UNITED STATES SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

Form 10-K

ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d)

OF THE SECURITIES EXCHANGE ACT OF 1934

For the

Fiscal Year Ended December 31, 2013

Commission file number 001-35714

MPLX LP

(Exact name of registrant as specified in its charter)

|

Delaware

|

45-5010536

|

|

|

(State or other jurisdiction of incorporation or organization)

|

(I.R.S. Employer Identification No.)

|

|

200 E. Hardin Street, Findlay, Ohio 45840

(Address of principal executive offices)

(419) 672-6500

(Registrant’s telephone number, including area code)

Securities registered pursuant to Section 12(b) of the Act:

|

Title of each class

|

Name of each exchange on which registered

|

|

|

Common Units Representing Limited Partnership Interests

|

New York Stock Exchange

|

|

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act.

Yes

x

No

¨

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Act. Yes

¨

No

x

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes

x

No

¨

Indicate by check mark whether the registrant has submitted electronically and posted on its corporate web site, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T (§232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files.) Yes

x

No

¨

Indicate by check mark if disclosure of delinquent filers pursuant to Item 405 of Regulation S-K (§ 229.405 of this chapter) is not contained herein, and will not be contained, to the best of registrant’s knowledge, in definitive proxy or information statements incorporated by reference in Part III of this Form 10-K or any amendment to this Form 10-K.

x

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer or a smaller reporting company. See the definitions of “large accelerated filer,” “accelerated filer” and “smaller reporting company” in Rule 12b-2 of the Exchange Act. (Check one):

Large accelerated filer

þ

Accelerated filer

¨

Non-accelerated filer

¨

Smaller reporting company

¨

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act) Yes

¨

No

x

The aggregate market value of Common Units held by non-affiliates as of June 28, 2013 was approximately

$715.9 million

. Common Units held by executive officers and directors of the registrant and its affiliates are not included in the computation. The registrant, solely for the purpose of this required presentation, has deemed its directors and executive officers and those of its affiliates to be affiliates.

MPLX LP had

36,956,712

common units,

36,951,515

subordinated units and

1,508,331

general partner units outstanding at

February 14, 2014

.

DOCUMENTS INCORPORATED BY REFERENCE:

None

MPLX LP

Unless the context otherwise requires, references in this report to the “Predecessor,” “we,” “our,” “us,” or like terms, when used in periods prior to October 31, 2012, refer to MPLX LP Predecessor, our predecessor for accounting purposes. References in this report to “MPLX LP,” “the Partnership,” “we,” “our,” “us,” or like terms used in the present tense or periods starting on or after October 31, 2012, refer to MPLX LP and its subsidiaries, including MPLX Operations LLC (“MPLX Operations”) and MPLX Terminal and Storage LLC (“MPLX Terminal and Storage”), both wholly-owned subsidiaries, and MPLX Pipe Line Holdings LP (“Pipe Line Holdings”), of which as of

December 31, 2013

MPLX LP owned a

56.0

percent general partner interest. Pipe Line Holdings owns 100 percent of Marathon Pipe Line LLC ("MPL") and Ohio River Pipe Line LLC ("ORPL"). References to “MPC” refer collectively to Marathon Petroleum Corporation and its subsidiaries, other than the Partnership. Prior to June 30, 2011, MPC was a wholly owned subsidiary of Marathon Oil Corporation. Marathon Oil Corporation and all its subsidiaries and equity method investments not spun off with MPC are referred to as “Marathon Oil.”

Table of Contents

|

|

|

Page

|

|

Item 1.

|

||

|

Item 1A.

|

||

|

Item 1B

|

||

|

Item 2.

|

||

|

Item 3.

|

||

|

Item 4.

|

||

|

Item 5.

|

||

|

Item 6.

|

||

|

Item 7.

|

||

|

Item 7A.

|

||

|

Item 8.

|

||

|

Item 9.

|

||

|

Item 9A.

|

||

|

Item 9B.

|

||

|

Item 10.

|

||

|

Item 11.

|

||

|

Item 12.

|

||

|

Item 13.

|

||

|

Item 14.

|

||

|

Item 15.

|

||

Disclosures Regarding Forward-Looking Statements

This Annual Report on Form 10-K, particularly Item 1. Business, Item 1A. Risk Factors, Item 3. Legal Proceedings, Item 7. Management’s Discussion and Analysis of Financial Condition and Results of Operations and Item 7A. Quantitative and Qualitative Disclosures about Market Risk, includes forward-looking statements. You can identify our forward-looking statements by words such as “anticipate,” “believe,” “estimate,” “expect,” “forecast,” “project,” “could,” “may,” “should,” “would,” “will” or other similar expressions that convey the uncertainty of future events or outcomes. In accordance with “safe harbor” provisions of the Private Securities Litigation Reform Act of 1995, these statements are accompanied by cautionary language identifying important factors, though not necessarily all such factors, that could cause future outcomes to differ materially from those set forth in the forward-looking statements.

Forward-looking statements include, but are not limited to, statements that relate to, or statements that are subject to risks, contingencies or uncertainties that relate to:

|

•

|

future levels of revenues and other income, income from operations, net income attributable to MPLX LP, earnings per unit, Adjusted EBITDA or Distributable Cash Flow (please read Item 7. Management’s Discussion and Analysis of Financial Condition and Results of Operations – How We Evaluate Our Operations – Adjusted EBITDA and Distributable Cash Flow for the definitions of Adjusted EBITDA and Distributable Cash Flow);

|

|

•

|

anticipated volumes of throughput of crude oil, refined products or other hydrocarbon-based products;

|

|

•

|

anticipated levels of regional, national and worldwide prices of crude oil and refined products;

|

|

•

|

future levels of capital, environmental or maintenance expenditures, general and administrative and other expenses;

|

|

•

|

the success or timing of completion of ongoing or anticipated capital or maintenance projects;

|

|

•

|

expectations regarding the acquisition or divestiture of assets;

|

|

•

|

the effect of restructuring or reorganization of business components;

|

|

•

|

the potential effects of judicial or other proceedings on our business, financial condition, results of operations and cash flows; and

|

|

•

|

the anticipated effects of actions of third parties such as competitors, or federal, foreign, state or local regulatory authorities, or plaintiffs in litigation.

|

We have based our forward-looking statements on our current expectations, estimates and projections about our industry and our partnership. We caution that these statements are not guarantees of future performance and you should not rely unduly on them, as they involve risks, uncertainties, and assumptions that we cannot predict. In addition, we have based many of these forward-looking statements on assumptions about future events that may prove to be inaccurate. While our management considers these assumptions to be reasonable, they are inherently subject to significant business, economic, competitive, regulatory and other risks, contingencies and uncertainties, most of which are difficult to predict and many of which are beyond our control. Accordingly, our actual results may differ materially from the future performance that we have expressed or forecast in our forward-looking statements. Differences between actual results and any future performance suggested in our forward-looking statements could result from a variety of factors, including the following:

|

•

|

changes in general economic, market or business conditions;

|

|

•

|

domestic and foreign supplies of crude oil and other feedstocks;

|

|

•

|

domestic and foreign supplies of refined products such as gasoline, diesel fuel, jet fuel, home heating oil and petrochemicals;

|

|

•

|

foreign imports of refined products;

|

|

•

|

refining industry overcapacity or undercapacity;

|

|

•

|

changes in the cost or availability of third-party vessels, pipelines and other means of transportation for crude oil, feedstocks and refined products;

|

1

|

•

|

the price, availability and acceptance of alternative fuels and alternative-fuel vehicles and laws mandating such fuels or vehicles;

|

|

•

|

fluctuations in consumer demand for refined products, including seasonal fluctuations;

|

|

•

|

political and economic conditions in nations that consume refined products, including the United States, and in crude oil producing regions, including the Middle East, Africa, Canada and South America;

