|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Table of Contents

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 10-K

| x |

ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the fiscal year ended December 31, 2010

OR

| ¨ |

TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the transition period from to

Commission file number 000-22418

ITRON, INC.

(Exact name of registrant as specified in its charter)

| Washington | 91-1011792 | |

| (State of Incorporation) | (I.R.S. Employer Identification Number) |

2111 N Molter Road, Liberty Lake, Washington 99019

(509) 924-9900

(Address and telephone number of registrant’s principal executive offices)

Securities registered pursuant to Section 12(b) of the Act:

|

Title of each class |

Name of each exchange on which registered |

|

| Common stock, no par value | NASDAQ Global Select Market | |

| Preferred share purchase rights | NASDAQ Global Select Market |

Securities registered pursuant to Section 12(g) of the Act: None

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. Yes x No ¨

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Act. Yes ¨ No x

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes x No ¨

Indicate by check mark whether the registrant has submitted electronically and posted on its corporate Web site, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T (§ 232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files). Yes x No ¨

Indicate by check mark if disclosure of delinquent filers pursuant to Item 405 of Regulation S-K (§ 229.405 of this chapter) is not contained herein, and will not be contained, to the best of registrant’s knowledge, in definitive proxy or information statements incorporated by reference in Part III of this Form 10-K or any amendment to this Form 10-K. x

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, or a smaller reporting company. See the definitions of “large accelerated filer,” “accelerated filer” and “smaller reporting company” in Rule 12b-2 of the Exchange Act.

|

Large accelerated filer x |

Accelerated filer ¨ | |

|

Non-accelerated filer ¨ (Do not check if a smaller reporting company) |

Smaller reporting company ¨ |

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Act). Yes ¨ No x

As of June 30, 2010 (the last business day of the registrant’s most recently completed second fiscal quarter), the aggregate market value of the shares of common stock held by non-affiliates of the registrant (based on the closing price for the common stock on the NASDAQ Global Select Market) was $2,495,975,576.

As of January 31, 2011, there were outstanding 40,509,260 shares of the registrant’s common stock, no par value, which is the only class of common stock of the registrant.

DOCUMENTS INCORPORATED BY REFERENCE

The information called for by Part III is incorporated by reference to the definitive Proxy Statement for the Annual Meeting of Shareholders of the Company to be held on May 3, 2011.

Table of Contents

Itron, Inc.

| Page | ||||||

|

PART I |

||||||

| 1 | ||||||

| 5 | ||||||

| 13 | ||||||

| 13 | ||||||

| 13 | ||||||

| 13 | ||||||

|

PART II |

||||||

| 14 | ||||||

| 16 | ||||||

|

ITEM 7: MANAGEMENT’S DISCUSSION AND ANALYSIS OF FINANCIAL CONDITION AND RESULTS OF OPERATIONS |

17 | |||||

|

ITEM 7A: QUANTITATIVE AND QUALITATIVE DISCLOSURES ABOUT MARKET RISK |

30 | |||||

| 32 | ||||||

| 34 | ||||||

| 35 | ||||||

| 36 | ||||||

| 37 | ||||||

| 38 | ||||||

|

ITEM 9: CHANGES IN AND DISAGREEMENTS WITH ACCOUNTANTS ON ACCOUNTING AND FINANCIAL DISCLOSURE |

81 | |||||

| 81 | ||||||

| 82 | ||||||

|

PART III |

||||||

|

ITEM 10: DIRECTORS, EXECUTIVE OFFICERS AND CORPORATE GOVERNANCE |

83 | |||||

| 83 | ||||||

| 83 | ||||||

|

ITEM 13: CERTAIN RELATIONSHIPS AND RELATED TRANSACTIONS AND DIRECTOR INDEPENDENCE |

83 | |||||

| 83 | ||||||

|

PART IV |

||||||

| 84 | ||||||

| 87 | ||||||

| 88 | ||||||

Table of Contents

In this Annual Report on Form 10-K, the terms “we,” “us,” “our,” “Itron” and the “Company” refer to Itron, Inc.

Certain Forward-Looking Statements

This document contains forward-looking statements concerning our operations, financial performance, revenues, earnings growth, liquidity, and other items. This document reflects our current plans and expectations and is based on information currently available as of the date of this Annual Report on Form 10-K. When we use the words “expect,” “intend,” “anticipate,” “believe,” “plan,” “project,” “estimate,” “future,” “objective,” “may,” “will,” “will continue,” and similar expressions, they are intended to identify forward-looking statements. Forward-looking statements rely on a number of assumptions and estimates. These assumptions and estimates could be inaccurate and cause our actual results to vary materially from expected results. Risks and uncertainties include 1) the rate and timing of customer demand for our products, 2) rescheduling or cancellations of current customer orders and commitments, 3) competition, 4) changes in estimated liabilities for product warranties and/or litigation, 5) our dependence on customers’ acceptance of new products and their performance, 6) changes in domestic and international laws and regulations, 7) future business combinations, 8) changes in estimates for stock-based compensation and pension costs, 9) changes in foreign currency exchange rates and interest rates, 10) international business risks, 11) our own and our customers’ or suppliers’ access to and cost of capital, and 12) other factors. You should not solely rely on these forward-looking statements as they are only valid as of the date of this Annual Report on Form 10-K. We do not have any obligation to publicly update or revise any forward-looking statement in this document. For a more complete description of these and other risks, refer to Item 1A: “Risk Factors” included in this Annual Report on Form 10-K.

Available Information

Documents we provide to the Securities and Exchange Commission (SEC) are available free of charge under the Investors section of our website at www.itron.com as soon as practicable after they are filed with or furnished to the SEC. In addition, these documents are available at the SEC’s website (http:// www.sec.gov ) and at the SEC’s Headquarters at 100 F Street, NE, Washington, DC 20549, or by calling 1-800-SEC-0330.

General

Itron is a technology company dedicated to delivering end-to-end smart metering solutions to electric, natural gas, and water utilities around the world. Our smart metering solutions, meter data management software, and knowledge application solutions bring additional value to a utility’s metering and grid systems. Our professional services help our customers project-manage, install, implement, operate, and maintain their systems.

We were incorporated in 1977. In 2004, we entered the electricity meter manufacturing business with the acquisition of Schlumberger Electricity Metering. In 2007, we expanded our presence in global meter manufacturing and systems with the acquisition of Actaris Metering Systems SA (Actaris).

The following is a discussion of our major products, our markets, and our operating segments. Refer to Item 7: “Management’s Discussion and Analysis of Financial Condition and Results of Operations” included in this Annual Report on Form 10-K for specific segment results.

Our Business

Our offerings include electricity, natural gas, and water metering systems, software, and services. We classify metering systems into three categories: standard metering, advanced metering systems and technology, and smart metering systems and technology. These categories are described in more detail below:

Standard Metering

A standard meter measures electricity, natural gas, or water by mechanical, electromechanical, or electronic means, with no built-in remote-reading communication capability. Standard meters require manual reading, which is typically performed by a utility representative or meter reading service provider. Worldwide, we produce standard residential, commercial and industrial (C&I), and transmission and distribution (T&D) electricity, natural gas, and water meters.

1

Table of Contents

Advanced Metering Systems and Technology

Advanced metering uses a communication module embedded in the meter to collect and store detailed meter data, which is transmitted to handheld computers, mobile units, and/or fixed networks, allowing utilities to collect the data for billing systems and analyze the meter data for more efficient resource management and streamlined operations. Worldwide, we produce electricity, natural gas, and water advanced metering systems and technology. Depending on the country, communication technologies include telephone, RF (radio frequency), GSM (Global System for Mobile communications), PLC (power line carrier), and Ethernet devices.

