|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Table of Contents

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 10-K

| x | Annual Report Pursuant to Section 13 or 15(d) of the Securities Exchange Act of 1934 |

For the fiscal year ended February 28, 2013

OR

| ¨ | Transition Report Pursuant to Section 13 or 15(d) of the Securities Exchange Act of 1934 |

For the transition period from to

Commission File Number 1-5807

ENNIS, INC.

(Exact Name of Registrant as Specified in Its Charter)

| Texas | 75-0256410 | |

|

(State or Other Jurisdiction of Incorporation or Organization) |

(I.R.S. Employer Identification No.) |

|

|

2441 Presidential Pkwy., Midlothian, Texas |

76065 | |

| (Address of Principal Executive Offices) | (Zip code) | |

(972) 775-9801

(Registrant’s Telephone Number, Including Area Code)

Securities registered pursuant to Section 12(b) of the Act:

|

Title of each class |

Name of each exchange on which registered |

|

| Common Stock, par value $2.50 per share | New York Stock Exchange |

Securities registered pursuant to Section 12(g) of the Act: None

Indicate by check mark if the Registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. Yes ¨ No x

Indicate by check mark if the Registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Act. Yes ¨ No x

Indicate by check mark whether the Registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the Registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes x No ¨

Indicate by check mark whether the registrant has submitted electronically and posted on its corporate Web site, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files). Yes x No ¨

Indicate by check mark if disclosure of delinquent filers pursuant to Item 405 of Regulation S-K is not contained herein, and will not be contained, to the best of Registrant’s knowledge, in definitive proxy or information statements incorporated by reference in Part III of this Form 10-K or any amendment to this Form 10-K. ¨

Indicate by check mark whether the Registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer or a smaller reporting company. See the definitions of “large accelerated filer,” “accelerated filer” and “smaller reporting company” in Rule 12b-2 of the Exchange Act. (Check one).

| Large accelerated Filer | ¨ | Accelerated filer | x | |||

| Non-accelerated filer | ¨ (Do not check if a smaller reporting company) | Smaller reporting company | ¨ | |||

Indicate by check mark whether the Registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act). Yes ¨ No x

The aggregate market value of voting stock held by non-affiliates of the Registrant as of August 31, 2012 was approximately $368.0 million. Shares of voting stock held by executive officers, directors and holders of more than 10% of the outstanding voting stock have been excluded from this calculation because such persons may be deemed to be affiliates. Exclusion of such shares should not be construed to indicate that any of such persons possesses the power, direct or indirect, to control the Registrant, or that any such person is controlled by or under common control with the Registrant.

The number of shares of the Registrant’s Common Stock, par value $2.50, outstanding at April 30, 2013 was 26,160,918.

DOCUMENTS INCORPORATED BY REFERENCE

Portions of the Registrant’s Proxy Statement for the 2013 Annual Meeting of Shareholders are incorporated by reference into Part III of this Report.

Table of Contents

ENNIS, INC. AND SUBSIDIARIES

FORM 10-K

FOR THE PERIOD ENDED FEBRUARY 28, 2013

2

Table of Contents

Cautionary Statements Regarding Forward-Looking Statements

All of the statements in this Annual Report on Form 10-K, other than historical facts, are forward-looking statements, including, without limitation, the statements made in the “Management’s Discussion and Analysis of Financial Condition and Results of Operations,” particularly under the caption “Overview.” As a general matter, forward-looking statements are those focused upon anticipated events or trends, expectations, and beliefs relating to matters that are not historical in nature. The words “could,” “should,” “feel,” “anticipate,” “aim,” “preliminary,” “expect,” “believe,” “estimate,” “intend,” “intent,” “plan,” “will,” “foresee,” “project,” “forecast,” or the negative thereof or variations thereon, and similar expressions identify forward-looking statements.

The Private Securities Litigation Reform Act of 1995 provides a “safe harbor” for these forward-looking statements. In order to comply with the terms of the safe harbor, Ennis, Inc. notes that forward-looking statements are subject to known and unknown risks, uncertainties and other factors relating to its operations and business environment, all of which are difficult to predict and many of which are beyond the control of Ennis, Inc. These known and unknown risks, uncertainties and other factors could cause actual results to differ materially from those matters expressed in, anticipated by or implied by such forward-looking statements.

These statements reflect the current views and assumptions of management with respect to future events. Ennis, Inc. does not undertake, and hereby disclaims, any duty to update these forward-looking statements, even though its situation and circumstances may change in the future. Readers are cautioned not to place undue reliance on forward-looking statements, which speak only as of the date of this report. The inclusion of any statement in this report does not constitute an admission by Ennis, Inc. or any other person that the events or circumstances described in such statement are material.

| ITEM 1. | BUSINESS |

Overview

Ennis, Inc. (formerly Ennis Business Forms, Inc.) was organized under the laws of Texas in 1909. Ennis, Inc. and its subsidiaries (collectively known as the “Company,” “Registrant,” “Ennis,” “we,” “us,” or “our”) print and manufacture a broad line of business forms and other business products (the “Print Segment”) and also manufacture a line of activewear (the “Apparel Segment”) for distribution throughout North America. The Print Segment distributes business products and forms throughout the United States primarily through independent dealers. This distributor channel encompasses print distributors, stationers, quick printers, computer software developers, and advertising agencies, among others. The Apparel Segment produces and sells activewear, including t-shirts, fleece goods and other wearables. Distribution of our activewear throughout the United States, Canada and Mexico is primarily through sales representatives. The distributor channel encompasses activewear wholesalers and screen printers. We offer a great selection of high-quality activewear apparel and hats with a wide variety of styles and colors in sizes ranging from toddler to 6XL. The apparel line features a wide variety of tees, fleece and shorts.

On February 10, 2012, we acquired from Cenveo Corporation (“Cenveo”) and its subsidiaries, Cenveo Resale Ohio, LLC and Printegra Corporation, certain assets of Cenveo’s document business, including the manufacturing facilities branded under the names PrintXcel and Printegra for $40.0 million plus the assumption of certain trade liabilities. The cash portion of the purchase was funded by borrowing under our line of credit facility. The original purchase price of $40.0 million was subsequently reduced to $36.2 million as a result of an adjustment made during the quarter ended August 31, 2012 to the acquisition date inventory balances and pursuant to the terms of the purchase agreement. The combined sales of the purchased operations were $74.4 million during the twelve month period ended December 31, 2011. The acquired assets are being operated under their respective trade names of PrintXcel and Printegra. The acquired assets expanded our pressure seal and high color commercial print capabilities, as well as our business check product lines, which are being sold through our independent distributor network.

On September 30, 2011, we purchased all of the outstanding equity of PrintGraphics, LLC (“PrintGraphics”), as well as associated land and buildings for an aggregate amount of $6.0 million in cash. PrintGraphics has locations in Vandalia, Ohio and Nevada, Iowa. The sales of the purchased operations were $15.1 million during the twelve month period ended December 31, 2010. The acquisition of PrintGraphics continued our strategy of targeted growth in the Print Segment of products to further service our existing customer base.

3

Table of Contents

Business Segment Overview

We are one of the largest providers of business forms to independent distributors in the United States and are also one of the largest providers of blank t-shirts in North America to the activewear market. We operate in two reportable segments: Print and Apparel. For additional financial information concerning segment reporting, please see Note 14 of the Notes to the Consolidated Financial Statements beginning on page F-26 included elsewhere herein, which information is incorporated herein by reference.

Print Segment

The Print Segment, which represented 63%, 54%, and 50% of our consolidated net sales for the fiscal years ended February 28, 2013, February 29, 2012, and February 28, 2011, respectively, is in the business of manufacturing, designing and selling business forms and other printed business products primarily to distributors located in the United States. The Print Segment operates 49 manufacturing locations throughout the United States in 19 strategically located states. Approximately 96% of the business products manufactured by the Print Segment are custom and semi-custom products, constructed in a wide variety of sizes, colors, number of parts and quantities on an individual job basis depending upon the customers’ specifications.

