INVENTRUST PROPERTIES CORP.

10-Ks and 10-Qs

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

WASHINGTON, D.C. 20549

FORM 10-K

|

x

|

ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934

|

|

FOR THE FISCAL YEAR ENDED DECEMBER 31, 2012

|

|

|

¨

|

TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934

|

|

FOR THE TRANSITION PERIOD FROM TO

|

|

COMMISSION FILE NUMBER: 000-51609

Inland American Real Estate Trust, Inc.

(Exact name of registrant as specified in its charter)

|

Maryland

|

|

34-2019608

|

|

(State or other jurisdiction of

incorporation or organization)

|

|

(I.R.S. Employer

Identification No.)

|

|

2901 Butterfield Road, Oak Brook, Illinois

|

|

60523

|

|

(Address of principal executive offices)

|

|

(Zip Code)

|

630-218-8000

(Registrant’s telephone number, including area code)

Securities registered pursuant to Section 12(b) of the Act:

None

Securities registered pursuant to Section 12(g) of the Act:

Common stock, $0.001 par value per share

(Title of Class)

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. Yes

¨

No

x

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Act. Yes

¨

No

x

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to the filing requirements for the past 90 days. Yes

x

No

¨

Indicate by check mark whether the Registrant has submitted electronically and posted on its corporate website, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T (§232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files). Yes

x

No

¨

Indicate by check mark if disclosure of delinquent filers pursuant to Item 405 of Regulation S-K is not contained herein, and will not be contained, to the best of registrant’s knowledge, in definitive proxy or information statements incorporated by reference in Part III of this Form 10-K or any amendment to this Form 10-K.

x

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer or a smaller reporting company. (See definitions of “large accelerated filer,” “accelerated filer” and “smaller reporting company” in Rule 12b-2 of the Exchange Act).

|

Large accelerated filer

|

¨

|

|

Accelerated filer

|

¨

|

|

Non-accelerated filer

|

x

|

|

Smaller reporting company

|

¨

|

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act). Yes

¨

No

x

There is no established market for the registrant’s shares of common stock. The aggregate market value of the registrant’s common stock held by non-affiliates of the registrant as of June 30, 2012 (the last business day of the registrant’s most recently completed second quarter) was approximately $6,327,641,846, based on the estimated per share value of $7.22, as established by the registrant on December 29, 2011.

As of March 1, 2013, there were 892,531,979 shares of the registrant’s common stock outstanding.

INLAND AMERICAN REAL ESTATE TRUST, INC.

TABLE OF CONTENTS

|

|

|

Page

|

|

Item 1.

|

||

|

Item 1A.

|

||

|

Item 1B.

|

||

|

Item 2.

|

||

|

Item 3.

|

||

|

Item 4.

|

||

|

Item 5.

|

||

|

Item 6.

|

||

|

Item 7.

|

||

|

Item 7A.

|

||

|

Item 8.

|

||

|

Item 9.

|

||

|

Item 9A.

|

||

|

Item 9B.

|

||

|

Item 10.

|

||

|

Item 11.

|

||

|

Item 12.

|

||

|

Item 13.

|

||

|

Item 14.

|

||

|

Item 15.

|

||

This Annual Report on Form 10-K includes references to certain trademarks. Courtyard by Marriott

®

, Marriott

®

, Marriott Suites

®

, Residence Inn by Marriott

®

and SpringHill Suites by Marriott

®

trademarks are the property of Marriott International, Inc. (“Marriott”) or one of its affiliates. Doubletree

®

, Embassy Suites

®

, Hampton Inn

®

, Hilton Garden Inn

®

, Hilton Hotels

®

and Homewood Suites by Hilton

®

trademarks are the property of Hilton Hotels Corporation (“Hilton”) or one or more of its affiliates. Hyatt Place

®

trademark is the property of Hyatt Corporation (“Hyatt”). Intercontinental Hotels

®

trademark is the property of IHG. Wyndham

®

and Baymont Inn & Suites

®

trademarks are the property of Wyndham Worldwide. Comfort Inn

®

trademark is the property of Choice Hotels International. Fairmont Hotels and Resorts is a trademark. The Aloft service name is the property of Starwood. For convenience, the applicable trademark or service mark symbol has been omitted but will be deemed to be included wherever the above-referenced terms are used.

General

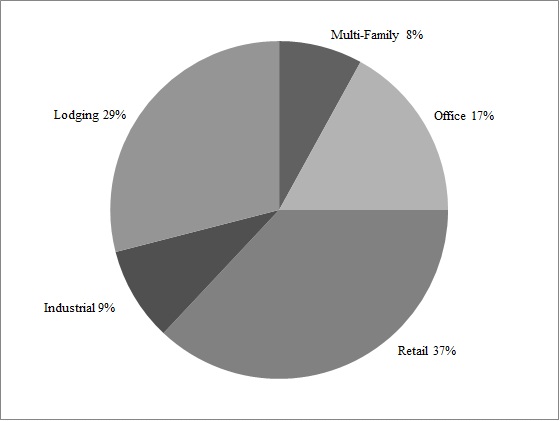

Inland American Real Estate Trust, Inc., a Maryland corporation, was incorporated in October 2004. We have elected to be taxed, and currently qualify, as a real estate investment trust (“REIT”) for federal tax purposes. We acquire, own, operate and develop a diversified portfolio of commercial real estate, including retail, multi-family, industrial, lodging, and office properties, located in the United States. In addition, we own assets through joint ventures in which we do not own a controlling interest, as well as properties in development. We also invest in marketable securities and other assets.

As of

December 31, 2012

, our portfolio was comprised of

794

properties representing 45.6 million square feet of retail, office and industrial space,

5,311

multi-family units,

5,212

student housing beds and

16,345

hotel rooms. We believe that a diversified portfolio balances our risk exposure compared to a portfolio with a single asset class. During the economic recession and ongoing sluggish recovery, we believe that a diversified portfolio like ours provides our stockholders with significant benefits and reduces their risk relative to a portfolio concentrated on one property sector or properties located in one geographical area or region. Because we believe that most real estate markets are cyclical in nature, we plan to maintain our diversified portfolio but focus on three specific real estate segments, lodging, student housing and multi-tenant retail. We believe our diversity and size will allow us to continue to effectively deploy capital into sectors and locations where the underlying investment fundamentals are relatively strong. The following chart depicts the allocation of our real estate assets for each segment, as of

December 31, 2012

, based on undepreciated assets within our property portfolio.

Strategy and Objectives

We have defined our long-term portfolio strategy by focusing our diversified assets in three specific real estate asset classes - retail, lodging and student housing. We believe this strategy presents the best opportunity to capitalize on current market trends in commercial real estate and realize income growth in these sectors. A key outcome of our strategy will be an opportunity to explore multiple liquidity events by segment.

Also part of our strategy is to improve the overall quality of our retail, lodging and student housing segments for long-term growth through selective asset acquisition and sales. We continue to use our expertise to capitalize on opportunities in the real estate industry. We believe our capacity to identify and react to investment opportunities is one of our biggest strengths. This strategy will take time as we dispose of less strategic assets and rotate capital into our targeted segments. Our focus has been, and will continue to be, maximizing stockholder value over the long-term.

