As filed with the Securities and Exchange Commission on February 20, 2018.

SECURITIES AND EXCHANGE COMMISSION

WASHINGTON, D.C. 20549

FORM 20-F

|

REGISTRATION STATEMENT PURSUANT TO SECTION 12(b) OR 12(g) OF THE SECURITIES EXCHANGE ACT OF 1934

|

|

Or

|

þ

|

ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934

|

For the fiscal year ended December 31, 2017

Or

|

TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934

|

|

Or

|

SHELL COMPANY REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934

|

|

Date of event requiring this shell company report ____________

For the transition period from N/A to N/A

Commission file number: 001-14930

HSBC Holdings plc

(Exact name of Registrant as specified in its charter)

|

N/A

|

United Kingdom

|

|

|

(Translation of Registrant’s name into English)

|

(Jurisdiction of incorporation or organisation)

|

|

8 Canada Square

London E14 5HQ

United Kingdom

(Address of principal executive offices)

Gavin A Francis

8 Canada Square

London E14 5HQ

United Kingdom

Tel +44 (0) 20 7991 8888

Fax +44 (0) 20 7992 4880

(Name, Telephone, Email and/or Facsimile number and Address of Company Contact Person)

Securities registered or to be registered pursuant to Section 12(b) of the Securities Exchange Act of 1934:

|

Title of each class

|

Name of each exchange on which registered

|

|

|

Ordinary Shares, nominal value US$0.50 each.

|

London Stock Exchange

|

|

|

Hong Kong Stock Exchange

|

||

|

Euronext Paris

|

||

|

Bermuda Stock Exchange

|

||

|

New York Stock Exchange*

|

||

|

American Depository Shares, each representing 5

Ordinary Shares of nominal value US$0.50 each.

|

New York Stock Exchange

|

|

|

6.20% Non-Cumulative Dollar Preference Shares, Series A

|

New York Stock Exchange*

|

|

|

American Depositary Shares evidenced by American Depositary receipts, each representing one-fortieth of a Share of 6.20% Non-Cumulative Dollar Preference Shares, Series A

|

New York Stock Exchange

|

|

|

5.10% Senior Unsecured Notes Due 2021

|

New York Stock Exchange

|

|

|

4.00% Senior Unsecured Notes Due 2022

|

New York Stock Exchange

|

|

|

4.875% Senior Unsecured Notes Due 2022

|

New York Stock Exchange

|

|

|

7.625% Subordinated Notes due 2032

|

New York Stock Exchange

|

|

|

7.35% Subordinated Notes due 2032

|

New York Stock Exchange

|

|

|

6.5% Subordinated Notes 2036

|

New York Stock Exchange

|

|

|

6.5% Subordinated Notes 2037

|

New York Stock Exchange

|

|

|

6.8% Subordinated Notes Due 2038

|

New York Stock Exchange

|

|

|

6.100% Senior Unsecured Notes due 2042

|

New York Stock Exchange

|

|

|

8.125% Perpetual Subordinated Capital Securities Exchangeable at the Issuer’s Option into Non-Cumulative Dollar Preference Shares

|

New York Stock Exchange

|

|

|

8.00% Perpetual Subordinated Capital Securities Exchangeable at the Issuer’s Option into Non-

Cumulative Dollar Preference Shares, Series 2

|

New York Stock Exchange

|

|

|

4.250% Subordinated Notes due 2024

|

New York Stock Exchange

|

|

|

5.250% Subordinated Notes due 2044

|

New York Stock Exchange

|

|

|

4.250% Subordinated Notes due 2025

|

New York Stock Exchange

|

|

|

3.400% Senior Unsecured Notes due 2021

|

New York Stock Exchange

|

|

|

4.300% Senior Unsecured Notes due 2026

|

New York Stock Exchange

|

|

|

Floating Rate Senior Unsecured Notes due 2021

|

New York Stock Exchange

|

|

|

2.950% Senior Unsecured Notes due 2021

|

New York Stock Exchange

|

|

|

3.600% Senior Unsecured Notes due 2023

|

New York Stock Exchange

|

|

|

3.900% Senior Unsecured Notes due 2026

|

New York Stock Exchange

|

|

|

Floating Rate Senior Unsecured Notes due 2021

|

New York Stock Exchange

|

|

|

2.650% Senior Unsecured Notes due 2022

|

New York Stock Exchange

|

|

|

Floating Rate Senior Unsecured Notes due 2022

|

New York Stock Exchange

|

|

|

4.375% Subordinated Notes due 2026

|

New York Stock Exchange

|

|

|

3.262% Fixed Rate/Floating Rate Senior Unsecured Notes due 2023

|

New York Stock Exchange

|

|

|

3.033% Fixed Rate/Floating Rate Senior Unsecured Notes due 2023

|

New York Stock Exchange

|

|

|

4.041% Fixed Rate/Floating Rate Senior Unsecured Notes due 2028

|

New York Stock Exchange

|

|

Securities registered or to be registered pursuant to Section 12(g) of the Securities Exchange Act of 1934:

None

Securities for which there is a reporting obligation pursuant to Section 15(d) of the Securities Exchange Act of 1934:

None

Indicate the number of outstanding shares of each of the issuer’s classes of capital or common stock as of the close of the period covered by the annual report:

Ordinary Shares, nominal value US$0.50 each

20,321,372,907

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act.

þ

Yes

¨

No

If this report is an annual or transition report, indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or 15(d) of the Securities Exchange Act of 1934.

¨

Yes

þ

No

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days.

þ

Yes

¨

No

Indicate by check mark whether the registrant has submitted electronically and posted on its corporate Web site, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T (§232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files).

þ

Yes

¨

No

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, or a non-accelerated filer. See definition of “accelerated filer and large accelerated filer” in Rule 12b-2 of the Exchange Act. (Check one):

|

Large accelerated filer

þ

|

Accelerated filer

|

Non-accelerated filer

|

||

Indicate by check mark which basis of accounting the registrant has used to prepare the financial statements included in this filing:

|

U.S. GAAP

|

International Financial Reporting Standards as issued by the

International Accounting Standards Board

þ

|

Other

|

||

If “Other” has been checked in response to the previous question indicate by check mark which financial statement item the registrant has elected to follow.

¨

Item 17

¨

Item 18

If this is an annual report, indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act).

¨

Yes

þ

No

|

*

|

Not for trading, but only in connection with the registration of American Depositary Shares.

|

Connecting customers to opportunities

HSBC aims to be where the growth is, enabling business to thrive and economies to prosper, and ultimately helping people to fulfil their hopes and realise their ambitions.

Our cover image

Guangzhou is one of China’s largest and most dynamic cities. It is the capital of Guangdong Province and lies at the heart of China’s Pearl River Delta (PRD), one of the country’s fastest growing economic regions. The PRD in recent years has transformed from being the exporting factory floor of the world into a global leader in digital commerce and innovation. HSBC has had a presence in China for more than 150 years. China is an important part of the Group’s strategy and we have branches across the PRD. In December 2017 HSBC Qianhai Securities Limited, the first joint venture securities company in mainland China to be majority-owned by a foreign bank, opened for business in the PRD.

Inside front cover image

Dubai financial district.

Our photo competition winners

This report showcases five images taken by our employees around the world. The images were selected from more than 2,100 submissions to a Group-wide photography competition. Launched in June 2017, HSBC NOW Photo is an ongoing project that encourages employees to capture and share the diverse world around them with a camera.

None of the websites referred to in this Annual Report on Form 20-F for the year ended December 31, 2017 (the “Form 20-F”), including where a link is provided, nor any of the information contained on such websites is incorporated by reference in the Form 20-F.

