Table of Contents

As filed with the Securities and Exchange Commission on April 29, 2015

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

WASHINGTON, D.C. 20549

FORM 20-F

(Mark One)

| ¨ | REGISTRATION STATEMENT PURSUANT TO SECTION 12(b) OR (g) OF THE SECURITIES EXCHANGE ACT OF 1934 |

OR

| x | ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the fiscal year ended December 31, 2014

OR

| ¨ | TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the transition period from to .

OR

| ¨ | SHELL COMPANY REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

Date of event requiring this shell company report .

Commission file number 000-53445

KB Financial Group Inc.

(Exact name of Registrant as specified in its charter)

KB Financial Group Inc.

(Translation of Registrant’s name into English)

The Republic of Korea

(Jurisdiction of incorporation or organization)

84, Namdaemoon-ro, Jung-gu, Seoul 100-703, Korea

(Address of principal executive offices)

Kyu Sul Choi

84, Namdaemoon-ro, Jung-gu, Seoul 100-703, Korea

Telephone No.: +82-2-2073-2844

Facsimile No.: +82-2-2073-2848

(Name, telephone, e-mail and/or facsimile number and address of company contact person)

Securities registered or to be registered pursuant to Section 12(b) of the Act.

|

Title of each class |

Name of each exchange on which registered |

|

|

American Depositary Shares, each representing

one share of Common Stock |

New York Stock Exchange | |

| Common Stock, par value ₩5,000 per share | New York Stock Exchange* |

Securities registered or to be registered pursuant to Section 12(g) of the Act.

None

Securities for which there is a reporting obligation pursuant to Section 15(d) of the Act.

None

Indicate the number of outstanding shares of each of the issuer’s classes of capital or common stock as of the close of the period covered by the annual report.

386,351,693 shares of Common Stock, par value ₩ 5,000 per share

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. x Yes ¨ No

If this report is an annual or transition report, indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or 15(d) of the Securities Exchange Act of 1934. ¨ Yes x No

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. x Yes ¨ No

Indicate by check mark whether the registrant has submitted electronically and posted on its Web site, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T (§232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files). ¨ Yes ¨ No

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, or a non-accelerated filer. See definition of “accelerated filer and large accelerated filer” in Rule 12b-2 of the Exchange Act. (Check one):

x Large accelerated filer ¨ Accelerated filer ¨ Non-accelerated filer

Indicate by check mark which basis of accounting the registrant has used to prepare the financial statements included in this filing:

| ¨ U.S. GAAP |

x International Financial Reporting Standards as issued by the International Accounting Standards Board |

¨ | Other | |||||

If “Other” has been checked in response to the previous question, indicate by check mark which financial statement item the registrant has elected to follow. ¨ Item 17 ¨ Item 18

If this is an annual report, indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act). ¨ Yes x No

(APPLICABLE ONLY TO ISSUERS INVOLVED IN BANKRUPTCY PROCEEDINGS DURING THE PAST FIVE YEARS)

Indicate by check mark whether the registrant has filed all documents and reports required to be filed by Sections 12, 13 or 15(d) of the Securities Exchange Act of 1934 subsequent to the distribution of securities under a plan confirmed by a court. ¨ Yes ¨ No

| * | Not for trading, but only in connection with the registration of the American Depositary Shares. |

Table of Contents

i

Table of Contents

ii

Table of Contents

PRESENTATION OF FINANCIAL AND OTHER INFORMATION

The financial statements included in this annual report are prepared in accordance with International Financial Reporting Standards, or IFRS, as issued by the International Accounting Standards Board, or IASB. As such, we make an explicit and unreserved statement of compliance with IFRS as issued by the IASB with respect to our consolidated financial statements as of January 1, 2013, December 31, 2013 and 2014 and for the years ended December 31, 2012, 2013 and 2014 included in this annual report. Unless indicated otherwise, the financial information in this annual report as of and for the years ended December 31, 2010, 2011, 2012, 2013 and 2014 has been prepared in accordance with IFRS as issued by the IASB, which is not comparable to information prepared in accordance with generally accepted accounting principles in the United States, or U.S. GAAP.

In accordance with rule amendments adopted by the U.S. Securities and Exchange Commission which became effective on March 4, 2008, we are not required to provide a reconciliation to U.S. GAAP.

Unless expressly stated otherwise, all financial data included in this annual report are presented on a consolidated basis.

In this annual report:

| • |

references to “we,” “us” or “KB Financial Group” are to KB Financial Group Inc. and, unless the context otherwise requires, its subsidiaries; |

| • |

references to “Korea” are to the Republic of Korea; |

| • |

references to the “government” are to the government of the Republic of Korea; |

| • |

references to “Won” or “₩” are to the currency of Korea; and |

| • |

references to “U.S. dollars,” “$” or “US$” are to United States dollars. |

Discrepancies between totals and the sums of the amounts contained in any table may be a result of rounding.

For your convenience, this annual report contains translations of Won amounts into U.S. dollars at the noon buying rate of the Federal Reserve Bank of New York for Won in effect on December 31, 2014, which was ₩1,090.9 = US$1.00.

1

Table of Contents

The U.S. Securities and Exchange Commission encourages companies to disclose forward-looking information so that investors can better understand a company’s future prospects and make informed investment decisions. This annual report contains forward-looking statements.

Words and phrases such as “aim,” “anticipate,” “assume,” “believe,” “contemplate,” “continue,” “estimate,” “expect,” “future,” “goal,” “intend,” “may,” “objective,” “plan,” “positioned,” “predict,” “project,” “risk,” “seek to,” “shall,” “should,” “will likely result,” “will pursue,” “plan” and words and terms of similar substance used in connection with any discussion of future operating or financial performance or our expectations, plans, projections or business prospects identify forward-looking statements. In particular, the statements under the headings “Item 3.D. Risk Factors,” “Item 5. Operating and Financial Review and Prospects” and “Item 4.B. Business Overview” regarding our financial condition and other future events or prospects are forward-looking statements. All forward-looking statements are management’s present expectations of future events and are subject to a number of factors and uncertainties that could cause actual results to differ materially from those described in the forward-looking statements.

In addition to the risks related to our business discussed under “Item 3.D. Risk Factors,” other factors could cause actual results to differ materially from those described in the forward-looking statements. These factors include, but are not limited to:

| • |

our ability to successfully implement our strategy; |

| • |

future levels of non-performing loans; |

| • |

our growth and expansion; |

| • |

the adequacy of allowances for credit and investment losses; |

| • |

technological changes; |

| • |

interest rates; |

| • |

investment income; |

| • |

availability of funding and liquidity; |

| • |

cash flow projections; |

| • |

our exposure to market risks; and |

| • |

adverse market and regulatory conditions. |

By their nature, certain disclosures relating to these and other risks are only estimates and could be materially different from what actually occurs in the future. As a result, actual future gains, losses or impact on our income or results of operations could materially differ from those that have been estimated. For example, revenues could decrease, costs could increase, capital costs could increase, capital investment could be delayed and anticipated improvements in performance might not be fully realized.

In addition, other factors that could cause actual results to differ materially from those estimated by the forward-looking statements contained in this annual report could include, but are not limited to:

| • |

general economic and political conditions in Korea or other countries that have an impact on our business activities or investments; |

| • |

the monetary and interest rate policies of Korea; |

| • |

inflation or deflation; |

| • |

unanticipated volatility in interest rates; |

2

Table of Contents

| • |

foreign exchange rates; |

| • |

prices and yields of equity and debt securities; |

| • |

the performance of the financial markets in Korea and globally; |

| • |

changes in domestic and foreign laws, regulations and taxes; |

| • |

changes in competition and the pricing environments in Korea; and |

| • |

regional or general changes in asset valuations. |

For further discussion of the factors that could cause actual results to differ, see the discussion under “Item 3.D. Risk Factors” contained in this annual report. We caution you not to place undue reliance on the forward-looking statements, which speak only as of the date of this annual report. Except as required by law, we are not under any obligation, and expressly disclaim any obligation, to update or alter any forward-looking statements, whether as a result of new information, future events or otherwise.

