|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 10-Q

| x | QUARTERLY REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

| For the quarterly period ended June 30, 2017 | |

| Or | |

| o | TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

| For the transition period from _________ to _________ |

Commission File Number: 001-34499

GULF RESOURCES, INC.

(Exact name of registrant as specified in its charter)

| Nevada | 13-3637458 | |

| (State or other jurisdiction of incorporation or organization) | (I.R.S. Employer Identification No.) | |

|

Level 11,Vegetable Building, Industrial Park of the East City, Shouguang City,Shandong, |

262700 | |

| (Address of principal executive offices) | (Zip Code) |

Registrant’s telephone number, including area code: +86 (536) 567 0008

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days.

Yes x No o

Indicate by check mark whether the registrant has submitted electronically and posted on its corporate Web site, if any, every, Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T (§232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files).

Yes x No o

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, or a smaller reporting company. See the definitions of “large accelerated filer,” “accelerated filer” and “smaller reporting company” in Rule 12b-2 of the Exchange Act.

| Large accelerated filer o | Accelerated filer o | Emerging Growth Company o |

| Non-accelerated filer (Do not check if a smaller reporting company) ☐ | Smaller reporting company x | |

If an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided pursuant to Section 13(a) of the Exchange Act. ☐

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act).

Yes o No x

As of August 6, 2017, the registrant had outstanding 46,793,791 shares of common stock.

| Part I – Financial Information | |

| Item 1. Financial Statements | 1 |

| Item 2. Management’s Discussion and Analysis of Financial Condition and Results of Operations | 20 |

| Item 3. Quantitative and Qualitative Disclosures about Market Risk | 39 |

| Item 4. Controls and Procedures | 40 |

| Part II – Other Information | |

| Item 1. Legal Proceedings | 40 |

| Item 1A. Risk Factors | 41 |

| Item 2. Unregistered Shares of Equity Securities and Use of Proceeds | 41 |

| Item 3. Defaults Upon Senior Securities | 41 |

| Item 4. Mine Safety Disclosures | 41 |

| Item 5. Other Information | 41 |

| Item 6. Exhibits | 41 |

| Signatures | 42 |

| GULF RESOURCES, INC. |

| AND SUBSIDIARIES |

| CONDENSED CONSOLIDATED BALANCE SHEETS |

| (Expressed in U.S. dollars) |

|

June 30, 2017 Unaudited |

December 31, 2016 Audited |

|||||||

| Current Assets | ||||||||

| Cash | $ | 176,303,274 | $ | 163,884,574 | ||||

| Accounts receivable | 86,858,779 | 51,835,218 | ||||||

| Inventories, net | 4,842,564 | 5,881,681 | ||||||

| Prepayments and deposits | 20,000 | 117,338 | ||||||

| Prepaid land leases | 783,741 | 47,255 | ||||||

| Other receivable | 2,035 | 1,424 | ||||||

| Total Current Assets | 268,810,393 | 221,767,490 | ||||||

| Non-Current Assets | ||||||||

| Property, plant and equipment, net | 100,712,418 | 108,731,126 | ||||||

| Property, plant and equipment under capital leases, net | 414,977 | 554,257 | ||||||

| Prepaid land leases, net of current portion | 4,725,437 | 4,754,169 | ||||||

| Deferred tax assets | 2,268,957 | 2,215,772 | ||||||

| Goodwill | 28,332,661 | 27,668,539 | ||||||

| Total non-current assets | 136,454,450 | 143,923,863 | ||||||

| Total Assets | $ | 405,264,843 | $ | 365,691,353 | ||||

| Liabilities and Stockholders’ Equity | ||||||||

| Current Liabilities | ||||||||

| Accounts payable and accrued expenses | $ | 14,540,121 | $ | 8,682,318 | ||||

| Retention payable | - | 733,869 | ||||||

| Capital lease obligation, current portion | 117,558 | 187,678 | ||||||

| Taxes payable | 7,783,712 | 4,341,331 | ||||||

| Total Current Liabilities | 22,441,391 | 13,945,196 | ||||||

| Non-Current Liabilities | ||||||||

| Capital lease obligation, net of current portion | 2,222,247 | 2,284,959 | ||||||

| Total Liabilities | $ | 24,663,638 | $ | 16,230,155 | ||||

| Stockholders’ Equity | ||||||||

| PREFERRED STOCK; $0.001 par value; 1,000,000 shares authorized; none outstanding | $ | - | $ | - | ||||

| COMMON STOCK; $0.0005 par value; 80,000,000 shares authorized as of June 30, 2017 and December 31, 2016; 47,052,940 and 47,052,940 shares issued; and 46,793,791 and 46,793,791 shares outstanding as of June 30,2017 and December 31, 2016, respectively | 23,525 | 23,525 | ||||||

| Treasury stock; 259,149 and 259,149 shares as of June 30, 2017 and December 31, 2016 at cost | (577,141 | ) | (577,141 | ) | ||||

| Additional paid-in capital | 94,171,379 | 94,156,679 | ||||||

| Retained earnings unappropriated | 268,444,917 | 248,941,696 | ||||||

| Retained earnings appropriated | 25,234,543 | 22,910,966 | ||||||

| Accumulated other comprehensive loss | (6,696,018 | ) | (15,994,527 | ) | ||||

| Total Stockholders’ Equity | 380,601,205 | 349,461,198 | ||||||

| Total Liabilities and Stockholders’ Equity | $ | 405,264,843 | $ | 365,691,353 | ||||

See accompanying notes to the condensed consolidated financial statements.

1

GULF RESOURCES, INC.

AND SUBSIDIARIES

CONDENSED CONSOLIDATED STATEMENTS OF INCOME AND COMPREHENSIVE INCOME

(Expressed in U.S. dollars)

(UNAUDITED)

| Three-Month Period Ended June 30, | Six-Month Period Ended June 30, | |||||||||||||||

| 2017 | 2016 | 2017 | 2016 | |||||||||||||

| NET REVENUE | ||||||||||||||||

| Net revenue | $ | 47,531,989 | $ | 47,600,767 | $ | 80,320,482 | $ | 82,096,217 | ||||||||

| OPERATING INCOME (EXPENSE) | ||||||||||||||||

| Cost of net revenue | (26,931,742 | ) | (29,195,255 | ) | (47,145,605 | ) | (53,076,901 | ) | ||||||||

| Sales, marketing and other operating expenses | (100,613 | ) | (104,369 | ) | (176,446 | ) | (186,270 | ) | ||||||||

| Research and development cost | (65,274 | ) | (70,378 | ) | (127,172 | ) | (130,215 | ) | ||||||||

| General and administrative expenses | (2,056,943 | ) | (1,009,882 | ) | (3,785,403 | ) | (2,925,912 | ) | ||||||||

| Other operating income | 105,055 | 110,239 | 209,613 | 220,521 | ||||||||||||

| (29,049,517 | ) | (30,269,645 | ) | (51,025,013 | ) | (56,098,777 | ) | |||||||||

| INCOME FROM OPERATIONS | 18,482,472 | 17,331,122 | 29,295,469 | 25,997,440 | ||||||||||||

| OTHER INCOME (EXPENSE) | ||||||||||||||||

| Interest expense | (42,065 | ) | (46,009 | ) | (83,976 | ) | (92,138 | ) | ||||||||

| Interest income | 132,721 | 122,328 | 258,581 | 236,774 | ||||||||||||

| INCOME BEFORE TAXES | 18,573,128 | 17,407,441 | 29,470,074 | 26,142,076 | ||||||||||||

| INCOME TAXES | (4,821,450 | ) | (4,210,422 | ) | (7,643,276 | ) | (6,478,093 | ) | ||||||||

| NET INCOME | $ | 13,751,678 | $ | 13,197,019 | $ | 21,826,798 | $ | 19,663,983 | ||||||||

| COMPREHENSIVE INCOME(LOSS): | ||||||||||||||||

| NET INCOME | $ | 13,751,678 | $ | 13,197,019 | $ | 21,826,798 | $ | 19,663,983 | ||||||||

| OTHER COMPREHENSIVE INCOME (LOSS) | ||||||||||||||||

| - Foreign currency translation adjustments | 7,261,237 | (9,760,773 | ) | 9,298,509 | (7,867,712 | ) | ||||||||||

| COMPREHENSIVE INCOME | $ | 21,012,915 | $ | 3,436,246 | $ | 31,125,307 | $ | 11,796,271 | ||||||||

| EARNINGS PER SHARE: | ||||||||||||||||

| BASIC | $ | 0.29 | $ | 0.29 | $ | 0.47 | $ | 0.43 | ||||||||

| DILUTED | $ | 0.29 | $ | 0.28 | $ | 0.47 | $ | 0.42 | ||||||||

| WEIGHTED AVERAGE NUMBER OF SHARES: | ||||||||||||||||

| BASIC | 46,793,791 | 46,008,102 | 46,793,791 | 46,007,611 | ||||||||||||

| DILUTED | 46,796,848 | 46,631,091 | 46,800,545 | 46,685,709 | ||||||||||||

See accompanying notes to the condensed consolidated financial statements.