During the execution of our strategy, we will focus on maintaining a stable income stream to provide a sustainable monthly distribution to our shareholders.

1

Our three objectives in the execution of our strategy are:

|

•

|

Sustaining a monthly stockholder distribution while maintaining capital preservation

|

|

•

|

Tailoring our portfolio to lodging, student housing and retail by expanding and enhancing these growth portfolios

|

|

•

|

Positioning for stockholder liquidity through multiple liquidity events by segment type

|

2012 Highlights

Distributions

We have paid a monthly cash distribution to our stockholders which totaled in the aggregate

$439.2 million

for the year ended

December 31, 2012

, which was equal to $0.50 per share for 2012, assuming that a share was outstanding the entire year. The distributions paid for the year ended

December 31, 2012

were funded from cash flow from operations, distributions from unconsolidated joint ventures and gains on sale of properties.

Investing Activities

Our acquisition and disposition activities in 2012 highlight our move to divesting of less strategic assets and redeploying the capital into our long-term strategic segments, lodging, student housing and multi-tenant retail. We acquired seven upper upscale lodging properties consisting of 2,624 rooms for $525.1 million. We acquired two student housing properties and placed two student housing properties into service for a total of 2,566 beds for $171.9 million. In addition, we acquired two multi-tenant retail properties and expanded two existing multi-tenant retail properties consisting of 554,026 square feet for $106.9 million. As part of our strategy to realign our asset segments with higher performing assets, we sold

166

properties for a gross disposition price of

$603.5 million

, including 143 bank branches (142 retail branches and one office branch), four retail properties, thirteen midscale lodging properties, two industrial properties, and four multi-family properties.

Financing Activities

We successfully refinanced our 2012 maturities of approximately $671.4 million and placed debt on new and existing properties. We were able to obtain favorable rates while still maintaining a manageable debt maturity schedule for future years. As of

December 31, 2012

, we had mortgage debt of approximately

$5.9

billion and have a weighted average interest rate of

5.1%

per annum. Our debt maturities for 2013 are

$882.9 million

.

Operating Results

We experienced organic growth in our lodging and multi-family segments as our same store net operating income results increased

6.7%

and

9.2%

, respectively, from the year ended

December 31, 2011

to 2012. These increases are due to high occupancy and RevPAR and rental rate increases, in the lodging and multi-family segments, respectively. Our retail and industrial segments improved slightly due to maintaining occupancy rates and contractual rental rates. Our office segment remained unchanged as compared to the prior year with a stable occupancy rate.

The following table represents our same store net operating income for the years ended

December 31, 2012 and 2011

. Net operating income is calculated in Item 7 of this Annual Report on Form 10-K.

|

2012 Net

operating

income

|

2011 Net

operating

income

|

Increase

(decrease)

|

Increase

(decrease)

|

Economic

Occupancy

as of

December 31,

2012

|

Economic

Occupancy

as of

December 31,

2011

|

|||||||||||||||

|

Retail

|

$

|

254,082

|

|

$

|

250,385

|

|

$

|

3,697

|

|

1.5

|

%

|

93

|

%

|

94

|

%

|

|||||

|

Lodging

|

169,532

|

|

158,817

|

|

10,715

|

|

6.7

|

%

|

73

|

%

|

72

|

%

|

||||||||

|

Office

|

132,229

|

|

132,050

|

|

179

|

|

0.1

|

%

|

93

|

%

|

93

|

%

|

||||||||

|

Industrial

|

77,094

|

|

75,988

|

|

1,106

|

|

1.5

|

%

|

97

|

%

|

98

|

%

|

||||||||

|

Multi-family

|

46,949

|

|

42,984

|

|

3,965

|

|

9.2

|

%

|

93

|

%

|

93

|

%

|

||||||||

|

$

|

679,886

|

|

$

|

660,224

|

|

$

|

19,662

|

|

3.0

|

%

|

||||||||||

In 2013, we expect similar increases in operating results compared to 2012 in our lodging and multi-family portfolios due to the growth projected in these segments. As occupancy rates increase close to peak levels in lodging and multi-family, the ability to increase rooms rates and rental rates, respectively, will help grow our revenue for each segment in 2013. We believe that our

2

stable occupancy in our retail, office, and industrial portfolios will result in consistent operating performances in these segments.

Effective July 1, 2012, the Company entered into new master management agreements with its property managers, and the subsidiaries of the Company that directly own its properties entered into new property management agreements with the property managers. Each agreement has an initial term ending December 31, 2013, which term will automatically be renewed until June 30, 2015 unless either party to the agreement provides written notice of cancellation before June 30, 2013. Under the agreements, the Company will pay the property managers monthly management fees by property type, as follows: (i) for any bank branch facility (office or retail), 2.50% of the gross income generated by the property; (ii) for any multi-tenant industrial property, 4.00% of the gross income generated by the property; (iii) for any multi-family property, 3.75% of the gross income generated by the property; (iv) for any multi-tenant office property, 3.75% of the gross income generated by the property; (v) for any multi-tenant retail property, 4.50% of the gross income generated by the property; (vi) for any single-tenant industrial property, 2.25% of the gross income generated by the property; (vii) for any single-tenant office property, 2.90% of the gross income generated by the property; and (viii) for any single-tenant retail property, 2.90% of the gross income generated by the property.

Segment Data

We have five business segments: Retail, Lodging, Office, Industrial, and Multi-family. We evaluate segment performance primarily based on net operating income. Net operating income of the segments does not include interest expense, depreciation and amortization, general and administrative expenses, or interest and other investment income from corporate investments. The non-segmented assets include our cash and cash equivalents, investment in marketable securities, construction in progress, and investment in unconsolidated entities. Information related to our business segments, including a measure of profits or loss and revenues from external customers for each of the last three fiscal years and total assets for each of the last two fiscal years, is set forth in Note 14 to our consolidated financial statements in Item 8 of this Annual Report on Form 10-K.

Significant Tenants

For the year ended

December 31, 2012

, we generated more than 18% of our rental revenue (excluding lodging, multi-family, and development properties) from two tenants, SunTrust Banks, Inc. and AT&T, Inc. SunTrust Banks, Inc. leases multiple properties that we own and that are located throughout the United States. These properties collectively generated approximately 10% of our rental revenue for the year ended

December 31, 2012

. For the year ended

December 31, 2012

, approximately 8% of our rental revenue was generated by three properties leased to AT&T, Inc.

Tax Status

We have elected to be taxed as a REIT, under Sections 856 through 860 of the Internal Revenue Code of 1986 as amended (the “Code”) beginning with the tax year ended December 31, 2005. Because we qualify for taxation as a REIT, we generally will not be subject to federal income tax on taxable income that is distributed to stockholders. If we fail to qualify as a REIT in any taxable year, without the benefit of certain relief provisions, we will be subject to federal and state income tax on our taxable income at regular corporate rates. Even if we qualify for taxation as a REIT, we may be subject to certain state and local taxes on our income, property or net worth, respectively, and to Federal income and excise taxes on our undistributed income.

