|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Table of Contents

UNITED STATES SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 10-Q

QUARTERLY REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934

For the quarterly period ended March 31, 2019

Commission File Number 1-11758

(Exact Name of Registrant as specified in its charter)

|

Delaware (State or other jurisdiction of incorporation or organization) |

1585 Broadway New York, NY 10036 (Address of principal executive offices, including zip code)

|

36-3145972 (I.R.S. Employer Identification No.) |

(212) 761-4000 (Registrant’s telephone number, including area code) |

|||

|

Securities registered pursuant to Section 12(b) of the Act: |

||||||

| Title of each class |

Name of exchange on

which registered |

Trading Symbol(s) |

||||

|

Common Stock, $0.01 par value |

New York Stock Exchange | MS | ||||

|

Depositary Shares, each representing 1/1,000th

interest in a share of Floating Rate

|

New York Stock Exchange | MS/PA | ||||

|

Depositary Shares, each representing 1/1,000th interest in a share of Fixed-to-Floating Rate Non-Cumulative Preferred Stock, Series E, $0.01 par value |

New York Stock Exchange | MS/PE | ||||

|

Depositary Shares, each representing 1/1,000th interest in a share of Fixed-to-Floating Rate Non-Cumulative Preferred Stock, Series F, $0.01 par value |

New York Stock Exchange | MS/PF | ||||

|

Depositary Shares, each representing 1/1,000th

interest in a share of 6.625%

|

New York Stock Exchange | MS/PG | ||||

|

Depositary Shares, each representing 1/1,000th interest in a share of Fixed-to-Floating Rate Non-Cumulative Preferred Stock, Series I, $0.01 par value |

New York Stock Exchange | MS/PI | ||||

|

Depositary Shares, each representing 1/1,000th interest in a share of Fixed-to-Floating Rate Non-Cumulative Preferred Stock, Series K, $0.01 par value |

New York Stock Exchange | MS/PK | ||||

|

Global Medium-Term Notes, Series A, Fixed Rate

Step-Up

Senior Notes Due 2026 of

|

New York Stock Exchange | MS/26C | ||||

|

Market Vectors ETNs due March 31, 2020 (two issuances) |

NYSE Arca, Inc. | URR/DDR | ||||

|

Market Vectors ETNs due April 30, 2020 (two issuances) |

NYSE Arca, Inc. | CNY/INR | ||||

|

Morgan Stanley Cushing ® MLP High Income Index ETNs due March 21, 2031 |

NYSE Arca, Inc. | MLPY | ||||

Indicate by check mark whether the Registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the Registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes ☒ No ☐

Indicate by check mark whether the Registrant has submitted electronically every Interactive Data File required to be submitted pursuant to Rule 405 of Regulation S-T (§ 232.405 of this chapter) during the preceding 12 months (or for such shorter period that the Registrant was required to submit such files). Yes ☒ No ☐

Indicate by check mark whether the Registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, smaller reporting company, or an emerging growth company. See the definitions of “large accelerated filer,” “accelerated filer,” “smaller reporting company,” and “emerging growth company” in Rule 12b-2 of the Exchange Act. (Check one):

| Large Accelerated Filer ☒ |

Accelerated Filer ☐ |

Non-Accelerated Filer ☐ |

Smaller reporting company ☐ |

Emerging growth company ☐ |

If an emerging growth company, indicate by check mark if the Registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided pursuant to Section 13(a) of the Exchange Act. ☐

Indicate by check mark whether the Registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act). Yes ☐ No ☒

As of April 30, 2019, there were 1,682,234,555 shares of the Registrant’s Common Stock, par value $0.01 per share, outstanding.

Table of Contents

For the quarter ended March 31, 2019

| Table of Contents | Part | Item | Page | |||||||||||

| I | 1 | |||||||||||||

|

Management’s Discussion and Analysis of Financial Condition and Results of Operations |