All subsequent forward-looking statements attributable to us or any person acting on our behalf are expressly qualified in their entirety by the cautionary statements contained or referred to in this annual report.

| Item 1. | IDENTITY OF DIRECTORS, SENIOR MANAGEMENT AND ADVISERS |

Not applicable.

| Item 2. | OFFER STATISTICS AND EXPECTED TIMETABLE |

Not applicable.

| Item 3. | KEY INFORMATION |

| Item 3.A. | Selected Financial Data |

The selected consolidated financial and operating data set forth below as of and for the years ended December 31, 2010, 2011, 2012, 2013 and 2014 have been derived from our audited consolidated financial statements, which have been prepared in accordance with IFRS as issued by the IASB. Our consolidated financial statements as of and for the years ended December 31, 2010, 2011, 2012, 2013 and 2014 have been audited by independent registered public accounting firm Samil PricewaterhouseCoopers.

You should read the following data together with the more detailed information contained in “Item 5. Operating and Financial Review and Prospects” and our consolidated financial statements included elsewhere in this annual report. Historical results do not necessarily predict future results.

3

Table of Contents

| Year Ended December 31, | ||||||||||||||||||||||||

| 2010 (1) | 2011 (1) | 2012 (1)(2) | 2013 (1)(2) | 2014 (1)(2) | 2014 (3) | |||||||||||||||||||

| (in billions of Won, except common share data) |

(in millions of US$,

except common share data) |

|||||||||||||||||||||||

|

Interest income |

₩ | 13,052 | ₩ | 13,956 | ₩ | 14,210 | ₩ | 12,357 | ₩ | 11,635 | US$ | 10,666 | ||||||||||||

|

Interest expense |

(6,878 | ) | (6,852 | ) | (7,172 | ) | (5,834 | ) | (5,219 | ) | (4,785 | ) | ||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||

|

Net interest income |

6,174 | 7,104 | 7,038 | 6,523 | 6,416 | 5,881 | ||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||

|

Fee and commission income |

2,482 | 2,830 | 2,754 | 2,657 | 2,666 | 2,444 | ||||||||||||||||||

|

Fee and commission expense |

(777 | ) | (1,035 | ) | (1,187 | ) | (1,178 | ) | (1,283 | ) | (1,176 | ) | ||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||

|

Net fee and commission income |

1,705 | 1,795 | 1,567 | 1,479 | 1,383 | 1,268 | ||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||

|

Net gains on financial assets and liabilities at fair value through profit or loss |

815 | 1,036 | 812 | 757 | 439 | 403 | ||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||

|

Net other operating income (expenses) |

(1,068 | ) | (1,092 | ) | (1,532 | ) | (1,305 | ) | (1,041 | ) | (954 | ) | ||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||

|

General and administrative expenses |

(4,380 | ) | (3,887 | ) | (3,846 | ) | (3,984 | ) | (4,010 | ) | (3,676 | ) | ||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||

|

Operating profit before provision for credit losses |

3,246 | 4,956 | 4,039 | 3,470 | 3,187 | 2,922 | ||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||

|

Provision for credit losses |

(2,871 | ) | (1,513 | ) | (1,607 | ) | (1,443 | ) | (1,228 | ) | (1,126 | ) | ||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||

|

Net operating profit |

375 | 3,443 | 2,432 | 2,027 | 1,959 | 1,796 | ||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||

|

Share of profit (loss) of associates and joint ventures |

(211 | ) | 5 | (15 | ) | (199 | ) | 13 | 12 | |||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||

|

Net other non-operating income (expense) |

(28 | ) | (142 | ) | (118 | ) | (12 | ) | (71 | ) | (65 | ) | ||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||

|

Net non-operating profit (loss) |

(239 | ) | (137 | ) | (133 | ) | (211 | ) | (58 | ) | (53 | ) | ||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||

|

Profit before income tax |

136 | 3,306 | 2,299 | 1,816 | 1,901 | 1,743 | ||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||

|

Tax income (expense) (4) |

(254 | ) | (565 | ) | (520 | ) | (541 | ) | (486 | ) | (446 | ) | ||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||

|

Profit for the year (4) |

₩ | (118 | ) | ₩ | 2,741 | ₩ | 1,779 | ₩ | 1,275 | ₩ | 1,415 | US$ | 1,297 | |||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||

|

Items that will not be reclassified to profit or loss: |

||||||||||||||||||||||||

|

Actuarial gains (losses) on post defined benefit pension plans |

9 | (32 | ) | (30 | ) | 41 | (100 | ) | (91 | ) | ||||||||||||||

|

Items that may be reclassified subsequently to profit or loss: |

||||||||||||||||||||||||

|

Exchange differences on translating foreign operations |

(7 | ) | 6 | (26 | ) | (2 | ) | 17 | 16 | |||||||||||||||

|

Change in value of financial investments |

108 | (240 | ) | 246 | (4 | ) | 249 | 228 | ||||||||||||||||

|

Shares of other comprehensive loss of associates and joint ventures |

(2 | ) | (1 | ) | (44 | ) | (10 | ) | (32 | ) | (29 | ) | ||||||||||||

|

Cash flow hedges |

— | (1 | ) | (1 | ) | 2 | (10 | ) | (10 | ) | ||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||

|

Other comprehensive income (loss) for the year, net of tax |

108 | (268 | ) | 145 | 27 | 124 | 114 | |||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||

|

Total comprehensive income for

the

|

₩ | (10 | ) | ₩ | 2,473 | ₩ | 1,924 | ₩ | 1,302 | ₩ | 1,539 | US$ | 1,411 | |||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||

|

Profit attributable to: |

||||||||||||||||||||||||

|

Stockholders |

₩ | (191 | ) | ₩ | 2,686 | ₩ | 1,770 | ₩ | 1,272 | ₩ | 1,401 | US$ | 1,284 | |||||||||||

|

Non-controlling interests |

73 | 55 | 9 | 3 | 14 | 13 | ||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||

| ₩ | (118 | ) | ₩ | 2,741 | ₩ | 1,779 | ₩ | 1,275 | ₩ | 1,415 | US$ | 1,297 | ||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||

|

Total comprehensive income attributable to: |

||||||||||||||||||||||||

|

Stockholders |

₩ | (103 | ) | ₩ | 2,414 | ₩ | 1,904 | ₩ | 1,313 | ₩ | 1,526 | US$ | 1,399 | |||||||||||

|

Non-controlling interests |

93 | 59 | 20 | (11 | ) | 13 | 12 | |||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||

| ₩ | (10 | ) | ₩ | 2,473 | ₩ | 1,924 | ₩ | 1,302 | ₩ | 1,539 | US$ | 1,411 | ||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||

|

Earnings per share (4) |

||||||||||||||||||||||||

|

Basic earnings per share |

₩ | (558 | ) | ₩ | 7,310 | ₩ | 4,580 | ₩ | 3,291 | ₩ | 3,626 | US$ | 3.32 | |||||||||||

|

Diluted earnings per share |

(558 | ) | 7,293 | 4,567 | 3,277 | 3,611 | 3.31 | |||||||||||||||||

4

Table of Contents

| (1) |

Pursuant to amendments to International Accounting Standards 19, or IAS 19, Employee Benefits , which are effective beginning in 2013, our consolidated financial statements as of and for the years ended December 31, 2013 and 2014 reflect changes in the methodology for recognition and measurement of actuarial gains and losses and expected returns and service costs relating to our employee pension plans. Our consolidated financial statements as of and for the year ended December 31, 2012 have been restated to retroactively apply such changes. Amounts for 2012 reflect such restatement, and amounts for 2010 and 2011 have been correspondingly restated. |

| (2) |

Pursuant to the adoption of IFRS 10, Consolidated Financial Statements , which is effective beginning in 2013, our consolidated financial statements as of and for the years ended December 31, 2013 and 2014 include trust accounts for which we guarantee only the repayment of principal, as well as certain other entities, which were not previously subject to consolidation, while excluding certain other entities that were previously consolidated. Our consolidated financial statements as of and for the year ended December 31, 2012 have been restated to retroactively apply this change. Amounts for 2012 reflect such restatement, while amounts for 2010 and 2011 have not been correspondingly restated. |

| (3) |

Won amounts are expressed in U.S. dollars at the rate of ₩1,090.9 to US$1.00, the noon buying rate in effect on December 31, 2014 as quoted by the Federal Reserve Bank of New York in the United States. |

| (4) |

The amounts for 2014 reflect a change in our accounting policy with respect to uncertain tax positions in 2014, based on the guidance in International Accounting Standards 12, or IAS 12, Income Taxes , which allows recognition of tax payments as current income tax assets to the extent it is probable that they will be recovered from the tax authorities. Corresponding amounts for 2010, 2011, 2012 and 2013 have been restated to retroactively apply this change. See “Item 5.A. Operating Results—Overview—Changes in Accounting Policies” and Note 2.1 of the notes to our consolidated financial statements included elsewhere in this annual report. |

