|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Table of Contents

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 10-K

| x |

ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the Fiscal Year Ended December 31, 2011

or

| ¨ |

TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the transition period from to

Commission File Number: 1-11718

EQUITY LIFESTYLE PROPERTIES, INC.

(Exact name of registrant as specified in its charter)

| Maryland | 36-3857664 | |

|

(State or Other Jurisdiction of

Incorporation or Organization) |

(I.R.S. Employer

Identification No.) |

|

|

Two North Riverside Plaza,

Suite 800, Chicago, Illinois |

60606 | |

|

(Address of Principal

Executive Offices) |

(Zip Code) | |

(312) 279-1400

(Registrant’s Telephone Number, Including Area Code)

Securities registered pursuant to Section 12(b) of the Act:

| Common Stock, $.01 Par Value | New York Stock Exchange | |

| (Title of Class) | (Name of exchange on which registered) | |

|

8.034% Series A Cumulative

Redeemable Perpetual Preferred Stock |

New York Stock Exchange | |

| (Title of Class) | (Name of exchange on which registered) | |

Securities registered pursuant to Section 12(g) of the Act:

None

Indicate by check mark if the Registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. Yes x No ¨

Indicate by check mark if the Registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Act. Yes ¨ No x

Indicate by check mark whether the Registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the Registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes x No ¨

Indicate by check mark whether the Registrant has submitted electronically and posted on its corporate Website, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T (§232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files). Yes x No ¨

Indicate by check mark if disclosure of delinquent filers pursuant to Item 405 of Regulation S-K (§229.405 of this chapter) is not contained herein, and will not be contained, to the best of the Registrant’s knowledge, in definitive proxy or information statements incorporated by reference in Part III of this Form 10-K or any amendment to this Form 10-K. ¨

Indicate by check mark whether the Registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer or a smaller reporting company. See definitions of “large accelerated filer,” “accelerated filer” and “smaller reporting company” in Rule 12b-2 of the Exchange Act. (Check one):

|

Large accelerated filer |

x |

Accelerated filer |

¨ |

|||

|

Non-accelerated filer |

¨ (Do not check if a smaller reporting company) |

Smaller reporting company |

¨ |

|||

Indicate by check mark whether the Registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act). Yes ¨ No x

The aggregate market value of voting stock held by non-affiliates was approximately $2,137.1 million as of June 30, 2011 based upon the closing price of $62.44 on such date using beneficial ownership of stock rules adopted pursuant to Section 13 of the Securities Exchange Act of 1934 to exclude voting stock owned by Directors and Officers, some of whom may not be held to be affiliates upon judicial determination.

At February 27, 2012, 41,296,856 shares of the Registrant’s common stock were outstanding.

DOCUMENTS INCORPORATED BY REFERENCE:

Part III incorporates by reference portions of the Registrant’s Proxy Statement relating to the Annual Meeting of Stockholders to be held on May 8, 2012.

Table of Contents

Equity LifeStyle Properties, Inc.

| Page | ||||||||

|

PART I. |

||||||||

|

Item 1. |

1 | |||||||

|

Item 1A. |

8 | |||||||

|

Item 1B. |

18 | |||||||

|

Item 2. |

18 | |||||||

|

Item 3. |

28 | |||||||

|

Item 4. |

28 | |||||||

|

PART II. |

||||||||

|

Item 5. |

29 | |||||||

|

Item 6. |

30 | |||||||

|

Item 7. |

Management’s Discussion and Analysis of Financial Condition and Results of Operations |

33 | ||||||

|

Item 7A. |

55 | |||||||

| 55 | ||||||||

|

Item 8. |

57 | |||||||

|

Item 9. |

Changes in and Disagreements with Accountants on Accounting and Financial Disclosure |

58 | ||||||

|

Item 9A. |

58 | |||||||

|

Item 9B. |

59 | |||||||

|

PART III. |

||||||||

|

Item 10. |

60 | |||||||

|

Item 11. |

60 | |||||||

|

Item 12. |

Security Ownership of Certain Beneficial Owners and Management and Related Stockholder Matters |

60 | ||||||

|

Item 13. |

Certain Relationships and Related Transactions and Director Independence |

60 | ||||||

|

Item 14. |

60 | |||||||

|

PART IV. |

||||||||

|

Item 15. |

61 | |||||||

- i -

Table of Contents

| Item 1. | Business |

Equity LifeStyle Properties, Inc.

General

Equity LifeStyle Properties, Inc., a Maryland corporation, together with MHC Operating Limited Partnership (the “Operating Partnership”) and its other consolidated subsidiaries (the “Subsidiaries”), are referred to herein as the “Company” and “ELS.” ELS elected to be taxed as a real estate investment trust (“REIT”), for U.S. federal income tax purposes commencing with its taxable year ended December 31, 1993.

The Company is a fully integrated owner and operator of lifestyle-oriented properties (“Properties”). The Company leases individual developed areas (“sites”) with access to utilities for placement of factory built homes, cottages, cabins or recreational vehicles (“RVs”). Customers may lease individual sites or enter right-to-use contracts providing the customer access to specific Properties for limited stays. The Company was formed in December 1992 to continue the property operations, business objectives and acquisition strategies of an entity that had owned and operated Properties since 1969. As of December 31, 2011, the Company owned or had an ownership interest in a portfolio of 382 Properties located throughout the United States and Canada, consisting of 141,132 residential sites. These Properties are located in 32 states and British Columbia (with the number of Properties in each state or province shown parenthetically) as follows: Florida (119), California (49), Arizona (41), Michigan (15), Pennsylvania (15), Texas (15), Washington (15), Colorado (10), Oregon (9), North Carolina (8), Delaware (7), Indiana (7), Nevada (7), New York (7), Virginia (7), Maine (5), Massachusetts (5), Wisconsin (5), Idaho (4), Illinois (4), Minnesota (4), New Jersey (4), South Carolina (3), Utah (3), Maryland (2), New Hampshire (2), North Dakota (2), Ohio (2), Tennessee (2), Alabama (1), Connecticut (1), Kentucky (1), and British Columbia (1).

Properties are designed and improved for several home options of various sizes and designs that are produced off-site, installed and set on designated sites (“Site Set”) within the Properties. These homes can range from 400 to over 2,000 square feet. The smallest of these homes are referred to as “Resort Cottages.” Properties may also have sites that can accommodate a variety of RVs. Properties generally contain centralized entrances, internal road systems and designated sites. In addition, Properties often provide a clubhouse for social activities and recreation and other amenities, which may include restaurants, swimming pools, golf courses, lawn bowling, shuffleboard courts, tennis courts, laundry facilities and cable television service. In some cases, utilities are provided or arranged for by the Company; otherwise, the customer contracts for the utility directly. Some Properties provide water and sewer service through municipal or regulated utilities, while others provide these services to customers from on-site facilities. Properties generally are designed to attract retirees, empty-nesters, vacationers and second home owners; however, certain of the Company’s Properties focus on affordable housing for families. The Company focuses on owning properties in or near large metropolitan markets and retirement and vacation destinations.

Employees and Organizational Structure

The Company has an annual average of approximately 3,500 full-time, part-time and seasonal employees dedicated to carrying out its operating philosophy and strategies of value enhancement and service to its customers. The operations of each Property are coordinated by an on-site team of employees that typically includes a manager, clerical staff and maintenance workers, each of whom works to provide maintenance and care to the Properties. Direct supervision of on-site management is the responsibility of the Company’s regional vice presidents and regional and district managers. These individuals have substantial experience in addressing the needs of customers and in finding or creating innovative approaches to maximize value and increase cash flow from property operations. Complementing this field management staff are approximately 200 full-time corporate employees who assist on-site and regional management in all property functions.