I | 2 | 1 | |||||||||||

| 1 | ||||||||||||||

| 2 | ||||||||||||||

| 6 | ||||||||||||||

| 13 | ||||||||||||||

| 13 | ||||||||||||||

| 14 | ||||||||||||||

| 14 | ||||||||||||||

| 14 | ||||||||||||||

| 19 | ||||||||||||||

| I | 3 | 24 | ||||||||||||

| 24 | ||||||||||||||

| 26 | ||||||||||||||

| 30 | ||||||||||||||

| 33 | ||||||||||||||

| I | 1 | 34 | ||||||||||||

| 34 | ||||||||||||||

| 35 | ||||||||||||||

| 36 | ||||||||||||||

|

Consolidated Statements of Changes in Total Equity (Unaudited) |

37 | |||||||||||||

| 38 | ||||||||||||||

| 39 | ||||||||||||||

| 39 | ||||||||||||||

| 40 | ||||||||||||||

| 40 | ||||||||||||||

| 48 | ||||||||||||||

| 51 | ||||||||||||||

| 54 | ||||||||||||||

| 55 | ||||||||||||||

| 57 | ||||||||||||||

| 58 | ||||||||||||||

| 58 | ||||||||||||||

| 58 | ||||||||||||||

| 63 | ||||||||||||||

| 65 | ||||||||||||||

| 67 | ||||||||||||||

| 69 | ||||||||||||||

| 69 | ||||||||||||||

| 69 | ||||||||||||||

| 70 | ||||||||||||||

| 71 | ||||||||||||||

| 72 | ||||||||||||||

| 73 | ||||||||||||||

| II | 75 | |||||||||||||

| II | 1 | 75 | ||||||||||||

| II | 2 | 76 | ||||||||||||

| I | 4 | 77 | ||||||||||||

| II | 6 | 77 | ||||||||||||

| E-1 | ||||||||||||||

| S-1 | ||||||||||||||

i

Table of Contents

Available Information

We file annual, quarterly and current reports, proxy statements and other information with the SEC. The SEC maintains an internet site, www.sec.gov , that contains annual, quarterly and current reports, proxy and information statements and other information that issuers file electronically with the SEC. Our electronic SEC filings are available to the public at the SEC’s internet site.

Our internet site is www.morganstanley.com . You can access our Investor Relations webpage at www.morganstanley.com/about-us-ir . We make available free of charge, on or through our Investor Relations webpage, our Proxy Statements, Annual Reports on Form 10-K, Quarterly Reports on Form 10-Q, Current Reports on Form 8-K and any amendments to those reports filed or furnished pursuant to the Securities Exchange Act of 1934, as amended (“Exchange Act”), as soon as reasonably practicable after such material is electronically filed with, or furnished to, the SEC. We also make available, through our Investor Relations webpage, via a link to the SEC’s internet site, statements of beneficial ownership of our equity securities filed by our directors, officers, 10% or greater shareholders and others under Section 16 of the Exchange Act.

You can access information about our corporate governance at www.morganstanley.com/about-us-governance. Our Corporate Gover-nance webpage includes:

| • |

Amended and Restated Certificate of Incorporation; |

| • |

Amended and Restated Bylaws; |

| • |

Charters for our Audit Committee, Compensation, Management Development and Succession Committee, Nominating and Governance Committee, Operations and Technology Committee, and Risk Committee; |

| • |

Corporate Governance Policies; |

| • |

Policy Regarding Corporate Political Activities; |

| • |

Policy Regarding Shareholder Rights Plan; |

| • |

Equity Ownership Commitment; |

| • |

Code of Ethics and Business Conduct; |

| • |

Code of Conduct; |

| • |

Integrity Hotline Information; and |

| • |

Environmental and Social Policies. |

Our Code of Ethics and Business Conduct applies to all directors, officers and employees, including our Chief Executive Officer, Chief Financial Officer and Deputy Chief Financial Officer. We will post any amendments to the Code of Ethics and Business Conduct and any waivers that are required to be disclosed by the rules of either the SEC or the New York Stock Exchange LLC (“NYSE”) on our internet site. You can request a copy of these documents, excluding exhibits, at no cost, by contacting Investor Relations, 1585 Broadway, New York, NY 10036 (212-761-4000). The information on our internet site is not incorporated by reference into this report.