Contents

Strategic Report

An overview of how we are structured, what we do and where, our strategic actions, the principal risks we face, and high-level performance information. The section is introduced by both the Group Chairman and the Group Chief Executive, and also explains the role of the Board.

This Strategic Report was approved by the Board on 20 February 2018.

Mark E Tucker

Group Chairman

2

Highlights

1a Forward-looking statements and Certain defined terms

4

Group Chairman’s Statement

7

Group Chief Executive’s Review

10

Our strategy

12

Strategic actions

14

Financial overview

18

Global businesses

22

How we do business

28

Risk overview

30

Remuneration

Financial Review

Detailed reporting of our financial performance, at Group level as well as within our matrix structure. It also includes our full risk report and reporting on how we manage capital.

32

Financial summary

64

Global businesses and geographical regions

83

Other information

86

Regulation and supervision

93 Disclosures pursuant to section 13(r) of the Securities Exchange Act

95

Risk

162

Capital

Corporate Governance

Details of our Board of Directors and senior management, and our approach to corporate governance and remuneration.

166

Corporate Governance Report

167

Biographies of Directors and senior management

171

Board of Directors

172

Board committees

178

Internal control

179

Going concern

179

Share capital and other disclosures

183

Employees

186

Directors’ Remuneration Report

Financial Statements

Our financial statements and related notes and reports.

210

Report of the Independent Registered Public Accounting Firm to the Board of Directors and Shareholders of HSBC Holdings plc

211

Financial Statements

222

Notes on the Financial Statements

Other Information

Important information for our shareholders, including contact information. Like any industry and company, we have our set of abbreviations and terminology. Accordingly, we provide an explanation of the abbreviations used. A glossary of key terms is available online at www.hsbc.com/investor-relations.

298

Shareholder information

306

Glossary of accounting terms and US equivalents

307 2016 HSBC 20F reconciliations table

309

Abbreviations

Our values

Our values define who we are as an organisation and make us distinctive.

Dependable

We are dependable, standing firm for what is right and delivering on commitments.

Open

We are open to different ideas and cultures, and value diverse perspectives.

Connected

We are connected to our customers, communities, regulators and each other, caring about individuals and their progress.

As a reminder

Reporting currency

We use US dollars.

Adjusted

measures

We supplement our IFRS figures with adjusted measures used by management internally. These measures are highlighted with the following symbol:

<

>

Ñ

Further explanation may be found on page

32

.

|

HSBC Holdings plc

|

1

|

|

Cautionary statement regarding forward-looking statements

The

Form 20-F

contains certain forward-looking statements with respect to HSBC’s financial condition, results of operations and business.

Statements that are not historical facts, including statements about HSBC’s beliefs and expectations, are forward-looking statements. Words such as ‘expects’, ‘targets’, ‘anticipates’, ‘intends’, ‘plans’, ‘believes’, ‘seeks’, ‘estimates’, ‘potential’ and ‘reasonably possible’, variations of these words and similar expressions are intended to identify forward-looking statements. These statements are based on current plans, estimates and projections, and therefore undue reliance should not be placed on them. Forward-looking statements speak only as of the date they are made. HSBC makes no commitment to revise or update any forward-looking statements to reflect events or circumstances occurring or existing after the date of any forward-looking statements.

Written and/or oral forward-looking statements may also be made in the periodic reports to the US Securities and Exchange Commission, summary financial statements to shareholders, proxy statements, offering circulars and prospectuses, press releases and other written materials, and in oral statements made by HSBC’s Directors, officers or employees to third parties, including financial analysts.

Forward-looking statements involve inherent risks and uncertainties. Readers are cautioned that a number of factors could cause actual results to differ, in some instances materially, from those anticipated or implied in any forward-looking statement. These include, but are not limited to:

|

•

|

Changes in general economic conditions in the markets in which we operate, such as continuing or deepening recessions and fluctuations in employment beyond those factored into consensus forecasts; changes in foreign exchange rates and interest rates; volatility in equity markets; lack of liquidity in wholesale funding markets; illiquidity and downward price pressure in national real estate markets; adverse changes in central banks’ policies with respect to the provision of liquidity support to financial markets; heightened market concerns over sovereign creditworthiness in over-indebted countries; adverse changes in the funding status of public or private defined benefit pensions; and consumer perception as to the continuing availability of credit and price competition in the market segments we serve.

|

|

•

|

Changes in government policy and regulation, including the monetary, interest rate and other policies of central banks and other regulatory authorities; initiatives to change the size, scope of activities and interconnectedness of financial institutions in connection with the implementation of stricter regulation of financial institutions in key markets worldwide; revised capital and liquidity benchmarks which could serve to deleverage bank balance sheets and lower returns available from the current business model and portfolio mix; imposition of levies or taxes designed to change business mix and risk appetite; the practices, pricing or responsibilities of financial institutions serving their consumer markets; expropriation, nationalisation, confiscation of assets and changes in legislation relating to foreign ownership; changes in bankruptcy legislation in the principal markets in which we operate and the consequences thereof; general changes in government policy that may significantly influence investor decisions; extraordinary government actions as a result of current market turmoil; other unfavourable political or diplomatic developments producing social instability or legal uncertainty which in turn may affect demand for our products and services; the costs, effects and outcomes of product regulatory reviews, actions or litigation, including any additional compliance requirements; and the effects of competition in the markets where we operate including increased competition from non-bank financial services companies, including securities firms.

|

|

•

|

Factors specific to HSBC, including our success in adequately identifying the risks we face, such as the incidence of loan losses or delinquency, and managing those risks (through account management, hedging and other techniques). Effective risk management depends on, among other things, our ability through stress testing and other techniques to prepare for events that cannot be captured by the statistical models it uses; and our success in addressing operational, legal and regulatory, and litigation challenges; and other risks and uncertainties we identify in ‘top and emerging risks’ on pages

95

to

106

.

|

Certain defined terms

Unless the context requires otherwise, ‘HSBC Holdings’ means HSBC Holdings plc and ‘HSBC’, the ‘Group’, ‘we’, ‘us’ and ‘our’ refer to HSBC Holdings together with its subsidiaries. Within this document the Hong Kong Special Administrative Region of the People’s Republic of China is referred to as ‘Hong Kong’. When used in the terms ‘shareholders’ equity’ and ‘total shareholders’ equity’, ‘shareholders’ means holders of HSBC Holdings ordinary shares and those preference shares and capital securities issued by HSBC Holdings classified as equity. The abbreviations ‘$m’, ‘$bn’ and ‘$tn’ represent millions, billions (thousands of millions) and trillions of US dollars, respectively.

|

HSBC Holdings plc

|

1a

|

Highlights

Our international network, universal banking model and capital strength deliver long-term value for customers and shareholders.

Group

For year ended 31 Dec 2017

(2016:

$7.1bn

)

$17.2bn

(2016:

$18.9bn

)

$21.0bn

(2016:

$48.0bn

)

$51.4bn

At 31 Dec 2017

(2016:

$857

bn)

$871bn

(2016: 13.6%)

14.5

%

(2016:

$2,375bn

)

$2,522bn

Strategy execution

|

–

|

Delivered growth from our international network with a 6% increase in transaction banking product revenue and a 13% rise in revenue synergies between global businesses compared with 2016.

|

|

–

|

Achieved annualised run-rate savings of $6.1bn since our Investor Update in 2015, while continuing to invest in growth, and regulatory programmes and compliance; 2017 exit run-rate in line with 2014 cost base.

|

|

–

|

Exceeded our risk-weighted assets (‘RWAs’) reduction target; extracting a total of $338bn of RWAs from the business since the start of 2015.

|

|

–

|

Pivot to Asia generating returns and driving over 75% of Group reported and adjusted profit in 2017.

|

|

–

|

Delivered a return on equity of 5.9% in 2017, up from 0.8% in 2016. We will continue to invest for growth and manage our capital efficiently to achieve our medium-term ROE target of >10%.

|

About HSBC

Around

38 million

customers bank with us.

