UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

Form 20-F

| ☐ |

REGISTRATION STATEMENT PURSUANT TO SECTION 12(b) OR (g) OF THE SECURITIES EXCHANGE ACT OF 1934

|

OR

| ☒ |

ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934

|

For the fiscal year ended December 31, 2017

OR

| ☐ |

TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934

|

OR

| ☐ |

SHELL COMPANY REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934

|

Commission File Number: 001-36761

KENON HOLDINGS LTD.

(Exact name of registrant as specified in its charter)

(Company Registration No. 201406588W)

|

Singapore

|

4911

|

Not Applicable

|

|

(State or other jurisdiction of

incorporation or organization)

|

(Primary Standard Industrial

Classification Code Number)

|

(I.R.S. Employer

Identification No.) |

|

1 Temasek Avenue #36-01

Millenia Tower Singapore 039192 +65 6351 1780 |

||

|

(Address, including zip code, and telephone number, including area code, of registrant’s principal executive offices)

|

||

Copies to:

Scott V. Simpson

James A. McDonald

Skadden, Arps, Slate, Meagher and Flom (UK) LLP

40 Bank Street

London E14 5DS

Telephone: +44 20 7519 7000

Facsimile: +44 20 7519 7070

Scott V. Simpson

James A. McDonald

Skadden, Arps, Slate, Meagher and Flom (UK) LLP

40 Bank Street

London E14 5DS

Telephone: +44 20 7519 7000

Facsimile: +44 20 7519 7070

Securities registered or to be registered pursuant to Section 12(b) of the Act:

|

Title of Each Class

|

Name of Each Exchange on Which Registered

|

|

Ordinary Shares, no par value

|

The New York Stock Exchange

|

Securities registered or to be registered pursuant to Section 12(g) of the Act: None

Securities for which there is a reporting obligation pursuant to Section 15(d) of the Act: None

Indicate the number of outstanding shares of each of the issuer’s classes of capital or common stock as of the close of the period covered by the annual report:

53,807,578 shares

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act.

Yes

☐

No

☒

If this report is an annual or transition report, indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or 15(d) of the Securities Exchange Act of 1934.

Yes

☐

No

☒

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such a shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days.

Yes

☒

No

☐

Indicate by check mark whether the registrant has submitted electronically or posted on its corporate Web site, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T (§232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files).

Yes ☒ No

☐

Indicate by check mark whether the registrant is an accelerated filer, a large accelerated filer, a non-accelerated filer, or an emerging growth company. See definition of “large accelerated filer,” “accelerated filer,” and “emerging growth company” in Rule 12b-2 of the Exchange Act. (Check one):

|

Large accelerated filer

☒

|

Accelerated filer

☐

|

Non-accelerated filer

☐

|

Emerging growth company

☐

|

If an emerging growth company that prepares its financial statements in accordance with U.S. GAAP, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards † provided pursuant to Section 13(a) of the Exchange Act.

☐

† The term “new or revised financial accounting standard” refers to any update issued by the Financial Accounting Standards Board to its Accounting Standards Codification after April 5, 2012.

Indicate by check mark which basis of accounting the registrant has used to prepare the financial statements included in this filing:

|

U.S. GAAP

☐

|

International Financial Reporting Standards as issued by the International Accounting Standards Board

☒

|

Other

☐

|

If “Other” has been checked in response to the previous question, indicate by check mark which financial statement item the Registrant has elected to follow:

Item 17

☐

Item 18

☐

If this is an annual report, indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act).

Yes

☐

No

☒

TABLE OF CONTENTS

|

11

|

||

|

11

|

||

|

A.

|

Directors and Senior Management

|

11

|

|

B.

|

Advisers

|

11

|

|

C.

|

Auditors

|

11

|

|

11

|

||

|

12

|

||

|

A.

|

Selected Financial Data

|

12

|

|

B.

|

Capitalization and Indebtedness

|

18

|

|

C.

|

Reasons for the Offer and Use of Proceeds

|

18

|

|

D.

|

Risk Factors

|

18

|

|

58

|

||

|

A.

|

History and Development of the Company

|

58

|

|

B.

|

Business Overview

|

58

|

|

C.

|

Organizational Structure

|

106

|

|

D.

|

Property, Plants and Equipment

|

106

|

|

106

|

||

|

106

|

||

|

A.

|

Operating Results

|

116

|

|

B.

|

Liquidity and Capital Resources

|

127

|

|

C.

|

Research and Development, Patents and Licenses, Etc.

|

139

|

|

D.

|

Trend Information

|

139

|

|

E.

|

Off-Balance Sheet Arrangements

|

140

|

|

F.

|

Tabular Disclosure of Contractual Obligations

|

140

|

|

G.

|

Safe Harbor

|

141

|

|

141

|

||

|

A.

|

Directors and Senior Management

|

141

|

|

B.

|

Compensation

|

144

|

|

C.

|

Board Practices

|

144

|

|

D.

|

Employees

|

147

|

|

E.

|

Share Ownership

|

147

|

|

148

|

||

|

A.

|

Major Shareholders

|

148

|

|

B.

|

Related Party Transactions

|

149

|

|

C.

|

Interests of Experts and Counsel

|

149

|

1

|

150

|

||

|

A.

|

Consolidated Statements and Other Financial Information

|

150

|

|

B.

|

Significant Changes

|

150

|

|

150

|

||

|

A.

|

Offer and Listing Details.

|

150

|

|

B.

|

Plan of Distribution

|

151

|

|

C.

|

Markets

|

151

|

|

D.

|

Selling Shareholders

|

151

|

|

E.

|

Dilution.

|

151

|

|

F.

|

Expenses of the Issue

|

151

|

|

151

|

||

|

A.

|

Share Capital

|

151

|

|

B.

|

Constitution

|

151

|

|

C.

|

Material Contracts

|

166

|

|

D.

|

Exchange Controls

|

167

|

|

E.

|

Taxation

|

167

|

|

F.

|

Dividends and Paying Agents

|

171

|

|

G.

|

Statement by Experts

|

171

|

|

H.

|

Documents on Display

|

171

|

|

I.

|

Subsidiary Information

|

172

|

|

172

|

||

|

172

|

||

|

A.

|

Debt Securities

|

172

|

|

B.

|

Warrants and Rights

|

173

|

|

C.

|

Other Securities

|

173

|

|

D.

|

American Depositary Shares

|

173

|

|

173

|

||

|

173

|

||

|

173

|

||

|

173

|

||

|

174

|

||

|

174

|

||

|

174

|

||

|

174

|

||

|

175

|

||

|

175

|

||

|

175

|

2

|

175

|

||

|

175

|

||

|

175

|

||

|

175

|

||

|

175

|

||

|

176

|

3

INTRODUCTION AND USE OF CERTAIN TERMS

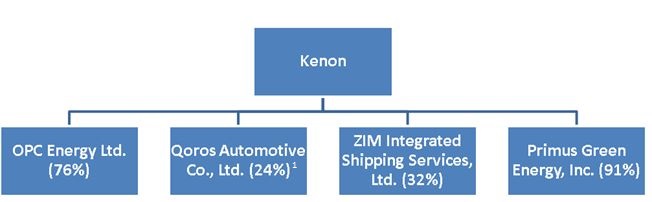

We have prepared this annual report using a number of conventions, which you should consider when reading the information contained herein. In this annual report, the “Company,” “we,” “us” and “our” shall refer to Kenon Holdings Ltd., or Kenon, and each of our subsidiaries and associated companies, collectively, as the context may require, including:

| · |

I.C. Power Asia Development Ltd. (“ICP”), formerly I.C. Power Ltd., an Israeli holding company, in which Kenon has an indirect 100% interest. ICP holds a 76% direct interest in OPC;

|

| · |

IC Power Ltd. (“IC Power”), formerly IC Power Pte. Ltd, a Singaporean holding company, in which Kenon has a direct 100% interest. IC Power holds a direct 100% interest in ICP;

|

| · |

“Inkia” means Inkia Energy Limited, a Bermudian corporation and wholly-owned subsidiary of IC Power. In December 2017, Inkia sold all of its Latin American and Caribbean businesses;

|

| · |

OPC Energy Ltd. (“OPC”), an owner, developer and operator of power generation facilities in the Israeli power market, in which ICP has a 76% interest;

|

| · |

Qoros Automotive Co., Ltd. (“Qoros”), a Chinese automotive company based in China, in which Kenon, through its 100%-owned subsidiary Quantum (2007) LLC, has a 24% interest;

|

| · |

ZIM Integrated Shipping Services, Ltd. (“ZIM”), an Israeli global container shipping company, in which Kenon has a 32% interest; and

|

| · |

Primus Green Energy, Inc. (“Primus”), a New Jersey corporation which is a developer of an alternative fuel technology, in which Kenon, through IC Green, has a 91% interest.

|

Additionally, this annual report uses the following conventions:

| · |

“Ansonia” means Ansonia Holdings Singapore B.V., a company organized under the laws of Singapore, which owns approximately 58% of the outstanding shares of Kenon;

|

| · |

“CDA” means Cerro del Águila S.A., a Peruvian corporation;

|

| · |

“DEOCSA” means Distribuidora de Electricidad de Occidente, S.A., a Guatemalan corporation, which was owned by Inkia prior to the sale of the Inkia Business in December 2017;

|

| · |

“DEORSA” means Distribuidora de Electricidad de Oriente, S.A., a Guatemalan corporation, which was owned by Inkia prior to the sale of the Inkia Business in December 2017;

|

| · |

“Hadera Paper” means Hadera Paper Ltd., an Israeli corporation, which is owned by OPC;

|

| · |

“HelioFocus” means HelioFocus Ltd., an Israeli corporation, in which Kenon, through IC Green, held a 70% interest, and which was liquidated on July 6, 2017;

|

| · |

“IC” means Israel Corporation Ltd., an Israeli corporation traded on the Tel Aviv Stock Exchange, or the “TASE,” and Kenon’s former parent company;

|

| · |

“IC Green” means IC Green Energy Ltd., an Israeli corporation, which holds Kenon’s equity interests in Primus and previously held Kenon’s equity interest in HelioFocus;

|

| · |

IC Power Distribution Holdings Pte. Ltd. (“ICPDH”), a Singaporean corporation;

|

| · |

“IEC” means Israel Electric Corporation, a government-owned entity, which generates and supplies the majority of electricity in Israel, transmits and distributes all of the electricity in Israel, acts as the system operator of Israel’s electricity system, determines the dispatch order of generation units, grants interconnection surveys, and sets spot prices, among other roles;

|

4

| · |

“Inkia Business” means Inkia’s Latin American and Caribbean power generation and distribution businesses, which were sold in December 2017;

|

| · |

“Kallpa” means Kallpa Generación SA. In August 2017, Kallpa merged with CDA, with the surviving entity renamed Kallpa Generación SA;

|

| · | “New Qoros Investor” means the China-based investor related to the Baoneng group that completed a transaction to purchase 51% of Qoros from Kenon and Chery for RMB3.315 billion (approximately $526 million) 1 , which is part of an investment structure to invest a total of approximately RMB6.63 billion (approximately $1,052 million) by the New Qoros Investor of which RMB6.5 billion will ultimately be invested in Qoros’ equity as Kenon announced in January 2018; |

| · |

“OPC-Rotem” means O.P.C. Rotem Ltd., an Israeli corporation, which is owned by OPC;

|

| · |

“OPC-Hadera” is the trade name of Advanced Integrated Energy Ltd., an Israeli corporation, which is owned by OPC;

|

| · |

“Petrotec” means Petrotec AG, a German company listed on the Frankfurt Stock Exchange, which IC Green sold in December 2014;

|

| · |

“Quantum” means Quantum (2007) LLC, a Delaware limited liability company, which is the direct owner of our 24% interest in Qoros;

|

| · |

“our businesses” shall refer to each of our subsidiaries and associated companies, collectively, as the context may require;

|

| · |

“Samay I” means Samay I S.A., a Peruvian corporation;

|

| · |

“spin-off” shall refer to (i) IC’s January 7, 2015 contribution to Kenon of its interests in each of IC Power, Qoros, ZIM, Tower, Primus, HelioFocus and the Renewable Energy Group (“REG”), as well as other intermediate holding companies related to these entities, and (ii) IC’s January 9, 2015 distribution of Kenon’s issued and outstanding ordinary shares, via a dividend-in-kind, to IC’s existing shareholders; and

|

| · |

“Tower” means Tower Semiconductor Ltd., an Israeli specialty foundry semiconductor manufacturer, listed on the NASDAQ stock exchange, or “NASDAQ,” and the TASE, in which Kenon used to hold an interest.

|

Additionally, this annual report uses the following conventions for OPC:

| · |

“COD” means the commercial operation date of a development project;

|

| · |

“distribution” refers to the transfer of electricity from the transmission lines at grid supply points and its delivery to consumers at lower voltages through a distribution system;

|

| · |

“EPC” means engineering, procurement and construction;

|

| · |

“firm capacity” means the amount of energy available for production that, pursuant to applicable regulations, must be guaranteed to be available at a given time for injection to a certain power grid;

|

| · |

“greenfield projects” means projects constructed on unused land with no need to demolish or remodel existing structures;

|

| · |

“GWh” means gigawatt hours (one GWh is equal to 1,000 MWh);

|

| · |

“HFO” means heavy fuel oil;

|

1

Convenience translations of RMB amounts into US Dollars use a rate of 6.3: 1, unless otherwise indicated.

5

| · |

“OPC’s capacity” or “OPC’s installed capacity” means, with respect to each asset, 100% of the capacity of such asset, regardless of OPC’s ownership interest in the entity that owns such asset;

|

| · |

“installed capacity” means the intended full-load sustained output of energy that a generation unit is designed to produce (also referred to as name-plate capacity);

|

| · |

“IPP” means independent power producer, excluding co-generators and generators for self-consumption;

|

| · |

“kWh” means kilowatts per hour;

|

| · |

“MW” means megawatts (one MW is equal to 1,000 kilowatts or kW);

|

| · |

“MWh” means megawatt per hour;

|

| · |

“OEM” means original equipment manufacturer;

|

| · |

“PPA” means power purchase agreement;

|

| · |

“transmission” refers to the bulk transfer of electricity from generating facilities to the distribution system at load center station in which the electricity is stabilized by means of the transmission grid; and

|

| · |

“weighted average availability” refers to the number of hours that a generation facility is available to produce electricity divided by the total number of hours in a year.

|

SALE OF THE INKIA BUSINESS

On December 31, 2017, our subsidiary Inkia completed the sale of substantially all of its businesses, the Inkia Business, consisting of power generation and distribution businesses in Latin America and the Caribbean. The sale is described in more detail under “

Item 4.B. – Business – Discontinued Operations – Inkia Business – Sale of the Inkia Business.

