|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Table of Contents

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

WASHINGTON, D.C. 20549

FORM 10-Q

| x | Quarterly Report Pursuant To Section 13 or 15(d) of the Securities Exchange Act of 1934 |

FOR THE QUARTERLY PERIOD ENDED SEPTEMBER 30, 2013

OR

| ¨ | Transition Report Pursuant to Section 13 or 15(d) of the Securities Exchange Act of 1934 |

For the transition period from to

|

Commission File Number |

Exact name of registrant as specified in its charter and principal office address and telephone number |

State of

|

I.R.S. Employer

|

|||

| 1-14514 | Consolidated Edison, Inc. | New York | 13-3965100 | |||

| 4 Irving Place, New York, New York 10003 | ||||||

| (212) 460-4600 | ||||||

| 1-1217 | Consolidated Edison Company of New York, Inc. | New York | 13-5009340 | |||

| 4 Irving Place, New York, New York 10003 | ||||||

| (212) 460-4600 | ||||||

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days.

| Consolidated Edison, Inc. (Con Edison) | Yes x | No ¨ | ||||||

| Consolidated Edison of New York, Inc. (CECONY) | Yes x | No ¨ | ||||||

Indicate by check mark whether the registrant has submitted electronically and posted on its corporate Web site, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T (§232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files).

| Con Edison | Yes x | No ¨ | ||||||

| CECONY | Yes x | No ¨ | ||||||

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, or a smaller reporting company. See the definitions of “large accelerated filer”, “accelerated filer” and “smaller reporting company” in Rule 12b-2 of the Exchange Act.

| Con Edison | ||||||

| Large accelerated filer x | Accelerated filer ¨ | Non-accelerated filer ¨ | Smaller reporting company ¨ | |||

| CECONY | ||||||

| Large accelerated filer ¨ | Accelerated filer ¨ | Non-accelerated filer x | Smaller reporting company ¨ | |||

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act).

| Con Edison | Yes ¨ | No x | ||||||

| CECONY | Yes ¨ | No x | ||||||

As of October 30, 2013, Con Edison had outstanding 292,888,192 Common Shares ($.10 par value). All of the outstanding common equity of CECONY is held by Con Edison.

Filing Format

This Quarterly Report on Form 10-Q is a combined report being filed separately by two different registrants: Consolidated Edison, Inc. (Con Edison) and Consolidated Edison Company of New York, Inc. (CECONY). CECONY is a subsidiary of Con Edison and, as such, the information in this report about CECONY also applies to Con Edison. As used in this report, the term the “Companies” refers to Con Edison and CECONY. However, CECONY makes no representation as to the information contained in this report relating to Con Edison or the subsidiaries of Con Edison other than itself.

Table of Contents

Glossary of Terms

The following is a glossary of frequently used abbreviations or acronyms that are used in the Companies’ SEC reports:

| Con Edison Companies | ||

| Con Edison | Consolidated Edison, Inc. | |

| CECONY | Consolidated Edison Company of New York, Inc. | |

| Con Edison Development | Consolidated Edison Development, Inc. | |

| Con Edison Energy | Consolidated Edison Energy, Inc. | |

| Con Edison Solutions | Consolidated Edison Solutions, Inc. | |

| O&R | Orange and Rockland Utilities, Inc. | |

| Pike | Pike County Light & Power Company | |

| RECO | Rockland Electric Company | |

| The Companies | Con Edison and CECONY | |

| The Utilities | CECONY and O&R | |

| Regulatory Agencies, Government Agencies, and Quasi-governmental Not-for-Profits | ||

| EPA | U. S. Environmental Protection Agency | |

| FERC | Federal Energy Regulatory Commission | |

| IRS | Internal Revenue Service | |

| ISO-NE | ISO New England Inc. | |

| NJBPU | New Jersey Board of Public Utilities | |

| NJDEP | New Jersey Department of Environmental Protection | |

| NYISO | New York Independent System Operator | |

| NYPA | New York Power Authority | |

| NYSAG | New York State Attorney General | |

| NYSDEC | New York State Department of Environmental Conservation | |

| NYSERDA | New York State Energy Research and Development Authority | |

| NYSPSC | New York State Public Service Commission | |

| NYSRC | New York State Reliability Council, LLC | |

| PAPUC | Pennsylvania Public Utility Commission | |

| PJM | PJM Interconnection LLC | |

| SEC | U.S. Securities and Exchange Commission | |

| Accounting | ||

| ABO | Accumulated Benefit Obligation | |

| ASU | Accounting Standards Update | |

| FASB | Financial Accounting Standards Board | |

| LILO | Lease In/Lease Out | |

| OCI | Other Comprehensive Income | |

| SFAS | Statement of Financial Accounting Standards | |

| VIE | Variable interest entity | |

| Environmental | ||

| CO 2 | Carbon dioxide | |

| GHG | Greenhouse gases | |

| MGP Sites | Manufactured gas plant sites | |

| PCBs | Polychlorinated biphenyls | |

| PRP | Potentially responsible party | |

| SO 2 | Sulfur dioxide | |

| Superfund | Federal Comprehensive Environmental Response, Compensation and Liability Act of 1980 and similar state statutes | |

| 2 |

Table of Contents

| Units of Measure | ||

| AC | Alternating current | |

| dths | Dekatherms | |

| kV | Kilovolt | |

| kWh | Kilowatt-hour | |

| mdths | Thousand dekatherms | |

| MMlbs | Million pounds | |

| MVA | Megavolt ampere | |

| MW | Megawatt or thousand kilowatts | |

| MWH | Megawatt hour | |

| Other | ||

| AFDC | Allowance for funds used during construction | |

| COSO | Committee of Sponsoring Organizations of the Treadway Commission | |

| EMF | Electric and magnetic fields | |

| ERRP | East River Repowering Project | |

| Fitch | Fitch Ratings | |

| First Quarter Form 10-Q | The Companies’ combined Quarterly Report on Form 10-Q for the quarterly period ended March 31 of the current year | |

| Form 10-K | The Companies’ combined Annual Report on Form 10-K for the year ended December 31, 2012 | |

| LTIP | Long Term Incentive Plan | |

| Moody’s | Moody’s Investors Service | |

| S&P | Standard & Poor’s Financial Services LLC | |

| Second Quarter Form 10-Q | The Companies’ combined Quarterly Report on Form 10-Q for the quarterly period ended June 30 of the current year | |

| Third Quarter Form 10-Q | The Companies’ combined Quarterly Report on Form 10-Q for the quarterly period ended September 30 of the current year | |

| VaR | Value-at-Risk |

| 3 |

Table of Contents

| PAGE | ||||||

| PART I—Financial Information | ||||||

| ITEM 1 |

Financial Statements (Unaudited) |

|||||

|

Con Edison |

||||||

| 6 | ||||||

| 7 | ||||||

| 8 | ||||||

| 9 | ||||||

| 11 | ||||||

|

CECONY |

||||||

| 12 | ||||||

| 13 | ||||||

| 14 | ||||||

| 15 | ||||||

| 17 | ||||||

| 18 | ||||||

| ITEM 2 |

Management’s Discussion and Analysis of Financial Condition and Results of Operations |

48 | ||||

| ITEM 3 | 80 | |||||

| ITEM 4 | 80 | |||||

| PART II—Other Information | ||||||

| ITEM 1 | 81 | |||||

| ITEM 1A | 81 | |||||

| ITEM 2 | 82 | |||||

| ITEM 6 | 83 | |||||

| Signatures | 85 | |||||

| 4 |

Table of Contents

FORWARD-LOOKING STATEMENTS

This report includes forward-looking statements intended to qualify for the safe-harbor provisions of Section 27A of the Securities Act of 1933, as amended, and Section 21E of the Securities Exchange Act of 1934, as amended. Forward-looking statements are statements of future expectation and not facts. Words such as “expects,” “estimates,” “anticipates,” “intends,” “believes,” “plans,” “will” and similar expressions identify forward-looking statements. Forward-looking statements are based on information available at the time the statements are made, and accordingly speak only as of that time. Actual results or developments might differ materially from those included in the forward-looking statements because of various risks, including:

| • |

the failure to operate energy facilities safely and reliably could adversely affect the Companies; |

| • |

the failure to properly complete construction projects could adversely affect the Companies; |

| • |

the failure of processes and systems and the performance of employees and contractors could adversely affect the Companies; |

| • |

the Companies are extensively regulated and are subject to penalties; |

| • |

the Utilities’ rate plans may not provide a reasonable return; |

| • |

the Companies may be adversely affected by changes to the Utilities’ rate plans; |

| • |

the Companies are exposed to risks from the environmental consequences of their operations; |

| • |

a disruption in the wholesale energy markets or failure by an energy supplier could adversely affect the Companies; |

| • |

the Companies have substantial unfunded pension and other postretirement benefit liabilities; |

| • |

Con Edison’s ability to pay dividends or interest depends on dividends from its subsidiaries; |

| • |

the Companies require access to capital markets to satisfy funding requirements; |

