SANFILIPPO JOHN B & SON INC

10-Ks and 10-Qs

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM

10-Q

(Mark one)

|

|

QUARTERLY REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934

|

For the quarterly period ended

March 25,

2021

OR

|

|

TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934

|

Commission File Number

0-19681

(Exact Name of Registrant as Specified in Its Charter)

|

|

|

|

|

(State or Other Jurisdiction of

Incorporation or Organization)

|

(I.R.S. Employer

Identification No.)

|

|

|

|

|

|

(Address of Principal Executive Offices)

|

(Zip Code)

|

(

847

)

289-1800

(Registrant’s Telephone Number, Including Area Code)

Securities registered pursuant to Section 12(b) of the Act:

|

Title of Each Class

|

Trading

Symbol |

Name of Each Exchange

on Which Registered |

||

|

, $.01 par value per share

|

|

|

|

The NASDAQ

Stock Market LLC

(NASDAQ Global Select Market)

|

Securities registered pursuant to Section 12(g) of the Act: None

Indicate by check mark whether the registrant: (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past

90 days. ☒

☐ No

Indicate by check mark whether the registrant has submitted electronically every Interactive Data File required to be submitted pursuant to Rule 405 of Regulation

S-T

during the preceding 12 months (or for such shorter period that the registrant was required to submit such files). ☒

☐ No

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a

non-accelerated

filer, a smaller reporting company, or an emerging growth company. See the definitions of “large accelerated filer,” “accelerated filer”, “smaller reporting company” and “emerging growth company” in Rule

12b-2

of the Exchange Act. (Check One)

|

|

☒ | Accelerated filer | ☐ | |||

| Non-accelerated filer | ☐ | Smaller reporting company |

|

|||

| Emerging growth company |

|

|||||

If an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided pursuant to Section 13(a) of the Exchange Act. ☐

Indicate by check mark whether the registrant is a shell company (as defined in Rule

☒

No

12b-2

of the Exchange Act). ☐ Yes

As of April 22, 2021,

8,870,912

shares of the Registrant’s Common Stock, $0.01 par value per share and

2,597,426

shares of the Registrant’s Class A Common Stock, $0.01 par value per share, were outstanding.

JOHN B. SANFILIPPO & SON, INC.

FORM

10-Q

FOR THE QUARTER ENDED MARCH 25, 2021

INDEX

|

|

|

Page

|

|

|

|

|

||||

|

|

||||

|

|

|

3

|

|

|

|

|

|

4

|

|

|

|

|

|

6

|

|

|

|

|

|

7

|

|

|

|

|

|

8

|

|

|

|

|

|

18

|

|

|

|

|

|

30

|

|

|

|

|

|

30

|

|

|

|

|

||||

|

|

|

30

|

|

|

|

|

|

30

|

|

|

|

|

|

30

|

|

|

|

|

|

31

|

|

|

|

|

|

35

|

|

|

2

PART I—FINANCIAL INFORMATION

Item 1. Financial Statements

JOHN B. SANFILIPPO & SON, INC.

CONSOLIDATED STATEMENTS OF COMPREHENSIVE INCOME

(Unaudited)

(Dollars in thousands, except share and per share amounts)

|

For the Quarter Ended

|

For the Thirty-Nine Weeks

Ended |

|||||||||||||||

|

March 25,

2021

|

March 26,

2020

|

March 25,

2021 |

March 26,

2020 |

|||||||||||||

|

Net sales

|

$ |

|

$ |

|

$ |

|

$ |

|

||||||||

|

Cost of sales

|

|

|

|

|

||||||||||||

|

|

|

|

|

|

|

|

|

|||||||||

|

Gross profit

|

|

|

|

|

||||||||||||

|

|

|

|

|

|

|

|

|

|||||||||

|

Operating expenses:

|

||||||||||||||||

|

Selling expenses

|

|

|

|

|

||||||||||||

|

Administrative expenses

|

|

|

|

|

||||||||||||

|

|

|

|

|

|

|

|

|

|||||||||

|

Total operating expenses

|

|

|

|

|

||||||||||||

|

|

|

|

|

|

|

|

|

|||||||||

|

Income from operations

|

|

|

|

|

||||||||||||

|

|

|

|

|

|

|

|

|

|||||||||

|

Other expense:

|

||||||||||||||||

|

Interest expense including $

|

|

|

|

|

||||||||||||

|

Rental and miscellaneous expense, net

|

|

|

|

|

||||||||||||

|

Other expense

|

|

|

|

|

||||||||||||

|

|

|

|

|

|

|

|

|

|||||||||

|

Total other expense, net

|

|

|

|

|

||||||||||||

|

|

|

|

|

|

|

|

|

|||||||||

|

Income before income taxes

|

|

|

|

|

||||||||||||

|

Income tax expense

|

|

|

|

|

||||||||||||

|

|

|

|

|

|

|

|

|

|||||||||

|

Net income

|

$ |

|

$ |

|

$ |

|

$ |

|

||||||||

|

Other comprehensive income:

|

||||||||||||||||

|

Amortization of prior service cost and actuarial loss included in net periodic pension cost

|

|

|

|

|

||||||||||||

|

Income tax expense related to pension adjustments

|

(

|

) |

(

|

) |

(

|

) |

(

|

) | ||||||||

|

|

|

|

|

|

|

|

|

|||||||||

|

Other comprehensive income, net of tax

|

|

|

|

|

||||||||||||

|

|

|

|

|

|

|

|

|

|||||||||

|

Comprehensive income

|

$ |

|

$ |

|

$ |

|

$ |

|

||||||||

|

|

|

|

|

|

|

|

|

|||||||||

|

Net income per common share-basic

|

$ |

|

$ |

|

$ |

|

$ |

|

||||||||

|

|

|

|

|

|

|

|

|

|||||||||

|

Net income per common share-diluted

|

$ |

|

$ |

|

$ |

|

$ |

|

||||||||

|

|

|

|

|

|

|

|

|

|||||||||

The accompanying unaudited notes are an integral part of these consolidated financial statements.

3

JOHN B. SANFILIPPO & SON, INC.

