EASTGROUP PROPERTIES INC

10-Ks and 10-Qs

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

WASHINGTON, D.C. 20549

FORM 10-K

ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF

THE SECURITIES EXCHANGE ACT OF 1934

FOR THE FISCAL YEAR ENDED

DECEMBER 31, 2016

COMMISSION FILE NUMBER 1-07094

EASTGROUP PROPERTIES, INC.

(EXACT NAME OF REGISTRANT AS SPECIFIED IN ITS CHARTER)

|

MARYLAND

|

13-2711135

|

|

(State or other jurisdiction

|

(I.R.S. Employer

|

|

of incorporation or organization)

|

Identification No.)

|

|

|

|

|

190 EAST CAPITOL STREET

|

|

|

SUITE 400

|

|

|

JACKSON, MISSISSIPPI

|

39201

|

|

(Address of principal executive offices)

|

(Zip code)

|

|

|

|

|

Registrant’s telephone number: (601) 354-3555

|

|

SECURITIES REGISTERED PURSUANT TO SECTION 12(b) OF THE ACT:

SHARES OF COMMON STOCK, $.0001 PAR VALUE,

NEW YORK STOCK EXCHANGE

SECURITIES REGISTERED PURSUANT TO SECTION 12(g) OF THE ACT: NONE

Indicate by check mark if the Registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. YES (x) NO ( )

Indicate by check mark if the Registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Exchange Act. YES ( ) NO (x)

Indicate by check mark whether the Registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the Registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. YES (x) NO ( )

Indicate by check mark whether the registrant has submitted electronically and posted on its corporate Web site, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files). YES (x) NO ( )

Indicate by check mark if disclosure of delinquent filers pursuant to Item 405 of Regulation S-K is not contained herein, and will not be contained, to the best of Registrant's knowledge, in definitive proxy or information statements incorporated by reference in Part III of this Form 10-K or any amendment to this Form 10-K. (x)

Indicate by check mark whether the Registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer or a smaller reporting company. See the definitions of “large accelerated filer,” “accelerated filer” and “smaller reporting company” in Rule 12b-2 of the Exchange Act. (Check one):

Large Accelerated Filer (x) Accelerated Filer ( ) Non-accelerated Filer ( ) Smaller Reporting Company ( )

Indicate by check mark whether the Registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act). YES ( ) NO (x)

State the aggregate market value of the voting and non-voting common equity held by non-affiliates computed by reference to the price at which the common equity was last sold, or the average bid and asked price of such common equity, as of June 30, 2016, the last business day of the Registrant's most recently completed second fiscal quarter: $2,188,222,000.

1

The number of shares of common stock, $.0001 par value, outstanding as of

February 14, 2017

was

33,314,596

.

DOCUMENTS INCORPORATED BY REFERENCE

Portions of the Registrant’s Proxy Statement for the

2017

Annual Meeting of Stockholders are incorporated by reference into Part

III.

2

|

Page

|

||

|

PART I

|

|

|

|

PART II

|

||

|

PART III

|

||

|

PART IV

|

||

3

Organization

EastGroup Properties, Inc. (the Company or EastGroup) is an equity real estate investment trust (REIT) organized in 1969. The Company has elected to be taxed and intends to continue to qualify as a REIT under Sections 856-860 of the Internal Revenue Code (the Code), as amended.

Available Information

The Company maintains a website at eastgroup.net. The Company posts its annual reports on Form 10-K, quarterly reports on Form 10-Q, current reports on Form 8-K and amendments to those reports filed or furnished pursuant to Section 13(a) of the Securities Exchange Act of 1934, as amended, as soon as reasonably practicable after it electronically files or furnishes such materials to the Securities and Exchange Commission (SEC). In addition, the Company's website includes items related to corporate governance matters, including, among other things, the Company's corporate governance guidelines, charters of various committees of the Board of Directors, and the Company's code of business conduct and ethics applicable to all employees, officers and directors. The Company intends to disclose on its website any amendment to, or waiver of, any provision of this code of business conduct and ethics applicable to the Company's directors and executive officers that would otherwise be required to be disclosed under the rules of the SEC or the New York Stock Exchange. Copies of these reports and corporate governance documents may be obtained, free of charge, from the Company's website. Any shareholder also may obtain copies of these documents, free of charge, by sending a request in writing to: Investor Relations, EastGroup Properties, Inc., 190 East Capitol Street, Suite 400, Jackson, MS 39201-2152.

Administration

EastGroup maintains its principal executive office and headquarters in Jackson, Mississippi. The Company also has regional offices in Orlando, Houston and Phoenix and asset management offices in Charlotte and Dallas. EastGroup has property management offices in Jacksonville, Tampa, Ft. Lauderdale and San Antonio. Offices at these locations allow the Company to provide property management services to all of its Florida, Texas (except Austin and El Paso), Arizona, Mississippi and North Carolina properties, which together account for 80% of the Company’s total portfolio on a square foot basis. In addition, the Company currently provides property administration (accounting of operations) for its entire portfolio. The regional offices in Florida, Texas and Arizona provide oversight of the Company's development program. As of

February 14, 2017

, EastGroup had 68 full-time employees and 3 part-time employees.

Operations

EastGroup is focused on the development, acquisition and operation of industrial properties in major Sunbelt markets throughout the United States with an emphasis in the states of Florida, Texas, Arizona, California and North Carolina. The Company’s goal is to maximize shareholder value by being a leading provider of functional, flexible and quality business distribution space for location sensitive tenants primarily in the 5,000 to 50,000 square foot range. EastGroup’s strategy for growth is based on the ownership of premier distribution facilities generally clustered near major transportation features in supply constrained submarkets. Over 99% of the Company’s revenue consists of rental income from real estate properties.

During

2016

, EastGroup increased its holdings in real estate properties through its acquisition and development programs. The Company purchased four warehouse distribution complexes (1,354,000 square feet) and

197

acres of development land for a total of $157 million. Also during

2016

, the Company began construction of nine development projects containing 1.2 million square feet and transferred

nine

projects (

1.0 million

square feet) from its development program to real estate properties with costs of

$68.1 million

at the date of transfer.

Typically, the Company initially funds its development and acquisition programs through its $335 million unsecured bank credit facilities. As market conditions permit, EastGroup issues equity and/or employs fixed-rate debt, including variable-rate debt that has been swapped to an effectively fixed rate through the use of interest rate swaps, to replace short-term bank borrowings. In March 2016, Moody's Investors Service affirmed the Company's issuer rating of Baa2 with a stable outlook. In April 2016, Fitch Ratings affirmed EastGroup's issuer rating of BBB with a stable outlook. A security rating is not a recommendation to buy, sell, or hold securities and may be subject to revision or withdrawal at any time by the assigning rating agency. Each rating should be evaluated independently of any other rating. The Company intends to issue primarily unsecured fixed-rate debt, including variable-rate debt that has been swapped to an effectively fixed rate through the use of interest rate swaps, in the future. The Company may also access the public debt market in the future as a means to raise capital.

EastGroup holds its properties as long-term investments but may determine to sell certain properties that no longer meet its investment criteria. The Company may provide financing in connection with such sales of property if market conditions require. In

4

addition, the Company may provide financing to a partner or co-owner in connection with an acquisition of real estate in certain situations.