| • |

a cyber attack could adversely affect the Companies; and |

| • |

the Companies also face other risks that are beyond their control. |

| 5 |

Table of Contents

|

|

|

For the Three Months

Ended September 30, |

For the Nine Months

Ended September 30, |

|||||||||||||||

| 2013 | 2012 | 2013 | 2012 | |||||||||||||

| (Millions of Dollars/Except Share Data) | ||||||||||||||||

|

OPERATING REVENUES |

||||||||||||||||

|

Electric |

$ | 2,822 | $ | 2,810 | $ | 6,799 | $ | 6,762 | ||||||||

|

Gas |

225 | 216 | 1,333 | 1,161 | ||||||||||||

|

Steam |

72 | 68 | 522 | 414 | ||||||||||||

|

Non-utility |

365 | 344 | 833 | 950 | ||||||||||||

|

TOTAL OPERATING REVENUES |

3,484 | 3,438 | 9,487 | 9,287 | ||||||||||||

|

OPERATING EXPENSES |

||||||||||||||||

|

Purchased power |

946 | 930 | 2,421 | 2,440 | ||||||||||||

|

Fuel |

56 | 59 | 261 | 213 | ||||||||||||

|

Gas purchased for resale |

74 | 56 | 443 | 314 | ||||||||||||

|

Other operations and maintenance |

795 | 826 | 2,400 | 2,365 | ||||||||||||

|

Depreciation and amortization |

258 | 240 | 764 | 709 | ||||||||||||

|

Taxes, other than income taxes |

500 | 476 | 1,431 | 1,360 | ||||||||||||

|

TOTAL OPERATING EXPENSES |

2,629 | 2,587 | 7,720 | 7,401 | ||||||||||||

|

OPERATING INCOME |

855 | 851 | 1,767 | 1,886 | ||||||||||||

|

OTHER INCOME (DEDUCTIONS) |

||||||||||||||||

|

Investment and other income |

8 | 4 | 19 | 14 | ||||||||||||

|

Allowance for equity funds used during construction |

1 | 1 | 2 | 3 | ||||||||||||

|

Other deductions |

(4 | ) | (3 | ) | (12 | ) | (13 | ) | ||||||||

|

TOTAL OTHER INCOME (DEDUCTIONS) |

5 | 2 | 9 | 4 | ||||||||||||

|

INCOME BEFORE INTEREST AND INCOME TAX EXPENSE |

860 | 853 | 1,776 | 1,890 | ||||||||||||

|

INTEREST EXPENSE |

||||||||||||||||

|

Interest on long-term debt |

145 | 146 | 433 | 440 | ||||||||||||

|

Other interest |

2 | 6 | 143 | 17 | ||||||||||||

|

Allowance for borrowed funds used during construction |

(1 | ) | — | (1 | ) | (2 | ) | |||||||||

|

NET INTEREST EXPENSE |

146 | 152 | 575 | 455 | ||||||||||||

|

INCOME BEFORE INCOME TAX EXPENSE |

714 | 701 | 1,201 | 1,435 | ||||||||||||

|

INCOME TAX EXPENSE |

250 | 261 | 373 | 501 | ||||||||||||

|

NET INCOME |

464 | 440 | 828 | 934 | ||||||||||||

|

Preferred stock dividend requirements of subsidiary |

— | — | — | (3 | ) | |||||||||||

|

NET INCOME FOR COMMON STOCK |

$ | 464 | $ | 440 | $ | 828 | $ | 931 | ||||||||

|

Net income for common stock per common share—basic |

$ | 1.58 | $ | 1.50 | $ | 2.83 | $ | 3.18 | ||||||||

|

Net income for common stock per common share—diluted |

$ | 1.58 | $ | 1.49 | $ | 2.81 | $ | 3.16 | ||||||||

|

DIVIDENDS DECLARED PER SHARE OF COMMON STOCK |

$ | 0.615 | $ | 0.605 | $ | 1.845 | $ | 1.815 | ||||||||

|

AVERAGE NUMBER OF SHARES OUTSTANDING—BASIC (IN MILLIONS) |

292.9 | 292.9 | 292.9 | 292.9 | ||||||||||||

|

AVERAGE NUMBER OF SHARES OUTSTANDING—DILUTED (IN MILLIONS) |

294.3 | 294.6 | 294.3 | 294.6 | ||||||||||||

The accompanying notes are an integral part of these financial statements.

| 6 |

Table of Contents

|

CONSOLIDATED STATEMENT OF COMPREHENSIVE INCOME (UNAUDITED) |

|

For the Three Months

Ended September 30, |

For the Nine Months

Ended September 30, |

|||||||||||||||

| 2013 | 2012 | 2013 | 2012 | |||||||||||||

| (Millions of Dollars) | ||||||||||||||||

|

NET INCOME |

$464 | $440 | $828 | $934 | ||||||||||||

|

OTHER COMPREHENSIVE INCOME/(LOSS), NET OF TAXES |

||||||||||||||||

|

Pension plan liability adjustments, net of $1 and $4 in 2013 and $1 and $5 taxes in 2012, respectively |

2 | 2 | 7 | 8 | ||||||||||||

|

TOTAL OTHER COMPREHENSIVE INCOME/(LOSS), NET OF TAXES |

2 | 2 | 7 | 8 | ||||||||||||

|

COMPREHENSIVE INCOME |

466 | 442 | 835 | 942 | ||||||||||||

|

Preferred stock dividend requirements of subsidiary |

— | — | — | (3 | ) | |||||||||||

|

COMPREHENSIVE INCOME FOR COMMON STOCK |

$466 | $442 | $835 | $939 | ||||||||||||

The accompanying notes are an integral part of these financial statements.

| 7 |

Table of Contents

|

|

|

For the Nine Months Ended September 30, |

||||||||

| 2013 | 2012 | |||||||

| (Millions of Dollars) | ||||||||

|

OPERATING ACTIVITIES |

||||||||

|

Net Income |

$ | 828 | $ | 934 | ||||

|

PRINCIPAL NON-CASH CHARGES/(CREDITS) TO INCOME |

||||||||

|

Depreciation and amortization |

764 | 709 | ||||||

|

Deferred income taxes |

116 | 344 | ||||||

|

Rate case amortization and accruals |

1 | 32 | ||||||

|

Common equity component of allowance for funds used during construction |

(2 | ) | (3 | ) | ||||

|

Net derivative (gains)/losses |

(6 | ) | (61 | ) | ||||

|

Pre-tax gains on the termination of LILO transactions |

(95 | ) | — | |||||

|

Other non-cash items (net) |

46 | (53 | ) | |||||

|

CHANGES IN ASSETS AND LIABILITIES |

||||||||

|

Accounts receivable – customers, less allowance for uncollectibles |

(51 | ) | (196 | ) | ||||

|

Special deposits |

(305 | ) | — | |||||

|

Materials and supplies, including fuel oil and gas in storage |

(38 | ) | 1 | |||||

|

Other receivables and other current assets |

(8 | ) | 54 | |||||

|

Prepayments |

(362 | ) | (288 | ) | ||||

|

Accounts payable |

(193 | ) | 18 | |||||

|

Pensions and retiree benefits obligations |

665 | 713 | ||||||

|

Pensions and retiree benefits contributions |

(887 | ) | (821 | ) | ||||

|

Accrued taxes |

217 | (80 | ) | |||||

|

Accrued interest |

171 | 46 | ||||||

|

Superfund and environmental remediation costs (net) |

(6 | ) | 7 | |||||

|

Deferred charges, noncurrent assets and other regulatory assets |

(6 | ) | 183 | |||||

|

Deferred credits and other regulatory liabilities |

291 | 83 | ||||||

|

Other assets |

51 | — | ||||||

|

Other liabilities |

47 | 16 | ||||||

|

NET CASH FLOWS FROM OPERATING ACTIVITIES |

1,238 | 1,638 | ||||||

|

INVESTING ACTIVITIES |

||||||||

|

Utility construction expenditures |

(1,701 | ) | (1,450 | ) | ||||

|

Cost of removal less salvage |

(144 | ) | (118 | ) | ||||

|

Non-utility construction expenditures |

(149 | ) | (68 | ) | ||||

|

Investments in solar energy projects |

(174 | ) | (258 | ) | ||||

|

Proceeds from grants related to solar energy projects |

88 | 27 | ||||||

|

Increase in restricted cash |

(15 | ) | — | |||||

|

Proceeds from the termination of LILO transactions |

200 | — | ||||||

|

NET CASH FLOWS USED IN INVESTING ACTIVITIES |

(1,895 | ) | (1,867 | ) | ||||

|

FINANCING ACTIVITIES |

||||||||

|

Net proceeds of short-term debt |

681 | 340 | ||||||

|

Preferred stock redemption |

— | (239 | ) | |||||

|

Issuance of long-term debt |

919 | 400 | ||||||

|

Retirement of long-term debt |

(707 | ) | (304 | ) | ||||

|

Issuance of common shares for stock plans, net of repurchases |

(4 | ) | (16 | ) | ||||

|

Debt issuance costs |

(12 | ) | (4 | ) | ||||

|

Common stock dividends |

(540 | ) | (524 | ) | ||||

|

Preferred stock dividends |

— | (3 | ) | |||||

|

NET CASH FLOWS FROM (USED IN) FINANCING ACTIVITIES |

337 | (350 | ) | |||||

|

CASH AND TEMPORARY CASH INVESTMENTS: |

||||||||

|

NET CHANGE FOR THE PERIOD |

(320 | ) | (579 | ) | ||||

|

BALANCE AT BEGINNING OF PERIOD |

394 | 648 | ||||||

|

BALANCE AT END OF PERIOD |

$ | 74 | $ | 69 | ||||

|

SUPPLEMENTAL DISCLOSURE OF CASH FLOW INFORMATION |

||||||||

|

Cash paid during the period for: |

||||||||

|

Interest |

$ | 372 | $ | 379 | ||||

|

Income taxes |

$ | 27 | $ | 46 | ||||

The accompanying notes are an integral part of these financial statements.

| 8 |

Table of Contents

|

|

|

September 30,

2013 |

December 31,

2012 |

|||||||

| (Millions of Dollars) | ||||||||

|

ASSETS |

||||||||

|

CURRENT ASSETS |

||||||||

|

Cash and temporary cash investments |

$ | 74 | $ | 394 | ||||

|

Special deposits |

375 | 70 | ||||||

|

Accounts receivable – customers, less allowance for uncollectible accounts of $95 and $94 in 2013 and 2012, respectively |