CONSOLIDATED BALANCE SHEETS

(Unaudited)

(Dollars in thousands, except share and per share amounts)

|

March 25,

2021

|

June 25,

2020

|

March 26,

2020

|

||||||||||

|

ASSETS

|

||||||||||||

|

CURRENT ASSETS:

|

||||||||||||

|

Cash

|

$ |

|

$ |

|

$ |

|

||||||

|

Accounts receivable, less allowance for doubtful accounts of $

|

|

|

|

|||||||||

|

Inventories

|

|

|

|

|||||||||

|

Prepaid expenses and other current assets

|

|

|

|

|||||||||

|

|

|

|

|

|

|

|||||||

|

TOTAL CURRENT ASSETS

|

|

|

|

|||||||||

|

PROPERTY, PLANT AND EQUIPMENT:

|

||||||||||||

|

Land

|

|

|

|

|||||||||

|

Buildings

|

|

|

|

|||||||||

|

Machinery and equipment

|

|

|

|

|||||||||

|

Furniture and leasehold improvements

|

|

|

|

|||||||||

|

Vehicles

|

|

|

|

|||||||||

|

Construction in progress

|

|

|

|

|||||||||

|

|

|

|

||||||||||

|

Less: Accumulated depreciation

|

|

|

|

|||||||||

|

|

|

|

||||||||||

|

Rental investment property, less accumulated depreciation of $

|

|

|

|

|||||||||

|

|

|

|

|

|

|

|||||||

|

TOTAL PROPERTY, PLANT AND EQUIPMENT

|

|

|

|

|||||||||

|

|

|

|

|

|

|

|||||||

|

Intangible assets, net

|

|

|

|

|||||||||

|

Cash surrender value of officers’ life insurance and other assets

|

|

|

|

|||||||||

|

Deferred income taxes

|

|

|

|

|||||||||

|

Goodwill

|

|

|

|

|||||||||

|

Operating lease

right-of-use

|

|

|

|

|||||||||

|

|

|

|

|

|

|

|||||||

|

TOTAL ASSETS

|

$ |

|

$ |

|

$ |

|

||||||

|

|

|

|

|

|

|

|||||||

The accompanying unaudited notes are an integral part of these consolidated financial statements.

4

JOHN B. SANFILIPPO & SON, INC.

CONSOLIDATED BALANCE SHEETS

(Unaudited)

(Dollars in thousands, except share and per share amounts)

|

March 25,

2021

|

June 25,

2020

|

March 26,

2020

|

||||||||||

|

LIABILITIES & STOCKHOLDERS’ EQUITY

|

||||||||||||

|

CURRENT LIABILITIES:

|

||||||||||||

|

Revolving credit facility borrowings

|

$ |

|

$ |

|

$ |

|

||||||

|

Current maturities of long-term debt, including related party debt of $

|

|

|

|

|||||||||

|

Accounts payable

|

|

|

|

|||||||||

|

Bank overdraft

|

|

|

|

|||||||||

|

Accrued payroll and related benefits

|

|

|

|

|||||||||

|

Other accrued expenses

|

|

|

|

|||||||||

|

TOTAL CURRENT LIABILITIES

|

|

|

|

|||||||||

|

|

|

|

|

|

|

|||||||

|

LONG-TERM LIABILITIES:

|

||||||||||||

|

Long-term debt, less current maturities, including related party debt of $

|

|

|

|

|||||||||

|

Retirement plan

|

|

|

|

|||||||||

|

Long-term operating lease liabilities, net of current portion

|

|

|

|

|||||||||

|

Other

|

|

|

|

|||||||||

|

|

|

|

|

|

|

|||||||

|

TOTAL LONG-TERM LIABILITIES

|

|

|

|

|||||||||

|

|

|

|

|

|

|

|||||||

|

TOTAL LIABILITIES

|

|

|

|

|||||||||

|

|

|

|

|

|

|

|||||||

|

COMMITMENTS AND CONTINGENCIES

|

|

|

|

|||||||||

|

STOCKHOLDERS’ EQUITY:

|

||||||||||||

|

Class A Common Stock, convertible to Common Stock on a per share basis, cumulative voting rights of ten votes per share, $

par value;

|

|

|

|

|||||||||

|

Common Stock,

non-cumulative

voting rights of one vote per share, $

par value;

|

|

|

|

|||||||||

|

Capital in excess of par value

|

|

|

|

|||||||||

|

Retained earnings

|

|

|

|

|||||||||

|

Accumulated other comprehensive loss

|

(

|

) |

(

|

) |

(

|

) | ||||||

|

Treasury stock, at cost;

|

(

|

) |

(

|

) |

(

|

) | ||||||

|

|

|

|

|

|

|

|||||||

|

TOTAL STOCKHOLDERS’ EQUITY

|

|

|

|

|||||||||

|

|

|

|

|

|

|

|||||||

|

TOTAL LIABILITIES & STOCKHOLDERS’ EQUITY

|

$ |

|

$ |

|

$ |

|

||||||

|

|

|

|

|

|

|

|||||||

The accompanying unaudited notes

are

an integral part of these consolidated financial statements.

5

JOHN B. SANFILIPPO & SON, INC.

CONSOLIDATED STATEMENTS OF STOCKHOLDERS’ EQUITY

(Unaudited)

(Dollars in thousands, except share and per share amounts)

|

Class A Common

Stock |

Common Stock

|

Capital in

Excess of Par Value |

Retained

Earnings |

Accumulated

Other Comprehensive Loss |

Treasury

Stock |

||||||||||||||||||||||||||||||||||||||||

|

Shares

|

Amount

|

Shares

|

Amount

|

Total

|

|||||||||||||||||||||||||||||||||||||||||

|

Balance, June 25, 2020

|

|

$ |

|

|

$ |

|

$ |

|

$ |

|

$ |

(

|

) | $ |

(

|

) | $ |

|

|||||||||||||||||||||||||||

|

Net income

|

|

|

|||||||||||||||||||||||||||||||||||||||||||

|

Cash dividends ($

|

(

|

) |

(

|

) | |||||||||||||||||||||||||||||||||||||||||

|

Pension liability amortization, net of income tax expense of $

|

|

|

|||||||||||||||||||||||||||||||||||||||||||

|

Equity award exercises

|

|

— | — | — | |||||||||||||||||||||||||||||||||||||||||

|

Stock-based compensation expense

|

|

|

|||||||||||||||||||||||||||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||||||||||||||||||||||||||

|

Balance, September 24, 2020

|

|

$ |

|

|

$ |

|

$ |

|

$ |

|

$ |

(

|

) | $ |

(

|

) | $ |

|

|||||||||||||||||||||||||||

|

Net income

|

|

|

|||||||||||||||||||||||||||||||||||||||||||

|

Pension liability amortization, net of income tax expense of $

|

|

|

|||||||||||||||||||||||||||||||||||||||||||

|

Equity award exercises , net of shares withheld for employee taxes

|

|

|

(

|

) |

(

|

) | |||||||||||||||||||||||||||||||||||||||

|

Stock-based compensation expense

|

|

|

|||||||||||||||||||||||||||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||||||||||||||||||||||||||

|

Balance, December 24, 2020

|

|

$ |

|

|

$ |

|

$ |

|

$ |

|

$ |

(

|

) | $ |

(

|

) | $ |

|

|||||||||||||||||||||||||||

|

Net income

|

|

|

|||||||||||||||||||||||||||||||||||||||||||

|

Cash dividends ($

|

(

|

) |

(

|

) | |||||||||||||||||||||||||||||||||||||||||

|

Pension liability amortization, net of income tax expense of $

|

|

|

|||||||||||||||||||||||||||||||||||||||||||

|

Equity award exercises , net of shares withheld for employee taxes

|

|

— |

(

|

) |

(

|

) | |||||||||||||||||||||||||||||||||||||||

|

Stock-based compensation expense

|

|

|

|||||||||||||||||||||||||||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||||||||||||||||||||||||||