Subject to the requirements necessary to maintain EastGroup’s qualifications as a REIT, the Company may acquire securities of entities engaged in real estate activities or securities of other issuers, including for the purpose of exercising control over those entities.

The Company intends to continue to qualify as a REIT under the Code. To maintain its status as a REIT, the Company is required to distribute at least 90% of its ordinary taxable income to its stockholders. If the Company has a capital gain, it has the option of (i) deferring recognition of the capital gain through a tax-deferred exchange, (ii) declaring and paying a capital gain dividend on any recognized net capital gain resulting in no corporate level tax, or (iii) retaining and paying corporate income tax on its net long-term capital gain, with shareholders reporting their proportional share of the undistributed long-term capital gain and receiving a credit or refund of their share of the tax paid by the Company.

EastGroup has no present intention of acting as an underwriter of offerings of securities of other issuers. The strategies and policies set forth above were determined and are subject to review by EastGroup's Board of Directors, which may change such strategies or policies based upon its evaluation of the state of the real estate market, the performance of EastGroup's assets, capital and credit market conditions, and other relevant factors. EastGroup provides annual reports to its stockholders, which contain financial statements audited by the Company’s independent registered public accounting firm.

Environmental Matters

Under various federal, state and local laws, ordinances and regulations, an owner of real estate may be liable for the costs of removal or remediation of certain hazardous or toxic substances on or in such property. Many such laws impose liability without regard to whether the owner knows of, or was responsible for, the presence of such hazardous or toxic substances. The presence of such substances, or the failure to properly remediate such substances, may adversely affect the owner’s ability to sell or rent such property or to use such property as collateral in its borrowings. EastGroup’s properties have been subjected to Phase I Environmental Site Assessments (ESAs) by independent environmental consultants and as necessary, have been subjected to Phase II ESAs. These reports have not revealed any potential significant environmental liability. Management of EastGroup is not aware of any environmental liability that would have a material adverse effect on EastGroup’s business, assets, financial position or results of operations.

In addition to the other information contained or incorporated by reference in this document, readers should carefully consider the following risk factors. Any of these risks or the occurrence of any one or more of the uncertainties described below could have a material adverse effect on the Company's financial condition and the performance of its business. The Company refers to itself as "we", "us" or "our" in the following risk factors.

Real Estate Industry Risks

We face risks associated with local real estate conditions in areas where we own properties.

We may be adversely affected by general economic conditions and local real estate conditions. For example, an oversupply of industrial properties in a local area or a decline in the attractiveness of our properties to tenants would have a negative effect on us. Other factors that may affect general economic conditions or local real estate conditions include:

|

•

|

population and demographic trends;

|

|

•

|

employment and personal income trends;

|

|

•

|

income and other tax laws;

|

|

•

|

changes in interest rates and availability and costs of financing;

|

|

•

|

increased operating costs, including insurance premiums, utilities and real estate taxes, due to inflation and other factors which may not necessarily be offset by increased rents;

|

|

•

|

changes in the price of oil; and

|

|

•

|

construction costs.

|

We may be unable to compete for properties and tenants

. The real estate business is highly competitive. We compete for interests in properties with other real estate investors and purchasers, some of whom have greater financial resources, revenues and geographical diversity than we have. Furthermore, we compete for tenants with other property owners. All of our industrial properties are subject to significant local competition. We also compete with a wide variety of institutions and other investors for capital funds necessary to support our investment activities and asset growth.

5

We are subject to significant regulation that constrains our activities.

Local zoning and land use laws, environmental statutes and other governmental requirements restrict our expansion, rehabilitation and reconstruction activities. These regulations may prevent us from taking advantage of economic opportunities. Legislation such as the Americans with Disabilities Act may require us to modify our properties, and noncompliance could result in the imposition of fines or an award of damages to private litigants. Future legislation may impose additional requirements. We cannot predict what requirements may be enacted or what changes may be implemented to existing legislation.

Risks Associated with Our Properties

We may be unable to lease space.

When a lease expires, a tenant may elect not to renew it. We may not be able to re-lease the property on similar terms, if we are able to re-lease the property at all. The terms of renewal or re-lease (including the cost of required renovations and/or concessions to tenants) may be less favorable to us than the prior lease. We also routinely develop properties with no pre-leasing. If we are unable to lease all or a substantial portion of our properties, or if the rental rates upon such leasing are significantly lower than expected rates, our cash generated before debt repayments and capital expenditures and our ability to make expected distributions to stockholders may be adversely affected.

We have been and may continue to be affected negatively by tenant bankruptcies and leasing delays.

At any time, a tenant may experience a downturn in its business that may weaken its financial condition. Similarly, a general decline in the economy may result in a decline in the demand for space at our industrial properties. As a result, our tenants may delay lease commencement, fail to make rental payments when due, or declare bankruptcy. Any such event could result in the termination of that tenant’s lease and losses to us, and distributions to investors may decrease. We receive a substantial portion of our income as rents under mid-term and long-term leases. If tenants are unable to comply with the terms of their leases because of rising costs or falling sales, we may deem it advisable to modify lease terms to allow tenants to pay a lower rent or a smaller share of taxes, insurance and other operating costs. If a tenant becomes insolvent or bankrupt, we cannot be sure that we could recover the premises from the tenant promptly or from a trustee or debtor-in-possession in any bankruptcy proceeding relating to the tenant. We also cannot be sure that we would receive rent in the proceeding sufficient to cover our expenses with respect to the premises. If a tenant becomes bankrupt, the federal bankruptcy code will apply and, in some instances, may restrict the amount and recoverability of our claims against the tenant. A tenant’s default on its obligations to us could adversely affect our financial condition and the cash we have available for distribution.

We face risks associated with our property development.

We intend to continue to develop properties where market conditions warrant such investment. Once made, our investments may not produce results in accordance with our expectations. Risks associated with our current and future development and construction activities include:

|

•

|

the availability of favorable financing alternatives;

|

|

•

|

the risk that we may not be able to obtain land on which to develop or that due to the increased cost of land, our activities may not be as profitable;

|

|

•

|

construction costs exceeding original estimates due to rising interest rates and increases in the costs of materials and labor;

|

|

•

|

construction and lease-up delays resulting in increased debt service, fixed expenses and construction costs;

|

|

•

|

expenditure of funds and devotion of management's time to projects that we do not complete;

|

|

•

|

fluctuations of occupancy and rental rates at newly completed properties, which depend on a number of factors, including market and economic conditions, resulting in lower than projected rental rates and a corresponding lower return on our investment; and

|

|

•

|

complications (including building moratoriums and anti-growth legislation) in obtaining necessary zoning, occupancy and other governmental permits.