1

Table of Contents

Formation of the Company

The operations of the Company are conducted primarily through the Operating Partnership. The Company contributed the proceeds from its initial public offering in 1993 and subsequent offerings to the Operating Partnership for a general partnership interest. In 2004, the general partnership interest was contributed to MHC Trust, a private REIT subsidiary owned by the Company. The financial results of the Operating Partnership and the Subsidiaries are consolidated in the Company’s consolidated financial statements. In addition, since certain activities, if performed by the Company, may not be qualifying REIT activities under the Internal Revenue Code of 1986, as amended (the “Code”), the Company has formed taxable REIT subsidiaries, as defined in the Code, to engage in such activities.

Realty Systems, Inc. (“RSI”) is a wholly owned taxable REIT subsidiary of the Company that is engaged in the business of purchasing and selling or leasing Site Set homes that are located in Properties owned and managed by the Company. RSI also provides brokerage services to residents at such Properties who move from a Property but do not relocate their homes. RSI may provide brokerage services, in competition with other local brokers, by seeking buyers for the Site Set homes. Subsidiaries of RSI also operate ancillary activities at certain Properties, such as golf courses, pro shops, stores and restaurants. Several Properties are also wholly owned by taxable REIT subsidiaries of the Company.

Business Objectives and Operating Strategies

The Company’s primary business objective is to maximize both current income and long-term growth in income. The Company’s operating strategy is to own and operate the highest quality properties in sought-after locations near urban areas and retirement and vacation destinations across the United States.

The Company focuses on properties that have strong cash flow and plans to hold such properties for long-term investment and capital appreciation. In determining cash flow potential, the Company evaluates its ability to attract and retain high quality customers to its Properties who take pride in the Property and in their homes. The Company’s investment, operating and financing strategies include:

| • |

Providing consistently high levels of services and amenities in attractive surroundings to foster a strong sense of community and pride of home ownership; |

| • |

Efficiently managing the Properties to increase operating margins by controlling expenses, increasing occupancy and maintaining competitive market rents; |

| • |

Increasing income and property values by strategic expansion and, where appropriate, renovation of the Properties |

| • |

Utilizing management information systems to evaluate potential acquisitions, identify and track competing properties and monitor customer satisfaction; |

| • |

Selectively acquiring properties that have potential for long-term cash flow growth and creating property concentrations in and around major metropolitan areas and retirement or vacation destinations to capitalize on operating synergies and incremental efficiencies; and |

| • |

Managing the Company’s debt balances such that the Company maintains financial flexibility, has minimal exposure to interest rate fluctuations and maintains an appropriate degree of leverage to maximize return on capital. |

The Company focuses on creating an attractive residential environment by providing a well-maintained, comfortable Property with a variety of recreational and social activities and superior amenities, as well as offering a multitude of lifestyle housing choices. In addition, the Company regularly conducts evaluations of the cost of housing in the marketplaces in which its Properties are located and surveys rental rates of competing properties. From time to time the Company also conducts satisfaction surveys of its customers to determine the

2

Table of Contents

factors they consider most important in choosing a property. The Company seeks to improve site utilization and efficiency by tracking types of customers and usage patterns and marketing to those specific customer groups.

These business objectives and their implementation are determined by the Company’s Board of Directors and may be changed at any time.

Acquisitions and Dispositions

Over the last decade the Company’s portfolio of Properties has grown significantly from 148 owned or partly owned Properties with over 50,000 sites to 382 owned or partly-owned Properties with over 141,000 sites. During the year ended December 31, 2011, the Company acquired 75 Properties with over 30,000 sites. The Company continually reviews the Properties in its portfolio to ensure that they fit the Company’s business objectives. Over the last five years, the Company sold 12 Properties, and it redeployed capital to markets it believes have greater long-term potential. In that same time period the Company acquired 84 Properties located in high growth areas such as Florida, Arizona and California.

The Company believes that opportunities for property acquisitions are still available. Increasing acceptability of and demand for a lifestyle that includes Site Set homes and RVs, as well as continued constraints on development of new properties, adds to the attractiveness of the Company’s Properties as investments. The Company believes it has a competitive advantage in the acquisition of additional properties due to its experienced management, significant presence in major real estate markets and substantial capital resources. The Company is actively seeking to acquire additional properties and is engaged in various stages of negotiations relating to the possible acquisition of a number of properties. At any time these negotiations are at varying stages, which may include contracts outstanding, to acquire certain Properties, which are subject to the satisfactory completion of the Company’s due diligence review.

The Company anticipates that new acquisitions will generally be located in the United States, although it may consider other geographic locations provided they meet certain acquisition criteria. The Company utilizes market information systems to identify and evaluate acquisition opportunities, including the use of a market database to review the primary economic indicators of the various locations in which it expects to expand its operations. Acquisitions will be financed from the most appropriate sources of capital, which may include undistributed funds from operations, issuance of additional equity securities, sales of investments, collateralized and uncollateralized borrowings and issuance of debt securities. In addition, the Company may acquire properties in transactions that include the issuance of limited partnership interests in the Operating Partnership (“Units”) as consideration for the acquired properties. The Company believes that an ownership structure that includes the Operating Partnership will permit it to acquire additional properties in transactions that may defer all or a portion of the sellers’ tax consequences.

When evaluating potential acquisitions, the Company considers such factors as:

| • |

The replacement cost of the property, including land values, entitlements and zoning; |

| • |

The geographic area and type of the property; |

| • |

The location, construction quality, condition and design of the property; |

| • |

The current and projected cash flow of the property and the ability to increase cash flow; |

| • |

The potential for capital appreciation of the property; |

| • |

The terms of tenant leases or usage rights, including the potential for rent increases; |

| • |

The potential for economic growth and the tax and regulatory environment of the community in which the property is located; |

| • |

The potential for expansion of the physical layout of the property and the number of sites; |

3

Table of Contents

| • |

The occupancy and demand by customers for properties of a similar type in the vicinity and the customers’ profile; |

| • |

The prospects for liquidity through sale, financing or refinancing of the property; and |

| • |

The competition from existing properties and the potential for the construction of new properties in the area. |

When evaluating potential dispositions, the Company considers such factors as:

| • |

Its ability to sell the Property at a price that it believes will provide an appropriate return for its stockholders; |

| • |

Its desire to exit certain non-core markets and recycle the capital into core markets; and |

| • |

Whether the Property meets its current investment criteria. |

When investing capital, the Company considers all potential uses of the capital, including returning capital to its stockholders. The Company’s Board of Directors continues to review the conditions under which it will repurchase the Company’s stock. These conditions include, but are not limited to, market price, balance sheet flexibility, other opportunities and capital requirements.

Property Expansions

Several of the Company’s Properties have available land for expanding the number of sites available to be utilized by its customers. Development of these sites (“Expansion Sites”) is evaluated based on the following: local market conditions; ability to subdivide; accessibility through the Property or externally; infrastructure needs including utility needs and access as well as additional common area amenities; zoning and entitlement; costs and uses of working capital; topography; and ability to market new sites. When justified, development of Expansion Sites allows the Company to leverage existing facilities and amenities to increase the income generated from the Properties. Where appropriate, facilities and amenities may be upgraded or added to certain Properties to make those Properties more attractive in their markets. The Company’s acquisition philosophy includes owning Properties with potential Expansion Site development. Approximately 79 of the Company’s Properties have expansion potential, with up to approximately 5,300 acres available for expansion.