The products sold include snap sets, continuous forms, laser cut sheets, tags, labels, envelopes, integrated products, jumbo rolls and pressure sensitive products in short, medium and long runs under the following labels: Ennis ® , Royal Business Forms ® , Block Graphics ® , Specialized Printed Forms ® , 360º Custom Labels SM , Enfusion ® , Uncompromised Check Solutions ® , VersaSeal ® , Witt Printing ® , B&D Litho ® , Genforms ® , PrintGraphics SM , Calibrated Forms ® , PrintXcel™ and Printegra ® . The Print Segment also sells the Adams-McClure ® brand (which provides Point of Purchase advertising for large franchise and fast food chains as well as kitting and fulfillment); the Admore ® brand (which provides presentation folders and document folders); Ennis Tag & Label SM (which provides tags and labels, promotional products and advertising concept products); Atlas Tag & Label ® (which provides tags and labels); Trade Envelopes ® and Block Graphics ® (which provide custom and imprinted envelopes); and Northstar ® and General Financial Supply ® (which provide financial and security documents).

The Print Segment sells predominantly through private printers and independent distributors. Northstar also sells direct to a small number of customers, generally large banking organizations (where a distributor is not acceptable or available to the end-user), as does Adams-McClure, where sales are generally through advertising agencies.

The printing industry generally sells its products either through sales made predominantly to end users, a market dominated by a few large manufacturers, such as R.R. Donnelley, Standard Register, and Cenveo, or, like the Company, through a variety of independent distributors and distributor groups. While it is not possible, because of the lack of adequate public statistical information, to determine the Company’s share of the total business products market, management believes the Company is one of the largest producers of business forms in the United States distributing primarily through independent dealers and that its business forms offering is more diversified than that of most companies in the business forms industry.

There are a number of competitors that operate in this segment, ranging in size from single employee-owner operations to multi-plant organizations. We believe our strategic locations and buying power permit us to compete on a favorable basis within the distributor market on competitive factors, such as service, quality, and price.

Distribution of business forms and other business products throughout the United States is primarily done through independent dealers, including business forms distributors, stationers, printers, computer software developers, and advertising agencies.

Raw materials of the Print Segment principally consist of a wide variety of weights, widths, colors, sizes, and qualities of paper for business products purchased from a number of major suppliers at prevailing market prices.

Business products usage in the printing industry is generally not seasonal. General economic conditions and contraction of the traditional business forms industry are the predominant factor in quarterly volume fluctuations.

Apparel Segment

The Apparel Segment represented 37%, 46%, and 50% of our consolidated net sales for the fiscal years ended February 28, 2013, February 29, 2012, and February 28, 2011, respectively, and operates under the name of Alstyle Apparel (“Alstyle”). Alstyle markets high quality knitted activewear (including t-shirts, tank tops and fleece) across

4

Table of Contents

all market segments. The main products of Alstyle are standardized shirts manufactured in a variety of sizes and colors. Approximately 98.3% of Alstyle’s revenues are derived from t-shirt sales, of which 90.8% are domestic sales. Alstyle’s branded product lines are sold mainly under the AAA ® and Murina ® brands.

Effective July 2011, Alstyle began operations in an owned manufacturing facility located in Agua Prieta, Mexico. Previously Alstyle operated in a leased manufacturing facility located in Anaheim, CA. Alstyle has three cut and sew facilities in Mexico (Agua Prieta, Ensenada and Hermosillo). In addition to its own cut and sew facilities, Alstyle may also use outsourced manufacturers from time to time to supplement a portion of its cut and sew needs. After sewing and packaging is completed, the product is shipped to one of Alstyle’s nine distribution centers located across the United States, Canada, and Mexico.

Alstyle utilizes a customer-focused internal sales team comprised of twenty-two sales representatives assigned to specific geographic territories in the United States, Canada, and Mexico. Sales representatives are assigned performance objectives for their respective territories and are provided financial incentives for achievement of their target objectives. Sales representatives are responsible for developing business with large accounts and spend a majority of their time in the field.

Alstyle employs a staff of customer service representatives that handle call-in orders from smaller customers. Sales personnel sell directly to Alstyle’s customer base, which consists primarily of screen printers, embellishers, retailers, and mass marketers.

A majority of Alstyle’s sales are branded products, with the remainder being customer private label products. Generally, sales to screen printers and mass marketers are driven by price and the availability of products, which directly impacts our inventory level requirements. Sales in the private label business are characterized by slightly higher customer loyalty.

Alstyle’s most popular styles are produced based on demand management forecasts to permit quick shipment and to level production schedules. Alstyle offers same-day shipping and uses third-party carriers to ship products to its customers.

Alstyle’s sales are seasonal, with sales in the first and second fiscal quarters generally being the highest. The apparel industry is characterized by rapid shifts in fashion, consumer demand and competitive pressures, resulting in both price and demand volatility. However, the imprinted activewear market to which Alstyle sells is generally “event” driven. Blank t-shirts can be thought of as “walking billboards” promoting movies, concerts, sports teams, and “image” brands. Still, the demand for any particular product varies from time to time based largely upon changes in consumer preferences and general economic conditions affecting the apparel industry.

The apparel industry is comprised of numerous companies who manufacture and sell a wide range of products. Alstyle is primarily involved in the activewear market and produces t-shirts and outsources such products as fleece, hats, shorts, pants and other such activewear apparel from China, Thailand, Pakistan, and other foreign sources to sell to its customers through its sales representatives. Alstyle competes with many branded and private label manufacturers of knit apparel in the United States, Canada, and Mexico, some of which are larger in size and have greater financial resources than Alstyle. Alstyle competes on the basis of price, quality, service, and delivery. Alstyle’s strategy is to provide the best value to its customers by delivering a consistent, high-quality product at a competitive price. Alstyle’s competitive disadvantage is that its brand name, Alstyle Apparel, is not as well known as the brand names of its largest competitors, such as Gildan, Delta, Hanes, and Russell. While it is not possible to calculate precisely, because of the lack of adequate public statistical information, management believes that Alstyle is one of the top five providers of blank t-shirts in North America.

Raw materials of the Apparel Segment principally consist of cotton and polyester yarn purchased from a number of major suppliers at prevailing market prices, although we purchase 45% of our cotton and yarn from one supplier.

Patents, Licenses, Franchises and Concessions

We acquired a patent for our VersaSeal product in the acquisition of assets from Cenveo. We do not have any significant patents, licenses, franchises, or concessions.

5

Table of Contents

Intellectual Property

We market our products under a number of trademarks and tradenames. We have registered trademarks in the United States for Ennis®, EnnisOnline SM , Alstyle®, A Alstyle Apparel®, AA Alstyle Apparel & Activewear®, AAA Alstyle Apparel & Activewear®, B&D Litho of AZ®, B&D Litho®, ACR®, Block Graphics®, Classic by Alstyle Apparel®, Enfusion®, Murina®, 360º Custom Labels SM , Admore®, CashManagementSupply.com SM , Securestar®, Northstar®, MICRLink®, MICR Connection TM , Ennisstores.com TM , General Financial Supply®, Calibrated Forms®, PrintXcel™, Printegra®, Trade Envelopes®, Witt Printing®, Genforms®, Royal Business Forms®, Crabar/GBF SM , BF&S SM, Adams McClure®, Advertising Concepts TM , ColorWorx®, Atlas Tag & Label®, Printgraphics SM , Uncompromised Check Solutions®, VersaSeal®, Star Award Ribbon®, Canu SM , Platinum Canoe SM , EOSTouchpoint TM , and Printersmall.com SM , and variations of these brands as well as other trademarks. We have similar trademark registrations internationally. The protection of our trademarks is important to our business. We believe that our registered and common law trademarks have significant value and these trademarks are instrumental to our ability to create and sustain demand for our products.