|

|

•

|

actions taken by our competitors and the expansion and retirement of pipeline capacity in response to market conditions;

|

|

•

|

changes in fuel and utility costs for our facilities;

|

|

•

|

failure to realize the benefits projected for capital projects, or cost overruns associated with such projects;

|

|

•

|

the ability to successfully implement new assets and growth strategies, whether through organic growth or acquisitions;

|

|

•

|

accidents or other unscheduled shutdowns affecting our pipelines or equipment, or those of our suppliers or customers;

|

|

•

|

unusual weather conditions and natural disasters;

|

|

•

|

disruptions due to equipment interruption or failure;

|

|

•

|

acts of war, terrorism or civil unrest that could impair our ability to transport crude oil or refined products;

|

|

•

|

legislative or regulatory action, which may adversely affect our business or operations;

|

|

•

|

rulings, judgments or settlements in litigation or other legal, tax or regulatory matters, including unexpected environmental remediation costs, in excess of any reserves or insurance coverage;

|

|

•

|

labor and material shortages;

|

|

•

|

the ability and willingness of parties with whom we have material relationships to perform their obligations to us;

|

|

•

|

changes in the availability of unsecured credit and changes affecting the credit markets generally; and

|

|

•

|

the other factors described in Item 1A. Risk Factors.

|

We undertake no obligation to update any forward-looking statements except to the extent required by applicable law.

2

We are a fee-based, growth-oriented master limited partnership formed by MPC to own, operate, develop and acquire pipelines and other midstream assets related to the transportation and storage of crude oil, refined products and other hydrocarbon-based products. At

December 31, 2013

, our assets primarily consisted of a

56.0

percent indirect interest in a network of common carrier crude oil and product pipeline systems and associated storage assets in the Midwest and Gulf Coast regions of the United States. We believe our network of petroleum pipelines is one of the largest in the United States, based on total annual volumes delivered. MPC has retained a

44.0

percent interest in our network of pipeline systems, barge dock and tank farms. We also own a

100

percent interest in a butane cavern in Neal, West Virginia with approximately

1.0

million barrels of storage capacity. Our assets are integral to the success of MPC’s operations.

We generate revenue primarily by charging tariffs for transporting crude oil, refined products and other hydrocarbon-based products through our pipelines and at our barge dock and fees for storing crude oil and products at our storage facilities. We are also the operator of additional crude oil and product pipelines owned by MPC and third parties for which we are paid operating fees. We do not take ownership of the crude oil or products that we transport and store for our customers, and we do not engage in the trading of any commodities. However, we could be required to purchase crude oil volumes in the open market to make up negative imbalances. See Item 7A. Quantitative and Qualitative Disclosures about Market Risk for information on imbalances.

MPC historically has been the source of the substantial majority of our revenues. In connection with the MPLX LP initial public offering (the “Offering”) completed on October 31, 2012, we entered into multiple transportation and storage services agreements with MPC. These agreements are long-term, fee-based agreements with minimum volume commitments under which MPC will continue to be the source of the substantial majority of our revenues for the foreseeable future. We believe these transportation and storage services agreements will promote stable and predictable cash flows.

MPC has stated that it intends for us to be the primary growth vehicle for its midstream business. MPC owns a substantial portfolio of other midstream assets including a

44.0

percent interest in Pipe Line Holdings, which owns our network of pipeline systems, our barge dock and our tank farms. MPC also owns a significant interest in us through its ownership of our general partner, a

71.6

percent limited partner interest in us and all of our incentive distribution rights. Given MPC’s significant ownership interest in us and its stated intent to use us to grow its midstream business, we believe MPC will continue to offer us the opportunity to purchase additional midstream assets that it owns, including additional interests in Pipe Line Holdings. We also may pursue acquisitions cooperatively with MPC. MPC is under no obligation, however, to offer to sell us additional assets or to pursue acquisitions cooperatively with us, and we are under no obligation to buy any such additional assets or pursue any such cooperative acquisitions. We also intend to grow our business by constructing new assets, increasing the utilization of, and revenue generated by, our existing assets and acquiring assets from third parties.

On

February 27, 2014

, we entered into an agreement to acquire an additional

13.0 percent

interest in Pipe Line Holdings from MPC for consideration of

$310.0 million

, effective

March 1, 2014

. Subsequent to this transaction, our ownership in Pipe Line Holdings will be

69.0 percent

. We intend to finance this transaction with $40.0 million of cash on hand and by borrowing $270.0 million on our revolving credit agreement.

Our operations consist of one reportable segment and are all conducted in the United States. All of our assets are located in the United States. See Item 8. Financial Statements and Supplementary Data for financial information on our operations and assets, which is incorporated herein by reference.

3

ORGANIZATIONAL STRUCTURE

The following diagram depicts our organizational structure and MPC’s ownership interests in us as of February 14, 2014.

4

BUSINESS STRATEGIES

Our primary business objectives are to generate stable cash flows and increase our quarterly cash distribution per unit over an extended period of time. We intend to accomplish these objectives by executing the following strategies:

Focus on Fee-Based Businesses.

We are focused on generating stable cash flows by providing fee-based midstream services to MPC and third parties. We also intend to mitigate volatility in cash flows by continuing to minimize our exposure to commodity price fluctuations.

Increase Revenue and Pursue Organic Growth Opportunities.

We intend to increase revenue on our network of pipeline systems by evaluating and capitalizing on organic investment opportunities that may arise from the growth of MPC’s operations and from increased third-party activity in our areas of operations. We will evaluate organic growth projects within our geographic footprint, as well as in new areas, that provide attractive returns and cash flow characteristics.

Grow through Acquisitions.

We plan to pursue acquisitions of complementary assets from MPC as well as third parties. We believe MPC will offer us the opportunity to purchase additional midstream assets that it owns, including its additional interest in Pipe Line Holdings. We also may pursue acquisitions cooperatively with MPC. Our third-party acquisition strategy may include midstream assets both within our existing geographic footprint and in new areas.

Sustain Long-Term Growth.

Our goal is to maintain an attractive distribution growth profile over the long term. During 2013, we increased our distributions every quarter and for the full year our distributions increased 19 percent. We believe our ability to sustain an attractive distribution growth profile is supported by MPC's significant number and variety of midstream assets, which we may potentially acquire, and the organic growth opportunities we plan to pursue.

Maintain Safe and Reliable Operations.

We believe that providing safe, reliable and efficient services is a key component in generating stable cash flows, and we are committed to maintaining and improving the safety, reliability and efficiency of our operations. As part of MPC’s broader corporate programs, we have adopted, and intend to continue to participate in, the Responsible Care

®

initiative, which promotes a higher standard for safety and environmental stewardship. In December 2009, we received third-party certification from Det Norske Veritas of our Responsible Care Management System

®

and we obtained recertification in December 2012.

COMPETITIVE STRENGTHS

We believe we are well positioned to execute our business strategies based on the following competitive strengths:

Multiple Growth Opportunities.

We have organic growth prospects associated with the anticipated growth of MPC’s operations and third-party activity in our areas of operation that will augment expected revenue growth from annual tariff increases under Federal Energy Regulatory Commission ("FERC") indexing methodology and market-based rates and increased throughput volumes on our pipelines. We also plan to pursue acquisitions of complementary assets from or cooperatively with MPC. We believe MPC will continue to offer us the opportunity to purchase additional midstream assets that it owns, including additional interests in Pipe Line Holdings.

Strategic Relationship with MPC.