Smart Metering Systems and Technology

Smart meters initiate and respond to two-way communications with the utility to automatically collect and transmit meter data frequently to support various applications beyond monthly billings. Our smart metering solutions also have substantially more features and functions than our advanced metering systems and technology. Smart meters are able to send and receive detailed data, collect and store interval data, and interface with other devices, such as in-home displays, smart thermostats and appliances, home area networks, advanced control systems, and more.

Bookings and Backlog of Orders

Bookings for a reported period represent customer contracts and purchase orders received during the period that have met certain regulatory and/or contractual conditions. Total backlog represents committed but undelivered contracts and purchase orders at period-end. Twelve-month backlog represents the portion of total backlog that we estimate will be recognized as revenue over the next 12 months. Backlog is not a complete measure of our future business as we have significant book-and-ship orders. Bookings and backlog may fluctuate significantly due to the timing of large project awards. In addition, annual or multi-year contracts are subject to rescheduling and cancellation by customers due to the long-term nature of the contracts. Beginning total backlog, plus bookings, minus revenues, will not equal ending total backlog due to miscellaneous contract adjustments, foreign currency fluctuations, and other factors. Information on bookings and backlog is summarized as follows:

|

Year Ended |

Annual Bookings | Total Backlog | 12-Month Backlog | |||||||||

| (in millions) | ||||||||||||

|

December 31, 2010 |

$ | 2,396 | $ | 1,620 | $ | 913 | ||||||

|

December 31, 2009 |

$ | 1,849 | $ | 1,488 | $ | 807 | ||||||

|

December 31, 2008 |

$ | 2,543 | $ | 1,309 | $ | 418 | ||||||

Our Operating Segments

We operate under the Itron brand worldwide. Our operating segments as of December 31, 2010 are Itron North America and Itron International. Itron North America generates the majority of its revenues in the United States and Canada. Itron International generates the majority of its revenues in Europe, and the balance primarily in South America and Asia/Pacific.

Sales and Distribution

We use a combination of direct and indirect sales channels in both Itron North America and Itron International. A direct sales force is utilized for the largest electric, natural gas, and water utilities, with which we have long-established relationships. For smaller utilities, we typically use an indirect sales force that consists of distributors, representative agencies, partners, and meter manufacturer representatives.

One customer, Southern California Edison, of our Itron North America operating segment, represented 11% of total Company revenues for the year ended December 31, 2010. No single customer represented more than 10% of total revenues for each of the two years ended December 31, 2009 and 2008. Our 10 largest customers in each of the years ended December 31, 2010, 2009, and 2008 accounted for approximately 34%, 17%, and 15%, of total revenues, respectively.

Raw Materials

Our products require a wide variety of components and materials. Although we have multiple sources of supply for most of our material requirements, certain components and raw materials are supplied by sole-source vendors, and our ability to perform certain contracts depends on the availability of these materials. Refer to Item 1A: “Risk Factors”, included in this Annual Report on Form 10-K, for further discussion related to risks.

2

Table of Contents

Product Development

Our product development is focused on both improving existing technology and developing next-generation technology for electricity, natural gas, water, and heat meters, data collection software, communications technologies, data warehousing, and knowledge application solutions. We spent approximately $140 million, $122 million, and $121 million on product development in 2010, 2009, and 2008, which represented 6%, 7%, and 6% of total revenues in those respective years.

Workforce

As of December 31, 2010, we had approximately 9,500 people in our workforce, including permanent and temporary employees and contractors. We have not experienced any work stoppages and consider our employee relations to be good.

Competition

We provide a broad portfolio of products, systems, and services to customers in the utility industry and have a large number of competitors who offer similar products, systems, and services. We believe that our competitive advantage is based on our ability to provide complete end-to-end integrated solutions, our established customer relationships, and our track record of delivering reliable, accurate, and long-lived products and services. Refer to Item 1A: “Risk Factors” included in this Annual Report on Form 10-K for a discussion of the competitive pressures we face.

Our primary competitors include the following:

|

Badger Meter, Inc. |

Emerson Electric Co. | OSIsoft, LLC | ||

|

Cooper Industries plc |

eMeter Corporation | Pietro Fiorentini S.p.A. | ||

|

Datamatic, Ltd. |

ESCO Technologies Inc. | Roper Industries, Inc. | ||

|

Diehl Group |

General Electric Company | Sensus | ||

|

Dresser, Inc. |

Jiangxi Sanchuan Water Meter Co Ltd. | Silver Spring Networks | ||

|

Echelon Corporation |

Landis+Gyr AG | SmartSynch, Inc. | ||

|

Ecologic Analytics, LLC |

Master Meter, Inc. | Telvent GIT, S.A. | ||

|

El Sewedy Electric Company |

Ningbo Water Meter Co., Ltd. | Trilliant Incorporated | ||

|

Elster Group S.E. |

Oracle Corporation |

Strategic Alliances

We pursue strategic alliances with other companies in areas where collaboration can produce product advancement and acceleration of entry into new markets. The objectives and goals of a strategic alliance can include one or more of the following: technology exchange, product development, joint sales and marketing, or access to new geographic markets. Refer to Item 1A: “Risk Factors” included in this Annual Report on Form 10-K for a discussion of risks associated with strategic alliances.

Intellectual Property

Our patents and patent applications cover a range of technologies, which relate to standard metering, advanced metering systems and technology, smart metering systems and technology, meter data management software, and knowledge application solutions. We also rely on a combination of copyrights and trade secrets to protect our products and technologies. We have registered trademarks for most of our major product lines in the United States and many international countries.

Disputes over the ownership, registration, and enforcement of intellectual property rights arise in the ordinary course of our business. While we believe patents and trademarks are important to our operations and in the aggregate constitute valuable assets, no single patent or trademark, or group of patents or trademarks, is critical to the success of our business. We license some of our technology to other companies, some of which are our competitors.

Environmental Regulations

In the ordinary course of our business we use metals, solvents, and similar materials that are stored on-site. We believe we are in compliance with environmental laws, rules, and regulations applicable to the operation of our business.

3

Table of Contents

MANAGEMENT

Set forth below are the names, ages, and titles of our executive officers as of February 16, 2011.

|

Name |

Age |

Position |

||

|

Malcolm Unsworth |

61 | President and Chief Executive Officer | ||

|

Steven M. Helmbrecht |

48 | Sr. Vice President and Chief Financial Officer | ||

|

John W. Holleran |

56 | Sr. Vice President, General Counsel and Corporate Secretary | ||

|

Philip C. Mezey |

51 | Sr. Vice President and Chief Operating Officer - Itron North America | ||

|

Marcel Regnier |

54 | Sr. Vice President and Chief Operating Officer - Itron International | ||

|

Jared P. Serff |

43 | Vice President, Competitive Resources | ||

Malcolm Unsworth is President and Chief Executive Officer, and a member of our Board of Directors. Mr. Unsworth joined Itron in July 2004 as Sr. Vice President, Hardware Solutions, upon our acquisition of Schlumberger’s electricity metering business. In 2007, following our acquisition of Actaris (now known as Itron International), he was promoted to Sr. Vice President and Chief Operating Officer – Itron International. Mr. Unsworth was appointed President and Chief Operating Officer of Itron in April 2008, and promoted to President and Chief Executive Officer effective March 2009. Mr. Unsworth was elected to the Board of Directors in December 2008.

Steve Helmbrecht is Sr. Vice President and Chief Financial Officer. Mr. Helmbrecht joined Itron in 2002 as Vice President and General Manager, International, and was named Sr. Vice President and Chief Financial Officer in 2005. Previously, Mr. Helmbrecht was Chief Financial Officer of LineSoft Corporation, acquired by Itron in 2002.