Competition

The commercial real estate market is highly competitive. We compete for tenants in all of our markets with other owners and operators of commercial properties. We compete based on a number of factors that include location, rental rates, security, suitability of the property’s design to tenants’ needs and the manner in which the property is operated and marketed. The number of competing properties in a particular market could have a material effect on a property’s occupancy levels, rental rates and operating income.

We compete with many third parties engaged in real estate investment activities including other REITs, including other REITs sponsored by our sponsor, specialty finance companies, savings and loan associations, banks, mortgage bankers, insurance companies, mutual funds, institutional investors, investment banking firms, lenders, hedge funds, governmental bodies and other entities. There are also other REITs with investment objectives similar to ours and others may be organized in the future. In addition, these same entities seek financing through the same channels that we do. Therefore, we compete for funding in a market where funds for real estate investment may decrease, or grow less than the underlying demand.

3

Employees

As of

December 31, 2012

, we have 88 full-time individuals employed primarily by our multi-family subsidiaries.

We do not employ our executive officers and they do not receive any compensation from us for their services as such officers. Our executive officers are officers of one or more of The Inland Group, Inc.’s affiliated entities, including our business manager, and are compensated by these entities, in part, for their services rendered to us. We do not reimburse the business manager for any compensation paid to persons serving as one of our executive officers or as an executive officer of the business manger or property managers. For the purposes of reimbursement, our secretary is not considered an “executive officer.”

We have entered into a business management agreement with Inland American Business Manager & Advisor, Inc. pursuant to which it serves as our business manager, with responsibility for overseeing and managing our day-to-day operations. We have also entered into property management agreements with each of our property managers. We pay fees to our business manager and our property managers in consideration for the services they perform for us pursuant to these agreements. Except as noted above, we also reimburse these entities for the expenses they incur in performing services for us including the compensation expenses for persons providing services to us.

Conflicts of Interest

Our governing documents require a majority of our directors to be independent. Further, any transactions between The Inland Group, Inc. or its affiliates, including our business manager and property managers, and us must be approved by a majority of our independent directors.

Environmental Matters

Compliance with federal, state and local environmental laws has not had a material adverse effect on our business, assets, or results of operations, financial condition and ability to pay distributions, and we do not believe that our existing portfolio will require us to incur material expenditures to comply with these laws and regulations. However, we cannot predict the impact of unforeseen environmental contingencies or new or changed laws or regulations on our properties.

Seasonality

The lodging segment is seasonal in nature, reflecting higher revenue and operating income during the second and third quarters. This seasonality can be expected to cause fluctuations in our net operating income for the lodging segment. None of our other segments are seasonal in nature.

Access to Company Information

We electronically file our Annual Report on Form 10-K, Quarterly Reports on Form 10-Q, Current Reports on Form 8-K and all amendments to those reports with the Securities and Exchange Commission (“SEC”). The public may read and copy any of the reports that are filed with the SEC at the SEC’s Public Reference Room at 100 F Street, NE, Washington, DC 20549. The public may obtain information on the operation of the Public Reference Room by calling the SEC at (800)-SEC-0330. The SEC maintains an Internet site at www.sec.gov that contains reports, proxy and information statements and other information regarding issuers that file electronically.

We make available, free of charge, by responding to requests addressed to our customer relations group, the Annual Report on Form 10-K, Quarterly Reports on Form 10-Q, Current Reports on Form 8-K and all amendments to those reports on our website, www.inland-american.com. These reports are available as soon as reasonably practicable after such material is electronically filed or furnished to the SEC.

Certifications

We have filed with the Securities and Exchange Commission the principal executive officer and principal financial officer certifications required pursuant to Section 302 of the Sarbanes-Oxley Act of 2002, which are attached as Exhibits 31.1 and 31.2 to this Annual Report on Form 10-K.

4

The occurrence of any of the risks discussed below could have a material adverse effect on our business, financial condition, results of operations and ability to pay distributions to our stockholders.

Risks Related to Our Business

Disruptions in the financial markets or economic conditions could adversely affect our ability to refinance or secure additional debt financing at attractive terms

Credit markets are subject to rapid changes from macro economic factors, including rising interest rates, perceptions of the overall health in the US economy and real estate in particular, and the health and regulatory environment in which our lenders operate and the overall availability of lending sources.

In addition, disruptions in the financial markets or economic conditions may negatively impact commercial real estate fundamentals which could have various negative impacts on the value of our investments including:

|

•

|

a decrease in the values of our investments in commercial properties, below the amounts paid for these investments; or

|

|

•

|

a decrease in revenues from our properties, due to lower occupancy and rental rates, which may make it more difficult for us to pay distributions or meet our debt service obligations on debt financing.

|

Our ongoing strategy depends, in part, upon future acquisitions, and we may not be successful in identifying and consummating these transactions

.

Our long-term business strategic plan is to refine our diversified portfolio of assets and to focus on the retail, lodging, and student housing sectors. As we continue to execute on this strategy, we will rotate capital out of our other asset classes - such as multi-family, office and industrial - to enhance and expand our strategic holdings. There is no assurance we will be able to sell assets at acceptable prices or identify suitable replacement assets on satisfactory terms, if at all. We may also face delays in reinvesting net sales proceeds in new assets which would impact the return we earn on our assets.

We face significant competition for attractive investment opportunities from an indeterminate number of other real estate investors, including investors with significant capital resources such as domestic and foreign corporations and financial institutions, publicly traded and privately held REITs, private institutional investment funds, investment banking firms, life insurance companies and pension funds. As a result of competition, we may be unable to acquire additional properties as we desire or the purchase price may be significantly elevated.

In light of current market conditions and real estate values, we may face significant competition to acquire stabilized properties, or have to accept lease-up risk associated with properties that have lower occupancy. As market conditions and real estate values recover, more properties may become available for acquisition, but we can provide no assurances that these properties will meet our investment objectives or that we will be successful in acquiring these properties. If we are unable to acquire sufficient debt financing at suitable rates or at all, we may be unable to acquire as many additional properties as we anticipate.

Our ongoing strategy involves the disposition of properties; however, we may be unable to sell a property at acceptable terms and conditions, if at all.

As we execute on our long-term strategy we will rotate capital out of certain asset classes, such as multi-family, office and industrial to reinvest into retail, lodging or student housing. Besides executing on our strategy, it may make economic sense to sell properties in any asset class when we believe the value of the leases in place at a property will significantly decline over the remaining lease term, or when the property has limited or no equity with a near-term debt maturity, or when a property has equity but the projected returns do not justify further investment, or when the equity in a property can be redeployed in the portfolio in order to achieve better returns or strategic goals. As we engage to sell these properties, general economic conditions along with property specific issues, such as vacancies, lease terminations and debt defeasance, may negatively affect the value of our properties and therefore reducing our return on the investment or prevent us from selling the property on acceptable terms. Real estate investments often cannot be sold quickly. As a result economic conditions may prevent potential purchasers from obtaining financing on acceptable terms, if at all, thereby delaying our ability to sell our properties.