Consolidated statements of financial position data

| Year Ended December 31, | ||||||||||||||||||||||||

| 2010 (1) | 2011 (1) | 2012 (1)(2) | 2013 (1)(2) | 2014 (1)(2) | 2014 (3) | |||||||||||||||||||

| (in billions of Won) |

(in millions of US$) |

|||||||||||||||||||||||

|

Assets |

||||||||||||||||||||||||

|

Cash and due from financial institutions |

₩ | 6,830 | ₩ | 9,178 | ₩ | 10,593 | ₩ | 14,793 | ₩ | 15,424 | US$ | 14,139 | ||||||||||||

|

Financial assets at fair value through profit or loss |

4,014 | 6,326 | 9,560 | 9,329 | 10,758 | 9,862 | ||||||||||||||||||

|

Derivative financial assets |

2,595 | 2,449 | 2,091 | 1,819 | 1,968 | 1,804 | ||||||||||||||||||

|

Loans |

197,621 | 212,107 | 213,645 | 219,001 | 231,450 | 212,166 | ||||||||||||||||||

|

Financial investments |

36,190 | 35,432 | 36,467 | 34,849 | 34,961 | 32,048 | ||||||||||||||||||

|

Investments in associates and joint ventures |

723 | 892 | 935 | 755 | 670 | 614 | ||||||||||||||||||

|

Property and equipment |

3,150 | 3,186 | 3,100 | 3,061 | 3,083 | 2,826 | ||||||||||||||||||

|

Investment property |

53 | 52 | 53 | 166 | 378 | 346 | ||||||||||||||||||

|

Intangible assets |

505 | 468 | 493 | 443 | 489 | 448 | ||||||||||||||||||

|

Current income tax assets (4)(5) |

135 | 292 | 333 | 347 | 306 | 281 | ||||||||||||||||||

|

Deferred income tax assets |

4 | 22 | 18 | 16 | 16 | 14 | ||||||||||||||||||

|

Assets held for sale |

9 | 10 | 35 | 38 | 70 | 64 | ||||||||||||||||||

|

Other assets (5) |

6,942 | 7,467 | 8,747 | 7,551 | 8,783 | 8,052 | ||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||

|

Total assets |

₩ | 258,771 | ₩ | 277,881 | ₩ | 286,070 | ₩ | 292,168 | ₩ | 308,356 | US$ | 282,664 | ||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||

|

Liabilities |

||||||||||||||||||||||||

|

Financial liabilities at fair value through profit or loss |

₩ | 1,295 | ₩ | 1,388 | ₩ | 1,851 | ₩ | 1,115 | ₩ | 1,819 | US$ | 1,667 | ||||||||||||

|

Derivative financial liabilities |

2,236 | 2,059 | 2,055 | 1,795 | 1,797 | 1,648 | ||||||||||||||||||

|

Deposits |

179,862 | 190,337 | 197,346 | 200,882 | 211,549 | 193,923 | ||||||||||||||||||

|

Debts |

11,745 | 16,824 | 15,965 | 14,101 | 15,865 | 14,543 | ||||||||||||||||||

|

Debentures |

29,107 | 27,070 | 24,270 | 27,040 | 29,201 | 26,768 | ||||||||||||||||||

|

Provisions |

1,020 | 798 | 670 | 678 | 614 | 563 | ||||||||||||||||||

|

Defined benefit liabilities |

125 | 128 | 84 | 64 | 76 | 69 | ||||||||||||||||||

|

Current income tax liabilities |

30 | 589 | 265 | 211 | 232 | 213 | ||||||||||||||||||

|

Deferred income tax liabilities |

284 | 221 | 154 | 62 | 93 | 85 | ||||||||||||||||||

|

Other liabilities |

13,401 | 15,087 | 18,328 | 20,237 | 19,597 | 17,965 | ||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||

|

Total liabilities |

₩ | 239,105 | ₩ | 254,501 | ₩ | 260,988 | ₩ | 266,185 | ₩ | 280,843 | US$ | 257,444 | ||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||

5

Table of Contents

| Year Ended December 31, | ||||||||||||||||||||||||

| 2010 (1) | 2011 (1) | 2012 (1)(2) | 2013 (1)(2) | 2014 (1)(2) | 2014 (3) | |||||||||||||||||||

| (in billions of Won) |

(in millions of US$) |

|||||||||||||||||||||||

|

Total Equity |

||||||||||||||||||||||||

|

Capital stock |

₩ | 1,932 | ₩ | 1,932 | ₩ | 1,932 | ₩ | 1,932 | ₩ | 1,932 | US$ | 1,771 | ||||||||||||

|

Capital surplus |

15,990 | 15,842 | 15,840 | 15,855 | 15,855 | 14,534 | ||||||||||||||||||

|

Accumulated other comprehensive income |

440 | 168 | 295 | 336 | 461 | 422 | ||||||||||||||||||

|

Retained earnings (4) |

2,612 | 5,256 | 6,820 | 7,860 | 9,067 | 8,312 | ||||||||||||||||||

|

Treasury shares |

(2,477 | ) | — | — | — | — | — | |||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||

|

Equity attributable to stockholders |

18,497 | 23,198 | 24,887 | 25,983 | 27,315 | 25,039 | ||||||||||||||||||

|

Non-controlling interests |

1,169 | 182 | 195 | — | 198 | 181 | ||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||

|

Total equity |

₩ | 19,666 | ₩ | 23,380 | ₩ | 25,082 | ₩ | 25,983 | ₩ | 27,513 | US$ | 25,220 | ||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||

|

Total liabilities and equity |

₩ | 258,771 | ₩ | 277,881 | ₩ | 286,070 | ₩ | 292,168 | ₩ | 308,356 | US$ | 282,664 | ||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||

| (1) |

Pursuant to amendments to IAS19, Employee Benefits , which are effective beginning in 2013, our consolidated financial statements as of and for the years ended December 31, 2013 and 2014 reflect changes in the methodology for recognition and measurement of actuarial gains and losses and expected returns and service costs relating to our employee pension plans. Our consolidated financial statements as of and for the year ended December 31, 2012 have been restated to retroactively apply such changes. Amounts as of December 31, 2012 reflect such restatement, and amounts as of December 31, 2010 and 2011 have been correspondingly restated. |

| (2) |

Pursuant to the adoption of IFRS 10, Consolidated Financial Statements , which is effective beginning in 2013, our consolidated financial statements as of and for the years ended December 31, 2013 and 2014 include trust accounts for which we guarantee only the repayment of principal, as well as certain other entities, which were not previously subject to consolidation, while excluding certain other entities that were previously consolidated. Our consolidated financial statements as of and for the year ended December 31, 2012 have been restated to retroactively apply this change. Amounts as of December 31, 2012 reflect such restatement, while amounts as of December 31, 2010 and 2011 have not been correspondingly restated. |

| (3) |

Won amounts are expressed in U.S. dollars at the rate of ₩1,090.9 to US$1.00, the noon buying rate in effect on December 31, 2014 as quoted by the Federal Reserve Bank of New York in the United States. |

| (4) |

The amounts as of December 31, 2014 reflect a change in our accounting policy with respect to uncertain tax positions in 2014, based on the guidance in IAS 12, Income Taxes , which allows recognition of tax payments as current income tax assets to the extent it is probable that they will be recovered from the tax authorities. Corresponding amounts as of December 31, 2010, 2011, 2012 and 2013 have been restated to retroactively apply this change. See “Item 5.A. Operating Results—Overview—Changes in Accounting Policies” and Note 2.1 of the notes to our consolidated financial statements included elsewhere in this annual report. |

| (5) |

Prepaid income tax expenses amounting to ₩135 billion, ₩12 billion, ₩15 billion and ₩18 billion as of December 31, 2010, 2011, 2012 and 2013, respectively, have been reclassified from other assets into current income tax assets. See Note 33 of the notes to our consolidated financial statements included elsewhere in this annual report. |