|

We face risks associated with property acquisitions

. We acquire individual properties and portfolios of properties and intend to continue to do so. Our acquisition activities and their success are subject to the following risks:

|

•

|

when we are able to locate a desired property, competition from other real estate investors may significantly increase the purchase price;

|

|

•

|

acquired properties may fail to perform as expected;

|

|

•

|

the actual costs of repositioning or redeveloping acquired properties may be higher than our estimates;

|

|

•

|

acquired properties may be located in new markets where we face risks associated with an incomplete knowledge or understanding of the local market, a limited number of established business relationships in the area and a relative unfamiliarity with local governmental and permitting procedures;

|

|

•

|

we may be unable to quickly and efficiently integrate new acquisitions, particularly acquisitions of portfolios of properties, into our existing operations, and as a result, our results of operations and financial condition could be adversely affected; and

|

6

|

•

|

we may acquire properties subject to liabilities and without any recourse, or with only limited recourse, to the transferor with respect to unknown liabilities. As a result, if a claim were asserted against us based upon ownership of those properties, we might have to pay substantial sums to settle it, which could adversely affect our cash flow.

|

Coverage under our existing insurance policies may be inadequate to cover losses

. We generally maintain insurance policies related to our business, including casualty, general liability and other policies, covering our business operations, employees and assets as appropriate for the markets where our properties and business operations are located. However, we would be required to bear all losses that are not adequately covered by insurance. In addition, there may be certain losses that are not generally insured against or that are not generally fully insured against because it is not deemed economically feasible or prudent to do so, including losses due to floods, wind, earthquakes, acts of war, acts of terrorism or riots. If an uninsured loss or a loss in excess of insured limits occurs with respect to one or more of our properties, then we could lose the capital we invested in the properties, as well as the anticipated future revenue from the properties. In addition, if the damaged properties are subject to recourse indebtedness, we would continue to be liable for the indebtedness, even if these properties were irreparably damaged.

We face risks due to lack of geographic and real estate sector diversity.

Substantially all of our properties are located in the Sunbelt region of the United States with an emphasis in the states of Florida, Texas, Arizona, California and North Carolina. As of

December 31, 2016

, we owned operating properties totaling 5.9 million square feet in Houston, which represents 17.0% of the Company's total

Real estate properties

on a square foot basis. A downturn in general economic conditions and local real estate conditions in these geographic regions, as a result of oversupply of or reduced demand for industrial properties, local business climate, business layoffs and changing demographics, would have a particularly strong adverse effect on us. Our investments in real estate assets are concentrated in the industrial distribution sector. This concentration may expose us to the risk of economic downturns in this sector to a greater extent than if our business activities included other sectors of the real estate industry.

We face risks due to the illiquidity of real estate which may limit our ability to vary our portfolio.

Real estate investments are relatively illiquid. Our ability to vary our portfolio in response to changes in economic and other conditions will therefore be limited. In addition, because of our status as a REIT, the Internal Revenue Code limits our ability to sell our properties. If we must sell an investment, we cannot ensure that we will be able to dispose of the investment on terms favorable to the Company.

We are subject to environmental laws and regulations.

Current and previous real estate owners and operators may be required under various federal, state and local laws, ordinances and regulations to investigate and clean up hazardous substances released at the properties they own or operate. They may also be liable to the government or to third parties for substantial property or natural resource damage, investigation costs and cleanup costs. Such laws often impose liability without regard to whether the owner or operator knew of, or was responsible for, the release or presence of such hazardous substances. In addition, some environmental laws create a lien on the contaminated site in favor of the government for damages and costs the government incurs in connection with the contamination. Contamination may adversely affect the owner’s ability to use, sell or lease real estate or to borrow using the real estate as collateral. We have no way of determining at this time the magnitude of any potential liability to which we may be subject arising out of environmental conditions or violations with respect to the properties we currently or formerly owned. Environmental laws today can impose liability on a previous owner or operator of a property that owned or operated the property at a time when hazardous or toxic substances were disposed of, released from, or present at the property. A conveyance of the property, therefore, may not relieve the owner or operator from liability. Although ESAs have been conducted at our properties to identify potential sources of contamination at the properties, such ESAs do not reveal all environmental liabilities or compliance concerns that could arise from the properties. Moreover, material environmental liabilities or compliance concerns may exist, of which we are currently unaware, that in the future may have a material adverse effect on our business, assets or results of operations.

Compliance with new laws or regulations related to climate change, including compliance with “green” building codes, may require us to make improvements to our existing properties.

Proposed legislation could also increase the costs of energy and utilities. The cost of the proposed legislation may adversely affect our financial position, results of operations and cash flows. We may be adversely affected by floods, hurricanes and other climate related events.

Financing Risks

We face risks associated with the use of debt to fund acquisitions and developments, including refinancing risk.

We are subject to the risks normally associated with debt financing, including the risk that our cash flow will be insufficient to meet required payments of principal and interest. In addition, certain of our debt will have significant outstanding principal balances on their maturity dates, commonly known as “balloon payments.” Therefore, we will likely need to refinance at least a portion of our outstanding debt as it matures. There is a risk that we may not be able to refinance existing debt or that the terms of any refinancing will not be as favorable as the terms of the existing debt.

7

We face risks associated with our dependence on external sources of capital.

In order to qualify as a REIT, we are required each year to distribute to our stockholders at least 90% of our ordinary taxable income, and we are subject to tax on our income to the extent it is not distributed. Because of this distribution requirement, we may not be able to fund all future capital needs from cash retained from operations. As a result, to fund capital needs, we rely on third-party sources of capital, which we may not be able to obtain on favorable terms, if at all. Our access to third-party sources of capital depends upon a number of factors, including (i) general market conditions; (ii) the market’s perception of our growth potential; (iii) our current and potential future earnings and cash distributions; and (iv) the market price of our capital stock. Additional debt financing may substantially increase our debt-to-total market capitalization ratio. Additional equity financing may dilute the holdings of our current stockholders.

Covenants in our credit agreements could limit our flexibility and adversely affect our financial condition

. The terms of our various credit agreements and other indebtedness require us to comply with a number of customary financial and other covenants, such as maintaining debt service coverage and leverage ratios and maintaining insurance coverage. These covenants may limit our flexibility in our operations, and breaches of these covenants could result in defaults under the instruments governing the applicable indebtedness even if we had satisfied our payment obligations. If we are unable to refinance our indebtedness at maturity or meet our payment obligations, the amount of our distributable cash flow and our financial condition would be adversely affected.

Adverse changes in our credit ratings could impair our ability to obtain additional debt and equity financing on favorable terms, if at all.

Our credit ratings are based on our operating performance, liquidity and leverage ratios, overall financial position and other factors employed by the credit rating agencies in their rating analysis of us. Our credit ratings can affect the amount and type of capital we can access, as well as the terms of any financings we may obtain. There can be no assurance that we will be able to maintain our current credit ratings. In the event our current credit ratings deteriorate, it may be more difficult or expensive to obtain additional financing or refinance existing obligations and commitments. Also, a downgrade in our credit ratings would trigger additional costs or other potentially negative consequences under our current and future credit facilities and debt instruments.

Increases in interest rates would increase our interest expense.