1,273 | 1,222 | ||||||

|

Accrued unbilled revenue |

425 | 516 | ||||||

|

Other receivables, less allowance for uncollectible accounts of $8 and $10 in 2013 and 2012, respectively |

257 | 228 | ||||||

|

Fuel oil, gas in storage, materials and supplies, at average cost |

368 | 330 | ||||||

|

Prepayments |

521 | 159 | ||||||

|

Deferred tax assets – current |

186 | 296 | ||||||

|

Regulatory assets |

46 | 74 | ||||||

|

Other current assets |

179 | 162 | ||||||

|

TOTAL CURRENT ASSETS |

3,704 | 3,451 | ||||||

|

INVESTMENTS |

444 | 467 | ||||||

|

UTILITY PLANT, AT ORIGINAL COST |

||||||||

|

Electric |

23,041 | 22,376 | ||||||

|

Gas |

5,388 | 5,120 | ||||||

|

Steam |

2,117 | 2,049 | ||||||

|

General |

2,301 | 2,302 | ||||||

|

TOTAL |

32,847 | 31,847 | ||||||

|

Less: Accumulated depreciation |

6,952 | 6,573 | ||||||

|

Net |

25,895 | 25,274 | ||||||

|

Construction work in progress |

1,450 | 1,027 | ||||||

|

NET UTILITY PLANT |

27,345 | 26,301 | ||||||

|

NON-UTILITY PLANT |

||||||||

|

Non-utility property, less accumulated depreciation of $84 and $68 in 2013 and 2012, respectively |

581 | 555 | ||||||

|

Construction work in progress |

29 | 83 | ||||||

|

NET PLANT |

27,955 | 26,939 | ||||||

|

OTHER NONCURRENT ASSETS |

||||||||

|

Goodwill |

429 | 429 | ||||||

|

Intangible assets, less accumulated amortization of $4 in 2013 and 2012 |

4 | 2 | ||||||

|

Regulatory assets |

9,190 | 9,705 | ||||||

|

Other deferred charges and noncurrent assets |

238 | 216 | ||||||

|

TOTAL OTHER NONCURRENT ASSETS |

9,861 | 10,352 | ||||||

|

TOTAL ASSETS |

$ | 41,964 | $ | 41,209 | ||||

The accompanying notes are an integral part of these financial statements.

| 9 |

Table of Contents

|

Consolidated Edison, Inc. CONSOLIDATED BALANCE SHEET (UNAUDITED) |

|

September 30,

2013 |

December 31,

2012 |

|||||||

| (Millions of Dollars) | ||||||||

|

LIABILITIES AND SHAREHOLDERS’ EQUITY |

||||||||

|

CURRENT LIABILITIES |

||||||||

|

Long-term debt due within one year |

$ | 483 | $ | 706 | ||||

|

Notes payable |

1,220 | 539 | ||||||

|

Accounts payable |

925 | 1,215 | ||||||

|

Customer deposits |

316 | 304 | ||||||

|

Accrued taxes |

379 | 162 | ||||||

|

Accrued interest |

324 | 153 | ||||||

|

Accrued wages |

93 | 94 | ||||||

|

Fair value of derivative liabilities |

25 | 47 | ||||||

|

Regulatory liabilities |

117 | 183 | ||||||

|

Uncertain income tax liabilities |

— | 44 | ||||||

|

Other current liabilities |

491 | 498 | ||||||

|

TOTAL CURRENT LIABILITIES |

4,373 | 3,945 | ||||||

|

NONCURRENT LIABILITIES |

||||||||

|

Obligations under capital leases |

2 | 2 | ||||||

|

Provision for injuries and damages |

195 | 149 | ||||||

|

Pensions and retiree benefits |

3,816 | 4,678 | ||||||

|

Superfund and other environmental costs |

512 | 545 | ||||||

|

Asset retirement obligations |

164 | 159 | ||||||

|

Fair value of derivative liabilities |

29 | 31 | ||||||

|

Uncertain income tax liabilities |

8 | — | ||||||

|

Other noncurrent liabilities |

120 | 125 | ||||||

|

TOTAL NONCURRENT LIABILITIES |

4,846 | 5,689 | ||||||

|

DEFERRED CREDITS AND REGULATORY LIABILITIES |

||||||||

|

Deferred income taxes and investment tax credits |

8,481 | 8,372 | ||||||

|

Regulatory liabilities |

1,557 | 1,202 | ||||||

|

Other deferred credits |

48 | 70 | ||||||

|

TOTAL DEFERRED CREDITS AND REGULATORY LIABILITIES |

10,086 | 9,644 | ||||||

|

LONG-TERM DEBT |

10,493 | 10,062 | ||||||

|

COMMON SHAREHOLDERS’ EQUITY (See Statement of Common Shareholders’ Equity) |

12,166 | 11,869 | ||||||

|

TOTAL LIABILITIES AND SHAREHOLDERS’ EQUITY |

$ | 41,964 | $ | 41,209 | ||||

The accompanying notes are an integral part of these financial statements.

| 10 |

Table of Contents

|

CONSOLIDATED STATEMENT OF COMMON SHAREHOLDERS’ EQUITY (UNAUDITED) |

||

| Common Stock |

Additional

|

Retained

|

Treasury Stock |

Capital

|

Accumulated

Other Comprehensive Income/(Loss) |

|||||||||||||||||||||||||||||||

| (Millions of Dollars/Except Share Data) | Shares | Amount | Shares | Amount | Total | |||||||||||||||||||||||||||||||

|

BALANCE AS OF DECEMBER 31, 2011 |

292,888,521 | $ | 32 | $ | 4,991 | $ | 7,568 | 23,194,075 | $(1,033 | ) | $(64 | ) | $(58 | ) | $11,436 | |||||||||||||||||||||

|

Net income for common stock |

277 | 277 | ||||||||||||||||||||||||||||||||||

|

Common stock dividends |

(177 | ) | (177 | ) | ||||||||||||||||||||||||||||||||

|

Issuance of common shares for stock plans, net of repurchases |

(7,225 | ) | 7,225 | (2 | ) | (2 | ) | |||||||||||||||||||||||||||||

|

Preferred stock redemption |

4 | 4 | ||||||||||||||||||||||||||||||||||

|

Other comprehensive income |

7 | 7 | ||||||||||||||||||||||||||||||||||

|

BALANCE AS OF MARCH 31, 2012 |

292,881,296 | $ | 32 | $ | 4,991 | $ | 7,668 | 23,201,300 | $(1,035 | ) | $(60 | ) | $(51 | ) | $11,545 | |||||||||||||||||||||

|

Net income for common stock |

214 | 214 | ||||||||||||||||||||||||||||||||||

|

Common stock dividends |

(178 | ) | (178 | ) | ||||||||||||||||||||||||||||||||

|

Issuance of common shares for stock plans, net of repurchases |

1,700 | (1,700 | ) | (1 | ) | (1 | ) | |||||||||||||||||||||||||||||

|

Other comprehensive loss |

(1 | ) | (1 | ) | ||||||||||||||||||||||||||||||||

|

BALANCE AS OF JUNE 30, 2012 |

292,882,996 | $ | 32 | $ | 4,991 | $ | 7,704 | 23,199,600 | $(1,035 | ) | $(61 | ) | $(52 | ) | $11,579 | |||||||||||||||||||||

|

Net income for common stock |

440 | 440 | ||||||||||||||||||||||||||||||||||

|

Common stock dividends |

(177 | ) | (177 | ) | ||||||||||||||||||||||||||||||||

|

Issuance of common shares for stock plans, net of repurchases |

(11,100 | ) | 11,100 | (2 | ) | (2 | ) | |||||||||||||||||||||||||||||

|

Other comprehensive income |

2 | 2 | ||||||||||||||||||||||||||||||||||

|

BALANCE AS OF SEPTEMBER 30, 2012 |

292,871,896 | $ | 32 | $ | 4,991 | $ | 7,967 | 23,210,700 | $(1,037 | ) | $(61 | ) | $(50 | ) | $11,842 | |||||||||||||||||||||

|

BALANCE AS OF DECEMBER 31, 2012 |

292,871,896 | $ | 32 | $ | 4,991 | $ | 7,997 | 23,210,700 | $(1,037 | ) | $(61 | ) | $(53 | ) | $11,869 | |||||||||||||||||||||

|

Net income for common stock |

192 | 192 | ||||||||||||||||||||||||||||||||||

|

Common stock dividends |

(180 | ) | (180 | ) | ||||||||||||||||||||||||||||||||

|

Issuance of common shares for stock plans, net of repurchases |

95,468 | (2 | ) | (95,468 | ) | 7 | 5 | |||||||||||||||||||||||||||||

|

Other comprehensive income |

3 | 3 | ||||||||||||||||||||||||||||||||||

|

BALANCE AS OF MARCH 31, 2013 |

292,967,364 | $ | 32 | $ | 4,989 | $ | 8,009 | 23,115,232 | $(1,030 | ) | $(61 | ) | $(50 | ) | $11,889 | |||||||||||||||||||||

|

Net income for common stock |

172 | 172 | ||||||||||||||||||||||||||||||||||

|

Common stock dividends |

(180 | ) | (180 | ) | ||||||||||||||||||||||||||||||||

|

Issuance of common shares for stock plans, net of repurchases |

(4,078 | ) | 1 | 4,078 | (1 | ) | — | |||||||||||||||||||||||||||||

|

Other comprehensive income |

2 | 2 | ||||||||||||||||||||||||||||||||||

|

BALANCE AS OF JUNE 30, 2013 |

292,963,286 | $ | 32 | $ | 4,990 | $ | 8,001 | 23,119,310 | $(1,031 | ) | $(61 | ) | $(48 | ) | $11,883 | |||||||||||||||||||||

|

Net income for common stock |

464 | 464 | ||||||||||||||||||||||||||||||||||

|

Common stock dividends |

(180 | ) | (180 | ) | ||||||||||||||||||||||||||||||||

|

Issuance of common shares for stock plans, net of repurchases |

(34,931 | ) | 34,931 | (3 | ) | (3 | ) | |||||||||||||||||||||||||||||

|

Other comprehensive income |

2 | 2 | ||||||||||||||||||||||||||||||||||

|

BALANCE AS OF SEPTEMBER 30, 2013 |

292,928,355 | $ | 32 | $ | 4,990 | $ | 8,285 | 23,154,241 | $(1,034 | ) | $(61 | ) | $(46 | ) | $12,166 | |||||||||||||||||||||