Leases or Usage Rights

At the Company’s Properties, a typical lease entered into between the owner or renter of a home and the Company for the rental of a site is for a month-to-month or year-to-year term, renewable upon the consent of both parties or, in some instances, as provided by statute. These leases are cancelable, depending on applicable law, for non-payment of rent, violation of Property rules and regulations or other specified defaults. Non-cancelable long-term leases, with remaining terms ranging up to ten years, are in effect at certain sites in 31 of the Properties. Some of these leases are subject to rental rate increases based on the Consumer Price Index (“CPI”), in some instances taking into consideration market conditions, certain floors and ceilings and allowing for pass-throughs of certain items such as real estate taxes, utility expenses and capital expenditures. Generally, market rate adjustments, if appropriate, are made on an annual basis. At Properties zoned for RV use, long-term customers typically enter into rental agreements and many customers prepay for their stays. Many resort customers also leave deposits to reserve a site for the following year. Generally these customers cannot live full time on the Property. At resort Properties designated for use by customers who have entered a right-to-use or membership contract, the contract generally grants the customer access to designated Properties on a continuous basis of up to 14 days. The customer may make a nonrefundable upfront payment, and annual dues payments are required to renew the contract. Most of the contracts provide for an annual dues increase, usually based on increases in the CPI. Approximately 35% of current customers are not subject to annual dues increases in accordance with the terms of their contracts, generally because the customers are over 61 years old or in certain other limited circumstances.

4

Table of Contents

Regulations and Insurance

General . The Company’s Properties are subject to a variety of laws, ordinances and regulations, including regulations relating to recreational facilities such as swimming pools, clubhouses and other common areas, regulations relating to providing utility services, such as electricity, and regulations relating to operating water and wastewater treatment facilities at certain of its Properties. The Company believes that each Property has all material permits and approvals necessary to operate.

Rent Control Legislation . At certain of the Company’s Properties, principally in California, state and local rent control laws limit the Company’s ability to increase rents and to recover increases in operating expenses and the costs of capital improvements. Enactment of such laws has been considered from time to time in other jurisdictions. The Company presently expects to continue to maintain Properties, and may purchase additional properties, in markets that are either subject to rent control or in which rent-limiting legislation exists or may be enacted. For example, Florida has enacted a law requiring that rental increases be reasonable. Also, certain jurisdictions in California in which the Company owns Properties limit rent increases to changes in the CPI or some percentage of it. As part of the Company’s effort to realize the value of Properties subject to restrictive regulation, it has initiated lawsuits against several municipalities imposing such regulations in an attempt to balance the interests of its stockholders with the interests of its customers (see Item 3. “Legal Proceedings”). Further, at certain of the Company’s Properties primarily used as membership campgrounds, state statutes limit the Company’s ability to close a Property unless a reasonable substitute property is made available for members’ use. Many states also have consumer protection laws regulating right-to-use or campground membership sales and the financing of such sales. Some states have laws requiring the Company to register with a state agency and obtain a permit to market (see Item 1A. “Risk Factors”).

Insurance . The Properties are insured against all risks causing property damage and business interruption caused by fire, flood, earthquake, or windstorm, and the relevant insurance policies contain various deductible requirements, such as coverage limits and particular exclusions. The Company’s current property and casualty insurance policies, which it plans to renew, expire on April 1, 2012. The Company has a $100 million loss limit with respect to its all-risk property insurance program including named windstorms, which include, for example, hurricanes. This loss limit is subject to additional sub-limits as set forth in the policy form, including, among others, a $25 million loss limit for an earthquake in California. Policy deductibles primarily range from a $125,000 minimum to 5% per unit of insurance for most catastrophic events. A deductible indicates ELS’ maximum exposure, subject to policy sub-limits, in the event of a loss.

INDUSTRY

The Company believes that modern properties similar to its Properties provide an opportunity for increased cash flows and appreciation in value. These may be achieved through increases in occupancy rates and rents, as well as expense controls, expansion of existing Properties and opportunistic acquisitions, for the following reasons:

| • |

Barriers to Entry : The Company believes that the supply of new properties in locations targeted by the Company will be constrained by barriers to entry. The most significant barrier has been the difficulty of securing zoning permits from local authorities. This has been the result of (i) the public’s historically poor perception of manufactured housing, and (ii) the fact that properties generate less tax revenue than conventional housing properties because the homes are treated as personal property (a benefit to the homeowner) rather than real property. Another factor that creates substantial barriers to entry is the length of time between investment in a property’s development and the attainment of stabilized occupancy and the generation of revenues. The initial development of the infrastructure may take up to two or three years. Once a property is ready for occupancy, it may be difficult to attract customers to an empty property. Substantial occupancy levels may take several years to achieve. |

5

Table of Contents

| • |

Industry Consolidation : According to various industry reports, there are approximately 50,000 manufactured home properties and approximately 8,750 RV properties (excluding government owned properties) in North America. Most of these properties are not operated by large owner/operators, and of the RV properties approximately 1,300 contain 200 sites or more. The Company believes that this relatively high degree of fragmentation provides the Company, as a national organization with experienced management and substantial financial resources, the opportunity to purchase additional properties as evidenced by the acquisitions during the year ended December 31, 2011. |

| • |

Customer Base : The Company believes that properties tend to achieve and maintain a stable rate of occupancy due to the following factors: (i) customers typically own their own homes, (ii) properties tend to foster a sense of community as a result of amenities such as clubhouses and recreational and social activities, (iii) since moving a Site Set home from one property to another involves substantial cost and effort, customers often sell their homes in-place (similar to site-built residential housing) with no interruption of rental payments to the Company. |

| • |

Lifestyle Choice : According to the Recreational Vehicle Industry Association (“RVIA”), nearly one in ten U.S. vehicle-owning households owns an RV and there are 8.9 million current RV owners. The 77 million people born from 1946 to 1964 or “baby boomers” make up the fastest growing segment of this market. According to U.S. Census figures, every day 10,000 Americans turn 50. The Company believes that this population segment, seeking an active lifestyle, will provide opportunities for future cash flow growth for the Company. Current RV owners, once finished with the more active RV lifestyle, will often seek more permanent retirement or vacation establishments. Site Set housing has become an increasingly popular housing alternative for retirement, second-home, and “empty-nest” living. According to U.S. Census figures, the baby-boom generation will constitute almost 17% of the U.S. population within the next 20 years. Among those individuals who are nearing retirement (age 46 to 64), approximately 47% plan on moving upon retirement. |

The Company believes that the housing choices in its Properties are especially attractive to such individuals throughout this lifestyle cycle. The Company’s Properties offer an appealing amenity package, close proximity to local services, social activities, low maintenance and a secure environment. In fact, many of the Company’s Properties allow for this cycle to occur within a single Property.