We employ

229,000

people around the world*.

We have

200,000

shareholders in 131 countries and territories.

Today, HSBC has around

3,900

offices in 67 countries and territories worldwide.

*Full-time equivalent staff

|

2

|

HSBC Holdings plc

|

Our global businesses

Our operating model consists of four global businesses and a Corporate Centre, supported by HSBC Operations Services and Technology, and

11

global functions, including: risk, finance, financial crime risk, legal, marketing and human resources.

|

Retail Banking and Wealth Management (‘RBWM’)

|

Commercial Banking (‘CMB’)

|

Global Banking and Markets (‘GB&M’)

|

Global Private Banking (‘GPB’)

|

|

We help millions of people across the world to manage their finances, buy their homes, and save and invest for the future. Our Insurance and Asset Management businesses support all our global businesses in meeting their customers’ needs.

|

We support approximately 1.7 million business customers in 53 countries and territories with banking products and services to help them operate and grow. Our customers range from small enterprises focused primarily on their domestic markets, through to large companies operating globally.

|

We provide financial services and products to companies, governments and institutions. Our comprehensive range of products and solutions, across capital financing, advisory and transaction banking services, can be combined and customised to meet clients’ specific objectives.

|

We help high net worth individuals and their families to grow, manage and preserve their wealth.

|

|

Adjusted profit before tax

<

>

|

|||

|

(2016: $5.2bn)

|

(2016: $5.9bn)

|

(2016: $5.5bn)

|

(2016: $0.3bn)

|

|

$6.5bn

|

$6.8bn

|

$5.8bn

|

$0.3bn

|

|

Adjusted risk-weighted assets

<

>

|

|||

|

(31 Dec 2016: $114.7bn)

|

(31 Dec 2016: $286.9bn)

|

(31 Dec 2016: $307.7bn)

|

(31 Dec 2016: $15.7bn)

|

|

$121.5bn

|

$301.0bn

|

$299.3bn

|

$16.0bn

|

<

>

Our global businesses are presented on an adjusted basis, which is consistent with the way in which we assess the performance of our global businesses.

Delivery against Group financial targets

|

Return on equity

5.9%

|

Adjusted jaws

<

>

+1%

|

Dividends per ordinary share in respect of 2017

$0.51

|

Ñ

For further details, see page

17

.

|

HSBC Holdings plc

|

3

|

|

Group Chairman’s Statement

With an international network covering 90% of global trade flows and a leading presence in the world’s fastest growing region, we are in a prime position to help our customers capitalise on broad-based global growth.

Our 2017 results demonstrate both the strength and the potential of the Group. A large increase in reported profit before tax reflected both a healthy business and the non-recurrence of significant items from 2016. All of our global businesses grew adjusted profits and our three main global businesses generated improved adjusted revenue.

Strong revenue growth more than covered the cost of business investment, and increased lending laid a foundation for future performance. Asia again contributed a substantial proportion of the Group’s profits, particularly in Commercial Banking and Retail Banking and Wealth Management. Together, this delivered an adjusted Group profit before tax of $21bn, up 11% on 2016.

This performance has enabled us to approve an unchanged fourth interim dividend of $0.21. This brings the total dividend for 2017 to $0.51, representing a total shareholder return of 24% for 2017.

Board changes

As I start my first full year as Group Chairman, I am very grateful to my predecessor, Douglas Flint, and to Stuart Gulliver for ensuring a smooth handover. They steered HSBC through challenging waters during and after the global financial crisis, and renewed HSBC’s reputation as one of the world’s strongest and safest international banks. They have passed on a strong legacy.

My first responsibility as Group Chairman was to appoint a successor to Stuart who would be capable of building on his achievements while further enhancing the qualities that make HSBC unique. With an exceptional record of managing a diverse range of international businesses and a deep understanding of HSBC’s heritage and culture, John Flint was clearly the outstanding candidate. The Board and I look forward to working closely with John and his management team.

2017 also saw other Board changes as we said goodbye to Rachel Lomax, Sam Laidlaw and Paul Walsh. All three provided valuable service and wise counsel to the Board and I thank them warmly for their advice and support. I am especially grateful to Rachel for her excellent work as the Senior Independent Director and to Sam for his thoughtful leadership of the Nomination Committee.

|

4

|

HSBC Holdings plc

|

The year ahead

The Board is focused on sustaining resilience by enhancing reputation and performance. We will further develop our strategy to deliver value to all of our stakeholders within a governance framework that provides stability, prudence and effective oversight.

We expect the world’s major economies to show reasonable growth in 2018, helped by relatively low unemployment, recovering consumer confidence and improving trade. Fears of a hard landing in China have receded, and markets across Asia look set for a strong year. The anticipated conclusion of large regional trade agreements in 2018, mostly involving Asian nations, also provides cause for optimism. With an international network covering 90% of global trade flows and a leading presence in the world’s fastest growing region, we are in a prime position to help our customers capitalise on this broad-based global growth.

While we are optimistic about the prospects for the global economy, rising international tensions, the threat of protectionism and a lack of inclusive growth all have the potential to disrupt economic activity. We continue to model and anticipate a wide range of scenarios as part of our day-to-day risk management, to cover unlikely but not impossible events. As a well-diversified business underpinned by historically stable revenue generation and significant capital strength, HSBC is well equipped to manage the risks and uncertainty inherent in today’s world.

|

HSBC Holdings plc

|

5

|

|

Transparency and disclosure

Last year, we published a range of environmental, social and governance (‘ESG’) metrics to enable investors and customers to assess our non-financial performance. The data we disclose will continue to evolve as we learn more about what our stakeholders find useful and improve our ability to collect the necessary information. We will publish our next ESG Update on our website in April 2018.

We are also making our first disclosure under the terms of the Financial Stability Board’s Task Force on Climate-related Financial Disclosures. This can be found on page 27. As one of the world’s largest international banks, we take seriously our responsibility to help develop a voluntary, consistent and comparable system of climate-related financial disclosure. We intend to continue to expand and improve the quality and specificity of these disclosures, and to encourage all those who work with us to do the same.

Supporting our people

It is important not just to achieve good results, but to do so in a way that treats all of our stakeholders – employees, customers, regulators and shareholders – in a fair and transparent way. We are committed to holding ourselves to account in meeting that aim, and to being accountable to our stakeholders for our actions.

As part of this commitment, the Board and I are determined to ensure that HSBC remains a place where all our people have the opportunity to fulfil their potential in a nurturing environment that encourages the right behaviour. Our stakeholders expect honesty and integrity and we will continue to promote a culture in which people do the right thing.

My special thanks are due on behalf of the Board to each of the 229,000 people who work for HSBC around the world. In my short time as Group Chairman I have been enormously impressed by the effort, energies and ability of our people in each country I have visited. These results are a testament to their hard work and dedication.

Mark E Tucker

Group Chairman

20 February 2018

|

6

|

HSBC Holdings plc

|

Group Chief Executive’s Review

HSBC is simpler, stronger and more secure than it was in 2011, and better able to connect customers to opportunities in the world’s fastest growing regions.

2017 was an important year for HSBC. We completed the transformation programme that we started in 2015, maximising the benefits of our network and increasing our competitive advantages. By the end of the year we had exceeded our risk-weighted asset and cost-saving targets, rebuilt our Mexico business, delivered revenue growth from our international network in excess of global economic growth, and accelerated investment in our operations in Asia. We also opened new businesses and launched products that considerably strengthen the service that we offer our international clients.