At

December 31, 2016

, we had $112.0 million of variable-rate debt outstanding not protected by interest rate hedge contracts. We may incur additional variable-rate debt in the future. If interest rates increase, then so would the interest expense on our unhedged variable-rate debt, which would adversely affect our financial condition and results of operations. From time to time, we manage our exposure to interest rate risk with interest rate hedge contracts that effectively fix or cap a portion of our variable-rate debt. In addition, we refinance fixed-rate debt at times when we believe rates and terms are appropriate. Our efforts to manage these exposures may not be successful. Our use of interest rate hedge contracts to manage risk associated with interest rate volatility may expose us to additional risks, including a risk that a counterparty to a hedge contract may fail to honor its obligations. Developing an effective interest rate risk strategy is complex and no strategy can completely insulate us from risks associated with interest rate fluctuations. There can be no assurance that our hedging activities will have the desired beneficial impact on our results of operations or financial condition. Termination of interest rate hedge contracts typically involves costs, such as transaction fees or breakage costs.

A lack of any limitation on our debt could result in our becoming more highly leveraged

. Our governing documents do not limit the amount of indebtedness we may incur. Accordingly, we may incur additional debt and would do so, for example, if it were necessary to maintain our status as a REIT. We might become more highly leveraged as a result, and our financial condition and cash available for distribution to stockholders might be negatively affected and the risk of default on our indebtedness could increase.

Other Risks

The market value of our common stock could decrease based on our performance and market perception and conditions.

The market value of our common stock may be affected by the market’s perception of our operating results, growth potential, and current and future cash dividends and may also be affected by the real estate market value of our underlying assets. The market price of our common stock may be influenced by the dividend on our common stock relative to market interest rates. Rising interest rates may lead potential buyers of our common stock to expect a higher dividend rate, which would adversely affect the market price of our common stock. In addition, rising interest rates would result in increased expense, thereby adversely affecting cash flow and our ability to service our indebtedness and pay dividends.

The state of the economy or other adverse changes in general or local economic conditions may adversely affect our operating results and financial condition.

Turmoil in the global financial markets may have an adverse impact on the availability of credit to businesses generally and could lead to a further weakening of the U.S. and global economies. Currently these conditions have not impaired our ability to access credit markets and finance our operations. However, our ability to access the capital markets may be restricted at a time when we would like, or need, to raise financing, which could have an impact on our flexibility to react to changing economic and business conditions. Furthermore, deteriorating economic conditions including business layoffs, downsizing, industry slowdowns and other similar factors that affect our customers could continue to negatively impact commercial real estate fundamentals and result in lower occupancy, lower rental rates and declining values in our real estate portfolio and in

8

the collateral securing any loan investments we may make. Additionally, an adverse economic situation could have an impact on our lenders or customers, causing them to fail to meet their obligations to us. No assurances can be given that the effects of an adverse economic situation will not have a material adverse effect on our business, financial condition and results of operations.

We may fail to qualify as a REIT.

If we fail to qualify as a REIT, we will not be allowed to deduct distributions to stockholders in computing our taxable income and will be subject to federal income tax, including any applicable alternative minimum tax, at regular corporate rates. In addition, we may be barred from qualification as a REIT for the four years following disqualification. The additional tax incurred at regular corporate rates would significantly reduce the cash flow available for distribution to stockholders and for debt service. Furthermore, we would no longer be required by the Internal Revenue Code to make any distributions to our stockholders as a condition of REIT qualification. Any distributions to stockholders would be taxable as ordinary income to the extent of our current and accumulated earnings and profits. Corporate distributees, however, may be eligible for the dividends received deduction on the distributions, subject to limitations under the Internal Revenue Code. To qualify as a REIT, we must comply with certain highly technical and complex requirements. We cannot be certain we have complied with these requirements because there are few judicial and administrative interpretations of these provisions. In addition, facts and circumstances that may be beyond our control may affect our ability to qualify as a REIT. We cannot assure you that new legislation, regulations, administrative interpretations or court decisions will not change the tax laws significantly with respect to our qualification as a REIT or with respect to the federal income tax consequences of qualification. We cannot assure you that we will remain qualified as a REIT.

There is a risk of changes in the tax law applicable to real estate investment trusts

. Since the Internal Revenue Service, the United States Treasury Department and Congress frequently review federal income tax legislation, we cannot predict whether, when or to what extent new federal tax laws, regulations, interpretations or rulings will be adopted. Any such legislative action may prospectively or retroactively modify our tax treatment and, therefore, may adversely affect taxation of us and/or our investors.

We face possible adverse changes in tax laws.

From time to time, changes in state and local tax laws or regulations are enacted which may result in an increase in our tax liability. A shortfall in tax revenues for states and municipalities in which we operate may lead to an increase in the frequency and size of such changes. If such changes occur, we may be required to pay additional taxes on our assets or income. These increased tax costs could adversely affect our financial condition, results of operations and the amount of cash available for the payment of dividends.

To maintain our status as a REIT, we limit the amount of shares any one stockholder can own

. The Internal Revenue Code imposes certain limitations on the ownership of the stock of a REIT. For example, not more than 50% in value of our outstanding shares of capital stock may be owned, directly or indirectly, by five or fewer individuals (as defined in the Code) during the last half of any taxable year. To protect our REIT status, our charter prohibits any holder from acquiring more than 9.8% (in value or in number, whichever is more restrictive) of our outstanding equity stock (defined as all of our classes of capital stock, except our excess stock (of which there is none outstanding)) unless our Board of Directors grants a waiver. The ownership limit may limit the opportunity for stockholders to receive a premium for their shares of common stock that might otherwise exist if an investor were attempting to assemble a block of shares in excess of 9.8% of the outstanding shares of equity stock or otherwise effect a change in control.

Certain tax and anti-takeover provisions of our charter and bylaws may inhibit a change of our control

. Certain provisions contained in our charter and bylaws and the Maryland General Corporation Law may discourage a third party from making a tender offer or acquisition proposal to us. If this were to happen, it could delay, deter or prevent a change in control or the removal of existing management. These provisions also may delay or prevent the shareholders from receiving a premium for their common shares over then-prevailing market prices. These provisions include:

|

•

|

the REIT ownership limit described above;

|

|

•

|

special meetings of our stockholders may be called only by the chairman of the board, the chief executive officer, the president, a majority of the board or by stockholders possessing a majority of all the votes entitled to be cast at the meeting;

|

|

•

|

our Board of Directors may authorize and issue securities without stockholder approval; and

|

|

•

|

advance-notice requirements for proposals to be presented at stockholder meetings.

|

In addition, Maryland law provides protection for Maryland corporations against unsolicited takeovers by limiting, among other things, the duties of the directors in unsolicited takeover situations. The duties of directors of Maryland corporations do not require them to (a) accept, recommend or respond to any proposal by a person seeking to acquire control of the corporation, (b) authorize the corporation to redeem any rights under, or modify or render inapplicable, any stockholders rights plan, (c) make a determination under the Maryland Business Combination Act or the Maryland Control Share Acquisition Act, or (d) act or fail to act solely because of the effect of the act or failure to act may have on an acquisition or potential acquisition of control of the corporation

9

or the amount or type of consideration that may be offered or paid to the stockholders in an acquisition. Moreover, under Maryland law the act of a director of a Maryland corporation relating to or affecting an acquisition or potential acquisition of control is not subject to any higher duty or greater scrutiny than is applied to any other act of a director. Maryland law also contains a statutory presumption that an act of a director of a Maryland corporation satisfies the applicable standards of conduct for directors under Maryland law.