The accompanying notes are an integral part of these financial statements.

| 11 |

Table of Contents

|

Consolidated Edison Company of New York, Inc. CONSOLIDATED INCOME STATEMENT (UNAUDITED) |

|

For the Three Months

Ended September 30, |

For the Nine Months

Ended September 30, |

|||||||||||||||

| 2013 | 2012 | 2013 | 2012 | |||||||||||||

| (Millions of Dollars) | ||||||||||||||||

|

OPERATING REVENUES |

||||||||||||||||

|

Electric |

$ | 2,622 | $ | 2,611 | $ | 6,309 | $ | 6,307 | ||||||||

|

Gas |

199 | 189 | 1,190 | 1,017 | ||||||||||||

|

Steam |

72 | 68 | 522 | 414 | ||||||||||||

|

TOTAL OPERATING REVENUES |

2,893 | 2,868 | 8,021 | 7,738 | ||||||||||||

|

OPERATING EXPENSES |

||||||||||||||||

|

Purchased power |

624 | 604 | 1,548 | 1,554 | ||||||||||||

|

Fuel |

56 | 59 | 261 | 213 | ||||||||||||

|

Gas purchased for resale |

58 | 45 | 376 | 264 | ||||||||||||

|

Other operations and maintenance |

686 | 725 | 2,102 | 2,065 | ||||||||||||

|

Depreciation and amortization |

237 | 225 | 705 | 664 | ||||||||||||

|

Taxes, other than income taxes |

480 | 456 | 1,370 | 1,300 | ||||||||||||

|

TOTAL OPERATING EXPENSES |

2,141 | 2,114 | 6,362 | 6,060 | ||||||||||||

|

OPERATING INCOME |

752 | 754 | 1,659 | 1,678 | ||||||||||||

|

OTHER INCOME (DEDUCTIONS) |

||||||||||||||||

|

Investment and other income |

1 | 2 | 7 | 6 | ||||||||||||

|

Allowance for equity funds used during construction |

1 | — | 1 | 2 | ||||||||||||

|

Other deductions |

(3 | ) | (2 | ) | (10 | ) | (10 | ) | ||||||||

|

TOTAL OTHER INCOME (DEDUCTIONS) |

(1 | ) | — | (2 | ) | (2 | ) | |||||||||

|

INCOME BEFORE INTEREST AND INCOME TAX EXPENSE |

751 | 754 | 1,657 | 1,676 | ||||||||||||

|

INTEREST EXPENSE |

||||||||||||||||

|

Interest on long-term debt |

127 | 130 | 384 | 395 | ||||||||||||

|

Other interest |

1 | 8 | 12 | 19 | ||||||||||||

|

Allowance for borrowed funds used during construction |

— | — | (1 | ) | (1 | ) | ||||||||||

|

NET INTEREST EXPENSE |

128 | 138 | 395 | 413 | ||||||||||||

|

INCOME BEFORE INCOME TAX EXPENSE |

623 | 616 | 1,262 | 1,263 | ||||||||||||

|

INCOME TAX EXPENSE |

222 | 227 | 431 | 436 | ||||||||||||

|

NET INCOME |

401 | 389 | 831 | 827 | ||||||||||||

|

Preferred stock dividend requirements |

— | — | — | (3 | ) | |||||||||||

|

NET INCOME FOR COMMON STOCK |

$ | 401 | $ | 389 | $ | 831 | $ | 824 | ||||||||

The accompanying notes are an integral part of these financial statements.

| 12 |

Table of Contents

|

Consolidated Edison Company of New York, Inc. CONSOLIDATED STATEMENT OF COMPREHENSIVE INCOME (UNAUDITED) |

|

For the Three Month

Ended September 30, |

For the Nine Months

Ended September 30, |

|||||||||||||||

| 2013 | 2012 | 2013 | 2012 | |||||||||||||

| (Millions of Dollars) | ||||||||||||||||

|

NET INCOME |

$ | 401 | $ | 389 | $ | 831 | $ | 827 | ||||||||

|

OTHER COMPREHENSIVE INCOME/(LOSS), NET OF TAXES |

||||||||||||||||

|

Pension plan liability adjustments, net of $(1) taxes in 2012 |

— | — | — | (2 | ) | |||||||||||

|

TOTAL OTHER COMPREHENSIVE INCOME, NET OF TAXES |

— | — | — | (2 | ) | |||||||||||

|

COMPREHENSIVE INCOME |

$ | 401 | $ | 389 | $ | 831 | $ | 825 | ||||||||

The accompanying notes are an integral part of these financial statements.

| 13 |

Table of Contents

|

Consolidated Edison Company of New York, Inc. CONSOLIDATED STATEMENT OF CASH FLOWS (UNAUDITED) |

|

For the Nine Months

Ended September 30, |

||||||||

| 2013 | 2012 | |||||||

| (Millions of Dollars) | ||||||||

|

OPERATING ACTIVITIES |

||||||||

|

Net income |

$ | 831 | $ | 827 | ||||

|

PRINCIPAL NON-CASH CHARGES/(CREDITS) TO INCOME |

||||||||

|

Depreciation and amortization |

705 | 664 | ||||||

|

Deferred income taxes |

364 | 220 | ||||||

|

Rate case amortization and accruals |

1 | 32 | ||||||

|

Common equity component of allowance for funds used during construction |

(1 | ) | (2 | ) | ||||

|

Other non-cash items (net) |

(72 | ) | 84 | |||||

|

CHANGES IN ASSETS AND LIABILITIES |

||||||||

|

Accounts receivable—customers, less allowance for uncollectibles |

(39 | ) | (197 | ) | ||||

|

Materials and supplies, including fuel oil and gas in storage |

(26 | ) | 12 | |||||

|

Other receivables and other current assets |

(27 | ) | (41 | ) | ||||

|

Prepayments |

(347 | ) | (308 | ) | ||||

|

Accounts payable |

(180 | ) | 50 | |||||

|

Pensions and retiree benefits obligations |

616 | 639 | ||||||

|

Pensions and retiree benefits contributions |

(830 | ) | (761 | ) | ||||

|

Superfund and environmental remediation costs (net) |

(6 | ) | 7 | |||||

|

Accrued taxes |

(92 | ) | 40 | |||||

|

Accrued interest |

43 | 46 | ||||||

|

Deferred charges, noncurrent assets and other regulatory assets |

63 | 84 | ||||||

|

Deferred credits and other regulatory liabilities |

302 | 88 | ||||||

|

Other liabilities |

64 | (21 | ) | |||||

|

NET CASH FLOWS FROM OPERATING ACTIVITIES |

1,369 | 1,463 | ||||||

|

INVESTING ACTIVITIES |

||||||||

|

Utility construction expenditures |

(1,614 | ) | (1,368 | ) | ||||

|

Cost of removal less salvage |

(139 | ) | (115 | ) | ||||

|

NET CASH FLOWS USED IN INVESTING ACTIVITIES |

(1,753 | ) | (1,483 | ) | ||||

|

FINANCING ACTIVITIES |

||||||||

|

Net proceeds of short-term debt |

621 | 332 | ||||||

|

Preferred stock redemption |

— | (239 | ) | |||||

|

Issuance of long-term debt |

700 | 400 | ||||||

|

Retirement of long-term debt |

(700 | ) | (300 | ) | ||||

|

Debt issuance costs |

(7 | ) | (4 | ) | ||||

|

Dividend to parent |

(545 | ) | (512 | ) | ||||

|

Preferred stock dividends |

— | (3 | ) | |||||

|

NET CASH FLOWS FROM (USED IN) FINANCING ACTIVITIES |

69 | (326 | ) | |||||

|

CASH AND TEMPORARY CASH INVESTMENTS: |

||||||||

|

NET CHANGE FOR THE PERIOD |

(315 | ) | (346 | ) | ||||

|

BALANCE AT BEGINNING OF PERIOD |

353 | 372 | ||||||

|

BALANCE AT END OF PERIOD |

$ | 38 | $ | 26 | ||||

|

SUPPLEMENTAL DISCLOSURE OF CASH FLOW INFORMATION |

||||||||

|

Cash paid during the period for: |

||||||||

|

Interest |

$ | 336 | $ | 344 | ||||

|

Income taxes |

$ | 117 | $ | 50 | ||||

The accompanying notes are an integral part of these financial statements.

| 14 |

Table of Contents

|

Consolidated Edison Company of New York, Inc. CONSOLIDATED BALANCE SHEET (UNAUDITED) |

|

September 30,

2013 |

December 31,

2012 |

|||||||

| (Millions of Dollars) | ||||||||

|

ASSETS |

||||||||

|

CURRENT ASSETS |

||||||||

|

Cash and temporary cash investments |

$ | 38 | $ | 353 | ||||

|

Special deposits |

86 | 65 | ||||||

|

Accounts receivable – customers, less allowance for uncollectible accounts of $89 and $87 in 2013 and 2012, respectively |