ii

Table of Contents

Table of Contents

Management’s Discussion and Analysis

| March 2019 Form 10-Q | 2 |

Table of Contents

Management’s Discussion and Analysis

| 3 | March 2019 Form 10-Q |

Table of Contents

Management’s Discussion and Analysis

| March 2019 Form 10-Q | 4 |

Table of Contents

Management’s Discussion and Analysis

| 5 | March 2019 Form 10-Q |

Table of Contents

Management’s Discussion and Analysis

| March 2019 Form 10-Q | 6 |

Table of Contents

Management’s Discussion and Analysis

| 7 | March 2019 Form 10-Q |

Table of Contents

Management’s Discussion and Analysis

| March 2019 Form 10-Q | 8 |

Table of Contents

Management’s Discussion and Analysis

| 9 | March 2019 Form 10-Q |

Table of Contents

Management’s Discussion and Analysis

Wealth Management

| March 2019 Form 10-Q | 10 |

Table of Contents

Management’s Discussion and Analysis

| 11 | March 2019 Form 10-Q |

Table of Contents

Management’s Discussion and Analysis

| March 2019 Form 10-Q | 12 |

Table of Contents

Management’s Discussion and Analysis

| 13 | March 2019 Form 10-Q |

Table of Contents

Management’s Discussion and Analysis

| March 2019 Form 10-Q | 14 |

Table of Contents

Management’s Discussion and Analysis

| 15 | March 2019 Form 10-Q |

Table of Contents

Management’s Discussion and Analysis

| March 2019 Form 10-Q | 16 |

Table of Contents

Management’s Discussion and Analysis

| 17 | March 2019 Form 10-Q |

Table of Contents

Management’s Discussion and Analysis

| March 2019 Form 10-Q | 18 |

Table of Contents

Management’s Discussion and Analysis

| 19 | March 2019 Form 10-Q |

Table of Contents

Management’s Discussion and Analysis

| March 2019 Form 10-Q | 20 |

Table of Contents

Management’s Discussion and Analysis

| 21 | March 2019 Form 10-Q |

Table of Contents

Management’s Discussion and Analysis

| March 2019 Form 10-Q | 22 |

Table of Contents

Management’s Discussion and Analysis

| 23 | March 2019 Form 10-Q |

Table of Contents

Table of Contents

Risk Disclosures

| 25 | March 2019 Form 10-Q |

Table of Contents

Risk Disclosures

| March 2019 Form 10-Q | 26 |

Table of Contents

Risk Disclosures

| 27 | March 2019 Form 10-Q |

Table of Contents

Risk Disclosures

| March 2019 Form 10-Q | 28 |

Table of Contents

Risk Disclosures

| 29 | March 2019 Form 10-Q |

Table of Contents

Risk Disclosures

| March 2019 Form 10-Q | 30 |

Table of Contents

Risk Disclosures

| 31 | March 2019 Form 10-Q |

Table of Contents

Risk Disclosures

| March 2019 Form 10-Q | 32 |

Table of Contents

Table of Contents

|

Consolidated Income Statements (Unaudited) |

|

|

Three Months Ended

March 31, |

||||||||

| in millions, except per share data | 2019 | 2018 | ||||||

|

Revenues |

||||||||

|

Investment banking |

$ | 1,242 | $ | 1,634 | ||||

|

Trading |

3,441 | 3,770 | ||||||

|

Investments |

273 | 126 | ||||||

|

Commissions and fees |

966 | 1,173 | ||||||

|

Asset management |

3,049 | 3,192 | ||||||

|

Other |

301 | 207 | ||||||

|

Total non-interest revenues |

9,272 | 10,102 | ||||||

|

Interest income |

4,290 | 2,860 | ||||||

|

Interest expense |

3,276 | 1,885 | ||||||

|

Net interest |

1,014 | 975 | ||||||

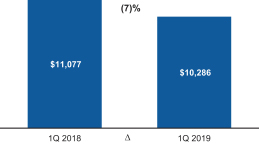

|

Net revenues |

10,286 | 11,077 | ||||||

|

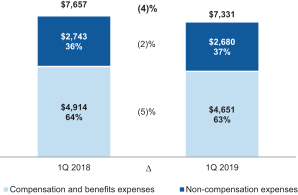

Non-interest expenses |

||||||||

|

Compensation and benefits |

4,651 | 4,914 | ||||||

|

Occupancy and equipment |

347 | 336 | ||||||

|

Brokerage, clearing and exchange fees |

593 | 627 | ||||||

|

Information processing and communications |

532 | 478 | ||||||

|

Marketing and business development |

141 | 140 | ||||||

|

Professional services |

514 | 510 | ||||||

|

Other |

553 | 652 | ||||||

|

Total non-interest expenses |

7,331 | 7,657 | ||||||

|

Income from continuing operations before income taxes |

2,955 | 3,420 | ||||||

|

Provision for income taxes |

487 | 714 | ||||||

|

Income from continuing operations |

2,468 | 2,706 | ||||||

|

Income (loss) from discontinued operations, net of income taxes |

— | (2 | ) | |||||

|

Net income |

$ | 2,468 | $ | 2,704 | ||||

|

Net income applicable to noncontrolling interests |

39 | 36 | ||||||

|

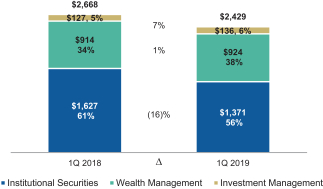

Net income applicable to Morgan Stanley |

$ | 2,429 | $ | 2,668 | ||||

|

Preferred stock dividends and other |

93 | 93 | ||||||

|

Earnings applicable to Morgan Stanley common shareholders |

$ | 2,336 | $ | 2,575 | ||||

|

Earnings per common share |

||||||||

|

Basic |

$ | 1.41 | $ | 1.48 | ||||

|

Diluted |

$ | 1.39 | $ | 1.45 | ||||

|

Average common shares outstanding |

||||||||

|

Basic |

1,658 | 1,740 | ||||||

|

Diluted |

1,677 | 1,771 | ||||||

| March 2019 Form 10-Q | 34 | See Notes to Consolidated Financial Statements |