|

Balance, March 25, 2021

|

|

$ |

|

|

$ |

|

$ |

|

$ |

|

$ |

(

|

) | $ |

(

|

) | $ |

|

|||||||||||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||||||||||||||||||||||||||

|

Class A Common

Stock |

Common Stock

|

Capital in

Excess of Par Value |

Retained

Earnings |

Accumulated

Other Comprehensive Loss |

Treasury

Stock |

|||||||||||||||||||||||||||||||||

|

Shares

|

Amount

|

Shares

|

Amount

|

Total

|

||||||||||||||||||||||||||||||||||

|

Balance, June 27, 2019

|

|

$ |

|

|

$ |

|

$ |

|

$ |

|

$ |

(

|

) | $ |

(

|

) | $ |

|

||||||||||||||||||||

|

Net income

|

|

|

||||||||||||||||||||||||||||||||||||

|

Cash dividends ($

|

(

|

) |

(

|

) | ||||||||||||||||||||||||||||||||||

|

Pension liability amortization, net of income tax expense of $

|

|

|

||||||||||||||||||||||||||||||||||||

|

Impact of adopting ASU

2018-02

|

|

(

|

) |

|

||||||||||||||||||||||||||||||||||

|

Stock-based compensation expense

|

|

|

||||||||||||||||||||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||||||||||

|

Balance, September 26, 2019

|

|

$ |

|

|

$ |

|

$ |

|

$ |

|

$ |

(

|

) | $ |

(

|

) | $ |

|

||||||||||||||||||||

|

Net income

|

|

|

||||||||||||||||||||||||||||||||||||

|

Cash dividends ($

|

(

|

) |

(

|

) | ||||||||||||||||||||||||||||||||||

|

Pension liability amortization, net of income tax expense of $

|

|

|

||||||||||||||||||||||||||||||||||||

|

Equity award exercises , net of shares withheld for employee taxes

|

|

— |

(

|

) |

(

|

) | ||||||||||||||||||||||||||||||||

|

Stock-based compensation expense

|

|

|

||||||||||||||||||||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||||||||||

|

Balance, December 26, 2019

|

|

$ |

|

|

$ |

|

$ |

|

$ |

|

$ |

(

|

) | $ |

(

|

) | $ |

|

||||||||||||||||||||

|

Net income

|

|

|

||||||||||||||||||||||||||||||||||||

|

Pension liability amortization, net of income tax expense of $

|

|

|

||||||||||||||||||||||||||||||||||||

|

Equity award exercises , net of shares withheld for employee taxes

|

|

— |

(

|

) |

(

|

) | ||||||||||||||||||||||||||||||||

|

Stock-based compensation expense

|

|

|

||||||||||||||||||||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||||||||||

|

Balance, March 26, 2020

|

|

$ |

|

|

$ |

|

$ |

|

$ |

|

$ |

(

|

) | $ |

(

|

) | $ |

|

||||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||||||||||

The accompanying unaudited notes are an integral part of these consolidated financial statements.

6

JOHN B. SANFILIPPO & SON, INC.

CONSOLIDATED STATEMENTS OF CASH FLOWS

(Unaudited)

(Dollars in thousands)

|

For the Thirty-Nine

|

||||||||

|

March 25,

|

March 26,

|

|||||||

|

CASH FLOWS FROM OPERATING ACTIVITIES:

|

||||||||

|

Net income

|

$ |

|

$ |

|

||||

|

Depreciation and amortization

|

|

|

||||||

|

Gain on disposition of assets, net

|

(

|

) |

(

|

) | ||||

|

Deferred income tax expense (benefit)

|

|

(

|

) | |||||

|

Stock-based compensation expense

|

|

|

||||||

|

Change in assets and liabilities:

|

||||||||

|

Accounts receivable, net

|

(

|

) |

(

|

) | ||||

|

Inventories

|

|

(

|

) | |||||

|

Prepaid expenses and other current assets

|

|

|

||||||

|

Accounts payable

|

|

|

||||||

|

Accrued expenses

|

(

|

) |

(

|

) | ||||

|

Income taxes payable

|

(

|

) |

|

|||||

|

Other long-term assets and liabilities

|

|

|

||||||

|

Other, net

|

|

|

||||||

|

|

|

|

|

|||||

|

Net cash provided by operating activities

|

|

|

||||||

|

|

|

|

|

|||||

|

CASH FLOWS FROM INVESTING ACTIVITIES:

|

||||||||

|

Purchases of property, plant and equipment

|

(

|

) |

(

|

) | ||||

|

Proceeds from insurance recoveries

|

|

|

||||||

|

Other

|

(

|

) |

(

|

) | ||||

|

Net cash used in investing activities

|

(

|

) |

(

|

) | ||||

|

CASH FLOWS FROM FINANCING ACTIVITIES:

|

||||||||

|

Net short-term (repayments) borrowings

|

(

|

) |

|

|||||

|

Debt issue costs

|

— |

(

|

) | |||||

|

Principal payments on long-term debt

|

(

|

) |

(

|

) | ||||

|

(Decrease) increase in bank overdraft

|

(

|

) |

|

|||||

|

Dividends paid

|

(

|

) |

(

|

) | ||||

|

Taxes paid related to net share settlement of equity awards

|

(

|

) |

(

|

) | ||||

|

|

|

|

|

|||||

|

Net cash used in financing activities

|

(

|

) |

(

|

) | ||||

|

NET DECREASE IN CASH

|

(

|

) |

(

|

) | ||||

|

Cash, beginning of period

|

|

|

||||||

|

|

|

|

|

|||||

|

Cash, end of period

|

$ |

|

$ |

|

||||

|

|

|

|

|

|||||

|

Supplemental disclosure of

non-cash

activities:

|

||||||||

|

Right-of-use

No. 2016-02

transition

|

— | $ |

|

|||||

The accompanying unaudited notes are an integral part of these consolidated financial statements.

7

JOHN B. SANFILIPPO & SON, INC.

NOTES TO CONSOLIDATED FINANCIAL STATEMENTS

(Unaudited)

(Dollars in thousands, except where noted and per share data)

Note 1 – Basis of Presentation and Description of Business

As used herein, unless the context otherwise indicates, the terms “we”, “us”, “our” or “Company” collectively refer to John B. Sanfilippo & Son, Inc. and our wholly-owned subsidiary, JBSS Ventures, LLC. Our fiscal year ends on the final Thursday of June each year, and typically consists of

fifty-two

weeks (four thirteen-week quarters). Additional information on the comparability of the periods presented is as follows:

| • |

References herein to fiscal 2021 and fiscal 2020 are to the fiscal year ending June 24, 2021 and the fiscal year ended June 25, 2020, respectively.

|

| • |

References herein to the third quarter of fiscal 2021 and fiscal 2020 are to the quarters ended March 25, 2021 and March 26, 2020, respectively.

|

| • |

References herein to the first three quarters or first thirty-nine weeks of fiscal 2021 and fiscal 2020 are to the thirty-nine weeks ended March 25, 2021 and March 26, 2020, respectively.

|

We are one of the leading processors and distributors of peanuts, pecans, cashews, walnuts, almonds, and other nuts in the United States. These nuts are sold under our

,

,

,

and

brand names and under a variety of private brands. We also market and distribute, and in most cases, manufacture or process, a diverse product line of food and snack products, including peanut butter, almond butter, cashew butter, candy and confections, snacks and trail mixes, snack bites, sunflower kernels, dried fruit, corn snacks, chickpea snacks, sesame sticks and other sesame snack products under our brand names and under private brands. Our products are sold through

three

primary distribution channels, including food retailers in the consumer channel, commercial ingredient users and contract packaging customers.