We have a strategic relationship with MPC, which we believe to be the fourth-largest petroleum products refiner in the United States and the largest petroleum products refiner in the Midwest region of the United States based on crude oil refining capacity. MPC is well-capitalized, with an investment grade credit rating, and owns our general partner, a

71.6

percent limited partner interest in us and all of our incentive distribution rights. MPC also owns other substantial midstream assets that are broadly estimated to generate annual earnings before interest, tax, depreciation and amortization of $800 million. In addition, MPC is pursuing a number of projects that will likely increase the amount of midstream assets it will own and the related earnings and cash flow. For example, MPC recently announced the agreement with Enbridge Energy Partners, L.P. ("Enbridge") to serve as an anchor shipper on the Sandpiper pipeline, which will run from Beaver Lodge, North Dakota to Superior, Wisconsin. MPC also recently announced an agreement with Enbridge Inc. to serve as the anchor shipper on the proposed Southern Access Extension pipeline. We believe that our relationship with MPC will provide us with significant growth opportunities, as well as a stable base of cash flows.

Stable and Predictable Cash Flows.

Our assets primarily consist of common carrier pipeline systems that generate stable revenue from FERC-based tariffs. We generate the substantial majority of our revenue under long-term, fee-based transportation and storage services agreements with MPC that include minimum volume commitments. We believe these agreements enhance cash flow stability and predictability. We also expect that, based on MPC’s historical shipping patterns, MPC will ship volumes on the majority of our pipelines in excess of its minimum volume commitments. For those pipeline systems where MPC does not ship the minimum quarterly volume commitments, we will receive quarterly deficiency payments that support our cash flows.

5

Strategically Located Assets.

Our assets are primarily located in the Midwest and Gulf Coast regions of the United States, which collectively comprised approximately

72

percent of total U.S. crude distillation capacity and approximately

48

percent of total U.S. finished products demand for the year ended December 31, 2012, according to the U.S. Energy Information Administration (“EIA”). MPC owns and operates seven refineries in the Midwest and Gulf Coast regions of the United States, which have an aggregate crude oil refining capacity of approximately

1.7 million

barrels per calendar day. Our assets are integral to the success of MPC’s operations. Our assets are located near several emerging shale plays including the Marcellus, Utica, New Albany, Antrim and Illinois Basin in Pennsylvania, Ohio, Indiana, Michigan and Illinois, respectively. MPC is currently transporting crude oil and condensate from the Utica shale play and is actively evaluating similar growth opportunities in other emerging shale plays.

High-Quality, Well-Maintained Asset Base.

We continually invest in the maintenance and integrity of our assets and have developed various programs to help us efficiently monitor and maintain them. For example, we utilize MPC’s patented integrity management program that employs state-of-the-art mechanical integrity inspection and repair programs to enhance the safety of our pipelines.

Financial Flexibility.

We have an undrawn revolving credit facility of

$500.0 million

. As of December 31, 2013, we also had

$54.1 million

of cash available to fund future expansion capital expenditures related to our assets. We believe that we will have the financial flexibility to execute our growth strategy through our cash reserves, borrowing capacity under our revolving credit facility and access to the debt and equity capital markets.

Experienced Management Team.

Our management team has substantial experience in the management and operation of pipelines, barge docks, storage facilities and other midstream assets. Our management team also has expertise in acquiring and integrating assets as well as executing growth strategies in the midstream sector.

6

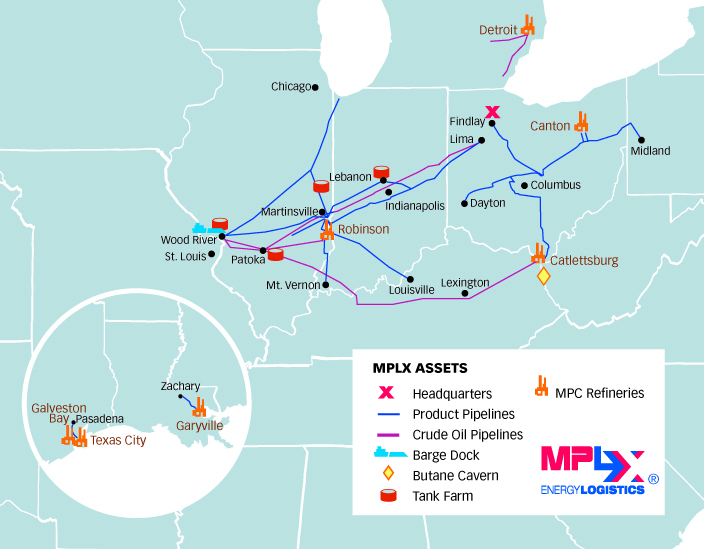

OUR ASSETS AND OPERATIONS

As of December 31, 2013, our primary assets consisted of:

|

•

|

a

56.0 percent

general partner interest in Pipe Line Holdings, an entity that owns a

100 percent

interest in MPL and ORPL, which in turn collectively own:

|

|

•

|

a network of pipeline systems that includes approximately

1,004 miles

of common carrier crude oil pipelines and approximately

1,902 miles

of common carrier product pipelines extending across nine states. This network includes approximately

230 miles

of common carrier crude oil and product pipelines that we operate under long-term leases with third parties;

|

|

•

|

a barge dock located on the Mississippi River near Wood River, Illinois with

84

thousand barrels per day (“mbpd”) of crude oil and product throughput capacity; and

|

|

•

|

crude oil and product tank farms located in Patoka, Wood River and Martinsville, Illinois and Lebanon, Indiana.

|

|

•

|

a

100 percent

interest in a butane cavern located in Neal, West Virginia with approximately

1.0 million

barrels of storage capacity that serves MPC’s Catlettsburg, Kentucky refinery.

|

As the sole general partner of Pipe Line Holdings, we control all aspects of the management of Pipe Line Holdings, including its cash distribution policy. The remaining limited partnership interest in Pipe Line Holdings is retained by MPC.

7

Crude Oil Pipeline Systems

The following table sets forth certain information regarding our crude oil pipeline systems, each of which has an associated transportation services agreement with MPC (other than the inactive pipelines):

Crude Oil Pipeline Systems

|

System name

|

Diameter

(inches) |

Length

(miles) |

Capacity

(mbpd) (1) |

Associated MPC refineries

|

||||||

|

Patoka to Lima crude system

|

||||||||||

|

Patoka, IL to Lima, OH

|

20”/22”

|

302

|

|

249

|

|

Detroit, MI; Canton, OH

|

||||

|

Catlettsburg and Robinson crude system

|

||||||||||

|

Patoka, IL to Robinson, IL

|

20”

|

78

|

|

225

|

|

Robinson, IL

|

||||

|

Patoka, IL to Catlettsburg, KY

|

24”/20”

|

406

|

|

270

|

|

Catlettsburg, KY

|

||||

|

Subtotal

|

484

|

|

495

|

|

||||||

|

Detroit crude system

|

||||||||||

|

Samaria, MI to Detroit, MI

|

16”

|

44

|

|

140

|

|

Detroit, MI

|

||||

|

Romulus, MI to Detroit, MI

(2)

|

16”

|

17

|

|

180

|

|

Detroit, MI

|

||||

|

Subtotal

|

61

|

|

320

|

|

||||||

|

Wood River to Patoka crude system

|

||||||||||

|

Wood River, IL to Patoka, IL

|

22”

|

57

|

|

215

|

|

All Midwest refineries

|

||||

|

Roxanna, IL to Patoka, IL

(3)

|

12”

|

58

|

|

99

|

|

All Midwest refineries

|

||||

|

Subtotal

|

115

|

|

314

|

|

||||||

|

Inactive pipelines

|

42

|

|

n/a

|

|

||||||

|

Total crude oil pipelines

|

1,004

|

|

1,378

|

|

||||||

|

(1)

|

Capacity shown is

100 percent

of the capacity of these pipeline systems and based on physical barrels. At December 31, 2013, we owned a

56.0 percent

indirect interest in these pipeline systems through Pipe Line Holdings.

|

|

(2)

|

Includes approximately

16 miles

of pipeline leased from a third party.

|

|

(3)

|

This pipeline is leased from a third party.

|

Our crude oil pipeline systems and related assets are strategically positioned to support diverse and flexible crude oil supply options for MPC’s Midwest refineries, which receive imported and domestic crude oil through a variety of sources. Imported and domestic crude oil is transported to supply hubs in Wood River and Patoka, Illinois from a variety of regions, including: Cushing, Oklahoma on the Ozark pipeline system; Western Canada, Wyoming and North Dakota on the Keystone, Platte, Mustang and Enbridge pipeline systems; and the Gulf Coast on the Capline crude oil pipeline system. Our major crude oil pipeline systems are connected to these supply hubs and transport crude oil to refineries owned by MPC and third parties.