These achievements, and the work that preceded them, were a critical factor in delivering a strong financial performance in 2017. The strength of our three main global businesses generated significant increases in both reported and adjusted Group profit before tax (‘PBT’), while reported PBT also benefited from the non-recurrence of a number of large significant items from 2016. Adjusted PBT and adjusted revenue were up in four out of five regions. We grew adjusted revenue faster than adjusted costs, and continued to increase our market share in strategic product areas.

Business performance

Retail Banking and Wealth Management had an excellent 2017, with strong adjusted revenue increases across a number of business lines. In Retail Banking, interest rate rises helped to grow revenue as our robust balance sheet and capital strength continued to attract deposits, particularly in Hong Kong. We continued to grow lending in our target markets, especially Hong Kong, the UK and Mexico. Wealth Management benefited from improving customer investment appetite, strong product sales across all categories and the impact of market movements on our life insurance manufacturing businesses.

Commercial Banking adjusted revenue grew well on the back of an outstanding performance in Global Liquidity and Cash Management. Higher lending volumes helped Credit and Lending overcome the impact of narrower spreads. Global Trade and Receivables Finance revenue stabilised after a difficult 2016 and we increased our share of major markets, including trade finance in Hong Kong and receivables finance in the UK. HSBC was voted market leader for trade finance in

Euromoney’s

annual trade finance survey in January 2018.

Global Banking and Markets grew adjusted revenue, driven particularly by strong growth in Global Liquidity and Cash Management, and Securities Services. Growth in the first three quarters of the year in Markets and Banking enabled both to withstand the effects of subdued market activity in the fourth quarter.

Global Private Banking adjusted revenue reflected the impact of historical repositioning, but was stable over the course of 2017. The business grew adjusted revenue by 10% in its target markets.

Our strong revenue generation meant that the Group achieved positive adjusted jaws in 2017. We accelerated investment to grow the business, particularly in Retail Banking and Wealth Management, which contributed to an increase in adjusted costs. Performance-related compensation also grew in line with profit before tax.

|

HSBC Holdings plc

|

7

|

|

Adjusted loan impairment charges were significantly lower than 2016, mainly due to improved conditions in the oil and gas industry in North America.

Our strong common equity tier one ratio of 14.5% included the effect of recent changes in US tax legislation, which reduced our capital position by 9 basis points. It also included the impact of our most recent $2bn share buy-back. In 2017, we returned a total of $3bn to shareholders through share buy-backs and paid more in dividends than any other European or American bank. We achieved this while maintaining one of the strongest capital ratios in the industry.

Strategic actions

The strength of our business is due in large part to the strategic actions that we first announced in June 2015. This programme concluded at the end of 2017 with eight out of ten actions completed on time and on target (see page

12

).

HSBC is much more capital efficient and capable of producing stronger returns for investors as a consequence of these actions. Our cost-reduction programmes have enabled us to absorb the cost of growing the business and protecting HSBC from financial crime, while improving the efficiency and security of our processes.

Our previously underperforming Mexico business is increasingly profitable and well positioned for further growth. Whilst our US business remains a work in progress, it is a valuable source of business for other regions and continues to make important progress. We also completed the run-off of our legacy US consumer and mortgage lending portfolio, bringing an end to a difficult chapter in HSBC’s recent history.

Our international network is now much better able to connect customers to opportunities and delivering revenue growth above that of the global economy. 53% of client revenue now comes from international clients, up from 50% in 2015. Global Liquidity and Cash Management in particular is now a major component of the bank’s success, and Global Trade and Receivables Finance has extended its leadership of the global trade finance market.

The Group’s business mix is more oriented towards Asia, improving our ability to channel the economic and social changes taking place within the world’s fastest growing region. Asia contributes a larger proportion of the Group’s profits than in 2015, reflecting regional investment in growing our loan book, building our insurance and asset management businesses, and connecting customers to opportunities within the region.

We continued to expand our presence in mainland China with the launch of new retail banking products and increased lending in the Pearl River Delta. In December we launched HSBC Qianhai Securities, the first securities joint venture in mainland China to be

majority-owned by an international bank. This allows us to offer our clients increased access to China’s rapidly expanding capital markets and provides an unprecedented opportunity to establish and grow a securities business in mainland China with strong international standards. This underlines our status as the leading international bank in mainland China.

We won a number of significant new business mandates related to the China-led Belt and Road Initiative in 2017, and opened new China desks in Poland, Luxembourg, Thailand and Macau to capture further opportunities. We now have a total of 24 China desks aimed at supporting Chinese businesses with global outbound ambitions, 20 of which are along the ‘Belt and Road’ routes. In November we were named ‘Best Bank for Belt and Road’ at the

FinanceAsia

Achievement Awards 2017.

|

8

|

HSBC Holdings plc

|

Fighting financial crime

For the past five years, we have been weaving Global Standards into the fabric of HSBC. The investment that we have made in our financial crime risk management capabilities has considerably strengthened our ability to protect the integrity of the financial system. We have assembled a highly expert team which is helping to shape the debate about our industry’s role in the fight against financial crime. We have made great strides in building a compliance function fit for the many evolving challenges we face, and built partnerships to combat financial crime with regulatory and law enforcement authorities around the world.

The expiration in December of the five-year deferred prosecution agreement that we entered into with the US Department of Justice in 2012 (‘AML DPA’) was an important milestone for HSBC. Nevertheless, exiting the AML DPA was a product rather than the focus of the essential work that we have done to transform our compliance capabilities and protect the financial system. This work will continue as we seek to ensure that the changes we have made are effective and sustainable. Combating financial crime is a never-ending exercise and will be a constant focus for the Group’s management.

Thank you

As I prepare to pass on the stewardship of HSBC to my successor, I am proud of our achievements of the last seven and a half years. After the most extensive transformation programme in HSBC’s 153 year history, HSBC is simpler, stronger and more secure than it was in 2011, and better able to connect customers to opportunities in the world’s fastest growing regions. We have also delivered excellent value to shareholders through a higher share price, $64.7bn in declared dividends and $5.5bn in share buy-backs, representing a total shareholder return of 70.3% from 2011 to the end of 2017.

I am pleased to be handing over to such a capable successor as John Flint, whose intimate knowledge of HSBC and its culture will be a considerable asset to the bank and its clients. I am grateful to my colleagues on the Group Management Board for their support since 2011, and to Douglas Flint and Mark Tucker for their backing.

Finally, my sincere thanks go to all of my HSBC colleagues around the world, past and present, whose hard work and commitment are the foundation of the bank’s success. It has been my privilege to work with them for the last 38 years.

Stuart Gulliver

Group Chief Executive

20 February 2018

|

HSBC Holdings plc

|

9

|

|

Our strategy

We have developed a long-term strategy that reflects our purpose and enables us to capture value from our international network.

Two-pronged long-term strategy

Develop our international network

To serve enterprises across geographies and facilitate international trade and capital flows, thereby helping our clients to grow their business.

Invest in wealth and retail businesses with local scale

To make the most of global social mobility, wealth creation and long-term demographic changes in our select retail banking and wealth management markets.

Value of the network and our strategy

Access to global growth opportunities

Our unparalleled network covers countries accounting for approximately 90% of global GDP, trade and capital flows. We have a leading presence in large and fast-growing economies.

Our network covers all of the world’s 30 largest trade corridors forecast for 2030. These top 30 corridors are expected to have a compound annual growth rate well in excess of GDP growth expectations from 2016 to 2030.