5

We are the subject of an ongoing investigation by the SEC and have received two related derivative demands by stockholders to conduct investigations. The SEC's investigation, the derivative demands, or both could have a material adverse impact on our business.

We have learned that the SEC is conducting a non-public, formal, fact-finding investigation (the “Investigation”) to determine whether there have been violations of certain provisions of the federal securities laws related to the business management fees, property management fees, transactions with affiliates, timing and amount of distributions paid to investors, determination of property impairments, and any decision regarding whether the Company might become a self-administered REIT.

Our business manager offered to the extent allowed by law or governmental regulation to reduce its business management fee in an aggregate amount necessary to reimburse us for any costs, fees, fines, or assessments, if any, that we may incur as a result of the pending Investigation, other than legal fees incurred by us or fees and costs otherwise covered by insurance. The business manager also offered to waive its reimbursement of legal fees or costs that the business manager incurs in connection with the Investigation. In the event that the business management agreement is terminated or expires in accordance with its terms prior to the conclusion of the pending Investigation or prior to us realizing the full benefit of the business manager's offer to reduce its business management fee in the event that we realize costs, fees, fines or assessments in connection with the Investigation, then we will be required to pay any such costs, fees, fines or assessments. In the event of a termination of the business management agreement, we may not be able to execute our business plan and may suffer losses, which could materially decrease cash available for distribution to our stockholders and have a material adverse impact on our business and financial condition.

We have also received two related demands (“Derivative Demands”) by stockholders to conduct investigations regarding claims that the officers, the board of directors, the business manager, and the affiliates of the business manager (the “Inland American Parties”) breached their fiduciary duties to us in connection with the matters that we disclosed are subject to the Investigation. The first demand claims that the Inland American Parties (i) falsely reported the value of our common stock until September 2010; (ii) caused us to purchase shares of our common stock from stockholders at prices in excess of their value; and (iii) disguised returns of capital paid to stockholders as REIT income resulting in the payment of fees to the business manager for which it was not entitled. The three stockholders in that demand contend that legal proceedings should seek recovery of damages in an unspecified amount allegedly sustained by us. The second demand by another shareholder makes similar claims and further alleges that the Inland American Parties (i) caused us to engage in transactions that unduly favored related parties, (ii) falsely disclosed the timing and amount of distributions, and (iii) falsely disclosed whether we might become a self-administered REIT. A special litigation committee has been formed by the board to investigate the matters related to the Investigation and the Derivative Demands. That investigation is ongoing.

We cannot reasonably estimate the timing or outcome of either the Investigation or the investigation by the special litigation committee, nor can we predict whether or not any of these items may have a material adverse effect on our business. These items may cause us to incur significant legal expense, both directly and as the result of any indemnification obligations. In addition, the Investigation and the Derivative Demands may also divert management's attention from our ordinary business operations or may also limit our ability to obtain financing to fund our on-going operating requirements, which could cause our business to suffer. Adverse findings by the SEC or the special litigation committee, future litigation related thereto, or the incurrence of costs, fees, fines or penalties that are not reimbursed by our business manager by reducing its business management fee or reimbursed by insurance policies, could have a material adverse impact on our business.

We depend on our business manager and our property managers and may not find a suitable replacement if our business management agreement or the property management agreements are terminated.

Most of our officers and our staff are employees of the business manager. We rely on our business manager and our property managers, to design and implement our operating policies and strategies. The agreement with the business manager is terminable upon 60 days' notice by either party or whose term expires July 31, 2013

.

The agreement with the property manager has a term until December 31, 2013 and will extend for an additional eighteen months unless terminated on or before June 30, 2013.

If we, or they, terminate the agreements

,

or permit them to expire in accordance with their terms, we may not be able to execute our business plan and may suffer losses.

If we lose or are unable to obtain key personnel, our ability to implement our investment strategies could be delayed or hindered.

Our success depends to a significant degree upon the contributions of our executive officers and other key personnel of our business manager and property managers. If any of the key personnel of our business manager or property managers were to cease their

6

affiliation with our business manager or property managers, respectively, our operating results could suffer. Further, we do not separately maintain “key person” life insurance that would provide us with proceeds in the event of death or disability of these persons. We believe our future success depends, in part, upon the ability of our business manager and property managers to hire and retain highly skilled managerial, operational and marketing personnel. Competition for such personnel is intense, and we cannot assure you that our business manager or property managers will be successful in attracting and retaining skilled personnel.

We may internalize or partially internalize our management functions and your interests could be diluted.

We may internalize some or all of the functions performed for us by our business manager and/or property managers and the method by which we could internalize these functions could take many forms. For example, we could acquire the business manager and/or property managers through a merger or by purchasing their stock or assets and the consideration we would pay may be cash, shares of our common stock or promissory notes. Issuing shares of common stock would reduce the percentage ownership of our existing stockholders and issuing notes or incurring debt could reduce our cash flow from operating activities or our ability to borrow additional funds.

Internalization transactions involving the acquisition of advisors affiliated with entity sponsors have also, in some cases, been the subject of litigation. Even if these claims are without merit, we could be forced to spend significant amounts of money defending claims.

If we internalize some or all of our management functions, the nature of our costs will change.

If we internalize our management functions, we will likely become directly responsible for the expenses currently paid by the business manager or property manager. Although we currently reimburse our business manager and property managers for most of the general and administrative expenses they incur on our behalf, we cannot be certain that once we internalize these functions our costs will not be higher than the amounts would be if we did not internalize. Further, although we would no longer be required to pay fees for the functions that are internalized, we would expect to incur additional compensation and benefits costs of our officers that are now paid by our business manager and its affiliates and which we do not reimburse. We may also issue equity awards to officers, employees and consultants. Although we would expect that the total compensation and benefits paid to our executive officers will be less than the fees we no longer would have to pay, there is no assurance of this outcome.

If we internalize some or all of our management functions, we could have difficulty integrating these functions as a stand-alone entity, and we may fail to properly identify the appropriate mix of personnel and capital needs to operate as a stand-alone entity. An inability to manage an internalization transaction effectively could, therefore, result in our incurring additional costs and/or experiencing other difficulties. Such difficulties could cause us to incur additional costs, and our management's attention could be diverted from most effectively managing our business and properties.

There is no assurance that we will reach an agreement with our business manager or property managers on the terms of an internalization transaction.

Our business manager and property managers are not obligated to enter into an internalization transaction with us or to do so at any particular price. Our independent directors, as a whole, or a committee thereof, would have to negotiate the specific terms and conditions of any agreement or agreements to acquire these entities, including the actual purchase price. There is no assurance that we will be able to enter into an agreement with the business manager and/or property managers on mutually acceptable terms and in that case, we would have to seek alternative courses of actions to internalize our management functions.

If we seek to internalize our management functions, other than by acquiring our business manager and/or property managers, we could incur greater costs and lose key personnel.

We may decide to pursue an internalization by hiring our own group of executives and other employees or entering into an agreement with a third party, such as a merger, instead of by acquiring our business manager and property managers. The costs that we would incur in this case are uncertain and may be substantial. In addition, certain key personnel of the business manager and/or property managers have employment agreements with those entities, which could restrict our ability to retain such personnel if we do not acquire the business manager and property managers. Further, we would lose the benefit of the experience of the business manager and property managers.