The Maryland Business Combination Act provides that unless exempted, a Maryland corporation may not engage in business combinations, including mergers, dispositions of 10 percent or more of its assets, certain issuances of shares of stock and other specified transactions, with an "interested stockholder" or an affiliate of an interested stockholder for five years after the most recent date on which the interested stockholder became an interested stockholder, and thereafter unless specified criteria are met. An interested stockholder is generally a person owning or controlling, directly or indirectly, 10 percent or more of the voting power of the outstanding stock of the Maryland corporation.

The Maryland Control Share Acquisition Act provides that "control shares" of a corporation acquired in a "control share acquisition" shall have no voting rights except to the extent approved by a vote of two-thirds of the votes eligible to cast on the matter. "Control Shares" means shares of stock that, if aggregated with all other shares of stock previously acquired by the acquirer, would entitle the acquirer to exercise voting power in electing directors within one of the following ranges of the voting power: one-tenth or more but less than one-third, one-third or more but less than a majority, or a majority or more of all voting power. A "control share acquisition" means the acquisition of control shares, subject to certain exceptions.

If voting rights of control shares acquired in a control share acquisition are not approved at a stockholders' meeting, then subject to certain conditions and limitations, the issuer may redeem any or all of the control shares for fair value. If voting rights of such control shares are approved at a stockholders' meeting and the acquirer becomes entitled to vote a majority of the shares of stock entitled to vote, all other stockholders may exercise appraisal rights.

The Company faces risks in attracting and retaining key personnel.

Many of our senior executives have strong industry reputations, which aid us in identifying acquisition and development opportunities and negotiating with tenants and sellers of properties. The loss of the services of these key personnel could affect our operations because of diminished relationships with existing and prospective tenants, property sellers and industry personnel. In addition, attracting new or replacement personnel may be difficult in a competitive market.

We have severance and change in control agreements with certain of our officers that may deter changes in control of the Company.

If, within a certain time period (as set in the officer’s agreement) following a change in control, we terminate the officer's employment other than for cause, or if the officer elects to terminate his or her employment with us for reasons specified in the agreement, we will make a severance payment equal to the officer's average annual compensation times an amount specified in the officer's agreement, together with the officer's base salary and vacation pay that have accrued but are unpaid through the date of termination. These agreements may deter a change in control because of the increased cost for a third party to acquire control of us.

We rely on information technology in our operations, and any material failure, inadequacy, interruption or security failure of that technology could harm our business.

We rely on information technology networks and systems, including the internet, to process, transmit and store electronic information, and to manage or support a variety of business processes, including financial transactions and records, and maintaining personal identifying information and customer and lease data. We purchase some of our information technology from vendors, on whom our systems depend. We rely on commercially available systems, software, tools and monitoring to provide security for the processing, transmission and storage of confidential customer data, including individually identifiable information relating to financial accounts. Although we have taken steps to protect the security of our information systems and the data maintained in those systems, it is possible that our safety and security measures will not prevent the systems' improper functioning or damage, or the improper access or disclosure of personally identifiable information such as in the event of cyber-attacks. Security breaches, including physical or electronic break-ins, computer viruses, attacks by hackers and similar breaches, can create system disruptions, shutdowns or unauthorized disclosure of confidential information. In some cases, it may be difficult to anticipate or immediately detect such incidents and the damage they cause. Any failure to maintain proper function, security and availability of our information systems could interrupt our operations, damage our reputation, subject us to liability claims or regulatory penalties and could have a materially adverse effect on our business, financial condition and results of operations.

We may be impacted by changes in U.S. social, political, regulatory and economic conditions or laws and policies.

Any changes to U.S. tax laws, foreign trade, manufacturing, and development and investment in the territories and countries where our customers operate could adversely affect our operating results and our business.

10

None.

EastGroup owned 327 industrial properties and one office building at

December 31, 2016

. These properties are located primarily in the Sunbelt states of Florida, Texas, Arizona, California and North Carolina, and the majority are clustered around major transportation features in supply constrained submarkets. As of

February 14, 2017

, EastGroup’s portfolio was 95.8% leased and 95.2% occupied. The Company has developed approximately 44% of its total portfolio (on a square foot basis), including real estate properties and development properties in lease-up and under construction. The Company’s focus is the ownership of business distribution space (87% of the total portfolio) with the remainder in bulk distribution space (9%) and business service space (4%). Business distribution space properties are typically multi-tenant buildings with a building depth of 200 feet or less, clear height of 24-30 feet, office finish of 10-25% and truck courts with a depth of 100-120 feet. See Consolidated Financial Statement Schedule III – Real Estate Properties and Accumulated Depreciation for a detailed listing of the Company’s properties.

At

December 31, 2016

, EastGroup did not own any single property with a book value that was 10% or more of total book value or with gross revenues that were 10% or more of total gross revenues.

The Company's lease expirations, excluding month-to-month leases of 243,000 square feet, for the next ten years are detailed below:

|

Years Ending December 31,

|

Number of Leases Expiring

|

Total Area of Leases Expiring

(in Square Feet)

|

Annualized Current Base Rent of Leases Expiring

(1)

|

% of Total Base Rent of Leases Expiring

|

|||||||

|

2017

|

249

|

4,739,000

|

|

$

|

28,604,000

|

|

14.9%

|

||||

|

2018

|

310

|

5,042,000

|

|

$

|

29,518,000

|

|

15.3%

|

||||

|

2019

|

267

|

5,524,000

|

|

$

|

31,307,000

|

|

16.3%

|

||||

|

2020

|

216

|

4,963,000

|

|

$

|

28,763,000

|

|

14.9%

|

||||

|

2021

|

180

|

5,633,000

|

|

$

|

30,630,000

|

|

15.9%

|

||||

|

2022

|

76

|

2,872,000

|

|

$

|

16,078,000

|

|

8.4%

|

||||

|

2023

|

44

|

1,790,000

|

|

$

|

9,645,000

|

|

5.0%

|

||||

|

2024

|

28

|

1,542,000

|

|

$

|

6,485,000

|

|

3.4%

|

||||

|

2025

|

10

|

772,000

|

|

$

|

4,597,000

|

|

2.4%

|

||||

|

2026 and beyond

|

25

|

895,000

|

|

$

|

5,357,000

|

|

2.8%

|

||||

|

(1)

|

Represents the monthly cash rental rates, excluding tenant expense reimbursements, as of

December 31, 2016

, multiplied by 12 months.

|

The Company is not presently involved in any material litigation nor, to its knowledge, is any material litigation threatened against the Company or its properties, other than routine litigation arising in the ordinary course of business or which is expected to be covered by the Company’s liability insurance.

Not applicable.

11

The Company’s shares of common stock are listed for trading on the New York Stock Exchange under the symbol “EGP.” The following table shows the high and low share prices for each quarter reported by the New York Stock Exchange during the past two years and the per share distributions paid for each quarter.