Customers

No single customer accounts for as much as five percent of our consolidated net sales.

Backlog

At February 28, 2013, our backlog of orders was approximately $19.0 million as compared to approximately $23.3 million at February 29, 2012. The decline in our backlog at February 28, 2013 related to the decline in our Apparel backlog. See Item 7 – “Management’s Discussion and Analysis of Financial Condition and Results of Operations” section of this report on factors impacting our Apparel sales.

Research and Development

While we seek new products to sell through our distribution channel, there have been no material amounts spent on research and development in the fiscal year ended February 28, 2013.

Environment

We are subject to various federal, state, and local environmental laws and regulations concerning, among other things, wastewater discharges, air emissions and solid waste disposal. Our manufacturing processes do not emit substantial foreign substances into the environment. We do not believe that our compliance with federal, state, or local statutes or regulations relating to the protection of the environment has any material effect upon capital expenditures, earnings or our competitive position. There can be no assurance, however, that future changes in federal, state, or local regulations, interpretations of existing regulations or the discovery of currently unknown problems or conditions will not require substantial additional expenditures. Similarly, the extent of our liability, if any, for past failures to comply with laws, regulations, and permits applicable to our operations cannot be determined.

Employees

At February 28, 2013, we had approximately 5,818 employees. Approximately 3,519 of the employees are in Mexico, and approximately 22 employees are in Canada. Of the domestic employees, approximately 318 are represented by labor unions under collective bargaining agreements, which are subject to periodic renegotiations. Two unions represent all of our hourly employees in Mexico with contracts expiring at various times.

Available Information

We make our annual report on Form 10-K, quarterly reports on Form 10-Q, current reports on Form 8-K, and amendments to reports filed or furnished pursuant to Section 13(a) or 15(d) of the Securities and Exchange Act of 1934 available free of charge under the Investors Relations page on our website, www.ennis.com , as soon as reasonably practicable after such reports are electronically filed with, or furnished to, the Securities and Exchange Commission (“SEC”). Information on our website is not included as a part of, or incorporated by reference into, this report. Our SEC filings are also available through the SEC’s website, www.sec.gov . In addition, the public may read and copy any materials we file with the SEC at the SEC’s Public Reference Room at 100 F Street NE, Washington, DC 20549. Information regarding the operation of the Public Reference Room may be obtained by calling the SEC at 1-800-SEC-0330.

6

Table of Contents

| ITEM 1A. | RISK FACTORS |

You should carefully consider the risks described below, as well as the other information included or incorporated by reference in this Annual Report on Form 10-K, before making an investment in our common stock. The risks described below are not the only ones we face in our business. Additional risks and uncertainties not presently known to us or that we currently believe to be immaterial may also impair our business operations. If any of the following risks occur, our business, financial condition or operating results could be materially harmed. In such an event, our common stock could decline in price and you may lose all or part of your investment.

Our results and financial condition are affected by global and local market conditions, and competitors’ pricing strategies, which can adversely affect our sales, margins, and net income.

Our results of operations are substantially affected not only by global economic conditions, but also by local market conditions, and competitors’ pricing strategies, which can vary substantially by market. Unfavorable conditions can depress sales in a given market and may prompt promotional or other actions that adversely affect our margins, constrain our operating flexibility or result in charges. Certain macroeconomic events, such as the recent crisis in the financial markets, could have a more wide-ranging and prolonged impact on the general business environment, which could also adversely affect us. Whether we can manage these risks effectively depends mainly on the following:

| • | Our ability to manage upward pressure on commodity prices and the impact of government actions to manage national economic conditions such as consumer spending, inflation rates and unemployment levels, particularly given the current volatility in the global financial markets; and |

| • | The impact on our margins of labor costs given our labor-intensive business model, the trend toward higher wages in both mature and developing markets and the potential impact of union organizing efforts on day-to-day operations of our manufacturing facilities. |

Declining economic conditions could negatively impact our business.

Our operations are affected by local, national and worldwide economic conditions. The consequences of domestic and international economic uncertainty or instability, volatility in commodity markets, domestic or international policy uncertainty, all of what we have seen of late, and all of which can impact economic activity. This in turn can impact the demand for our products. Instability in the financial markets also may affect our cost of capital and our ability to raise capital, if needed.

The terms and conditions of our credit facility impose certain restrictions on our operations. We may not be able to raise additional capital, if needed, for proposed expansion projects.

The terms and conditions of our credit facility impose certain restrictions on our ability to incur additional debt, make capital expenditures, acquisitions and asset dispositions, as well as imposing other customary covenants, such as requiring a tangible equity level and a ratio of total funded debt to the sum of net earnings plus interest, tax, depreciation and amortization (“EBITDA”). Our ability to comply with the covenants may be affected by events beyond our control, such as distressed and volatile financial markets which could trigger an impairment charge to our recorded long-lived assets. A breach of any of these covenants could result in a default under our credit facility. In the event of a default, the bank could elect to declare the outstanding principal amount of our credit facility, all interest thereon, and all other amounts payable under our credit facility to be immediately due and payable. As of February 28, 2013, we were in compliance with all terms and conditions of our credit facility, which matures on August 18, 2016.

Declining financial market conditions and continued decline in long-term interest rates could adversely impact the funding status of our pension plan.

We maintain a noncontributory defined benefit retirement plan (the “Pension Plan”) covering approximately 9% of our employees. Included in our financial results are Pension Plan costs that are measured using actuarial valuations. The actuarial assumptions used may differ from actual results. In addition, as our Pension Plan assets are invested in marketable securities, severe fluctuations in market values could potentially negatively impact our funding status, recorded pension liability, and future required minimum contribution levels. In addition, declining interest rates in long-term debt instruments over the past several years has continued to put downward pressure on the discount rate used by plan sponsors to determine their pension liabilities. Each 10 basis point drop in the discount rate increases our computed liability by about $800,000. So, just like fluctuations in market values, a continued drop in the discount rate could potentially negatively impact our funded status, recorded pension liability and future contribution levels.

7

Table of Contents

We may be required to write down goodwill and other intangible assets which could cause our financial condition and results of operations to be negatively affected in the future.

When we acquire a business, a portion of the purchase price of the acquisition may be allocated to goodwill and other identifiable intangible assets. The amount of the purchase price which is allocated to goodwill and other intangible assets is the excess of the purchase price over the net identifiable tangible assets acquired. The annual impairment test is based on several factors requiring judgment. A decline in market conditions caused by a recession, protracted recovery there from, or other factors may indicate a potential impairment of goodwill. An impairment test was completed for our fiscal year ended February 28, 2013, and we concluded that no impairment charge was necessary. However, the spread between the carrying cost of our Apparel assets and their indicated fair market value at February 29, 2012 and February 28, 2013 declined from an average spread of 14.8% to 4.8%. While no impairment was indicated at February 28, 2013, continued sale-side pressure due to competitor’s pricing strategies or continued economic instability and/or uncertainty, could result in an impairment charge in the future. And while this charge would be a non-cash charge, it would impact the Company’s reported operating results for the period and its financial position. At February 28, 2013, our goodwill and other intangible assets were approximately $121.8 million and $84.2 million (includes $0.6 million relating to patents included in other long-term assets), respectively.

Digital technologies will continue to erode the demand for our printed business documents.

The increasing sophistication of software, internet technologies, and digital equipment combined with our customers’ general preference, as well as governmental influences, for paperless business environments will continue to reduce the number of traditional printed documents sold. Moreover, the documents that will continue to coexist with software applications will likely contain less value-added print content.

Many of our custom-printed documents help companies control their internal business processes and facilitate the flow of information. These applications will increasingly be conducted over the internet or through other electronic payment systems. The predominant method of our clients’ communication to their customers is by printed information. As their customers become more accepting of internet communications, our clients may increasingly opt for the less costly electronic option, which would reduce our revenue. The pace of these trends is difficult to predict. These factors will tend to reduce the industry-wide demand for printed documents and require us to gain market share to maintain or increase our current level of print-based revenue.