| • |

Construction Quality : Since 1976, all factory built housing has been required to meet stringent federal standards, resulting in significant increases in quality. The Department of Housing and Urban Development’s (“HUD”) standards for Site Set housing construction quality are the only federal standards governing housing quality of any type in the United States. Site Set homes produced since 1976 have received a “red and silver” government seal certifying that they were built in compliance with the federal code. The code regulates Site Set home design and construction, strength and durability, fire resistance and energy efficiency, and the installation and performance of heating, plumbing, air conditioning, thermal and electrical systems. In newer homes, top grade lumber and dry wall materials are common. Also, manufacturers are required to follow the same fire codes as builders of site-built structures. In addition, although Resort Cottages do not come under the same regulations, many of the manufacturers of Site Set homes also produce Resort Cottages with many of the same quality standards. |

| • |

Comparability to Site-Built Homes: The Site Set housing industry has experienced a trend towards multi-section homes. Many modern Site Set homes are longer (up to 80 feet, compared to 50 feet in the 1960’s) and wider than earlier models. Many such homes have nine-foot ceilings or vaulted ceilings, fireplaces and as many as four bedrooms and closely resemble single-family ranch-style site-built homes. At the Company’s Properties, there is an active resale market for these larger homes. |

| • |

Second Home Demographics : According to 2011 National Association of Realtors (“NAR”) reports, sales of second homes in 2010 accounted for 27% of residential transactions, or 1.41 million second-home sales in 2010. There were approximately 7.9 million vacation homes in 2010. The typical vacation-home buyer is 49 years old and earned $99,500 in 2010. According to 2010 NAR reports, |

6

Table of Contents

|

approximately 32% of vacation homes were purchased in the south; 24% were purchased in the west; 21% were purchased in the northeast; and 20% were purchased in the Midwest. In looking ahead, NAR believes that baby boomers are still in their peak earning years, and the leading edge of their generation is approaching retirement. As they continue to have the financial wherewithal to purchase a second home as a vacation property, investment opportunity, or perhaps as a retirement retreat, those baby boomers will continue to drive the market for second homes. The Company believes it is likely that over the next decade it will continue to see historically high levels of second-home sales, and resort homes and cottages in its Properties will continue to provide a viable second-home alternative to site-built homes. |

Notwithstanding the Company’s belief that the industry information highlighted above provides the Company with significant long-term growth opportunities, its short-term growth opportunities could be disrupted by the following:

| • |

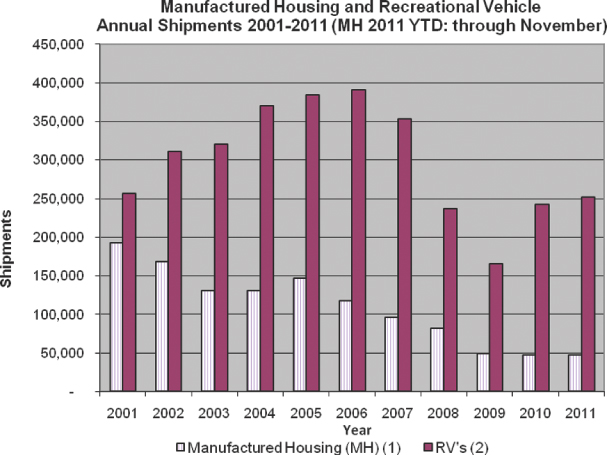

Shipments —According to statistics compiled by the U.S. Census Bureau, shipments of new manufactured homes declined from 2005 through 2009. Shipments for 2010 as compared to 2009 were flat. Although new manufactured home shipments continue to be below historical levels, shipments for the first eleven months in 2011 increased over 1% to 47,800 units as compared to shipments for the first eleven months in 2010 of 47,300 units. According to the RVIA, wholesale shipments of RVs increased 4.1% in 2011 to 252,300 units as compared to 2010, which continued a positive trend in RV shipments that started in late 2009. Certain industry experts have predicted that 2012 RV shipments will decrease 4.6%, as compared to 2011, to 240,600. |

| (1) |

Source: Institute for Building Technology and Safety |

7

Table of Contents

| (2) |

Source: RVIA |

| • |

Sales —Retail sales of RVs increased almost 4% to 182,400 for the first 11 months of 2011, as compared to 175,600 the first 11 months of 2010. A total of 183,200 RVs were sold during the year ended December 31, 2010, representing an increase of almost 8% over the prior year. The Company believes that consumers remain concerned about the current economy, and by prospects that the economy might remain sluggish in the years ahead. However, the enduring appeal of the RV lifestyle has translated into continued strength in RV sales despite the economic turmoil. According to RVIA, RV ownership has reached record levels: 8.9 million American households now own an RV, the highest level ever recorded, which constitutes an increase of 16% since 2001 and 64% since 1980. RV sales could continue to benefit as aging baby-boomers continue to enter the age range in which RV ownership is highest. |

| • |

Availability of financing —The current credit crisis has made it difficult for manufactured home and RV manufacturers to obtain floor plan financing and for potential customers to obtain loans for manufactured home or RV purchases. Further, legislation enacted in 2010 known as the SAFE Act (Safe Mortgage Licensing Act) requires community owners interested in financing customer purchases of manufactured homes to register as a mortgage loan originator in states in which they engage in such financing. These requirements are generally more burdensome for lenders financing the purchase of manufactured homes than for lenders financing the purchase of site-built homes. In addition, as compared to financing available to owners and purchasers of site-built single family homes, available financing for a manufactured home involves higher down payments, higher FICO scores, higher interest rates and shorter maturity. Certain government stimulus packages have also provided government guarantees for site-built single family home loans, thereby increasing the supply of financing for that market. |

Please see the Company’s risk factors, financial statements and related notes contained in this Form 10-K for more detailed information.

Available Information

The Company files reports electronically with the Securities and Exchange Commission (“SEC”). The public may read and copy any materials the Company files with the SEC at the SEC’s Public Reference Room at 100 F Street, NE, Washington, DC 20549. The public may obtain information on the operation of the Public Reference Room by calling the SEC at 1-800-SEC-0330. The SEC maintains an Internet site that contains reports, proxy information and statements and other information regarding issuers that file electronically with the SEC at http://www.sec.gov . The Company maintains an Internet site with information about the Company and hyperlinks to its filings with the SEC at http://www.equitylifestyle.com , free of charge. Requests for copies of the Company’s filings with the SEC and other investor inquiries should be directed to:

Investor Relations Department

Equity LifeStyle Properties, Inc.

Two North Riverside Plaza

Chicago, Illinois 60606

Phone: 1-800-247-5279

e-mail: investor_relations@equitylifestyle.com

| Item 1A. | Risk Factors |

The Company’s Performance and Common Stock Value Are Subject to Risks Associated With the Real Estate Industry.