Fisher

Orchard Valley Harvest

Squirrel Brand

Southern Style Nuts

Sunshine Country

The accompanying unaudited financial statements fairly present the consolidated statements of comprehensive income, consolidated balance sheets, consolidated statements of stockholders’ equity and consolidated statements of cash flows, and reflect all adjustments, consisting only of normal recurring adjustments which are necessary for the fair statement of the results of the interim periods. Preparing financial statements requires management to make estimates and assumptions that affect the reported amounts of assets, liabilities, revenues and expenses.

The interim results of operations are not necessarily indicative of the results to be expected for a full year. The balance sheet data as of June 25, 2020 was derived from audited financial statements, but does not include all disclosures required by accounting principles generally accepted in the United States of America (“GAAP”). Accordingly, these unaudited financial statements and related notes should be read in conjunction with the audited consolidated financial statements and notes thereto included in our 2020 Annual Report on Form

10-K

for the fiscal year ended June 25, 2020.

Note 2 – Revenue Recognition

We recognize revenue to depict the transfer of promised goods or services to customers in an amount that reflects the consideration to which we expect to be entitled in exchange for those goods or services. For each customer contract, a five-step process is followed in which we identify the contract, identify performance obligations, determine the transaction price, allocate the contract transaction price to the performance obligations, and recognize the revenue when (or as) the performance obligation is transferred to the customer.

When Performance Obligations Are Satisfied

A performance obligation is a promise in a contract to transfer a distinct good or service to the customer and is the unit of account for revenue recognition. A contract’s transaction price is allocated to each distinct performance obligation and recognized as revenue when, or as, the performance obligation is satisfied. The Company’s performance obligations are primarily for the delivery of raw and processed recipe and snack nuts, nut butters and trail mixes.

8

Our customer contracts do not include more than one performance obligation. If a contract were to contain more than one performance obligation, we are required to allocate the contract’s transaction price to each performance obligation based on its relative standalone selling price. The standalone selling price for each distinct good is generally determined by directly observable data.

Revenue recognition is generally completed at a point in time when product control is transferred to the customer. For virtually all of our revenues, control transfers to the customer when the product is shipped or delivered to the customer based upon applicable shipping terms, as the customer can then direct the use and obtain substantially all of the remaining benefits from the asset at that point in time. Therefore, the timing of our revenue recognition requires little judgment.

Variable Consideration

Some of our products are sold through specific incentive programs consisting of promotional allowances, volume and customer rebates,

in-store

display incentives and marketing allowances, among others, to consumer and some commercial ingredient customers. The ultimate cost of these programs is dependent on certain factors such as actual purchase volumes or customer activities and is dependent on significant management judgment when determining estimates. The Company accounts for these programs as variable consideration and recognizes a reduction in revenue (and a corresponding reduction in the transaction price) in the same period as the underlying program based upon the terms of the specific arrangements.

Trade promotions, consisting primarily of customer pricing allowances, merchandising funds and consumer coupons, are also offered through various programs to customers and consumers. A provision for estimated trade promotions is recorded as a reduction of revenue (and a reduction in the transaction price) in the same period when the sale is recognized. Revenues are also recorded net of expected customer deductions which are provided for based upon past experiences. Evaluating these estimates requires management judgment.

We generally use the most likely amount method to determine the variable consideration. We believe there will not be significant changes to our estimates of variable consideration when any related uncertainties are resolved with our customers. The Company reviews and updates its estimates and related accruals of variable consideration and trade promotions at least quarterly based on the terms of the agreements and historical experience. Any uncertainties in the ultimate resolution of variable consideration due to factors outside of the Company’s influence are typically resolved within a short timeframe, therefore, no additional constraint on the variable consideration is required.

Contract Balances

Contract assets or liabilities result from transactions with revenue recorded over time. If the measure of remaining rights exceeds the measure of the remaining performance obligations the Company records a contract asset. Conversely, if the measure of the remaining performance obligations exceeds the measure of the remaining rights, the Company records a contract liability. There was

no

contract asset balance for any periods presented. The Company generally does not have material deferred revenue or contract liability balances arising from transactions with customers.

Disaggregation of Revenue

Revenue disaggregated by sales channel is as follows:

|

For the Quarter Ended

|

For the Thirty-Nine

Ended |

|||||||||||||||

|

Distribution Channel

|

March 25,

2021

|

March 26,

2020

|

March 25,

2021

|

March 26,

2020

|

||||||||||||

|

Consumer

|

$ |

|

$ |

|

$ |

|

$ |

|

||||||||

|

Commercial Ingredients

|

|

|

|

|

||||||||||||

|

Contract Packaging

|

|

|

|

|

||||||||||||

|

|

|

|

|

|

|

|

|

|||||||||

|

Total

|

$ |

|

$ |

|

$ |

|

$ |

|

||||||||

|

|

|

|

|

|

|

|

|

|||||||||

9

Note 3 – Leases

Description of Leases

We lease equipment used in the transportation of goods in our warehouses, as well as a limited number of automobiles and a small warehouse near our Bainbridge, Georgia facility. Our leases generally do not contain

non-lease

components and do not contain any explicit guarantees of residual value. Our leases for warehouse transportation equipment generally require the equipment to be returned to the lessor in good working order.

We determine if an arrangement is a lease at inception and analyze the lease to determine if it is operating or finance. Operating lease

assets represent our right to use an underlying asset for the lease term and lease liabilities represent our obligation to make lease payments arising from the lease. Operating lease

assets and liabilities are recognized at the lease commencement date based on the present value of lease payments over the lease term. As most of our leases do not provide an implicit rate, we use our incremental collateralized borrowing rate based on the information available at the commencement date in determining the present value of lease payments. Implicit rates are used when readily determinable. None of our leases currently contain options to extend the term. In the event of an option to extend the term of a lease, the lease term used in measuring the liability would include options to extend or terminate the lease if it is reasonably certain that the Company will exercise that option. Lease expense for operating lease payments is recognized on a straight-line basis over the respective lease term. Our leases have remaining terms of up to

5.3

years.

right-of-use

right-of-use

It is our accounting policy to not apply lease recognition requirements to short term leases, defined as leases with an initial term of 12 months or less. As such, leases with an initial term of 12 months or less are not recorded in the Consolidated Balance Sheet. We have also made the policy election to not separate lease and

non-lease

components for all leases.