In response to the gradual obsolescence of our standardized forms business, we continue to develop our capability to provide custom and full-color products. If new printing capabilities and new product introductions do not continue to offset the obsolescence of our standardized business forms products, and we aren’t able to increase our market share, our sales and profits will be affected. Decreases in sales of our standardized business forms and products due to obsolescence could also reduce our gross margins. This reduction could in turn adversely impact our profits, unless we are able to offset the reduction through the introduction of new high margin products and services or realize cost savings in other areas.

Our distributors face increased competition from various sources, such as office supply superstores. Increased competition may require us to reduce prices or to offer other incentives in order to enable our distributors to attract new customers and retain existing customers.

Low price, high value office supply chain stores offer standardized business forms, checks and related products. Because of their size, these superstores have the buying power to offer many of these products at competitive prices. These superstores also offer the convenience of “one-stop” shopping for a broad array of office supplies that our distributors do not offer. In addition, superstores have the financial strength to reduce prices or increase promotional discounts to expand market share. This could result in us reducing our prices or offering incentives in order to enable our distributors to attract new customers and retain existing customers, which could reduce our profits.

Technological improvements may reduce our competitive advantage over some of our competitors, which could reduce our profits.

Improvements in the cost and quality of printing technology are enabling some of our competitors to gain access to products of complex design and functionality at competitive costs. Increased competition from these competitors could force us to reduce our prices in order to attract and retain customers, which could reduce our profits.

8

Table of Contents

We could experience labor disputes that could disrupt our business in the future.

As of February 28, 2013, approximately 14% of our domestic employees are represented by labor unions under collective bargaining agreements, which are subject to periodic renegotiations. Two unions represent all of our hourly employees in Mexico. While we feel we have a good working relationship with all of the unions, there can be no assurance that any future labor negotiations will prove successful, which may result in a significant increase in the cost of labor, or may break down and result in the disruption of our business or operations.

We obtain our raw materials from a limited number of suppliers, and any disruption in our relationships with these suppliers, or any substantial increase in the price of raw materials or material shortages could have a material adverse effect on us.

Cotton yarn is the primary raw material used in Alstyle’s manufacturing processes and represents a significant portion of its manufacturing costs. Alstyle acquires its yarn from three major sources that meet stringent quality and on-time delivery requirements. The largest supplier provided 48% of Alstyle’s yarn requirements during the year and has an entire yarn mill dedicated to Alstyle’s production. To maintain our high standard of color control associated with our apparel products, we purchase our dyeing chemicals from limited sources. If Alstyle’s relations with its suppliers are disrupted, Alstyle may not be able to enter into arrangements with substitute suppliers on terms as favorable as its current terms, and our results of operations could be materially adversely affected.

We also purchase our paper products from a limited number of sources, which meet stringent quality and on-time delivery standards under long-term contracts. However, fluctuations in the quality of our paper, unexpected price increases or other factors that relate to our paper products could have a material adverse effect on our operating results.

Both cotton and paper are commodities that are subject to periodic increases or decreases in price, which are sometimes quite significant. There is no effective market to cost-effectively insulate us against unexpected changes in price of paper, and corporate negotiated purchase contracts provide only limited protection against price increases. We generally acquire our cotton yarn under short-term purchase contracts with our suppliers. While we generally do not use derivative instruments, including cotton option contracts, to manage our exposure to movements in cotton market prices, we believe we are competitive with other companies in the United States apparel industry in negotiating the price of cotton. Generally, when cotton or paper prices are increased, we attempt to recover the higher costs by raising the prices of our products to our customers. In the price-competitive marketplaces in which we operate, we may not always be able to pass through any or all of the higher costs. As such, any significant increase in the price of paper or cotton or shortages in the availability of either, could have a material adverse effect on our results of operations.

We face intense competition to gain market share, which may lead some competitors to sell substantial amounts of goods at prices against which we cannot profitably compete.

Demand for Alstyle’s products is dependent on the general demand for shirts and the availability of alternative sources of supply. Alstyle’s strategy in this market environment is to be a low cost producer and to differentiate itself by providing quality service and quality products to its customers. Even if this strategy is successful, its results may be offset by reductions in demand or price declines due to competitors’ pricing strategies. Our Print Segment also faces the risk of our competition following a strategy of selling their products at or below cost in order to cover some amount of fixed costs, especially in distressed economic times.

The apparel industry is heavily influenced by general economic cycles.

The apparel industry is cyclical and dependent upon the overall level of discretionary consumer spending, which changes as regional, domestic and international economic conditions change. These include, but are not limited to, employment levels, energy costs, interest rates, tax rates, personal debt levels, and uncertainty about the future. Any deterioration in general economic conditions that creates uncertainty or alters discretionary consumer spending habits could reduce our sales, increase our costs of goods sold or require us to significantly modify our current business practices, and consequently negatively impact our results of operations.

9

Table of Contents

Our foreign-based apparel manufacturing operations could be subject to unexpected changes in regulatory requirements, tariffs and other market barriers, political and economic instability, social unrest, as well as disruption of services in the countries where it operates, which could negatively impact our operating results.

Alstyle operates manufacturing facilities in Mexico and from time to time sources product manufacturing and purchases from El Salvador, Thailand, India, Pakistan, China and other foreign sources. Alstyle’s foreign operations could be subject to unexpected changes in regulatory requirements, tariffs, and other market barriers, political and economic instability, social unrest in the countries where it operates, as well as utility and other service disruption. The impact of any such events that may occur in the future could subject Alstyle to additional costs or loss of sales, which could adversely affect our operating results. In particular, Alstyle operates its facilities in Mexico pursuant to the “maquiladora” duty-free program established by the Mexican and United States governments. This program enables Alstyle to take advantage of generally lower costs in Mexico, without paying duty on inventory shipped into or out of Mexico. There can be no assurance that the governments of Mexico and the United States will continue the program currently in place or that Alstyle will continue to be able to benefit from this program. The loss of these benefits could have an adverse effect on our business.

In addition, all Alstyle’s knit and dye operations are located in one facility in Agua Prieta, Mexico. Any disruptions in utility or other services required to continue operations that are caused by any of the above factors, as well as others, could have a material adverse effect on the Company’s operational results.

Our apparel products are subject to foreign competition, which in the past have been faced with significant U.S. government import restrictions.

Foreign producers of apparel often have significant labor cost advantages. Given the number of these foreign producers, the substantial elimination of import protections that protect domestic apparel producers could materially adversely affect Alstyle’s business. The extent of import protection afforded to domestic apparel producers has been, and is likely to remain, subject to considerable political considerations.

The North American Free Trade Agreement (NAFTA) became effective on January 1, 1994 and has created a free-trade zone among Canada, Mexico, and the United States. NAFTA contains a rule of origin requirement that products be produced in one of the three countries in order to benefit from the agreement. NAFTA has phased out all trade restrictions and tariffs among the three countries on apparel products competitive with those of Alstyle. Alstyle manufactures all of its products in the Agua Prieta manufacturing plant and performs substantially all of its cutting and sewing in three plants located in Mexico in order to take advantage of the NAFTA benefits. Subsequent repeal or alteration of NAFTA could adversely affect our business.

The Central American Free Trade Agreement (CAFTA) became effective May 28, 2004 and retroactive to January 1, 2004 for textiles and apparel. It creates a free trade zone similar to NAFTA by and between the United States and Central American countries (El Salvador, Honduras, Costa Rica, Nicaragua, and Dominican Republic). Textiles and apparel are duty-free and quota-free immediately if they meet the agreement’s rule of origin, promoting new opportunities for U.S. and Central American fiber, yarn, fabric and apparel manufacturing. The agreement gives duty-free benefits to some apparel made in Central America that contains certain fabrics from NAFTA partners Mexico and Canada. Alstyle did not outsource any of its production to outside contract manufacturers during this fiscal year, and we do not anticipate that alteration or subsequent repeal of CAFTA would have a material effect on our operations.