7

The failure of any bank in which we deposit our funds could reduce the amount of cash we have available to pay distributions and make additional investments.

We have deposited our cash and cash equivalents in several banking institutions in an attempt to minimize exposure to the failure or takeover of any one of these entities. However, the Federal Insurance Deposit Corporation, or “FDIC,” generally only insures limited amounts per depositor per insured bank. At December 31, 2012 we had cash and cash equivalents and restricted cash deposited in interest bearing transaction accounts at certain financial institutions exceeding these federally insured levels. If any of the banking institutions in which we have deposited funds ultimately fails, we may lose our deposits over the federally insured levels. The loss of our deposits could reduce the amount of cash we have available to distribute or invest.

Risks Related to our Real Estate Assets

There are inherent risks with real estate investments.

Investments in real estate assets are subject to varying degrees of risk. For example, an investment in real estate cannot generally be quickly converted to cash, limiting our ability to promptly vary our portfolio in response to changing economic, financial and investment conditions. Investments in real estate assets also are subject to adverse changes in general economic conditions which, for example, reduce the demand for rental space.

Among the factors that could impact our real estate assets and the value of an investment in us are:

|

•

|

local conditions such as an oversupply of space or reduced demand for real estate assets of the type that we own or seek to acquire, including, with respect to our lodging facilities, quick changes in supply of and demand for rooms that are rented or leased on a day-to-day basis;

|

|

•

|

inability to collect rent from tenants;

|

|

•

|

vacancies or inability to rent space on favorable terms;

|

|

•

|

inflation and other increases in operating costs, including insurance premiums, utilities and real estate taxes;

|

|

•

|

increases in energy costs or airline fares or terrorist incidents which impact the propensity of people to travel and therefore impact revenues from our lodging facilities, although operating costs cannot be adjusted as quickly;

|

|

•

|

adverse changes in the federal, state or local laws and regulations applicable to us, including those affecting rents, zoning, prices of goods, fuel and energy consumption, water and environmental restrictions;

|

|

•

|

the relative illiquidity of real estate investments;

|

|

•

|

changing market demographics;

|

|

•

|

an inability to acquire and finance, or refinance, properties on favorable terms, if at all;

|

|

•

|

acts of God, such as earthquakes, floods or other uninsured losses;

|

|

•

|

changes or increases in interest rates and availability of financing locally or world-wide.

|

In addition, periods of economic slowdown or recession, or declining demand for real estate, or the public perception that any of these events may occur, could result in a general decline in rents or increased defaults under existing leases. We have experienced these impacts in the last few years. There is no assurance that conditions will improve or that these impacts will not occur in the future.

We depend on tenants for our revenue, and accordingly, lease terminations, tenant default, and bankruptcies could adversely affect the income produced by our properties.

The success of our investments depends on the financial stability of our tenants. Certain economic conditions may adversely affect one or more of our tenants. For example, business failures and downsizings can affect the tenants of our office and industrial properties. Reduced consumer demand for retail products and services may affect the tenants of our retail properties. In addition, our retail shopping center properties typically are anchored by large, nationally recognized tenants, any of which may experience a downturn in their business that may weaken significantly their financial condition. Further, mergers or consolidations among large retail establishments could result in the closure of existing stores or duplicate or geographically overlapping store locations, which could include tenants at our retail properties.

As a result of these factors, our tenants may delay lease commencements, decline to extend or renew their leases upon expiration, fail to make rental payments when due, or declare bankruptcy. Any of these actions could result in the termination of the tenants' leases, the expiration of existing leases without renewal, or the loss of rental income attributable to the terminated or expired leases. In the event of a tenant default or bankruptcy, we may experience delays in enforcing our rights as a landlord and may incur substantial costs in protecting our investment and re-leasing our property. Specifically, a bankruptcy filing by, or relating to, one of our tenants or a lease guarantor would bar efforts by us to collect pre-bankruptcy debts from that tenant or lease guarantor,

8

or its property, unless we receive an order permitting us to do so from the bankruptcy court. In addition, we cannot evict a tenant solely because of bankruptcy. The bankruptcy of a tenant or lease guarantor could delay our efforts to collect past due balances under the relevant leases, and could ultimately preclude collection of these sums. If a lease is assumed by the tenant in bankruptcy, all pre-bankruptcy balances due under the lease must be paid to us in full. If, however, a lease is rejected by a tenant in bankruptcy, we would have only a general, unsecured claim for damages. An unsecured claim would only be paid to the extent that funds are available and only in the same percentage as is paid to all other holders of general, unsecured claims. Restrictions under the bankruptcy laws further limit the amount of any other claims that we can make if a lease is rejected. As a result, it is likely that we would recover substantially less than the full value of the remaining rent during the term.

Geographic concentration also exposes us to risks of oversupply and competition in these markets. Significant increases in the supply of certain property types, including hotels, without corresponding increases in demand could have a material adverse effect on our financial condition, results of operations and our ability to pay distributions.

As of December 31, 2012, approximately, 4%, 5%, 7% and 12% of our base rental income of our consolidated portfolio, excluding our lodging facilities, was generated by a certain property located in the Minneapolis, Dallas, Chicago and Houston metropolitan areas, respectively. Additionally, at December 31, 2012, forty-four of our lodging facilities, or approximately 50% of our lodging portfolio, were located in Washington D.C. and the ten eastern seaboard states ranging from Connecticut to Florida, including seven hotels in North Carolina and seventeen properties in Texas.

Two of our tenants generated a significant portion of our revenue, and rental payment defaults by these significant tenants could adversely affect our results of operations.

For the year ended December 31, 2012, approximately 10% of our rental revenue was generated by over 400 retail banking properties leased to SunTrust Banks, Inc.. Also, for the year ended December 31, 2012, approximately 8% of our rental revenue was generated by three properties leased to AT&T, Inc. The leases for two of the AT&T properties, with approximately 1.7 million and 1.5 million square feet, expire in 2016 and 2017, respectively. As a result of the concentration of revenue generated from these properties, if either SunTrust or AT&T were to cease paying rent or fulfilling its other monetary obligations, we could have significantly reduced rental revenues or higher expenses until the defaults were cured or the properties were leased to a new tenant or tenants.

Leases representing approximately 5.8% of the rentable square feet of our retail, office, and industrial portfolio are scheduled to expire in 2013. We may be unable to renew leases or lease vacant space at favorable rates or at all.

As of December 31, 2012, leases representing approximately 5.8% of the 45,552,250 rentable square feet of our retail, office, and industrial portfolio were scheduled to expire in 2013 and an additional 5.9% of the square footage of our retail, office, and industrial portfolio was available for lease. We may be unable to extend or renew any of these leases, or we may be able to lease these spaces only at rental rates equal to or below existing rental rates. In addition, some of our tenants have leases that include early termination provisions that permit the lessee to terminate all or a portion of its lease with us after a specified date or upon the occurrence of certain events with little or no liability to us. We may be required to offer substantial rent abatements, tenant improvements, early termination rights or below-market renewal options to retain these tenants or attract new ones. Portions of our properties may remain vacant for extended periods of time. Further, some of our leases currently provide tenants with options to renew the terms of their leases at rates that are less than the current market rate or to terminate their leases prior to the expiration date thereof. If we are unable to obtain new rental rates that are on average comparable to our asking rents across our portfolio, then our ability to generate cash flow growth will be negatively impacted.

