is included in profit after tax for the financial year from discontinued operations.

|

* Non-current assets comprise property, plant and equipment, intangible assets and investments accounted for using the equity method. |

Table of Contents

|

CRH ANNUAL REPORT AND FORM 20-F | 2019 |

151 |

|

* EBITDA is defined as earnings before interest, taxes, depreciation, amortisation, asset impairment charges, profit on disposals and the Group’s share of equity accounted investments’ profit after tax. |

Table of Contents

|

152 |

CRH ANNUAL REPORT AND FORM 20-F | 2019 |

4. Cost Analysis

Continuing operations

|

2019 € m |

2018 € m |

2017 € m |

||||||||||

| Cost of sales analysis | ||||||||||||

|

Raw materials and goods for resale |

5,216 | 5,058 | 4,785 | |||||||||

|

Employment costs (note 7) |

3,467 | 3,155 | 2,869 | |||||||||

|

Energy conversion costs |

1,307 | 1,222 | 1,004 | |||||||||

|

Repairs and maintenance |

980 | 882 | 811 | |||||||||

|

Depreciation, amortisation and impairment (i) |

1,225 | 939 | 830 | |||||||||

|

Change in inventory |

(62) | (179) | (117) | |||||||||

|

Other production expenses (primarily sub-contractor costs) |

4,713 | 4,495 | 4,093 | |||||||||

|

Total |

16,846 | 15,572 | 14,275 | |||||||||

|

Operating costs analysis |

||||||||||||

|

Selling and distribution costs |

4,062 | 3,822 | 3,561 | |||||||||

|

Administrative expenses |

1,727 | 1,776 | 1,890 | |||||||||

|

Total |

5,789 | 5,598 | 5,451 | |||||||||

|

(i) Depreciation, amortisation and impairment analysis |

| Cost of sales | Operating costs | Total | ||||||||||||||||||||||||||||||||||||||||||

|

2019 € m |

2018 € m |

2017 € m |

2019 € m |

2018 € m |

2017 € m |

2019 € m |

2018 € m |

2017 € m |

||||||||||||||||||||||||||||||||||||

|

Depreciation and depletion (note 15, 22) |

1,219 | 903 | 830 | 223 | 127 | 121 | 1,442 | 1,030 | 951 | |||||||||||||||||||||||||||||||||||

|

Amortisation of intangible assets (note 16) |

- | - | - | 57 | 59 | 52 | 57 | 59 | 52 | |||||||||||||||||||||||||||||||||||

|

Impairment of property, plant and equipment (note 15) |

6 | 36 | - | 1 | - | - | 7 | 36 | - | |||||||||||||||||||||||||||||||||||

|

Impairment of intangible assets (note 16) |

- | - | - | - | 20 | - | - | 20 | - | |||||||||||||||||||||||||||||||||||

|

Total |

1,225 | 939 | 830 | 281 | 206 | 173 | 1,506 | 1,145 | 1,003 | |||||||||||||||||||||||||||||||||||

Table of Contents

|

CRH ANNUAL REPORT AND FORM 20-F | 2019 |

153 |

5. Auditor’s Remuneration

Continuing operations

Table of Contents

|

154 |

CRH ANNUAL REPORT AND FORM 20-F | 2019 |

6. Business and Non-Current Asset Disposals

| Business disposals |

Disposal of other

non-current assets |

Total |

||||||||||||||||||||||||||||||||||||||||||

|

2019

€ m |

2018

€ m |

2017

€ m |

2019

€ m |

2018

€ m |

2017

€ m |

2019

€ m |

2018

€ m |

2017

€ m |

||||||||||||||||||||||||||||||||||||

|

Continuing operations |

||||||||||||||||||||||||||||||||||||||||||||

| Assets/(liabilities) disposed of at net carrying amount: | ||||||||||||||||||||||||||||||||||||||||||||

|

- non-current assets |

596 | 622 | 47 | 140 | 56 | 78 | 736 | 678 | 125 | |||||||||||||||||||||||||||||||||||

|

- cash and cash equivalents |

45 | 60 | 11 | - | - | - | 45 | 60 | 11 | |||||||||||||||||||||||||||||||||||

|

- working capital and provisions |

83 | 132 | 29 | - | - | - | 83 | 132 | 29 | |||||||||||||||||||||||||||||||||||

|

- current tax |

(1) | (2) | - | - | - | - | (1) | (2) | - | |||||||||||||||||||||||||||||||||||

|

- lease liabilities |

(48) | - | - | (29) | - | - | (77) | - | - | |||||||||||||||||||||||||||||||||||

|

- deferred tax |

(3) | (2) | 2 | - | - | - | (3) | (2) | 2 | |||||||||||||||||||||||||||||||||||

|

- retirement benefit obligations |

(2) | (6) | - | - | - | - | (2) | (6) | - | |||||||||||||||||||||||||||||||||||

|

Net assets disposed |

670 | 804 | 89 | 111 | 56 | 78 | 781 | 860 | 167 | |||||||||||||||||||||||||||||||||||