Shares of Common Stock Market Prices and Dividends

|

Quarter

|

Calendar Year 2016

|

Calendar Year 2015

|

||||||||||||||||||||

|

High

|

Low

|

Distributions

|

High

|

Low

|

Distributions

|

|||||||||||||||||

|

First

|

$

|

60.46

|

|

49.31

|

|

$

|

0.60

|

|

$

|

67.42

|

|

57.98

|

|

$

|

0.57

|

|

||||||

|

Second

|

69.35

|

|

58.28

|

|

0.60

|

|

62.11

|

|

55.00

|

|

0.57

|

|

||||||||||

|

Third

|

76.00

|

|

68.40

|

|

0.62

|

|

60.85

|

|

51.76

|

|

0.60

|

|

||||||||||

|

Fourth

|

74.71

|

|

63.99

|

|

0.62

|

|

59.51

|

|

53.15

|

|

0.60

|

|

||||||||||

|

|

|

|

|

|

$

|

2.44

|

|

|

|

|

|

$

|

2.34

|

|

||||||||

As of

February 14, 2017

, there were

495

holders of record of the Company’s

33,314,596

outstanding shares of common stock. The Company distributed all of its

2016

and

2015

taxable income to its stockholders. Accordingly, no significant provisions for income taxes were necessary. The following table summarizes the federal income tax treatment for all distributions by the Company for the years

2016

and

2015

.

Federal Income Tax Treatment of Share Distributions

|

|

Years Ended December 31,

|

|||||

|

2016

|

2015

|

|||||

|

Common Share Distributions:

|

|

|

||||

|

Ordinary dividends

|

$

|

2.10494

|

|

2.24258

|

|

|

|

Nondividend distributions

|

0.05202

|

|

0.02774

|

|

||

|

Unrecaptured Section 1250 capital gain

|

0.12872

|

|

0.06968

|

|

||

|

Other capital gain

|

0.15432

|

|

—

|

|

||

|

Total Common Distributions

|

$

|

2.44000

|

|

2.34000

|

|

|

Securities Authorized For Issuance Under Equity Compensation Plans

See Item 12 of this Annual Report on Form 10-K, “Security Ownership of Certain Beneficial Owners and Management and Related Stockholder Matters,” for certain information regarding the Company’s equity compensation plans.

Purchases of Equity Securities by the Issuer and Affiliated Purchasers

No shares of common stock were purchased by the Company or withheld by the Company to satisfy any tax withholding obligations during the three-month period ended December 31, 2016.

12

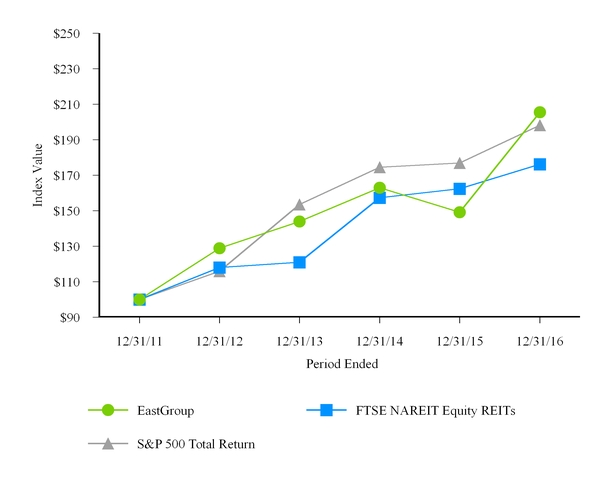

Performance Graph

The following graph compares, over the five years ended

December 31, 2016

, the cumulative total shareholder return on EastGroup’s common stock with the cumulative total return of the Standard & Poor’s 500 Total Return Index (S&P 500 Total Return) and the FTSE Equity REIT index prepared by the National Association of Real Estate Investment Trusts (FTSE NAREIT Equity REITs).

The performance graph and related information shall not be deemed “soliciting material” or be deemed to be “filed” with the SEC, nor shall such information be incorporated by reference into any future filing, except to the extent that the Company specifically incorporates it by reference into such filing.

|

|

Fiscal years ended December 31,

|

|||||||||||||||||

|

2011

|

2012

|

2013

|

2014

|

2015

|

2016

|

|||||||||||||

|

EastGroup

|

$

|

100.00

|

|

128.89

|

|

144.01

|

|

163.04

|

|

149.21

|

|

205.58

|

|

|||||

|

FTSE NAREIT Equity REITs

|

100.00

|

|

118.06

|

|

120.97

|

|

157.43

|

|

162.46

|

|

176.30

|

|

||||||

|

S&P 500 Total Return

|

100.00

|

|

116.00

|

|

153.57

|

|

174.60

|

|

177.01

|

|

198.18

|

|

||||||

The information above assumes that the value of the investment in shares of EastGroup’s common stock and each index was $100 on December 31, 2011, and that all dividends were reinvested.

The following table sets forth selected consolidated financial data for the Company derived from the audited consolidated financial statements and should be read in conjunction with the consolidated financial statements and notes thereto included elsewhere in this report.

|

|

Years Ended December 31,

|

||||||||||||||

|

2016

|

2015

|

2014

|

2013

|

2012

|

|||||||||||

|

OPERATING DATA

|

(In thousands, except per share data)

|

||||||||||||||

|

REVENUES

|

|

|

|

|

|

||||||||||

|

Income from real estate operations

|

$

|

252,961

|

|

234,918

|

|

219,706

|

|

201,849

|

|

185,783

|

|

||||

|

Other income

|

86

|

|

90

|

|

123

|

|

322

|

|

61

|

|

|||||

|

|

253,047

|

|

235,008

|

|

219,829

|

|

202,171

|

|

185,844

|

|

|||||

|

Expenses

|

|

|

|

|

|

|

|

|

|

|

|||||

|

Expenses from real estate operations

|

74,347

|

|

67,402

|

|

62,797

|

|

57,885

|

|

52,891

|

|

|||||

|

Depreciation and amortization

|

77,935

|

|

73,290

|

|

70,314

|

|

65,789

|

|

61,345

|

|

|||||

|

General and administrative

|

13,232

|

|

15,091

|

|

12,726

|

|

11,725

|

|

10,488

|

|

|||||

|

Acquisition costs

|

161

|

|

164

|

|

210

|

|

191

|

|

188

|

|

|||||

|

|

165,675

|

|

155,947

|

|

146,047

|

|

135,590

|

|

124,912

|

|

|||||

|

Operating income

|

87,372

|

|

79,061

|

|

73,782

|

|

66,581

|

|

60,932

|

|

|||||

|

Other income (expense)

|

|

|

|

|

|

|

|

|

|

|

|||||

|

Interest expense

|

(35,213

|

)

|

(34,666

|

)

|

(35,486

|

)

|

(35,192

|

)

|

(35,371

|

)

|

|||||

|

Gain, net of loss, on sales of real estate investments

|

42,170

|

|

2,903

|

|

9,188

|

|

—

|

|

—

|

|

|||||

|

Other

|

1,765

|

|

1,101

|

|

989

|

|

949

|

|

456

|

|

|||||

|

Income from continuing operations

|

96,094

|

|

48,399

|

|

48,473

|

|

32,338

|

|

26,017

|

|

|||||

|

Discontinued operations

|

|

|

|

|

|

|

|

|

|

|

|||||

|

Income from real estate operations

|

—

|

|

—

|

|

—

|

|

89

|

|

360

|

|

|||||

|

Gain on sales of nondepreciable real estate investments

|

—

|

|

—

|

|

—

|

|

—

|

|

167

|

|

|||||

|

Gain on sales of real estate investments

|

—

|

|

—

|

|

—

|

|

798

|

|

6,343

|

|

|||||

|

Income from discontinued operations

|

—

|

|

—

|

|

—

|

|

887

|

|

6,870

|

|

|||||

|

Net income

|

96,094

|

|

48,399

|

|

48,473

|

|

33,225

|

|

32,887

|

|

|||||

|

Net income attributable to noncontrolling interest in joint ventures

|

(585

|

)