We may be required to make significant capital expenditures to improve our properties in order to retain and attract tenants.

We expect that, upon the expiration of leases at our properties, we may be required to provide rent or other concessions to tenants, accommodate requests for renovations, build-to-suit remodeling and other improvements or provide additional services to our tenants. As a result, we may have to pay for significant leasing costs or tenant improvements in order to retain tenants whose leases are expiring and to attract new tenants in sufficient numbers. Additionally, we may need to raise capital to fund these expenditures. If we are unable to do so, or if capital is otherwise unavailable, we may be unable to fund the required expenditures. This could result in non-renewals by tenants upon expiration of their leases or the ability to attract new tenants, which would result in declines in revenues from operations.

9

We face significant competition in the leasing market, which may decrease or prevent increases in the occupancy and rental rates of our properties.

We own properties located throughout the United States. We compete with numerous developers, owners and operators of commercial properties, many of which own properties similar to, and in the same market areas as, our properties. If our competitors offer space at rental rates below current market rates, or below the rental rates we currently charge our tenants, we may lose existing or potential tenants and we may be pressured to reduce our rental rates below those we currently charge in order to attract new tenants and retain existing tenants when their leases expire. Also, if our competitors develop additional properties in locations near our properties, there may be increased competition for creditworthy tenants, which may require us to make capital improvements to properties that we would not have otherwise made.

Acts of God, such as earthquakes, floods or other uninsured losses may make us susceptible to adverse economic developments from the effects of these natural disasters in those areas.

Because our properties are concentrated in certain geographic areas, our operating results are likely to be impacted by economic changes affecting the real estate markets in those areas. Adverse events such as hurricanes, floods, wildfires, earthquakes, blizzards or other natural disasters, could cause a loss of revenues at our real estate properties. Elements such as water, wind, hail, or fire damage can increase or accelerate wear on our properties' weatherproofing, and mechanical, electrical and other systems, and cause mold issues. As a result, we may incur additional operating costs and expenditures for capital improvements at these properties.

To qualify as a REIT, we must rely on third parties to operate our hotels.

To continue qualifying as a REIT, we may not, among other things, operate any hotel, or directly participate in the decisions affecting the daily operations of any hotel. Thus, we have retained third party managers to operate our hotel properties. We do not have the authority to directly control any particular aspect of the daily operations of any hotel, such as setting room rates. Thus, even if we believe our hotels are being operated in an inefficient or sub-optimal manner, we may not be able to require an immediate change to the method of operation. Our only alternative for changing the operation of our hotels may be to replace the third party manager of one or more hotels in situations where the applicable management agreement permits us to terminate the existing manager. Certain of these agreements may not be terminated without cause, which generally requires fraud, misrepresentation and other illegal acts. Even if we terminate or replace any manager, there is no assurance that we will be able to find another manager or that we will be able to enter into new management agreements favorable to us. Any change of hotel management would disrupt operations, which could have an adverse material effect on our operating results and financial condition.

Conditions of franchise agreements could adversely affect us.

Our lodging properties are operated pursuant to agreements with nationally recognized franchisors including Marriott International, Inc., Hilton Hotels Corporation, Intercontinental Hotels Group PLC, Hyatt Corporation, and Wyndham Worldwide Corporation. These agreements generally contain specific standards for, and restrictions and limitations on, the operation and maintenance of a hotel in order to maintain uniformity within the particular franchisor's system. These standards are subject to change, in some cases at the discretion of the franchisor, and may restrict our ability to make improvements or modifications to a hotel without the consent of the franchisor. Conversely, these standards may require us to make certain improvements or modifications to a hotel, even if we do not believe the capital improvements are necessary or desirable or will result in an acceptable return on our investment.

These agreements also permit the franchisor to terminate the agreement in certain cases such as a failure to pay royalties and fees or to perform covenants continued in the franchise agreement, bankruptcy, abandonment of the franchise, commission of a felony, assignment of the franchise without the consent of the franchisor or failure to comply with applicable law or maintain applicable standards in the operation and condition of the relevant hotel. If a franchise license terminates due to our failure to comply with the terms and conditions of the agreement, we may be liable to the franchisor for a termination payment. These payments vary. Also, these franchise agreements do not renew automatically. If we were to lose a franchise agreement, there is no assurance that we would be able to enter into an agreement with a different franchisor. Loss of a franchise agreement could have a material adverse effect on our results of operations and financial condition.

Actions of our joint venture partners could negatively impact our performance.

As of December 31, 2012 we had entered into joint venture agreements with nine entities to fund investment is in office, industrial/distribution, retail, lodging, and mixed use properties. The carrying value of our investment in these joint ventures, which we do

10

not consolidate for financial reporting purposes, was $253.4 million. For the year ended December 31, 2012, we recorded income of $1.6 million and impairments and losses of $12.3 million associated with these ventures.

With respect to these investments, we are not in a position to exercise sole decision-making authority regarding the property, or the joint venture. Consequently, our joint venture investments may involve risks not otherwise present with other methods of investing in real estate. For example, our venture partner may have economic or business interests or goals which are or which become inconsistent with our business interests or goals or may take action contrary to our instructions or requests or contrary to our policies or objectives. We have experienced these events from time to time with our current or former venture partners, which in some cases has resulted in litigation. An adverse outcome in any lawsuit could have a material effect on our results of operations and forward condition. In addition, any litigation increases our expenses and prevents our officers and directors from focusing their time and effort on other aspects of our business. Our relationships with our venture partners are contractual in nature. These agreements may restrict our ability to sell our interest when we desire or on advantageous terms and, on the other hand, may be terminated or dissolved under the terms of the agreements and, in each event, we may not continue to own or operate the interests or assets underlying the relationship or may need to purchase these interests or assets at an above-market price to continue ownership.

Credit market disruptions and certain economic trends may increase the likelihood of a commercial developer defaulting on its obligations with respect to our development projects, including projects where we have notes receivable, or becoming bankrupt or insolvent.

We have invested in, and may continue to invest in, projects that are in various stages of pre-development and development. Investing in properties in pre-development or under development, and in lodging facilities in particular, which typically must be renovated or otherwise improved on a regular basis, including renovations and improvements required by existing franchise agreements, subjects us to uncertainties such as the ability to achieve desired zoning for development, environmental concerns of governmental entities or community groups, ability to control construction costs or to build in conformity with plans, specifications and timetables. In many cases, developers may not have adequate capital to address downturns in the market. Further, the developers of the projects in which we have invested are exposed to risks not only with respect to our projects, but also other projects in which they are involved. A default by a developer in respect to one of our development project investments, or the bankruptcy, insolvency or other failure of a developer for one of these projects, may require that we determine whether we want to assume the senior loan, fund monies beyond what we are contractually obligated to fund, take over development of the project, find another developer for the project, or sell our interest in the project. Developer failures could give tenants the right to terminate pre-construction leases, delay efforts to complete or sell the development project and could ultimately preclude us from realizing our anticipated returns. These events could cause a decrease in the value of our development assets and compel us to seek additional sources of funding, which may or may not be available, in order to hold and complete the development project.