Profitability ratios and other data

| As of or for the year Ended December 31, | ||||||||||||||||||||

| 2010 | 2011 | 2012 | 2013 | 2014 | ||||||||||||||||

| (Percentages) | ||||||||||||||||||||

|

Profit (loss) attributable to stockholders as a percentage of: |

||||||||||||||||||||

|

Average total assets (1) |

(0.07 | )% | 0.99 | % | 0.60 | % | 0.44 | % | 0.47 | % | ||||||||||

|

Average stockholders’ equity (1) |

(0.98 | ) | 11.47 | 7.13 | 5.00 | 5.30 | ||||||||||||||

|

Dividend payout ratio (2) |

(21.47 | ) | 10.23 | 13.40 | 15.01 | 21.48 | ||||||||||||||

|

Net interest spread (3) |

2.37 | 2.64 | 2.48 | 2.31 | 2.22 | |||||||||||||||

|

Net interest margin (4) |

2.58 | 2.88 | 2.71 | 2.51 | 2.39 | |||||||||||||||

|

Efficiency ratio (5) |

57.44 | 43.96 | 48.78 | 53.45 | 55.72 | |||||||||||||||

|

Cost-to-average assets ratio (6) |

1.64 | 1.41 | 1.33 | 1.37 | 1.34 | |||||||||||||||

|

Won loans (gross) as a percentage of Won deposits |

107.56 | 107.97 | 106.37 | 107.12 | 107.73 | |||||||||||||||

|

Total loans (gross) as a percentage of total deposits |

111.96 | 113.25 | 109.92 | 110.44 | 110.57 | |||||||||||||||

6

Table of Contents

| (1) |

Average balances are based on daily balances for our banking, credit card and investment and securities operations and monthly or quarterly balances for our other operations. |

| (2) |

Represents the ratio of total dividends declared on common stock as a percentage of profit attributable to stockholders. |

| (3) |

Represents the difference between the yield on average interest earning assets and cost of average interest bearing liabilities. |

| (4) |

Represents the ratio of net interest income to average interest earning assets. |

| (5) |

Represents the ratio of general and administrative expenses to the sum of net interest income, net fee and commission income, net gain on financial assets and liabilities at fair value through profit or loss and net other operating income. |

| (6) |

Represents the ratio of general and administrative expenses to average total assets. |

Capital ratios

| As of or for the year Ended December 31, | ||||||||||||

| 2012 (1) | 2013 | 2014 | ||||||||||

| (Percentages) | ||||||||||||

|

Consolidated capital adequacy ratio of KB Financial Group (2) |

13.90 | % | 15.38 | % | 15.53 | % | ||||||

|

Capital adequacy ratios of Kookmin Bank |

||||||||||||

|

Tier I capital adequacy ratio (3) |

10.87 | 12.61 | 13.38 | |||||||||

|

Common equity Tier I capital adequacy ratio (3) |

— | 12.61 | 13.38 | |||||||||

|

Tier II capital adequacy ratio (3) |

3.53 | 2.81 | 2.59 | |||||||||

|

Average stockholders’ equity as a percentage of average total assets |

8.47 | 8.87 | 8.83 | |||||||||

| (1) |

With effect from December 1, 2013, the Financial Services Commission adopted amended guidelines that implemented capital adequacy requirements in Korea based on Basel III. Capital adequacy ratios as of December 31, 2012 were computed in accordance with previously applicable guidelines based on Basel I (for KB Financial Group) and Basel II (for Kookmin Bank) and therefore are not directly comparable to corresponding ratios as of December 31, 2013 and 2014. |

| (2) |

Under applicable guidelines of the Financial Services Commission, we, as a bank holding company, are required to maintain a minimum consolidated capital adequacy ratio of 8%. See “Item 4.B. Business Overview—Supervision and Regulation—Principal Regulations Applicable to Financial Holding Companies—Capital Adequacy.” |

| (3) |

Kookmin Bank’s capital adequacy ratios are computed in accordance with the guidelines issued by the Financial Services Commission. See “Item 4.B. Business Overview—Supervision and Regulation—Principal Regulations Applicable to Banks—Capital Adequacy.” |

Credit portfolio ratios and other data

| As of December 31, | ||||||||||||||||||||

| 2010 | 2011 | 2012 | 2013 | 2014 | ||||||||||||||||

| (in billions of Won, except percentages) | ||||||||||||||||||||

|

Total loans (1) |

₩ | 201,377 | ₩ | 215,555 | ₩ | 216,914 | ₩ | 221,862 | ₩ | 233,902 | ||||||||||

|

Total non-performing loans (2) |

1,612 | 1,180 | 1,606 | 1,421 | 1,068 | |||||||||||||||

|

Other impaired loans not included in non-performing loans |

2,204 | 2,285 | 2,086 | 2,669 | 1,996 | |||||||||||||||

|

Total of non-performing loans and other impaired loans |

3,816 | 3,465 | 3,692 | 4,090 | 3,064 | |||||||||||||||

|

Total allowances for loan losses |

3,756 | 3,448 | 3,269 | 2,861 | 2,452 | |||||||||||||||

|

Non-performing loans as a percentage of total loans |

0.80 | % | 0.55 | % | 0.74 | % | 0.64 | % | 0.46 | % | ||||||||||

|

Non-performing loans as a percentage of total assets |

0.62 | % | 0.42 | % | 0.56 | % | 0.49 | % | 0.35 | % | ||||||||||

|

Total of non-performing loans and other impaired loans as a percentage of total loans |

1.89 | % | 1.61 | % | 1.70 | % | 1.84 | % | 1.31 | % | ||||||||||

|

Allowances for loan losses as a percentage of total loans |

1.87 | % | 1.60 | % | 1.51 | % | 1.29 | % | 1.05 | % | ||||||||||

| (1) |

Before deduction of allowances for loan losses. |

| (2) |

Non-performing loans are defined as those loans, including corporate, retail and other loans, which are past due by 90 days or more. |

7

Table of Contents

Selected Statistical Information

The following table shows our average balances and interest rates for the past three years:

| Year Ended December 31, | ||||||||||||||||||||||||||||||||||||

| 2012 | 2013 | 2014 | ||||||||||||||||||||||||||||||||||

|

Average

Balance (1) |

Interest

Income (2)(3) |

Average

Yield |

Average

Balance (1) |

Interest

Income (2)(3) |

Average

Yield |

Average

Balance (1) |

Interest

Income (2)(3) |

Average

Yield |

||||||||||||||||||||||||||||

| (in billions of Won, except percentages) | ||||||||||||||||||||||||||||||||||||

|

Assets |

||||||||||||||||||||||||||||||||||||

|

Cash and interest earning deposits in other banks |

₩ | 4,808 | ₩ | 160 | 3.33 | % | ₩ | 5,905 | ₩ | 146 | 2.47 | % | ₩ | 7,811 | ₩ | 190 | 2.43 | % | ||||||||||||||||||

|

Financial investment (debt securities) (4) |

33,382 | 1,426 | 4.27 | 33,339 | 1,269 | 3.81 | 31,530 | 1,120 | 3.55 | |||||||||||||||||||||||||||

|

Loans: |

||||||||||||||||||||||||||||||||||||

|

Corporate |

102,773 | 5,328 | 5.18 | 100,614 | 4,526 | 4.50 | 101,875 | 4,145 | 4.07 | |||||||||||||||||||||||||||

|

Mortgage |

44,444 | 2,161 | 4.86 | 44,514 | 1,826 | 4.10 | 48,160 | 1,746 | 3.63 | |||||||||||||||||||||||||||

|

Home equity |

30,170 | 1,535 | 5.09 | 30,275 | 1,287 | 4.25 | 32,030 | 1,216 | 3.80 | |||||||||||||||||||||||||||

|

Other consumer |

29,721 | 2,163 | 7.28 | 30,536 | 1,974 | 6.46 | 32,981 | 2,019 | 6.12 | |||||||||||||||||||||||||||