|

(533

|

)

|

(532

|

)

|

(610

|

)

|

(503

|

)

|

|||||

|

Net income attributable to EastGroup Properties, Inc. common stockholders

|

95,509

|

|

47,866

|

|

47,941

|

|

32,615

|

|

32,384

|

|

|||||

|

Other comprehensive income (loss) - Cash flow hedges

|

5,451

|

|

(1,099

|

)

|

(3,986

|

)

|

2,021

|

|

(392

|

)

|

|||||

|

TOTAL COMPREHENSIVE INCOME

|

$

|

100,960

|

|

46,767

|

|

43,955

|

|

34,636

|

|

31,992

|

|

||||

|

BASIC PER COMMON SHARE DATA FOR NET INCOME ATTRIBUTABLE TO EASTGROUP PROPERTIES, INC. COMMON STOCKHOLDERS

|

|

|

|

|

|

|

|

|

|

|

|||||

|

Income from continuing operations

|

$

|

2.93

|

|

1.49

|

|

1.53

|

|

1.05

|

|

0.89

|

|

||||

|

Income from discontinued operations

|

—

|

|

—

|

|

—

|

|

0.03

|

|

0.24

|

|

|||||

|

Net income attributable to common stockholders

|

$

|

2.93

|

|

1.49

|

|

1.53

|

|

1.08

|

|

1.13

|

|

||||

|

Weighted average shares outstanding

|

32,563

|

|

32,091

|

|

31,341

|

|

30,162

|

|

28,577

|

|

|||||

|

DILUTED PER COMMON SHARE DATA FOR NET INCOMEATTRIBUTABLE TO EASTGROUP PROPERTIES, INC. COMMON STOCKHOLDERS

|

|

|

|

|

|

|

|

|

|

|

|||||

|

Income from continuing operations

|

$

|

2.93

|

|

1.49

|

|

1.52

|

|

1.05

|

|

0.89

|

|

||||

|

Income from discontinued operations

|

—

|

|

—

|

|

—

|

|

0.03

|

|

0.24

|

|

|||||

|

Net income attributable to common stockholders

|

$

|

2.93

|

|

1.49

|

|

1.52

|

|

1.08

|

|

1.13

|

|

||||

|

Weighted average shares outstanding

|

32,628

|

|

32,196

|

|

31,452

|

|

30,269

|

|

28,677

|

|

|||||

|

AMOUNTS ATTRIBUTABLE TO EASTGROUP

PROPERTIES, INC. COMMON STOCKHOLDERS

|

|

|

|

|

|

|

|

|

|

|

|||||

|

Income from continuing operations

|

$

|

95,509

|

|

47,866

|

|

47,941

|

|

31,728

|

|

25,514

|

|

||||

|

Income from discontinued operations

|

—

|

|

—

|

|

—

|

|

887

|

|

6,870

|

|

|||||

|

Net income attributable to common stockholders

|

$

|

95,509

|

|

47,866

|

|

47,941

|

|

32,615

|

|

32,384

|

|

||||

|

OTHER PER SHARE DATA

|

|

|

|

|

|

|

|

|

|

|

|||||

|

Book value, at end of year

|

$

|

19.13

|

|

17.11

|

|

17.72

|

|

16.61

|

|

16.25

|

|

||||

|

Common distributions declared

|

2.44

|

|

2.34

|

|

2.22

|

|

2.14

|

|

2.10

|

|

|||||

|

Common distributions paid

|

2.44

|

|

2.34

|

|

2.22

|

|

2.14

|

|

2.10

|

|

|||||

|

BALANCE SHEET DATA (AT END OF YEAR)

|

|

|

|

|

|

|

|

|

|

|

|||||

|

Real estate investments, at cost

(1)

|

$

|

2,419,414

|

|

2,232,327

|

|

2,087,821

|

|

1,938,960

|

|

1,780,098

|

|

||||

|

Real estate investments, net of accumulated depreciation

(1)

|

1,725,164

|

|

1,574,873

|

|

1,487,295

|

|

1,388,847

|

|

1,283,851

|

|

|||||

|

Total assets

|

1,825,764

|

|

1,661,904

|

|

1,572,112

|

|

1,468,963

|

|

1,350,586

|

|

|||||

|

Unsecured bank credit facilities, unsecured debt and secured debt

|

1,101,333

|

|

1,027,909

|

|

929,465

|

|

889,296

|

|

810,411

|

|

|||||

|

Total liabilities

|

1,183,898

|

|

1,102,703

|

|

996,497

|

|

950,258

|

|

859,410

|

|

|||||

|

Noncontrolling interest in joint ventures

|

4,205

|

|

4,339

|

|

4,486

|

|

4,707

|

|

4,864

|

|

|||||

|

Total stockholders’ equity

|

637,661

|

|

554,862

|

|

571,129

|

|

513,998

|

|

486,312

|

|

|||||

|

(1)

|

Includes mortgage loans receivable and unconsolidated investment. See Notes 3 and 4 in the Notes to Consolidated Financial Statements.

|

13

OVERVIEW

EastGroup’s goal is to maximize shareholder value by being a leading provider in its markets of functional, flexible and quality business distribution space for location sensitive customers (primarily in the 5,000 to 50,000 square foot range). The Company develops, acquires and operates distribution facilities, the majority of which are clustered around major transportation features in supply constrained submarkets in major Sunbelt regions. The Company’s core markets are in the states of Florida, Texas, Arizona, California and North Carolina.

The Company believes its current operating cash flow and unsecured bank credit facilities provide the capacity to fund the operations of the Company, and the Company also believes it can issue common and/or preferred equity and obtain debt financing. During

2016

, EastGroup obtained unsecured debt totaling $205 million and issued 875,052 shares of common stock through its continuous common equity program, providing net proceeds to the Company of $59.3 million. EastGroup's financing and equity issuances are further described in

Liquidity and Capital Resources

.

The Company’s primary revenue is rental income; as such, EastGroup’s greatest challenge is leasing space. During

2016

, leases expired on 6,676,000 square feet (19.1% of EastGroup’s total square footage of 34,951,000), and the Company was successful in renewing or re-leasing 89% of the expiring square feet. In addition, EastGroup leased 1,778,000 square feet of other vacant space during the year. During

2016

, average rental rates on new and renewal leases increased by 11.9%. Property net operating income (PNOI) from same properties, defined as operating properties owned during the entire current period and prior year reporting period, increased 3.1% for

2016

compared to 2015.

EastGroup’s total leased percentage was 97.3% at December 31,

2016

compared to 97.2% at December 31, 2015. Leases scheduled to expire in 2017 were 13.6% of the portfolio on a square foot basis at December 31,

2016

. As of

February 14, 2017

, leases scheduled to expire during the remainder of 2017 were 10.7% of the portfolio on a square foot basis.