John Holleran is Sr. Vice President, General Counsel, and Corporate Secretary. Mr. Holleran joined Itron in January 2007. In 2006, Mr. Holleran was associated with Holleran Law Offices PLLC, and in 2005 was Executive Vice President, Administration, and Chief Legal Officer for Boise Cascade, LLC, the paper and forest products company resulting from the reorganization of Boise Cascade Corporation, in 2004. While with Boise Cascade Corporation, Mr. Holleran most recently served as Sr. Vice President, Human Resources, and General Counsel.

Philip Mezey is Sr. Vice President and Chief Operating Officer - Itron North America. Mr. Mezey joined Itron in March 2003 as Managing Director of Software Development for Itron’s Energy Management Solutions Group with Itron’s acquisition of Silicon Energy Corp. Mr. Mezey was promoted to Group Vice President and Manager of Software Solutions in 2004. In 2005, Mr. Mezey became Sr. Vice President Software Solutions and was promoted to his current position in 2007.

Marcel Regnier is Sr. Vice President and Chief Operating Officer - Itron International. Mr. Regnier joined Itron in April 2007 as part of our acquisition of Actaris. Mr. Regnier served as Actaris’ Managing Director of its water and heat business unit from 2001, when Actaris was created as a result of the reorganization of Schlumberger’s operations, until April 2008, when he was promoted to his current position.

Jared Serff is Vice President, Competitive Resources. Mr. Serff joined Itron in July 2004 upon our acquisition of Schlumberger’s electricity metering business. Mr. Serff spent six years with Schlumberger, the last four of which were as Director of Human Resources with Schlumberger’s electricity metering business where he was in charge of personnel for all locations in Canada, Mexico, France, Taiwan, and the United States.

4

Table of Contents

We are dependent on the utility industry, which has experienced volatility in capital spending.

We derive the majority of our revenues from sales of products and services to utilities. Purchases of our products may be deferred as a result of many factors including economic downturns, slowdowns in new residential and commercial construction, customers’ access to capital at acceptable terms, utility specific financial circumstances, mergers and acquisitions, regulatory decisions, weather conditions, and rising interest rates. We have experienced, and may in the future experience, variability in operating results on an annual and a quarterly basis as a result of these factors.

Utility industry sales cycles can be lengthy and unpredictable.

The utility industry is subject to substantial government regulation. Regulations have often influenced the frequency of meter replacements. Sales cycles for standalone meter products have typically been based on annual or bi-annual bid-based agreements. Utilities place purchase orders against these agreements as their inventories decline, which can create fluctuations in our sales volumes.

Sales cycles for advanced and smart metering systems are generally long and unpredictable due to several factors, including budgeting, purchasing, and regulatory approval processes that can take several years to complete. Our utility customers typically issue requests for quotes and proposals, establish evaluation committees, review different technical options with vendors, analyze performance and cost/benefit justifications, and perform a regulatory review, in addition to applying the normal budget approval process within a utility. Today, governments around the world are implementing new laws and regulations to promote increased energy efficiency, slow or reverse growth in the consumption of scarce resources, reduce carbon dioxide emissions, and protect the environment. Many of the legislative and regulatory initiatives encourage utilities to develop a smart grid infrastructure, and some of these initiatives provide for government subsidies, grants, or other incentives to utilities and other participants in their industry to promote transition to smart grid technologies.

Section 1252 of the U.S. Energy Policy Act of 2005 requires electric utilities to consider offering their customers time-based rates. The Act also directs these utilities and state utility commissions to study and evaluate methods for implementing demand response, to shift consumption away from peak hours, and to improve power generation.

The European Union has issued the EU Energy Package, which includes directives and regulations intended to strengthen consumer rights and protection in the EU energy market. The EU’s 20-20-20 goals include a 20% increase in energy efficiency, a 20% reduction of carbon dioxide emissions compared with 1990 levels, and producing 20% of its energy from renewable sources by 2020. The package requires EU Member States to ensure the implementation of smart metering systems and outlines deployment by 2022, with 80% of electric consumers equipped with smart metering systems by 2020.

While we believe these initiatives will provide opportunities for sales of our products, the pace at which these markets will grow is unknown due to the timing of legislation, regulatory approvals related to the deployment of new technology, capital budgets of the utilities, and purchasing decisions by our customers. If government regulations regarding the smart grid and smart metering are delayed, revised to permit lower or different investment levels in metering infrastructure, or terminated altogether, this could have a material adverse effect on our results of operation, cash flow, and financial condition.

We are subject to international business uncertainties, obstacles to the repatriation of earnings, and foreign currency fluctuations.

A substantial portion of our revenues is derived from operations conducted outside the United States. International sales and operations may be subjected to risks such as the imposition of government controls, government expropriation of facilities, lack of a well-established system of laws and enforcement of those laws, access to a legal system free of undue influence or corruption, political instability, terrorist activities, restrictions on the import or export of critical technology, currency exchange rate fluctuations, adverse tax burdens, availability of qualified third-party financing, generally longer receivable collection periods than those commonly practiced in the United States, trade restrictions, changes in tariffs, labor disruptions, difficulties in staffing and managing international operations, difficulties in imposing and enforcing operational and financial controls at international locations potential insolvency of international distributors, burdens of complying with different permitting standards and a wide variety of foreign laws, and obstacles to the repatriation of earnings and cash. Fluctuations in the value of international currencies may impact our operating results due to the translation to the U.S. dollar as well as our ability to compete in international markets. International expansion and market acceptance depend on our ability to modify our technology to take into account such factors as the applicable regulatory and business environment, labor costs, and other economic conditions. In addition, the laws of certain countries do not protect our products or technologies in the same manner as the laws of the United States. There can be no assurance that these factors will not

5

Table of Contents

have a material adverse effect on our future international sales and, consequently, on our business, financial condition, and results of operations.

We depend on our ability to develop new competitive products.

Our future success will depend, in part, on our ability to continue to design and manufacture new competitive products and to enhance and sustain our existing products, keep pace with technological advances and changing customer requirements, gain international market acceptance, and manage other factors in the markets in which we sell our products. Product development will require continued investment in order to maintain our market position. We may not have the necessary capital, or access to capital at acceptable terms, to make these investments. We have made, and expect to continue to make, substantial investments in technology development. However, we may experience unforeseen problems in the development or performance of our technologies or products. In addition, we may not meet our product development schedules. New products often require certifications or regulatory approvals before the products can be used and we cannot be certain that our new products will be approved in a timely manner. Finally, we may not achieve market acceptance of our new products and services.

We may face product-failure exposure.

We provide product warranties for varying lengths of time and establish allowances in anticipation of warranty expenses. In addition, we record contingent liabilities for additional product-failure related costs. These warranty and related product-failure allowances may be inadequate due to undetected product defects, unanticipated component failures, as well as changes in various estimates for material, labor, and other costs we may incur to replace projected product failures. As a result, we may incur additional warranty and related expenses in the future with respect to new or established products. Systems that we sell could fail to perform as intended, resulting in potentially substantial claims against us that could materially and adversely affect our financial position. We sell vending and pre-payment systems with security features that if compromised, may lead to claims against us, which could materially and adversely affect our financial position.

Business interruptions could adversely affect our business.

Our worldwide operations could be subject to hurricanes, tornados, earthquakes, floods, fires, extreme weather conditions, medical epidemics or pandemics, or other natural or manmade disasters or business interruptions. The occurrence of any of these business disruptions could seriously harm our business, financial condition, and results of operations.

Our key manufacturing facilities are concentrated and in the event of a significant interruption in production at any of our manufacturing facilities, considerable expense, time, and effort could be required to establish alternative production lines to meet contractual obligations, which would have a material adverse effect on our business, financial condition, and results of operations.