1,147 | 1,108 | ||||||

|

Other receivables, less allowance for uncollectible accounts of $6 and $9 in 2013 and 2012, respectively |

142 | 106 | ||||||

|

Accrued unbilled revenue |

329 | 406 | ||||||

|

Accounts receivable from affiliated companies |

35 | 61 | ||||||

|

Fuel oil, gas in storage, materials and supplies, at average cost |

311 | 285 | ||||||

|

Prepayments |

428 | 81 | ||||||

|

Regulatory assets |

42 | 60 | ||||||

|

Deferred tax assets – current |

123 | 193 | ||||||

|

Other current assets |

60 | 69 | ||||||

|

TOTAL CURRENT ASSETS |

2,741 | 2,787 | ||||||

|

INVESTMENTS |

231 | 207 | ||||||

|

UTILITY PLANT AT ORIGINAL COST |

||||||||

|

Electric |

21,680 | 21,079 | ||||||

|

Gas |

4,794 | 4,547 | ||||||

|

Steam |

2,117 | 2,049 | ||||||

|

General |

2,123 | 2,126 | ||||||

|

TOTAL |

30,714 | 29,801 | ||||||

|

Less: Accumulated depreciation |

6,357 | 6,009 | ||||||

|

Net |

24,357 | 23,792 | ||||||

|

Construction work in progress |

1,373 | 947 | ||||||

|

NET UTILITY PLANT |

25,730 | 24,739 | ||||||

|

NON-UTILITY PROPERTY |

||||||||

|

Non-utility property, less accumulated depreciation of $25 in 2013 and 2012 |

5 | 6 | ||||||

|

NET PLANT |

25,735 | 24,745 | ||||||

|

OTHER NONCURRENT ASSETS |

||||||||

|

Regulatory assets |

8,497 | 8,972 | ||||||

|

Other deferred charges and noncurrent assets |

171 | 174 | ||||||

|

TOTAL OTHER NONCURRENT ASSETS |

8,668 | 9,146 | ||||||

|

TOTAL ASSETS |

$ | 37,375 | $ | 36,885 | ||||

The accompanying notes are an integral part of these financial statements.

| 15 |

Table of Contents

|

Consolidated Edison Company of New York, Inc. CONSOLIDATED BALANCE SHEET (UNAUDITED) |

|

September 30,

2013 |

December 31,

2012 |

|||||||

| (Millions of Dollars) | ||||||||

|

LIABILITIES AND SHAREHOLDER’S EQUITY |

||||||||

|

CURRENT LIABILITIES |

||||||||

|

Long-term debt due within one year |

$ | 475 | $ | 700 | ||||

|

Notes payable |

1,042 | 421 | ||||||

|

Accounts payable |

737 | 989 | ||||||

|

Accounts payable to affiliated companies |

16 | 22 | ||||||

|

Customer deposits |

304 | 292 | ||||||

|

Accrued taxes |

20 | 37 | ||||||

|

Accrued taxes to affiliated companies |

140 | 215 | ||||||

|

Accrued interest |

176 | 133 | ||||||

|

Accrued wages |

89 | 84 | ||||||

|

Fair value of derivative liabilities |

19 | 28 | ||||||

|

Uncertain income tax liabilities |

— | 36 | ||||||

|

Regulatory liabilities |

86 | 145 | ||||||

|

Other current liabilities |

419 | 410 | ||||||

|

TOTAL CURRENT LIABILITIES |

3,523 | 3,512 | ||||||

|

NONCURRENT LIABILITIES |

||||||||

|

Obligations under capital leases |

2 | 2 | ||||||

|

Provision for injuries and damages |

188 | 141 | ||||||

|

Pensions and retiree benefits |

3,414 | 4,220 | ||||||

|

Superfund and other environmental costs |

403 | 433 | ||||||

|

Asset retirement obligations |

163 | 158 | ||||||

|

Fair value of derivative liabilities |

7 | 11 | ||||||

|

Other noncurrent liabilities |

109 | 115 | ||||||

|

TOTAL NONCURRENT LIABILITIES |

4,286 | 5,080 | ||||||

|

DEFERRED CREDITS AND REGULATORY LIABILITIES |

||||||||

|

Deferred income taxes and investment tax credits |

7,888 | 7,452 | ||||||

|

Regulatory liabilities |

1,431 | 1,077 | ||||||

|

Other deferred credits |

43 | 67 | ||||||

|

TOTAL DEFERRED CREDITS AND REGULATORY LIABILITIES |

9,362 | 8,596 | ||||||

|

LONG-TERM DEBT |

9,366 | 9,145 | ||||||

|

COMMON SHAREHOLDER’S EQUITY (See Statement of Common Shareholder’s Equity) |

10,838 | 10,552 | ||||||

|

TOTAL LIABILITIES AND SHAREHOLDER’S EQUITY |

$ | 37,375 | $ | 36,885 | ||||

The accompanying notes are an integral part of these financial statements.

| 16 |

Table of Contents

|

Consolidated Edison Company of New York, Inc. CONSOLIDATED STATEMENT OF COMMON SHAREHOLDER’S EQUITY (UNAUDITED) |

||

| Common Stock |

Additional

|

Retained

|

Repurchased

|

Capital

|

Accumulated

Other Comprehensive Income/(Loss) |

Total |

||||||||||||||||||||||||||

| (Millions of Dollars/Except Share Data) | Shares | Amount | ||||||||||||||||||||||||||||||

|

BALANCE AS OF DECEMBER 31, 2011 |

235,488,094 | $ | 589 | $ | 4,234 | $ | 6,429 | $ | (962) | $ | (64) | $ | (8 | ) | $ | 10,218 | ||||||||||||||||

|

Net income |

276 | 276 | ||||||||||||||||||||||||||||||

|

Common stock dividend to parent |

(171 | ) | (171 | ) | ||||||||||||||||||||||||||||

|

Cumulative preferred dividends |

(3 | ) | (3 | ) | ||||||||||||||||||||||||||||

|

Preferred stock redemption |

4 | 4 | ||||||||||||||||||||||||||||||

|

Other comprehensive income |

— | — | ||||||||||||||||||||||||||||||

|

BALANCE AS OF MARCH 31, 2012 |

235,488,094 | $ | 589 | $ | 4,234 | $ | 6,531 | $ | (962) | $ | (60) | $ | (8 | ) | $ | 10,324 | ||||||||||||||||

|

Net income |

163 | 163 | ||||||||||||||||||||||||||||||

|

Common stock dividend to parent |

(171 | ) | (171 | ) | ||||||||||||||||||||||||||||

|

Other comprehensive loss |

(2 | ) | (2 | ) | ||||||||||||||||||||||||||||

|

BALANCE AS OF JUNE 30, 2012 |

235,488,094 | $ | 589 | $ | 4,234 | $ | 6,523 | $ | (962) | $ | (60) | $ | (10 | ) | $ | 10,314 | ||||||||||||||||

|

Net income |

389 | 389 | ||||||||||||||||||||||||||||||

|

Common stock dividend to parent |

(171 | ) | (171 | ) | ||||||||||||||||||||||||||||

|

Cumulative preferred dividends |

— | — | ||||||||||||||||||||||||||||||

|

Other comprehensive loss |

— | — | ||||||||||||||||||||||||||||||

|

BALANCE AS OF SEPTEMBER 30, 2012 |

235,488,094 | $ | 589 | $ | 4,234 | $ | 6,741 | $ | (962) | $ | (60) | $ | (10 | ) | $ | 10,532 | ||||||||||||||||

|

BALANCE AS OF DECEMBER 31, 2012 |

235,488,094 | $ | 589 | $ | 4,234 | $ | 6,761 | $ | (962) | $ | (61) | $ | (9 | ) | $ | 10,552 | ||||||||||||||||

|

Net income |

277 | 277 | ||||||||||||||||||||||||||||||

|

Common stock dividend to parent |

(182 | ) | (182 | ) | ||||||||||||||||||||||||||||

|

Other comprehensive income |

— | — | ||||||||||||||||||||||||||||||

|

BALANCE AS OF MARCH 31, 2013 |

235,488,094 | $ | 589 | $ | 4,234 | $ | 6,856 | $ | (962 | ) | $ | (61 | ) | $ | (9 | ) | $ | 10,647 | ||||||||||||||

|

Net income |

153 | 153 | ||||||||||||||||||||||||||||||

|

Common stock dividend to parent |

(182 | ) | (182 | ) | ||||||||||||||||||||||||||||

|

Other comprehensive income |

— | — | ||||||||||||||||||||||||||||||

|

BALANCE AS OF JUNE 30, 2013 |

$ | 235,488,094 | $ | 589 | $ | 4,234 | $ | 6,827 | $ | (962 | ) | $ | (61 | ) | $ | (9 | ) | $ | 10,618 | |||||||||||||

|

Net income |

401 | 401 | ||||||||||||||||||||||||||||||

|

Common stock dividend to parent |

(181 | ) | (181 | ) | ||||||||||||||||||||||||||||

|

Other comprehensive income |

— | — | ||||||||||||||||||||||||||||||

|

BALANCE AS OF SEPTEMBER 30, 2013 |

$ | 235,488,094 | $ | 589 | $ | 4,234 | $ | 7,047 | $ | (962 | ) | $ | (61 | ) | $ | (9 | ) | $ | 10,838 | |||||||||||||

The accompanying notes are an integral part of these financial statements.

| 17 |

Table of Contents

NOTES TO THE FINANCIAL STATEMENTS (UNAUDITED)

General

These combined notes accompany and form an integral part of the separate consolidated financial statements of each of the two separate registrants: Consolidated Edison, Inc. and its subsidiaries (Con Edison) and Consolidated Edison Company of New York, Inc. and its subsidiaries (CECONY). CECONY is a subsidiary of Con Edison and as such its financial condition and results of operations and cash flows, which are presented separately in the CECONY consolidated financial statements, are also consolidated, along with those of Con Edison’s other utility subsidiary, Orange and Rockland Utilities, Inc. (O&R), and Con Edison’s competitive energy businesses (discussed below) in Con Edison’s consolidated financial statements. The term “Utilities” is used in these notes to refer to CECONY and O&R.