” As a result of this sale, our remaining power generation business consists of our 76% interest in OPC. The results of the Inkia Business are presented as discontinued operations in our audited financial statements for the three years ended December 31, 2017, and prior periods presented herein have been reclassified for comparative purposes.

FINANCIAL INFORMATION

We produce financial statements in accordance with the International Financial Reporting Standards issued by the International Accounting Standards Board, or IFRS, and all financial information included in this annual report is derived from our IFRS financial statements, except as otherwise indicated. In particular, this annual report contains certain non-IFRS financial measures which are defined under “

Item 3.A Selected Financial Data” and “Item 4.B Business Overview—Our Businesses—OPC.

”

Our consolidated financial statements included in this annual report comprise the consolidated statements of profit and loss, other comprehensive income, changes in equity, and cash flows for the years ended December 31, 2017

,

2016

and 2015

and the consolidated statement of financial position as of December 31, 2017

and

2016. We present our consolidated financial statements in U.S. Dollars.

Our financial statements as of and for the year ended December 31, 2013 and 2014 included within selected financial data presented in Item 3.A., are presented as combined carve-out financial statements and have been derived from the consolidated financial statements of IC, our former parent. These combined financial statements reflect the assets, liabilities, revenues and expenses directly attributable to us, as well as allocations deemed reasonable by us, to present our combined financial position, profit and loss and other comprehensive income, changes in equity attributable to the owners of the company and cash flows. These combined carve-out financial statements are not necessarily indicative of our financial position, profit and loss and other comprehensive income, or cash flows had we operated as a separate entity throughout the periods presented. We present our combined carve-out financial statements in U.S. Dollars.

6

The results of the Inkia Business are presented as discontinued operations in our audited financial statements for the year ended December 31, 2017. Our consolidated financial statements as of and for the years ended December 31, 2016 and 2015 and in our combined carve-out selected data as of and for the two years ended December 31, 2014, have been reclassified for comparative purposes to reflect the Inkia Business as discontinued operations.

In July 2014, ZIM completed the restructuring of its outstanding indebtedness, which resulted in IC, and consequently, Kenon, owning 32% of the restructured ZIM as compared to IC’s previous interest in ZIM of approximately 99.7%. As a result of the restructuring, ZIM’s results of operations for 2013 and the six months ended June 30, 2014 are also presented as discontinued operations.

All references in this annual report to (i) “U.S. Dollars”, “$” or “USD” are to the legal currency of the United States of America; (ii) “RMB” are to Yuan, the legal currency of the People’s Republic of China, or China; (iii) “NIS” or “New Israeli Shekel” are to the legal currency of the State of Israel, or Israel; and (iv) “S$” are to Singapore Dollars, the legal currency of the Republic of Singapore, or Singapore. We have made rounding adjustments to reach some of the figures included in this annual report. Consequently, numerical figures shown as totals in some tables may not be arithmetic aggregations of the figures that precede them.

In this annual report, we also include the consolidated financial statements of profit or loss and other comprehensive income, changes in equity, and cash flows for the years ended December 31, 2017, 2016 and 2015, and consolidated statements of financial position as of December 31, 2017 and 2016 for Qoros, pursuant to Rule 3-09 of Regulation S-X.

NON-IFRS FINANCIAL INFORMATION

In this annual report, we disclose non-IFRS financial measures, namely EBITDA and net debt, each as defined under “

Item 3.A Selected Financial Data–Selected Reportable Segment Data” and “Item 3.A Selected Financial Data–Selected Reportable Segment Data–OPC” and “Item 4.B Business Overview—Our Businesses—OPC—OPC’s Description of Operations.

” Each of these measures are important measures used by us, and our businesses, to assess financial performance. We believe that the disclosure of EBITDA and net debt provides transparent and useful information to investors and financial analysts in their review of our, or our subsidiaries’ and associated companies’, operating performance and in the comparison of such operating performance to the operating performance of other companies in the same industry or in other industries that have different capital structures, debt levels and/or income tax rates.

EXCHANGE RATE INFORMATION

The following tables set forth the historical period-end, average, high and low noon buying rates in New York City for cable transfers in foreign currencies as certified by the Federal Reserve Bank of New York for the U.S. Dollar expressed in RMB per one U.S. Dollar for the periods indicated:

|

RMB/U.S. Dollar

|

||||||||||||||||

|

Year

|

Period end

1

|

Average rate

2

|

High

|

Low

|

||||||||||||

|

2013

|

6.0537

|

6.1412

|

6.2438

|

6.0537

|

||||||||||||

|

2014

|

6.2046

|

6.1701

|

6.2591

|

6.0402

|

||||||||||||

|

2015

|

6.4778

|

6.2869

|

6.4896

|

6.1870

|

||||||||||||

|

2016

|

6.9430

|

6.6549

|

6.9580

|

6.4480

|

||||||||||||

|

2017

|

6.5063

|

6.7350

|

6.9575

|

6.4773

|

||||||||||||

| (1) |

Represents the closing exchange rate on the last business day of the applicable period.

|

| (2) |

Represents the average of the closing exchange rates on the last business day of each month during the relevant one-year periods.

|

7

|

|

RMB/U.S. Dollar

|

|||||||

|

Month

|

High

|

Low

|

||||||

|

October 2017

|

6.6533

|

6.5712

|

||||||

|

November 2017

|

6.6385

|

6.5967

|

||||||

|

December 2017

|

6.6210

|

6.5063

|

||||||

|

January 2018

|

6.5263

|

6.2841

|

||||||

|

February 2018

|

6.3471

|

6.2649

|

||||||

|

March 2018

|

6.3565

|

6.2685

|

||||||

MARKET AND INDUSTRY DATA

Certain information relating to the industries in which each of our subsidiaries and associated companies operate and their position in such industries used or referenced in this annual report were obtained from internal analysis, surveys, market research, publicly available information and industry publications. Unless otherwise indicated, all sources for industry data and statistics are estimates or forecasts contained in or derived from internal or industry sources we believe to be reliable. Market data used throughout this annual report was obtained from independent industry publications and other publicly available information. Such data, as well as internal surveys, industry forecasts and market research, while believed to be reliable, have not been independently verified. In addition, in certain cases we have made statements in this annual report regarding the industries in which each of our subsidiaries and associated companies operate and their position in such industries based upon the experience of our businesses and their individual investigations of the market conditions affecting their respective operations. We cannot assure you that any of these statements are accurate or correctly reflect the position of subsidiaries and associated companies in such industries, and none of our internal surveys or information has been verified by independent sources.

Market data and statistics are inherently predictive and speculative and are not necessarily reflective of actual market conditions. Such statistics are based upon market research, which itself is based upon sampling and subjective judgments by both the researchers and the respondents. In addition, the value of comparisons of statistics for different markets is limited by many factors, including that (i) the markets are defined differently, (ii) the underlying information was gathered by different methods and (iii) different assumptions were applied in compiling the data. Accordingly, although we believe and operate as though all market and industry information presented in this annual report is accurate, the market statistics included in this annual report should be viewed with caution.

REPRESENTATION OF OPC CAPACITY AND PRODUCTION FIGURES

Unless otherwise indicated, statistics provided throughout this annual report with respect to power generation units are expressed in MW, in the case of the capacity of such power generation units, and in GWh, in the case of the electricity production of such power generation units. One GWh is equal to 1,000 megawatt hours, or MWh, and one MWh is equal to 1,000 kilowatt hours, or kWh. Statistics relating to aggregate annual electricity production are expressed in GWh and are based on a year of 8,760 hours. Unless otherwise indicated, OPC’s capacity figures provided in this annual report reflect 100% of the capacity of all of OPC’s assets, regardless of OPC’s ownership interest in the entity that owns each such asset. For information on OPC’s ownership interest in each of its operating companies and associated companies, see “

Item 4.B Business Overview—Our Businesses—OPC.”