We are facing increasing competition.

We face competitive pressures from a variety of companies in each of the markets we serve. Some of our present and potential future competitors have, or may have, substantially greater financial, marketing, technical, or manufacturing resources and, in some cases, have greater name recognition and experience. Some competitors may enter markets we serve and sell products at lower prices in order to grow market share. Our competitors may be able to respond more quickly to new or emerging technologies and changes in customer requirements. They may also be able to devote greater resources to the development, promotion, and sale of their products and services than we can. Some competitors have made, and others may make, strategic acquisitions or establish cooperative relationships among themselves or with third parties that enhance their ability to address the needs of our prospective customers. It is possible that new competitors or alliances among current and new competitors may emerge and rapidly gain significant market share. Other companies may also drive technological innovation and develop products that are equal in quality and performance or superior to our products, which could put pressure on our market position, reduce our overall sales, and require us to invest additional funds in new technology development. In addition, there is a risk that low-cost providers will enter, or form alliances or cooperative relationships with our competitors, thereby contributing to future price erosion. Some of our products and services may become commoditized and we may have to adjust the prices of some of our products to stay competitive. Should we fail to compete successfully with current or future competitors, we could experience material adverse effects on our business, financial condition, results of operations, and cash flows.

6

Table of Contents

We are affected by the availability and regulation of radio spectrum and interference with the radio spectrum that we use.

A significant number of our products use radio spectrum, which are subject to regulation by the Federal Communications Commission (FCC) in the United States. The FCC may adopt changes to the rules for our licensed and unlicensed frequency bands that are incompatible with our business. In the past, the FCC has adopted changes to the requirements for equipment using radio spectrum, and it is possible that the FCC or the U.S. Congress will adopt additional changes.

Although radio licenses are generally required for radio stations, Part 15 of the FCC’s rules permits certain low-power radio devices (Part 15 devices) to operate on an unlicensed basis. Part 15 devices are designed for use on frequencies used by others. These other users may include licensed users, which have priority over Part 15 users. Part 15 devices cannot cause harmful interference to licensed users and must be designed to accept interference from licensed radio devices. In the United States, our advanced and smart metering systems are typically Part 15 devices that transmit information to (and receive information from, if applicable) handheld, mobile, or fixed network systems pursuant to these rules.

The FCC has initiated a rulemaking proceeding in which it is considering adopting “spectrum etiquette” requirements for unlicensed Part 15 devices operating in the 902-928 MHz band, which many of our advanced and smart metering systems utilize. The outcome of the proceeding may require us to make material changes to our equipment.

The FCC has also adopted service rules governing the use of the 1427-1432 MHz band. We use this band with various devices in our network solutions. Among other things, the rules reserve parts of the band for general telemetry, including utility telemetry, and provide that nonexclusive licenses will be issued in accordance with Part 90 rules and the recommendations of frequency coordinators. Telemetry licensees must comply with power limits and out-of-band emission requirements that are designed to avoid interference with other users of the band. The FCC issues licenses on a nonexclusive basis and it is possible that the demand for spectrum will exceed supply,

Our radio-based products primarily employ unlicensed radio frequencies. We depend upon sufficient radio spectrum to be allocated by the FCC for our intended uses. As to the licensed frequencies, there is some risk that there may be insufficient available frequencies in some markets to sustain our planned operations. The unlicensed frequencies are available for a wide variety of uses and may not be entitled to protection from interference by other users who operate in accordance with FCC rules. The unlicensed frequencies are also often the subject of proposals to the FCC requesting a change in the rules under which such frequencies may be used. If the unlicensed frequencies become crowded to unacceptable levels, restrictive, or subject to changed rules governing their use, our business could be materially adversely affected.

We have committed, and will continue to commit, significant resources to the development of products that use particular radio frequencies. Action by the FCC could require modifications to our products. The inability to modify our products to meet such requirements, the possible delays in completing such modifications, and the cost of such modifications all could have a material adverse effect on our future business, financial condition, and results of operations.

Outside of the United States, certain of our products require the use of RF and are subject to regulations in those jurisdictions where we have deployed such equipment. In some jurisdictions, radio station licensees are generally required to operate a radio transmitter and such licenses may be granted for a fixed term and must be periodically renewed. In other jurisdictions, the rules permit certain low power devices to operate on an unlicensed basis. Our advanced and smart metering systems typically transmit to (and receive information from, if applicable) handheld, mobile, or fixed network reading devices in unlicensed bands pursuant to rules regulating such use. Generally, we use the unlicensed Industrial, Scientific, and Medical (ISM) bands with the various reading devices in our solutions. In Europe, we generally use the 433 MHz and 868 MHz bands. In the rest of the world, we primarily use the 433 MHz and 2.4000-2.4835 GHz bands, as well as other local unlicensed bands. To the extent we introduce new products designed for use in the United States or another country into a new market, such products may require significant modification or redesign in order to meet frequency requirements and other regulatory specifications. In some countries, limitations on frequency availability or the cost of making necessary modifications may preclude us from selling our products in those countries. In addition, new consumer products may create interference with the performance of our products, which could lead to claims against us.

We may face liability associated with alleged adverse health effects from the use of our product.

We may be subject to claims that there are adverse health effects from the radio frequencies utilized in connection with our products. If these claims succeed, our customers could suspend implementation or purchase substitute products, which could cause a loss of sales.

7

Table of Contents

We may be unable to adequately protect our intellectual property.

While we believe that our patents and other intellectual property have significant value, it is uncertain that this intellectual property or any intellectual property acquired or developed by us in the future will provide meaningful competitive advantages. There can be no assurance that our patents or pending applications will not be challenged, invalidated, or circumvented by competitors or that rights granted thereunder will provide meaningful proprietary protection. Moreover, competitors may infringe our patents or successfully avoid them through design innovation. To combat infringement or unauthorized use, we may need to commence litigation, which can be expensive and time-consuming. In addition, in an infringement proceeding a court may decide that a patent or other intellectual property right of ours is not valid or is unenforceable, or may refuse to stop the other party from using the technology or other intellectual property right at issue on the grounds that it is non-infringing or the legal requirements for an injunction have not been met. Policing unauthorized use of our intellectual property is difficult and expensive, and we cannot provide assurance that we will be able to, or have the resources to, prevent misappropriation of our proprietary rights, particularly in countries that do not protect such rights in the same manner as they do in the United States.

A significant portion of our revenue is generated with a limited number of customers.

Historically, our revenues have been concentrated with a limited number of customers, which change over time. The 10 largest customers accounted for 34%, 17%, and 15% of revenues for 2010, 2009, and 2008, respectively. One customer represented 11% of total revenues for the year ended December 31, 2010. No single customer represented more than 10% of total Company revenues for each of the two years ended December 31, 2009 and 2008. We are often a party to large, multi-year contracts that are subject to cancellation or rescheduling by our customers due to many factors, such as extreme, unexpected weather conditions that cause our customers to redeploy resources, convenience, regulatory issues, or possible acts of terrorism. Cancellation or postponement of one or more of these significant contracts could have a material adverse effect on our financial and operating results. In addition, if a large customer contract is not replaced upon its expiration with new business of similar magnitude, our financial and operating results would be adversely affected.

As we enter into agreements related to the deployment of smart metering systems and technology, the value of these contracts is substantially larger than contracts we have had with our customers in the past. These deployments last several years and may exceed the length of prior deployment agreements. The terms and conditions of these smart metering system agreements related to testing, contractual liabilities, warranties, performance, and indemnities can be substantially different than the terms and conditions associated with our previous contracts.

We may face liability associated with the use of products for which patent ownership or other intellectual property rights are claimed.