Lower risk profile and volatility from our geographically diversified universal banking model

We operate a balanced universal banking model across both wholesale and retail businesses and we are geographically diversified. This has resulted in a lower risk profile and lower earnings volatility compared to our global peers. Our business model has remained resilient through business cycles, and it helps ensure stable funding and liquidity.

Strong capital and funding base

CET1 ratio of

14.5

% supported by increased shareholders’ equity to meet new regulatory requirements since the end of 2010.

Four interconnected, global businesses share balance sheets and liquidity in addition to strong commercial links.

Stable shareholder returns

Industry leading dividend – approximately $65bn declared from 2011 to 2017 – as well as circa $5.5bn of share repurchases.

|

10

|

HSBC Holdings plc

|

Long-term trends

Our strategy positions us to capitalise on several long-term trends.

Increasing connectivity and global flows of trade, finance and data are key drivers of GDP growth.

Source: Global Insight’s Comparative World Overview.

Emerging market economies are expected to be twice the size of developed economies by 2050.

Source: United Nations Conference on Trade and Development.

The middle class is expected to grow by over two billion people from 2017 to 2030, driven by growth in Asia’s middle class.

Source: Global Economy and Development at Brookings, The Unprecedented Expansion of the Middle Class (2017).

Climate change is accelerating and global temperatures are trending significantly higher. Investment in renewable energy capacity will be needed to limit the global temperature increase to 2°C.

|

Required by 2050 as per IEA 66% 2°C scenario

|

|

|

Current (2016)

|

|

Source: OECD, Investing in Climate, Investing in Growth (2017).

*

The scenario assumes a 66% probability of keeping the mean global surface temperature rise throughout the 21st century to below 2°C above pre-industrialised levels.

Client examples

Trina Solar (‘Trina’): China, renewable energy

Exporter of solar panels globally. Trina’s aim is to bring China’s green energy solutions to countries along the Belt and Road Initiative route, and has thus stepped up its overseas investment, particularly in the ASEAN region. HSBC created a digital platform for Trina that gave its headquarters a transparent view of its ASEAN-region subsidiaries’ cash positions and set up a cash pool in Singapore to seamlessly connect Trina’s HSBC accounts globally.

Reckitt Benckiser (‘RB’): UK, consumer goods

Global consumer health and hygiene company. HSBC acted as financial adviser and lead financier to Reckitt Benckiser on its $18bn acquisition of Mead Johnson Nutrition Company, a leader in infant and children’s nutrition. This acquisition marked one of the largest UK into US transactions and considerably strengthened RB’s presence in developing markets, particularly China.

Zhejiang Geely: China, automotive

Leading automobile manufacturer. HSBC served as sole financial adviser for Zhejiang Geely on two interlinked China outbound investments, one in Malaysian carmaker Proton Holdings and the second in Lotus Advance Technologies, a subsidiary of Proton based in the UK. These transactions were enabled by collaboration between HSBC teams in mainland China, Hong Kong, Singapore, Malaysia and London.

Morgan McKinley: Ireland, professional services

Global recruitment agency with operations in Ireland, UK, EMEA and APAC. In 2017, Morgan McKinley expanded HSBC’s global mandate to include cross-border Global Trade and Receivables Finance (‘GTRF’) facilities and Global Liquidity and Cash Management (‘GLCM’) services in Canada and Japan. HSBC’s ‘one-team’ approach, not separated by product, was cited by the client as being a key driver in the decision to switch to HSBC.

|

HSBC Holdings plc

|

11

|

|

Strategic actions

We met eight out of ten targets from the strategic actions outlined in our Investor Update in June 2015.

Capturing value from our international network

In June 2015, we outlined a series of strategic actions to make the most of our competitive advantages and respond to a changing environment.

These actions focused on using our resources more efficiently and on investing for growth. Each action had targets defined to the end of 2017. The table opposite contains a summary of our progress with additional details provided below.

Resizing and simplifying our business

We passed several significant milestones in resizing and simplifying our business in 2017. Our management actions delivered a gross reduction of risk-weighted assets (‘RWAs’) by $338bn, exceeding our RWA reduction target from management initiatives by $60bn on an FX-adjusted basis.

Among our NAFTA region Investor Update targets, we did not reach our US profit before tax (‘PBT’) target of $2bn. However, we have taken steps forward in, for example, our US Retail Banking and Wealth Management (‘RBWM’) business, where we increased PBT, revenues and deposits, and migrated over one million customers to our impending new core banking platform. We also completed the wind-down of our US consumer and mortgage lending (‘CML’) run-off portfolio. In Mexico, our adjusted PBT reached $440m, surpassing our Investor Update target on a local currency basis. We also grew adjusted revenue in Mexico by 11% compared with 2016, supported by increased loan balances from market share gains.

We remain on course to complete the set-up of our UK ring-fenced bank (‘RFB’) ahead of the 1 January 2019 statutory deadline. In 2017, we received a restricted bank licence for the RFB and are working through an agreed mobilisation plan with the Prudential Regulatory Authority and Financial Conduct Authority to receive an unrestricted licence in 2018.

We successfully concluded our cost-saving programme and realised $6.1bn of annual run-rate savings, over $1bn more than our Investor Update target. The programme enabled 2017 exit run-rate adjusted costs to be kept flat compared with the 2014 cost base. The savings offset increased costs from areas such as regulatory programmes and compliance, and investments to help facilitate further business growth. For example, in RBWM, we expanded the use of biometrics globally with over 1.5 million customers using voice recognition, and with fingerprint technology launched in nine of our markets. For our corporate customers, we improved our key digital channels with significant improvements to HSBCnet and HSBC Connect. Our costs-to-achieve transformation concluded with approximately $7bn spent since the start of the programme.

Redeploying capital to grow our business

Our international network remains core to our strategy, and we achieved our Investor Update target of revenue growth above GDP. In 2017, we grew our revenue from transaction banking products by 6%, including double-digit percentage growth in GLCM and HSBC Security Services (‘HSS’). We grew GTRF market share in key markets, in particular Hong Kong and receivables finance in the UK. Cross-border revenues from our priority corridors grew 10%, with double-digit percentage growth in four of our five largest priority corridors including our China-US corridor. We were named ‘Top Global Trade Finance Bank’ by our clients in the

Euromoney

Trade Finance Survey 2018.

We delivered on our 2015 Investor Update commitment to prioritise and accelerate investments in Asia. In 2017, we grew our loan portfolio in the region by $53bn to $426bn. Our asset management and insurance businesses in Asia realised 17% and 8% growth in AUM and annualised new business premiums, respectively. In mainland China, we reached over 400,000 cards in circulation since launching credit cards at the end of 2016, and we grew our customer loans in the Pearl River Delta region by 23%. We launched HSBC Qianhai Securities, the first securities joint venture in mainland China to be majority-owned by an international bank.

Revenue tied to renminbi (‘RMB’) internationalisation in 2017 of $1.2bn did not meet our Investor Update target of $2.0bn to $2.5bn. This was largely due to a decrease in overall market volumes. However, we continue to be recognised as the leading bank for international RMB products and services. We ranked first in

Bloomberg

’s offshore RMB bond underwriting league table in 2017 with 28% market share and first for the sixth year in a row in the

Asiamoney

Offshore RMB Poll 2017. We had the largest share, at 53%, of approved quota of RMB Qualified Foreign Institutional Investor (‘RQFII’) custodian business.