2

| GULF RESOURCES, INC. |

| AND SUBSIDIARIES |

| CONDENSED CONSOLIDATED STATEMENT OF STOCKHOLDERS’ EQUITY |

| SIX-MONTH PERIOD ENDED JUNE 30, 2017 |

| (Expressed in U.S. dollars) |

| Common stock | Accumulated | |||||||||||||||||||||||||||||||||||||||

| Number | Number | Number | Additional | Retained | Retained | other | ||||||||||||||||||||||||||||||||||

| of shares | of shares | of treasury | Treasury | Paid-in | earnings | earnings | comprehensive | |||||||||||||||||||||||||||||||||

| issued | outstanding | stock | Amount | stock | capital | unappropriated | appropriated | (loss) income | Total | |||||||||||||||||||||||||||||||

| BALANCE AT DECEMBER 31, 2016 Audited | 47,052,940 | 46,793,791 | 259,149 | $ | 23,525 | $ | (577,141 | ) | $ | 94,156,679 | $ | 248,941,696 | $ | 22,910,966 | $ | (15,994,527 | ) | $ | 349,461,198 | |||||||||||||||||||||

| Translation adjustment | - | — | — | - | - | - | - | 9,298,509 | 9,298,509 | |||||||||||||||||||||||||||||||

|

Issuance of stock options to employees and directors |

— | — | — | — | — | 14,700 | — | — | — | 14,700 | ||||||||||||||||||||||||||||||

| Net income for six-month period ended June 30, 2017 | - | — | — | - | — | - | 21,826,798 | — | - | 21,826,798 | ||||||||||||||||||||||||||||||

| Transfer to statutory common reserve fund | — | — | — | — | — | — | (2,323,577 | ) | 2,323,577 | — | — | |||||||||||||||||||||||||||||

| BALANCE AT JUNE 30, 2017 Unaudited | 47,052,940 | 46,793,791 | 259,149 | $ | 23,525 | $ | (577,141 | ) | $ | 94,171,379 | $ | 268,444,917 | $ | 25,234,543 | (6,696,018 | ) | $ | 380,601,205 | ||||||||||||||||||||||

See accompanying notes to the condensed consolidated financial statements.

3

| GULF RESOURCES, INC. |

| AND SUBSIDIARIES |

| CONDENSED CONSOLIDATED STATEMENTS OF CASH FLOWS |

| (Expressed in U.S. dollars) |

| (UNAUDITED) |

| Six-Month Period Ended June 30, | ||||||||

| 2017 | 2016 | |||||||

| CASH FLOWS FROM OPERATING ACTIVITIES | ||||||||

| Net income | $ | 21,826,798 | $ | 19,663,983 | ||||

| Adjustments to reconcile net income to net cash provided by operating activities: | ||||||||

| Interest on capital lease obligation | 83,128 | 91,764 | ||||||

| Amortization of prepaid land leases | 234,307 | 255,261 | ||||||

| Depreciation and amortization | 10,809,289 | 13,514,292 | ||||||

| Exchange (gain) loss on inter-company balances | 603,910 | (548,734 | ) | |||||

| Stock-based compensation expense | 14,700 | 12,800 | ||||||

| Changes in assets and liabilities: | ||||||||

| Accounts receivable | (33,349,844 | ) | (22,737,450 | ) | ||||

| Inventories | 1,165,420 | 328,685 | ||||||

| Prepayments and deposits | (19,129 | ) | (14,094 | ) | ||||

| Other receivables | (580 | ) | — | |||||

| Accounts payable and accrued expenses | 5,582,026 | 5,353,742 | ||||||

| Retention payable | (739,329 | ) | (1,112,087 | ) | ||||

| Taxes payable | 3,292,636 | 2,662,606 | ||||||

| Net cash provided by operating activities | 9,503,332 | 17,470,768 | ||||||

| CASH FLOWS USED IN INVESTING ACTIVITIES | ||||||||

| Additions of prepaid land leases | (818,957 | ) | (616,512 | ) | ||||

| Purchase of property, plant and equipment | (59,975 | ) | (870,875 | ) | ||||

| Net cash used in investing activities | (878,932 | ) | (1,487,387 | ) | ||||

| CASH FLOWS USED IN FINANCING ACTIVITIES | ||||||||

| Repayment of capital lease obligation | (273,873 | ) | (287,387 | ) | ||||

| Net cash used in financing activities | (273,873 | ) | (287,387 | ) | ||||

| EFFECTS OF EXCHANGE RATE CHANGES ON CASH AND CASH EQUIVALENTS | 4,068,173 | (3,029,146 | ) | |||||

| NET INCREASE IN CASH AND CASH EQUIVALENTS | 12,418,700 | 12,666,848 | ||||||

| CASH AND CASH EQUIVALENTS - BEGINNING OF PERIOD | 163,884,574 | 133,606,392 | ||||||

| CASH AND CASH EQUIVALENTS - END OF PERIOD | $ | 176,303,274 | $ | 146,273,240 | ||||

| SUPPLEMENTAL DISCLOSURE OF CASH FLOW INFORMATION | ||||||||

| Cash paid during the periods for: | ||||||||

| Income taxes | $ | 4,634,040 | $ | 4,586,259 | ||||

|

SUPPLEMENTAL DISCLOSURE OF NON-CASH INVESTING

AND FINANCING ACTIVITIES Par value of common stock issued upon cashless exercise of options |

$ | — | $ | 4 | ||||

See accompanying notes to the condensed consolidated financial statements.

4

GULF RESOURCES, INC.

AND SUBSIDIARIES

NOTES TO CONDENSED CONSOLIDATED FINANCIAL STATEMENTS

JUNE 30, 2017

(Expressed in U.S. dollars)

(UNAUDITED)

NOTE 1 – BASIS OF PRESENTATION AND SUMMARY OF SIGNIFICANT ACCOUNTING POLICIES

(a) Basis of Presentation and Consolidation

The accompanying condensed financial statements have been prepared by Gulf Resources, Inc. a Nevada corporation and its subsidiaries (collectively, the “Company”), without audit, in accordance with the instructions to Form 10-Q and, therefore, do not necessarily include all information and footnotes necessary for a fair statement of its financial position, results of operations and cash flows in accordance with accounting principles generally accepted in the United States (“US GAAP”).

In the opinion of management, the unaudited financial information for the three and six months ended June 30, 2017 presented reflects all adjustments, which are only normal and recurring, necessary for a fair statement of results of operations, financial position and cash flows. These condensed financial statements should be read in conjunction with the financial statements included in the Company’s 2016 Form 10-K. Operating results for the interim periods are not necessarily indicative of operating results for an entire fiscal year.

The preparation of financial statements in conformity with US GAAP requires management to make estimates and assumptions that affect the amounts that are reported in the financial statements and accompanying disclosures. Although these estimates are based on management’s best knowledge of current events and actions that the Company may undertake in the future, actual results may be different from the estimates. The Company also exercises judgments in the preparation of these condensed financial statements in certain areas, including classification of leases and related party transactions.

On September 2, 2016, the Company announced the planned merger of two of its 100% owned subsidiaries, Shouguan Yuxin Chemical Co., Limited (“SYCI”) and Shouguan Rongyuan Chemical Co., Ltd (“SCRC”). On March 24, 2017, the legal process of the merger was completed and SCRC was officially deregistered on March 28, 2017. The results of these two subsidiaries were reported as SYCI in the three and six months ended June 30, 2017.

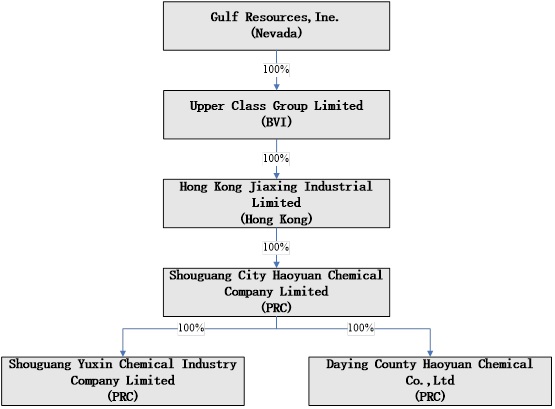

The consolidated financial statements include the accounts of Gulf Resources, Inc. and its wholly-owned subsidiary, Upper Class Group Limited, a company incorporated in the British Virgin Islands, which owns 100% of Hong Kong Jiaxing Industrial Limited, a company incorporated in Hong Kong (“HKJI”). HKJI owns 100% of Shouguang City Haoyuan Chemical Company Limited ("SCHC") which owns 100% of Shouguang Yuxin Chemical Industry Co., Limited (“SYCI”) and Daying County Haoyuan Chemical Company Limited (“DCHC”). All material intercompany transactions have been eliminated on consolidation.

(b) Nature of the Business

The Company manufactures and trades bromine and crude salt through its wholly-owned subsidiary, Shouguang City Haoyuan Chemical Company Limited ("SCHC"), manufactures chemical products for use in the oil industry, pesticides and paper manufacturing industry and for human and animal antibiotics through its wholly-owned subsidiary, Shouguang Yuxin Chemical Industry Co., Limited ("SYCI") in the People’s Republic of China (“PRC”). DCHC was established to further explore and develop natural gas and brine resources (including bromine and crude salt) in PRC.

(c) Allowance for Doubtful Accounts

As of June 30, 2017 and December 31, 2016, allowances for doubtful accounts were nil. No allowances for doubtful accounts were charged to the condensed consolidated statements of income for the three-month and six-month periods ended June 30, 2017 and 2016.

(d) Concentration of Credit Risk

The Company is exposed to credit risk in the normal course of business, primarily related to accounts receivable and cash and cash equivalents. Substantially all of the Company’s cash and cash equivalents are maintained with financial institutions in the PRC, namely, Industrial and Commercial Bank of China Limited, China Merchants Bank Company Limited and Sichuan Rural Credit Union, which are not insured or otherwise protected. The Company placed $176,303,274 and $163,884,574 with these institutions as of June 30, 2017 and December 31, 2016, respectively. The Company has not experienced any losses in such accounts in the PRC.