We may be subject to claims or inquiries regarding alleged unauthorized use of third party’s intellectual property. An adverse outcome in any intellectual property litigation or negotiation could subject us to significant liabilities to third parties, require us to license technology or other intellectual property rights from others, require us to comply with injunctions to cease marketing or the use of certain products or brands, or require us to redesign, re-engineer, or rebrand certain products or packaging, any of which could affect our business, financial condition, and results of operations. If we are required to seek licenses under patents or other intellectual property rights of others, we may not be able to acquire these licenses at acceptable terms, if at all. In addition, the cost of responding to an intellectual property infringement claim, in terms of legal fees, expenses, and the diversion of management resources, whether or not the claim is valid, could have a material adverse effect on our business, financial condition, and results of operations.

If our products potentially infringe the intellectual property rights of others, we may be required to indemnify our customers for any damages they suffer. We generally indemnify our customers with respect to infringement by our products of the proprietary rights of third parties. Third parties may assert infringement claims against our customers. These claims may require us to initiate or defend protracted and costly litigation on behalf of our customers, regardless of the merits of these claims. If any of these claims succeed, we may be forced to pay damages on behalf of our customers or may be required to obtain licenses for the products they use. If we cannot obtain all necessary licenses on commercially reasonable terms, our customers may be forced to stop using our products.

We depend on certain key vendors and components.

Certain of our products, subassemblies, and system components are procured from limited sources. Our reliance on such limited sources involves certain risks, including the possibility of shortages and reduced control over delivery schedules, quality and costs, and our vendors’ access to capital at acceptable terms. Any adverse change in the supply, or price, of these

8

Table of Contents

components could adversely affect our business, financial condition, and results of operations. In addition, we depend on a small number of contract manufacturing vendors for a large portion of our low-volume manufacturing business and all of our repair services for our domestic handheld meter reading units. Should any of these vendors become unable to perform up to their responsibilities, our operations could be materially disrupted.

A number of key personnel are critical to the success of our business.

Our success depends in large part on the efforts of our highly qualified technical and management personnel in all disciplines. The loss of one or more of these employees and the inability to attract and retain qualified replacements could have a material adverse effect on our business.

We may not realize the expected benefits from strategic alliances.

We have several strategic alliances with large and complex organizations and other companies with which we work to offer complementary products and services. There can be no assurance we will realize the expected benefits from these strategic alliances. If successful, these relationships may be mutually beneficial and result in shared growth. However, alliances carry an element of risk because, in most cases, we must both compete and collaborate with the same company from one market to the next. Should our strategic partnerships fail to perform, Itron could experience delays in product development or experience other operational difficulties.

Our acquisitions of and investments in third parties have risks.

We may complete additional acquisitions or make investments in the future, both within and outside of the United States. In order to finance future acquisitions, we may need to raise additional funds through public or private financings, and there are no assurances that such financing would be available at acceptable terms. Acquisitions and investments involve numerous risks such as the diversion of senior management’s attention, unsuccessful integration of the acquired entity’s personnel, operations, technologies, and products, lack of market acceptance of new services and technologies, or difficulties in operating businesses in foreign legal jurisdictions. We may experience difficulties that could affect our internal control over financial reporting, which could create a significant deficiency or material weakness in our overall internal controls under Section 404 of the Sarbanes-Oxley Act of 2002. Failure to properly or adequately address these issues could result in the diversion of management’s attention and resources and materially and adversely impact our ability to manage our business. Impairment of an investment, goodwill, or an intangible asset may also result if these risks were to materialize. For investments in entities that are not wholly owned by Itron, such as joint ventures, a loss of control as defined by U.S. generally accepted accounting principles (GAAP) could result in a significant change in accounting treatment and a change in the carrying value of the entity. There can be no assurances that an acquired business will perform as expected, accomplish our strategic objective, or generate significant revenues, profits, or cash flows. During prior years, we have incurred impairments of noncontrolling interest investments. In addition, acquisitions and investments in third parties may involve the assumption of obligations, significant write-offs, or other charges associated with the acquisition.

Impairment of our intangible assets, long-lived assets, goodwill, or deferred tax assets could result in significant charges that would adversely impact our future operating results.

We have significant intangible assets, long-lived assets, goodwill, and deferred tax assets that are susceptible to valuation adjustments as a result of changes in various factors or conditions.

We assess impairment of amortizable intangible and long-lived assets whenever events or changes in circumstances indicate that the carrying value may not be recoverable. Factors that could trigger an impairment of such assets include the following:

| • |

underperformance relative to projected future operating results; |

| • |

changes in the manner or use of the acquired assets or the strategy for our overall business; |

| • |

negative industry or economic trends; |

| • |

decline in our stock price for a sustained period or decline in our market capitalization below net book value; and |

| • |

changes in our organization or management reporting structure, which could result in additional reporting units, requiring greater aggregation or disaggregation in our analysis by reporting unit and potentially alternative methods/assumptions of estimating fair values. |

We assess the potential impairment of goodwill each year as of October 1. We also assess the potential impairment of goodwill whenever events or changes in circumstances indicate that the carrying value may not be recoverable. Adverse

9

Table of Contents

changes in economic conditions or our operations could affect the assumptions we use to calculate the fair value, which in turn could result in an impairment charge in future periods that would impact our results of operations and financial position in that period. Refer to Item 1: “Management’s Discussion and Analysis of Financial Condition and Results of Operations, Critical Accounting Estimates ” included in this Annual Report on Form 10-K for additional information regarding the results of our October 1, 2010 goodwill impairment assessment.

The realization of our deferred tax assets is supported in part by projections of future taxable income. We provide a valuation allowance based on estimates of future taxable income in the respective taxing jurisdiction and the amount of deferred taxes that are expected to be realizable. If future taxable income is different from that expected, we may not be able to realize some or all of the tax benefit, which could have a material adverse effect on our financial results and cash flows.

We are subject to regulatory compliance.

We are subject to various governmental regulations in all of the jurisdictions in which we conduct business. Failure to comply with current or future regulations could result in the imposition of substantial fines, suspension of production, alteration of our production processes, cessation of operations, or other actions, which could materially and adversely affect our business, financial condition, and results of operations.

Changes in environmental regulations, violations of the regulations, or future environmental liabilities could cause us to incur significant costs and adversely affect our operations.

Our business and our facilities are subject to a number of laws, regulations, and ordinances governing, among other things, the storage, discharge, handling, emission, generation, manufacture, disposal, remediation of, and exposure to toxic or other hazardous substances, and certain waste products. Many of these environmental laws and regulations subject current or previous owners or operators of land to liability for the costs of investigation, removal, or remediation of hazardous materials. In addition, these laws and regulations typically impose liability regardless of whether the owner or operator knew of, or was responsible for, the presence of any hazardous materials and regardless of whether the actions that led to the presence were conducted in compliance with the law. In the ordinary course of our business, we use metals, solvents, and similar materials, which are stored on-site. The waste created by the use of these materials is transported off-site on a regular basis by unaffiliated waste haulers. Many environmental laws and regulations require generators of waste to take remedial actions at, or in relation to, the off-site disposal location even if the disposal was conducted in compliance with the law. The requirements of these laws and regulations are complex, change frequently, and could become more stringent in the future. Failure to comply with current or future environmental regulations could result in the imposition of substantial fines, suspension of production, alteration of our production processes, cessation of operations, or other actions, which could materially and adversely affect our business, financial condition, and results of operations. There can be no assurance that a claim, investigation, or liability will not arise with respect to these activities, or that the cost of complying with governmental regulations in the future will not have a material adverse effect on us.

Our credit facility and the indenture related to our convertible senior subordinated notes limit our ability and the ability of most of our subsidiaries to take certain actions.