Selected awards and recognition

Euromoney Trade Finance Survey 2018

Top Global Trade Finance Bank

Euromoney Awards for Excellence 2017

World’s Best Bank

World’s Best Investment Bank in the Emerging Markets

Asia’s Best Bank

North America’s Best Bank for Transaction Services

Euromoney Cash Management Survey 2017

Best Global Cash Manager for Corporates

Best Global Cash Manager for Financial Institutions for all Transactions

Asiamoney New Silk Road Finance Awards 2017

Best Overall International Bank for Belt and Road Initiative

|

12

|

HSBC Holdings plc

|

This page is intentionally left blank

|

HSBC Holdings plc

|

13

|

|

Financial overview

Reported results

|

Reported results

|

2017

$m

|

|

2016

$m

|

|

2015

$m

|

|

|

Net interest income

|

28,176

|

|

29,813

|

|

32,531

|

|

|

Net fee income

|

12,811

|

|

12,777

|

|

14,705

|

|

|

Net trading income

|

7,719

|

|

9,452

|

|

8,723

|

|

|

Other income

|

2,739

|

|

(4,076

|

)

|

3,841

|

|

|

Net operating income before loan impairment charges and other credit risk provisions (‘revenue’)

|

51,445

|

|

47,966

|

|

59,800

|

|

|

Loan impairment charges and other credit risk provisions

|

(1,769

|

)

|

(3,400

|

)

|

(3,721

|

)

|

|

Net operating income

|

49,676

|

|

44,566

|

|

56,079

|

|

|

Total operating expenses

|

(34,884

|

)

|

(39,808

|

)

|

(39,768

|

)

|

|

Operating profit

|

14,792

|

|

4,758

|

|

16,311

|

|

|

Share of profit in associates and joint ventures

|

2,375

|

|

2,354

|

|

2,556

|

|

|

Profit before tax

|

17,167

|

|

7,112

|

|

18,867

|

|

This table shows our reported results for the last three years, ended 31 December 2017, 2016 and 2015.

All commentary in this financial overview compares the 2017 results with 2016, unless otherwise stated.

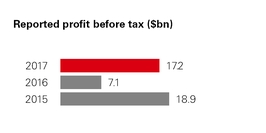

Reported profit before tax

Reported profit before tax of

$17.2bn

was

$10.1bn

or

141%

higher, mainly reflecting a net favourable movement of significant items of

$8.5bn

, which is described in more detail on page

32

. Excluding significant items and an adverse effect of foreign currency translation of

$0.5bn

, profit before tax increased by

$2.1bn

or

11%

.

Reported revenue

Reported revenue of

$51.4bn

was

$3.5bn

or

7%

higher, partly reflecting a net favourable movement in significant items of

$2.0bn

, which included:

|

–

|

in 2016, unfavourable fair value movements on our own debt designated at fair value reflecting changes in our own credit spread of

$1.8bn

, which are now reported in other comprehensive income, following our partial early adoption of IFRS 9 ‘Financial Instruments’ on 1 January 2017; and

|

|

–

|

favourable fair value movements in 2017 of

$0.1bn

on non-qualifying hedges, compared with adverse movements of

$0.7bn

in 2016.

|

Net favourable movements were partly offset by:

|

–

|

in 2016, a

$0.7bn

gain on the disposal of our membership interests in Visa Europe and Visa Inc. This compared with a

$0.3bn

gain on the disposal of our shares in Visa Inc. during 2017;

|

|

–

|

adverse debit value adjustments on derivative contracts in 2017 of

$0.4bn

, compared with minimal movements in 2016; and

|

|

–

|

in 2017, a

$0.1bn

provision related to customer redress programmes in the UK, and a $0.1bn charge arising from the opportunity to increase our investment in new businesses.

|

Significant items also included a loss of $1.7bn recognised in 2016 on the sale of operations in Brazil to Banco Bradesco S.A., which was completed on 1 July 2016. This loss was substantially offset by the reported revenue earned by the Brazil business during 2016 of $1.5bn.

Excluding significant items, and an adverse effect of foreign currency translation of

$0.7bn

, revenue increased by

$2.2bn

or

5%

, reflecting growth in Retail Banking and Wealth Management (‘RBWM’), Commercial Banking (‘CMB’) and Global Banking and Markets (‘GB&M’).

Reported LICs

Reported loan impairment charges and other credit risk provisions (‘LICs’) of

$1.8bn

were

$1.6bn

lower, in part reflecting the effect of significant items, which comprised the LICs incurred by our operations in Brazil in 2016 of

$0.7bn

.

Excluding significant items and the adverse effect of foreign currency translation of

$0.1bn

, LICs decreased by

$0.8bn

or

32%

. The reduction in LICs was primarily in CMB, RBWM and Corporate Centre.

Reported operating expenses

Reported operating expenses of

$34.9bn

were

$4.9bn

or

12%

lower. This included a net decrease in significant items of

$5.6bn

, including:

|

–

|

a

$3.2bn

write-off of goodwill in our GPB business in Europe in 2016;

|

|

–

|

a net release of

$0.4bn

in settlements and provisions in connection with legal matters, compared with charges in 2016 of

$0.7bn

;

|

|

–

|

operating expenses of

$1.1bn

in 1H16 incurred by the operations in Brazil that we sold; and

|

|

–

|

costs to achieve of

$3.0bn

, compared with

$3.1bn

in 2016.

|

Excluding significant items and a favourable effect of foreign currency translation of

$0.3bn

, operating expenses increased by

$1.1bn

. This increase mainly reflected increased investment in growth programmes, primarily in RBWM, where investments were partly funded by the proceeds from our disposal of Visa shares, and higher performance-related pay.

|

14

|

HSBC Holdings plc

|

Reported income from associates and joint ventures

Reported income from associates and joint ventures of

$2.4bn

increased by

$21m

.

Dividends

On 20 February 2018, the Board announced a fourth interim dividend of $0.21 per ordinary share.

Adjusted performance

Our reported results are prepared in accordance with IFRSs as detailed in the Financial Statements on page

222

.

We present adjusted performance measures to align internal and external reporting, identify and quantify items management believes to be significant, and provide insight into how management assesses period-on-period performance. Adjusted performance measures are highlighted with the following symbol:

<

>

To derive adjusted performance, we adjust for:

|

–

|

the year-on-year effects of foreign currency translation differences; and

|

|

–

|

the effect of significant items that distort year-on-year comparisons and are excluded in order to improve understanding of the underlying trends in the business.

|

Ñ

For reconciliations of our reported results to an adjusted basis, including lists of significant items, see page

66

.

Adjusted results

<

>

This table shows our adjusted results for 2017 and 2016. These are discussed in more detail on the following pages.

|

Adjusted results

<

>

|

2017

$m

|

|

2016

$m

|

|

(%)

|

|

|

Net operating income before loan impairment charges and other credit risk provisions (adjusted revenue)

|

51,524

|

|

49,290

|

|

5

|

%

|

|

Loan impairment charges and other credit risk provisions

|

(1,769

|

)

|

(2,594

|

)

|

32

|

%

|

|

Total operating expenses

|

(31,140

|

)

|

(30,084

|

)

|

(4

|

)%

|

|

Operating profit

|

18,615

|

|

16,612

|

|

12

|

%

|

|

Share of profit in associates and joint ventures

|

2,375

|

|

2,322

|

|

2

|

%

|

|

Profit before tax

|

20,990

|

|

18,934

|

|

11

|

%

|

Adjusted profit before tax

<

>

On an adjusted basis, profit before tax of

$21.0bn

was

$2.1bn

or

11%

higher. This was driven by higher revenue (up

$2.2bn

), with growth in our three main global businesses, and a significant reduction in LICs (down

$0.8bn

), notably as 2016 included charges relating to exposures to the oil and gas, and mining sectors. These movements were partly offset by higher operating expenses (up