|

Credit cards (5) |

12,078 | 1,345 | 11.14 | 11,611 | 1,242 | 10.70 | 11,312 | 1,123 | 9.93 | |||||||||||||||||||||||||||

|

Foreign |

2,744 | 92 | 3.35 | 2,851 | 87 | 3.05 | 2,631 | 76 | 2.89 | |||||||||||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||||||||||||||

|

Loans (total) |

221,930 | 12,624 | 5.69 | 220,401 | 10,942 | 4.96 | 228,989 | 10,325 | 4.51 | |||||||||||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||||||||||||||

|

Total average interest earning assets |

₩ | 260,120 | ₩ | 14,210 | 5.46 | % | ₩ | 259,645 | ₩ | 12,357 | 4.76 | % | ₩ | 268,330 | ₩ | 11,635 | 4.34 | % | ||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||||||||||||||

|

Cash and due from banks |

7,622 | — | — | 7,688 | — | — | 7,978 | — | — | |||||||||||||||||||||||||||

|

Financial assets at fair value through profit or loss: |

||||||||||||||||||||||||||||||||||||

|

Debt securities (3) |

8,744 | — | — | 8,091 | — | — | 8,631 | — | — | |||||||||||||||||||||||||||

|

Equity securities |

1,026 | — | — | 1,280 | — | — | 847 | — | — | |||||||||||||||||||||||||||

|

Other |

36 | — | — | 42 | — | — | 47 | — | — | |||||||||||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||||||||||||||

|

Financial assets at fair value through profit or loss (total) |

9,806 | — | — | 9,413 | — | — | 9,525 | — | — | |||||||||||||||||||||||||||

|

Financial investment (equity securities) |

2,444 | — | — | 2,671 | — | — | 2,999 | — | — | |||||||||||||||||||||||||||

|

Investment in associates |

934 | — | — | 882 | — | — | 698 | — | — | |||||||||||||||||||||||||||

|

Derivative financial assets |

2,040 | — | — | 1,760 | — | — | 1,791 | — | — | |||||||||||||||||||||||||||

|

Premises and equipment |

3,212 | — | — | 3,191 | — | — | 3,197 | — | — | |||||||||||||||||||||||||||

|

Intangible assets |

539 | — | — | 475 | — | — | 463 | — | — | |||||||||||||||||||||||||||

|

Allowances for loan losses |

(4,159 | ) | — | — | (4,108 | ) | — | — | (3,556 | ) | — | — | ||||||||||||||||||||||||

|

Other non-interest earning assets |

7,472 | — | — | 8,555 | — | — | 7,570 | — | — | |||||||||||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||||||||||||||

|

Total average non-interest earning assets |

29,910 | — | — | 30,527 | — | — | 30,665 | — | — | |||||||||||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||||||||||||||

|

Total average assets |

₩ | 290,030 | ₩ | 14,210 | 4.90 | % | ₩ | 290,172 | ₩ | 12,357 | 4.26 | % | ₩ | 298,995 | ₩ | 11,635 | 3.89 | % | ||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||||||||||||||

8

Table of Contents

| Year Ended December 31, | ||||||||||||||||||||||||||||||||||||

| 2012 | 2013 | 2014 | ||||||||||||||||||||||||||||||||||

|

Average

Balance (1) |

Interest

Expense |

Average

Cost |

Average

Balance (1) |

Interest

Expense |

Average

Cost |

Average

Balance (1) |

Interest

Expense |

Average

Cost |

||||||||||||||||||||||||||||

| (in billions of Won, except percentages) | ||||||||||||||||||||||||||||||||||||

|

Liabilities |

||||||||||||||||||||||||||||||||||||

|

Deposits: |

||||||||||||||||||||||||||||||||||||

|

Demand deposits |

₩ | 56,154 | ₩ | 336 | 0.60 | % | ₩ | 60,894 | ₩ | 285 | 0.47 | % | ₩ | 67,612 | ₩ | 283 | 0.42 | % | ||||||||||||||||||

|

Time deposits |

136,617 | 5,047 | 3.69 | 130,286 | 3,940 | 3.02 | 130,258 | 3,516 | 2.70 | |||||||||||||||||||||||||||

|

Certificates of deposit |

1,735 | 67 | 3.86 | 1,780 | 54 | 3.03 | 1,689 | 46 | 2.72 | |||||||||||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||||||||||||||

|

Deposits (total) |

194,506 | 5,450 | 2.80 | 192,960 | 4,279 | 2.22 | 199,559 | 3,845 | 1.93 | |||||||||||||||||||||||||||

|

Debts |

21,773 | 460 | 2.11 | 20,173 | 365 | 1.81 | 19,085 | 342 | 1.79 | |||||||||||||||||||||||||||

|

Debentures |

24,552 | 1,262 | 5.14 | 25,319 | 1,190 | 4.70 | 28,048 | 1,032 | 3.68 | |||||||||||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||||||||||||||

|

Total average interest bearing liabilities |

₩ | 240,831 | ₩ | 7,172 | 2.98 | % | ₩ | 238,452 | ₩ | 5,834 | 2.45 | % | ₩ | 246,692 | ₩ | 5,219 | 2.12 | % | ||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||||||||||||||

|

Non-interest bearing demand deposits |

3,075 | — | — | 3,252 | — | — | 3,486 | — | — | |||||||||||||||||||||||||||

|

Derivative financial liabilities |

1,899 | — | — | 1,789 | — | — | 1,669 | — | — | |||||||||||||||||||||||||||

|

Financial liabilities at fair value through profit or loss |

1,724 | — | — | 1,697 | — | — | 1,497 | — | — | |||||||||||||||||||||||||||

|

Other non-interest bearing liabilities |

17,770 | — | — | 19,157 | — | — | 18,778 | — | — | |||||||||||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||||||||||||||

|

Total average non-interest bearing liabilities |

24,468 | — | — | 25,895 | — | — | 25,430 | — | — | |||||||||||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||||||||||||||

|

Total average liabilities |

265,299 | 7,172 | 2.70 | 264,347 | 5,834 | 2.21 | 272,122 | 5,219 | 1.92 | |||||||||||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||||||||||||||

|

Total equity |

24,731 | — | — | 25,825 | — | — | 26,873 | — | — | |||||||||||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||||||||||||||

|

Total average liabilities and equity |

₩ | 290,030 | ₩ | 7,172 | 2.48 | % | ₩ | 290,172 | ₩ | 5,834 | 2.01 | % | ₩ | 298,995 | ₩ | 5,219 | 1.75 | % | ||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||||||||||||||

| (1) |

Average balances are based on daily balances for our banking, credit card and investment and securities operations and monthly or quarterly balances for our other operations. |

| (2) |

We do not invest in any tax-exempt securities. |

| (3) |

Excludes interest income from debt securities at fair value through profit or loss. |

| (4) |

Information related to investment securities classified as available-for-sale has been computed using amortized cost, and therefore does not give effect to changes in fair value that are reflected as a component of total equity. |

| (5) |

Interest income from credit cards includes principally cash advance fees of ₩447 billion, ₩353 billion and ₩276 billion and interest on credit card loans of ₩457 billion, ₩435 billion and ₩408 billion for the years ended December 31, 2012, 2013 and 2014, respectively, but does not include interchange fees. |

The following table presents our net interest spread, net interest margin, and asset liability ratio for the past three years:

| Year Ended December 31, | ||||||||||||

| 2012 | 2013 | 2014 | ||||||||||

| (percentages) | ||||||||||||

|

Net interest spread (1) |

2.48 | % | 2.31 | % | 2.22 | % | ||||||

|

Net interest margin (2) |

2.71 | 2.51 | 2.39 | |||||||||

|

Average asset liability ratio (3) |

108.01 | 108.89 | 108.77 | |||||||||

| (1) |

The difference between the average rate of interest earned on interest earning assets and the average rate of interest paid on interest bearing liabilities. |

| (2) |

The ratio of net interest income to average interest earning assets. |

| (3) |

The ratio of average interest earning assets to average interest bearing liabilities. |