Adverse Economic Conditions and Other Factors Could Adversely Affect the Value of the Company’s Properties and the Company’s Cash Flow . Several factors may adversely affect the economic performance and value of the Company’s Properties. These factors include:

| • |

changes in the national, regional and local economic climate; |

8

Table of Contents

| • |

local conditions such as an oversupply of lifestyle-oriented properties or a reduction in demand for lifestyle-oriented properties in the area, the attractiveness of the Company’s Properties to customers, competition from manufactured home communities and other lifestyle-oriented properties and alternative forms of housing (such as apartment buildings and site-built single family homes); |

| • |

the ability of manufactured home and RV manufacturers to adapt to changes in the economic climate and the availability of units from these manufacturers; |

| • |

the ability of the Company’s potential customers to sell or lease their existing site-built residences in order to purchase resort homes or cottages in the Company’s Properties, and heightened price sensitivity for seasonal and second homebuyers; |

| • |

the possible reduced ability of the Company’s potential customers to obtain financing on the purchase of resort homes, resort cottages or RVs; |

| • |

performance of chattel loans purchased in connection with the Acquisition (see Note 19 in the Notes to the Consolidated Financial Statements contained in this Form 10-K for further discussion of the Acquisition); |

| • |

government stimulus intended to primarily benefit purchasers of site-built housing; |

| • |

fluctuations in the availability and price of gasoline, especially for the Company’s transient customers; |

| • |

the Company’s ability to collect rent, annual payments and principal and interest from customers and pay or control maintenance, insurance and other operating costs (including real estate taxes), which could increase over time; |

| • |

the failure of the Company’s assets to generate income sufficient to pay its expenses, service its debt and maintain its Properties, which may adversely affect the Company’s ability to make expected distributions to its stockholders; |

| • |

the Company’s inability to meet mortgage payments on any Property that is mortgaged, in which case the lender could foreclose on the mortgage and take the Property; |

| • |

interest rate levels and the availability of financing, which may adversely affect the Company’s financial condition; |

| • |

changes in laws and governmental regulations (including rent control laws and regulations governing usage, zoning and taxes), which may adversely affect the Company’s financial condition; |

| • |

poor weather, especially on holiday weekends in the summer, which could reduce the economic performance of the Company’s Northern resort Properties; and |

| • |

the Company’s ability to sell new or upgraded right-to-use contracts and to retain customers who have previously purchased a right-to-use contract. |

New Acquisitions May Fail to Perform as Expected and Competition for Acquisitions May Result in Increased Prices for Properties . The Company intends to continue to acquire properties. Newly acquired Properties may fail to perform as expected. The Company may underestimate the costs necessary to bring an acquired property up to standards established for its intended market position. Difficulties in integrating acquisitions may prove costly or time-consuming and could divert management attention. Additionally, the Company expects that other real estate investors with significant capital will compete with it for attractive investment opportunities. These competitors include publicly traded REITs, private REITs and other types of investors. Such competition increases prices for properties. The Company expects to acquire properties with cash from secured or unsecured financings, proceeds from offerings of equity or debt, undistributed funds from operations and sales of investments. The Company may not be in a position or have the opportunity in the future to make suitable property acquisitions on favorable terms.

The intended benefits of the Company’s acquisition of a portfolio of 74 manufactured home communities and one RV resort during the year ended December 31, 2011 may not be realized, which could have a negative impact on the market price of the Company’s common stock.

9

Table of Contents

The acquisition poses risks for our ongoing operations, including that:

| • |

senior management’s attention may be diverted from the management of daily operations to the integration of the acquisition portfolio; |

| • |

costs and expenses associated with any undisclosed or potential liabilities; |

| • |

the acquisition portfolio may not perform as well as the Company anticipates; and |

| • |

unforeseen difficulties may arise in integrating the acquisition portfolio into the Company’s portfolio. |

As a result of the foregoing, the Company cannot assure you that these acquisitions will be accretive to it in the near term or at all. Furthermore, if the Company fails to realize the intended benefits of the acquisition, the market price of its common stock could decline to the extent that the market price reflects those benefits.

Because Real Estate Investments Are Illiquid, The Company May Not be Able to Sell Properties When Appropriate . Real estate investments generally cannot be sold quickly. The Company may not be able to vary its portfolio promptly in response to economic or other conditions, forcing the Company to accept lower than market value. This inability to respond promptly to changes in the performance of the Company’s investments could adversely affect its financial condition and ability to service debt and make distributions to its stockholders.

Some Potential Losses Are Not Covered by Insurance. The Company carries comprehensive insurance coverage for losses resulting from property damage, environmental, liability claims and business interruption on all of its Properties. In addition the Company carries liability coverage for other activities not specifically related to property operations. These coverages include, but are not limited to, Directors & Officers liability, Employer Practices liability and Fiduciary liability. The Company believes that the policy specifications and coverage limits of these policies should be adequate and appropriate. There are, however, certain types of losses, such as lease and other contract claims that generally are not insured. Should an uninsured loss or a loss in excess of coverage limits occur, the Company could lose all or a portion of the capital it has invested in a Property or the anticipated future revenue from a Property. In such an event, the Company might nevertheless remain obligated for any mortgage debt or other financial obligations related to the Property.

The Company’s current property and casualty insurance policies, which it plans to renew, expire on April 1, 2012. The Company has a $100 million loss limit with respect to its all-risk property insurance program including named windstorms, which include, for example, hurricanes. This loss limit is subject to additional sub-limits as set forth in the policy form, including, among others, a $25 million loss limit for an earthquake in California. Policy deductibles primarily range from a $125,000 minimum to 5% per unit of insurance for most catastrophic events. A deductible indicates ELS’ maximum exposure, subject to policy sub-limits, in the event of a loss.

There can be no assurance that the actions of the U.S. government, Federal Reserve and other governmental and regulatory bodies instituted for the purpose of stabilizing the financial markets, or market response to those actions, will achieve the intended effect, and the Company’s business may not benefit from or may be adversely impacted by these actions, and further government or market developments could adversely impact the Company . In response to market disruptions, legislators and financial regulators implemented a number of mechanisms designed to add stability to the financial markets, including the provision of direct and indirect assistance to distressed financial institutions, assistance by the banking authorities in arranging acquisitions of weakened banks and broker-dealers, implementation of programs by the Federal Reserve to provide liquidity to the commercial paper markets and temporary prohibitions on short sales of certain financial institution securities. Numerous actions have been taken by the Federal Reserve, Congress, U.S. Treasury, SEC and others to address the liquidity and credit crisis that followed the sub-prime crisis that commenced in 2007. It is not clear at this time what long-term impact the liquidity and funding initiatives of the Federal Reserve and other agencies that have been previously announced, and any additional programs that may be initiated in the future, will have on the

10

Table of Contents

financial markets, including the extreme levels of volatility and limited credit availability currently being experienced, or on the U.S. banking and financial industries and the broader U.S. and global economies. Specifically, the Company believes that programs intended to provide relief to current or potential site-built or stick-built single family homeowners, and not purchasers of Site-Set homes who lease the underlying land and RV’s, negatively impacts its business.

Further, the overall effects of the legislative and regulatory efforts on the financial markets is uncertain, and they may not have the intended stabilization effects. Should these legislative or regulatory initiatives fail to stabilize and add liquidity to the financial markets, the Company’s business, financial condition, results of operations and prospects could be materially and adversely affected. Even if legislative or regulatory initiatives or other efforts successfully stabilize and add liquidity to the financial markets, the Company may need to modify its strategies, businesses or operations, and the Company may incur increased capital requirements and constraints or additional costs in order to satisfy new regulatory requirements or to compete in a changed business environment. It is uncertain what effects recently enacted or future legislation or regulatory initiatives will have on us.

Given the volatile nature of the current market disruption and the uncertainties underlying efforts to mitigate or reverse the disruption, the Company may not timely anticipate or manage existing, new or additional risks, contingencies or developments, including regulatory developments and trends in new products and services, in the current or future environment. The Company’s failure to do so could materially and adversely affect its business, financial condition, results of operations and prospects.