Concentrations of credit risk with respect to accounts receivable exists as the Company sells a substantial portion of its products to a limited number of customers. However, such concentrations of credit risks are limited since the Company performs ongoing credit evaluations of its customers’ financial condition and extends credit terms as and when appropriate. Approximately 64.3% and 61.6% of the balances of accounts receivable as of June 30, 2017 and December 31, 2016, respectively, are outstanding for less than three months. All outstanding receivables as of June 30, 2017 and December 31, 2016 are within the credit terms. For the balances of accounts receivable aged more than 90 days as of June 30, 2017, approximately 27% were settled in July 2017. For the balances of all accounts receivable as of June 30, 2017, approximately 15% were settled in July 2017.

The rate of collection for accounts receivable aged more than 90 days as of June 30, 2017 in July 2017 was analyzed as follows:

| Accounts Receivable Aging | Percent Collected |

| 90-120 days | 17% |

| 121-150 days | 31% |

| 151-180 days | 8% |

| 181-210 days | 54% |

| 211-240 days | 100% |

5

GULF RESOURCES, INC.

AND SUBSIDIARIES

NOTES TO CONDENSED CONSOLIDATED FINANCIAL STATEMENTS

JUNE 30, 2017

(Expressed in U.S. dollars)

(UNAUDITED)

NOTE 1 – BASIS OF PRESENTATION AND SUMMARY OF SIGNIFICANT ACCOUNTING POLICIES – Continued

(e) Property, Plant and Equipment

Property, plant and equipment are stated at cost less accumulated depreciation and any impairment losses. Expenditures for new facilities or equipment, and major expenditures for betterment of existing facilities or equipment are capitalized and depreciated using the straight-line method at rates sufficient to depreciate such costs less 5% residual value over the estimated productive lives. All other ordinary repair and maintenance costs are expensed as incurred.

Mineral rights are recorded at cost less accumulated depreciation and any impairment losses. Mineral rights are amortized ratably over the term of the lease, or the equivalent term under the units of production method, whichever is shorter.

Construction in process primarily represents direct costs of construction of plant, machinery and equipment. Costs incurred are capitalized and transferred to property and equipment upon completion, at which time depreciation commences.

The Company’s depreciation and amortization policies on property, plant and equipment, other than mineral rights and construction in process, are as follows:

|

Useful life (in years) |

||

| Buildings (including salt pans) | 8 - 20 | |

| Plant and machinery (including protective shells, transmission channels and ducts) | 3 - 8 | |

| Motor vehicles | 5 | |

| Furniture, fixtures and equipment | 3-8 |

Property, plant and equipment under the capital lease are depreciated over their expected useful lives on the same basis as owned assets, or where shorter, the term of the lease, which is 20 years.

(f) Retirement Benefits

Pursuant to the relevant laws and regulations in the PRC, the Company participates in a defined contribution retirement plan for its employees arranged by a governmental organization. The Company makes contributions to the retirement plan at the applicable rate based on the employees’ salaries. The required contributions under the retirement plans are charged to the condensed consolidated statement of income on an accrual basis when they are due. The Company’s contributions totaled $257,660 and $250,152 for the three-month period ended June 30, 2017 and 2016, respectively, and totaled $512,876 and $499,615 for the six-month period ended June 30, 2017 and 2016, respectively.

(g) Revenue Recognition

The Company recognizes revenue, net of value-added tax, when persuasive evidence of an arrangement exists, delivery of the goods has occurred, customer acceptance has been obtained, which means the significant risks and ownership have been transferred to the customer, the price is fixed or determinable and collectability is reasonably assured.

6

GULF RESOURCES, INC.

AND SUBSIDIARIES

NOTES TO CONDENSED CONSOLIDATED FINANCIAL STATEMENTS

JUNE 30, 2017

(Expressed in U.S. dollars)

(UNAUDITED)

NOTE 1 – BASIS OF PRESENTATION AND SUMMARY OF SIGNIFICANT ACCOUNTING POLICIES – Continued

(h) Recoverability of Long-lived Assets

In accordance with Financial Accounting Standards Board (“FASB”) Accounting Standards Codification (“ASC”) 360-10-35 “Impairment or Disposal of Long-lived Assets” , long-lived assets to be held and used are analyzed for impairment whenever events or changes in circumstances indicate that the carrying amount of an asset may not be fully recoverable or that the useful lives of those assets are no longer appropriate. The Company evaluates at each balance sheet date whether events and circumstances have occurred that indicate possible impairment.

The Company determines the existence of such impairment by measuring the expected future cash flows (undiscounted and without interest charges) and comparing such amount to the carrying amount of the assets. An impairment loss, if one exists, is then measured as the amount by which the carrying amount of the asset exceeds the discounted estimated future cash flows. Assets to be disposed of are reported at the lower of the carrying amount or fair value of such assets less costs to sell. Asset impairment charges are recorded to reduce the carrying amount of the long-lived asset that will be sold or disposed of to their estimated fair values. Charges for the asset impairment reduce the carrying amount of the long-lived assets to their estimated salvage value in connection with the decision to dispose of such assets.

For the three-month and six-month periods ended June 30, 2017 and 2016, the Company determined that there are no events or circumstances indicating possible impairment of its long-lived assets.

(i) Basic and Diluted Earnings per Share of Common Stock

Basic earnings per common share are based on the weighted average number of shares outstanding during the periods presented. Diluted earnings per share are computed using weighted average number of common shares plus dilutive common share equivalents outstanding during the period. Potential common shares that would have the effect of increasing diluted earnings per share are considered to be anti-dilutive, i.e. the exercise prices of the outstanding stock options were greater than the market price of the common stock. Anti-dilutive common stock equivalents which were excluded from the calculation of number of dilutive common stock equivalents amounted to 39,155 and 71,086 shares for the three-month period ended June 30, 2017 and 2016, respectively, and amounted to 32,077 and 64,139 shares for the six-month period ended June 30, 2017 and 2016, respectively. These awards could be dilutive in the future if the market price of the common stock increases and is greater than the exercise price of these awards.

7

GULF RESOURCES, INC.

AND SUBSIDIARIES

NOTES TO CONDENSED CONSOLIDATED FINANCIAL STATEMENTS

JUNE 30, 2017

(Expressed in U.S. dollars)

(UNAUDITED)

NOTE 1 – BASIS OF PRESENTATION AND SUMMARY OF SIGNIFICANT ACCOUNTING POLICIES – Continued

(i) Basic and Diluted Earnings per Share of Common Stock – Continued

The following table sets forth the computation of basic and diluted earnings per share:

| Three-Month Period Ended June 30, | Six-Month Period Ended June 30, | |||||||||||||||

| 2017 | 2016 | 2017 | 2016 | |||||||||||||

| Numerator | ||||||||||||||||

| Net income | $ | 13,751,678 | $ | 13,197,019 | $ | 21,826,798 | $ | 19,663,983 | ||||||||

| Denominator | ||||||||||||||||

| Basic: Weighted-average common shares outstanding during the period | 46,793,791 | 46,008,102 | 46,793,791 | 46,007,611 | ||||||||||||

| Add: Dilutive effect of stock options | 3,057 | 622,989 | 6,754 | 678,098 | ||||||||||||

| Diluted | 46,796,848 | 46,631,091 | 46,800,545 | 46,685,709 | ||||||||||||

| Earnings per share | ||||||||||||||||

| Basic | $ | 0.29 | $ | 0.29 | $ | 0.47 | $ | 0.43 | ||||||||

| Diluted | $ | 0.29 | $ | 0.28 | $ | 0.47 | $ | 0.42 | ||||||||

(j) Reporting Currency and Translation

The financial statements of the Company’s foreign subsidiaries are measured using the local currency, Renminbi (“RMB”), as the functional currency; whereas the functional currency and reporting currency of the Company is the United States dollar (“USD” or “$”).

As such, the Company uses the “current rate method” to translate its PRC operations from RMB into USD, as required under FASB ASC 830 “Foreign Currency Matters”. The assets and liabilities of its PRC operations are translated into USD using the rate of exchange prevailing at the balance sheet date. The capital accounts are translated at the historical rate. Adjustments resulting from the translation of the balance sheets of the Company’s PRC subsidiaries are recorded in stockholders’ equity as part of accumulated other comprehensive income. The statement of income and comprehensive income is translated at average rate during the reporting period. Gains or losses resulting from transactions in currencies other than the functional currencies are recognized in net income for the reporting periods as part of general and administrative expense. The statement of cash flows is translated at average rate during the reporting period, with the exception of the consideration paid for the acquisition of business which is translated at historical rates.

(k) Foreign Operations

All of the Company’s operations and assets are located in PRC. The Company may be adversely affected by possible political or economic events in this country. The effect of these factors cannot be accurately predicted.

(l) Exploration Costs

Exploration costs, which included the cost of researching for appropriate places to drill wells and the cost of well drilling in search of potential natural brine or other resources, are charged to the income statement as incurred. Once the commercial viability of a project has been confirmed, all subsequent costs are capitalized.