Table of Contents

|

Consolidated Comprehensive Income Statements (Unaudited) |

|

|

Three Months Ended March 31, |

||||||||

| $ in millions | 2019 | 2018 | ||||||

|

Net income |

$ | 2,468 | $ | 2,704 | ||||

|

Other comprehensive income (loss), net of tax: |

||||||||

|

Foreign currency translation adjustments |

$ | (22 | ) | $ | 117 | |||

|

Change in net unrealized gains (losses) on available-for-sale securities |

429 | (410 | ) | |||||

|

Pension, postretirement and other |

1 | 5 | ||||||

|

Change in net debt valuation adjustment |

(620 | ) | 451 | |||||

|

Total other comprehensive income (loss) |

$ | (212 | ) | $ | 163 | |||

|

Comprehensive income |

$ | 2,256 | $ | 2,867 | ||||

|

Net income applicable to noncontrolling interests |

39 | 36 | ||||||

|

Other comprehensive income (loss) applicable to noncontrolling interests |

(31 | ) | 72 | |||||

|

Comprehensive income applicable to Morgan Stanley |

$ | 2,248 | $ | 2,759 | ||||

| See Notes to Consolidated Financial Statements | 35 | March 2019 Form 10-Q |

Table of Contents

|

$ in millions, except share data |

(Unaudited)

At March 31, 2019 |

At

December 31, 2018 |

||||||

|

Assets |

||||||||

|

Cash and cash equivalents: |

||||||||

|

Cash and due from banks |

$ | 35,472 | $ | 30,541 | ||||

|

Interest bearing deposits with banks |

14,498 | 21,299 | ||||||

|

Restricted cash |

30,712 | 35,356 | ||||||

|

Trading assets at fair value ( $103,750 and $120,437 were pledged to various parties) |

264,818 | 266,299 | ||||||

|

Investment securities (includes $61,641 and $61,061 at fair value) |

97,944 | 91,832 | ||||||

|

Securities purchased under agreements to resell (includes $5 and $ — at fair value) |

96,570 | 98,522 | ||||||

|

Securities borrowed |

138,891 | 116,313 | ||||||

|

Customer and other receivables |

52,667 | 53,298 | ||||||

|

Loans: |

||||||||

|

Held for investment (net of allowance of $259 and $238) |

101,266 | 99,815 | ||||||

|

Held for sale |

14,931 | 15,764 | ||||||

|

Goodwill |

6,686 | 6,688 | ||||||

|

Intangible assets (net of accumulated amortization of $2,952 and $2,877) |

2,084 | 2,163 | ||||||

|

Other assets |

19,425 | 15,641 | ||||||

|

Total assets |

$ | 875,964 | $ | 853,531 | ||||

|

Liabilities |

||||||||

|

Deposits (includes $692 and $442 at fair value) |

$ | 179,731 | $ | 187,820 | ||||

|

Trading liabilities at fair value |

144,565 | 126,747 | ||||||

|

Securities sold under agreements to repurchase (includes $622 and $812 at fair value) |

47,948 | 49,759 | ||||||

|

Securities loaned |

12,508 | 11,908 | ||||||

|

Other secured financings (includes $4,283 and $5,245 at fair value) |

8,043 | 9,466 | ||||||

|

Customer and other payables |

193,092 | 179,559 | ||||||

|

Other liabilities and accrued expenses |

17,494 | 17,204 | ||||||

|

Borrowings (includes $56,464 and $51,184 at fair value) |

190,691 | 189,662 | ||||||

|

Total liabilities |

794,072 | 772,125 | ||||||

|

Commitments and contingent liabilities (see Note 11) |

||||||||

|

Equity |

||||||||

|

Morgan Stanley shareholders’ equity: |

||||||||

|

Preferred stock |

8,520 | 8,520 | ||||||

|

Common stock, $0.01 par value: |

||||||||

|

Shares authorized: 3,500,000,000 ; Shares issued: 2,038,893,979 ; Shares outstanding: 1,685,996,391 and 1,699,828,943 |

20 | 20 | ||||||

|

Additional paid-in capital |

23,178 | 23,794 | ||||||

|

Retained earnings |

66,061 | 64,175 | ||||||

|

Employee stock trusts |

3,000 | 2,836 | ||||||

|

Accumulated other comprehensive income (loss) |

(2,473 | ) | (2,292 | ) | ||||

|

Common stock held in treasury at cost, $0.01 par value ( 352,897,588 and 339,065,036 shares) |

(14,582 | ) | (13,971 | ) | ||||

|

Common stock issued to employee stock trusts |

(3,000 | ) | (2,836 | ) | ||||

|

Total Morgan Stanley shareholders’ equity |

80,724 | 80,246 | ||||||

|

Noncontrolling interests |

1,168 | 1,160 | ||||||

|

Total equity |

81,892 | 81,406 | ||||||

|

Total liabilities and equity |

$ | 875,964 | $ | 853,531 | ||||

| March 2019 Form 10-Q | 36 | See Notes to Consolidated Financial Statements |

Table of Contents

|

Consolidated Statements of Changes in Total Equity (Unaudited) |

|

| $ in millions |

Preferred

Stock |

Common

Stock |

Additional

Paid-in Capital |

Retained

Earnings |

Employee

Stock Trusts |

Accumulated

Other Comprehensive Income (Loss) |

Common

Stock Held in Treasury at Cost |

Common

Stock Issued to Employee Stock Trusts |

Non-

controlling Interests |

Total

Equity |

||||||||||||||||||||||||||||||

|

Balance at December 31, 2018 |

$ | 8,520 | $ | 20 | $ | 23,794 | $ | 64,175 | $ | 2,836 | $ | (2,292 | ) | $ | (13,971 | ) | $ | (2,836 | ) | $ | 1,160 | $ | 81,406 | |||||||||||||||||