DISTRIBUTION OF OUR INTEREST IN TOWER

On July 23, 2015, consistent with our strategy to realize value for our shareholders by, among other things, providing direct access to our businesses via distributions, we completed the pro rata distribution in specie of 18,030,041 ordinary shares of Tower, representing 23% of the then currently outstanding Tower shares and substantially all of our interest in Tower, to holders of our ordinary shares. In 2016, we sold our remaining interest in Tower.

8

SPECIAL NOTE REGARDING FORWARD-LOOKING STATEMENTS

This annual report contains forward-looking statements within the meaning of Section 21E of the Securities Exchange Act of 1934, or the Exchange Act, and reflects our current expectations and views of the quality of our assets, our anticipated financial performance, our future growth prospects, the future growth prospects of our businesses, the liquidity of our ordinary shares, and other future events. Forward-looking statements relate to expectations, beliefs, projections, future plans and strategies, anticipated events or trends and similar expressions concerning matters that are not historical facts, and are principally contained in the sections entitled “

Item 3. Key Information

,” “

Item 4. Information on the Company

” and “

Item 5. Operating and Financial Review and Prospects

.” These statements are made under the “safe harbor” provisions of the U.S. Private Securities Litigation Reform Act of 1995. Some of these forward-looking statements can be identified by terms and phrases such as “anticipate,” “should,” “likely,” “foresee,” “believe,” “estimate,” “expect,” “intend,” “continue,” “could,” “may,” “plan,” “project,” “predict,” “will,” and similar expressions.

These forward-looking statements relate to:

| · |

our goals and strategies;

|

| · |

our capital commitments and/or intentions with respect to each of our businesses;

|

| · |

our capital allocation principles, as set forth in “

Item 4.B Business Overview”

;

|

| · |

the funding requirements, strategies, and business plans of our businesses;

|

| · |

the potential listing, offering, distribution or monetization of our businesses;

|

| · |

expected trends in the industries and markets in which each of our businesses operate;

|

| · |

our expected tax status and treatment;

|

| · |

statements relating to litigation and/or regulatory proceedings;

|

| · |

statements relating to the sale of the Inkia Business, including estimated transaction costs, management compensation, advisor fees, other expenses and taxes, receipt of deferred consideration, expectations with respect to further tax liability, risks related to the pledge of OPC’s shares, the deferred payment agreement and Kenon’s guarantee, and statements with respect to claims relating to the Inkia Business

sale

retained by Kenon;

|

| · |

the expected effect of new accounting standards on Kenon;

|

| · |

with respect to OPC

:

|

| · |

the expected cost and timing of completion and commencement of construction and development projects, as well as the anticipated installed capacities of such projects, including OPC's project Tzomet Energy, including statements with respect to OPC continuing to seek relevant approvals to develop the Tzomet project and the expected payment of the remaining consideration, and the expected financing, total cost of construction, expected capacity and COD date of the OPC-Hadera power plant;

|

| · |

the OPC restructuring, including statements with respect to Kenon’s expectation in relation to future tax liability;

|

| · |

expected macroeconomic trends in Israel, including the expected growth in energy demand;

|

| · |

potential expansions;

|

| · |

its gas supply agreements;

|

| · |

its strategy;

|

9

| · |

expected trends in energy consumption;

|

| · |

regulatory trends;

|

| · |

its anticipated capital expenditures, including the expected sources of funding for capital expenditures;

|

| · |

the price and volume of gas available to OPC-Rotem and other IPPs in Israel; and

|

| · |

with respect to Qoros

:

|

| · |

Qoros’ expectation to renew or refinance its working capital facilities to support its continued operations and development;

|

| · |

Qoros’ strategy to increase its sales volumes;

|

| · |

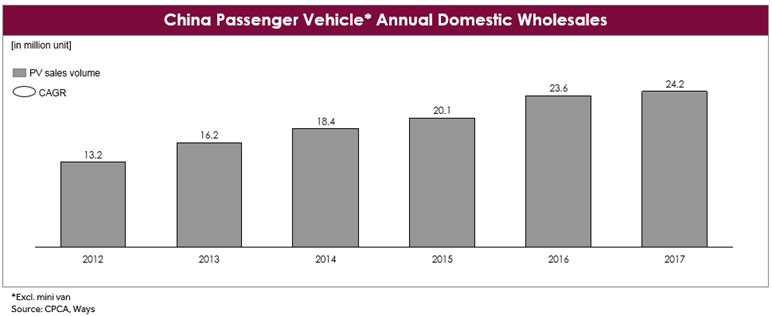

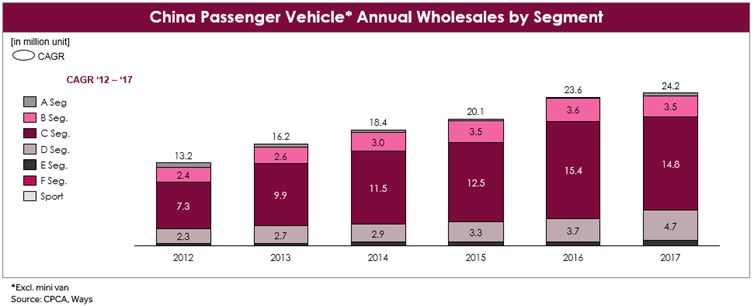

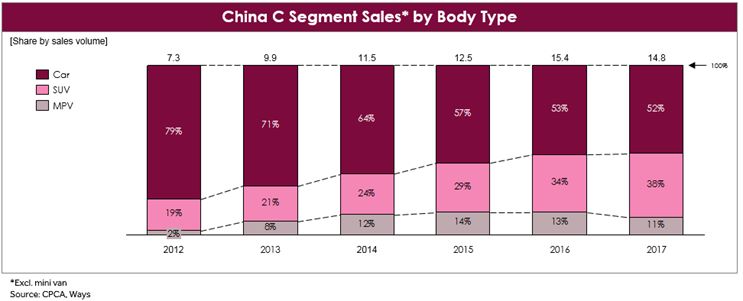

Qoros’ expectation of growth in the Chinese passenger vehicle market, particularly within the C-segment, C-segment SUV and New Energy Vehicle, or NEV, markets;

|

| · |

Qoros’ expectation of pricing trends in the Chinese passenger vehicle market;

|

| · |

Qoros’ liquidity position;

|

| · |

Qoros’ strategy to develop its dealer network;

|

| · |

Qoros’ expectation of an increase in environmental regulations and the expected effect of such regulations on Qoros’ business;

|

| · |

Qoros’ ability to increase its production capacity;

|

| · |

the investment by the New Qoros Investor into Qoros, including the various elements of the investment and expected timing thereof, including, the commitment by the investor or an affiliate to introduce vehicle purchase orders to Qoros, the requirement that Chery make payments to Kenon in connection with guarantee release

s

, the repayment or equity conversion of the Qoros shareholder loans, the put option and investor's right to make further investments under the investment agreement, and the commitment in the investment agreement that the New Qoros Investor will assume its proportionate share of Kenon and Chery’s guarantee obligations;

|

| · |

Qoros’ expectation of the development of the NEV market in China, including expected trends regarding government subsidies for the purchase of NEVs and the growth of NEV infrastructure.