(m) Goodwill

Goodwill represents the excess of the purchase price over the net of the fair value of the identifiable tangible and intangible assets acquired and the fair value of liabilities assumed in business acquisitions. Management of the Company evaluates the carrying value of goodwill annually or when a possible impairment is indicated. The Company performs its impairment assessment annually and between annual tests in certain circumstances and determined that there was no impairment of goodwill. Goodwill impairment is assessed using the expected present value of associated future cash flows.

(n) New Accounting Pronouncements

Recently Adopted Accounting Pronouncements

In March 2016, the FASB issued ASU No. 2016-09, Compensation – Stock Compensation (Topic 718): Improvements to Employee Share-Based Payment Accounting, which simplifies several aspects of the accounting for share-based payment award transactions, including: (1) income tax consequences; (2) classification of awards as either equity or liabilities, and (3) classification on the statement of cash flows. For public companies, the amendments in this ASU are effective for annual periods beginning after December 15, 2016, and interim periods within those annual periods. The Company adopted the amendments in this Update as of January 1, 2017. There is no impact on the financial statements since any excess tax benefits were fully offset by a valuation allowance and not recognized for financial statement purposes.

Recently Issued Accounting Pronouncements Not Yet Adopted

In May 2014, the FASB issued ASU No. 2014-09, Revenue from Contracts with Customers (Topic 606). The core principle of the guidance is that an entity should recognize revenue to depict the transfer of promised goods or services to customers in an amount that reflects the consideration to which the entity expects to be entitled in exchange for those goods or services. In August 2015, FASB issued ASU 2015-14 which deferred the effective date of Update 2014-09 to annual reporting periods beginning after December 15, 2017. Early application is permitted only as of annual reporting periods beginning after December 15, 2016. The Company expects to adopt the new standard in the first quarter of 2018. The Company does not expect the adoption of this Update to have a material effect on the financial statements.

In February 2016, the FASB issued ASU No. 2016-02, Leases (Topic 842). The amendments in this Update specify the accounting for leases. The core principle of Topic 842 is that a lessee should recognize the assets and liabilities that arise from leases. For public business entities, the amendments in this Update are effective for fiscal years beginning after December 15, 2018, including interim periods within those fiscal years. The Company is evaluating the impact of this on the consolidated financial statements and related disclosures.

In August 2016, the FASB issued ASU No. 2016-15, Statement of Cash Flows (Topic 230), Classification of Certain Cash Receipts and Cash Payments. The Update addresses eight specific changes to how cash receipts and cash payments are presented and classified in the statement of cash flows. The amendments in this Update are effective for public business entities for fiscal years beginning after December 15, 2017, and interim periods within those fiscal years. Early adoption is permitted. An entity that elects early adoption must adopt all of the amendments in the same period. The amendments in this Update should be applied using a retrospective transition method to each period presented. If it is impracticable to apply the amendments retrospectively for some of the issues, the amendments for those issues would be applied prospectively as of the earliest date practicable. The Company does not expect the adoption of this Update to have a material effect on the financial statements.

In January 2017, the FASB issued ASU No. 2017-01, Business Combinations (Topic 805), Clarifying the Definition of a Business. The amendments in this Update provide a more robust framework to use in determining when a set of assets and activities is a business. The amendments in this Update are effective for annual periods beginning after December 15, 2017, including interim periods within those periods. The Company does not expect the adoption of this Update to have a material effect on the financial statements.

In January 2017, the FASB issued ASU No. 2017-04, Intangibles – Goodwill and Other (Topic 350), Simplifying the Test for Goodwill Impairment. To simplify the subsequent measurement of goodwill, the Board eliminated Step 2 from the goodwill impairment test. Instead, under the amendments in this Update, an entity should perform its annual, or interim, goodwill impairment test by comparing the fair value of a reporting unit with its carrying amount. An entity should recognize an impairment charge for the amount by which the carrying amount exceeds the reporting unit’s fair value; however, the loss recognized should not exceed the total amount of goodwill allocated to that reporting unit. A public business entity that is a U.S. Securities and Exchange Commission (SEC) filer should adopt the amendments in this Update for its annual or any interim goodwill impairment tests in fiscal years beginning after December 15, 2019. The Company is currently evaluating the effect of the adoption of this Update.

In May 2017, the FASB issued ASU 2017-09, Compensation – Stock Compensation (Topic 718), Scope of Modification Accounting. The amendments in this Update provide guidance about which changes to the terms or conditions of a share-based payment award require an entity to apply modification accounting. The amendments in this Update are effective for all entities for annual periods, and interim periods within those annual periods, beginning after December 15, 2017. The amendments in this Update should be applied prospectively to an award modified on or after the adoption date.

8

GULF RESOURCES, INC.

AND SUBSIDIARIES

NOTES TO CONDENSED CONSOLIDATED FINANCIAL STATEMENTS

JUNE 30, 2017

(Expressed in U.S. dollars)

(UNAUDITED)

NOTE 2 – INVENTORIES

Inventories consist of:

|

June 30,

2017 |

December 31,

2016 |

|||||||

| Raw materials | $ | 617,048 | $ | 818,500 | ||||

| Finished goods | 3,421,363 | 4,370,331 | ||||||

| Work-in-process | 804,153 | 692,850 | ||||||

| $ | 4,842,564 | $ | 5,881,681 | |||||

NOTE 3 – PREPAID LAND LEASES

The Company prepaid for land leases with lease terms for periods ranging from one to fifty years to use the land on which the production facilities and warehouses of the Company are situated. The prepaid land lease is amortized on a straight line basis.

During the three-month period ended June 30, 2017 and 2016, amortization of prepaid land leases totaled $126,846 and $123,717, respectively, which amounts were recorded as cost of net revenue. During the six-month period ended June 30, 2017 and 2016, amortization of prepaid land leases totaled $234,307 and $255,261, respectively, which amounts were recorded as cost of net revenue.

The Company has the rights to use certain parcels of land located in Shouguang, PRC, through lease agreements signed with local townships or the government authority. For parcels of land that are collectively owned by local townships, the Company cannot obtain land use rights certificates. The parcels of land that the Company cannot obtain land use rights certificates cover a total of approximately 54.97 square kilometers with an aggregate carrying value of $1,270,668 and approximately 54.97 square kilometers with an aggregate carrying value of $620,978 as at June 30, 2017 and December 31, 2016, respectively.

NOTE 4 – PROPERTY, PLANT AND EQUIPMENT, NET

Property, plant and equipment, net consist of the following:

|

June 30,

2017 |

December 31,

2016 |

|||||||

| At cost: | ||||||||

| Mineral rights | $ | 4,544,643 | $ | 4,438,115 | ||||

| Buildings | 63,448,611 | 61,656,398 | ||||||

| Plant and machinery | 189,225,440 | 184,544,140 | ||||||

| Motor vehicles | 8,480 | 8,282 | ||||||

| Furniture, fixtures and office equipment | 4,662,769 | 4,553,473 | ||||||

| Construction in process | — | 374,790 | ||||||

| Total | 261,889,943 | 255,575,198 | ||||||

| Less: Accumulated depreciation and amortization | (161,177,525 | ) | (146,844,072 | ) | ||||

| Net book value | $ | 100,712,418 | $ | 108,731,126 | ||||

The Company has certain buildings and salt pans erected on parcels of land located in Shouguang, PRC, and such parcels of land are collectively owned by local townships or the government. The Company has not been able to obtain property ownership certificates over these buildings and salt pans. The aggregate carrying values of these properties situated on parcels of the land are $34,906,905 and $35,184,613 as at June 30, 2017 and December 31, 2016, respectively.

9

GULF RESOURCES, INC.

AND SUBSIDIARIES

NOTES TO CONDENSED CONSOLIDATED FINANCIAL STATEMENTS

JUNE 30, 2017

(Expressed in U.S. dollars)

(UNAUDITED)

NOTE 4 – PROPERTY, PLANT AND EQUIPMENT, NET – Continued

During the three-month period ended June 30, 2017, depreciation and amortization expense totaled $5,294,777, of which $5,001,792 and $292,985 were recorded as cost of net revenue and administrative expenses, respectively. During the three-month period ended June 30, 2016, depreciation and amortization expense totaled $6,644,571, of which $6,306,337 and $338,235 were recorded as cost of net revenue and administrative expenses, respectively. During the six-month period ended June 30, 2017, depreciation and amortization expense totaled $10,658,819, of which $10,074,234 and $584,585 were recorded as cost of net revenue and administrative expenses respectively. During the six-month period ended June 30, 2016, depreciation and amortization expense totaled $13,514,292, of which $12,827,797 and $686,495 were recorded as cost of revenue and administrative expenses respectively.

NOTE 5 – PROPERTY, PLANT AND EQUIPMENT UNDER CAPITAL LEASES, NET

Property, plant and equipment under capital leases, net consist of the following:

|

June 30,

2017 |

December 31,

2016 |

|||||||

| At cost: | ||||||||

| Buildings | $ | 121,470 | $ | 118,623 | ||||

| Plant and machinery | 2,283,296 | 2,229,775 | ||||||

| Total | 2,404,766 | 2,348,398 | ||||||

| Less: Accumulated depreciation and amortization | (1,989,789 | ) | (1,794,141 | ) | ||||

| Net book value | $ | 414,977 | $ | 554,257 | ||||

The above buildings erected on parcels of land located in Shouguang, PRC, are collectively owned by local townships. The Company has not been able to obtain property ownership certificates over these buildings as the Company could not obtain land use rights certificates on the underlying parcels of land.