|

Cumulative adjustments for accounting changes 1 |

— | — | — | 63 | — | — | — | — | — | 63 | ||||||||||||||||||||||||||||||

|

Net income applicable to Morgan Stanley |

— | — | — | 2,429 | — | — | — | — | — | 2,429 | ||||||||||||||||||||||||||||||

|

Net income applicable to noncontrolling interests |

— | — | — | — | — | — | — | — | 39 | 39 | ||||||||||||||||||||||||||||||

|

Preferred stock dividends 2 |

— | — | — | (93 | ) | — | — | — | — | — | (93 | ) | ||||||||||||||||||||||||||||

|

Common stock dividends ($0.30 per share) |

— | — | — | (513 | ) | — | — | — | — | — | (513 | ) | ||||||||||||||||||||||||||||

|

Shares issued under employee plans |

— | — | (618 | ) | — | 164 | — | 1,034 | (164 | ) | — | 416 | ||||||||||||||||||||||||||||

|

Repurchases of common stock and employee tax withholdings |

— | — | — | — | — | — | (1,645 | ) | — | — | (1,645 | ) | ||||||||||||||||||||||||||||

|

Net change in Accumulated other comprehensive income (loss) |

— | — | — | — | — | (181 | ) | — | — | (31 | ) | (212 | ) | |||||||||||||||||||||||||||

|

Other net increases |

— | — | 2 | — | — | — | — | — | — | 2 | ||||||||||||||||||||||||||||||

|

Balance at March 31, 2019 |

$ | 8,520 | $ | 20 | $ | 23,178 | $ | 66,061 | $ | 3,000 | $ | (2,473 | ) | $ | (14,582 | ) | $ | (3,000 | ) | $ | 1,168 | $ | 81,892 | |||||||||||||||||

|

Balance at December 31, 2017 |

$ | 8,520 | $ | 20 | $ | 23,545 | $ | 57,577 | $ | 2,907 | $ | (3,060 | ) | $ | (9,211 | ) | $ | (2,907 | ) | $ | 1,075 | $ | 78,466 | |||||||||||||||||

|

Cumulative adjustments for accounting changes 1 |

— | — | — | 306 | — | (437 | ) | — | — | — | (131 | ) | ||||||||||||||||||||||||||||

|

Net income applicable to Morgan Stanley |

— | — | — | 2,668 | — | — | — | — | — | 2,668 | ||||||||||||||||||||||||||||||

|

Net income applicable to noncontrolling interests |

— | — | — | — | — | — | — | — | 36 | 36 | ||||||||||||||||||||||||||||||

|

Preferred stock dividends 2 |

— | — | — | (93 | ) | — | — | — | — | — | (93 | ) | ||||||||||||||||||||||||||||

|

Common stock dividends ($0.25 per share) |

— | — | — | (449 | ) | — | — | — | — | — | (449 | ) | ||||||||||||||||||||||||||||

|

Shares issued under employee plans |

— | — | (285 | ) | — | — | — | 710 | — | — | 425 | |||||||||||||||||||||||||||||

|

Repurchases of common stock and employee tax withholdings |

— | — | — | — | — | — | (1,868 | ) | — | — | (1,868 | ) | ||||||||||||||||||||||||||||

|

Net change in Accumulated other comprehensive income (loss) |

— | — | — | — | — | 91 | — | — | 72 | 163 | ||||||||||||||||||||||||||||||

|

Other net increases |

— | — | — | — | — | — | — | — | 272 | 272 | ||||||||||||||||||||||||||||||

|

Balance at March 31, 2018 |

$ | 8,520 | $ | 20 | $ | 23,260 | $ | 60,009 | $ | 2,907 | $ | (3,406 | ) | $ | (10,369 | ) | $ | (2,907 | ) | $ | 1,455 | $ | 79,489 | |||||||||||||||||

| 1. |

Cumulative adjustments for accounting changes relate to the adoption of certain accounting updates during the current and prior year quarters. See Notes 2 and 14 for further information. |

| 2. |

See Note 14 for information regarding dividends per share for each class of preferred stock. |

| See Notes to Consolidated Financial Statements | 37 | March 2019 Form 10-Q |

Table of Contents

Consolidated Cash Flow Statements

(Unaudited)