As used in these notes, the term “Companies” refers to Con Edison and CECONY and, except as otherwise noted, the information in these combined notes relates to each of the Companies. However, CECONY makes no representation as to information relating to Con Edison or the subsidiaries of Con Edison other than itself.

The separate interim consolidated financial statements of each of the Companies are unaudited but, in the opinion of their respective managements, reflect all adjustments (which include only normally recurring adjustments) necessary for a fair presentation of the results for the interim periods presented. The Companies’ separate interim consolidated financial statements should be read together with their separate audited financial statements (including the combined notes thereto) included in Item 8 of their combined Annual Report on Form 10-K for the year ended December 31, 2012 and their separate unaudited financial statements (including the combined notes thereto) included in Part I, Item 1 of their combined Quarterly Reports on Form 10-Q for the quarterly periods ended March 31, 2013 and June 30, 2013.

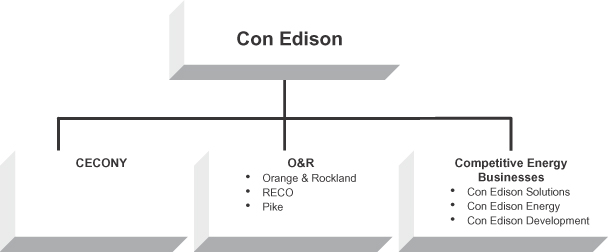

Con Edison has two regulated utility subsidiaries: CECONY and O&R. CECONY provides electric service and gas service in New York City and Westchester County. The company also provides steam service in parts of Manhattan. O&R, along with its regulated utility subsidiaries, provides electric service in southeastern New York and adjacent areas of northern New Jersey and eastern Pennsylvania and gas service in southeastern New York and adjacent areas of eastern Pennsylvania. Con Edison has the following competitive energy businesses: Consolidated Edison Solutions, Inc. (Con Edison Solutions), a retail energy services company that sells electricity and also offers energy-related services; Consolidated Edison Energy, Inc. (Con Edison Energy), a wholesale energy services company; and Consolidated Edison Development, Inc. (Con Edison Development), a company that develops and participates in infrastructure projects.

| 18 |

Table of Contents

Note A — Summary of Significant Accounting Policies

Reclassifications and Revisions

Prior period amounts have been reclassified where necessary to conform to the current period presentation.

Con Edison’s consolidated statement of cash flows for the six months ended June 30, 2013, incorrectly reduced net cash flows from financing activities and increased net cash flows from operating activities by an amount equal to the $108 million of net cash proceeds from the termination of the 1999 LILO transaction. A revision will be made on Con Edison’s consolidated statement of cash flows for the six months ended June 30, 2013 when the company files its Form 10-Q for the quarterly period ended June 30, 2014. The company does not deem this revision material to its consolidated financial statements for the six months ended June 30, 2013.

Earnings Per Common Share

For the three and nine months ended September 30, 2013 and 2012, basic and diluted earnings per share (EPS) for Con Edison are calculated as follows:

|

For the Three Months

Ended September 30, |

For the Nine Months

Ended September 30, |

|||||||||||||||

| (Millions of Dollars, except per share amounts/Shares in Millions) | 2013 | 2012 | 2013 | 2012 | ||||||||||||

|

Net income for common stock |

$ | 464 | $ | 440 | $ | 828 | $ | 931 | ||||||||

|

Weighted average common shares outstanding – basic |

292.9 | 292.9 | 292.9 | 292.9 | ||||||||||||

|

Add: Incremental shares attributable to effect of potentially dilutive securities |

1.4 | 1.7 | 1.4 | 1.7 | ||||||||||||

|

Adjusted weighted average common shares outstanding – diluted |

294.3 | 294.6 | 294.3 | 294.6 | ||||||||||||

|

Net income for common stock per common share – basic |

$ | 1.58 | $ | 1.50 | $ | 2.83 | $ | 3.18 | ||||||||

|

Net income for common stock per common share – diluted |

$ | 1.58 | $ | 1.49 | $ | 2.81 | $ | 3.16 | ||||||||

The computation of diluted EPS for the three and nine months ended September 30, 2013 and 2012 excludes immaterial amounts of performance share awards which were not included because of their anti-dilutive effect.

Changes in Accumulated Other Comprehensive Income by Component

For the three and nine months ended September 30, 2013, changes to accumulated other comprehensive income (OCI) for Con Edison and CECONY are as follows:

| (Millions of Dollars) | Con Edison | CECONY | ||||||

|

Accumulated OCI, net of taxes, at December 31, 2012 |

$ | (53 | ) | $ | (9 | ) | ||

|

OCI before reclassifications, net of tax of $1 and $- for Con Edison and CECONY, respectively |

1 | — | ||||||

|

Amounts reclassified from accumulated OCI related to pension plan liabilities, net of tax of $1 and $- for Con Edison and CECONY, respectively (a)(b) |

2 | — | ||||||

|

Total OCI, net of taxes, at March 31, 2013 |

$ | 3 | $ | — | ||||

|

Accumulated OCI, net of taxes, at March 31, 2013 (b) |

$ | (50 | ) | $ | (9 | ) | ||

|

OCI before reclassifications |

— | — | ||||||

|

Amounts reclassified from accumulated OCI related to pension plan liabilities, net of tax of $1 and $- for Con Edison and CECONY, respectively (a)(b) |

2 | — | ||||||

|

Total OCI, net of taxes, at June 30, 2013 |

$ | 2 | $ | — | ||||

|

Accumulated OCI, net of taxes, at June 30, 2013 (b) |

$ | (48 | ) | $ | (9 | ) | ||

|

OCI before reclassifications |

— | — | ||||||

|

Amounts reclassified from accumulated OCI related to pension plan liabilities, net of tax of $1 and $- for Con Edison and CECONY, respectively (a)(b) |

2 | — | ||||||

|

Total OCI, net of taxes, at September 30, 2013 |

$ | 2 | $ | — | ||||

|

Accumulated OCI, net of taxes, at September 30, 2013 (b) |

$ | (46 | ) | $ | (9 | ) | ||

| (a) | For the portion of unrecognized pension and other postretirement benefit costs relating to the regulated Utilities, costs are recorded into, and amortized out of, regulatory assets instead of OCI. The net actuarial losses and prior service costs recognized during the period are included in the computation of net periodic pension and other postretirement benefit cost. See Notes E and F. |

| (b) | Tax reclassified from accumulated OCI is reported in the income tax expense line item of the income statement. |

| 19 |

Table of Contents

Note B — Regulatory Matters

Rate Agreements

CECONY – Electric, Gas and Steam

In January 2013, CECONY filed requests for electric, gas and steam rate changes, effective January 1, 2014. The company requested electric and gas rate increases of $375 million and $25 million, respectively, and a steam rate decrease of $5 million, reflecting, among other things, a return on common equity of 10.35 percent and a common equity ratio of approximately 50 percent. In August 2013, the New York State Public Service Commission (NYSPSC) staff submitted its initial briefs which support decreases in the company’s electric, gas and steam rates of $146 million, $95 million and $10 million, respectively, reflecting, among other things, a return on common equity of 8.7 percent and a common equity ratio of 48 percent. In September 2013, the company submitted its reply briefs supporting increases in its electric, gas and steam rates of $418 million, $27 million and $8 million, respectively, reflecting, among other things, a return on common equity of 10.1 percent and a common equity ratio of approximately 50 percent. In October 2013, the NYSPSC’s Chief Administrative Law Judge appointed a settlement judge to assist in settlement discussions among the parties in these rate proceedings. There is no assurance that there will be a settlement, and any settlement would be subject to NYSPSC approval. Also, in October 2013, the company agreed to extend by one month the date by which the NYSPSC is required to issue a decision on the company’s rate requests, subject to a “make whole” provision that would keep the company and its customers in the same position they would have been absent the extension.

Other Regulatory Matters

In February 2009, the NYSPSC commenced a proceeding to examine the prudence of certain CECONY expenditures following the arrests of employees for accepting illegal payments from a construction contractor. Subsequently, additional employees were arrested for accepting illegal payments from materials suppliers and an engineering firm. The arrested employees were terminated by the company and have pled guilty or been convicted. Pursuant to NYSPSC orders, a portion of the company’s revenues (currently, $249 million, $32 million and $6 million on an annual basis for electric, gas and steam service, respectively) is being collected subject to potential refund to customers. The amount of electric revenues collected subject to refund, which was established in a different proceeding, and the amount of gas and steam revenues collected subject to refund were not established as indicative of the company’s potential liability in this proceeding. At September 30, 2013, the company had collected an estimated $1,318 million from customers subject to potential refund in connection with this proceeding. In January 2013, a NYSPSC consultant reported its estimate, with which the company does not agree, of $208 million of overcharges with respect to a substantial portion of the company’s construction expenditures from January 2000 to January 2009. The company is disputing the consultant’s estimate, including its determinations as to overcharges regarding specific construction expenditures it selected to review and its methodology of extrapolating such determinations over a substantial portion of the construction expenditures

| 20 |

Table of Contents

during this period. The NYSPSC’s consultant has not reviewed the company’s other expenditures. The company and NYSPSC staff are exploring a settlement in this proceeding. There is no assurance that there will be a settlement, and any settlement would be subject to NYSPSC approval. At September 30, 2013, the company had a $16 million regulatory liability for refund to customers of amounts recovered from vendors, arrested employees and insurers relating to this matter. The company is unable to estimate the amount, if any, by which any refund required by the NYSPSC may exceed this regulatory liability. The company currently estimates that any refund required by the NYSPSC could range in amount from the $16 million regulatory liability up to an amount based on the NYSPSC consultant’s $208 million estimate of overcharges.