During the three-month period ended June 30, 2017 and 2016, depreciation and amortization expense totaled $75,413 and $83,288, respectively, which was recorded as cost of net revenue. During the six-month period ended June 30, 2017 and 2016, depreciation and amortization expense totaled $150,470 and $166,608, respectively, which was recorded as cost of net revenue.

10

GULF RESOURCES, INC.

AND SUBSIDIARIES

NOTES TO CONDENSED CONSOLIDATED FINANCIAL STATEMENTS

JUNE 30, 2017

(Expressed in U.S. dollars)

(UNAUDITED)

NOTE 6 – ACCOUNTS PAYABLE AND ACCRUED EXPENSES

Accounts payable and accrued expenses consist of the following:

| June 30, | December 31, | |||||||

| 2017 | 2016 | |||||||

| Accounts payable | $ | 13,390,816 | $ | 7,513,075 | ||||

| Salary payable | 353,110 | 319,489 | ||||||

| Social security insurance contribution payable | 119,730 | 119,444 | ||||||

| Other payables | 676,465 | 730,310 | ||||||

| Total | $ | 14,540,121 | $ | 8,682,318 | ||||

NOTE 7 – RELATED PARTY TRANSACTIONS

During the three-month and six-month periods ended June 30, 2017, the Company borrowed $100,000 and $250,000, respectively, from Jiaxing Lighting Appliance Company Limited (Jiaxing Lighting”), in which Mr. Ming Yang, a shareholder and the Chairman of the Company, has a 100% equity interest. The amounts due to Jiaxing Lighting were unsecured, interest free and repayable on demand and were fully settled in the three-month period ended June 30, 2017. There was no balance owing to Jiaxing Lighting as of June 30, 2017.

During the fiscal year 2013, the Company entered into an agreement with the Shandong Shouguang Vegetable Seed Industry Group Co., Ltd, a related party, to provide property management services for an annual amount of approximately $100,000 for five years from January 1, 2013 to December 31, 2017. The expenses associated with this agreement for the three months period ended June 30, 2017 and 2016 were approximately $22,800 and $24,000. The expenses associated with this agreement for the six months period ended June 30, 2017 and 2016 were approximately $45,400 and $48,000.

NOTE 8 – TAXES PAYABLE

| Taxes payable consists of the following: |

| June 30, | December 31, | |||||||

| 2017 | 2016 | |||||||

| Income tax payable | $ | 4,943,143 | $ | 1,849,535 | ||||

| Natural resource tax | 332,089 | 651,230 | ||||||

| Value added tax payable | 1,547,329 | 887,913 | ||||||

| Land use tax payable | 782,072 | 818,921 | ||||||

| Other tax payables | 179,079 | 133,732 | ||||||

| Total | $ | 7,783,712 | $ | 4,341,331 | ||||

NOTE 9 – CAPITAL LEASE OBLIGATIONS

The components of capital lease obligations are as follows:

| Imputed | June 30, | December 31, | |||||||

| Interest rate | 2017 | 2016 | |||||||

| Total capital lease obligations | 6.7% | $ | 2,339,805 | $ | 2,472,637 | ||||

| Less: Current portion | (117,558 | ) | (187,678 | ) | |||||

| Capital lease obligations, net of current portion | $ | 2,222,247 | $ | 2,284,959 | |||||

Interest expenses from capital lease obligations amounted to $41,375 and $45,873 for the three-month period ended June 30, 2017 and 2016, respectively, which were charged to the condensed consolidated statement of income. Interest expenses from capital lease obligations amounted to $83,128 and $91,764 for the six-month period ended June 30, 2017 and 2016, respectively, which were charged to the condensed consolidated statement of income.

11

GULF RESOURCES, INC.

AND SUBSIDIARIES

NOTES TO CONDENSED CONSOLIDATED FINANCIAL STATEMENTS

JUNE 30, 2017

(Expressed in U.S. dollars)

(UNAUDITED)

NOTE 10 ––EQUITY

| (a) | Authorized shares |

During the annual general meeting held on June 18, 2013, the shareholders of the Company approved the amendment to the Certificate of Incorporation to decrease the number of the authorized shares of the Company’s common stock to 80,000,000. The Company filed an amended and restated Certificate of Incorporation with the Secretary of the State of Delaware to decrease the number of authorized shares of the Company’s common stock. Accordingly, 80,000,000 is disclosed as the authorized shares of the Company’s common stock in the consolidated balance sheets as of June 30, 2017 and December 31, 2016.

| (b) | Retained Earnings - Appropriated |

In accordance with the relevant PRC regulations and the PRC subsidiaries’ Articles of Association, the Company’s PRC subsidiaries are required to allocate its profit after tax to the following reserve:

Statutory Common Reserve Funds

SCHC, SYCI and DCHC are required each year to transfer at least 10% of the profit after tax as reported under the PRC statutory financial statements to the Statutory Common Reserve Funds until the balance reaches 50% of the registered share capital. This reserve can be used to make up any loss incurred or to increase share capital. Except for the reduction of losses incurred, any other application should not result in this reserve balance falling below 25% of the registered capital. The Statutory Common Reserve Fund as of June 30, 2017 for SCHC, SYCI and DCHC is 46%, 16% and 0% of its registered capital respectively.

NOTE 11 – STOCK-BASED COMPENSATION

Pursuant to the Company’s Amended and Restated 2007 Equity Incentive Plan approved in 2011(“Plan”), the aggregate number of shares of the Company’s common stock available for grant of stock options and issuance is 4,341,989 shares. On October 5, 2015, during the annual meeting of the Company’s stockholders, the aggregate number of shares reserved and available for grant and issuance pursuant to the Plan was increased to 10,341,989. As of June 30, 2017, the number of shares of the Company’s common stock available for issuance under the Plan is 7,325,989.

The fair value of each option award below is estimated on the date of grant using the Black-Scholes option-pricing model. The risk free rate is based on the yield-to-maturity in continuous compounding of the US Government Bonds with the time-to-maturity similar to the expected tenor of the option granted, volatility is based on the annualized historical stock price volatility of the Company, and the expected life is based on the historical option exercise pattern.

On March 2, 2017, the Company granted to an independent director an option to purchase 12,500 shares of the Company’s common stock at an exercise price of $1.98 per share and the options vested immediately. The options were valued at $9,000 fair value, with assumed 57.42% volatility, a three-year expiration term, with an expected tenor of 1.69 years, a risk free rate of 1.59% and no dividend yield. For the three-month and six-month periods ended June 30, 2017, $9,000 was recognized as general and administrative expenses.

On May 7, 2017, the Company granted to an independent director an option to purchase 12,500 shares of the Company’s common stock at an exercise price of $1.90 per share and the options vested immediately. The options were valued at $5,700 fair value, with assumed 45.71% volatility, a three-year expiration term with an expected tenor of 1.70 years, a risk free rate of 1.25% and no dividend yield. For the three-month and six-month period ended June 30, 2017, $5,700 was recognized as general and administrative expenses.

The following table summarizes all Company stock option transactions between January 1, 2017 and June 30, 2017.

|

Number of Option

and Warrants Outstanding and exercisable |

Weighted- Average Exercise price of Option

and Warrants |

Range of

Exercise Price per Common Share |

|||||||||||

| Balance, January 1, 2017 | 185,000 | $ | 2.19 | $1.54 - $4.80 | |||||||||

|

Granted and vested during the period Ended June 30, 2017 |

25,000 | $ | 1.94 | $1.90-1.98 | |||||||||

|

Expired during the period ended June 30, 2017 |

(37,500 | ) | $ | 2.18 | $1.83-2.55 | ||||||||

| Balance, June 30, 2017 | 172,500 | $ | 2.16 | $1.54 - $4.80 | |||||||||

12

GULF RESOURCES, INC.

AND SUBSIDIARIES

NOTES TO CONDENSED CONSOLIDATED FINANCIAL STATEMENTS

JUNE 30, 2017

(Expressed in U.S. dollars)

(UNAUDITED)

NOTE 11 – STOCK-BASED COMPENSATION – Continued

| Stock and Warrants Options Exercisable and Outstanding | |||||||

| Weighted Average | |||||||

| Remaining | |||||||

| Outstanding at June 30, 2017 |

Range of Exercise Prices |

Contractual Life (Years) |

|||||

|

Exercisable and outstanding |

172,500 | $1.54 - $4.80 | 1.89 | ||||

The aggregate intrinsic value of options outstanding and exercisable as of June 30, 2017 was $625.

NOTE 12 – INCOME TAXES

The Company utilizes the asset and liability method of accounting for income taxes in accordance with FASB ASC 740-10.

(a) United States

Gulf Resources, Inc. may be subject to the United States of America Tax law at a tax rate of 35%. No provision for the US federal income taxes has been made as the Company had no US taxable income for the three-month and six-month periods ended June 30, 2017 and 2016, and management believes that its earnings are permanently invested in the PRC.

(b) BVI

Upper Class Group Limited, a subsidiary of Gulf Resources, Inc., was incorporated in the BVI and, under the current laws of the BVI, it is not subject to tax on income or capital gain in the BVI. Upper Class Group Limited did not generate assessable profit for the three-month and six-month periods ended June 30, 2017 and 2016.

(c) Hong Kong

Hong Kong Jiaxing Industrial Limited, a subsidiary of Upper Class Group Limited, was incorporated in Hong Kong and is subject to Hong Kong profits tax. The Company is subject to Hong Kong taxation on its activities conducted in Hong Kong and income arising in or derived from Hong Kong. No provision for profits tax has been made as the Company has no assessable income for the three-month and six-month periods ended June 30, 2017 and 2016. The applicable statutory tax rates for the three-month and six-month periods ended June 30, 2017 and 2016 are 16.5%. There is no dividend withholding tax in Hong Kong.