The Company’s 8.034% Series A Cumulative Redeemable Perpetual Preferred Stock Has Not Been Rated. The Company has not sought to obtain a rating for its 8.034% Series A Cumulative Redeemable Perpetual Preferred Stock (“Series A Preferred Stock”). No assurance can be given, however, that one or more rating agencies might not independently determine to issue such a rating or that such a rating, if issued, would not adversely affect the market price of the Series A Preferred Stock. In addition, the Company may elect in the future to obtain a rating of its Series A Preferred Stock, which could adversely affect the market price of its Series A Preferred Stock. Ratings only reflect the views of the rating agency or agencies issuing the ratings and such ratings could be revised downward, placed on a watch list or withdrawn entirely at the discretion of the issuing rating agency if in its judgment circumstances so warrant. Any such downward revision, placing on a watch list or withdrawal of a rating could have an adverse effect on the market price of the Series A Preferred Stock.

Adverse changes in general economic conditions may adversely affect the Company’s business.

The Company’s success is dependent upon economic conditions in the U.S. generally and in the geographic areas in which a substantial number of the Company’s Properties are located. Adverse changes in national economic conditions and in the economic conditions of the regions in which the Company conducts substantial business may have an adverse effect on the real estate values of the Company’s Properties, its financial performance and the market price of its common stock.

In a recession or under other adverse economic conditions, non-earning assets and write-downs are likely to increase as debtors fail to meet their payment obligations. Although the Company maintains reserves for credit losses and an allowance for doubtful accounts in amounts that it believes should be sufficient to provide adequate protection against potential write-downs in its portfolio, these amounts could prove to be insufficient.

Campground Membership Properties Laws and Regulations Could Adversely Affect the Value of Certain Properties and the Company’s Cash Flow.

Many of the states in which the Company does business have laws regulating right-to-use or campground membership sales. These laws generally require comprehensive disclosure to prospective purchasers, and usually give purchasers the right to rescind their purchase between three to five days after the date of sale. Some states

11

Table of Contents

have laws requiring the Company to register with a state agency and obtain a permit to market. The Company is subject to changes, from time to time, in the application or interpretation of such laws that can affect its business or the rights of its members.

In some states, including California, Oregon and Washington, laws place limitations on the ability of the owner of a campground property to close the property unless the customers at the property receive access to a comparable property. The impact of the rights of customers under these laws is uncertain and could adversely affect the availability or timing of sale opportunities or the ability of the Company to realize recoveries from Property sales.

The government authorities regulating the Company’s activities have broad discretionary power to enforce and interpret the statutes and regulations that they administer, including the power to enjoin or suspend sales activities, require or restrict construction of additional facilities and revoke licenses and permits relating to business activities. The Company monitors its sales and marketing programs and debt collection activities to control practices that might violate consumer protection laws and regulations or give rise to consumer complaints.

Certain consumer rights and defenses that vary from jurisdiction to jurisdiction may affect the Company’s portfolio of contracts receivable. Examples of such laws include state and federal consumer credit and truth-in-lending laws requiring the disclosure of finance charges, and usury and retail installment sales laws regulating permissible finance charges.

In certain states, as a result of government regulations and provisions in certain of the right-to-use or campground membership agreements, the Company is prohibited from selling more than ten memberships per site. At the present time, these restrictions do not preclude the Company from selling memberships in any state. However, these restrictions may limit the Company’s ability to utilize Properties for public usage and/or the Company’s ability to convert sites to more profitable or predictable uses, such as annual rentals.

Debt Financing, Financial Covenants and Degree of Leverage Could Adversely Affect the Company’s Economic Performance.

Scheduled Debt Payments Could Adversely Affect the Company’s Financial Condition . The Company’s business is subject to risks normally associated with debt financing. The total principal amount of the Company’s outstanding indebtedness was approximately $2.3 billion as of December 31, 2011. The Company’s substantial indebtedness and the cash flow associated with serving its indebtedness could have important consequences, including the risks that:

| • |

the Company’s cash flow could be insufficient to pay distributions at expected levels and meet required payments of principal and interest; |

| • |

the Company might be required to use a substantial portion of its cash flow from operations to pay its indebtedness, thereby reducing the availability of its cash flow to fund the implementation of its business strategy, acquisitions, capital expenditures and other general corporate purposes; |

| • |

the Company’s debt service obligations could limit its flexibility in planning for, or reacting to, changes in its business and the industry in which it operates; |

| • |

the Company may not be able to refinance existing indebtedness (which in virtually all cases requires substantial principal payments at maturity) and, if it can, the terms of such refinancing might not be as favorable as the terms of existing indebtedness; |

| • |

if principal payments due at maturity cannot be refinanced, extended or paid with proceeds of other capital transactions, such as new equity capital, the Company’s cash flow will not be sufficient in all years to repay all maturing debt; and |

12

Table of Contents

| • |

if prevailing interest rates or other factors at the time of refinancing (such as the possible reluctance of lenders to make commercial real estate loans) result in higher interest rates, increased interest expense would adversely affect cash flow and the Company’s ability to service debt and make distributions to stockholders. |

Ability to obtain mortgage financing or to refinance maturing mortgages may adversely affect the Company’s financial condition . Lenders demands on borrowers as to the quality of the collateral and related cash flows may make it challenging to secure financing at all or on attractive terms. If financing proceeds are no longer available for any reason or if terms are no longer attractive, these factors may adversely affect cash flow and the Company’s ability to service debt and make distributions to stockholders.

Financial Covenants Could Adversely Affect the Company’s Financial Condition . If a Property is mortgaged to secure payment of indebtedness, and the Company is unable to meet mortgage payments, the mortgagee could foreclose on the Property, resulting in loss of income and asset value. The mortgages on the Company’s Properties contain customary negative covenants, which among other things limit the Company’s ability, without the prior consent of the lender, to further mortgage the Property and to discontinue insurance coverage. In addition, the Company’s unsecured credit facilities contain certain customary restrictions, requirements and other limitations on the Company’s ability to incur indebtedness, including total debt-to-assets ratios, debt service coverage ratios and minimum ratios of unencumbered assets to unsecured debt. Foreclosure on mortgaged Properties or an inability to refinance existing indebtedness would likely have a negative impact on the Company’s financial condition and results of operations.

The Company’s Degree of Leverage Could Limit Its Ability to Obtain Additional Financing . The Company’s debt-to-market-capitalization ratio (total debt as a percentage of total debt plus the market value of the outstanding common stock and Units held by parties other than the Company) was approximately 43% as of December 31, 2011. The degree of leverage could have important consequences to stockholders, including an adverse effect on the Company’s ability to obtain additional financing in the future for working capital, capital expenditures, acquisitions, development or other general corporate purposes, and makes the Company more vulnerable to a downturn in business or the economy generally.

The Company may be able to incur substantially more debt, which would increase the risks associated with its substantial leverage. Despite the Company’s current indebtedness levels, it may still be able to incur substantially more debt in the future. If new debt is added to the Company’s current debt levels, an even greater portion of its cash flow will be needed to satisfy its debt service obligations. As a result, the related risks that we now face could intensify and increase the risk of a default on the Company’s indebtedness.

The Company Depends on Its Subsidiaries’ Dividends and Distributions.

Substantially all of the Company’s assets are indirectly held through the Operating Partnership. As a result, the Company has no source of operating cash flow other than from distributions from the Operating Partnership. The Company’s ability to pay dividends to holders of common stock and Series A Preferred Stock depends on the Operating Partnership’s ability first to satisfy its obligations to its creditors and then to make distributions to MHC Trust and common Unit holders (in the case of common stock distributions). Similarly, MHC Trust must satisfy its obligations to its creditors (preferred stockholders in the case of common stock distributions) before making common stock or preferred stock distributions to the Company.