The World Trade Organization (WTO), a multilateral trade organization, was formed in January 1995 and is the successor to the General Agreement on Tariffs and Trade (GATT). This multilateral trade organization has set forth mechanisms by which world trade in clothing is being progressively liberalized by phasing-out quotas and reducing duties over a period of time that began in January of 1995. As it implements the WTO mechanisms, the United States government is negotiating bilateral trade agreements with developing countries, which are generally exporters of textile and apparel products, that are members of the WTO to get them to reduce their tariffs on imports of textiles and apparel in exchange for reductions by the United States in tariffs on imports of textiles and apparel.

In January 2005, United States import quotas were removed on knitted shirts from China. The elimination of quotas and the reduction of tariffs under the WTO may result in increased imports of certain apparel products into North America. In May 2005, quotas on three categories of clothing imports, including knitted shirts, from China were re-imposed. A reduction of import quotas and tariffs could make Alstyle’s products less competitive against low cost imports from developing countries.

10

Table of Contents

Environmental regulations may impact our future operating results.

We are subject to extensive and changing federal, state and foreign laws and regulations establishing health and environmental quality standards, concerning, among other things, wastewater discharges, air emissions and solid waste disposal, and may be subject to liability or penalties for violations of those standards. We are also subject to laws and regulations governing remediation of contamination at facilities currently or formerly owned or operated by us or to which we have sent hazardous substances or wastes for treatment, recycling or disposal. We may be subject to future liabilities or obligations as a result of new or more stringent interpretations of existing laws and regulations. In addition, we may have liabilities or obligations in the future if we discover any environmental contamination or liability at any of our facilities, or at facilities we may acquire.

Our manufacturing facility in Mexico is subject to certain risks regarding sales growth and cost savings as well as disruption in manufacturing risks.

Our manufacturing facility in Agua Prieta, Mexico was built to capture anticipated future growth and savings in production costs over our cost structure in Anaheim, CA. Should such growth or production savings not materialize, such events may impact our ability to achieve our expected return and/or could negatively impact our production levels, operational results and financial condition. In addition, as our apparel manufacturing through the cut process basically occurs only at our textile facility located at Agua Prieta, Mexico, any disruption in our utility services (i.e., water, electric, gas, etc.) can have a significant impact on our production levels, which depending on length of the disruption could significantly impact our sales and operational profitability.

We are exposed to the risk of non-payment by our customers on a significant amount of our sales.

Our extension of credit involves considerable judgment and is based on an evaluation of each customer’s financial condition and payment history. We monitor our credit risk exposure by periodically obtaining credit reports and updated financials on our customers. We see a heightened amount of bankruptcies by our customers, especially retailers, during economic downturns. While we maintain an allowance for doubtful receivables for potential credit losses based upon our historical trends and other available information, in times of economic turmoil, there is heightened risk that our historical indicators may prove to be inaccurate. The inability to collect on sales to significant customers or a group of customers could have a material adverse effect on our results of operations.

Our business incurs significant freight and transportation costs.

We incur significant freight costs to transport our goods, especially as it relates to our Apparel Segment where we transport yarn from our domestic suppliers to our textile facility in Mexico. The internal freight from the textile to the sewing facilities, as well as the logistic cost of keeping our product in the distribution centers to maintain our product close to the customer and on time to market is also significant. In addition, we incur transportation expenses to ship our products to our customers. Significant increases in the costs of freight and transportation could have a material adverse effect on our results of operations, as there can be no assurance that we could pass these increased costs to our customers.

The price of energy is prone to significant fluctuations and volatility.

Our apparel manufacturing operations require high inputs of energy, and therefore changes in energy prices directly impact our gross profit margins. We are focusing on manufacturing methods that will reduce the amount of energy used in the production of our apparel products to mitigate the rising costs of energy. Significant increases in energy prices could have a material adverse effect on our results of operations, as there can be no assurance that we could pass these increased costs to our customers given the competitive environment in which our Apparel segment operates.

We depend upon the talents and contributions of a limited number of individuals, many of whom would be difficult to replace.

The loss or interruption of the services of our Chief Executive Officer, Executive Vice President, Vice President of Apparel or Chief Financial Officer could have a material adverse effect on our business, financial condition or results of operations. Although we maintain employment agreements with these individuals, it cannot be assured that the services of such individuals will continue.

11

Table of Contents

Increases in the cost of employee benefits could impact the Company’s financial results and cash flow.

The Company’s expenses relating to employee health benefits are significant. Unfavorable changes in the cost of such benefits could impact the Company’s financial results and cash flow. Healthcare costs have risen significantly in recent years, and recent legislative and private sector initiatives regarding healthcare reform could result in significant changes to the U.S. healthcare system. The Company is not able at this time to determine the impact that healthcare reform could have on the Company-sponsored medical plans.

| ITEM 1B. | UNRESOLVED STAFF COMMENTS |

There are no unresolved SEC staff comments.

| ITEM 2. | PROPERTIES |

Our corporate headquarters are located in Midlothian, Texas. We operate manufacturing and distribution facilities throughout the United States and in Mexico and Canada. See the table below for additional information on our locations.

All of the Print Segment properties are used for the production, warehousing and shipping of the following: business forms, flexographic printing, advertising specialties and Post-it ® Notes (Wolfe City, Texas); presentation products (Macomb, Michigan and Anaheim, California); and printed and electronic promotional media (Denver, Colorado); envelopes (Portland, Oregon; Columbus, Kansas and Tullahoma, Tennessee); financial forms (Minneapolis/St. Paul, Minnesota; Nevada, Iowa and Bridgewater, Virginia) and other business products. The Apparel Segment properties are used for the manufacturing or distribution of t-shirts and other activewear apparel.

Our plants are operated at production levels required to meet our forecasted customer demands. Production levels fluctuate with market demands and depend upon the product mix at any given point in time. Equipment is added as existing machinery becomes obsolete or not repairable, and as new equipment becomes necessary to meet market demands; however, at any given time, these additions and replacements are not considered to be material additions to property, plant and equipment, although such additions or replacements may increase a plant’s efficiency or capacity.

All of the foregoing facilities are considered to be in good condition. We do not anticipate that substantial expansion, refurbishing, or re-equipping will be required in the near future.

All of the rented property is held under leases with original terms of one or more years, expiring at various times through April 2018. No difficulties are presently foreseen in maintaining or renewing such leases as they expire.

The accompanying list contains each of our owned and leased locations:

| Approximate Square Footage | ||||||||||

|

Location |

General Use |

Owned | Leased | |||||||

|

Print Segment |

||||||||||

|

Ennis, Texas |

Three Manufacturing Facilities * | 325,118 | — | |||||||

|

Chatham, Virginia |

Two Manufacturing Facilities | 127,956 | — | |||||||

|

Paso Robles, California |

Manufacturing | 94,120 | — | |||||||

|

DeWitt, Iowa |

Two Manufacturing Facilities | 95,000 | — | |||||||

|

Knoxville, Tennessee |

Manufacturing | 48,057 | — | |||||||

|

Ft. Scott, Kansas |

Manufacturing | 86,660 | — | |||||||

|

Portland, Oregon |

Manufacturing | — | 103,402 | |||||||

|

Wolfe City, Texas |

Two Manufacturing Facilities | 119,259 | — | |||||||

|

Moultrie, Georgia |

Manufacturing | 25,000 | — | |||||||

|

Coshocton, Ohio |

Manufacturing | 24,750 | — | |||||||

|

Macomb, Michigan |

Manufacturing | 56,350 | — | |||||||

|

Anaheim, California |

Three Manufacturing Facilities | — | 49,000 | |||||||

|

Bellville, Texas |

Leasing | 70,196 | — | |||||||

|

Denver, Colorado |

Four Manufacturing Facilities | 60,000 | 101,600 | |||||||

|

San Antonio, Texas |

Manufacturing ** | 47,426 | — | |||||||

|

Brooklyn Park, Minnesota |

Manufacturing | 94,800 | — | |||||||

12

Table of Contents

| Approximate Square Footage | ||||||||||

|

Location |

General Use |

Owned | Leased | |||||||

|

Roseville, Minnesota |

Manufacturing | — | 41,300 | |||||||

|

Roseville, Minnesota |

Warehouse | — | 20,119 | |||||||

|

Nevada, Iowa |

Two Manufacturing | 290,752 | — | |||||||

|

Bridgewater, Virginia |

Manufacturing | — | 27,000 | |||||||

|

Columbus, Kansas |

Manufacturing and Warehouse | 174,089 | — | |||||||

|

Leipsic, Ohio |

Manufacturing | 83,216 | — | |||||||

|

El Dorado Springs, Missouri |

Manufacturing | 70,894 | — | |||||||

|

Princeton, Illinois |

Manufacturing | — | 44,190 | |||||||

|

Arlington, Texas |

Two Manufacturing Facilities | 69,935 | 30,700 | |||||||

|

Tullahoma, Tennessee |

Manufacturing | 24,950 | ||||||||

|

Caledonia, New York |

Manufacturing | 138,730 | — | |||||||

|

Sun City, California |

Manufacturing | 52,617 | — | |||||||

|

Phoenix, Arizona |

Manufacturing and Warehouse | 59,000 | ||||||||

|

Neenah, Wisconsin |

Manufacturing | 57,786 | ||||||||

|

West Chester, Pennsylvania |

Sales Office | 1,150 | ||||||||

|

Vandalia, Ohio |

Manufacturing | 47,820 | ||||||||

|

Fairport, New York |

Manufacturing | 40,800 | ||||||||

|

Jaffrey, New Hampshire |

Sales Office | 647 | ||||||||

|

Indianpolis, Indiana |

Manufacturing | 24,754 | ||||||||

|

Livermore, California |

Manufacturing | 21,568 | ||||||||

|

Smyrna, Georgia |

Manufacturing | 65,000 | ||||||||

|

Clarksville, Tennessee |

Manufacturing | 51,900 | ||||||||

|

Fairhope, Alabama |

Manufacturing | 65,000 | ||||||||

|

Toledo, Ohio |

Manufacturing | 51,900 | ||||||||

|

Visalia, California |

Manufacturing | 56,000 | ||||||||

|

|

|

|

|

|||||||

| 2,396,495 | 744,016 | |||||||||

|

|

|

|

|

|||||||

|

Apparel Segment |

||||||||||

|

Anaheim, California |

Office and Distribution Center | — | 151,000 | |||||||

|

Chicago, Illinois |

Distribution Center | — | 82,100 | |||||||

|

Orlando, Flordia |

Distribution Center | — | 37,804 | |||||||

|

Carrollton, Texas |

Distribution Center | — | 26,136 | |||||||

|

Bensalem, Pennsylvania |

Distribution Center | — | 60,848 | |||||||

|

Mississauga, Canada |

Distribution Center | — | 53,982 | |||||||

|

Los Angeles, California |

Distribution Center | — | 31,600 | |||||||

|

Agua Prieta, Mexico |

Manufacturing | 700,000 | — | |||||||

|

Ensenada, Mexico |

Manufacturing | 87,145 | — | |||||||

|

Ensenada, Mexico |

Car Parking | — | 37,125 | |||||||

|

Ensenada, Mexico |

Warehouse | — | 16,146 | |||||||

|

Hermosillo, Mexico |

Manufacturing | — | 76,145 | |||||||

|

Hermosillo, Mexico |

Yard Space | — | 19,685 | |||||||

|

Hermosillo, Mexico |

Vacant | — | 8,432 | |||||||

|

Hermosillo, Mexico |

Storage for Machines | — | 1,640 | |||||||

|

|

|

|

|

|||||||

| 787,145 | 602,643 | |||||||||

|

|

|

|

|

|||||||

|

Corporate Offices |

||||||||||

|

Ennis, Texas |

Administrative Offices | 9,300 | — | |||||||

|

Midlothian, Texas |

Executive and Administrative Offices | 28,000 | — | |||||||

|

|

|

|

|

|||||||

| 37,300 | — | |||||||||

|

|

|

|

|

|||||||

| Totals | 3,220,940 | 1,346,659 | ||||||||

|

|

|

|

|

|||||||

| * | 7,000 square feet of Ennis, Texas location leased |

| ** | Subsequent to the end of the fiscal year, this facility has been transferred to “Held for Sale” |

13

Table of Contents

| ITEM 3. | LEGAL PROCEEDINGS |

From time to time we are involved in various litigation matters arising in the ordinary course of our business. We do not believe the disposition of any current matter will have a material adverse effect on our consolidated financial position or results of operations.

| ITEM 4. | MINE SAFETY DISCLOSURES |

Not applicable.

14

Table of Contents

| ITEM 5. | MARKET FOR REGISTRANT’S COMMON EQUITY, RELATED STOCKHOLDER MATTERS AND ISSUER PURCHASES OF EQUITY SECURITIES |

Our common stock is traded on the New York Stock Exchange (“NYSE”) under the trading symbol “EBF”. The following table sets forth the high and low sales prices, the common stock trading volume as reported by the New York Stock Exchange and dividends per share paid by the Company for the periods indicated:

| Common Stock | Dividends | |||||||||||||||

| Trading Volume | per share of | |||||||||||||||

| Common Stock Price Range | (number of shares | Common | ||||||||||||||

| High | Low | in thousands) | Stock | |||||||||||||

|

Fiscal Year Ended February 28, 2013 |

||||||||||||||||

|

First Quarter |

$ | 17.13 | $ | 13.92 | 1,841 | $ | 0.175 | |||||||||

|

Second Quarter |

16.22 | 13.71 | 1,985 | $ | 0.175 | |||||||||||

|

Third Quarter |

17.05 | 13.90 | 1,428 | $ | 0.175 | |||||||||||

|

Fourth Quarter |

16.09 | 14.58 | 1,535 | $ | 0.350 | |||||||||||

|

Fiscal Year Ended February 29, 2012 |

||||||||||||||||

|

First Quarter |

$ | 20.23 | $ | 14.91 | 2,660 | $ | 0.155 | |||||||||

|

Second Quarter |

19.04 | 13.81 | 3,109 | $ | 0.155 | |||||||||||

|

Third Quarter |

16.43 | 12.08 | 3,575 | $ | 0.155 | |||||||||||

|

Fourth Quarter |

17.74 | 12.80 | 2,171 | $ | 0.155 | |||||||||||

The last reported sale price of our common stock on NYSE on April 30, 2013 was $15.37. As of that date, there were approximately 936 shareholders of record of our common stock. Cash dividends may be paid or repurchases of our common stock may be made from time to time, as our Board of Directors deems appropriate, after considering our growth rate, operating results, financial condition, cash requirements, restrictive lending covenants, and such other factors as the Board of Directors may deem appropriate.