The following table provides supplemental information related to operating lease

assets and liabilities:

right-of-use

|

March 25,

2021

|

June 25,

2020

|

March 26,

2020 |

Affected Line Item in

Consolidated Balance Sheet |

|||||||||||||

|

Assets

|

||||||||||||||||

|

Operating lease

right-of-use

|

$ |

|

$ |

|

$ |

|

Operating lease

right-of-use

|

|||||||||

|

|

|

|

|

|

|

|||||||||||

|

Total lease

right-of-use

|

$ |

|

$ |

|

$ |

|

||||||||||

|

|

|

|

|

|

|

|||||||||||

|

Liabilities

|

||||||||||||||||

|

Current:

|

||||||||||||||||

|

Operating leases

|

$ |

|

$ |

|

$ |

|

Other accrued expenses

|

|||||||||

|

Noncurrent:

|

||||||||||||||||

|

Operating leases

|

|

|

|

Long-term operating lease liabilities

|

||||||||||||

|

|

|

|

|

|

|

|||||||||||

|

Total lease liabilities

|

$ |

|

$ |

|

$ |

|

||||||||||

|

|

|

|

|

|

|

|||||||||||

The following tables summarize the Company’s total lease costs and other information arising from operating lease transactions:

|

For the Quarter Ended

|

For the Thirty-nine

|

|||||||||||||||

|

March 25,

2021

|

March 26,

2020

|

March 25,

2021

|

March 26,

2020 |

|||||||||||||

|

Operating lease costs

(a)

|

$ |

|

$ |

|

$ |

|

$ |

|

||||||||

|

Variable lease costs

(b)

|

|

|

|

|

||||||||||||

|

Total Lease Cost

|

$ |

|

$ |

|

$ |

|

$ |

|

||||||||

|

|

|

|

|

|

|

|

|

|||||||||

|

(a)

|

Includes short-term leases which are immaterial.

|

|

(b)

|

Variable lease costs consist of sales tax.

|

10

Supplemental cash flow and other information related to leases was as follows:

|

For the Thirty-nine

|

||||||||

|

March 25,

2021 |

March 26,

2020 |

|||||||

|

Operating cash flows information:

|

||||||||

|

Cash paid for amounts included in measurements for lease liabilities

|

$ |

|

$ |

|

||||

|

Non-cash

activity:

|

||||||||

|

Right-of-use

|

$ |

|

$ |

|

||||

|

March 25,

2021 |

June 25,

2020

|

March 26,

2020 |

||||||||||

|

Weighted Average Remaining Lease Term (in years)

|

|

|

|

|||||||||

|

Weighted Average Discount Rate

|

|

% |

|

% |

|

% | ||||||

Maturities of operating lease liabilities as of March 25, 2021 are as follows:

|

Fiscal year ending

|

||||

|

June 24, 2021 (excluding the thirty-nine weeks ended March 25, 2021)

|

$ |

|

||

|

June 30, 2022

|

|

|||

|

June 29, 2023

|

|

|||

|

June 27, 2024

|

|

|||

|

June 26, 2025

|

|

|||

|

June 25, 2026

|

|

|||

|

Thereafter

|

|

|||

|

|

|

|||

|

Total lease payment

|

|

|||

|

Less imputed interest

|

(

|

) | ||

|

|

|

|||

|

Present value of operating lease liabilities

|

$ |

|

||

|

|

|

Lessor Accounting

We lease office space in our four-story office building located in Elgin, Illinois. As a lessor, we retain substantially all of the risks and benefits of ownership of the investment property and under Topic 842 we continue to account for all of our leases as operating leases. Lease agreements may include options to renew. We accrue fixed lease income on a

straight-line

basis over the terms of the leases. There is generally no variable lease consideration and an immaterial amount of

non-lease

components such as recurring utility and storage fees. Leases between related parties are immaterial.

Leasing revenue is as follows:

|

For the Quarter ended

|

For the Thirty-nine

|

|||||||||||||||

|

March 25,

2021 |

March 26,

2020 |

March 25,

2021 |

March 26,

2020 |

|||||||||||||

|

Lease income related to lease payments

|

$ |

|

$ |

|

$ |

|

$ |

|

||||||||

11

The future minimum, undiscounted fixed cash flows under

non-cancelable

tenant operating leases for each of the next five years and thereafter is presented below.

|

Fiscal year ending

|

||||

|

June 24, 2021 (excluding the thirty-nine weeks ended March 25, 2021)

|

$ |

|

||

|

June 30, 2022

|

|

|||

|

June 29, 2023

|

|

|||

|

June 27, 2024

|

|

|||

|

June 26, 2025

|

|

|||

|

June 25, 2026

|

|

|||

|

Thereafter

|

|

|||

|

|

|

|||

| $ |

|

Note 4 – Inventories

Inventories consist of the following:

|

March 25,

2021

|

June 25,

2020

|

March 26,

2020

|

||||||||||

|

Raw material and supplies

|

$ |

|

$ |

|

$ |

|

||||||

|

Work-in-process

|

|

|

|

|||||||||

|

|

|

|

|

|

|

|||||||

|

Total

|

$ |

|

$ |

|

$ |

|

||||||

|

|

|

|

|

|

|

|||||||

Note 5 – Goodwill and Intangible Assets

Identifiable intangible assets that are subject to amortization consist of the following:

|

March 25,

|

June 25,

|

March 26,

|

||||||||||

|

Customer relationships

|

$ |

|

$ |

|

$ |

|

||||||

|

Brand names

|

|

|

|

|||||||||

|

Non-compete

agreement

|

|

|

|

|||||||||

|

|

|

|

|

|

|

|||||||

|

|

|

|

||||||||||

|

Less accumulated amortization:

|

||||||||||||

|

Customer relationships

|

(

|

) |

(

|

) |

(

|

) | ||||||

|

Brand names

|

(

|

) |

(

|

) |

(

|

) | ||||||

|

Non-compete

agreement

|

(

|

) |

(

|

) |

(

|

) | ||||||

|

|

|

|

|

|

|

|||||||

|

(

|

) |

(

|

) |

(

|

) | |||||||

|

|

|

|

|

|

|

|||||||

|

Net intangible assets

|

$ |

|

$ |

|

$ |

|

||||||

|

|

|

|

|

|

|

|||||||

Customer relationships are being amortized on an accelerated basis. The brand names remaining to be amortized consist of the

and

brand names.

Squirrel Brand

Southern Style Nuts

Total amortization expense related to intangible assets, which is recorded within Administrative expense, was $

504

and $

1,661

for the quarter and thirty-nine weeks ended March 25, 2021, respectively. Amortization expense for the remainder of fiscal 2021 is expected to be approximately $

504

and

expected amortization expense the next five fiscal years is as follows:

|

Fiscal year ending

|

||||

|

June 30, 2022

|

$ |

|

||

|

June 29, 2023

|

|

|||

|

June 27, 2024

|

|

|||

|

June 26, 2025

|

|

|||

|

June 25, 2026

|

|

|||

12

Our net goodwill of $

9,650

relates entirely to the Squirrel Brand acquisition completed in the second quarter of fiscal 2018. There was no change in the carrying amount of goodwill during the thirty-nine weeks ended March 25, 2021.