$1.1bn

), in part due to investment in growth initiatives. In 2017, we achieved positive adjusted jaws of

1.0%

.

|

HSBC Holdings plc

|

15

|

|

Adjusted revenue

<

>

Adjusted revenue of

$51.5bn

was

$2.2bn

or

5%

higher, as growth in our three main global businesses was partly offset by reductions in GPB and Corporate Centre.

|

–

|

In RBWM, revenue increased by

$1.7bn

or

9%

, driven by growth in Retail Banking from current accounts, savings and deposits, reflecting balance growth and wider spreads primarily in Hong Kong, and also in the US and Mexico, partly offset by lower personal lending revenue. Revenue also increased in Wealth Management, mainly in insurance manufacturing driven by favourable market impacts compared with adverse market impacts in 2016, notably in Asia. In addition, investment distribution income increased, reflecting increased investor confidence in Hong Kong.

|

|

–

|

In CMB, revenue increased by

$0.6bn

or

5%

, driven by growth in Global Liquidity and Cash Management (‘GLCM’), notably in Asia. This primarily reflected wider spreads and increased average deposit balances. Revenue in Credit and Lending (‘C&L’)

|

increased as we grew lending balances in key markets, while revenue in Global Trade and Receivables Finance (‘GTRF’) fell marginally, due to managed client exits in MENA despite balance sheet growth in Asia and the UK.

|

–

|

In GB&M, revenue increased by

$0.4bn

or

3%

, mainly in GLCM and Securities Services. In Global Markets, revenue was marginally higher as growth in Equities, reflecting increased market share in Prime Financing, was partly offset by lower revenue in Fixed Income, Currencies and Commodities that reflected lower market volatility, as well as a net adverse movement on credit and funding valuations adjustments.

|

These increases were partly offset:

|

–

|

In GPB, revenue was

$45m

or

3%

lower, reflecting the impact of our customer repositioning actions. This was partly offset by increased revenue in the markets that we have targeted for growth, notably Hong Kong, due to higher investment revenue reflecting increased client activity and growth in deposit revenue as we benefited from wider spreads.

|

|

–

|

In Corporate Centre, revenue decreased by

$0.4bn

, with reductions in the US run-off portfolio (down

$0.7bn

), following the disposal of the remaining portfolio during 2017, and in Central Treasury (down

$0.1bn

). These decreases were partly offset in other income (up

$0.4

bn), which included revaluation gains on investment properties.

|

Movement in adjusted revenue compared with 2016

<

>

|

2017

$m

|

|

2016

$m

|

|

Variance

$m

|

|

%

|

|

|

|

Retail Banking and Wealth Management

|

20,287

|

|

18,542

|

|

1,745

|

|

9

|

%

|

|

Commercial Banking

|

13,223

|

|

12,619

|

|

604

|

|

5

|

%

|

|

Global Banking and Markets

|

15,091

|

|

14,715

|

|

376

|

|

3

|

%

|

|

Global Private Banking

|

1,703

|

|

1,748

|

|

(45

|

)

|

(3

|

)%

|

|

Corporate Centre

|

1,220

|

|

1,666

|

|

(446

|

)

|

(27

|

)%

|

|

Total

|

51,524

|

|

49,290

|

|

2,234

|

|

5

|

%

|

Adjusted LICs

<

>

Adjusted LICs of

$1.8bn

were

$0.8bn

lower, reflecting reductions in:

|

–

|

CMB (

$0.5bn

lower), notably in the UK and North America, primarily as 2016 included charges against exposures in the oil and gas sector. In addition, there were reductions in France, Spain and Singapore as we incurred individually assessed LICs against a small number of corporate exposures in 2016.

|

|

–

|

RBWM (

$0.2bn

lower), primarily in Turkey and the US, reflecting improved credit quality, partly offset by increases in Mexico, notably from growth in unsecured lending which resulted in an associated increase in delinquency rates.

|

|

–

|

LICs in GB&M of

$0.5bn

were broadly unchanged from the prior year. LICs in the current year related to two large corporate exposures in Europe. This compared with a small number of individually assessed LICs, notably on exposures in the oil and gas, and mining sectors in the US in 2016.

|

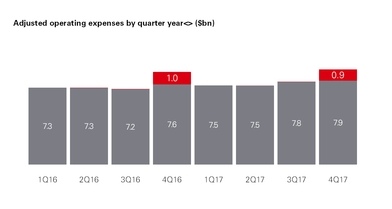

Adjusted operating expenses

<

>

Adjusted operating expenses of

$31.1bn

were

$1.1bn

or

4%

higher. This reflected investments in business growth programmes ($0.6bn), primarily in RBWM where investments were partly funded by the proceeds from the disposal of our shares in Visa, as well as an increase in performance-related pay (up

$0.4bn

). Compared with 2016, our UK bank levy charge was broadly unchanged, at $916m. The impact of our cost-saving initiatives broadly offset inflation and continued investment in our regulatory programmes and compliance.

Our total investment in regulatory programmes and compliance was $3.0bn, up $0.2bn or 7%. This notably reflected the continued implementation of our Global Standards programme to enhance financial crime risk controls and capabilities.

The number of employees expressed in full-time equivalent staff at 31 December 2017 was 228,687, a decrease of 6,488 from 31 December 2016. This reflected reductions resulting from our transformation programmes and the completion of these programmes, partly offset by increases from our investments in Global Standards and in our business growth programmes.

Adjusted income from associates and joint ventures

<

>

Adjusted income from associates and joint ventures of

$2.4bn

increased by

$0.1bn

.

|

UK bank levy

|

Adjusted operating expenses (excluding bank levy)

|

||

2016:

$30.1bn

2017:

$31.1bn

|

16

|

HSBC Holdings plc

|

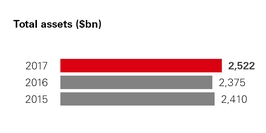

Balance sheet strength

Total reported assets were $

2.5tn

, 6% higher than at 31 December 2016 on a reported basis, and 1% higher on a constant currency basis. We have maintained the strength of our balance sheet, as we continued our targeted asset growth, notably in Asia.

Distributable reserves

The distributable reserves of HSBC Holdings at 31 December 2017 were $38bn, compared with $42bn at 31 December 2016. The decrease was driven by distributions to shareholders of $8.3bn, which were higher than profits generated of $5.5bn, as well as fair value losses net of tax due to movements in our own credit risk of $0.8bn.

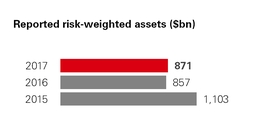

Capital strength

We manage our capital in an effort to ensure we exceed current regulatory requirements and are well placed to meet those expected in the future. We monitor our position using capital ratios. These measure capital relative to a regulatory assessment of risks taken. We quantify how these risks relate to our businesses using RWAs.

Ñ

Details of these risks are included on page

162

.

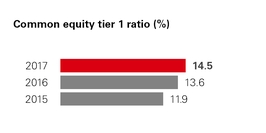

Our CET1 ratio at 31 December 2017 was

14.5%

,

up

from 13.6% at 31 December 2016.

Implementation of IFRS 9

IFRS 9 ‘Financial Instruments’ was adopted on 1 January 2018. The adoption of IFRS 9 will reduce the Group’s net assets at 1 January 2018 by $1.0bn. We do not expect this to have a significant impact on our regulatory capital position.

Ñ

Further explanation of the expected impact of the implementation of IFRS 9 is provided in Note 1 on the Financial Statements on page

222

.