Stockholders’ Ability to Effect Changes of Control of the Company is Limited.

Provisions of the Company’s Charter and Bylaws Could Inhibit Changes of Control . Certain provisions of the Company’s charter and bylaws may delay or prevent a change of control of the Company or other transactions that could provide its stockholders with a premium over the then-prevailing market price of their common stock or Series A Preferred Stock or which might otherwise be in the best interest of its stockholders. These include the

13

Table of Contents

Ownership Limit described below. Also, any future series of preferred stock may have certain voting provisions that could delay or prevent a change of control or other transaction that might involve a premium price or otherwise be beneficial to the Company’s stockholders.

Maryland Law Imposes Certain Limitations on Changes of Control . Certain provisions of Maryland law prohibit “business combinations” (including certain issuances of equity securities) with any person who beneficially owns 10% or more of the voting power of outstanding common stock, or with an affiliate of the Company who, at any time within the two-year period prior to the date in question, was the owner of 10% or more of the voting power of the outstanding voting stock (an “Interested Stockholder”), or with an affiliate of an Interested Stockholder. These prohibitions last for five years after the most recent date on which the Interested Stockholder became an Interested Stockholder. After the five-year period, a business combination with an Interested Stockholder must be approved by two super-majority stockholder votes unless, among other conditions, the Company’s common stockholders receive a minimum price for their shares and the consideration is received in cash or in the same form as previously paid by the Interested Stockholder for its shares of common stock. The Board of Directors has exempted from these provisions under the Maryland law any business combination with Samuel Zell, who is the Chairman of the Board of the Company, certain holders of Units who received them at the time of the Company’s initial public offering, the General Motors Hourly Rate Employees Pension Trust and the General Motors Salaried Employees Pension Trust, and the Company’s officers who acquired common stock at the time the Company was formed and each and every affiliate of theirs.

The Company Has a Stock Ownership Limit for REIT Tax Purposes . To remain qualified as a REIT for U.S. federal income tax purposes, not more than 50% in value of the Company’s outstanding shares of capital stock may be owned, directly or indirectly, by five or fewer individuals (as defined in the federal income tax laws applicable to REITs) at any time during the last half of any taxable year. To facilitate maintenance of the Company’s REIT qualification, the Company’s charter, subject to certain exceptions, prohibits Beneficial Ownership (as defined in the Company’s charter) by any single stockholder of more than 5% (in value or number of shares, whichever is more restrictive) of the Company’s outstanding capital stock. The Company refers to this as the “Ownership Limit.” Within certain limits, the Company’s charter permits the Board of Directors to increase the Ownership Limit with respect to any class or series of stock. The Board of Directors, upon receipt of a ruling from the IRS, opinion of counsel, or other evidence satisfactory to the Board of Directors and upon 15 days prior written notice of a proposed transfer which, if consummated, would result in the transferee owning shares in excess of the Ownership Limit, and upon such other conditions as the Board of Directors may direct, may exempt a stockholder from the Ownership Limit. Absent any such exemption, capital stock acquired or held in violation of the Ownership Limit will be transferred by operation of law to the Company as trustee for the benefit of the person to whom such capital stock is ultimately transferred, and the stockholder’s rights to distributions and to vote would terminate. Such stockholder would be entitled to receive, from the proceeds of any subsequent sale of the capital stock transferred to the Company as trustee, the lesser of (i) the price paid for the capital stock or, if the owner did not pay for the capital stock (for example, in the case of a gift, devise on other such transaction), the market price of the capital stock on the date of the event causing the capital stock to be transferred to the Company as trustee or (ii) the amount realized from such sale. A transfer of capital stock may be void if it causes a person to violate the Ownership Limit. The Ownership Limit could delay or prevent a change in control of the Company and, therefore, could adversely affect its stockholders’ ability to realize a premium over the then-prevailing market price for their common stock or adversely affect the best interest of the Company’s stockholders.

Conflicts of Interest Could Influence the Company’s Decisions.

Certain Stockholders Could Exercise Influence in a Manner Inconsistent With the Stockholders’ Best Interests . As of December 31, 2011, Mr. Samuel Zell and certain affiliated holders beneficially owned approximately 8.8% of the Company’s outstanding common stock (in each case including common stock issuable upon the exercise of stock options and the exchange of Units). Mr. Zell is the chairman of the Company’s Board of Directors. Accordingly, Mr. Zell has significant influence on the Company’s management and operation. Such influence

14

Table of Contents

could be exercised in a manner that is inconsistent with the interests of other stockholders.

Mr. Zell and His Affiliates Continue to be Involved in Other Investment Activities . Mr. Zell and his affiliates have a broad and varied range of investment interests, including interests in other real estate investment companies involved in other forms of housing, including multifamily housing. Mr. Zell and his affiliates may acquire interests in other companies. Mr. Zell may not be able to control whether any such company competes with the Company. Consequently, Mr. Zell’s continued involvement in other investment activities could result in competition to the Company as well as management decisions which might not reflect the interests of the Company’s stockholders.

Members of Management May Have a Conflict of Interest Over Whether To Enforce Terms of Mr. McAdams’s Employment and Noncompetition Agreement. Mr. McAdams was the Company’s President until January 31, 2011 and had an employment and noncompetition agreement with the Company that expired on December 31, 2010. For the most part these restrictions apply to him both during his employment and for two years thereafter. Mr. McAdams is also prohibited from otherwise disrupting or interfering with the Company’s business through the solicitation of the Company’s employees or customers or otherwise. To the extent that the Company chooses to enforce its rights under any of these agreements, it may determine to pursue available remedies, such as actions for damages or injunctive relief, less vigorously than the Company otherwise might because of its desire to maintain its ongoing relationship with Mr. McAdams. Additionally, the non-competition provisions of his agreement, despite being limited in scope and duration, could be difficult to enforce, or may be subject to limited enforcement, should litigation arise over it in the future. (See Note 13 in the Notes to Consolidated Financial Statements contained in this Form 10-K.)

Risk of Eminent Domain and Tenant Litigation.

The Company owns Properties in certain areas of the country where real estate values have increased faster than rental rates in its Properties either because of locally imposed rent control or long term leases. In such areas, the Company has learned that certain local government entities have investigated the possibility of seeking to take the Company’s Properties by eminent domain at values below the value of the underlying land. While no such eminent domain proceeding has been commenced, and the Company would exercise all of its rights in connection with any such proceeding, successful condemnation proceedings by municipalities could adversely affect its financial condition. Moreover, certain of its Properties located in California are subject to rent control ordinances, some of which not only severely restrict ongoing rent increases but also prohibit the Company from increasing rents upon turnover. Such regulations allow customers to sell their homes for a premium representing the value of the future discounted rent-controlled rents. As part of the Company’s effort to realize the value of its Properties subject to rent control, the Company has initiated lawsuits against several municipalities in California. In response to the Company’s efforts, tenant groups have filed lawsuits against the Company seeking not only to limit rent increases, but to be awarded large damage awards. If the Company is unsuccessful in its efforts to challenge rent control ordinances, it is likely that the Company will not be able to charge rents that reflect the intrinsic value of the affected Properties. Finally, tenant groups in non-rent controlled markets have also attempted to use litigation as a means of protecting themselves from rent increases reflecting the rental value of the affected Properties. An unfavorable outcome in the tenant group lawsuits could have an adverse impact on the Company’s financial condition.