Our credit facility and convertible notes place restrictions on our ability and the ability of most of our subsidiaries to, among other things:

|

• incur more debt; |

• pay dividends and make distributions; |

|

|

• make certain investments; |

• incur capital expenditures above a set limit; |

|

|

• redeem or repurchase capital stock; |

• create liens; |

|

|

• enter into transactions with affiliates; |

• enter into sale lease-back transactions; |

|

|

• merge or consolidate; |

• transfer or sell assets. |

Our credit facility contains other customary covenants, including the requirement to meet specified financial ratios. Our ability to borrow under our credit facility will depend on the satisfaction of these covenants. Events beyond our control can affect our ability to meet those covenants. Our failure to comply with obligations under our borrowing arrangements may result in declaration of an event of default. An event of default, if not cured or waived, may permit acceleration of required payments against such indebtedness. We cannot be certain we will be able to remedy any such defaults. If our required payments are accelerated, we cannot be certain that we will have sufficient funds available to pay the indebtedness or that we will have the ability to raise sufficient capital to replace the indebtedness on terms favorable to us or at all. In addition, in the case of an event of default under our secured indebtedness such as our credit facility, the lenders may be permitted to foreclose on our assets securing that indebtedness.

10

Table of Contents

Our credit facility is sensitive to interest rate and foreign currency exchange rate risks that could impact our financial position and results of operations.

Our ability to service our indebtedness is dependent on our ability to generate cash, which is influenced by many factors beyond our control.

Our ability to make payments on or refinance our indebtedness, fund planned capital expenditures, and continue research and development will depend on our ability to generate cash in the future. This is subject to general economic, financial, competitive, legislative, regulatory, and other factors that are beyond our control, including counterparty risks with banks and other financial institutions. We may need to refinance all or a portion of our indebtedness on or before maturity. We cannot provide assurance that we will be able to refinance any of our indebtedness on commercially reasonable terms or at all.

We are exposed to counterparty default risks with our financial institutions and insurance providers.

The financial strength of some depository institutions has diminished as a result of the recent financial crisis, and this trend may continue. If one or more of the depository institutions in which we maintain significant cash balances were to fail, our ability to access these funds might be temporarily or permanently limited, and we could face material liquidity problems and financial losses.

At December 31, 2010, we had outstanding standby letters of credit (LOC’s) of $43.5 million issued under our credit facility’s $240 million multicurrency revolver, resulting in $196.5 million being available for additional borrowings. The lenders of our credit facility consist of several participating financial institutions. Our revolving line of credit allows us to provide LOC’s in support of our obligations for customer contracts and provides additional liquidity, including an option for refinancing our convertible senior subordinated notes. Our convertible notes are classified as current due to the combination of put, call, and conversion options that are part of the terms, including the option of the holder to convert the notes between July 1, 2011 and August 1, 2011. If our lenders are not able to honor their line of credit commitments due to the loss of a participating financial institution or other circumstance, we would need to seek alternative financing, which may not be under acceptable terms, and therefore could adversely impact our ability to successfully bid on future sales contracts and adversely impact our liquidity and ability to fund some of our internal initiatives or future acquisitions.

As of December 31, 2010, approximately 93% of our outstanding term loans were at fixed London Interbank Offered Rate (LIBOR) rates as a result of interest rate swaps. These interest rate swaps protect us against the risk of adverse fluctuations in the borrowing’s denominated LIBOR. Currently, our exposure to default risk on our interest rate swap agreements is minimal as we are in a liability position on all interest rate swaps. However, if the LIBOR rates were to significantly increase, there is a risk that one or more counterparties may be unable to meet its obligations under the swap agreement.

If we fail to maintain an effective system of internal controls, we may not be able to accurately report our financial results or prevent fraud.

Effective internal controls are necessary for us to provide reliable and accurate financial reports and effectively prevent fraud. We have devoted significant resources and time to comply with the internal control over financial reporting requirements of the Sarbanes-Oxley Act of 2002. In addition, Section 404 under the Sarbanes-Oxley Act of 2002 requires that our auditors attest to the design and operating effectiveness of our controls over financial reporting. Our compliance with the annual internal control report requirement for each fiscal year will depend on the effectiveness of our financial reporting, data systems, and controls across our operating subsidiaries. Furthermore, an important part of our growth strategy has been, and will likely continue to be, the acquisition of complementary businesses, and we expect these systems and controls to become increasingly complex to the extent that we integrate acquisitions and our business grows. Likewise, the complexity of our transactions, systems, and controls may become more difficult to manage. We cannot be certain that these measures will ensure that we design, implement, and maintain adequate controls over our financial processes and reporting in the future, especially for acquisition targets that may not have been required to be in compliance with Section 404 of the Sarbanes-Oxley Act of 2002 at the date of acquisition. Any failure to implement required new or improved controls, difficulties encountered in their implementation or operation, or difficulties in the assimilation of acquired businesses into our control system could harm our operating results or cause it to fail to meet our financial reporting obligations. Inadequate internal controls could also cause investors to lose confidence in our reported financial information, which could have a negative effect on the trading price of our stock and our access to capital.

11

Table of Contents

We rely on information technology systems.

We are dependent on information technology systems, including, but not limited to, networks, applications, and outsourced services. We continually enhance and implement new systems and processes throughout our global operations. During 2011, we are upgrading our primary enterprise resource planning (ERP) systems to more compatible ERP systems that allow greater depth and breadth of functionality. System conversions are expensive and time consuming undertakings that impact all areas of the Company. While a successful implementation will provide many benefits to us, an unsuccessful or delayed implementation may cost us significant time and resources, as well as expense. The failure of these systems to operate effectively, problems with transitioning to upgraded or replacement systems, or a breach in security of these systems could materially and adversely affect our business, financial condition, and results of operations by harming our ability to accurately forecast sales demand, manage our supply chain and production facilities, achieve accuracy in the conversion of electronic data and records, and to report financial and management information on a timely and accurate basis. In addition, due to the systemic internal control features within ERP systems, we may experience difficulties that could affect our internal control over financial reporting, which could create a significant deficiency or material weakness in our overall internal controls under Section 404 of the Sarbanes-Oxley Act of 2002.

Changes in tax laws and unanticipated tax liabilities could adversely affect our effective income tax rate and profitability.

We are subject to income taxes in the United States and numerous foreign jurisdictions. Our effective income tax rate in the future could be adversely affected by a number of factors, including: changes in the mix of earnings in countries with differing statutory tax rates, changes in the realization of deferred tax assets, changes in tax laws, the outcome of income tax audits in various jurisdictions around the world, and any repatriation of non-U.S. earnings for which we have not previously provided for U.S. taxes. We regularly assess all of these matters to determine the adequacy of our tax provision, which is subject to significant discretion.

Our quarterly results may fluctuate substantially due to several additional factors.

We have experienced variability in quarterly results, including losses, and believe our quarterly results will continue to fluctuate as a result of many factors, including those risks and events previously mentioned. Additional factors that may cause the price of our common stock to decline include:

| • |

a higher proportion of products sold with fewer features and functionality, resulting in lower revenues and gross margins; |

| • |

a shift in sales channel mix, which could impact the revenue received and commissions paid; |

| • |

a change in accounting standards or practices that may impact us to a greater degree than other companies due to our product mix, which would impact revenue recognition, or our borrowing structure, including our convertible notes; and |

| • |

a change in existing taxation rules or practices due to our specific operating structure that may not be comparable to other companies. |

12

Table of Contents

None.