Note 6 – Credit Facility

Our Amended and Restated Credit Agreement dated March 5, 2020 provides for a $

117,500

senior secured revolving credit facility (the “Credit Facility”). The Credit Facility is secured by substantially all our assets other than machinery and equipment, real property and fixtures.

At March 25, 2021, we had $

88,310

of available credit under the Credit Facility which reflects borrowings of $

26,005

and reduced availability as a result of $

3,185

in outstanding letters of credit. As of March 25, 2021, we were in compliance with all financial covenants under the Credit Facility and Mortgage Facility (as defined below).

Note 7 – Earnings Per Common Share

The following table presents the reconciliation of the weighted average shares outstanding used in computing basic and diluted earnings per share:

|

For the Quarter Ended

|

For the Thirty-Nine Weeks

Ended |

|||||||||||||||

|

March 25,

2021

|

March 26,

2020

|

March 25,

2021

|

March 26,

2020

|

|||||||||||||

|

Weighted average number of shares outstanding – basic

|

|

|

|

|

||||||||||||

|

Effect of dilutive securities:

|

||||||||||||||||

|

Stock options and restricted stock units

|

|

|

|

|

||||||||||||

|

|

|

|

|

|

|

|

|

|||||||||

|

Weighted average number of shares outstanding – diluted

|

|

|

|

|

||||||||||||

|

|

|

|

|

|

|

|

|

|||||||||

The following table presents a summary of anti-dilutive awards excluded from the computation of diluted earnings per share:

|

For the Quarter Ended

|

For the Thirty-Nine Weeks

Ended

|

|||||||||||||||

|

March 25,

2021

|

March 26,

2020

|

March 25,

2021

|

March 26,

2020

|

|||||||||||||

|

Weighted average number of anti-dilutive awards:

|

|

|

|

|

||||||||||||

|

Weighted average exercise price per award:

|

$ |

|

$ |

|

$ |

|

$ |

|

||||||||

Note 8 – Stock-Based Compensation Plans

The following is a summary of restricted stock unit (“RSU”) activity for the first thirty-nine weeks of fiscal 2021:

|

Restricted Stock Units

|

Shares

|

Weighted

Average Grant Date Fair Value |

||||||

|

Outstanding at June 25,

|

|

$ |

|

|||||

|

Activity:

|

||||||||

|

Granted

|

|

|

||||||

|

Vested

(a)

|

(

|

) |

|

|||||

|

Forfeited

|

(

|

) |

|

|||||

|

|

|

|

|

|||||

|

Outstanding at March 25, 2021

|

|

$ |

|

|||||

|

|

|

|

|

|||||

|

(a)

|

The number of RSUs vested includes shares that were withheld on behalf of employees to satisfy the statutory income tax withholding requirements.

|

13

At March 25, 2021, there are

47,127

RSUs outstanding that are vested but deferred.

The following table summarizes compensation expense charged to earnings for all equity compensation plans for the periods presented:

|

For the Quarter Ended

|

For the Thirty-Nine

Ended

|

|||||||||||||||

|

March 25,

2021

|

March 26,

2020

|

March 25,

2021

|

March 26,

2020

|

|||||||||||||

|

Stock-based compensation expense

|

$ |

|

$ |

|

$ |

|

$ |

|

||||||||

As of March 25, 2021, there was $

4,602

of total unrecognized compensation expense related to

1.6

years.

non-vested

RSUs granted under our stock-based compensation plans. We expect to recognize that cost over a weighted average period of

Note 9 – Retirement Plan

The Supplemental Employee Retirement Plan is an unfunded,

The components of net periodic benefit cost are as follows:

non-qualified

deferred compensation plan that will provide eligible participants with monthly benefits upon retirement, disability or death, subject to certain conditions. The monthly benefit is based upon each participant’s earnings and his or her number of years of service.

|

For the Quarter Ended

|

For the Thirty-Nine

Ended |

|||||||||||||||

|

March 25,

2021

|

March 26,

2020

|

March 25,

2021

|

March 26,

2020

|

|||||||||||||

|

Service cost

|

$ |

|

$ |

|

$ |

|

$ |

|

||||||||

|

Interest cost

|

|

|

|

|

||||||||||||

|

Amortization of prior service cost

|

|

|

|

|

||||||||||||

|

Amortization of loss

|

|

|

|

|

||||||||||||

|

|

|

|

|

|

|

|

|

|||||||||

|

Net periodic benefit cost

|

$ |

|

$ |

|

$ |

|

$ |

|

||||||||

|

|

|

|

|

|

|

|

|

|||||||||

The components of net periodic benefit cost other than the service cost component are included in the line item “Other expense” in the Consolidated Statements of Comprehensive Income.

Note 10 – Accumulated Other Comprehensive Loss

The table below sets forth the changes to accumulated other comprehensive loss (“AOCL”) for the thirty-nine weeks ended March 25, 2021 and March 26, 2020.

These changes are all related to our defined benefit pension plan.

|

For the Thirty-Nine

Weeks Ended |

||||||||

|

Changes to AOCL

(a)

|

March 25,

2021

|

March 26,

2020

|

||||||

|

Balance at beginning of period

|

$ |

(

|

) | $ |

(

|

) | ||

|

Other comprehensive income before reclassifications

|

|

|

||||||

|

Amounts reclassified from accumulated other comprehensive loss

|

|

|

||||||

|

Tax effect

|

(

|

) |

(

|

) | ||||

|

|

|

|

|

|||||

|

Net current-period other comprehensive income

|

|

|

||||||

|

Impact of adopting ASU

2018-02

|

— |

(

|

) | |||||

|

|

|

|

|

|||||

|

Balance at end of period

|

$ |

(

|

) | $ |

(

|

) | ||

|

|

|

|

|

|||||

|

(a)

|

Amounts in parenthesis indicate debits/expense.

|

14

The reclassifications out of AOCL for the quarter and thirty-nine weeks ended March 25, 2021 and March 26, 2020 were as follows:

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Affected line

item in

the Consolidated

Statements of Comprehensive Income |

|

|||||

|

Reclassifications from AOCL to earnings

(b)

|

|

For the Quarter Ended

|

|

|

For the Thirty-Nine Weeks

Ended |

|

||||||||||||||

|

|

March 25,

2021

|

|

|

March 26,

2020

|

|

|

March 25,

2021

|

|

|

March 26,

2020

|

|

|||||||||

|

Amortization of defined benefit pension items:

|

|

|

|

|

|

|||||||||||||||

|

Unrecognized prior service cost

|

|

$

|

(

|

)

|

|

$

|

(

|

)

|

|

$

|

(

|

)

|

|

$

|

(

|

)

|

|

|

Other expense

|

|

|

Unrecognized net loss

|

|

|

(

|

)

|

|

|

(

|

)

|

|

|

(

|

)

|

|

|

(

|

)

|

|

|

Other expense

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||

|

Total before tax

|

|

|

(

|

)

|

|

|

(

|

)

|

|

|

(

|

)

|

|

|

(

|

)

|

|

|||

|

Tax effect

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Income tax expense

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||

|

Amortization of defined pension items, net of tax

|

|

$

|

(

|

)

|

|

$

|

(

|

)

|

|

$

|

(

|

)

|

|

$

|

(

|

)

|

|

|||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||

|

(b)

|

Amounts in parenthesis indicate debits to expense. See Note 9 – “Retirement Plan” above for additional details.

|

Note 11 – Commitments and Contingent Liabilities

We are currently a party to various legal proceedings in the ordinary course of business. While management presently believes that the ultimate outcomes of these proceedings, individually and in the aggregate, will not materially affect our Company’s financial position, results of operations or cash flows, legal proceedings are subject to inherent uncertainties, and unfavorable outcomes could occur. Unfavorable outcomes could include substantial monetary damages in excess of any appropriate accruals, which management has established. Where such unfavorable final outcomes to occur, there exists the possibility of a material adverse effect on our financial position, results of operations and cash flows.