9

Table of Contents

Analysis of Changes in Net Interest Income—Volume and Rate Analysis

The following table provides an analysis of changes in interest income, interest expense and net interest income based on changes in volume and changes in rate for 2012 compared to 2013 and 2013 compared to 2014. Information is provided with respect to: (1) effects attributable to changes in volume (changes in volume multiplied by prior rate) and (2) effects attributable to changes in rate (changes in rate multiplied by prior volume). Changes attributable to the combined impact of changes in rate and volume have been allocated proportionately to the changes due to volume changes and changes due to rate changes.

|

2013 vs. 2012

Increase/(Decrease) Due to Change in |

2014 vs. 2013

Increase/(Decrease) Due to Change in |

|||||||||||||||||||||||

| Volume | Rate | Total | Volume | Rate | Total | |||||||||||||||||||

| (in billions of Won) | ||||||||||||||||||||||||

|

Interest earning assets |

||||||||||||||||||||||||

|

Cash and interest earning deposits in other banks |

₩ | 32 | ₩ | (46 | ) | ₩ | (14 | ) | ₩ | 46 | ₩ | (2 | ) | ₩ | 44 | |||||||||

|

Financial investment (debt securities) |

(2 | ) | (155 | ) | (157 | ) | (66 | ) | (83 | ) | (149 | ) | ||||||||||||

|

Loans: |

||||||||||||||||||||||||

|

Corporate |

(110 | ) | (692 | ) | (802 | ) | 57 | (438 | ) | (381 | ) | |||||||||||||

|

Mortgage |

3 | (338 | ) | (335 | ) | 141 | (221 | ) | (80 | ) | ||||||||||||||

|

Home equity |

5 | (253 | ) | (248 | ) | 71 | (142 | ) | (71 | ) | ||||||||||||||

|

Other consumer |

58 | (247 | ) | (189 | ) | 152 | (107 | ) | 45 | |||||||||||||||

|

Credit cards |

(51 | ) | (52 | ) | (103 | ) | (31 | ) | (88 | ) | (119 | ) | ||||||||||||

|

Foreign |

3 | (8 | ) | (5 | ) | (7 | ) | (4 | ) | (11 | ) | |||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||

|

Total interest income |

₩ | (62 | ) | ₩ | (1,791 | ) | ₩ | (1,853 | ) | ₩ | 363 | ₩ | (1,085 | ) | ₩ | (722 | ) | |||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||

|

2013 vs. 2012

Increase/(Decrease) Due to Change in |

2014 vs. 2013

Increase/(Decrease) Due to Change in |

|||||||||||||||||||||||

| Volume | Rate | Total | Volume | Rate | Total | |||||||||||||||||||

| (in billions of Won) | ||||||||||||||||||||||||

|

Interest bearing liabilities |

||||||||||||||||||||||||

|

Deposits: |

||||||||||||||||||||||||

|

Demand deposits |

₩ | 27 | ₩ | (78 | ) | ₩ | (51 | ) | ₩ | 30 | ₩ | (32 | ) | ₩ | (2 | ) | ||||||||

|

Time deposits |

(225 | ) | (882 | ) | (1,107 | ) | (1 | ) | (423 | ) | (424 | ) | ||||||||||||

|

Certificates of deposit |

2 | (15 | ) | (13 | ) | (3 | ) | (5 | ) | (8 | ) | |||||||||||||

|

Debts |

(32 | ) | (63 | ) | (95 | ) | (19 | ) | (4 | ) | (23 | ) | ||||||||||||

|

Debentures |

39 | (111 | ) | (72 | ) | 119 | (277 | ) | (158 | ) | ||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||

|

Total interest expense |

(189 | ) | (1,149 | ) | (1,338 | ) | 126 | (741 | ) | (615 | ) | |||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||

|

Total net interest income |

₩ | 127 | ₩ | (642 | ) | ₩ | (515 | ) | ₩ | 237 | ₩ | (344 | ) | ₩ | (107 | ) | ||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||

10

Table of Contents

Exchange Rates

The table below sets forth, for the periods and dates indicated, information concerning the noon buying rate for Won, expressed in Won per one U.S. dollar. The “noon buying rate” is the rate in New York City for cable transfers in foreign currencies as certified for customs purposes by the Federal Reserve Bank of New York. Unless otherwise stated, translations of Won amounts into U.S. dollars in this annual report were made at the noon buying rate in effect on December 31, 2014, which was ₩1,090.9 to US$1.00. We do not intend to imply that the Won or U.S. dollar amounts referred to herein could have been or could be converted into U.S. dollars or Won, as the case may be, at any particular rate, or at all. On April 24, 2015, the noon buying rate was ₩1,075.9 = US$1.00.

| Won per U.S. dollar (noon buying rate) | ||||||||||||||||

| Low | High | Average (1) | Period-End | |||||||||||||

|

2010 |

1,104.0 | 1,253.2 | 1,155.7 | 1,130.6 | ||||||||||||

|

2011 |

1,049.2 | 1,197.5 | 1,106.9 | 1,158.5 | ||||||||||||

|

2012 |

1,063.2 | 1,185.0 | 1,126.2 | 1,063.2 | ||||||||||||

|

2013 |

1,050.1 | 1,161.3 | 1,094.7 | 1,055.3 | ||||||||||||

|

2014 |

1,008.9 | 1,117.7 | 1,052.3 | 1,090.9 | ||||||||||||

|

October |

1,043.9 | 1,074.4 | 1,060.3 | 1,073.1 | ||||||||||||

|

November |

1,077.0 | 1,114.7 | 1,097.9 | 1,112.1 | ||||||||||||

|

December |

1,080.8 | 1,117.7 | 1,102.6 | 1,090.9 | ||||||||||||

|

2015 (through April 24) |

1,075.9 | 1,100.4 | 1,088.1 | 1,075.9 | ||||||||||||

|

January |

1,075.3 | 1,109.1 | 1,088.1 | 1,104.3 | ||||||||||||

|

February |

1,086.8 | 1,112.8 | 1,101.5 | 1,100.7 | ||||||||||||

|

March |

1,095.7 | 1,135.7 | 1,112.9 | 1,107.7 | ||||||||||||

|

April (through April 24) |

1,075.3 | 1,135.7 | 1,098.2 | 1,075.9 | ||||||||||||

Source : Federal Reserve Bank of New York.

| (1) |

The average of the daily noon buying rates of the Federal Reserve Bank in effect during the relevant period (or portion thereof). |

| Item 3.B. |

|

Not applicable.

| Item 3.C. | Reasons for the Offer and Use of Proceeds |

Not applicable.

| Item 3.D. | Risk Factors |

Risks relating to our retail credit portfolio

Future changes in market conditions as well as other factors may lead to increases in delinquency levels of our retail loan portfolio.

In recent years, consumer debt has increased significantly in Korea. Our portfolio of retail loans, including mortgage and home equity loans, decreased slightly from ₩103,855 billion as of December 31, 2011 to ₩103,432 billion as of December 31, 2012 but increased to ₩107,644 billion as of December 31, 2013 and ₩119,249 billion as of December 31, 2014. As of December 31, 2014, our retail loans represented 51.0% of our total lending. Within our retail loan portfolio, the outstanding balance of other consumer loans, which unlike mortgage or home equity loans are often unsecured and therefore tend to carry a higher credit risk, has increased from ₩28,275 billion as of December 31, 2011 to ₩32,255 billion as of December 31, 2014; as a percentage of total outstanding retail loans, such balance has remained relatively stable at 27.2% as of December 31, 2011 and

11

Table of Contents

27.0% as of December 31, 2014. The growth of our retail lending business, which generally offers higher margins than other lending activities, contributed significantly to our interest income and profitability in recent years.

The growth of our retail loan portfolio, together with adverse economic conditions in Korea and globally in recent years, may lead to further increases in delinquency levels and a deterioration in asset quality. The amount of our non-performing retail loans (defined as those that are past due by 90 days or more) increased from ₩642 billion as of December 31, 2011 to ₩762 billion as of December 31, 2012 but decreased to ₩546 billion as of December 31, 2013 and ₩395 billion as of December 31, 2014. However, higher delinquencies in our retail loan portfolio in the future will require us to increase our loan loss provisions and charge-offs, which in turn will adversely affect our financial condition and results of operations.