|

| · |

with respect to ZIM

:

|

| · |

the assumptions used in Kenon’s and ZIM’s impairment analysis with respect to Kenon’s investment in ZIM, and ZIM’s assets, respectively, including with respect to expected fuel price, freight rates, demand trends;

|

| · |

ZIM’s strategy with respect to its debt obligations;

|

| · |

ZIM’s expectation of modifications with respect to its and other shipping companies’ operating fleet and lines, including the utilization of larger vessels within certain trade zones and modifications made in light of environmental regulations; and

|

10

| · |

trends related to the global container shipping industry, including with respect to fluctuations in container supply, industry consolidation, demand, bunker prices and charter/freights rates;

|

| · |

with respect to Primus, its

:

|

| · |

strategy;

|

| · |

plans to raise capital;

|

| · |

plans and expectations in relation to Project Marcellus;

|

| · |

potential customers;

|

| · |

project pipeline; and

|

| · |

potential sources of revenue.

|

The preceding list is not intended to be an exhaustive list of each of our forward-looking statements. The forward-looking statements are based on our beliefs, assumptions and expectations of future performance, taking into account the information currently available to us and are only predictions based upon our current expectations and projections about future events. There are important factors that could cause our actual results, level of activity, performance or achievements to differ materially from the results, level of activity, performance or achievements expressed or implied by these forward-looking statements which are set forth in “

Item 3.D Risk Factors

.” Given these risks and uncertainties, you should not place undue reliance on forward-looking statements as a prediction of actual results.

Except as required by law, we undertake no obligation to publicly update or revise any forward-looking statements, whether as a result of new information, future events or otherwise. The foregoing factors that could cause our actual results to differ materially from those contemplated in any forward-looking statement included in this annual report should not be construed as exhaustive. You should read this annual report, and each of the documents filed as exhibits to the annual report, completely, with this cautionary note in mind, and with the understanding that our actual future results may be materially different from what we expect.

A.

Directors and Senior Management

Not applicable.

B.

Advisers

Not applicable.

C.

Auditors

Not applicable.

Not applicable.

11

A.

Selected Financial Data

The following tables set forth our selected combined carve-out financial and other data as of and for the years ended December 31, 2014 and 2013 and selected consolidated financial and other data as of and for the years ended December 31, 2017, 2016 and 2015. This selected financial data should be read in conjunction with our audited consolidated financial statements, and the related notes thereto, as of December 31, 2017 and 2016 and for the years ended December 31, 2017, 2016 and 2015, included elsewhere in this annual report, and the information contained in “Item 5. Operating and Financial Review and Prospects” and “Item 3.D Risk Factors.” The historical financial and other data included here and elsewhere in this annual report should not be assumed to be indicative of our future financial condition or results of operations.

Our consolidated financial statements as of and for the year ended December 31, 2017 reflect the Inkia Business as discontinued operations and our consolidated financial statements as of and for the years ended 2016 and 2015 and our selected combined carve-out financials set forth below have been reclassified for comparative purposes to account for the Inkia Business as discontinued operations.

ZIM’s results of operations for 2013 and the six months ended June 30, 2014 are also presented as discontinued operations for the relevant periods.

Our financial statements presented in this annual report have been prepared in accordance with IFRS.

12

The selected financial data below also includes certain non-IFRS measures used by us to evaluate our economic and financial performance. These measures are not identified as accounting measures under IFRS and therefore should not be considered as an alternative measure to evaluate our performance.

|

Year Ended December 31,

|

||||||||||||||||||||

|

2017

|

2016

1

|

2015

1

|

2014

1

|

2013

1,2

|

||||||||||||||||

|

(in millions of USD, except share data)

|

||||||||||||||||||||

|

Statements of Profit and Loss Data

3

|

||||||||||||||||||||

|

Revenue

|

$

|

366

|

$

|

324

|

$

|

326

|

$

|

413

|

$

|

187

|

||||||||||

|

Cost of sales and services (excluding depreciation)

|

(267

|

)

|

(251

|

)

|

(245

|

)

|

(297

|

)

|

(139

|

)

|

||||||||||

|

Depreciation

|

(31

|

)

|

(27

|

)

|

(25

|

)

|

(24

|

)

|

(11

|

)

|

||||||||||

|

Gross profit

|

$

|

68

|

$

|

46

|

$

|

56

|

$

|

92

|

$

|

37

|

||||||||||

|

Selling, general and administrative expenses

|

(56

|

)

|

(47

|

)

|

(50

|

)

|

(86

|

)

|

(40

|

)

|

||||||||||

|

Gain from distribution of dividend in kind

|

-

|

-

|

210

|

-

|

-

|

|||||||||||||||

|

Gain from disposal of investees

|

-

|

-

|

-

|

157

|

-

|

|||||||||||||||

|

Gain on bargain purchase

|

-

|

-

|

-

|

-

|

1

|

|||||||||||||||

|

Impairment of assets and investments

|

29

|

(72

|

)

|

(7

|

)

|

(48

|

)

|

-

|

||||||||||||

|

Dilution gains from reduction in equity interest held in associates

|

-

|

-

|

33

|

-

|

-

|

|||||||||||||||

|

Other expenses

|

-

|

-

|

(1

|

)

|

(6

|

)

|

(5

|

)

|

||||||||||||

|

Other income

|

1

|

1

|

4

|

(55

|

)

|

1

|

||||||||||||||

|

Operating profit / (loss) from continuing operations

|

$

|

42

|

$

|

(72

|

)

|

$

|

245

|

$

|

54

|

$

|

(6

|

)

|

||||||||

|

Financing expenses

|

(70

|

)

|

(47

|

)

|

(36

|

)

|

(49

|

)

|

(25

|

)

|

||||||||||

|

Financing income

|

3

|

7

|

11

|

14

|

-

|

|||||||||||||||

|

Financing expenses, net

|

$

|

(67

|

)

|

$

|

(40

|

)

|

$

|

(25

|

)

|

$

|

(35

|

)

|

$

|

(25

|

)

|

|||||

|

Provision of financial guarantee

|

-

|

(130

|

)

|

-

|

-

|

-

|

||||||||||||||

|

Share in losses of associated companies, net of tax

4

|

(111

|

)

|

(186

|

)

|

(187

|

)

|

(185

|

)

|

(160

|

)

|

||||||||||

|

(Loss) / profit from continuing operations before income taxes

|

$

|

(136

|

)

|

$

|

(428

|

)

|

$

|

33

|

$

|

(166

|

)

|

$

|

(191

|

)

|

||||||

|

Income taxes

|

(73

|

)

|

(2

|

)

|

(9

|

)

|

(68

|

)

|

(2

|

)

|

||||||||||

|

(Loss) / profit for the year from continuing operations

|

$

|

(209

|

)

|

$

|

(430

|

)

|

$

|

24

|

$

|

(234

|

)

|

$

|

(193

|

)

|

||||||

|

Profit and gain from sale of discontinued operations (after taxes)