Environmental and Utility-Related Problems Are Possible and Can be Costly.

Federal, state and local laws and regulations relating to the protection of the environment may require a current or previous owner or operator of real estate to investigate and clean up hazardous or toxic substances or petroleum product releases at such property. The owner or operator may have to pay a governmental entity or third parties for property damage and for investigation and clean-up costs incurred by such parties in connection with the contamination. Such laws typically impose clean-up responsibility and liability without regard to whether the owner or operator knew of or caused the presence of the contaminants. Even if more than one person

15

Table of Contents

may have been responsible for the contamination, each person covered by the environmental laws may be held responsible for all of the clean-up costs incurred. In addition, third parties may sue the owner or operator of a site for damages and costs resulting from environmental contamination emanating from that site.

Environmental laws also govern the presence, maintenance and removal of asbestos. Such laws require that owners or operators of property containing asbestos properly manage and maintain the asbestos, that they notify and train those who may come into contact with asbestos and that they undertake special precautions, including removal or other abatement, if asbestos would be disturbed during renovation or demolition of a building. Such laws may impose fines and penalties on real property owners or operators who fail to comply with these requirements and may allow third parties to seek recovery from owners or operators for personal injury associated with exposure to asbestos fibers.

Utility-related laws and regulations also govern the provision of utility services and operations of water and wastewater treatment facilities. Such laws regulate, for example, how and to what extent owners or operators of property can charge renters for provision of, for example, electricity, and whether and to what extent such utility services can be charged separately from the base rent. Such laws also regulate the operations and performance of water treatment facilities and wastewater treatment facilities. Such laws may impose fines and penalties on real property owners or operators who fail to comply with these requirements.

The Company has a Significant Concentration of Properties in Florida and California, and Natural Disasters or Other Catastrophic Events in These or Other States Could Adversely Affect the Value of Its Properties and the Its Cash Flow.

As of December 31, 2011, the Company owned or had an ownership interest in 382 Properties located in 32 states and British Columbia, including 119 Properties located in Florida and 49 Properties located in California. The occurrence of a natural disaster or other catastrophic event in any of these areas may cause a sudden decrease in the value of the Company’s Properties. While the Company has obtained insurance policies providing certain coverage against damage from fire, flood, property damage, earthquake, wind storm and business interruption, these insurance policies contain coverage limits, limits on covered property and various deductible amounts that the Company must pay before insurance proceeds are available. Such insurance may therefore be insufficient to restore the Company’s economic position with respect to damage or destruction to its Properties caused by such occurrences. Moreover, each of these coverages must be renewed every year and there is the possibility that all or some of the coverages may not be available at a reasonable cost. In addition, in the event of such a natural disaster or other catastrophic event, the process of obtaining reimbursement for covered losses, including the lag between expenditures incurred by the Company and reimbursements received from the insurance providers, could adversely affect the Company’s economic performance.

Market Interest Rates May Have an Effect on the Value of the Company’s Common Stock.

One of the factors that investors consider important in deciding whether to buy or sell shares of a REIT is the distribution rates with respect to such shares (as a percentage of the price of such shares) relative to market interest rates. If market interest rates go up, prospective purchasers of REIT shares may expect a higher distribution rate. Higher interest rates would not, however, result in more funds for the Company to distribute and, in fact, would likely increase its borrowing costs and potentially decrease funds available for distribution. Thus, higher market interest rates could cause the market price of the Company’s publicly traded securities to go down.

The Company Is Dependent on External Sources of Capital.

To qualify as a REIT, the Company must distribute to its stockholders each year at least 90% of its REIT taxable income (determined without regard to the deduction for dividends paid and excluding any net capital gain). In addition, the Company intends to distribute all or substantially all of its net income so that it will generally not be

16

Table of Contents

subject to U.S. federal income tax on its earnings. Because of these distribution requirements, it is not likely that the Company will be able to fund all future capital needs, including for acquisitions, from income from operations. The Company therefore will have to rely on third-party sources of debt and equity capital financing, which may or may not be available on favorable terms or at all. The Company’s access to third-party sources of capital depends on a number of things, including conditions in the capital markets generally and the market’s perception of its growth potential and its current and potential future earnings. It may be difficult for the Company to meet one or more of the requirements for qualification as a REIT, including but not limited to its distribution requirement. Moreover, additional equity offerings may result in substantial dilution of stockholders’ interests, and additional debt financing may substantially increase the Company’s leverage.

The Company’s Qualification as a REIT is Dependent on Compliance With U.S. Federal Income Tax Requirements.

The Company believes it has been organized and operated in a manner so as to qualify for taxation as a REIT, and it intends to continue to operate so as to qualify as a REIT for U.S. federal income tax purposes. Qualification as a REIT for U.S. federal income tax purposes, however, is governed by highly technical and complex provisions of the Code for which there are only limited judicial or administrative interpretations. In connection with certain transactions, the Company has received, and relied upon, advice of counsel as to the impact of such transactions on its qualification as a REIT. The Company’s qualification as a REIT requires analysis of various facts and circumstances that may not be entirely within its control, and it cannot provide any assurance that the Internal Revenue Service (the “IRS”) will agree with its analysis or the analysis of its tax counsel. In particular, the proper federal income tax treatment of right-to-use membership contracts is uncertain and there is no assurance that the IRS will agree with the Company’s treatment of such contracts. If the IRS were to disagree with the Company’s analysis or its tax counsel’s analysis of various facts and circumstances, the Company’s ability to qualify as a REIT could be adversely affected. Such matters could affect the Company’s qualification as a REIT. In addition, legislation, new regulations, administrative interpretations or court decisions might significantly change the tax laws with respect to the requirements for qualification as a REIT or the U.S. federal income tax consequences of qualification as a REIT.

If, with respect to any taxable year, the Company failed to maintain the Company’s qualification as a REIT (and if specified relief provisions under the Code were not applicable to such disqualification), it could not deduct distributions to stockholders in computing its net taxable income and it would be subject to U.S. federal income tax on its net taxable income at regular corporate rates. Any U.S. federal income tax payable could include applicable alternative minimum tax. If the Company had to pay U.S. federal income tax, the amount of money available to distribute to stockholders and pay indebtedness would be reduced for the year or years involved, and the Company would no longer be required to distribute money to stockholders. In addition, the Company would also be disqualified from treatment as a REIT for the four taxable years following the year during which qualification was lost, unless it was entitled to relief under the relevant statutory provisions. Although the Company currently intends to operate in a manner designed to allow the Company to qualify as a REIT, future economic, market, legal, tax or other considerations may cause it to revoke the REIT election.

Interpretation of and Changes to Accounting Policies and Standards Could Adversely Affect the Company’s Reported Financial Results.

The Company’s Accounting Policies and Methods Are the Basis on Which It Reports Its Financial Condition and Results of Operations, and They May Require Management to Make Estimates About Matters that Are Inherently Uncertain. The Company’s accounting policies and methods are fundamental to the manner in which it records and reports its financial condition and results of operations. Management must exercise judgment in selecting and applying many of these accounting policies and methods in order to ensure that they comply with generally accepted accounting principles and reflect management’s judgment as to the most appropriate manner in which to record and report the Company’s financial condition and results of operations. In some cases, management must select the accounting policy or method to apply from two or more alternatives, any of which might be

17

Table of Contents

reasonable under the circumstances yet might result in reporting materially different amounts than would have been reported under a different alternative.