The following are descriptions of each of our crude oil pipeline systems and related assets:

Patoka to Lima crude system

. Our Patoka to Lima crude system is comprised of approximately

76 miles

of

20

-inch pipeline extending from Patoka, Illinois to Martinsville, Illinois, and approximately

226 miles

of

22

-inch pipeline extending from Martinsville to Lima, Ohio. This system also includes associated breakout tankage. Crude oil delivered on this system to MPC’s tank farm in Lima can then be shipped to MPC’s Canton, Ohio refinery through MPC’s Lima to Canton pipeline, to MPC’s Detroit refinery through MPC’s undivided joint interest portion of the Maumee pipeline, and our Samaria to Detroit pipeline, or to other third-party refineries in Lima and Toledo, Ohio. This pipeline system has a capacity of

249

mbpd.

Catlettsburg and Robinson crude system

. Our Catlettsburg and Robinson crude system is comprised of the following pipelines:

|

•

|

Patoka to Robinson

. Our Patoka to Robinson pipeline consists of approximately

78 miles

of

20

-inch pipeline that delivers crude oil from Patoka, Illinois to MPC’s Robinson, Illinois refinery. This pipeline has a capacity of

225

mbpd.

|

8

|

•

|

Patoka to Catlettsburg

. Our Patoka to Catlettsburg pipeline consists of approximately

140 miles

of

20

-inch pipeline extending from Patoka, Illinois to Owensboro, Kentucky, and approximately

266 miles

of

24

-inch pipeline extending from Owensboro to MPC’s Catlettsburg refinery. Crude oil can enter this pipeline at Patoka, and into the Owensboro to Catlettsburg portion of the pipelines at Lebanon Junction, Kentucky, from the third-party Mid-Valley pipeline system. This pipeline has a capacity of

270

mbpd.

|

Detroit crude system

. Our Detroit crude system is comprised of the following pipelines:

|

•

|

Samaria to Detroit

. Our Samaria to Detroit pipeline consists of approximately

44 miles

of

16

-inch pipeline that delivers crude oil from Samaria, Michigan to MPC’s Detroit, Michigan refinery. This pipeline includes a tank farm and crude oil truck offloading facility located at Samaria. This pipeline has a capacity of

140

mbpd.

|

|

•

|

Romulus to Detroit

. Our Romulus to Detroit pipeline consists of approximately

17 miles

of

16

-inch pipeline extending from Romulus, Michigan to MPC’s Detroit refinery. We lease an existing 16-mile portion of this pipeline from a third party under a long-term lease that expires in 2019 and may be renewed for up to four additional five-year terms at our option. We constructed the remaining approximately one mile of this pipeline. This pipeline has a capacity of

180

mbpd and delivers crude oil received from pipeline systems operated by third parties at Romulus to MPC’s Detroit refinery.

|

Wood River to Patoka crude system

. Our Wood River to Patoka crude system is comprised of the following pipelines:

|

•

|

Wood River to Patoka

. Our Wood River to Patoka pipeline consists of approximately

57 miles

of

22

-inch pipeline that delivers crude oil received in Wood River, Illinois from the third-party Platte and Ozark pipeline systems to Patoka, Illinois. This pipeline has a capacity of

215

mbpd.

|

|

•

|

Roxanna to Patoka

. Our Roxanna to Patoka pipeline consists of approximately

58 miles

of

12

-inch pipeline that transports crude oil received in Roxanna, Illinois from the Ozark pipeline system to our tank farm in Patoka, Illinois. We lease this pipeline from a third party under a long-term lease that expires in 2020. This pipeline has a capacity of

99

mbpd.

|

9

Product Pipeline Systems

The following table sets forth certain information regarding our product pipeline systems, each of which has an associated transportation services agreement with MPC (other than our Louisville Airport products system, which currently transports only third-party volumes, and the inactive pipelines):

Product Pipeline Systems

|

System name

|

Diameter

(inches) |

Length

(miles) |

Capacity

(mbpd)

(1)

|

Associated MPC refineries

|

||||||

|

Garyville products system

|

||||||||||

|

Garyville, LA to Zachary, LA

|

20”

|

70

|

|

389

|

|

Garyville, LA

|

||||

|

Zachary, LA to connecting pipelines

(2)

|

36”

|

2

|

|

—

|

|

Garyville, LA

|

||||

|

Subtotal

|

72

|

|

389

|

|

||||||

|

Texas City products system

|

||||||||||

|

Texas City, TX to Pasadena, TX

|

16”

|

39

|

|

215

|

|

Texas City, TX; Galveston Bay, TX

|

||||

|

Pasadena, TX to connecting pipelines

(2)

|

36”/30”

|

3

|

|

—

|

|

Texas City, TX; Galveston Bay, TX

|

||||

|

Subtotal

|

42

|

|

215

|

|

||||||

|

ORPL products system

|

||||||||||

|

Kenova, WV to Columbus, OH

|

14”

|

150

|

|

68

|

|

Catlettsburg, KY

|

||||

|

Canton, OH to East Sparta, OH

(3,4)

|

6”

|

17

|

|

73

|

|

Canton, OH

|

||||

|

East Sparta, OH to Heath, OH

(4)

|

8”

|

81

|

|

29

|

|

Canton, OH

|

||||

|

East Sparta, OH to Midland, PA

(4)

|

8”

|

62

|

|

29

|

|

Canton, OH

|

||||

|

Heath, OH to Dayton, OH

|

6”

|

108

|

|

24

|

|

Catlettsburg, KY; Canton, OH

|

||||

|

Heath, OH to Findlay, OH

|

10”/8”

|

100

|

|

18

|

|

Catlettsburg, KY; Canton, OH

|

||||

|

Subtotal

|

518

|

|

241

|

|

||||||

|

Robinson products system

|

||||||||||

|

Robinson, IL to Lima, OH

|

10”

|

250

|

|

51

|

|

Robinson, IL

|

||||

|

Robinson, IL to Louisville, KY

|

16”

|

129

|

|

92

|

|

Robinson, IL

|

||||

|

Robinson, IL to Mt. Vernon, IN

(5)

|

10”

|

79

|

|

43

|

|

Robinson, IL

|

||||

|

Wood River, IL to Clermont, IN

|

10”

|

319

|

|

48

|

|

Robinson, IL

|

||||

|

Dieterich, IL to Martinsville, IL

|

10”

|

40

|

|

59

|

|

Robinson, IL

|

||||

|

Wabash Pipeline System:

|

||||||||||

|

West leg—Wood River, IL to Champaign, IL

|

12”

|

130

|

|

71

|

|

Robinson, IL

|

||||

|

East leg—Robinson, IL to Champaign, IL

|

12”

|

86

|

|

99

|

|

Robinson, IL

|

||||

|

Champaign, IL to Hammond, IN

|

16”/12”

|

140

|

|

85

|

|

Robinson, IL

|

||||

|

Subtotal

|

1,173

|

|

548

|

|

||||||

|

Louisville Airport products system

|

||||||||||

|

Louisville, KY to Louisville International Airport

|

8”/6”

|

14

|

|

29

|

|

Robinson, IL

|

||||

|

Inactive pipelines

(6)

|

83

|

|

n/a

|

|

||||||

|

Total product pipelines

|

1,902

|

|

1,422

|

|

||||||

|

(1)

|

Capacity shown is

100 percent

of the capacity of these pipeline systems. At December 31, 2013, we owned a

56.0 percent

indirect interest in these pipeline systems through Pipe Line Holdings.