Our large exposure to consumer debt means that we are exposed to changes in economic conditions affecting Korean consumers. Accordingly, a rise in unemployment, an increase in interest rates, a deterioration of the real estate market or difficulties in the Korean economy may have an adverse effect on Korean consumers, which could result in reduced growth and further deterioration in the credit quality of our retail loan portfolio. See “Risks relating to Korea—Unfavorable financial and economic developments in Korea may have an adverse effect on us.” In order to minimize our risk as a result of such exposure, we are continuing to strengthen our risk management processes, including further improving the retail lending process, upgrading our retail credit rating system, as well as strengthening the overall management of our portfolio. Despite our efforts, however, there is no assurance that we will be able to prevent significant credit quality deterioration in our retail loan portfolio.

In light of adverse conditions in the Korean economy affecting consumers, in March 2009, the Financial Services Commission requested Korean banks, including us, to establish a “pre-workout program,” including a credit counseling and recovery service, for retail borrowers with outstanding short-term debt. Under the pre-workout program, which has been in operation since April 2009, maturity extensions and/or interest reductions are provided for retail borrowers with total loans of ₩1.5 billion or less (consisting of no more than ₩500 million of unsecured loans and ₩1 billion of secured loans) who are in arrears on their payments for more than 30 days but less than 90 days or for retail borrowers with an annual income of ₩40 million or less who have been in arrears on their payments for more than 30 days on an aggregate basis for the 12 months prior to their application. In addition, in March 2015, in response to increasing levels of consumer debt and amid concerns over the debt-servicing capacity of retail borrowers if interest rates were to rise, the Korean government launched, and requested Korean banks to participate in, a mortgage loan refinancing program aimed at reducing the payment burden on and improving the asset quality of outstanding mortgage loans. Under such refinancing program, over 340,000 qualified retail borrowers converted their outstanding non-amortizing floating-rate mortgage loans from Korean commercial banks (including us) into amortizing fixed-rate mortgage loans with lower interest rates, amounting to an aggregate principal amount of ₩34 trillion for all commercial banks in 2015. Our participation in such refinancing program may lead to a decrease in our interest income on our outstanding mortgage loans, as well as in our overall net interest margin. More generally, our participation in such government-led initiatives to provide financial support to retail borrowers may lead us to offer credit terms for such borrowers that we would not otherwise offer, in the absence of such initiatives, which may have an adverse effect on our results of operations and financial condition.

Our credit card operations may generate losses in the future, which could hurt our financial condition and results of operations.

With respect to our credit card portfolio, our delinquency ratio (which represents the ratio of amounts that are overdue by 30 days or more to total outstanding balances) decreased from 1.5% as of December 31, 2011 to 1.3% as of December 31, 2012, increased to 1.7% as of December 31, 2013 and decreased to 1.5% as of December 31, 2014. In line with industry practice, we have restructured a portion of delinquent credit card account balances (defined as balances overdue by 30 days or more) as loans. As of December 31, 2014, these restructured loans outstanding amounted to ₩45 billion. Because these loans are not treated as being delinquent

12

Table of Contents

at the time of conversion or for a period of time thereafter, our delinquency ratios may not fully reflect all delinquent amounts relating to our outstanding loans. Including all restructured loans, outstanding balances overdue by 30 days or more accounted for 1.9% of our credit card receivables (including credit card loans) as of December 31, 2014. Delinquencies may increase further in 2015 and in the future as a result of, among other things, adverse economic conditions in Korea and the inability of Korean consumers to manage increased household debt.

Despite our continuing efforts to sustain and improve our credit card asset quality and performance, we may experience increased delinquencies or deterioration of the asset quality of our credit card portfolio, which would require us to increase our loan loss provisions and charge-offs and adversely affect our overall financial condition and results of operations.

In addition, in February 2014, the Financial Services Commission suspended the new credit card issuance and other related activities of our credit card subsidiary, KB Kookmin Card Co., Ltd., for three months from February to May 2014, in response to an incident involving the misappropriation of the personal information of a large number of its customers by an employee of an external credit information company in the first half of 2013. Specifically, during such suspension period, KB Kookmin Card was prohibited from engaging in the following activities:

| • |

adding new subscribers for credit cards, prepaid cards and debit cards or issuing such types of cards (except as permitted by the chairman of the Financial Services Commission for public policy purposes); |

| • |

providing new or additional credit lines to credit card customers; and |

| • |

providing new services through mail order or telemarketing channels or related to travel or insurance products. |

Furthermore, in connection with the misappropriation incident, a number of customers have filed lawsuits against KB Kookmin Card seeking damages, and it could become subject to additional litigation and regulatory sanctions. See “Item 8A. Consolidated Statements and Other Financial Information—Legal Proceedings.” KB Kookmin Card has also incurred and may continue to incur significant costs relating to the issuance of replacement cards for customers and the compensation of customers for losses incurred as a result of the fraudulent use of the misappropriated personal information. Accordingly, the misappropriation incident and the resulting regulatory sanctions (including the three-month suspension of KB Kookmin Card’s new business activities), customer claims and costs could have a material adverse effect on our business, reputation, results of operations and financial condition.

Risks relating to our small- and medium-sized enterprise loan portfolio

We have significant exposure to small- and medium-sized enterprises, and any financial difficulties experienced by these customers may result in a deterioration of our asset quality and have an adverse impact on us.

One of our core businesses is lending to small- and medium-sized enterprises (as defined under “Item 4.B. Business Overview—Corporate Banking—Small- and Medium-sized Enterprise Banking”). Our loans to small- and medium-sized enterprises increased from ₩68,730 billion as of December 31, 2011 to ₩71,960 billion as of December 31, 2014. During that period, non-performing loans (defined as those loans that are past due by 90 days or more) to small- and medium-sized enterprises increased from ₩373 billion as of December 31, 2011 to ₩680 billion as of December 31, 2012 but decreased to ₩373 billion as of December 31, 2014, and the non-performing loan ratio for such loans increased from 0.5% as of December 31, 2011 to 0.8% as of December 31, 2013 but decreased to 0.5% as of December 31, 2014. However, our non-performing loans and non-performing loan ratio may increase in 2015. According to data compiled by the Financial Supervisory Service, the

13

Table of Contents

delinquency ratio for Won-currency loans by Korean commercial banks to small- and medium-sized enterprises was 0.8% as of December 31, 2014. The delinquency ratio for loans to small- and medium-sized enterprise is calculated as the ratio of (1) the outstanding balance of such loans in respect of which either principal or interest payments are overdue by one month or more to (2) the aggregate outstanding balance of such loans. Our delinquency ratio for such Won currency loans remained relatively stable at 1.0% as of December 31, 2011, 1.1% as of December 31, 2012 and 0.9% as of December 31, 2013, but decreased to 0.6% as of December 31, 2014. However, our delinquency ratio for such Won currency loans may increase in 2015. In recent years, we have taken measures which sought to stem rising delinquencies in our loans to small- and medium-sized enterprises, including through strengthening the review of loan applications and closer monitoring of the post-loan performance of small- and medium-sized enterprise borrowers in industry sectors that are relatively more sensitive to downturns in the economy and have shown higher delinquency ratios, such as construction, lodging, retail and wholesale, restaurants and real estate. Despite such efforts, however, there is no assurance that delinquency levels for our loans to small- and medium-sized enterprises will not rise in the future. In particular, financial difficulties experienced by small- and medium-sized enterprises as a result of, among other things, adverse economic conditions in Korea and globally in recent years may lead to a deterioration in the asset quality of our loans to this segment. Any such deterioration would result in increased charge-offs and higher provisioning and reduced interest and fee income from this segment, which could have a material adverse impact on our financial condition and results of operations.

In addition, many small- and medium-sized enterprises have close business relationships with the largest Korean commercial conglomerates, known as “ chaebols ,” primarily as suppliers. Any difficulties encountered by those chaebols would likely hurt the liquidity and financial condition of related small- and medium-sized enterprises, including those to which we have exposure, also resulting in an impairment of their ability to repay loans.

A substantial part of our small- and medium-sized enterprise lending comprises loans to “small office/home office” customers, or SOHOs. SOHOs, which we currently define to include sole proprietorships and individual business interests, are usually dependent on a limited number of suppliers or customers. SOHOs tend to be affected to a greater extent than larger corporate borrowers by fluctuations in the Korean economy. In addition, SOHOs often maintain less sophisticated financial records than other corporate borrowers. Although we continue to make efforts to improve our internally developed credit rating systems to rate potential borrowers, particularly with respect to SOHOs, and intend to manage our exposure to these borrowers closely in order to prevent any deterioration in the asset quality of our loans to this segment, we may not be able to do so as intended.