|

Three Months Ended

March 31, |

||||||||

| $ in millions | 2019 | 2018 | ||||||

|

Cash flows from operating activities |

||||||||

|

Net income |

$ | 2,468 | $ | 2,704 | ||||

|

Adjustments to reconcile net income to net cash provided by (used for) operating activities: |

||||||||

|

Stock-based compensation expense |

293 | 321 | ||||||

|

Depreciation and amortization |

658 | 390 | ||||||

|

Provision for credit losses on lending activities |

36 | 26 | ||||||

|

Other operating adjustments |

(92 | ) | (37 | ) | ||||

|

Changes in assets and liabilities: |

||||||||

|

Trading assets, net of Trading liabilities |

23,977 | 33,832 | ||||||

|

Securities borrowed |

(22,578 | ) | (11,825 | ) | ||||

|

Securities loaned |

600 | (36 | ) | |||||

|

Customer and other receivables and other assets |

1,567 | (13,019 | ) | |||||

|

Customer and other payables and other liabilities |

9,971 | 1,129 | ||||||

|

Securities purchased under agreements to resell |

1,952 | 4,012 | ||||||

|

Securities sold under agreements to repurchase |

(1,811 | ) | (4,849 | ) | ||||

|

Net cash provided by (used for) operating activities |

17,041 | 12,648 | ||||||

|

Cash flows from investing activities |

||||||||

|

Proceeds from (payments for): |

||||||||

|

Other assets—Premises, equipment and software, net |

(529 | ) | (410 | ) | ||||

|

Changes in loans, net |

(1,329 | ) | (3,801 | ) | ||||

|

Investment securities: |

||||||||

|

Purchases |

(15,895 | ) | (5,482 | ) | ||||

|

Proceeds from sales |

7,875 | 810 | ||||||

|

Proceeds from paydowns and maturities |

2,663 | 2,125 | ||||||

|

Other investing activities |

(12 | ) | (164 | ) | ||||

|

Net cash provided by (used for) investing activities |

(7,227 | ) | (6,922 | ) | ||||

|

Cash flows from financing activities |

||||||||

|

Net proceeds from (payments for): |

||||||||

|

Other secured financings |

(1,575 | ) | (2,101 | ) | ||||

|

Deposits |

(8,089 | ) | 988 | |||||

|

Proceeds from: |

||||||||

|

Issuance of Borrowings |

8,091 | 15,370 | ||||||

|

Payments for: |

||||||||

|

Borrowings |

(11,927 | ) | (11,377 | ) | ||||

|

Repurchases of common stock and employee tax withholdings |

(1,645 | ) | (1,868 | ) | ||||

|

Cash dividends |

(663 | ) | (599 | ) | ||||

|

Other financing activities |

(56 | ) | (50 | ) | ||||

|

Net cash provided by (used for) financing activities |

(15,864 | ) | 363 | |||||

|

Effect of exchange rate changes on cash and cash equivalents |

(464 | ) | 860 | |||||

|

Net increase (decrease) in cash and cash equivalents |

(6,514 | ) | 6,949 | |||||

|

Cash and cash equivalents, at beginning of period |

87,196 | 80,395 | ||||||

|

Cash and cash equivalents, at end of period |

$ | 80,682 | $ | 87,344 | ||||

|

Cash and cash equivalents: |

||||||||

|

Cash and due from banks |

$ | 35,472 | $ | 29,073 | ||||

|

Interest bearing deposits with banks |

14,498 | 22,980 | ||||||

|

Restricted cash |

30,712 | 35,291 | ||||||

|

Cash and cash equivalents, at end of period |

$ | 80,682 | $87,344 | |||||

|

Supplemental Disclosure of Cash Flow Information |

||||||||

|

Cash payments for: |

||||||||

|

Interest |

$ | 2,896 | $ | 1,407 | ||||

|

Income taxes, net of refunds |

245 | 250 | ||||||

| March 2019 Form 10-Q | 38 | See Notes to Consolidated Financial Statements |

Table of Contents

Table of Contents

Notes to Consolidated Financial Statements

(Unaudited)

| March 2019 Form 10-Q | 40 |

Table of Contents

Notes to Consolidated Financial Statements

(Unaudited)

| 41 | March 2019 Form 10-Q |

Table of Contents

Notes to Consolidated Financial Statements

(Unaudited)

| March 2019 Form 10-Q | 42 |

Table of Contents

Notes to Consolidated Financial Statements

(Unaudited)

| 43 | March 2019 Form 10-Q |

Table of Contents

Notes to Consolidated Financial Statements

(Unaudited)

| March 2019 Form 10-Q | 44 |

Table of Contents

Notes to Consolidated Financial Statements

(Unaudited)

| 45 | March 2019 Form 10-Q |

Table of Contents

Notes to Consolidated Financial Statements

(Unaudited)

| March 2019 Form 10-Q | 46 |

Table of Contents

Notes to Consolidated Financial Statements

(Unaudited)

| 47 | March 2019 Form 10-Q |

Table of Contents

Notes to Consolidated Financial Statements

(Unaudited)

| March 2019 Form 10-Q | 48 |

Table of Contents

Notes to Consolidated Financial Statements

(Unaudited)

| 49 | March 2019 Form 10-Q |

Table of Contents

Notes to Consolidated Financial Statements

(Unaudited)

| March 2019 Form 10-Q | 50 |

Table of Contents

Notes to Consolidated Financial Statements

(Unaudited)

| 51 | March 2019 Form 10-Q |

Table of Contents

Notes to Consolidated Financial Statements

(Unaudited)