On October 20, 2008, the Board of Directors authorized the repurchase of up to $5.0 million of our common stock through a stock repurchase program. Under the board-approved repurchase program, share purchases may be made from time to time in the open market or through privately negotiated transactions depending on market conditions, share price, trading volume and other factors, and such purchases, if any, will be made in accordance with applicable insider trading and other securities laws and regulations. These repurchases may be commenced or suspended at any time or from time to time without prior notice. While no shares have been repurchased during fiscal years 2011, 2012 or 2013 under the program, there have been a total of 96,000 shares of common stock that have been purchased under the repurchase program since its inception at an average price per share of $10.45. On April 20, 2012, the Board increased the authorized amount available to repurchase our shares by an additional $5.0 million, bringing the total available to repurchase our common stock to approximately $9.0 million. Unrelated to the stock repurchase program, the Company purchased 175 and 100 shares of common stock during the fiscal years ended February 28, 2013 and February 29, 2012, respectively.

| Total Number | ||||||||||||||||

| Total | of Shares | Maximum Amount | ||||||||||||||

| Number | Average | Purchased as | that May Yet Be Used | |||||||||||||

| of Shares | Price Paid | Part of Publicly | to Purchase Shares | |||||||||||||

|

Period |

Purchased | per Share | Announced Programs | Under the Program | ||||||||||||

|

March 1, 2012 - February 28, 2013 |

— | $ | — | — | $ | 8,997,084 | ||||||||||

|

March 1, 2011 - February 29, 2012 |

— | $ | — | — | $ | 3,997,084 | ||||||||||

|

March 1, 2010 - February 28, 2011 |

— | $ | — | — | $ | 3,997,084 | ||||||||||

15

Table of Contents

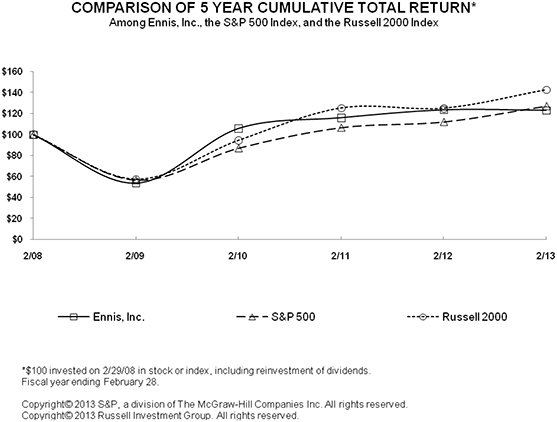

Stock Performance Graph

The graph below matches our cumulative 5-year total shareholder return on common stock with the cumulative total returns of the S & P 500 index and the Russell 2000 index. The graph tracks the performance of a $100 investment in our common stock and in each of the indexes (with the reinvestment of all dividends) from February 29, 2008 to February 28, 2013.

| 2008 | 2009 | 2010 | 2011 | 2012 | 2013 | |||||||||||||||||||

|

Ennis, Inc. |

$ | 100.00 | $ | 53.67 | $ | 105.77 | $ | 116.03 | $ | 123.52 | $ | 123.12 | ||||||||||||

|

S&P 500 |

100.00 | 56.68 | 87.07 | 106.72 | 112.19 | 127.29 | ||||||||||||||||||

|

Russell 2000 |

100.00 | 57.62 | 94.46 | 125.25 | 125.06 | 142.59 | ||||||||||||||||||

The stock price performance included in this graph is not necessarily indicative of future stock price performance.

| ITEM 6. | SELECTED FINANCIAL DATA |

The following selected financial data has been derived from our audited consolidated financial statements. Our consolidated financial statements and notes thereto as of February 28, 2013 and February 29, 2012, and for the three years in the period ended February 28, 2013, and the reports of Grant Thornton LLP are included in Item 15 of this Report. The selected financial data should be read in conjunction with Item 7 — “Management’s Discussion and Analysis of Financial Condition and Results of Operations” and the consolidated financial statements and notes thereto included in Item 15 of this Report.

16

Table of Contents

| Fiscal Years Ended | ||||||||||||||||||||

| 2013 | 2012 | 2011 | 2010 | 2009 | ||||||||||||||||

| (Dollars and shares in thousands, except per share amounts) | ||||||||||||||||||||

|

Operating results: |

||||||||||||||||||||

|

Net sales |

$ | 533,506 | $ | 517,014 | $ | 549,999 | $ | 517,738 | $ | 584,029 | ||||||||||

|

Gross profit margin |

124,152 | 130,513 | 154,498 | 135,319 | 143,476 | |||||||||||||||

|

SG&A expenses |

83,757 | 78,962 | 83,678 | 76,738 | 86,217 | |||||||||||||||

|

Impairment of goodwill and trademarks |

— | — | — | — | 67,851 | |||||||||||||||

|

Net earnings (loss) |

24,715 | 31,358 | 44,631 | 35,206 | (32,768 | ) | ||||||||||||||

|

Earnings (loss) and dividends per share: |

||||||||||||||||||||

|

Basic |

$ | 0.95 | $ | 1.21 | $ | 1.73 | $ | 1.37 | $ | (1.27 | ) | |||||||||

|

Diluted |

0.95 | 1.21 | 1.72 | 1.36 | (1.27 | ) | ||||||||||||||

|

Dividends |

0.88 | 0.62 | 0.62 | 0.62 | 0.62 | |||||||||||||||

|

Weighted average shares outstanding: |

||||||||||||||||||||

|

Basic |

26,036 | 25,946 | 25,855 | 25,769 | 25,724 | |||||||||||||||

|

Diluted |

26,053 | 25,968 | 25,888 | 25,797 | 25,790 | |||||||||||||||

|

Financial Position: |

||||||||||||||||||||

|

Working capital |

$ | 150,377 | $ | 168,969 | $ | 135,300 | $ | 116,638 | $ | 138,374 | ||||||||||

|

Current assets |

193,416 | 219,210 | 182,398 | 166,439 | 182,254 | |||||||||||||||

|

Total assets |

495,292 | 531,962 | 473,728 | 432,699 | 436,380 | |||||||||||||||

|

Current liabilities |

43,039 | 50,241 | 47,098 | 49,801 | 43,880 | |||||||||||||||

|

Long-term debt |

57,500 | 90,000 | 50,000 | 41,817 | 76,185 | |||||||||||||||

|

Total liabilities |

134,076 | 172,087 | 126,045 | 119,439 | 144,374 | |||||||||||||||

|

Shareholders’ equity |

361,216 | 359,875 | 347,683 | 313,260 | 292,006 | |||||||||||||||

|

Current ratio |

4.49 to 1.0 | 4.36 to 1.0 | 3.87 to 1.0 | 3.34 to 1.0 | 4.15 to 1.0 | |||||||||||||||

|

Long-term debt to equity ratio |

0.16 to 1.0 | 0.25 to 1.0 | 0.14 to 1.0 | 0.13 to 1.0 | 0.26 to 1.0 | |||||||||||||||

| ITEM 7. | MANAGEMENT’S DISCUSSION AND ANALYSIS OF FINANCIAL CONDITION AND RESULTS OF OPERATIONS |

The Management’s Discussion and Analysis provides material historical and prospective disclosures intended to enable investors and other users to assess our financial condition and results of operations. Statements that are not historical are forward-looking and involve risk and uncertainties, including those discussed under the caption “Risk Factors” in Item 1A starting on page 7 of this Annual Report on Form 10-K and elsewhere in this Report. You should read this discussion and analysis in conjunction with our Consolidated Financial Statements and the related notes appearing elsewhere in this Report. The words “anticipate,” “preliminary,” “expect,” “believe,” “intend” and similar expressions identify forward-looking statements. We believe these forward-looking statements are based upon reasonable assumptions. All such statements involve risks and uncertainties, and as a result, actual results could differ materially from those projected, anticipated, or implied by these statements.

In view of such uncertainties, investors should not place undue reliance on our forward-looking statements since such statements may prove to be inaccurate and speak only as of the date when made. We undertake no obligation to publicly update or revise any forward-looking statements, whether as a result of new information, future events or otherwise.