5

|

478

|

36

|

72

|

711

|

(423

|

)

|

||||||||||||||

|

Profit / (loss) for the year

|

$

|

269

|

$

|

(394

|

)

|

$

|

96

|

$

|

477

|

$

|

(616

|

)

|

||||||||

|

Attributable to:

|

||||||||||||||||||||

|

Kenon’s shareholders

|

$

|

237

|

$

|

(412

|

)

|

$

|

73

|

$

|

459

|

$

|

(631

|

)

|

||||||||

|

Non-controlling interests

|

32

|

18

|

23

|

18

|

15

|

|||||||||||||||

|

Basic/diluted (loss)/profit per share attributable to Kenon’s shareholders (in Dollars):

|

||||||||||||||||||||

|

Basic/diluted profit/(loss) per share

|

4.40

|

(7.67

|

)

|

1.36

|

8.58

|

(11.82

|

)

|

|||||||||||||

|

Basic/diluted profit/(loss) per share from continuing operations

|

(4.00

|

)

|

(8.08

|

)

|

0.24

|

(4.44

|

)

|

(3.67

|

)

|

|||||||||||

|

Basic/diluted profit/(loss) per share from discontinued operations

|

8.40

|

0.41

|

1.12

|

13.02

|

(8.15

|

)

|

||||||||||||||

|

Statements of Financial Position Data

|

||||||||||||||||||||

|

Cash and cash equivalents

|

$

|

1,417

|

$

|

327

|

$

|

384

|

$

|

610

|

$

|

671

|

||||||||||

|

Short-term investments and deposits

|

7

|

90

|

309

|

227

|

30

|

|||||||||||||||

|

Trade receivables, net

|

44

|

284

|

123

|

181

|

358

|

|||||||||||||||

|

Other current assets, including derivatives

|

36

|

50

|

45

|

59

|

98

|

|||||||||||||||

|

Income tax receivable

|

-

|

11

|

4

|

3

|

7

|

|||||||||||||||

|

Inventories

|

-

|

92

|

51

|

56

|

150

|

|||||||||||||||

|

Total current assets

|

1,504

|

854

|

916

|

1,136

|

1,314

|

|||||||||||||||

|

Total non-current assets

6

|

1,022

|

4,284

|

3,567

|

3,184

|

4,671

|

|||||||||||||||

|

Total assets

|

$

|

2,526

|

$

|

5,138

|

$

|

4,483

|

$

|

4,320

|

$

|

5,985

|

||||||||||

|

Total current liabilities

|

806

|

1,045

|

653

|

497

|

2,925

|

|||||||||||||||

|

Total non-current liabilities

|

$

|

669

|

$

|

3,199

|

$

|

2,566

|

$

|

2,385

|

$

|

2,113

|

||||||||||

|

Equity attributable to the owners of the Company

|

983

|

681

|

1,061

|

1,230

|

710

|

|||||||||||||||

|

Share capital

|

$

|

1,267

|

$

|

1,267

|

$

|

1,267

|

$

|

-

|

$

|

-

|

||||||||||

|

Total equity

|

$

|

1,051

|

$

|

894

|

$

|

1,264

|

$

|

1,438

|

$

|

947

|

||||||||||

|

Total liabilities and equity

|

$

|

2,526

|

$

|

5,138

|

$

|

4,483

|

$

|

4,320

|

$

|

5,985

|

||||||||||

|

Basic/Diluted weighted average common shares outstanding used in calculating profit/(loss) per share (thousands)

|

53,761

|

53,720

|

53,649

|

53,383

|

7

|

53,383

|

7

|

|||||||||||||

|

Statements of Cash Flow Data

|

||||||||||||||||||||

|

Net cash provided by operating activities

|

$

|

392

|

$

|

162

|

$

|

290

|

$

|

410

|

$

|

257

|

||||||||||

|

Net cash used in investing activities

|

585

|

(400

|

)

|

(737

|

)

|

(883

|

)

|

(278

|

)

|

|||||||||||

|

Net cash provided by financing activities

|

97

|

175

|

233

|

430

|

281

|

|||||||||||||||

|

(Decrease) / increase in cash and cash equivalents

|

1,074

|

(63

|

)

|

(214

|

)

|

(43

|

)

|

260

|

||||||||||||

| (1) |

Results during these periods have been reclassified to reflect the Inkia Business as discontinued operations. For further information, see Note 2

9

to our financial statements included in this annual report.

|

| (2) |

Results during this period have been reclassified to reflect ZIM and Petrotec as discontinued operations.

|

| (3) |

Consists of the consolidated results of OPC and Primus and, from June 30, 2014, the consolidated results of HelioFocus; prior to this date, Kenon did not consolidate HelioFocus’ results of operations.

|

| (4) |

Includes Kenon’s share in ZIM’s loss for the six months ended December 31, 2014 and the years ended December 31, 2015, 2016 and 2017. As from July 1, 2014, Kenon accounted for ZIM’s results of operations pursuant to the equity method of accounting.

|

13

| (5) |

Consists of (i) ZIM’s results of operations for 2013 and the six months ended June 30, 2014, (ii) Petrotec’s results of operations for 2013 through 2014 and (iii) the results of operations of the Inkia Business for 2013 through 2017.

|

| (6) |

Includes Kenon’s associated companies: (i) Qoros, (ii) Tower (until June 30, 2015), (iii) ZIM (from June 30, 2014); and (iv) HelioFocus (prior to June 30, 2014).

|

| (7) |

Based on 53,383,015 shares which were issued as of January 7, 2015, the date of our spin-off from IC.

|

Selected Reportable Segment Data

Kenon is a holding company of (i) a 76% interest in OPC, (ii) a 24% interest in Qoros, (iii) a 32% interest in ZIM, and (iv) a 91% interest in Primus. Kenon used to also hold interests in (i) the Inkia Business, which was sold effective December 31, 2017, (ii) a 22.5% interest in Tower, which was distributed to Kenon shareholders on July 23, 2015 and (iii) HelioFocus, which was liquidated in July 2017.

The results of the following companies are included in Kenon’s statements of profit and loss as share in losses of associated companies, net of tax, for the years set forth below, except as otherwise indicated: (i) Qoros, (ii) ZIM from June 30, 2014 and (iii) Tower until June 30, 2015.

Kenon’s segments are OPC, Qoros and Other. Kenon’s Other segment includes the results of ZIM, Primus, and from June 30, 2014, the results of HelioFocus and Kenon (Company level).

The following table sets forth selected financial data for Kenon’s reportable segments for the periods presented:

|

|

Year Ended December 31, 2017

1

|

|||||||||||||||||||

|

OPC

|

Qoros

2

|

Other

3

|

Adjustments

4

|

Consolidated Results

|

||||||||||||||||

|

(in millions of USD, unless otherwise indicated)

|

||||||||||||||||||||

|

Sales

|

$

|

365

|

$

|

-

|

$

|

1

|

$

|

-

|

$

|

366

|

||||||||||

|

Depreciation and amortization

|

(30

|

)

|

-

|

(1

|

)

|

-

|

(31

|

)

|

||||||||||||

|

Impairment of assets and investments

|

-

|

-

|

29

|

-

|

29

|

|||||||||||||||

|

Financing income

|

1

|

-

|

13

|

(11

|

)

|

3

|

||||||||||||||

|

Financing expenses

|

(34

|

)

|

-

|

(47

|

)

|

11

|

(70

|

)

|

||||||||||||

|

Share in (losses) income of associated companies

|

-

|

(121

|

)

|

10

|

-

|

(111

|

)

|

|||||||||||||

|

Profit / (Loss) before taxes

|

$

|

23

|

$

|

(121

|

)

|

$

|

(38

|

)

|

$

|

-

|

$

|

(136

|

)

|

|||||||

|

Income taxes

|

(9

|

)

|

-

|

(64

|

)

|

-

|

(73

|

)

|

||||||||||||

|

Profit / (Loss) from continuing operations

|

$

|

14

|

$

|

(121

|

)

|

$

|

(102

|

)

|

$

|

-

|

$

|

(209

|

)

|

|||||||

|

Segment assets

5

|

$

|

936

|

$

|

-

|

$

|

1,468

|

6

|

$

|

-

|

$

|

2,404

|

|||||||||

|

Investments in associated companies

|

-

|

2

|

120

|

-

|

122

|

|||||||||||||||

|

Segment liabilities

|

743

|

-

|

732

|

7

|

-

|

1,475

|

||||||||||||||

|

Capital expenditure

8

|

109

|

-

|

121

|

-

|

230

|

|||||||||||||||

| (1) |

In December 2017, Inkia completed the sale of the Inkia Business. For further information, see Note 2