The Company generates new sources of leasing revenue through its acquisition and development programs. EastGroup continues to see targeted development as a contributor to the Company’s long-term growth. The Company mitigates risks associated with development through a Board-approved maximum level of land held for development and by adjusting development start dates according to leasing activity.

During

2016

, EastGroup acquired Flagler Center, a three-building, 358,000 square foot business distribution complex in Jacksonville, Florida, for $24 million. Also during

2016

, the Company acquired three development-stage operating properties (996,000 square feet) in Dallas, Las Vegas and Weston (South Florida) and 197 acres of development land for $133 million. In addition, EastGroup began construction of nine development projects containing 1,234,000 square feet in Orlando, Tampa, Ft. Myers, San Antonio, Dallas and Tucson. Also in 2016, the Company transferred nine projects (1,004,000 square feet) in San Antonio, Houston, Dallas, Orlando, Tampa and Phoenix from its development program to real estate properties with costs of

$68.1 million

at the date of transfer. As of December 31, 2016, EastGroup's development program consisted of 17 buildings (2,891,000 square feet) located in San Antonio, Dallas, Orlando, Tampa, Ft. Myers, Ft. Lauderdale, Charlotte, Las Vegas, Phoenix and Tucson. The projected total cost for the development projects, which were collectively 57% leased as of

February 14, 2017

, is $235 million, of which $58 million remained to be invested as of December 31,

2016

.

During

2016

, EastGroup sold 1,256,000 square feet of operating properties and 25 acres of land, generating gross sales proceeds of $81.1 million. The Company recognized $42,170,000 in

Gain, net of loss, on sales of real estate investments

and $733,000 in

Gain on sales of non-operating real estate

(included in

Other

on the Consolidated Statements of Income and Comprehensive Income) during

2016

.

Typically, the Company initially funds its development and acquisition programs through its $335 million unsecured bank credit facilities (as discussed in

Liquidity and Capital Resources

). As market conditions permit, EastGroup issues equity and/or employs fixed-rate debt, including variable-rate debt that has been swapped to an effectively fixed rate through the use of interest rate swaps, to replace short-term bank borrowings. In March 2016, Moody's Investors Service affirmed the Company's issuer rating of Baa2 with a stable outlook. In April 2016, Fitch Ratings affirmed EastGroup's issuer rating of BBB with a stable outlook. A security rating is not a recommendation to buy, sell or hold securities and may be subject to revision or withdrawal at any time by the assigning rating agency. Each rating should be evaluated independently of any other rating. For future debt issuances, the Company intends to issue primarily unsecured fixed-rate debt, including variable-rate debt that has been swapped to an effectively fixed rate through the use of interest rate swaps. The Company may also access the public debt market in the future as a means to raise capital.

14

EastGroup has one reportable segment – industrial properties. These properties are primarily located in major Sunbelt regions of the United States, have similar economic characteristics and also meet the other criteria permitting the properties to be aggregated into one reportable segment. The Company’s chief decision makers use two primary measures of operating results in making decisions: (1) property net operating income (PNOI), defined as

Income from real estate operations

less

Expenses from real estate operations

(including market-based internal management fee expense) plus the Company's share of income and property operating expenses from its less-than-wholly-owned real estate investments, and (2) funds from operations attributable to common stockholders (FFO), defined as net income (loss) attributable to common stockholders computed in accordance with U.S. generally accepted accounting principles (GAAP), excluding gains or losses from sales of depreciable real estate property and impairment losses, plus real estate related depreciation and amortization, and after adjustments for unconsolidated partnerships and joint ventures. The Company calculates FFO based on the National Association of Real Estate Investment Trusts’ (NAREIT) definition.

PNOI is a supplemental industry reporting measurement used to evaluate the performance of the Company’s real estate investments. The Company believes the exclusion of depreciation and amortization in the industry’s calculation of PNOI provides a supplemental indicator of the properties’ performance since real estate values have historically risen or fallen with market conditions. PNOI as calculated by the Company may not be comparable to similarly titled but differently calculated measures for other real estate investment trusts (REITs). The major factors influencing PNOI are occupancy levels, acquisitions and sales, development properties that achieve stabilized operations, rental rate increases or decreases, and the recoverability of operating expenses. The Company’s success depends largely upon its ability to lease space and to recover from tenants the operating costs associated with those leases.

PNOI is comprised of

Income from real estate operations

, less

Expenses from real estate operations

plus the Company's share of income and property operating expenses from its less-than-wholly-owned real estate investments. PNOI was calculated as follows for the three fiscal years ended December 31,

2016

,

2015

and

2014

.

|

|

Years Ended December 31,

|

||||||||

|

2016

|

2015

|

2014

|

|||||||

|

(In thousands)

|

|||||||||

|

Income from real estate operations

|

$

|

252,961

|

|

234,918

|

|

219,706

|

|

||

|

Expenses from real estate operations

|

(74,347

|

)

|

(67,402

|

)

|

(62,797

|

)

|

|||

|

Noncontrolling interest in PNOI of consolidated 80% joint ventures

|

(823

|

)

|

(851

|

)

|

(848

|

)

|

|||

|

PNOI from 50% owned unconsolidated investment

|

906

|

|

842

|

|

789

|

|

|||

|

PROPERTY NET OPERATING INCOME

|

$

|

178,697

|

|

167,507

|

|

156,850

|

|

||

Income from real estate operations

is comprised of rental income, expense reimbursement pass-through income and other real estate income including lease termination fees.

Expenses from real estate operations

is comprised of property taxes, insurance, utilities, repair and maintenance expenses, management fees, other operating costs and bad debt expense. Generally, the Company’s most significant operating expenses are property taxes and insurance. Tenant leases may be net leases in which the total operating expenses are recoverable, modified gross leases in which some of the operating expenses are recoverable, or gross leases in which no expenses are recoverable (gross leases represent only a small portion of the Company’s total leases). Increases in property operating expenses are fully recoverable under net leases and recoverable to a high degree under modified gross leases. Modified gross leases often include base year amounts and expense increases over these amounts are recoverable. The Company’s exposure to property operating expenses is primarily due to vacancies and leases for occupied space that limit the amount of expenses that can be recovered.

15

The following table presents reconciliations of Net Income to PNOI for the three fiscal years ended December 31,

2016

,

2015

and

2014

.

|

|

Years Ended December 31,

|

||||||||

|

2016

|

2015

|

2014

|

|||||||

|

(In thousands)

|

|||||||||

|

NET INCOME

|

$

|

96,094

|

|

48,399

|

|

48,473

|

|

||

|

Gain, net of loss, on sales of real estate investments

|

(42,170

|

)

|

(2,903

|

)

|

(9,188

|

)

|

|||

|

Gain on sales of non-operating real estate

|

(733

|

)

|

(123

|

)

|

(98

|

)

|

|||

|

Interest income

|

(255

|

)

|

(258

|

)

|

(479

|

)

|

|||

|

Other income

|

(86

|

)

|

(90

|

)

|

(123

|

)

|

|||

|

Interest rate swap ineffectiveness

|