|

|

(2)

|

Capacity not shown, as the pipeline is designed to meet outgoing capacity for connecting third-party pipelines.

|

10

|

(3)

|

Consists of two separate approximately

8.5

-mile pipelines.

|

|

(4)

|

This pipeline is bi-directional.

|

|

(5)

|

This pipeline is leased from a third party.

|

|

(6)

|

Includes

77

miles of pipeline leased from a third party.

|

Our product pipeline systems are strategically positioned to transport products from six of MPC’s refineries to MPC’s marketing operations, as well as those of third parties. These pipeline systems also supply feedstocks to MPC’s Midwest refineries. These product pipeline systems are integrated with MPC’s expansive network of refined product marketing terminals, which support MPC’s integrated midstream business.

The following are descriptions of our Gulf Coast product pipeline systems:

Garyville products system

. Our Garyville products system is comprised of approximately

70 miles

of 20-inch pipeline that delivers refined products from MPC’s Garyville, Louisiana refinery to either the Plantation Pipeline in Baton Rouge, Louisiana or the MPC Zachary breakout tank farm in Zachary, Louisiana, and approximately

two miles

of 36-inch pipeline that delivers refined products from the MPC tank farm to Colonial Pipeline in Zachary. This pipeline system is the Garyville refinery’s primary pathway for pipeline distribution of refined products, and has a capacity of

389

mbpd.

Texas City products system

. Our Texas City products system is comprised of approximately

39 miles

of 16-inch pipeline that delivers refined products from refineries owned by MPC and third parties in Texas City, Texas to MPC’s Pasadena tank farm and third-party terminals in Pasadena, Texas. The system also includes approximately

three miles

of 30- and 36-inch pipeline that delivers refined products from MPC’s Pasadena tank farm to the third-party Enterprise, Colonial and Centennial pipeline systems. This pipeline system has a capacity of

215

mbpd.

The following are descriptions of our Midwest product pipeline systems:

ORPL products system

. Our ORPL products system is comprised of the following pipelines:

|

•

|

Kenova to Columbus

. Our Kenova to Columbus pipeline consists of approximately

150 miles

of 14-inch pipeline that delivers refined products from MPC’s Catlettsburg refinery (through a MPC terminal in Kenova, West Virginia) to MPC’s Columbus, Ohio area terminals. In Columbus, products can be further distributed to Dayton and Heath, Ohio. This pipeline has a capacity of

68

mbpd.

|

|

•

|

Canton to East Sparta

. Our Canton to East Sparta pipeline consists of two parallel pipelines that connect MPC’s Canton refinery with our East Sparta, Ohio breakout tankage and station. The first pipeline consists of approximately

8.5 miles

of six-inch pipeline that delivers products (distillates) from Canton to East Sparta. The second pipeline consists of approximately

8.5 miles

of six-inch bi-directional pipeline that can deliver products (gasoline) from Canton to East Sparta or light petroleum-based feedstocks from East Sparta to Canton. The first pipeline has a capacity of

31

mbpd. The second pipeline has a capacity of

42

mbpd.

|

|

•

|

East Sparta to Heath

. Our East Sparta to Heath pipeline consists of approximately

81 miles

of eight-inch pipeline that delivers products from our East Sparta, Ohio breakout tankage and station to MPC’s terminal in Heath, Ohio, which has a marketing load rack and is able to connect to certain of our other pipelines to deliver products to destinations in Findlay and Columbus, Ohio. This pipeline is bi-directional giving it the capability to also move product from Heath to East Sparta. This pipeline has a capacity of

29

mbpd.

|

|

•

|

East Sparta to Midland

. Our East Sparta to Midland pipeline consists of approximately

62 miles

of eight-inch bi-directional pipeline that can deliver products and light petroleum-based feedstocks between our breakout tankage and station in East Sparta, Ohio and MPC’s terminal in Midland, Pennsylvania. MPC’s Midland terminal has a marketing load rack and is able to connect to other Pittsburgh, Pennsylvania-area terminals through a pipeline owned by a third party and a river loading/unloading dock for products and petroleum feedstocks. This pipeline can also transport products to MPC’s terminals in Steubenville and Youngstown, Ohio through a connection at West Point, Ohio with a pipeline owned by MPC. This pipeline has a capacity of

29

mbpd.

|

|

•

|

Heath to Dayton

. Our Heath to Dayton pipeline consists of approximately

108 miles

of six-inch pipeline that delivers products from MPC’s terminals in Heath and Columbus, Ohio to terminals owned by third parties in Dayton, Ohio. This pipeline is bi-directional between Heath and Columbus for product deliveries. The pipeline extending from Columbus to Dayton was reactivated in December 2011. This pipeline has a capacity of

24

mbpd.

|

|

•

|

Heath to Findlay

. Our Heath to Findlay pipeline consists of approximately

100 miles

of eight- and 10-inch pipeline that delivers products from MPC’s terminal in Heath, Ohio to MPC’s tankage in Findlay, Ohio. From Findlay, products can be further distributed to various Ohio, Michigan, and Indiana destinations through connections with a pipeline owned by third-party pipeline systems. This pipeline has a capacity of

18

mbpd.

|

11

Robinson products system

. Our Robinson products system is comprised of the following pipelines:

|

•

|

Robinson to Lima

. Our Robinson to Lima pipeline consists of approximately

250 miles

of 10-inch pipeline that delivers products from MPC’s Robinson refinery to various MPC terminals in Indianapolis, Indiana, as well as to MPC terminals in Muncie, Indiana and Lima, Ohio. This pipeline has a capacity of

51

mbpd.

|

|

•

|

Robinson to Louisville

. Our Robinson to Louisville pipeline consists of approximately

129 miles

of 16-inch pipeline that delivers products from MPC’s Robinson, Illinois refinery to two MPC and multiple third-party terminals in Louisville, Kentucky. At Louisville, MPC is able to further distribute these products to its river-sourced terminals through barge loading facilities at its Louisville terminal dock and its marine transportation assets. In addition, these products can supply MPC and third-party terminals in Lexington, Kentucky through the Louisville to Lexington pipeline system owned by MPC and a third party. The Robinson to Louisville pipeline has a capacity of

92

mbpd.

|

|

•

|

Robinson to Mt. Vernon

. Our Robinson to Mt. Vernon pipeline consists of approximately

79 miles

of 10-inch pipeline that delivers products from MPC’s Robinson refinery to a MPC terminal located on the Ohio River in Mt. Vernon, Indiana. MPC is able to further distribute these products to its river-sourced terminals through dock loading facilities at its Mt. Vernon terminal and its marine transportation assets. We lease this pipeline from a third party under a long-term lease that expires in 2020. The pipeline has a capacity of

43

mbpd.

|

|

•

|

Wood River to Clermont

. Our Wood River to Clermont pipeline consists of approximately

153 miles

of 10-inch pipeline extending from MPC’s terminal in Wood River, Illinois to Martinsville, Illinois, and approximately

156 miles

of 10-inch pipeline extending from Martinsville, Illinois to Clermont, Indiana. This pipeline also includes approximately 10 miles of pipelines utilized for the local movement of products in and around Wood River, Illinois, and Clermont, Indiana. This pipeline has connecting segments from Martinsville, Illinois to MPC’s Robinson refinery, which allows bi-directional movements. This pipeline has a capacity of