The following table lists the number of factories and offices by region.

| Factories | Offices | |||||||||||||||

| Owned | Leased | Owned | Leased | |||||||||||||

|

North America |

4 | 11 | 1 | 14 | ||||||||||||

|

Europe |

14 | 6 | - | 22 | ||||||||||||

|

Asia/Pacific |

2 | 6 | - | 17 | ||||||||||||

|

Other (rest of world) |

4 | 8 | - | 11 | ||||||||||||

|

Total |

24 | 31 | 1 | 64 | ||||||||||||

Our major manufacturing facilities are owned, while smaller factories and sales offices may be leased. Our factory locations typically consist of manufacturing, assembly, service, and/or distribution, and may also include research and development and administrative functions. Our office locations consist primarily of sales and administration functions, and may also include research and development functions. Itron North America facilities are located primarily in the United States while Itron International’s facilities are in Europe, Asia/Pacific, and throughout the rest of the world. We own our headquarters facility, which is located in Liberty Lake, Washington. Our other principal properties are owned and in good condition, and we believe our current facilities will be sufficient to support our operations for the foreseeable future.

Our U.S. operations for advanced metering communication modules are located in Waseca, Minnesota and our electricity meter operations are located in Oconee, South Carolina. Our international operations are more diversified. If any of our facilities are disrupted, our production capacity could be reduced, though most significantly in the United States.

There are no material pending legal proceedings, as defined by Item 103 of Regulation S-K, at December 31, 2010.

No matters were submitted to a vote of shareholders of Itron, Inc. during the fourth quarter of 2010.

13

Table of Contents

Market Information for Common Stock

Our common stock is traded on the NASDAQ Global Select Market. The following table reflects the range of high and low common stock sales prices for the four quarters of 2010 and 2009 as reported by the NASDAQ Global Select Market.

| 2010 | 2009 | |||||||||||||||

| High | Low | High | Low | |||||||||||||

|

First Quarter |

$ | 75.96 | $ | 59.12 | $ | 66.66 | $ | 40.10 | ||||||||

|

Second Quarter |

$ | 81.95 | $ | 61.60 | $ | 62.19 | $ | 42.77 | ||||||||

|

Third Quarter |

$ | 66.87 | $ | 52.05 | $ | 67.89 | $ | 50.15 | ||||||||

|

Fourth Quarter |

$ | 67.58 | $ | 52.03 | $ | 69.49 | $ | 54.92 | ||||||||

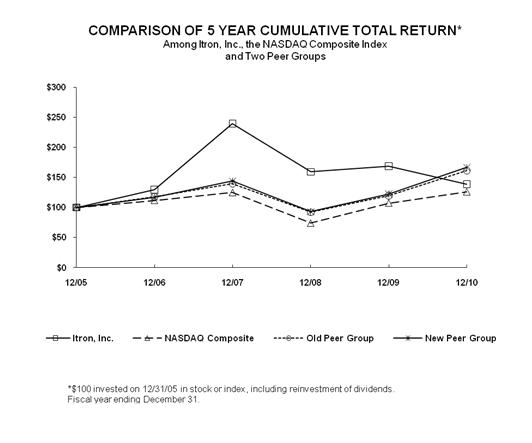

Performance Graph

The following graph compares the five-year cumulative total return to shareholders on our common stock with the five-year cumulative total return of the NASDAQ Composite Index, our peer group of companies used for the year ended December 31, 2010, and our previous peer group of companies used for the year ended December 31, 2009.

The above presentation assumes $100 invested on December 31, 2005 in the common stock of Itron, Inc., the NASDAQ Composite Index, and the peer groups, with all dividends reinvested. With respect to companies in the peer groups, the returns of each such corporation have been weighted to reflect relative stock market capitalization at the beginning of each annual period plotted. The stock prices shown above for our common stock are historical and not necessarily indicative of future price performance.

14

Table of Contents

In 2010, we reassessed our peer group to identify global companies that are either direct competitors or have similar industry and business operating characteristics. Our new peer group includes the following publicly traded companies: Badger Meter, Inc., Cooper Industries, Ltd., Echelon Corporation, ESCO Technologies Inc., National Instruments Corporation, and Roper Industries, Inc. Our previous peer group included the following publicly traded companies: Badger Meter, Inc., Cooper Industries, Ltd., ESCO Technologies Inc., Mueller Water Products, LLC, National Instruments Corporation, and Roper Industries, Inc.

Holders

At January 31, 2011, there were 303 holders of record of our common stock.

Dividends

Since the inception of the Company, we have not declared or paid cash dividends. In addition, our credit facility dated April 18, 2007 prohibits the declaration or payment of a cash dividend as long as this facility is in place. Upon repayment of our borrowings, we intend to retain future earnings for the development of our business and do not anticipate paying cash dividends in the foreseeable future.

15

Table of Contents

The selected consolidated financial data below is derived from our consolidated financial statements, which have been audited by independent registered public accounting firms. This selected consolidated financial and other data represents portions of our financial statements. You should read this information together with Item 7: “Management’s Discussion and Analysis of Financial Condition and Results of Operations” and Item 8: “Financial Statements and Supplementary Data” included in this Annual Report on Form 10-K. Historical results are not necessarily indicative of future performance.

| Year Ended December 31, | ||||||||||||||||||||

| 2010 | 2009 | 2008 | 2007 (2) | 2006 (3) | ||||||||||||||||

| (in thousands, except per share data) | ||||||||||||||||||||

|

Consolidated Statements of Operations Data |

||||||||||||||||||||

|

Revenues |

$ | 2,259,271 | $ | 1,687,447 | $ | 1,909,613 | $ | 1,464,048 | $ | 644,042 | ||||||||||

|

Cost of revenues |

1,561,032 | 1,149,991 | 1,262,756 | 976,761 | 376,600 | |||||||||||||||

|

Gross profit |

698,239 | 537,456 | 646,857 | 487,287 | 267,442 | |||||||||||||||

|

Operating income |

184,197 | 45,027 | 109,822 | 46,473 | 61,743 | |||||||||||||||

|

Net income (loss) |

104,770 | (2,249) | 19,811 | (22,851) | 33,759 | |||||||||||||||

|

Earnings (loss) per common share-Basic |

$ | 2.60 | $ | (0.06) | $ | 0.60 | $ | (0.77) | $ | 1.33 | ||||||||||

|

Earnings (loss) per common share-Diluted |

$ | 2.56 | $ | (0.06) | $ | 0.57 | $ | (0.77) | $ | 1.28 | ||||||||||

|

Weighted average common shares outstanding-Basic |

40,337 | 38,539 | 33,096 | 29,584 | 25,414 | |||||||||||||||

|

Weighted average common shares outstanding-Diluted |

40,947 | 38,539 | 34,951 | 29,584 | 26,283 | |||||||||||||||

|

Consolidated Balance Sheet Data |

||||||||||||||||||||

|

Working capital (1) |

$ | 178,483 | $ | 282,532 | $ | 293,296 | $ | 249,579 | $ | 492,861 | ||||||||||

|

Total assets |

2,745,797 | 2,854,621 | 2,856,348 | 3,030,457 | 988,522 | |||||||||||||||

|

Total debt |

610,941 | 781,764 | 1,151,767 | 1,538,799 | 469,324 | |||||||||||||||

|

Shareholders’ equity |

1,428,295 | 1,400,514 | 1,058,776 | 790,435 | 390,982 | |||||||||||||||

|

Other Financial Data |

||||||||||||||||||||

|

Cash provided by operating activities |

$ | 254,591 | $ | 140,787 | $ | 193,146 | $ | 133,327 | $ | 94,773 | ||||||||||

|

Cash used in investing activities |

(56,274) | (53,994) | (67,075) | (1,714,416) | (85,499) | |||||||||||||||

|

Cash (used in) provided by financing activities |

(148,637) | (114,121) | (63,376) | 1,310,360 | 318,493 | |||||||||||||||

|

Capital expenditures |

(62,822) | (52,906) | (63,430) | (40,602) | (31,739) | |||||||||||||||

| (1) |

Working capital represents current assets less current liabilities. |

| (2) |

On April 18, 2007, we completed the acquisition of Actaris Metering Systems SA (Actaris). The Consolidated Statement of Operations for the year ended December 31, 2007 includes the operating activities of the Actaris acquisition from April 18, 2007 through December 31, 2007. |