In late October 2012, Superstorm Sandy caused extensive damage to the Utilities’ electric distribution system and interrupted service to approximately 1.4 million customers. Superstorm Sandy also damaged CECONY’s steam system and interrupted service to many of its steam customers. As of September 30, 2013, CECONY and O&R incurred response and restoration costs for Superstorm Sandy of $471 million and $92 million, respectively (including capital expenditures of $143 million and $15 million, respectively). Most of the costs that were not capitalized were deferred for recovery as a regulatory asset under the Utilities’ electric rate plans. See “Regulatory Assets and Liabilities,” below. The Utilities’ New York electric rate plans include provisions for revenue decoupling, as a result of which delivery revenues generally are not affected by changes in delivery volumes from levels assumed when rates were approved. The provisions of the Utilities’ New York electric plans that impose penalties for operating performance provide for exceptions for major storms and catastrophic events beyond the control of the companies, including natural disasters such as hurricanes and floods. The NYSPSC is investigating, and the New York State Attorney General investigated, the preparation and performance of the Utilities in connection with Superstorm Sandy and other major storms.

In June 2013, a commission appointed by the Governor of New York issued its final report on utility storm preparation and response. The commission identified deficiencies in the performance of the Utilities and other New York utilities and made recommendations regarding, among other things, preparation and response to flooding; estimation of customer restoration times; reliability of website outage maps; coordination with local governments and providers of other utility services; availability and allocation of staffing and other resources (including the utility industry’s mutual aid process); and communications with affected communities and local officials. The commission’s report also addressed the Long Island Power Authority, energy efficiency programs, utility infrastructure investment and regulatory deficiencies.

In March 2013, the New Jersey Board of Public Utilities established a proceeding to review the prudency of costs incurred by New Jersey utilities, including Rockland Electric Company (RECO, an O&R subsidiary), in response to major storm events in 2011 and 2012. At September 30, 2013, RECO had $28 million of storm costs deferred for recovery as a regulatory asset and had incurred $6 million of capital expenditures related to the storms.

| 21 |

Table of Contents

Regulatory Assets and Liabilities

Regulatory assets and liabilities at September 30, 2013 and December 31, 2012 were comprised of the following items:

| Con Edison | CECONY | |||||||||||||||

| (Millions of Dollars) | 2013 | 2012 | 2013 | 2012 | ||||||||||||

|

Regulatory assets |

||||||||||||||||

|

Unrecognized pension and other postretirement costs |

$5,011 | $5,677 | $4,779 | $5,407 | ||||||||||||

|

Future income tax |

2,035 | 1,922 | 1,929 | 1,831 | ||||||||||||

|

Environmental remediation costs |

704 | 730 | 591 | 615 | ||||||||||||

|

Deferred storm costs |

451 | 432 | 340 | 309 | ||||||||||||

|

Pension and other postretirement benefits deferrals |

229 | 183 | 201 | 154 | ||||||||||||

|

Revenue taxes |

191 | 176 | 182 | 170 | ||||||||||||

|

Surcharge for New York State assessment |

119 | 73 | 113 | 68 | ||||||||||||

|

Net electric deferrals |

88 | 102 | 88 | 102 | ||||||||||||

|

Unamortized loss on reacquired debt |

67 | 74 | 64 | 70 | ||||||||||||

|

Deferred derivative losses – long-term |

34 | 40 | 13 | 20 | ||||||||||||

|

O&R transition bond charges |

34 | 39 | — | — | ||||||||||||

|

Preferred stock redemption |

28 | 29 | 28 | 29 | ||||||||||||

|

Property tax reconciliation |

20 | 16 | — | — | ||||||||||||

|

Workers’ compensation |

16 | 19 | 16 | 19 | ||||||||||||

|

Other |

163 | 193 | 153 | 178 | ||||||||||||

|

Regulatory assets – long-term |

9,190 | 9,705 | 8,497 | 8,972 | ||||||||||||

|

Deferred derivative losses – current |

45 | 69 | 42 | 60 | ||||||||||||

|

Recoverable energy costs – current |

1 | 5 | — | — | ||||||||||||

|

Regulatory assets – current |

46 | 74 | 42 | 60 | ||||||||||||

|

Total Regulatory Assets |

$9,236 | $9,779 | $8,539 | $9,032 | ||||||||||||

|

Regulatory liabilities |

||||||||||||||||

|

Allowance for cost of removal less salvage |

$ 522 | $ 503 | $ 436 | $ 420 | ||||||||||||

|

Property tax reconciliation |

290 | 187 | 290 | 187 | ||||||||||||

|

Property tax refunds |

130 | 7 | 129 | 6 | ||||||||||||

|

Net unbilled revenue deferrals |

104 | 136 | 104 | 136 | ||||||||||||

|

Long-term interest rate reconciliation |

94 | 62 | 94 | 62 | ||||||||||||

|

World Trade Center settlement proceeds |

62 | 62 | 62 | 62 | ||||||||||||

|

Carrying charges on T&D net plant – electric and steam |

30 | 31 | 20 | 13 | ||||||||||||

|

Expenditure prudence proceeding |

16 | 14 | 16 | 14 | ||||||||||||

|

Other |

309 | 200 | 280 | 177 | ||||||||||||

|

Regulatory liabilities – long-term |

1,557 | 1,202 | 1,431 | 1,077 | ||||||||||||

|

Refundable energy costs – current |

64 | 82 | 36 | 48 | ||||||||||||

|

Revenue decoupling mechanism |

51 | 72 | 49 | 68 | ||||||||||||

|

Deferred derivative gains – current |

2 | — | 1 | — | ||||||||||||

|

Electric surcharge offset |

— | 29 | — | 29 | ||||||||||||

|

Regulatory liabilities – current |

117 | 183 | 86 | 145 | ||||||||||||

|

Total Regulatory Liabilities |

$1,674 | $1,385 | $1,517 | $1,222 | ||||||||||||

“Deferred storm costs” represent response and restoration costs, other than capital expenditures, in connection with Superstorm Sandy and other major storms that were deferred by the Utilities. See “Other Regulatory Matters,” above.

| 22 |

Table of Contents

Note C — Capitalization

In February 2013, CECONY issued $700 million aggregate principal amount of 3.95 percent 30-year debentures and redeemed at maturity $500 million of 4.875 percent 10-year debentures. In June 2013, CECONY redeemed at maturity $200 million of 3.85 percent 10-year debentures. In April 2013, a Con Edison Development subsidiary issued $219 million aggregate principal amount of 4.78 percent senior notes secured by the company’s California solar energy projects. The notes have a weighted average life of 15 years and final maturity of 2037.

The carrying amounts and fair values of long-term debt are:

| (Millions of Dollars) | September 30, 2013 | December 31, 2012 | ||||||||||||||

| Long-Term Debt (including current portion) |

Carrying Amount |

Fair

Value |

Carrying Amount |

Fair

Value |

||||||||||||

|

Con Edison |

$10,976 | $12,213 | $10,768 | $12,935 | ||||||||||||

|

CECONY |

$ 9,841 | $10,925 | $ 9,845 | $11,751 | ||||||||||||

Fair values of long-term debt have been estimated primarily using available market information. For Con Edison, $11,577 million and $636 million of the fair value of long-term debt at September 30, 2013 are classified as Level 2 and Level 3, respectively. For CECONY, $10,289 million and $636 million of the fair value of long-term debt at September 30, 2013 are classified as Level 2 and Level 3, respectively (see Note L). The $636 million of long-term debt classified as Level 3 is CECONY’s tax-exempt, auction-rate securities for which the market is highly illiquid and there is a lack of observable inputs.

Note D — Short-Term Borrowing

At September 30, 2013, Con Edison had $1,220 million of commercial paper outstanding of which $1,042 million was outstanding under CECONY’s program. The weighted average interest rate was 0.3 percent for both Con Edison and CECONY. At December 31, 2012, Con Edison had $539 million of commercial paper outstanding of which $421 million was outstanding under CECONY’s program. The weighted average interest rate was 0.3 percent for both Con Edison and CECONY. At September 30, 2013 and December 31, 2012, no loans were outstanding under the Companies’ credit agreement and $29 million (including $11 million for CECONY) and $131 million (including $121 million for CECONY) of letters of credit were outstanding, respectively, under the credit agreement. In 2013, the termination date under the credit agreement was extended from October 2016 to October 2017 with respect to lenders with aggregate commitments under the credit agreement of approximately $2.1 billion.