Delivery against Group financial targets

Return on equity

Our medium-term target is to achieve a return on equity (‘RoE’) of more than 10%. In 2017, we achieved an RoE of 5.9% compared with 0.8% in 2016. In 2016, significant items, which included a write-off of goodwill in GPB in Europe, costs to achieve and adverse fair value movements arising from changes in credit spread on our own debt designated at fair value, had a significant effect on our reported RoE.

Adjusted jaws

<

>

|

Adjusted revenue up

|

|

||

|

5

|

%

|

Adjusted jaws

|

|

|

1

|

%

|

||

|

Adjusted costs up

|

|

||

|

4

|

%

|

||

Jaws measures the difference between the rates of change for revenue and costs. Positive jaws occurs when the figure for the annual percentage change in revenue is higher than, or less negative than, the corresponding rate for costs.

We calculate adjusted jaws using adjusted revenue and costs. Our target is to maintain positive adjusted jaws.

In 2017, adjusted revenue increased by

5%

and our adjusted operating expenses increased by

4%

. Adjusted jaws was therefore positive

1%

.

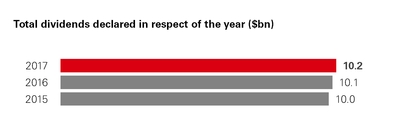

Dividends

In the current uncertain environment, we plan to sustain the annual dividend in respect of the year at its current level for the foreseeable future. Growing our dividend will depend on the overall profitability of the Group, delivering further release of less efficiently deployed capital and meeting regulatory capital requirements in a timely manner. Actions to address these points were core elements of our Investor Update in June 2015.

|

HSBC Holdings plc

|

17

|

|

Global businesses

We manage our products and services globally through our global businesses.

The ‘Management view of adjusted revenue’ tables provide a breakdown of revenue by major products, and reflect the basis on which each business is assessed and managed.

Ñ

The comparative period has been restated to reflect changes to reportable segments, as described on page

64

.

Commentary is on an adjusted basis, which is consistent with how we assess the performance of our global businesses.

<

>

Retail Banking and Wealth Management (‘RBWM’)

RBWM serves close to

37 million

customers worldwide through four main businesses: Retail Banking, Wealth Management, Asset Management and Insurance. Our HSBC Premier and Advance propositions are aimed at mass affluent and emerging affluent customers who value international connectivity and benefit from our global reach and scale. For customers with simpler banking needs, RBWM offers a full range of products and services reflecting local requirements.

Key events

|

–

|

Significant investment in digital transformation across our

six

core markets, reshaping the branch network and sales force, and improving customer engagement, including the launch of a payment app in Hong Kong (PayMe) and voice biometrics in the UK.

|

|

–

|

Continued to attract customer deposits (up

5%

), providing the potential to benefit from future interest rate rises; lending balances increased by

7%

.

|

|

–

|

Strong growth in sales of investment products, notably equities (up

45%

) and mutual funds (up

22%

), and growth in insurance annualised new business premiums (up

7%

), primarily in Asia.

|

Financial performance

Adjusted profit before tax of

$6.5bn

was

$1.2bn

or

24%

higher, reflecting strong revenue growth from deposits and Wealth Management, as well as lower LICs, partly offset by higher operating expenses. We achieved positive adjusted jaws of

4.0%

.

Adjusted revenue of

$20.3bn

was

$1.7bn

or

9%

higher, reflecting:

Higher revenue in Retail Banking (up

$0.8bn

or

6%

):

|

–

|

Growth in revenue from current accounts, savings and deposits (up

$1.1bn

) due to wider spreads and higher balances primarily in Hong Kong, and also in the US and Mexico.

|

This was partly offset by:

|

–

|

Lower personal lending revenue (down

$0.3bn

), reflecting mortgage spread compression, primarily in Hong Kong, mainland China and the US. This was partly offset by lending growth of

$22.2bn

, notably driven by mortgages in the UK and Hong Kong, where we grew our market share.

|

Higher revenue in Wealth Management (up

$0.9bn

or

18%

):

|

–

|

Growth in life insurance manufacturing revenue (up

$0.5bn

) including favourable movements in market impacts of

$0.3bn

in 2017 compared with adverse movements of

$0.4bn

in 2016, due to interest rate and equity market movements, notably in Asia and France, and to a lesser extent higher insurance sales in Asia.

|

|

–

|

Higher investment distribution revenue (up

$0.4bn

), primarily from higher sales of mutual funds and retail securities in Hong Kong, reflecting increased investor confidence.

|

Adjusted LICs of

$1.0bn

were

$0.2bn

or

14%

lower, reflecting reductions in Turkey of

$85m

and in the US of

$44m

, as credit quality improved. This was partly offset in Mexico where higher LICs (

$24m

) reflected targeted growth in unsecured lending and associated higher delinquency rates. In the UK LICs of

$132m

were marginally higher, but remained at very low levels (

10

bps of the portfolio) as higher LICs relating to mortgages and unsecured lending were partly offset by a release from the sale of a loan portfolio.

Adjusted operating expenses of

$12.8bn

were

$0.7bn

or

5%

higher, mainly due to investment in growth initiatives, notably in retail business banking, in our international proposition as we introduced new products and services, and in mainland China. Transformational and other cost savings partly offset inflation and higher performance-related pay.

|

2017 vs 2016

|

|||||||||||

|

Management view of adjusted revenue

<

>

|

Footnotes

|

2017

$m

|

|

2016

$m

|

|

2015

$m

|

|

$m

|

|

%

|

|

|

Net operating income

|

3

|

||||||||||

|

Retail Banking

|

13,495

|

|

12,695

|

|

12,508

|

|

800

|

|

6

|

%

|

|

|

– c

urrent accounts, savings and deposits

|

6,344

|

|

5,213

|

|

4,814

|

|

1,131

|

|

22

|

%

|

|

|

–

personal lending

|

7,151

|

|

7,482

|

|

7,694

|

|

(331

|

)

|

(4

|

)%

|

|

|

mortgages

|

2,337

|

|

2,546

|

|

2,648

|

|

(209

|

)

|

(8

|

)%

|

|

|

credit cards

|

2,899

|

|

3,034

|

|

3,218

|

|

(135

|

)

|

(4

|

)%

|

|

|

other personal lending

|

4

|

1,915

|

|

1,902

|

|

1,828

|

|

13

|

|

1

|

%

|

|

Wealth Management

|

6,224

|

|

5,292

|

|

5,748

|

|

932

|

|

18

|

%

|

|

|

– investment distribution

|

5

|

3,276

|

|

2,904

|

|

3,230

|

|

372

|

|

13

|

%

|

|

– life insurance manufacturing

|

1,893

|

|

1,401

|

|

1,544

|

|

492

|

|

35

|

%

|

|

|

– asset management

|

1,055

|

|

987

|

|

974

|

|

68

|

|

7

|

%

|

|

|

Other

|

6

|

568

|

|

555

|

|

582

|

|

13

|

|

2

|

%

|

|

Year ended 31 Dec

|

20,287

|

|

18,542

|

|

18,838

|

|

1,745

|

|

9

|

%

|

|

|

Adjusted RoRWA (%)

|

7

|

5.5

|

|

4.6

|

|

4.8

|

|

||||

Ñ

For footnotes, see page

85

.

Change in adjusted profit before tax

+24%

|

18

|

HSBC Holdings plc

|

Commercial Banking (‘CMB’)

CMB serves approximately

1.7 million

customers in

53

countries and territories. Our customers range from small enterprises focused primarily on their domestic markets to corporates operating globally. We support customers with tailored financial products and services to allow them to operate efficiently and grow.

Services provided include working capital, term loans, payment services and international trade facilitation, as well as expertise in mergers and acquisitions, and access to financial markets.

Key events

|

–

|

Corporate customer value from our international subsidiary banking proposition grew

19%

*