Note 12 – Fair Value of Financial Instruments

The Financial Accounting Standards Board (“FASB”) defines fair value as the price that would be received for an asset or paid to transfer a liability in an orderly transaction between market participants on the measurement date. The guidance establishes a fair value hierarchy that prioritizes observable and unobservable inputs used to measure fair value into three broad levels:

|

Level 1

|

|

–

|

|

Quoted prices in active markets that are accessible at the measurement date for identical assets and liabilities.

|

|

Level 2

|

|

–

|

|

Observable inputs other than quoted prices in active markets. For example, quoted prices for similar assets or liabilities in active markets or quoted prices for identical assets or liabilities in inactive markets.

|

|

Level 3

|

|

–

|

|

Unobservable inputs for which there is little or no market data available.

|

The carrying values of cash, trade accounts receivable and accounts payable approximate their fair values at each balance sheet date because of the short-term maturities and nature of these balances.

The carrying value of our revolving credit facility borrowings approximates fair value at each balance sheet date because interest rates on this instrument approximate current market rates (Level 2 criteria), and because of the short-term maturity and nature of this balance. In addition, there has been no significant change in our inherent credit risk.

15

The following table summarizes the carrying value and fair value estimate of our current and long-term debt, excluding unamortized debt issuance costs:

|

March 25,

2021 |

June 25,

2020

|

March 26,

2020

|

||||||||||

|

Carrying value of long-term debt:

|

$ |

|

$ |

|

$ |

|

||||||

|

Fair value of long-term debt:

|

|

|

|

|||||||||

The estimated fair value of our long-term debt was determined using a market approach based upon Level 2 observable inputs, which estimates fair value based on interest rates currently offered on loans with similar terms to borrowers of similar credit quality or broker quotes. In addition, there have been no significant changes in the underlying assets securing our long-term debt.

Note 13 – Related Party Transaction

In connection with the acquisition of the Squirrel Brand business in the second quarter of fiscal 2018, we incurred $

11,500

of unsecured debt pursuant to a promissory note (the “Promissory Note”) to the principal owner and seller of the Squirrel Brand business, who was subsequently appointed as an executive officer of the Company and was considered a related party. Late in the second quarter of fiscal 2020, the employment of this executive officer with the Company ceased. He is no longer considered a related party, and therefore the outstanding bala

, 2021 or the quarter ended March

127

for the thirty-nine weeks ended March

n

ce on the Promissory Note is not reflected as related party debt on our Consolidated Balance Sheet for any periods presented. There was no related party interest paid to this former executive officer during the thirty-nine weeks ended March

25

26

, 2020. Interest paid while the former executive officer was a related party was $

26

, 2020.

Note 14 – Garysburg, North Carolina Facility

On October 7, 2019 we experienced a fire at our peanut processing facility located in Garysburg, North Carolina. The fire occurred in our roasting room where all of the roasting equipment was destroyed. The fire also damaged some equipment in our packaging room and a portion of the roof. During fiscal 2020, the building and roof were repaired and brought back to their original condition.

After evaluating our options with regard to our peanut production operations, the Company currently plans to cease all operations permanently at the Garysburg facility. We completed shelling of the 2019 peanut crop during the second quarter of this fiscal year and the facility will continue to be used to store and ship inshell peanuts through the remainder of fiscal 2021. During fiscal 2020 we manufactured and sold approximately

6

million pounds of inshell peanuts from this facility and plan to discontinue that product line at the end of the current fiscal year. We also expect to spend the remainder of the 2021 fiscal year cleaning and preparing the facility for sale or other utilization in our operations. Employee separation and related closure costs were immaterial for all periods presented.

Insurance proceeds totaling $

2,934

were received from the insurance carrier in fiscal 2020, and the final payment of $

2,730

was received during the current third quarter. Insurance proceeds received for damage to capital equipment are recorded as investing activities on the Consolidated Statements of Cash Flows when received.

Note 15 – Recent Accounting Pronouncements

The following recent accounting pronouncements have been adopted in the current fiscal year:

In August 2018, the FASB issued ASU

”. The amendments in this Update align the requirements for capitalizing implementation costs incurred in a hosting arrangement that is a service contract with the requirements for capitalizing implementation costs incurred to develop or obtain

No. 2018-15

“

Intangibles – Goodwill and Other –

Internal-Use

Software (Subtopic

350-40):

Customer’s Accounting for Implementation Costs Incurred in a Cloud Computing Arrangement that is a Service Contract

internal-use

software (and hosting arrangements that include an internal use software license). ASU

No. 2018-15

was adopted using the prospective method in the first quarter of fiscal 2021 and did not have a material impact on our Consolidated Financial Statements.

16

In August 2018, the FASB issued ASU

”. The amendments in this Update modify the disclosure requirements for employers that sponsor defined benefit pension or other postretirement plans. The amendments in this Update remove disclosures that no longer are considered cost beneficial, clarify the specific requirements of disclosures, and add disclosure requirements identified as relevant. ASU

No. 2018-14

“

Compensation – Retirement Benefits – Defined Benefit Plans – General (Subtopic

715-20):

Disclosure Framework – Changes to the Disclosure Requirements for Defined Benefit Plans

No. 2018-14

was adopted on a retrospective basis to all periods presented in the first quarter of fiscal 2021 and had no impact on our quarterly Consolidated Financial Statements.

In January 2017, the FASB issued ASU

The amendments in this Update eliminate the need for entities to calculate the implied fair value of goodwill by assigning the fair value of a reporting unit to all of its assets and liabilities as if that reporting unit had been acquired in a business combination, commonly referred to as “Step 2”. Under this amendment, an entity will perform its goodwill impairment test by comparing the fair value of a reporting unit with its carrying amount. An impairment charge is recognized for the amount by which the carrying value exceeds the reporting unit’s fair value. ASU

No. 2017-04

“Intangibles—Goodwill and Other (Topic 350): Simplifying the Test for Goodwill Impairment”.

No. 2017-04

was adopted in the first quarter of fiscal 2021 and did not have a material impact on our Consolidated Financial Statements.