9

to our financial statements included in this annual report.

|

| (2) |

Associated company.

|

| (3) |

Includes the results of Primus and HelioFocus (which was liquidated in July 2017); the results of ZIM, as an associated company; as well as Kenon’s and IC Green’s holding company and general and administrative expenses.

|

14

| (4) |

“Adjustments” includes inter-segment financing income and expenses.

|

| (5) |

Excludes investments in associates.

|

| (6) |

Includes Kenon’s, IC Green’s and IC Power holding company assets.

|

| (7) |

Includes Kenon’s, IC Green’s and IC Power holding company liabilities.

|

| (8) |

Includes the additions of Property, Plant and Equipment, or PP&E, and intangibles based on an accrual basis.

|

|

|

Year Ended December 31, 2016

1

|

|||||||||||||||||||

|

OPC

|

Qoros

2

|

Other

3

|

Adjustments

4

|

Consolidated Results

|

||||||||||||||||

|

(in millions of USD, unless otherwise indicated)

|

||||||||||||||||||||

|

Sales

|

$

|

324

|

$

|

—

|

$

|

—

|

$

|

-

|

$

|

324

|

||||||||||

|

Depreciation and amortization

|

(27

|

)

|

—

|

-

|

-

|

(27

|

)

|

|||||||||||||

|

Impairment of assets and investments

|

-

|

—

|

(72

|

)

|

-

|

(72

|

)

|

|||||||||||||

|

Financing income

|

3

|

—

|

16

|

(12

|

)

|

7

|

||||||||||||||

|

Financing expenses

|

(23

|

)

|

—

|

(36

|

)

|

12

|

(47

|

)

|

||||||||||||

|

Share in losses of associated companies

|

-

|

(143

|

)

|

(43

|

)

|

-

|

(186

|

)

|

||||||||||||

|

Provision of financial guarantee

|

-

|

—

|

(130

|

)

|

-

|

(130

|

)

|

|||||||||||||

|

Profit/(Loss) before taxes

|

$

|

20

|

$

|

(143

|

)

|

$

|

(305

|

)

|

$

|

-

|

$

|

(428

|

)

|

|||||||

|

Income taxes

|

—

|

—

|

(2

|

)

|

-

|

(2

|

)

|

|||||||||||||

|

Profit/(Loss) from continuing operations

|

$

|

20

|

$

|

(143

|

)

|

$

|

(307

|

)

|

$

|

-

|

$

|

(430

|

)

|

|||||||

|

Segment assets

5

|

$

|

668

|

$

|

—

|

$

|

4,262

|

$

|

-

|

$

|

4,930

|

||||||||||

|

Investments in associated companies

|

-

|

118

|

90

|

-

|

208

|

|||||||||||||||

|

Segment liabilities

|

534

|

—

|

3,710

|

-

|

4,244

|

|||||||||||||||

|

Capital expenditure

8

|

73

|

—

|

245

|

-

|

318

|

|||||||||||||||

| (1) |

Results during this period have been reclassified to reflect the results of the Inkia Business as discontinued operations. For further information, see Note 29 to our financial statements included in this annual report.

|

| (2) |

Associated company.

|

| (3) |

Includes the results of Primus and HelioFocus (which was liquidated in July 2017); the results of ZIM, as an associated company; as well as Kenon’s and IC Green’s holding company and general and administrative expenses.

|

| (4) |

“Adjustments” includes inter-segment financing income and expenses.

|

| (5) |

Excludes investments in associates.

|

| (6) |

Includes Kenon’s, IC Green’s and IC Power holding company assets.

|

| (7) |

Includes Kenon’s, IC Green’s and IC Power holding company liabilities.

|

| (8) |

Includes the additions of PP&E and intangibles based on an accrual basis.

|

15

|

Year Ended December 31, 2015

1

|

||||||||||||||||||||

|

OPC

|

Qoros

2

|

Other

3

|

Adjustments

4

|

Consolidated Results

|

||||||||||||||||

|

(in millions of USD, unless otherwise indicated)

|

||||||||||||||||||||

|

Sales

|

$

|

326

|

$

|

—

|

$

|

—

|

$

|

-

|

$

|

326

|

||||||||||

|

Depreciation and amortization

|

(26

|

)

|

—

|

1

|

—

|

(25

|

)

|

|||||||||||||

|

Asset impairment

|

-

|

—

|

(7

|

)

|

—

|

(7

|

)

|

|||||||||||||

|

Financing income

|

3

|

—

|

8

|

—

|

11

|

|||||||||||||||

|

Financing expenses

|

(26

|

)

|

—

|

(10

|

)

|

—

|

(36

|

)

|

||||||||||||

|

Share in (losses) income of associated companies

|

-

|

(196

|

)

|

9

|

—

|

187

|

||||||||||||||

|

Gain from distribution of dividend in kind

|

-

|

—

|

210

|

—

|

210

|

|||||||||||||||

|

Profit/(Loss) before taxes

|

$

|

30

|

$

|

(196

|

)

|

$

|

199

|

$

|

—

|

$

|

33

|

|||||||||

|

Income taxes

|

(8

|

)

|

—

|

(1

|

)

|

—

|

(9

|

)

|

||||||||||||

|

Profit/(Loss) from continuing operations

|

$

|

22

|

$

|

(196

|

)

|

$

|

198

|

$

|

—

|

$

|

24

|

|||||||||

|

Segment assets

5

|

$

|

811

|

$

|

—

|

$

|

3,303

|

6

|

$

|

—

|

$

|

4,114

|

|||||||||

|

Investments in associated companies

|

-

|

159

|

210

|

—

|

369

|

|||||||||||||||

|

Segment liabilities

|

677

|

—

|

2,542

|

7

|

—

|

3,219

|

||||||||||||||

|

Capital expenditure

8

|

18

|

—

|

556

|

—

|

574

|

|||||||||||||||

| (1) |

Results during this period have been reclassified to reflect the results of the Inkia Business as discontinued operations. For further information, see Note 29 to our financial statements included in this annual report.

|

| (2) |

Associated company.

|

| (3) |

Includes the results of Primus and HelioFocus (which was liquidated in July 2017); the results of ZIM and Tower (up to June 30, 2015), as associated companies; as well as Kenon’s and IC Green’s holding company and general and administrative expenses.

|

| (4) |

“Adjustments” includes inter-segment sales.

|

| (5) |

Excludes investments in associates.

|

| (6) |

Includes Kenon’s, IC Green’s and IC Power holding company assets.

|

| (7) |

Includes Kenon’s, IC Green’s and IC Power holding company liabilities.

|

| (8) |

Includes the additions of PP&E and intangibles based on an accrual basis.