This Management’s Discussion and Analysis includes the following sections:

| • | Overview – An overall discussion on our Company, the business challenges and opportunities we believe are key to our success, and our plans for facing these challenges. |

| • | Critical Accounting Policies and Estimates – A discussion of the accounting policies that require our most critical judgments and estimates. This discussion provides insight into the level of subjectivity, quality, and variability involved in these judgments and estimates. This section also provides a summary of recently adopted and recently issued accounting pronouncements that have or may materially affect our business. |

| • | Results of Operations – An analysis of our consolidated results of operations and segment results for the three years presented in our consolidated financial statements. This analysis discusses material trends within our business and provides important information necessary for an understanding of our operating results. |

17

Table of Contents

| • | Liquidity and Capital Resources - An analysis of our cash flows and a discussion of our financial condition and contractual obligations. This section provides information necessary to evaluate our ability to generate cash and to meet existing and known future cash requirements over both the short and long term. |

References to 2013, 2012 and 2011 refer to the fiscal years ended February 28, 2013, February 29, 2012 and February 28, 2011, respectively.

Overview

The Company – We are one of the largest providers of business forms to independent distributors in the United States and are also one of the largest providers of blank t-shirts in North America to the activewear market. We operate in two reportable segments: Print and Apparel.

Our Print Business Challenges - In our Print Segment, we are engaged in an industry undergoing significant changes. Technology advances have made electronic distribution of documents, internet hosting, digital printing and print-on-demand valid, cost-effective alternatives to traditional custom printed documents and customer communications. In addition, the economic downturn in the economy and the associated credit crunch created highly competitive conditions in an already over-supplied, price-competitive industry, continue to present challenges today. Thus, we believe we are facing the following challenges in the Print Segment of our business:

| • | Transformation of our portfolio of products |

| • | Excess production capacity and price competition within our industry |

| • | Continued economic uncertainties |

The following is a discussion of these business challenges and our strategy for managing their effect on our print business.

Transformation of our portfolio of products – Traditional business documents are essential in order to conduct business. However, many are being replaced or devalued with advances in digital technologies, causing steady declines in demand for a large portion of our current product line. The same digital advances also introduce potential new growth opportunities, such as print-on-demand services and product offerings that assist customers in their transition to digital business environments. In addition, we will continue to look for new market opportunities and niches, such as the addition of our envelope offerings, healthcare wristbands, secure document solutions, innovative in-mold label offerings and long-run integrated products with high color web printing that provide us with an opportunity for growth and differentiate us from our competition. Transforming our product offerings in order to continue to provide innovative, valuable solutions to our customers on a proactive basis will require us to make investments in new and existing technology and to develop key strategic business relationships.

Excess production capacity and price competition within our industry – Paper mills continue to adjust production capacity through downtime and closures to attempt to keep supply in line with demand. Due to the limited number of paper mills, paper prices have been and are expected to remain fairly volatile.

Despite a continued competitive marketplace, we have generally been able to pass through increased paper costs, although it can often take several quarters to push these through due to the custom nature of our products and/or contractual relationships with some of our customers. We expect this trend to continue, however, any new downturn in the economy or continued protraction of the current recovery may limit our ability to recover all these costs. As such, we will continue to focus our efforts on effectively managing and controlling our product costs to minimize the effects of the foregoing on our operational results, primarily through the use of forecasting models and production and costing models. However, an inherent risk in this process is that our assumptions are inaccurate, which could have a negative impact on our reported profit margins.

Continued economic uncertainties – As a result of the past recessionary conditions, the economic climate has been volatile and challenging. Decreased demand and intense price competition resulted in a significant decline in our revenue during the past several fiscal years. Although we have seen improvement in some economic indicators within our markets, a generally weak domestic job market, global economic instabilities, a rather anemic domestic economic recovery and domestic policy uncertainties have and will continue to present a challenging environment for revenue growth. As we cannot predict the pace or continuance of the domestic economic recovery, the impact of

18

Table of Contents

continued global economic instability, nor the impact of domestic policy decisions, we continue to focus on customer retention, expanding our growth targeted products and continuing to develop new market niches. In addition, we have a proven history of managing our costs during tough economic times and would not expect this to change in the future.

Our Apparel Business Challenges - In our Apparel Segment, our market niche is highly competitive, commodity driven, and is generally dominated by a limited number of companies. The downturn in the economy and turmoil in the credit markets in 2009 and 2010 created an over-supply situation which further increased competitive pressures in this market. While the economic environment improved somewhat in 2011, which led to increased demand for our product during the later part of fiscal year 2011 and the start of fiscal year 2012, we have seen softness in the market due to domestic and global economic uncertainties. Whether the impact in the market associated with this instability is behind us or will still need to be dealt with for quarters to come is unknown. Such uncertainty and volatility in the economy is normally not a positive influence on the marketplace. In addition, a significant reduction in the spot price of cotton added additional complexities to an already competitive marketplace during fiscal year 2013. The divergence between the current purchase cost of cotton and the cost residing in most manufacturers’ finished goods inventories were at historical levels, creating market valuation issues for some and sale side pressure for others. However, at this point, most of the higher cost of cotton has worked through our finished goods inventory and the divergence between the current purchase cost of cotton and the average costs in our finished goods inventory has returned to a more normalized spread. Thus, we believe we are facing the following challenges in our Apparel Segment continuing into the next fiscal year:

| • | Cotton prices and market pricing |

| • | New manufacturing facility |

| • | Continued economic uncertainties |

Cotton prices – Cotton is a commodity product and subject to volatile fluctuations in price. Costs for cotton yarn and cotton-based textiles vary based upon the fluctuating cost of cotton, which is affected by, among other factors, weather, consumer demand, commodities market speculation, currency fluctuations, international actions and other factors that are generally unpredictable and beyond our control. The United States is the largest exporter of cotton in the world. Therefore, domestic prices can be significantly influenced by foreign governments actions. Over the past several years, we have seen cotton prices reach the highest historical levels and have recently seen the prices recede back to levels that, while still high, are more in line with historical averages. We are able to lock in the cost of cotton reflected in the price we pay for yarn from our primary suppliers in an attempt to protect our business from the volatility of the market price of cotton. However, our business can be affected by dramatic movements in cotton prices. The cost incurred for materials, i.e., yarn, thread, etc. are capitalized into inventory and impacts the Company’s operating results as this inventory is sold, which could be as much as six months plus after the materials were purchased, depending on inventory turns. Consequently, significant and rapid increases or decreases in cotton costs can have a material impact to the Company’s operational results. Most of the higher cost of cotton has worked through our finished goods inventory at this point, and the divergence between the current purchase cost of cotton and the average costs in our finished goods inventory has returned to a more normalized spread. Absent some economic disruption (see below), or market abnormalities, we expect to see continuing improvement in our apparel margins in the quarters to come.

Agua Prieta manufacturing facility – The manufacturing facility in Agua Prieta, Mexico (“AP”) became operational in July 2011, and all production has now been transitioned from our Anaheim, CA (“Anaheim”) facility to the AP facility. We began producing fabric from this facility during the first quarter of fiscal year 2012. Production levels at the plant are running at required levels to satisfy demand, but below originally estimated levels due to lower revenues, which can be attributed to market softness, economic conditions and the non-competitive cost position of our finished goods inventory during fiscal year 2013. In addition, from time-to-time we have had disruptions in our utility services which impacts our manufacturing through-put. However, given the improved cost position of our finished goods inventory and current level of utility services and absent some economic disruption, we expect to increase production at this facility fairly significantly during the coming year. This should allow us to realize savings through improved efficiency and utilization gains. However, the increase in production levels is dependent on economic (see below) and services stability.

Continued economic uncertainties – As a result of the past recessionary conditions, the economic climate has been and continues to be volatile and challenging both domestically and internationally. Although we saw an increase in our apparel revenues during fiscal year 2011 due to improving economic conditions, we saw a significant drop in our sales during the latter half of fiscal year 2012 due to competitive pricing pressures, which we attribute to softness in the market. International instability and continued domestic policy and economic issues continue to have an impact on the domestic economic environment and on domestic apparel sales. We are concerned with how our

19

Table of Contents