(d) PRC

Enterprise income tax (“EIT”) for SCHC, SYCI and DCHC in the PRC is charged at 25% of the assessable profits.

The operating subsidiaries SCHC, SYCI and DCHC are wholly foreign-owned enterprises (“FIE”) incorporated in the PRC and are subject to PRC Foreign Enterprise Income Tax Law.

On February 22, 2008, the Ministry of Finance (“MOF”) and the State Administration of Taxation (“SAT”) jointly issued CaiShui [2008] Circular 1 (“Circular 1”). According to Article 4 of Circular 1, distributions of accumulated profits earned by a FIE prior to January 1, 2008 to foreign investor(s) in 2008 will be exempted from withholding tax (“WHT”) while distribution of the profit earned by an FIE after January 1, 2008 to its foreign investor(s) shall be subject to WHT at 5% effective tax rate.

13

GULF RESOURCES, INC.

AND SUBSIDIARIES

NOTES TO CONDENSED CONSOLIDATED FINANCIAL STATEMENTS

JUNE 30, 2017

(Expressed in U.S. dollars)

(UNAUDITED)

NOTE 12 – INCOME TAXES – Continued

As of June 30, 2017 and December 31, 2016, the accumulated distributable earnings under the Generally Accepted Accounting Principles (GAAP”) of PRC of the FIE of the Company are $302,276,282 and $274,769,840, respectively. Since the Company intends to reinvest its earnings to further expand its businesses in mainland China, its foreign invested enterprises do not intend to declare dividends to their immediate foreign holding companies in the foreseeable future. Accordingly, as of June 30, 2017 and December 31, 2016, the Company has not recorded any WHT on the cumulative amount of distributable retained earnings of its foreign invested enterprises in China. As of June 30, 2017 and December 31, 2016, the unrecognized WHT are $14,108,455 and $12,756,698, respectively.

The Company’s tax returns are subject to the various tax authorities’ examination. The federal, state and local authorities of the United States may examine the Company’s tax returns filed in the United States for three years from the date of filing. The Company’s US tax returns since 2013 are currently subject to examination. Inland Revenue Department of Hong Kong may examine the Company’s tax returns filed in Hong Kong for seven years from date of filing. The Company’s Hong Kong tax returns from year 2010 are currently subject to examination.

The components of the provision for income taxes from continuing operations are:

| Three-Month Period Ended June 30, | Six-Month Period Ended June 30, | |||||||||||||||

| 2017 | 2016 | 2017 | 2016 | |||||||||||||

| Current taxes – PRC | $ | 4,821,450 | $ | 4,210,422 | $ | 7,643,276 | $ | 6,478,093 | ||||||||

| Deferred taxes – PRC | — | — | — | — | ||||||||||||

| $ | 4,821,450 | $ | 4,210,422 | $ | 7,643,276 | $ | 6,478,093 | |||||||||

The effective income tax expenses differ from the PRC statutory income tax rate of 25% from continuing operations in the PRC as follows:

| Three-Month Period Ended June 30, | Six-Month Period Ended June 30, | |||||||||||||||

| Reconciliations | 2017 | 2016 | 2017 | 2016 | ||||||||||||

| Statutory income tax rate | 25 | % | 25 | % | 25 | % | 25 | % | ||||||||

| Non-deductible (Non-taxable)item | 1 | % | (1 | %) | 1 | % | - | |||||||||

| Effective tax rate | 26 | % | 24 | % | 26 | % | 25 | % | ||||||||

Significant components of the Company’s deferred tax assets and liabilities at June 30, 2017 and December 31, 2016 are as follows:

| June 30, | December 31, | |||||||

| 2017 | 2016 | |||||||

| Deferred tax liabilities | $ | — | $ | — | ||||

| Deferred tax assets: | ||||||||

| Allowance for obsolete and slow-moving inventories | $ | — | $ | — | ||||

| Impairment on property, plant and equipment | 431,213 | 421,106 | ||||||

| Exploration costs | 1,837,744 | 1,794,666 | ||||||

| Compensation costs of unexercised stock options | 109,386 | 120,986 | ||||||

| US federal net operating loss | 11,660,000 | 11,575,000 | ||||||

| Total deferred tax assets | 14,038,343 | 13,911,758 | ||||||

| Valuation allowance | (11,769,386 | ) | (11,695,986 | ) | ||||

| Net deferred tax asset | $ | 2,268,957 | $ | 2,215,772 | ||||

The increase in valuation allowance for each of the three-month periods ended June 30, 2017 and 2016 is $32,600 and $1,495, respectively.

The increase in valuation allowance for the six-month period ended June 30, 2017 is $73,400.

The decrease in valuation allowance for the six-month period ended June 30, 2016 is $100,150.

There were no unrecognized tax benefits and accrual for uncertain tax positions as of June 30, 2017 and December 31, 2016.

14

GULF RESOURCES, INC.

AND SUBSIDIARIES

NOTES TO CONDENSED CONSOLIDATED FINANCIAL STATEMENTS

JUNE 30, 2017

(Expressed in U.S. dollars)

(UNAUDITED)

NOTE 13 – BUSINESS SEGMENTS

The Company has four reportable segments: bromine, crude salt, chemical products and natural gas. The reportable segments are consistent with how management views the markets served by the Company and the financial information that is reviewed by its chief operating decision maker.

An operating segment’s performance is primarily evaluated based on segment operating income, which excludes share-based compensation expense, certain corporate costs and other income not associated with the operations of the segment. These corporate costs (income) are separately stated below and also include costs that are related to functional areas such as accounting, treasury, information technology, legal, human resources, and internal audit. The Company believes that segment operating income, as defined above, is an appropriate measure for evaluating the operating performance of its segments. All the customers are located in PRC.

|

Three-Month Period Ended June 30, 2017 |

Bromine* |

Crude Salt* |

Chemical Products |

Natural Gas |

Segment Total |

Corporate | Total | |||||||||||||||||||||

|

Net revenue

(external customers) |

$ | 18,423,133 | $ | 2,521,883 | $ | 26,586,973 | $ | — | $ | 47,531,989 | $ | — | $ | 47,531,989 | ||||||||||||||

|

Net revenue

(intersegment) |

2,910,743 | — | — | — | 2,910,743 | — | 2,910,743 | |||||||||||||||||||||

| Income(loss) from operations before taxes | 9,740,981 | 1,051,202 | 8,318,480 | (33,529 | ) | 19,077,134 | (594,662 | ) | 18,482,472 | |||||||||||||||||||

| Income taxes | 2,464,085 | 245,164 | 2,112,201 | — | 4,821,450 | — | 4,821,450 | |||||||||||||||||||||

| Income (loss) from operations after taxes | 7,276,896 | 806,038 | 6,206,279 | (33,529 | ) | 14,255,684 | (594,662 | ) | 13,661,022 | |||||||||||||||||||

| Total assets | 162,696,276 | 32,749,355 | 207,885,555 | 1,819,284 | 405,150,470 | 114,373 | 405,264,843 | |||||||||||||||||||||

| Depreciation and amortization | 3,794,600 | 624,226 | 951,364 | — | 5,370,190 | — | 5,370,190 | |||||||||||||||||||||

| Goodwill | — | — | 28,332,661 | — | 28,332,661 | — | 28,332,661 | |||||||||||||||||||||

|

Three-Month Period Ended June 30, 2016 |

Bromine* |

Crude Salt* |

Chemical Products |

Natural Gas |

Segment Total |

Corporate | Total | |||||||||||||||||||||

|

Net revenue

(external customers) |

$ | 18,480,605 | $ | 2,305,688 | $ | 26,814,474 | $ | — | $ | 47,600,767 | $ | — | $ | 47,600,767 | ||||||||||||||

|

Net revenue

(intersegment) |

2,670,931 | — | — | — | 2,670,931 | — | 2,670,931 | |||||||||||||||||||||

| Income(loss) from operations before taxes | 8,199,652 | (10,099 | ) | 8,531,677 | (25 | ) | 16,721,205 | 609,917 | 17,331,122 | |||||||||||||||||||

| Income taxes | 1,810,252 | 235,779 | 2,164,391 | — | 4,210,422 | — | 4,210,422 | |||||||||||||||||||||

| Income (loss) from operations after taxes | 6,389,400 | (245,878 | ) | 6,367,286 | (25 | ) | 12,510,783 | 609,917 | 13,120,700 | |||||||||||||||||||

| Total assets | 149,221,327 | 30,673,443 | 193,703,787 | 1,058,651 | 374,657,208 | 118,573 | 374,775,781 | |||||||||||||||||||||

| Depreciation and amortization | 4,144,546 | 1,339,696 | 1,160,329 | — | 6,644,571 | — | 6,644,571 | |||||||||||||||||||||

| Capital expenditure | — | — | — | 813,589 | 813,589 | — | 813,589 | |||||||||||||||||||||

| Goodwill | — | — | 28,944,958 | — | 28,944,958 | — | 28,944,958 | |||||||||||||||||||||

15

GULF RESOURCES, INC.