Generally, under bankruptcy law and the bankruptcy guarantees we have required of certain of our joint venture development partners, we may seek recourse from the developer-guarantor to complete our development project with a substitute developer partner. However, in the event of a bankruptcy by the developer-guarantor, we cannot provide assurance that the developer or its trustee will satisfy its obligations. The bankruptcy of any developer or the failure of the developer to satisfy its obligations would likely cause us to have to complete the development or find a replacement developer, which could result in delays and increased costs. We cannot provide assurance that we would be able to complete the development on terms as favorable as when we first entered into the project. If we are not able to, or elect not to, the development costs ordinarily would be charged against income for the then-current period if we determine our costs are not recoverable.

Sale leaseback transactions may be recharacterized in a manner unfavorable to us.

From time to time we have entered into a sale leaseback transaction where we purchase a property and then lease the property to the seller. These transactions could, however, be characterized as a financing instead of a sale in the case of the seller's bankruptcy. In this case, we would not be treated as the owner of the property but rather as a creditor with no interest in the property itself. The seller may have the ability in a bankruptcy proceeding to restructure the financing by imposing new terms and conditions. The transaction also may be recharacterized as a joint venture. In this case, we would be treated as a joint venturer with liability, under some circumstances, for debts incurred by the seller relating to the property.

Our investments in equity and debt securities have materially impacted, and may in the future materially impact, our results.

As of December 31, 2012, we owned investment in real estate related equity and debt securities with an aggregate market value of $327.7 million. For the year ended December 31, 2012, we realized gains on sale of securities of $4.3 million, impairments of $1.9 million, and gross unrealized losses of

$2.0 million

. Real estate related equity securities are always unsecured and subordinated to other obligations of the issuer. Investments in real estate-related equity securities are subject to numerous risks including: (1)

11

limited liquidity in the secondary trading market in the case of unlisted or thinly traded securities; (2) substantial market price volatility resulting from, among other things, changes in prevailing interest rates in the overall market or related to a specific issuer, as well as changing investor perceptions of the market as a whole, REIT or real estate securities in particular or the specific issuer in question; (3) subordination to the liabilities of the issuer; (4) the possibility that earnings of the issuer may be insufficient to meet its debt service obligations or to pay distributions; and (5) with respect to investments in real estate-related preferred equity securities, the operation of mandatory sinking fund or call/redemption provisions during periods of declining interest rates that could cause the issuer to redeem the securities. In addition, investments in real estate-related securities involve special risks relating to the particular issuer of the securities, including the financial condition and business outlook of the issuer. Issuers of real estate-related securities generally invest in real estate or real estate-related assets and are subject to the inherent risks associated with real estate-related investments discussed herein. In fact, many of the entities that we have invested in have reduced the dividends paid on their securities. The stock prices for some of these entities have declined since our initial purchase, and in certain cases we have sold these investments at a loss.

Any mortgage loans that we originate or purchase are subject to the risks of delinquency and foreclosure.

We may originate and purchase mortgage loans. Mortgage loans are subject to risks of delinquency and foreclosure, and risks of loss. The ability of a borrower to repay a loan secured by an income-producing property depends primarily upon the successful operation of the property rather than upon the existence of independent income or assets of the borrower. If the net operating income of the property is reduced, the borrower's ability to repay the loan may be impaired. A property's net operating income can be affected by the any of the potential issues associated with real estate-related investments as discussed herein. We bear the risks of loss of principal to the extent of any deficiency between the value of the collateral and the principal and accrued interest of the mortgage loan. In the event of the bankruptcy of a mortgage loan borrower, the mortgage loan to that borrower will be deemed to be collateralized only to the extent of the value of the underlying collateral at the time of bankruptcy (as determined by the bankruptcy court), and the lien securing the mortgage loan will be subject to the avoidance powers of the bankruptcy trustee or debtor-in-possession to the extent the lien is unenforceable under state law. Foreclosure of a mortgage loan can be an expensive and lengthy process that could have a substantial negative effect on our anticipated return on the foreclosed mortgage loan. We may also be forced to foreclose on certain properties, be unable to sell these properties and be forced to incur substantial expenses to improve operations at the property.

We may make a mortgage loan to affiliates of, or entities sponsored by, our sponsor.

If we have excess working capital, we may, from time to time, and subject to the conditions in our articles, make a mortgage loan to affiliates of, or entities sponsored by, our sponsor. These loan arrangements will not be negotiated at arm's length and may contain terms and conditions that are not in our best interest and would not otherwise be applicable if we entered into arrangements with a third-party borrower not affiliated with these entities.

An increase in real estate taxes may decrease our income from properties.

From time to time, the amount we pay for property taxes increases as either property values increase or assessment rates are adjusted. Increases in a property's value or in the assessment rate result in an increase in the real estate taxes due on that property. If we are unable to pass the increase in taxes through to our tenants, our net operating income for the property will decrease.

Uninsured losses or premiums for insurance coverage may adversely affect a stockholder's returns.

We attempt to adequately insure all of our properties against casualty losses. There are types of losses, generally catastrophic in nature, such as losses due to wars, acts of terrorism, earthquakes, floods, hurricanes, pollution or environmental matters that are uninsurable or not economically insurable, or may be insured subject to limitations, such as large deductibles or co-payments. Risks associated with potential acts of terrorism could sharply increase the premiums we pay for coverage against property and casualty claims. Additionally, mortgage lenders sometimes require commercial property owners to purchase specific coverage against terrorism as a condition for providing mortgage loans. These policies may not be available at a reasonable cost, if at all, which could inhibit our ability to finance or refinance our properties. In such instances, we may be required to provide other financial support, either through financial assurances or self-insurance, to cover potential losses. If we incur any casualty losses not fully covered by insurance, the value of our assets will be reduced by the amount of the uninsured loss. In addition, other than any reserves we may establish, we have no designated source of funding to repair or reconstruct any uninsured damaged property.

12

Terrorist attacks and other acts of violence or war may affect the markets in which we operate our operations and our profitability.

We own estate assets located in areas that are susceptible to attack. These attacks may directly impact the value of our assets through damage, destruction, loss or increased security costs. Although we may obtain terrorism insurance, we may not be able to obtain sufficient coverage to fund any losses we may incur. Risks associated with potential acts of terrorism could sharply increase the premiums we pay for coverage against property and casualty claims. Further, certain losses resulting from these types of events are uninsurable or not insurable at reasonable costs.