48

mbpd.

|

|

•

|

Dieterich to Martinsville

. Our Dieterich to Martinsville pipeline consists of approximately

40 miles

of 10-inch pipeline that delivers products from the operational termination point of Centennial Pipeline to Martinsville, Illinois. From Martinsville, these products (including refinery feedstocks) can be further distributed to MPC’s Robinson refinery or to other destinations through our other pipeline systems. This pipeline has a capacity of

59

mbpd.

|

|

•

|

Wabash Pipeline System

. Our Wabash Pipeline System consists of three interconnected pipelines: approximately

130 miles

of 12-inch pipeline extending from Wood River, Illinois to Champaign, Illinois (the “West leg”); approximately

86 miles

of 12-inch pipeline extending from MPC’s Robinson refinery to Champaign (the “East leg”); and approximately

140 miles

of 12- and 16-inch pipeline extending from the junction with the East and West legs in Champaign to MPC’s terminals in Griffith and Hammond, Indiana. This pipeline system delivers products to MPC’s tanks at Martinsville, Champaign, Griffith and Hammond. This pipeline system also delivers products to tanks owned by a third party at Ashkum, Illinois. The Wabash Pipeline System connects to other pipeline systems and terminals in the Chicago area through a portion of the system located beyond MPC’s Griffith terminal. Overall, the pipeline system is capable of receiving products from or delivering products to five separate third-party pipeline systems. The West leg has a capacity of

71

mbpd, the East leg has a capacity of

99

mbpd and the remaining pipeline segment has a capacity of

85

mbpd.

|

Louisville Airport products system

. Our Louisville airport products system consists of approximately

14 miles

of eight- and six-inch pipeline that delivers jet fuel from MPC’s Louisville, Kentucky refined product terminals to customers at the Louisville International Airport. This pipeline system currently transports only third-party volumes. This pipeline system has a capacity of

29

mbpd.

12

Other Midstream Assets

The following table sets forth certain information regarding our other midstream assets, each of which currently has an associated transportation services agreement or storage services agreement with MPC:

Other Midstream Assets

|

Asset name

|

Capacity

(1)

|

Associated MPC refineries

|

||

|

Wood River Barge Dock

|

84 mbpd

|

Garyville, LA

|

||

|

Neal Butane Cavern

|

1,000 mbbls

|

Catlettsburg, KY

|

||

|

Patoka Tank Farm

|

1,386 mbbls

|

All Midwest refineries

|

||

|

Wood River Tank Farm

|

419 mbbls

|

All Midwest refineries

|

||

|

Martinsville Tank Farm

|

738 mbbls

|

Detroit, MI; Canton, OH

|

||

|

Lebanon Tank Farm

|

750 mbbls

|

Detroit, MI; Canton, OH

|

||

|

(1)

|

All capacity shown is for

100 percent

of the available storage capacity of our butane cavern and tank farms in thousands of barrels (“mbbls”) and

100 percent

of the barge dock’s average capacity. At December 31, 2013, we owned a

56.0 percent

indirect interest in our tank farms and our barge dock through Pipe Line Holdings. We own a

100 percent

interest in our butane cavern.

|

Wood River Barge Dock

Our barge dock is located on the Mississippi River in Wood River, Illinois and is used both for crude oil barge loading and products barge unloading. The barge dock is connected to our Wood River tank farm by approximately

two miles

of 14-inch pipeline that transfers crude oil from the tank farm to the dock, and two 10-inch pipelines that are each approximately

two miles

long and that transfer products and feedstocks from the dock to the tank farm. This dock generates revenue through a FERC tariff that is collected for the transfer and loading/unloading of crude oil and products. While the capacity of our barge dock and related pipelines can vary by product and other operational factors, based on volumes handled at the facility for the year ended

December 31, 2013

, the capacity of our barge dock and related pipelines was

84 mbpd

.

Neal Butane Cavern

Our butane cavern is located in Neal, West Virginia, across the Big Sandy River from MPC’s Catlettsburg refinery. This storage cavern has approximately

1.0 million

barrels of storage capacity and is connected to MPC’s Catlettsburg refinery. Rail access to the storage cavern is also available through connections with the refinery.

Tank Farms

We also own tank farms located in Patoka, Martinsville and Wood River, Illinois and Lebanon, Indiana that we use for storing both crude oil and products. These storage assets are integral to the operation of our pipeline systems in those areas. We utilize the substantial majority of our capacity at these tank farms as breakout tankage for our crude oil and product pipeline systems. We provide an aggregate of approximately

3.3 million

barrels of available capacity to MPC on a firm basis under our storage services agreements for our tank farms.

13

Volumes Transported

The following table sets forth the average aggregate daily number of barrels of crude oil transported on our pipeline systems and at our barge dock for MPC and for third parties, in physical barrels, for each of the last three years:

Crude Oil Volumes Transported

|

2013

|

2012

|

2011

|

|||||||

|

Crude oil transported for (mbpd)

(1)

:

|

|||||||||

|

MPC

|

841

|

|

827

|

|

811

|

|

|||

|

Third parties

|

222

|

|

202

|

|

182

|

|

|||

|

Total

|

1,063

|

|

1,029

|

|

993

|

|

|||

|

% MPC

|

79

|

%

|

80

|

%

|

82

|

%

|

|||

|

(1)

|

Volumes shown are

100 percent

of the volumes transported on the pipeline systems and barge dock. At December 31, 2013, we owned a

56.0 percent

indirect interest in our pipeline systems and our barge dock through Pipe Line Holdings. Volumes shown for all periods exclude volumes transported on two undivided joint interest crude oil pipeline systems not contributed to MPLX LP at the Offering.

|

The following table sets forth the average aggregate daily number of barrels of products transported on our pipeline systems for MPC and third parties for each of the last three years:

Product Volumes Transported

|

2013

|

2012

|

2011

|

|||||||

|

Products transported for (mbpd)

(1)

:

|

|||||||||

|

MPC

(2)

|

876

|

|

909

|

|

971

|

|

|||

|

Third parties

|

35

|

|

71

|

|

60

|

|

|||

|

Total

|

911

|

|

980

|

|

1,031

|

|

|||

|

% MPC

(2)

|

96

|

%

|

93

|

%

|

94

|

%

|

|||

|

(1)

|

Volumes shown are

100 percent

of the volumes transported on the pipeline systems. At December 31, 2013, we owned a

56.0 percent

indirect interest in the pipeline systems through Pipe Line Holdings.

|

|

(2)

|

Includes volumes shipped by MPC on various pipelines under joint tariffs with third parties. For accounting purposes, revenue attributable to these volumes is classified as third-party revenue because we receive payment from those third parties with respect to volumes shipped under the joint tariffs; however, the volumes associated with this revenue are applied towards MPC’s minimum quarterly volume commitments on the applicable pipelines because MPC is the shipper of record.

|

For a discussion of the effects of seasonality on our business, please read Item 7. Management’s Discussion and Analysis of Financial Condition and Results of Operations – Factors That Impact Our Business – Seasonality, which is incorporated herein by reference.

OUR TRANSPORTATION AND STORAGE SERVICES AGREEMENTS WITH MPC

Our assets are strategically located within, and integral to, MPC’s operations. We have entered into multiple transportation and storage services agreements with MPC. Under these long-term, fee-based agreements, we provide transportation and storage services to MPC, and MPC has committed to provide us with minimum quarterly throughput and storage volumes of crude oil and products and minimum storage volumes of butane. All of our transportation services agreements for our crude oil and product pipeline systems (other than our Wood River to Patoka crude system) include a 10-year term and automatically renew for up to two additional five-year terms unless terminated by either party no later than six months prior to the end of the term. The transportation services agreements for our Wood River to Patoka crude system and our barge dock each include a five-year term and automatically renew for up to four additional two-year terms unless terminated by either party no later than six months prior to the end of the term. Our butane cavern storage services agreement includes a 10-year term but does not automatically renew. Our storage services agreements for our tank farms include a three-year term and automatically renew for additional one-year terms unless terminated by either party no later than six months prior to the end of the term.