In June 2016, the FASB issued ASU

”. The main objective of this Update is to provide financial statement users with more decision-useful information about the expected credit losses on financial instruments and other commitments to extend credit held by a reporting entity at each reporting date. The amendments in this Update replace the incurred loss impairment methodology in current GAAP with a methodology that reflects expected credit losses and requires consideration of a broader range of reasonable and supportable information to inform credit loss estimates. ASU

No. 2016-13

“

Financial Instruments—Credit Losses (Topic 326): Measurement of Credit Losses on Financial Instruments

No. 2016-13

was adopted using a modified retrospective transition method in the first quarter of fiscal 2021 and did not have a material impact on our Consolidated Financial Statements.

There are no recent accounting pronouncements that have been issued and not yet adopted that are expected to have a material impact on our Consolidated Financial Statements.

17

Item 2. Management’s Discussion and Analysis of Financial Condition and Results of Operations

OVERVIEW

The following discussion and analysis should be read in conjunction with the unaudited Consolidated Financial Statements and the Notes to Consolidated Financial Statements.

Our fiscal year ends on the final Thursday of June each year, and typically consists of

fifty-two

weeks (four thirteen-week quarters). Additional information on the comparability of the periods presented is as follows:

| • |

References herein to fiscal 2021 and fiscal 2010 are to the fiscal year ending June 24, 2021 and the fiscal year ended June 25, 2020, respectively.

|

| • |

References herein to the third quarter of fiscal 2021 and fiscal 2020 are to the quarters ended March 25, 2021 and March 26, 2020, respectively.

|

| • |

References herein to the first three quarters or first thirty-nine weeks of fiscal 2021 and fiscal 2021 are to the thirty-nine weeks ended March 25, 2021 and March 26, 2020, respectively.

|

As used herein, unless the context otherwise indicates, the terms “we”, “us”, “our” or “Company” collectively refer to John B. Sanfilippo & Son, Inc. and our wholly-owned subsidiary, JBSS Ventures, LLC. Our Company’s Credit Facility and Mortgage Facility, as defined below, are sometimes collectively referred to as “our financing arrangements.”

We are one of the leading processors and distributors of peanuts, pecans, cashews, walnuts, almonds and other nuts in the United States. These nuts are sold under our

and

brand names and under a variety of private brands. We also market and distribute, and in most cases, manufacture or process, a diverse product line of food and snack products, including peanut butter, almond butter, cashew butter, candy and confections, snacks and trail mixes, snack bites, sunflower kernels, dried fruit, corn snacks, chickpea snacks, sesame sticks and other sesame snack products under our brand names and under private brands. We distribute our products in the consumer, commercial ingredients and contract packaging distribution channels.

Fisher, Orchard Valley Harvest,

Squirrel Brand, Southern Style Nuts

Sunshine Country

The Company’s long-term objective to drive profitable growth, as identified in our strategic plan (the “Strategic Plan”), includes continuing to grow

and

into leading brands and providing integrated nut solutions to grow

Fisher,

Orchard Valley Harvest, Squirrel Brand

Southern Style Nuts

non-branded

business across key customers. We plan to execute on our Strategic Plan to grow our branded business by reaching new consumers via product and packaging innovation, expanding distribution across current and alternative channels, diversifying our product offerings and focusing on new ways for consumers to buy our products, with an emphasis on increasing our sales via

e-commerce

platforms and retailers. In addition, during fiscal 2021 we have invested in our people and facilities in order to research, develop, market and sell new products in snack categories we currently are not in for our branded business and private brand partners.

We face a number of challenges in the future which include intensified competition on pricing and for market share from both private brand and name brand nut products. Our

recipe nut sales have been negatively impacted due to this increased competition for market share. We also face changing industry trends as consumer preferences evolve into shopping in smaller store formats like grocery and online. Additionally, the wooden pallet industry has been impacted for several months with low inventory levels, due in part to labor and lumber shortages. The pallet shortage has impacted our operations, primarily at our Elgin, IL facility, and led to some cost increases. We anticipate the industry to see some relief in the coming quarters. In the interim, we are working with our vendors, customers and JBSS facilities in other regions of the country to source additional supply. If the shortage continues, and we cannot secure an adequate supply of wooden pallets to fulfill customer orders, this shortage could have an unfavorable impact on net sales in our fourth quarter.

Fisher

18

We will continue to focus on seeking profitable business opportunities to maximize the utilization of our production capacity at our primary manufacturing, processing and distribution facility located in Elgin, Illinois. We expect to redirect our promotional and advertising activity with respect to our brands to focus on more digital and

branded products and expect that there will be additional opportunities to connect these brands to consumers’ desires for more functional snacking, baking and cooking ideas. We will continue to face the ongoing challenges specific to our business, such as food safety and regulatory compliance and the maintenance and growth of our customer base for branded and private label products. See the information referenced in Part II, Item 1A — “Risk Factors” of this report for additional information about our risks, challenges and uncertainties.

e-commerce

platforms to match consumer behavior. We continue to see strong

e-commerce

performance across several of our

COVID-19

Impacts

We will continue to face challenges in the remainder of our fiscal 2021 (and into fiscal year 2022) as result of the

COVID-19

pandemic and the uncertainty of future local, state and federal restrictions aimed to mitigate and control the pandemic. As many of these restrictions were eased near the conclusion of our fiscal 2020, we saw a gradual (albeit limited) increase in demand from our foodservice, restaurant, convenience store and

non-essential

retail customers. However, as conditions surrounding the pandemic deteriorated during the fall and winter of calendar 2020 and so far during calendar 2021, consumers were and continue to be limited in their ability to purchase meals outside their homes. As indoor dining restrictions continued due to the impact of

COVID-19,

consumers continued to snack, cook and bake more at home. While this trend has had a positive impact on certain aspects of our consumer business, demand continued to be suppressed from our foodservice, restaurant and

non-essential

retail customers. Additionally,

COVID-19

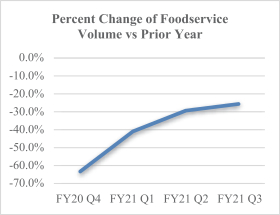

has had an unfavorable impact on a major customer’s business in our contract packaging distribution channel due to reduced foot traffic in convenience stores as people continue to work from home. Although demand has been suppressed from our foodservice customers, the chart below indicates that the rate of decline is recovering from its low point in our fourth quarter of fiscal 2020, and we believe that as the

COVID-19

vaccine becomes more widely distributed and accepted by the public, and restrictions are again loosened, sales volume with our foodservice, restaurant, convenience store and

non-essential

retail customers will continue to improve.

Also, during fiscal 2021, we have seen signs of a shortage in capacity in the transportation industry, which our transportation service providers believe is due, in part, to driver concerns related to the impacts of

COVID-19.

Compounding this driver shortage is an increase in demand driven by additional spending on consumer goods. This tightening in transportation capacity, including rail and ocean freight, is expected to continue into fiscal 2022, has led to increased transportation costs and may lead to potential disruptions in service to our customers and from our suppliers.

The Company’s

COVID-19