AND SUBSIDIARIES

NOTES TO CONDENSED CONSOLIDATED FINANCIAL STATEMENTS

JUNE 30, 2017

(Expressed in U.S. dollars)

(UNAUDITED)

NOTE 13 – BUSINESS SEGMENTS – Continued

|

Six-Month Period Ended June 30, 2017 |

Bromine* |

Crude Salt* |

Chemical Products |

Natural Gas |

Segment Total |

Corporate | Total | ||||||||||||||||||||

|

Net revenue (external customers) |

$ | 32,345,527 | $ | 4,335,661 | $ | 43,639,294 | $ | - | $ | 80,320,482 | $ | - | $ | 80,320,482 | |||||||||||||

|

Net revenue (intersegment) |

5,089,236 | - | - | - | 5,089,236 | - | 5,089,236 | ||||||||||||||||||||

| Income(loss) from operations before taxes | 15,012,915 | 1,937,089 | 13,264,657 | (57,287 | ) | 30,157,374 | (861,905 | ) | 29,295,469 | ||||||||||||||||||

| Income taxes | 3,794,188 | 468,746 | 3,380,342 | - | 7,643,276 | - | 7,643,276 | ||||||||||||||||||||

| Income (loss) from operations after taxes | 11,218,727 | 1,468,343 | 9,884,315 | (57,287 | ) | 22,514,098 | (861,905 | ) | 21,652,193 | ||||||||||||||||||

| Total assets | 162,696,276 | 32,749,355 | 207,885,555 | 1,819,284 | 405,150,470 | 114,373 | 405,264,843 | ||||||||||||||||||||

| Depreciation and amortization | 7,793,181 | 1,078,673 | 1,937,435 | - | 10,809,289 | - | 10,809,289 | ||||||||||||||||||||

| Goodwill | - | - | 28,332,661 | - | 28,332,661 | - | 28,332,661 | ||||||||||||||||||||

|

Six-Month Period Ended June 30, 2016 |

Bromine* |

Crude Salt* |

Chemical Products |

Natural Gas |

Segment Total |

Corporate | Total | ||||||||||||||||||||

|

Net revenue (external customers) |

$ | 31,650,133 | $ | 4,072,296 | $ | 46,373,788 | $ | - | $ | 82,096,217 | $ | - | $ | 82,096,217 | |||||||||||||

|

Net revenue (intersegment) |

4,493,133 | - | - | - | 4,493,133 | - | 4,493,133 | ||||||||||||||||||||

| Income(loss) from operations before taxes | 11,205,170 | 217,514 | 14,255,408 | (25 | ) | 25,678,067 | 319,373 | 25,997,440 | |||||||||||||||||||

| Income taxes | 2,553,622 | 299,283 | 3,625,188 | - | 6,478,093 | - | 6,478,093 | ||||||||||||||||||||

| Income (loss) from operations after taxes | 8,651,548 | (81,769 | ) | 10,630,220 | (25 | ) | 19,199,974 | 319,373 | 19,519,347 | ||||||||||||||||||

| Total assets | 149,221,327 | 30,673,443 | 193,703,787 | 1,058,651 | 374,657,208 | 118,573 | 374,775,781 | ||||||||||||||||||||

| Depreciation and amortization | 8,512,338 | 2,532,362 | 2,469,592 | - | 13,514,292 | - | 13,514,292 | ||||||||||||||||||||

| Capital expenditure | 52,777 | 4,509 | - | 813,589 | 870,875 | - | 870,875 | ||||||||||||||||||||

| Goodwill | - | - | 28,944,958 | - | 28,944,958 | - | 28,944,958 | ||||||||||||||||||||

* Certain common production overheads, operating and administrative expenses and asset items (mainly cash and certain office equipment) of bromine and crude salt segments in SCHC were split by reference to the average selling price and production volume of the respective segment.

16

GULF RESOURCES, INC.

AND SUBSIDIARIES

NOTES TO CONDENSED CONSOLIDATED FINANCIAL STATEMENTS

JUNE 30, 2017

(Expressed in U.S. dollars)

(UNAUDITED)

NOTE 13 – BUSINESS SEGMENTS – Continued

| Three-Month Period Ended June 30, | Six-Month Period Ended June 30, | |||||||||||||||

| Reconciliations | 2017 | 2016 | 2017 | 2016 | ||||||||||||

| Total segment operating income | $ | 19,077,134 | $ | 16,721,205 | $ | 30,157,374 | $ | 25,678,067 | ||||||||

| Corporate costs | (128,007 | ) | (69,279 | ) | (257,995 | ) | (229,361 | ) | ||||||||

| Unrealized gain/(loss) on translation of intercompany balance | (466,655 | ) | 679,196 | (603,910 | ) | 548,734 | ||||||||||

| Income from operations | 18,482,472 | 17,331,122 | 29,295,469 | 25,997,440 | ||||||||||||

| Other income, net of expense | 90,656 | 76,319 | 174,605 | 144,636 | ||||||||||||

| Income before taxes | $ | 18,573,128 | $ | 17,407,441 | $ | 29,470,074 | $ | 26,142,076 | ||||||||

The following table shows the major customer(s) (10% or more) for the three-month period ended June 30, 2017.

| Number | Customer |

Bromine (000’s) |

Crude Salt (000’s) |

Chemical Products (000’s) |

Total Revenue (000’s) |

Percentage of Total Revenue (%) |

|||||

| 1 | Shandong Morui Chemical Company Limited |

$ 3,111

|

$ 753

|

$ 1,684

|

$ 5,548 | 11.7% |

The following table shows the major customer(s) (10% or more) for the six-month period ended June 30, 2017.

| Number | Customer |

Bromine (000’s) |

Crude Salt (000’s) |

Chemical Products (000’s) |

Total Revenue (000’s) |

Percentage of Total Revenue (%) |

|||||

| 1 | Shandong Morui Chemical Company Limited |

$ 5,705

|

$ 1,251

|

$ 2,768

|

$ 9,724 | 12.1% |

The following table shows the major customer(s) (10% or more) for the three-month period ended June 30, 2016.

| Number | Customer |

Bromine (000’s) |

Crude Salt (000’s) |

Chemical Products (000’s) |

Total Revenue (000’s) |

Percentage of Total Revenue (%) |

|||||

| 1 | Shandong Morui Chemical Company Limited |

$ 3,269

|

$ 686

|

$ 1,696

|

$ 5,651 | 11.9% |

The following table shows the major customer(s) (10% or more) for the six-month period ended June 30, 2016.

| Number | Customer |

Bromine (000’s) |

Crude Salt (000’s) |

Chemical Products (000’s) |

Total Revenue (000’s) |

Percentage of Total Revenue (%) |

|||||

| 1 | Shandong Morui Chemical Company Limited |

$ 5,692

|

$ 1,172

|

$ 2,997

|

$ 9,861 | 12.0% |

NOTE 14 – CUSTOMER CONCENTRATION

During the three-month and six-month periods ended June 30, 2017, the Company sold 34.0% and 35.0% of its products to its top five customers, respectively. As of June 30, 2017, amounts due from these customers were $38,735,709. During the three-month and six-month periods ended June 30, 2016, the Company sold 33.9% and 34.1% of its products to its top five customers, respectively. As of June 30, 2016, amounts due from these customers were $28,870,903. This concentration makes the Company vulnerable to a near-term severe impact, should the relationships be terminated.

NOTE 15 – MAJOR SUPPLIERS

During the three-month and six-month periods ended June 30, 2017, the Company purchased 66.5% and 67.5% of its raw materials from its top five suppliers, respectively. As of June 30, 2017, amounts due to those suppliers for the three-month and six-month periods ended June 30, 2017 included in accounts payable were $8,048,563 and $6,833,430. During the three-month and six-month periods ended June 30, 2016, the Company purchased 54.5% and 54.8% of its raw materials from its top five suppliers, respectively. As of June 30, 2016, amounts due to those suppliers included in accounts payable were $6,542,424.This concentration makes the Company vulnerable to a near-term severe impact, should the relationships be terminated.

17

GULF RESOURCES, INC.

AND SUBSIDIARIES

NOTES TO CONDENSED CONSOLIDATED FINANCIAL STATEMENTS

JUNE 30, 2017

(Expressed in U.S. dollars)

(UNAUDITED)

NOTE 16 – FAIR VALUE OF FINANCIAL INSTRUMENTS

The carrying values of financial instruments, which consist of cash, accounts receivable and accounts payable and other payables, approximate their fair values due to the short-term nature of these instruments. There were no material unrecognized financial assets and liabilities as of June 30, 2017 and December 31, 2016.

NOTE 17 – CAPITAL COMMITMENT AND OPERATING LEASE COMMITMENTS

As of June 30, 2017, the Company has leased real property adjacent to Factory No. 1, with the related production facility, channels and ducts, other production equipment and the buildings located on the property, under a capital lease. The future minimum lease payments required under the capital lease, together with the present value of such payments, are included in the table shown below.

The Company has leased nine parcels of land under non-cancelable operating leases, which are fixed rentals and expire through December 2021, December 2023, December 2030, December 2031, December 2032, December 2040, February 2059, August 2059 and June 2060, respectively.

The following table sets forth the Company’s contractual obligations as of June 30, 2017:

| Capital Lease Obligations | Operating Lease Obligations | Property Management Fees | ||||||||||

| Payable within: | ||||||||||||

| the next 12 months | $ | 277,064 | $ | 953,773 | $ | 46,044 | ||||||

| the next 13 to 24 months | 277,064 | 973,475 | — | |||||||||

| the next 25 to 36 months | 277,064 | 997,246 | — | |||||||||

| the next 37 to 48 months | 277,064 | 1,018,890 | — | |||||||||

| the next 49 to 60 months | 277,064 | 879,430 | — | |||||||||

| thereafter | 2,216,512 | 16,060,555 | — | |||||||||

| Total | $ | 3,601,832 | $ | 20,883,369 | $ | 46,044 | ||||||

| Less: Amount representing interest | (1,262,027 | ) | ||||||||||

| Present value of net minimum lease payments | $ | 2,339,805 | ||||||||||

18

GULF RESOURCES, INC.