More generally, any terrorist attack, other act of violence or war, including armed conflicts, could result in increased volatility in or damage to, the United States and worldwide financial markets and economy. Any terrorist incident may, for example, deter people from traveling, which could affect the ability of our hotels to generate operating income and therefore our ability to pay distributions. Additionally, increased economic volatility could adversely affect our tenants' ability to pay rent on their leases or our ability to borrow money or issue capital stock at acceptable prices.

The cost of complying with environmental and other governmental laws and regulations may adversely affect us.

All real property and the operations conducted on real property are subject to federal, state and local laws and regulations (including those of foreign jurisdictions) relating to environmental protection and human health and safety. These laws and regulations generally govern wastewater discharges, air emissions, the operation and removal of underground and above-ground storage tanks, the use, storage, treatment, transportation and disposal of solid and hazardous materials, and the remediation of contamination associated with disposals. We also are required to comply with various local, state and federal fire, health, life-safety and similar regulations. Some of these laws and regulations may impose joint and several liabilities on tenants or owners for the costs of investigating or remediating contaminated properties. These laws and regulations often impose liability whether or not the owner knew of, or was responsible for, the presence of the hazardous or toxic substances. The cost of removing or remediating could be substantial. In addition, the presence of these substances, or the failure to properly remediate these substances, may adversely affect our ability to sell or rent a property or to use the property as collateral for borrowing.

Environmental laws and regulations also may impose restrictions on the manner in which properties may be used or businesses may be operated, and these restrictions may require substantial expenditures by us. Environmental laws and regulations provide for sanctions in the event of noncompliance and may be enforced by governmental agencies or, in certain circumstances, by private parties. Third parties may seek recovery from owners of real properties for personal injury or property damage associated with exposure to released hazardous substances. Compliance with new or more stringent laws or regulations or stricter interpretations of existing laws may require material expenditures by us. For example, various federal, regional and state laws and regulations have been implemented or are under consideration to mitigate the effects of climate change caused by greenhouse gas emissions. Among other things, “green” building codes may seek to reduce emissions through the imposition of standards for design, construction materials, water and energy usage and efficiency, and waste management. We are not aware of any such existing requirements that we believe will have a material impact on our current operations. However, future requirements could increase the costs of maintaining or improving our existing properties or developing new properties.

Our properties may contain or develop harmful mold, which could lead to liability for adverse health effects and costs of remediating the problem.

The presence of mold at any of our properties could require us to undertake a costly program to remediate, contain or remove the mold. Mold growth may occur when moisture accumulates in buildings or on building materials. Some molds may produce airborne toxins or irritants. Concern about indoor exposure to mold has been increasing because exposure to mold may cause a variety of adverse health effects and symptoms, including allergic or other reactions. The presence of mold could expose us to liability from our tenants, their employees and others if property damage or health concerns arise.

We may incur significant costs to comply with the Americans With Disabilities Act.

Our properties generally are subject to the Americans With Disabilities Act of 1990, as amended. Under this act, all places of public accommodation are required to comply with federal requirements related to access and use by disabled persons. The act has separate compliance requirements for “public accommodations” and “commercial facilities” that generally require that buildings and services be made accessible and available to people with disabilities. The act's requirements could require us to

13

remove access barriers and could result in the imposition of injunctive relief, monetary penalties or, in some cases, an award of damages.

Borrowings may reduce the funds available for distribution and increase the risk of loss since defaults may cause us to lose the properties securing the loans.

We have acquired, and may continue to acquire, real estate assets by using either existing financing or borrowing new monies. Our articles permit us to borrow up to 300% of our net assets. In addition, we may obtain loans secured by some or all of our properties or other assets to fund additional acquisitions or operations including to satisfy the requirement that we distribute at least 90% of our annual “REIT taxable income” (subject to certain adjustments) to our stockholders, or as is otherwise necessary or advisable to assure that we qualify as a REIT for federal income tax purposes. Payments required on any amounts we borrow reduce the funds available for, among other things, distributions to our stockholders because cash otherwise available for distribution is required to pay principal and interest associated with amounts we borrow.

Defaults on loans secured by a property we own may result in us losing the property or properties securing the loan that is in default as a result of foreclosure actions initiated by a lender. For tax purposes, a foreclosure would be treated as a sale of the property for a purchase price equal to the outstanding balance of the debt secured by the property. If the outstanding balance of the debt exceeds our tax basis in the property, we would recognize taxable gain on the foreclosure but would not receive any cash proceeds. We also may fully or partially guarantee any monies that subsidiaries borrow to purchase or operate real estate assets. In these cases, we will be responsible to the lender for repaying the loans if the subsidiary is unable to do so. If any mortgage contains cross-collateralization or cross-default provisions, more than one property may be affected by a default.

Lenders may restrict certain aspects of our operations, which could, among other things, limit our ability to make distributions.

The terms and conditions contained in any of our loan documents may require us to maintain cash reserves; limit the aggregate amount we may borrow on a secured and unsecured basis; require us to satisfy restrictive financial covenants; prevent us from entering into certain business transactions, such as a merger, sale of assets or other business combination; restrict our leasing operations; or require us to obtain consent from the lender to complete transactions or make investments that are ordinarily approved only by our board of directors. In addition, secured lenders typically restrict our ability to discontinue insurance coverage on a mortgaged property even though we may believe that the insurance premiums paid to insure against certain losses, such as losses due to wars, acts of terrorism, earthquakes, floods, hurricanes, pollution or environmental matters, are greater than the potential risk of loss

Interest-only indebtedness may increase our risk of default.

We have obtained, and continue to incur interest related to, interest-only mortgage indebtedness. During the interest only period, the amount of each scheduled payment is less than that of a traditional amortizing mortgage loan. The principal balance of the mortgage loan is not reduced (except in the case of prepayments) because there are no scheduled monthly payments of principal during this period. After the interest-only period, we are required either to make scheduled payments of amortized principal and interest or to make a lump-sum or “balloon” payment at maturity. These required principal or balloon payments increase the amount of our scheduled payments and may increase our risk of default under the related mortgage loan if we are unable to fund the lump-sum or balloon amount.

Increases in interest rates could increase the amount of our debt payments.

As of December 31, 2012, approximately $1.3 billion of our total indebtedness bore interest at variable rates. Increases in interest rates on variable rate debt that has not otherwise been hedged through the use of swap agreements reduce the funds available for other needs, including distribution to our stockholders. As fixed rate debt matures, we may not be able to borrow at rates equal to or lower than the rates on the expiring debt. In addition, if rising interest rates cause us to need additional capital to repay indebtedness, we may be forced to sell one or more of our properties or investments in real estate at times which may not permit us to realize the return on the investments we would have otherwise realized.

To hedge against interest rate fluctuations, we use derivative financial instruments, which may be costly and ineffective.

From time to time, we use derivative financial instruments to hedge exposures to changes in interest rates on certain loans secured by our assets. Our derivative instruments currently consist of interest rate swap contracts but may, in the future, include, interest

14

rate cap or floor contracts, futures or forward contracts, options or repurchase agreements. Our actual hedging decisions are determined in light of the facts and circumstances existing at the time of the hedge. There is no assurance that our hedging strategy will achieve our objectives. We may be subject to costs, such as transaction fees or breakage costs, if we terminate these arrangements.