| (3) |

On January 1, 2009, we adopted Financial Accounting Standards Board (FASB) Staff Position (FSP) APB 14-1, Accounting for Convertible Debt Instruments That May Be Settled in Cash upon Conversion (Including Partial Cash Settlement) (FSP 14-1) relating to our convertible senior subordinate notes issued in August 2006. (The guidance in FSP 14-1 is now embedded within Accounting Standards Codification TM (ASC) 470-20). We used the SEC staff’s Alternative A transition election for presenting prior financial information, and therefore the financial information as of and for the year ended December 31, 2006 has not been adjusted and is not comparable to the financial information as of and for the years ended December 31, 2010, 2009, 2008, and 2007. |

16

Table of Contents

| ITEM 7: | MANAGEMENT’S DISCUSSION AND ANALYSIS OF FINANCIAL CONDITION AND RESULTS OF OPERATIONS |

The following discussion and analysis should be read in conjunction with Item 8: “Financial Statements and Supplementary Data.”

Overview

We are a technology company, offering end-to-end smart metering solutions to electric, natural gas, and water utilities around the world. Our smart metering solutions, meter data management software, and knowledge application solutions bring additional value to a utility’s metering and grid systems. Our professional services help our customers project-manage, install, implement, operate, and maintain their systems.

Revenues for 2010 increased 34%, compared with 2009, primarily due to the deployment of our smart metering contracts in Itron North America. Total backlog increased 9% and twelve month backlog increased 13% in 2010, compared with 2009.

Total company gross margin decreased one percentage point in 2010, compared with 2009, due to several additional costs in 2010, the most significant including increased warranty expense of $14.4 million for arbitration claims in Sweden, which were settled in the third quarter of 2010.

Diluted earnings per share were $2.56 in 2010, compared with a diluted loss per share of $0.06 in 2009.

Total debt repayments in 2010 were $155.2 million, bringing the total debt outstanding to $610.9 million at December 31, 2010.

Total Company

| Year Ended December 31, | ||||||||||||||||

| 2010 | % Change | 2009 | % Change | 2008 | ||||||||||||

| (in thousands) | (in thousands) | (in thousands) | ||||||||||||||

|

Revenues |

$ | 2,259,271 | 34% | $ | 1,687,447 | (12%) | $ | 1,909,613 | ||||||||

|

Gross Profit |

698,239 | 30% | 537,456 | (17%) | 646,857 | |||||||||||

|

Gross Margin |

30.9% | 31.9% | 33.9% | |||||||||||||

| Year Ended December 31, | ||||||||||||

| 2010 | 2009 | 2008 | ||||||||||

| (in thousands) | ||||||||||||

|

Revenues by region (origin) |

||||||||||||

|

United States and Canada |

$ | 1,168,523 | $ | 606,472 | $ | 647,966 | ||||||

|

Europe |

756,013 | 806,540 | 916,288 | |||||||||

|

Other |

334,735 | 274,435 | 345,359 | |||||||||

|

Total revenues |

$ | 2,259,271 | $ | 1,687,447 | $ | 1,909,613 | ||||||

Revenues

Revenues increased 34%, or $571.8 million in 2010, compared with 2009. Consolidated foreign currency fluctuations were minor in 2010, compared with 2009. Revenues decreased 12%, or $222.2 million, in 2009, compared with 2008. A strengthening U.S. dollar against most foreign currencies accounted for 46% of the decrease in 2009 revenues. A more detailed analysis of these fluctuations is provided in Operating Segment Results .

One customer, Southern California Edison of our Itron North America operating segment, represented 11% of total Company revenues for the year ended December 31, 2010. No single customer represented more than 10% of total revenues for the years ended December 31, 2009 and 2008. Our 10 largest customers accounted for approximately 34%, 17%, and 15% of total revenues in 2010, 2009, and 2008.

Gross Margins

Gross margin was 30.9% in 2010, compared with 31.9% in 2009. While gross margins decreased for both operating segments in 2010, the growth in Itron North America’s revenues, which are at higher average margins compared with Itron

17

Table of Contents

International, moderated the decline in the consolidated margin. Approximately two-thirds of the two percentage point decline in gross margin in 2009, compared with 2008, was due to our North America operations and one-third was attributable to our International operations. A more detailed analysis of these fluctuations is provided in Operating Segment Results.

Meter and Module Summary

Meters can be broken down into three categories:

| • |

Standard metering – no built-in remote reading communication capability |

| • |

Advanced metering – one-way communication of meter data |

| • |

Smart metering – two-way communication including remote meter configuration and upgrade (consisting primarily of our OpenWay ® technology) |

In addition, advanced and smart meter communication modules can be sold separately from the meter. Depending on customers’ preferences, we also incorporate other vendors’ technology in our meters. A summary of our meter and communication module shipments is as follows:

| Year Ended December 31, | ||||||||||||

| 2010 | 2009 | 2008 | ||||||||||

| (units in thousands) | ||||||||||||

|

Total meters (standard, advanced, and smart) |

||||||||||||

|

Itron North America |

||||||||||||

|

Electricity |

6,940 | 3,480 | 4,800 | |||||||||

|

Gas |

510 | 350 | 390 | |||||||||

|

Itron International |

||||||||||||

|

Electricity |

7,870 | 7,790 | 7,840 | |||||||||

|

Gas |

4,020 | 4,980 | 5,400 | |||||||||

|

Water |

9,110 | 8,430 | 9,170 | |||||||||

|

Total meters |

28,450 | 25,030 | 27,600 | |||||||||

|

Additional meter information (Total Company) |

||||||||||||

|

Advanced meters |

3,980 | 3,110 | 4,690 | |||||||||

|

Smart meters |

4,460 | 710 | 20 | |||||||||

|

Standalone advanced and smart communication modules |

5,960 | 3,830 | 4,890 | |||||||||

|

Advanced and smart meters and communication modules |

14,400 | 7,650 | 9,600 | |||||||||

|

Meters with other vendors’ advanced or smart communication modules |

510 | 630 | 840 | |||||||||

18

Table of Contents

Operating Segment Results

For a description of our operating segments, refer to Item 8: “Financial Statements and Supplementary Data, Note 15: Segment Information” in this Annual Report on Form 10-K. The following tables and discussion highlight significant changes in trends or components of each operating segment.

| Year Ended December 31, | ||||||||||||||||

| 2010 | % Change | 2009 | % Change | 2008 | ||||||||||||

| (in thousands) | (in thousands) | (in thousands) | ||||||||||||||

|

Segment Revenues |

||||||||||||||||

|

Itron North America |

$ | 1,177,391 | 91% | $ | 615,731 | (12%) | $ | 696,688 | ||||||||

|

Itron International |

1,081,880 | 1% | 1,071,716 | (12%) | 1,212,925 | |||||||||||

|

Total revenues |

$ | 2,259,271 | 34% | $ | 1,687,447 | (12%) | $ | 1,909,613 | ||||||||

| Year Ended December 31, | ||||||||||||||||||||||||

| 2010 | 2009 | 2008 | ||||||||||||||||||||||

| Gross Profit | Gross Margin | Gross Profit | Gross Margin | Gross Profit | Gross Margin | |||||||||||||||||||

|