14

The following table sets forth additional information regarding our transportation and storage services agreements:

Transportation and Storage Services Agreements

|

Agreement

|

Initial

term (years) |

Weighted

average

tariff/storage

fee ($ per bbl)

(1)

|

MPC minimum

commitment

(2)

|

|||||||

|

Transportation Services (mbpd)

|

||||||||||

|

Crude Systems

|

||||||||||

|

Patoka to Lima crude system

(3)

|

10

|

|

$

|

0.53

|

|

40

|

|

|||

|

Catlettsburg and Robinson crude system

|

10

|

|

0.72

|

|

380

|

|

||||

|

Detroit crude system

|

10

|

|

0.24

|

|

155

|

|

||||

|

Wood River to Patoka crude system

(3)

|

5

|

|

0.23

|

|

130

|

|

||||

|

Wood River Barge Dock

(3)(4)

|

5

|

|

1.33

|

|

40

|

|

||||

|

Total

|

745

|

|

||||||||

|

Products Systems

|

||||||||||

|

Garyville products system

|

10

|

|

||||||||

|

Garyville to Zachary

(5)

|

$

|

0.55

|

|

300

|

|

|||||

|

Zachary to connecting pipelines

|

0.05

|

|

80

|

|

||||||

|

Texas City products system

|

10

|

|

||||||||

|

Texas City to Pasadena

(5)

|

0.27

|

|

81

|

|

||||||

|

Pasadena to connecting pipelines

|

0.07

|

|

61

|

|

||||||

|

ORPL products system

|

10

|

|

1.21

|

|

129

|

|

||||

|

Robinson products system

(5)

|

10

|

|

0.68

|

|

209

|

|

||||

|

Total

|

860

|

|

||||||||

|

Storage Services (mbbls)

|

||||||||||

|

Neal Butane Cavern

|

10

|

|

$

|

1.25

|

|

1,000

|

|

|||

|

Patoka Tank Farm

|

3

|

|

0.48

|

|

1,386

|

|

||||

|

Wood River Tank Farm

|

3

|

|

0.48

|

|

419

|

|

||||

|

Martinsville Tank Farm

|

3

|

|

0.48

|

|

738

|

|

||||

|

Lebanon Tank Farm

|

3

|

|

0.48

|

|

750

|

|

||||

|

Total

|

4,293

|

|

||||||||

|

(1)

|

Based on actual volumes transported or stored for 2013 and applicable tariffs or fees during the period, including general tariff increases on the majority of our pipeline systems in July 2013. Weighted average tariffs shown for transportation services agreements are presented on a per-barrel of throughput basis. Storage fees for our butane cavern and tank farms are shown per barrel of capacity per month.

|

|

(2)

|

Quarterly commitment for our transportation services agreements in thousands of barrels per day and committed storage capacity for our storage services agreements in thousands of barrels. Volumes shown for crude oil transportation services agreements are adjusted for crude viscosities.

|

|

(3)

|

MPC’s minimum commitment represents the lesser of (1) a base commitment and (2) a lesser amount reflecting increased third-party utilization of the applicable asset.

|

|

(4)

|

Historically, we have shipped primarily crude oil volumes; however, our barge dock can handle products as well as crude oil.

|

|

(5)

|

Includes revenue from volumes shipped by MPC on various pipelines under joint tariffs with third parties. For accounting purposes, this revenue is classified as third-party revenue because we receive payment from those third parties with respect to volumes shipped under the joint tariffs; however, the volumes associated with this revenue are applied towards MPC’s minimum volume commitments on the applicable pipelines because MPC is the shipper of record.

|

15

Under our transportation services agreements, if MPC fails to transport its minimum throughput volumes during any quarter, then MPC will pay us a deficiency payment equal to the volume of the deficiency multiplied by the tariff rate then in effect (the “Quarterly Deficiency Payment”). Under each of our transportation services agreements, other than the agreements covering our Wood River to Patoka crude system and our barge dock, the amount of any Quarterly Deficiency Payment paid by MPC may be applied as a credit for any volumes transported on the applicable pipeline system in excess of MPC’s minimum volume commitment during any of the succeeding four quarters, or eight quarters for the transportation services agreements covering our Wood River to Patoka crude system and our barge dock, after which time any unused credits will expire. Upon the expiration or termination of a transportation services agreement, MPC will have the opportunity to apply any such remaining credit amounts until the completion of any such four-quarter or eight-quarter period, as applicable. Unlike during the term of the agreement, any such remaining credits may be used against any volumes shipped by MPC on the applicable pipeline system, without regard to any minimum volume commitment that may have been in place during the term of the agreement.

In order to enable MPC to transport its minimum throughput commitment each quarter, we are obligated to maintain the stated minimum capacity of the pipeline systems. If the minimum capacity of the pipeline falls below the level of MPC’s commitment at any time or if capacity on the pipeline is required to be allocated among shippers because volume nominations exceed available capacity, depending on the cause of the reduction in capacity, MPC’s commitment may be reduced or MPC will receive a credit for its minimum volume commitment for that period. Generally, under our transportation services agreements, we may elect to adjust our tariff rates annually. MPC has agreed not to directly or indirectly take any action that indicates a lack of support for our tariffs for the term of the agreement. In addition to MPC’s minimum volume commitment, MPC is also responsible for any loading, handling, transfer and other charges with respect to volumes we transport for MPC.

Under our transportation services agreements, if we agree to make any capital expenditures at MPC’s request, MPC will reimburse us for, or we will have the right in certain circumstances to file for an increased tariff rate to recover, the actual cost of such capital expenditures. In addition, if new laws or regulations that affect the services that we provide to MPC under these agreements are enacted or promulgated that require us to make substantial and unanticipated capital expenditures, MPC will reimburse us for, or we will have the right to file for an increased tariff rate to cover, MPC’s proportionate share of the costs of complying with these laws or regulations, after we have made efforts to mitigate their effect. We and MPC will negotiate in good faith to agree on the level of the increased tariff rate which shall be sufficient to allow us to recover the costs of the substantial and unanticipated capital expenditures consistent with FERC ratemaking methodology. MPC will also reimburse us for, or we will also have the right to file for an increased tariff rate to recover, the amounts of any taxes (other than income taxes, gross receipt taxes, ad valorem taxes, property taxes and similar taxes) that we incur on MPC’s behalf for the services we provide to MPC under these agreements to the extent permitted by law.

MPC’s obligations under these transportation and storage services agreements will not terminate if MPC no longer controls our general partner.

Our transportation services agreements include provisions that permit MPC to suspend, reduce or terminate its obligations under the applicable agreement if certain events occur. These events include MPC deciding to permanently or indefinitely suspend refining operations at one or more of its refineries for at least twelve consecutive months and certain force majeure events that would prevent us or MPC from performing required services under the applicable agreement. As defined in our transportation and storage services agreements, force majeure events include any acts or occurrences that prevent services from being performed under the applicable agreement, such as:

|

•

|

acts of God, fires, floods or storms;

|

|

•

|

compliance with orders of courts or any governmental authority;

|

|

•

|

explosions, wars, terrorist acts, riots, strikes, lockouts or other industrial disturbances;

|

|

•

|

accidental disruption of service;

|

|

•

|

breakdown of machinery, storage tanks or pipelines and inability to obtain or unavoidable delays in obtaining material or equipment to repair or replace those assets; and

|

|

•

|

similar events or circumstances, so long as such events or circumstances are beyond the party’s reasonable control and could not have been prevented by the service provider’s reasonable due diligence.

|

Under our crude oil transportation services agreements, if MPC experiences a force majeure at one of its refineries that reduces such refinery’s crude oil throughput capacity by at least 50.0 percent for 30 days or more, MPC’s minimum volume commitment under the associated agreement will be reduced by 50.0 percent until such time that capacity is restored at the refinery.