In light of the deteriorating financial condition and liquidity position of small- and medium-sized enterprises in Korea since the global financial crisis commencing in the second half of 2008, the Korean government introduced policies and initiatives intended to encourage Korean banks to provide financial support to small- and medium-sized enterprises. For example, in November 2008, we entered into a memorandum of understanding with the Financial Supervisory Service under which we were required to improve the liquidity position of small- and medium-sized enterprises and exporters by providing them with adequate financing and to endeavor to alleviate burdens on low-income debtors by extending maturity dates or by delaying interest payments on loans owed to us. In addition, in October 2008, the Financial Supervisory Service requested Korean banks, including us, to establish a “fast track” program to provide liquidity assistance to small- and medium-sized enterprises on an expedited basis. Under the fast track program we established, which has been extended until December 31, 2015, we provide liquidity assistance to qualified small- and medium-sized enterprise borrowers applying for such assistance, in the form of new loans or maturity extensions or interest rate adjustments with respect to existing loans, after expedited credit review and approval by us. The overall prospects for the Korean economy in 2015 and beyond remain uncertain, and the Korean government may extend or renew existing or past policies and initiatives or introduce new policies or initiatives to encourage Korean banks to provide financial support to small- and medium-sized enterprises. Our participation in such government-led initiatives may lead us to extend credit to small- and medium-sized enterprise borrowers that we would not otherwise extend, or offer terms for such credit that we would not otherwise offer, in the absence of such initiatives. Furthermore, there is no

14

Table of Contents

guarantee that the financial condition and liquidity position of our small- and medium-sized enterprise borrowers benefiting from such initiatives will improve sufficiently for them to service their debt on a timely basis, or at all. Accordingly, increases in our exposure to small- and medium-sized enterprise borrowers resulting from such government-led initiatives may have a material adverse effect on our financial condition and results of operations.

We have exposure to Korean construction and shipbuilding companies, and financial difficulties of these companies may have an adverse impact on us .

As of December 31, 2014, we had loans outstanding to construction companies and shipbuilding companies (many of which are small- and medium-sized enterprises) in the amount of ₩3,778 billion and ₩820 billion, or 1.6% and 0.4% of our total loans, respectively. We also have other exposures to Korean construction and shipbuilding companies, including in the form of guarantees extended on behalf of such companies (which included ₩710 billion of confirmed guarantees for construction companies and ₩1,179 billion of confirmed guarantees for shipbuilding companies as of December 31, 2014) and debt and equity securities of such companies held by us. In the case of construction companies, such exposures include guarantees provided to us by general contractors with respect to financing extended by us for residential and commercial real estate development projects. In the case of shipbuilding companies, such exposures include refund guarantees extended by us on behalf of shipbuilding companies to cover their obligation to return a portion of the ship order contract amount to customers in the event of performance delays or defaults under shipbuilding contracts.

The construction industry in Korea has experienced a downturn in recent years, due to excessive investment in residential property development projects, stagnation of real property prices and reduced demand for residential property, especially in areas outside of Seoul, including as a result of the deterioration of the Korean economy. The shipbuilding industry in Korea has also experienced a severe downturn in recent years due to a significant decrease in ship orders, primarily due to adverse conditions in the global economy and the resulting slowdown in global trade. In response to the deteriorating financial condition and liquidity position of borrowers in the construction and shipbuilding industries, which were disproportionately impacted by adverse economic developments in Korea and globally, the Korean government implemented a program in 2009 to promote expedited restructuring of such borrowers by their Korean creditor financial institutions, under the supervision of major commercial banks. In accordance with such program, 24 construction companies and five shipbuilding companies became subject to workout in 2009, following review by their creditor financial institutions (including us) and the Korean government. In addition, in June 2010, the Financial Services Commission and the Financial Supervisory Service announced that, following credit risk evaluations conducted by creditor financial institutions (including us) of companies in Korea with outstanding debt of ₩50 billion or more, 65 companies had been selected by such financial institutions for restructuring in the form of workout, liquidation or court receivership. Of such 65 companies, 16 were construction companies and three were shipbuilding and shipping companies. Each year since June 2010, the Financial Services Commission and the Financial Supervisory Service has announced the results of subsequent credit risk evaluations conducted by creditor financial institutions (including us) of companies in Korea with outstanding debt of ₩50 billion or more and selected companies for restructuring in the form of workout, liquidation or court receivership. Most recently, in July 2014, 34 companies with outstanding debt of ₩50 billion or more (21 of which were construction companies and three of which were shipbuilding and shipping companies) were selected by such financial institutions for restructuring. However, there is no assurance that these measures will be successful in stabilizing the Korean construction and shipbuilding industries.

The allowances that we have established against our credit exposures to Korean construction and shipbuilding companies may not be sufficient to cover all future losses arising from these and other exposures. If the credit quality of our exposures to Korean construction and shipbuilding companies declines further, we may be required to take substantial additional provisions (including in connection with restructurings of such companies), which could adversely impact our results of operations and financial condition. Furthermore, although a portion of our credit exposures to construction and shipbuilding companies are secured by collateral, such collateral may not be sufficient to cover uncollectible amounts in respect of such credit exposures. See

15

Table of Contents

“—Other risks relating to our business—A decline in the value of the collateral securing our loans and our inability to realize full collateral value may adversely affect our credit portfolio.”

We also have construction-related credit exposures under our project financing loans for real estate development projects in Korea. In light of the general deterioration in the asset quality of real estate project financing loans in Korea in recent years, Korean banks, including Kookmin Bank, implemented a uniform set of guidelines to apply more stringent criteria in evaluating the asset quality of real estate project financing loans. As a result, we may be required to establish additional allowances with respect to our outstanding real estate project financing loans, which could adversely affect our financial condition and results of operations.

Risks relating to our financial holding company structure and strategy

We may not succeed in implementing our strategy to take advantage of, or fail to realize the anticipated benefits of, our financial holding company structure.

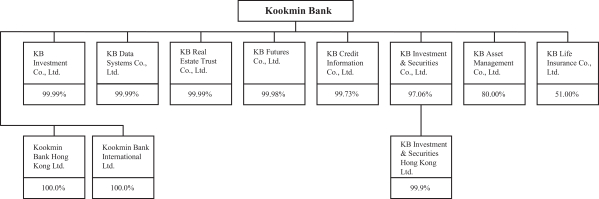

We were established as a new financial holding company in September 2008 pursuant to a “comprehensive stock transfer” under Korean law, following the completion of which Kookmin Bank, KB Investment & Securities Co., Ltd., KB Asset Management Co., Ltd., KB Real Estate Trust Co., Ltd., KB Investment Co., Ltd., KB Futures Co., Ltd., KB Credit Information Co., Ltd., and KB Data Systems Co., Ltd. became our wholly-owned subsidiaries. See “Item 4.A. History and Development of the Company—The Establishment of KB Financial Group.” In addition, as a part of our strategy to promote the growth of our credit card operations and enhance its synergies with our other businesses, we effected a horizontal spin-off of Kookmin Bank’s credit card business in March 2011. As a result, our credit card business is operated by a separate wholly-owned subsidiary, KB Kookmin Card Co., Ltd.

One of our principal strategies is to take advantage of our financial holding company structure to become a comprehensive financial services provider capable of offering a full range of products and services to our large existing base of retail and corporate banking customers. The continued implementation of these plans may require additional investments of capital, infrastructure, human resources and management attention. This strategy entails certain risks, including the possibility that we may face significant competition from other financial holding companies and more specialized financial institutions in particular segments. If our strategy does not succeed, we may incur losses on our investments and our results of operations and financial condition may suffer.

Furthermore, our success under a financial holding company structure depends on our ability to realize the anticipated synergies, growth opportunities and cost savings from coordinating the businesses of our various subsidiaries. Although we have been integrating certain aspects of our subsidiaries’ operations into our financial holding company structure, our subsidiaries will generally continue to operate as independent entities with separate management and staff and our ability to direct our subsidiaries’ day-to-day operations may be limited.