Investment Securities in an Unrealized Loss Position

| At March 31, 2019 | ||||||||||||||||||||||||||||||||

| Less than 12 Months | 12 Months or Longer | Total | ||||||||||||||||||||||||||||||

| $ in millions | Fair Value |

Gross

Unrealized Losses |

Fair Value |

Gross

Unrealized Losses |

Fair Value |

Gross

Unrealized Losses |

||||||||||||||||||||||||||

|

AFS securities |

||||||||||||||||||||||||||||||||

|

U.S. government and agency securities: |

||||||||||||||||||||||||||||||||

|

U.S. Treasury securities |

$ | 124 | $ | — | $ | 22,670 | $ | 448 | $ | 22,794 | $ | 448 | ||||||||||||||||||||

|

U.S. agency securities |

3,641 | 29 | 13,307 | 289 | 16,948 | 318 | ||||||||||||||||||||||||||

|

Total U.S. government and agency securities |

3,765 | 29 | 35,977 | 737 | 39,742 | 766 | ||||||||||||||||||||||||||

|

Corporate and other debt: |

||||||||||||||||||||||||||||||||

|

Agency CMBS |

64 | — | 802 | 54 | 866 | 54 | ||||||||||||||||||||||||||

|

Non-agency CMBS |

— | — | 336 | 7 | 336 | 7 | ||||||||||||||||||||||||||

|

Corporate bonds |

276 | 1 | 818 | 9 | 1,094 | 10 | ||||||||||||||||||||||||||

|

FFELP student loan ABS |

615 | 5 | 702 | 11 | 1,317 | 16 | ||||||||||||||||||||||||||

|

Total corporate and other debt |

955 | 6 | 2,658 | 81 | 3,613 | 87 | ||||||||||||||||||||||||||

|

Total AFS securities |

4,720 | 35 | 38,635 | 818 | 43,355 | 853 | ||||||||||||||||||||||||||

|

HTM securities |

||||||||||||||||||||||||||||||||

|

U.S. government and agency securities: |

||||||||||||||||||||||||||||||||

|

U.S. Treasury securities |

99 | — | 9,495 | 251 | 9,594 | 251 | ||||||||||||||||||||||||||

|

U.S. agency securities |

303 | 2 | 9,505 | 250 | 9,808 | 252 | ||||||||||||||||||||||||||

|

Total U.S. government and agency securities |

402 | 2 | 19,000 | 501 | 19,402 | 503 | ||||||||||||||||||||||||||

|

Corporate and other debt: |

||||||||||||||||||||||||||||||||

|

Non-agency CMBS |

66 | 1 | 110 | — | 176 | 1 | ||||||||||||||||||||||||||

|

Total HTM securities |

468 | 3 | 19,110 | 501 | 19,578 | 504 | ||||||||||||||||||||||||||

|

Total investment securities |

$ | 5,188 | $ | 38 | $ | 57,745 | $ | 1,319 | $ | 62,933 | $ | 1,357 | ||||||||||||||||||||

| At December 31, 2018 | ||||||||||||||||||||||||||||||||

| Less than 12 Months | 12 Months or Longer | Total | ||||||||||||||||||||||||||||||

| $ in millions | Fair Value |

Gross

Unrealized Losses |

Fair Value |

Gross

Unrealized Losses |

Fair Value |

Gross

Unrealized Losses |

||||||||||||||||||||||||||

|

AFS securities |

||||||||||||||||||||||||||||||||

|

U.S. government and agency securities: |

||||||||||||||||||||||||||||||||

|

U.S. Treasury securities |

$ | 19,937 | $ | 541 | $ | 5,994 | $ | 115 | $ | 25,931 | $ | 656 | ||||||||||||||||||||