| Reclassification of currency translation effects on disposal | 66 | 15 | 9 | - | - | - | 66 | 15 | 9 | |||||||||||||||||||||||||||||||||||

|

Total |

736 | 819 | 98 | 111 | 56 | 78 | 847 | 875 | 176 | |||||||||||||||||||||||||||||||||||

|

Proceeds from disposals (net of disposal costs) |

699 | 697 | 99 | 147 | 100 | 131 | 846 | 797 | 230 | |||||||||||||||||||||||||||||||||||

|

Asset exchange (note 32) |

- | 12 | - | - | - | - | - | 12 | - | |||||||||||||||||||||||||||||||||||

|

Profit on step acquisition (note 32) |

- | 39 | - | - | - | - | - | 39 | - | |||||||||||||||||||||||||||||||||||

| (Loss)/profit on disposals from continuing operations | (37) | (71) | 1 | 36 | 44 | 53 | (1) | (27) | 54 | |||||||||||||||||||||||||||||||||||

|

Discontinued operations |

||||||||||||||||||||||||||||||||||||||||||||

| Profit on disposals from discontinued operations (note 3) | 224 | 1,563 | - | 3 | 3 | 5 | 227 | 1,566 | 5 | |||||||||||||||||||||||||||||||||||

|

Total Group profit on disposals |

187 | 1,492 | 1 | 39 | 47 | 58 | 226 | 1,539 | 59 | |||||||||||||||||||||||||||||||||||

|

Net cash inflow arising on disposal |

||||||||||||||||||||||||||||||||||||||||||||

|

Continuing operations |

||||||||||||||||||||||||||||||||||||||||||||

| Proceeds from disposals from continuing operations | 699 | 697 | 99 | 147 | 100 | 131 | 846 | 797 | 230 | |||||||||||||||||||||||||||||||||||

|

Less: cash and cash equivalents disposed |

(45) | (60) | (11) | - | - | - | (45) | (60) | (11) | |||||||||||||||||||||||||||||||||||

| Less: deferred proceeds arising on disposal (note 21) (i) | (269) | (10) | (3) | - | - | - | (269) | (10) | (3) | |||||||||||||||||||||||||||||||||||

| Less: investment and loan to associate in lieu of cash proceeds (note 17) (ii) | - | (85) | - | - | - | - | - | (85) | - | |||||||||||||||||||||||||||||||||||

| Net cash inflow arising on disposal from continuing operations | 385 | 542 | 85 | 147 | 100 | 131 | 532 | 642 | 216 | |||||||||||||||||||||||||||||||||||

|

Discontinued operations |

||||||||||||||||||||||||||||||||||||||||||||

| Net cash inflow arising on disposal from discontinued operations (note 3) | 1,563 | 2,361 | - | 1 | 6 | 6 | 1,564 | 2,367 | 6 | |||||||||||||||||||||||||||||||||||

|

Total Group net cash inflow arising on disposal |

1,948 | 2,903 | 85 | 148 | 106 | 137 | 2,096 | 3,009 | 222 | |||||||||||||||||||||||||||||||||||

| (i) |

On 31 December, CRH completed the sale of the Group’s 50% stake in its joint venture in India, MHIL for deferred proceeds of € 0.3 billion which will be received in several agreed tranches. |

|

For the purposes of compliance with Indian law requirements, CRH is obliged to retain a minority shareholding and associated minority board representation in MHIL both of which will further reduce as the tranches are completed. The Group no longer has any rights to share in the profit/loss of MHIL or to receive any dividends. CRH has determined that MHIL has ceased to be a joint venture or an associate as the Group is no longer exposed to variability of returns from the performance of MHIL and does not have significant influence (as defined under IAS 28 Interests in Associates and Joint Ventures ) over MHIL. With the other partners acting in concert to exercise control, CRH effectively retains only protective voting rights in defined limited circumstances. Accordingly, the Group has discontinued the use of the equity method of accounting for its interest in MHIL from 31 December 2019. The fair value of the retained interest in MHIL is recorded as a financial asset within Other Receivables as it represents a contractual right to receive cash. |

| (ii) |