| 23 |

Table of Contents

Note E — Pension Benefits

Net Periodic Benefit Cost

The components of the Companies’ net periodic benefit costs for the three and nine months ended September 30, 2013 and 2012 were as follows:

| For the Three Months Ended September 30, | ||||||||||||||||

| Con Edison | CECONY | |||||||||||||||

| (Millions of Dollars) | 2013 | 2012 | 2013 | 2012 | ||||||||||||

|

Service cost – including administrative expenses |

$ 67 | $ 59 | $ 62 | $ 55 | ||||||||||||

|

Interest cost on projected benefit obligation |

134 | 137 | 126 | 128 | ||||||||||||

|

Expected return on plan assets |

(187 | ) | (176 | ) | (178 | ) | (168 | ) | ||||||||

|

Recognition of net actuarial loss |

208 | 177 | 197 | 168 | ||||||||||||

|

Recognition of prior service costs |

1 | 2 | 1 | 2 | ||||||||||||

|

NET PERIODIC BENEFIT COST |

$ 223 | $ 199 | $ 208 | $ 185 | ||||||||||||

|

Amortization of regulatory asset |

1 | — | 1 | — | ||||||||||||

|

TOTAL PERIODIC BENEFIT COST |

$ 224 | $ 199 | $ 209 | $ 185 | ||||||||||||

|

Cost capitalized |

(86 | ) | (64 | ) | (78 | ) | (60 | ) | ||||||||

|

Reconciliation to rate level |

(31 | ) | — | (34 | ) | (1 | ) | |||||||||

|

Cost charged to operating expenses |

$ 107 | $ 135 | $ 97 | $ 124 | ||||||||||||

| For the Nine Months Ended September 30, | ||||||||||||||||

| Con Edison | CECONY | |||||||||||||||

| (Millions of Dollars) | 2013 | 2012 | 2013 | 2012 | ||||||||||||

|

Service cost – including administrative expenses |

$ 200 | $ 177 | $ 186 | $ 165 | ||||||||||||

|

Interest cost on projected benefit obligation |

403 | 410 | 377 | 385 | ||||||||||||

|

Expected return on plan assets |

(563 | ) | (528 | ) | (534 | ) | (503 | ) | ||||||||

|

Recognition of net actuarial loss |

624 | 531 | 591 | 503 | ||||||||||||

|

Recognition of prior service costs |

4 | 6 | 3 | 4 | ||||||||||||

|

NET PERIODIC BENEFIT COST |

$ 668 | $ 596 | $ 623 | $ 554 | ||||||||||||

|

Amortization of regulatory asset |

2 | 1 | 2 | 1 | ||||||||||||

|

TOTAL PERIODIC BENEFIT COST |

$ 670 | $ 597 | $ 625 | $ 555 | ||||||||||||

|

Cost capitalized |

(256 | ) | (200 | ) | (241 | ) | (186 | ) | ||||||||

|

Reconciliation to rate level |

(55 | ) | (37 | ) | (56 | ) | (36 | ) | ||||||||

|

Cost charged to operating expenses |

$ 359 | $ 360 | $ 328 | $ 333 | ||||||||||||

Contributions

The Companies made contributions to the pension plan during 2013 of $867 million (of which $810 million was contributed by CECONY). The Companies’ policy is to fund their accounting cost to the extent tax deductible. During the first nine months of 2013, CECONY also funded $11 million for the non-qualified supplemental plans.

Note F — Other Postretirement Benefits

Net Periodic Benefit Cost

The components of the Companies’ net periodic postretirement benefit costs for the three and nine months ended September 30, 2013 and 2012 were as follows:

| For the Three Months Ended September 30, | ||||||||||||||||

| Con Edison | CECONY | |||||||||||||||

| (Millions of Dollars) | 2013 | 2012 | 2013 | 2012 | ||||||||||||

|

Service cost |

$ 6 | $ 6 | $ 5 | $ 5 | ||||||||||||

|

Interest cost on accumulated other postretirement benefit obligation |

13 | 18 | 12 | 16 | ||||||||||||

|

Expected return on plan assets |

(19 | ) | (21 | ) | (17 | ) | (19 | ) | ||||||||

|

Recognition of net actuarial loss |

16 | 24 | 14 | 22 | ||||||||||||

|

Recognition of prior service cost |

(7 | ) | (5 | ) | (6 | ) | (4 | ) | ||||||||

|

NET PERIODIC POSTRETIREMENT BENEFIT COST |

$ 9 | $ 22 | $ 8 | $ 20 | ||||||||||||

|

Cost capitalized |

(3 | ) | (8 | ) | (3 | ) | (7 | ) | ||||||||

|

Reconciliation to rate level |

14 | 3 | 12 | 3 | ||||||||||||

|

Cost charged to operating expenses |

$ 20 | $ 17 | $ 17 | $ 16 | ||||||||||||

| 24 |

Table of Contents

| For the Nine Months Ended September 30, | ||||||||||||||||

| Con Edison | CECONY | |||||||||||||||

| (Millions of Dollars) | 2013 | 2012 | 2013 | 2012 | ||||||||||||

|

Service cost |

$ 18 | $ 20 | $ 14 | $ 15 | ||||||||||||

|

Interest cost on accumulated other postretirement benefit obligation |

40 | 55 | 34 | 48 | ||||||||||||

|

Expected return on plan assets |

(58 | ) | (64 | ) | (51 | ) | (56 | ) | ||||||||

|

Recognition of net actuarial loss |

48 | 73 | 43 | 65 | ||||||||||||

|

Recognition of prior service cost |

(20 | ) | (16 | ) | (17 | ) | (13 | ) | ||||||||

|

Recognition of transition obligation |

— | 1 | — | 1 | ||||||||||||

|

NET PERIODIC POSTRETIREMENT BENEFIT COST |

$ 28 | $ 69 | $ 23 | $ 60 | ||||||||||||

|

Cost capitalized |

(10 | ) | (24 | ) | (9 | ) | (20 | ) | ||||||||

|

Reconciliation to rate level |

43 | 15 | 37 | 12 | ||||||||||||

|

Cost charged to operating expenses |

$ 61 | $ 60 | $ 51 | $ 52 | ||||||||||||

Contributions

Con Edison made a contribution of $9 million, nearly all of which is for CECONY, to the other postretirement benefit plans in 2013.

Note G — Environmental Matters

Superfund Sites

Hazardous substances, such as asbestos, polychlorinated biphenyls (PCBs) and coal tar, have been used or generated in the course of operations of the Utilities and their predecessors and are present at sites and in facilities and equipment they currently or previously owned, including sites at which gas was manufactured or stored.

The Federal Comprehensive Environmental Response, Compensation and Liability Act of 1980 and similar state statutes (Superfund) impose joint and several liability, regardless of fault, upon generators of hazardous substances for investigation and remediation costs (which include costs of demolition, removal, disposal, storage, replacement, containment, and monitoring) and natural resource damages. Liability under these laws can be material and may be imposed for contamination from past acts, even though such past acts may have been lawful at the time they occurred. The sites at which the Utilities have been asserted to have liability under these laws, including their manufactured gas plant sites and any neighboring areas to which contamination may have migrated, are referred to herein as “Superfund Sites.”

For Superfund Sites where there are other potentially responsible parties and the Utilities are not managing the site investigation and remediation, the accrued liability represents an estimate of the amount the Utilities will need to pay to investigate and, where

| 25 |

Table of Contents

determinable, discharge their related obligations. For Superfund Sites (including the manufactured gas plant sites) for which one of the Utilities is managing the investigation and remediation, the accrued liability represents an estimate of the company’s share of undiscounted cost to investigate the sites and, for sites that have been investigated in whole or in part, the cost to remediate the sites, if remediation is necessary and if a reasonable estimate of such cost can be made. Remediation costs are estimated in light of the information available, applicable remediation standards, and experience with similar sites.

The accrued liabilities and regulatory assets related to Superfund Sites at September 30, 2013 and December 31, 2012 were as follows:

| Con Edison | CECONY | |||||||||||||||

| (Millions of Dollars) | 2013 | 2012 | 2013 | 2012 | ||||||||||||

|

Accrued Liabilities: |

||||||||||||||||

|

Manufactured gas plant sites |

$439 | $462 | $332 | $351 | ||||||||||||

|

Other Superfund Sites |

73 | 83 | 71 | 82 | ||||||||||||

|

Total |

$512 | $545 | $403 | $433 | ||||||||||||

|

Regulatory assets |

$704 | $730 | $591 | $615 | ||||||||||||

Most of the accrued Superfund Site liability relates to sites that have been investigated, in whole or in part. However, for some of the sites, the extent and associated cost of the required remediation has not yet been determined. As investigations progress and information pertaining to the required remediation becomes available, the Utilities expect that additional liability may be accrued, the amount of which is not presently determinable but may be material. Under their current rate agreements, the Utilities are permitted to recover or defer as regulatory assets (for subsequent recovery through rates) certain site investigation and remediation costs.

Environmental remediation costs incurred and insurance recoveries received related to Superfund Sites for the three and nine months ended September 30, 2013 and 2012 were as follows:

| For the Three Months Ended September 30, | ||||||||||||||||

| Con Edison | CECONY | |||||||||||||||

| (Millions of Dollars) | 2013 | 2012 | 2013 | 2012 | ||||||||||||

|

Remediation costs incurred |

$10 | $3 | $10 | $1 | ||||||||||||

|

Insurance recoveries received |

— | — | — | — | ||||||||||||

| For the Nine Months Ended September 30, | ||||||||||||||||

| Con Edison | CECONY | |||||||||||||||

| (Millions of Dollars) | 2013 | 2012 | 2013 | 2012 | ||||||||||||

|

Remediation costs incurred |

$35 | $18 | $30 | $15 | ||||||||||||

|

Insurance recoveries received |

— | — | — | — | ||||||||||||

In 2010, CECONY estimated that for its manufactured gas plant sites, its aggregate undiscounted potential liability for the investigation and remediation of coal tar and/or other manufactured gas plant-related

| 26 |

Table of Contents

environmental contaminants could range up to $1.9 billion. In 2010, O&R estimated that for its manufactured gas plant sites, each of which has been investigated, the aggregate undiscounted potential liability for the remediation of such contaminants could range up to $200 million. These estimates were based on the assumption that there is contamination at all sites, including those that have not yet been fully investigated and additional assumptions about the extent of the contamination and the type and extent of the remediation that may be required. Actual experience may be materially different.

Asbestos Proceedings