16

Under our storage services agreements, we are obligated to make available to MPC on a firm basis the available storage capacity at our tank farms and butane cavern, and MPC has agreed to pay us a per-barrel fee for such storage capacity, regardless of whether MPC fully utilizes the available capacity. If the available capacity of our storage assets is reduced as a result of testing, repair or maintenance activities, a force majeure event or in order to comply with applicable law, rule or regulation, then MPC is entitled to a proportionate reduction in the amounts payable by MPC under the applicable agreement. We may adjust the per-barrel fees in our storage services agreements based on changes in the Producer Price Index for Finished Goods (“PPI”) in early 2014.

Under our transportation and storage services agreements, each party has agreed to indemnify the other party from any losses or liabilities incurred as a result of, among other things, the indemnifying party’s breach of the applicable transportation and storage services agreement. Additionally, we have agreed to indemnify MPC from any losses or liabilities, including third-party claims, incurred by MPC as a result of our gross negligence, willful misconduct or bad faith in the performance of the applicable transportation and storage services agreement. MPC has agreed to indemnify us from any losses or liabilities incurred for any third-party claims except to the extent resulting from our gross negligence, willful misconduct or bad faith in the provision of services under the applicable transportation and storage services agreement. There is no limit on the amount of the indemnification obligations under the transportation and storage services agreements.

None of these agreements may be assigned by us or MPC without the other party’s prior written consent, except that we or MPC may assign an agreement without the other party’s prior written consent to a successor in interest resulting from any merger, reorganization, consolidation or as part of a sale of all or substantially all of the assigning party’s assets. Upon termination of a transportation services agreement, if not due to a default by MPC or initiated by MPC for reasons of force majeure or the suspension of a refinery’s operations, (i) MPC has the right to require us to enter into a new transportation services agreement on commercial terms that are equal or more favorable to us than terms that would be agreed to with a third party at arm’s length and, (ii) if we propose to enter into a transportation services agreement with a third party, we must provide MPC with a right of first offer to enter into a transportation services agreement with us on terms no less favorable than those offered by the third party, provided that in either case the term of any such new agreement will not extend beyond December 31, 2032 (except with respect to our Wood River barge dock and Wood River to Patoka crude system, the terms of which will not extend beyond December 31, 2017 and December 31, 2025, respectively).

The following sets forth additional information regarding each of our transportation and storage services agreements:

Crude Oil Pipeline Systems

|

•

|

Patoka to Lima Crude System.

Under our Patoka to Lima transportation services agreement, we charge MPC, at the applicable FERC tariff rates, for transporting crude oil from Patoka, Illinois and any new or existing connections, including any injection and truck unloading points, along our Patoka to Lima pipeline system. MPC is obligated to transport on this pipeline system each quarter an average of at least the lesser of: (1)

40

mbpd of light equivalent crude oil and (2) 290 mbpd of light equivalent crude oil minus all third-party shipments of light equivalent crude oil on the system, each quarter on this pipeline system. Under this agreement, we may file with the FERC to adjust our tariff rates annually at a rate equal to the percentage change in any inflationary index promulgated by the FERC, in accordance with the FERC’s indexing methodology. If the FERC terminates its indexing methodology and does not adopt a new methodology, the parties will negotiate in good faith any adjustment to the existing tariff rates. MPC historically has shipped volumes of crude oil on this pipeline system in excess of its minimum throughput commitment, and we expect those excess shipments to continue.

|

|

•

|

Catlettsburg and Robinson Crude System.

Under our Catlettsburg and Robinson transportation services agreement, we charge MPC, at the applicable FERC tariff rates, for transporting crude oil from:

|

|

•

|

Patoka, Illinois and any new or existing connections, including any injection and truck unloading points, along our Patoka to Robinson pipeline extending from Patoka, Illinois to MPC’s Robinson refinery; and

|

|

•

|

Patoka, Illinois and any new or existing connections, including any injection and truck unloading points, along our Patoka to Owensboro to Catlettsburg pipeline extending from Patoka to MPC’s Catlettsburg refinery.

|

MPC is obligated to transport each quarter an average of at least

380

mbpd of light equivalent crude oil from origin points at Patoka, Owensboro or other connections on this pipeline system to MPC’s Robinson or Catlettsburg refineries. Under this agreement, we may file with the FERC to adjust our tariff rates annually at a rate equal to the percentage change in any inflationary index promulgated by the FERC, in accordance with the FERC’s indexing methodology. If the FERC terminates its indexing methodology and does not adopt a new methodology, the parties will negotiate in good faith any adjustment to the existing tariff rates. MPC historically has shipped volumes of crude oil on this pipeline system in excess of its minimum quarterly throughput commitment, and we expect those excess shipments to continue.

17

|

•

|

Detroit Crude System.

Under our Detroit transportation services agreement, we charge MPC, at the applicable FERC tariff rates, for transporting crude oil from:

|

|

•

|

Samaria, Michigan and any new or existing connections, including any injection and truck unloading points, along our Samaria to Detroit pipeline extending from Samaria, Michigan to MPC’s Detroit refinery; and

|

|

•

|

Romulus, Michigan and any new or existing connections, including any injection and truck unloading points, along our Romulus to Detroit pipeline extending from Romulus, Michigan to MPC’s Detroit refinery.

|

MPC is obligated to transport each quarter an average of at least

155

mbpd of light equivalent crude oil from origin points at Samaria, Romulus or other connections on this pipeline system to MPC’s Detroit refinery. Under this agreement, we may file with the FERC to adjust our tariff rates annually at a rate equal to the percentage change in any inflationary index promulgated by the FERC, in accordance with the FERC’s indexing methodology. If the FERC terminates its indexing methodology and does not adopt a new methodology, the parties will negotiate in good faith any adjustment to the existing tariff rates.

|

•

|

Wood River to Patoka Crude System

. Under our Wood River to Patoka transportation services agreement, we charge MPC, at the applicable FERC tariff rates, for transporting crude oil from:

|

|

•

|

Wood River, Illinois and any new or existing connections, including any injection and truck unloading points, along our pipeline extending from Wood River to Patoka, Illinois; and

|

|

•

|

Roxanna, Illinois and any new or existing connections, including any injection and truck unloading points, along our pipeline extending from Roxanna, Illinois to Patoka.

|

MPC is obligated to transport on this pipeline system each quarter an average of at least the lesser of: (1)

130

mbpd of light equivalent crude oil and (2) 279 mbpd light equivalent crude oil minus all third-party shipments of light equivalent crude oil on the system. Under this agreement, we may file with the FERC to adjust our tariff rates annually at a rate equal to the percentage change in any inflationary index promulgated by the FERC, in accordance with the FERC’s indexing methodology. If the FERC terminates its indexing methodology and does not adopt a new methodology, the parties will negotiate in good faith any adjustment to the existing tariff rates.

Product Pipeline Systems

|

•

|

Garyville Products System

.

Under our Garyville transportation services agreement, we charge MPC, at the applicable FERC tariff rates, for transporting products from Garyville, Louisiana and any new or existing connections, including any injection and truck unloading points, on our Garyville pipeline system to Baton Rouge and Zachary, Louisiana. MPC is obligated to transport an average each quarter of at least

300

mbpd of products from MPC’s Garyville refinery to Baton Rouge or Zachary, and an average each quarter of at least

80