|

OPC

The following tables set forth other financial and key operating data for OPC for the periods presented:

|

2017

|

2016

|

2015

|

||||||||||

|

($ millions, except as otherwise indicated)

|

||||||||||||

|

Net income for the period

|

14

|

20

|

22

|

|||||||||

|

EBITDA

1

|

86

|

67

|

79

|

|||||||||

|

Net Debt

2

|

395

|

371

|

289

|

|||||||||

|

Net energy generated (GWh)

|

3,655

|

3,510

|

3,736

|

3

|

||||||||

|

Energy sales (GWh)

|

3,988

|

3.996

|

3,953

|

4

|

||||||||

| (1) |

OPC defines “EBITDA” for each period as net income (loss) for the period before depreciation and amortization, financing expenses, net and income tax expense.

|

EBITDA is not recognized under IFRS or any other generally accepted accounting principles as a measure of financial performance and should not be considered as a substitute for net income or loss, cash flow from operations or other measures of operating performance or liquidity determined in accordance with IFRS. EBITDA is not intended to represent funds available for dividends or other discretionary uses because those funds may be required for debt service, capital expenditures, working capital and other commitments and contingencies. EBITDA presents limitations that impair its use as a measure of OPC’s profitability since it does not take into consideration certain costs and expenses that result from its business that could have a significant effect on OPC’s net income, such as finance expenses, taxes and depreciation.

16

The following table sets forth a reconciliation of OPC’s net income to its EBITDA for the periods presented. Other companies may calculate EBITDA differently, and therefore this presentation of EBITDA may not be comparable to other similarly titled measures used by other companies:

|

Year Ended December 31,

|

||||||||||||

|

2017

|

2016

|

2015

|

||||||||||

|

(in millions of USD)

|

||||||||||||

|

Net income for the period

|

$

|

14

|

$

|

20

|

$

|

22

|

||||||

|

Depreciation and amortization

|

30

|

27

|

26

|

|||||||||

|

Finance expenses, net

|

33

|

20

|

23

|

|||||||||

|

Income tax expense

|

9

|

-

|

8

|

|||||||||

|

EBITDA

|

$

|

86

|

$

|

67

|

$

|

79

|

||||||

| (2) |

Net debt is calculated as total debt, minus cash

(which includes

short term deposits and restricted cash and long-term deposits and restricted cash

)

. Net debt is not a measure recognized under IFRS. The tables below sets forth a reconciliation of OPC’s total debt to net debt.

|

|

Year Ended December 31, 2017

|

||||||||||||||||

|

OPC-Rotem

|

OPC-Hadera

|

Energy & Others

|

Total OPC

|

|||||||||||||

|

(in millions of USD)

|

||||||||||||||||

|

Total debt

(i)

|

383

|

144

|

91

|

618

|

||||||||||||

|

Cash

(ii)

|

86

|

31

|

106

|

223

|

||||||||||||

|

Net Debt

|

$

|

297

|

$

|

113

|

$

|

(15

|

)

|

$

|

395

|

|||||||

| (i) |

Total debt comprises loans from banks and third parties and debentures, and includes long term and short term debt.

|

| (ii) |

Includes short-term deposits and restricted cash of $0 million; and includes long-term deposits and restricted cash of $76 million (including $22 million in cash that was deposited into an escrow account in connection with the Tamar gas dispute. For further information, see “

|

|

Year Ended December 31, 2016

|

||||||||||||||||

|

OPC-Rotem

|

OPC-Hadera

|

Energy & Others

|

Total OPC

|

|||||||||||||

|

(in millions of USD)

|

||||||||||||||||

|

Total debt

(i)

|

365

|

—

|

52

|

417

|

||||||||||||

|

Cash

(ii)

|

22

|

1

|

23

|

46

|

||||||||||||

|

Net Debt

|

$

|

343

|

$

|

(1

|

)

|

$

|

29

|

$

|

371

|

|||||||

| (i) |

Total debt comprises loans from banks and third parties and debentures, and includes long term and short term debt.

|

| (ii) |

Includes short-term deposits and restricted cash of $4 million and long-term deposits and restricted cash of $19 million.

|

|

Year Ended

December 31,

2015

|

||||

|

Total OPC

|

||||

|

(in millions of USD)

|

||||

|

Total debt

(i)

|

473

|

|||

|

Cash

(ii)

|

184

|

|||

|

Net Debt

|

$

|

289

|

||

| (i) |

Total debt comprises loans from banks and third parties and debentures, and includes long term and short term debt.

|

| (ii) |

Includes short-term deposits and restricted cash of $

50

million and long-term deposits and restricted cash of $

17

million.

|

| (3) |

Includes generation of OPC-Rotem only.

|

| (4) |

Includes sales of OPC-Rotem only.

|

Set forth below is a summary of certain OPC key historical financial and other operational information, for the periods set forth below.

|

Year Ended December 31,

|

||||||||||||

|

2017

|

2016

|

2015

|

||||||||||

|

($ millions, except as otherwise indicated)

|

||||||||||||

|

Sales

|

365

|

324

|

326

|

|||||||||

|

Cost of Sales

|

(266

|

)

|

(251

|

)

|

(245

|

)

|

||||||

|

Operating income (loss)

|

69

|

46

|

57

|

|||||||||

|

Operating margins

|

19

|

%

|

14

|

%

|

17

|

%

|

||||||

|

Financing expenses, net

|

33

|

20

|

23

|

|||||||||

|

Net income for the period

|

14

|

20

|

22

|

|||||||||

|

Net Energy sales (GWh)

|

3,988

|

3.996

|

3,953

|

1

|

||||||||

| (1) |

Includes sales of OPC-Rotem only.

|

17

B.

Capitalization and Indebtedness

Not applicable.

C.

Reasons for the Offer and Use of Proceeds

Not applicable.

D.

Risk Factors

Our business, financial condition, results of operations and liquidity can suffer materially as a result of any of the risks described below. While we have described all of the risks we consider material, these risks are not the only ones we face. We are also subject to the same risks that affect many other companies, such as technological obsolescence, labor relations, geopolitical events, climate change and risks related to the conducting of international operations. Additional risks not known to us or that we currently consider immaterial may also impair our business operations. Our businesses routinely encounter and address risks, some of which may cause our future results to be different—sometimes materially different—than we presently anticipate.

Risks Related to Our Strategy and Operations

Some of our businesses have significant capital requirements.

The business plans of our businesses contemplate additional debt or equity financing which is expected to be raised from third parties. However, our businesses may be unable to raise the necessary capital from third party financing sources, and in this case Kenon would be their only source of funding. For example, Qoros will require additional cash to further its development and, until it achieves significant sales levels, to meet its operating expenses, financing expenses, and capital expenditures.

In the event that one or more of our businesses require capital, either in accordance with their business plans or in response to new developments or to meet operating expenses, and such businesses are unable to raise such financing, Kenon may (i) issue equity in the form of shares or convertible instruments (through a pre-emptive offering or otherwise), (ii) provide financing to a business using funds received from the operations or sales of Kenon’s other businesses, (iii) sell part, or all, of its interest in any of its businesses, (iv) raise debt financing at the Kenon level or (v) provide guarantees or collateral in support of the debt of its businesses. To the extent debt financing is available to it, any debt financing that Kenon incurs may not be on favorable terms, may require Kenon to agree to restrictive covenants that limit how Kenon manages its investments in its businesses, and may also limit dividends or other distributions by Kenon. In addition, any equity financing, whether in the form of a sale of shares or convertible instruments, would dilute existing holders of our ordinary shares and any such equity financing could be at prices that are lower than the current trading prices.