AND SUBSIDIARIES

NOTES TO CONDENSED CONSOLIDATED FINANCIAL STATEMENTS

JUNE 30, 2017

(Expressed in U.S. dollars)

(UNAUDITED)

NOTE 17 – CAPITAL COMMITMENT AND OPERATING LEASE COMMITMENTS – Continued

Rental expenses related to operating leases of the Company amounted to $256,447 and $264,240, which were charged to the condensed consolidated statements of income for the three months ended June 30, 2017 and 2016, respectively. Rental expenses related to operating leases of the Company amounted to $511,566 and $524,624, which were charged to the condensed consolidated statements of income for the six months ended June 30, 2017 and 2016, respectively.

19

Cautionary Note Regarding Forward-Looking Statements

The discussion below contains “forward-looking statements” within the meaning of the Private Securities Litigation Reform Act of 1995, Section 27A of the Securities Act, and Section 21E of the Exchange Act. We have used words such as “believes,” “intends,” “anticipates,” “expects” and similar expressions to identify forward-looking statements. These statements are based on information currently available to us and are subject to a number of risks and uncertainties that may cause our actual results of operations, financial condition, cash flows, performance, business prospects and opportunities and the timing of certain events to differ materially from those expressed in, or implied by, these statements. These risks, uncertainties and other factors include, without limitation, those matters discussed in Item 1A of Part I of our 2016 Form 10-K. Except as expressly required by the federal securities laws, we undertake no obligation to update such factors or to publicly announce the results of any of the forward-looking statements contained herein to reflect future events, developments, or changed circumstances, or for any other reason. The following discussion should be read in conjunction with our consolidated financial statements and notes thereto appearing in our 2016 Form 10-K and Item 1A, “Risk Factors” for the year ended December 31, 2016.

Overview

We are a holding company which conducts operations through our wholly-owned China-based subsidiaries. Our business is conducted and reported in four segments, namely, bromine, crude salt, chemical products and natural gas.

Through our wholly-owned subsidiary, SCHC, we produce and trade bromine and crude salt. We are one of the largest producers of bromine in China, as measured by production output. Elemental bromine is used to manufacture a wide variety of bromine compounds used in industry and agriculture. Bromine also is used to form intermediary chemical compounds such as Tetramethylbenzidine. Bromine is commonly used in brominated flame retardants, fumigants, water purification compounds, dyes, medicines and disinfectants. Crude salt is the principal material in alkali production as well as chlorine alkali production and is widely used in the chemical, food and beverage, and other industries.

Through our wholly-owned subsidiary, SYCI, we manufacture and sell chemical products used in oil and gas field exploration, oil and gas distribution, oil field drilling, wastewater processing, papermaking chemical agents and inorganic chemicals.

On December 12, 2006, we acquired, through a share exchange, Upper Class Group Limited, a British Virgin Islands holding corporation which then owned all of the outstanding shares of SCHC. Under accounting principles generally accepted in the United States, the share exchange is considered to be a capital transaction in substance, rather than a business combination. That is, the share exchange is equivalent to the issuance of stock by Upper Class for the net assets of our Company, accompanied by a recapitalization, and is accounted for as a change in capital structure. Accordingly, the accounting for the share exchange was identical to that resulting from a reverse acquisition, except no goodwill was recorded. Under reverse takeover accounting, the post reverse acquisition comparative historical consolidated financial statements of the legal acquirer, our Company, are those of the legal acquiree, Upper Class Group Limited, which is considered to be the accounting acquirer. Share and per share amounts reflected in this report have been retroactively adjusted to reflect the merger.

On February 5, 2007, the Company, acting through SCHC, acquired SYCI. Since the ownership of the Company and SYCI was then substantially the same, the transaction was accounted for as a transaction between entities under common control, whereby we recognized the assets and liabilities of SYCI at their carrying amounts. Share and per share amounts stated in this report have been retroactively adjusted to reflect the merger.

On August 31, 2008, SYCI completed the construction of a new chemical production line. It passed the examination by Shouguang City Administration of Work Safety and local fire department. This new production line focuses on producing environmental friendly additive products, solid lubricant and polyether lubricant, for use in oil and gas exploration. The line has an annual production capacity of 5,000 tons. Formal production of this chemical production line started on September 15, 2008. The total annual production capacity of SYCI is 36,300 tons.

20

On October 12, 2009 we completed a 1-for-4 reverse stock split of our common stock, such that for each four shares outstanding prior to the stock split there was one share outstanding after the reverse stock split. All shares of common stock referenced in this report have been adjusted to reflect the stock split figures. On October 27, 2009 our shares began trading on the NASDAQ Global Select Market under the ticker symbol “GFRE” and on June 30, 2011 we changed our ticker symbol to “GURE” to better reflection of our corporate name.

On January 12, 2015, the Company and SCHC entered into an Equity Interest Transfer Agreement with SCRC pursuant to which SCHC agreed to acquire SCRC and all rights, title and interest in and to all assets owned by SCRC, a leading manufacturer of materials for human and animal antibiotics in China and other parts of Asia.

On February 4, 2015 the Company closed the transactions contemplated by the agreement between the Company, SCHC and SCRC.

On the closing date, the Company issued 7,268,011 shares of its common stock, par value $0.0005 per share (the “Shares”), at the closing market price of $1.84 per Share on the closing date to the four former equity owners of SCRC .The issuance of the Shares was exempt from registration pursuant to Regulation S of the Securities Act of 1933, as amended. On the closing date, the Company entered into a lock-up agreement with the four former equity owners of SCRC. In accordance with the terms of the lock-up agreement, the shareholders agreed not to sell or transfer the Shares for five years from the date the stock certificates evidencing the Shares were issued.

The sellers of SCRC agreed as part of the purchase price to accept the Shares, based on a valuation of $2.00, which was a 73% premium to the price on the day the agreement was entered into. For accounting purposes, the Shares are now being valued at $1.84, which was the closing price of our stock on the day of the closing date of the agreement. The price difference between the original $2.00 and the current $1.84 is solely for accounting purposes. There has been no change in the number of shares issued.

On November 24, 2015, Gulf Resources, Inc., a Delaware corporation consummated a merger with and into its wholly-owned subsidiary, Gulf Resources, Inc., a Nevada corporation. As a result of the reincorporation, the Company is now a Nevada corporation.

On December 15, 2015, the Company registered a new subsidiary in the Sichuan Province of the PRC named Daying County Haoyuan Chemical Company Limited (“DCHC”) with registered Capital of RMB50,000,000, and there was RMB11,754,919 capital contributed by SCHC as of March 31, 2017. DCHC was established to further explore and develop natural gas and brine resources (including bromine and crude salt) in China.

On September 2, 2016, the Company announced the planned merger of two of its 100% owned subsidiaries, Shouguan Yuxin Chemical Co., Limited (“SYCI”) and Shouguan Rongyuan Chemical Co., Ltd (“SCRC”). On March 24, 2017, the legal process of the merger was completed and SCRC was officially deregistered on March 28, 2017. The results of these two subsidiaries were reported as SYCI in the three and six months ended June 30, 2017.

Our current corporate structure chart is set forth in the following diagram:

As a result of our acquisitions of SCHC and SYCI, our historical financial statements and the information presented below reflects the accounts of SCHC, SYCI and DCHC. The following discussion should be read in conjunction with our consolidated financial statements and notes thereto appearing elsewhere in this report.

21

RESULTS OF OPERATIONS

The following table presents certain information derived from the consolidated statements of operations, cash flows and stockholders equity for the three-month and six-month periods ended June 30, 2017 and 2016.

Comparison of the Three-Month Period Ended June 30, 2017 and 2016

|

Three-Month Period

Ended June 30, 2017 |

Three-Month Period

Ended June 30, 2016 |

Percent Change

Increase/ (Decrease) |

||||||||||

| Net revenue | $ | 47,531,989 | $ | 47,600,767 | — | |||||||

| Cost of net revenue | $ | (26,931,742 | ) | $ | (29,195,255 | ) | (8 | %) | ||||

| Gross profit | $ | 20,600,247 | $ | 18,405,512 | 12 | % | ||||||

| Sales, marketing and other operating expenses | $ | (100,613 | ) | $ | (104,369 | ) | (4 | %) | ||||

| Research and development costs | $ | (65,274 | ) | $ | (70,378 | ) | (7 | %) | ||||

| General and administrative expenses | $ | (2,056,943 | ) | $ | (1,009,882 | ) | 104 | % | ||||

| Other operating income | $ | 105,055 | $ | 110,239 | (5 | %) | ||||||

| Income from operations | $ | 18,482,472 | $ | 17,331,122 | 7 | % | ||||||

| Other income | $ | 90,656 | $ | 76,319 | 19 | % | ||||||

| Income before taxes | $ | 18,573,128 | $ | 17,407,441 | 7 | % | ||||||

| Income taxes | $ | (4,821,450 | ) | $ | (4,210,422 | ) | 15 | % | ||||

| Net income | $ | 13,751,678 | $ | 13,197,019 | 4 | % | ||||||