|

U.S. agency securities |

12,904 | 383 | 4,142 | 114 | 17,046 | 497 | ||||||||||||||||||||||||||

|

Total U.S. government and agency securities |

32,841 | 924 | 10,136 | 229 | 42,977 | 1,153 | ||||||||||||||||||||||||||

|

Corporate and other debt: |

||||||||||||||||||||||||||||||||

|

Agency CMBS |

808 | 62 | — | — | 808 | 62 | ||||||||||||||||||||||||||

|

Non-agency CMBS |

— | — | 446 | 14 | 446 | 14 | ||||||||||||||||||||||||||

|

Corporate bonds |

470 | 7 | 1,010 | 25 | 1,480 | 32 | ||||||||||||||||||||||||||

|

FFELP student loan ABS |

1,366 | 15 | — | — | 1,366 | 15 | ||||||||||||||||||||||||||

|

Total corporate and other debt |

2,644 | 84 | 1,456 | 39 | 4,100 | 123 | ||||||||||||||||||||||||||

|

Total AFS securities |

35,485 | 1,008 | 11,592 | 268 | 47,077 | 1,276 | ||||||||||||||||||||||||||

|

HTM securities |

||||||||||||||||||||||||||||||||

|

U.S. government and agency securities: |

||||||||||||||||||||||||||||||||

|

U.S. Treasury securities |

— | — | 11,161 | 403 | 11,161 | 403 | ||||||||||||||||||||||||||

|

U.S. agency securities |

410 | 1 | 10,004 | 445 | 10,414 | 446 | ||||||||||||||||||||||||||

|

Total U.S. government and agency securities |

410 | 1 | 21,165 | 848 | 21,575 | 849 | ||||||||||||||||||||||||||

|

Corporate and other debt: |

||||||||||||||||||||||||||||||||

|

Non-agency CMBS |

206 | 1 | 216 | 8 | 422 | 9 | ||||||||||||||||||||||||||

|

Total HTM securities |

616 | 2 | 21,381 | 856 | 21,997 | 858 | ||||||||||||||||||||||||||

|

Total investment securities |

$ | 36,101 | $ | 1,010 | $ | 32,973 | $ | 1,124 | $ | 69,074 | $ | 2,134 | ||||||||||||||||||||

| March 2019 Form 10-Q | 52 |

Table of Contents

Notes to Consolidated Financial Statements

(Unaudited)

| 53 | March 2019 Form 10-Q |

Table of Contents

Notes to Consolidated Financial Statements

(Unaudited)

| March 2019 Form 10-Q | 54 |

Table of Contents

Notes to Consolidated Financial Statements

(Unaudited)

| 55 | March 2019 Form 10-Q |

Table of Contents

Notes to Consolidated Financial Statements

(Unaudited)

| March 2019 Form 10-Q | 56 |

Table of Contents

Notes to Consolidated Financial Statements

(Unaudited)

| 57 | March 2019 Form 10-Q |

Table of Contents

Notes to Consolidated Financial Statements

(Unaudited)

| March 2019 Form 10-Q | 58 |

Table of Contents

Notes to Consolidated Financial Statements

(Unaudited)

| 59 | March 2019 Form 10-Q |

Table of Contents

Notes to Consolidated Financial Statements

(Unaudited)

| March 2019 Form 10-Q | 60 |

Table of Contents

Notes to Consolidated Financial Statements

(Unaudited)

| 61 | March 2019 Form 10-Q |

Table of Contents

Notes to Consolidated Financial Statements

(Unaudited)

| March 2019 Form 10-Q | 62 |

Table of Contents

Notes to Consolidated Financial Statements

(Unaudited)

| 63 | March 2019 Form 10-Q |

Table of Contents

Notes to Consolidated Financial Statements

(Unaudited)

| March 2019 Form 10-Q | 64 |

Table of Contents

Notes to Consolidated Financial Statements

(Unaudited)

| 65 | March 2019 Form 10-Q |

Table of Contents

Notes to Consolidated Financial Statements

(Unaudited)

| March 2019 Form 10-Q | 66 |

Table of Contents

Notes to Consolidated Financial Statements

(Unaudited)

| 67 | March 2019 Form 10-Q |

Table of Contents

Notes to Consolidated Financial Statements

(Unaudited)

| March 2019 Form 10-Q | 68 |

Table of Contents

Notes to Consolidated Financial Statements

(Unaudited)

| 69 | March 2019 Form 10-Q |

Table of Contents

Table of Contents

Notes to Consolidated Financial Statements

(Unaudited)

| 71 | March 2019 Form 10-Q |

Table of Contents

Financial Data Supplement (Unaudited)

Average Balances and Interest Rates and Net Interest Income

| Three Months Ended March 31, | ||||||||||||||||||||||||

| 2019 | 2018 | |||||||||||||||||||||||

|

$ in millions |

|

Average

Daily Balance |

|

Interest |

|

Annualized

Average

|

|

|

Average

Daily

|

|

Interest |

|

Annualized

Average Rate |

|

||||||||||

|

Interest earning assets |

||||||||||||||||||||||||

|

Investment securities 1 |

$ | 94,906 | $ | 475 | 2.0 | % | $ | 80,532 | $ | 424 | 2.1 % | |||||||||||||

|

Loans 1 |

116,698 | 1,195 | 4.2 | 104,407 | 938 | 3.6 | ||||||||||||||||||

|

Securities purchased under agreements to resell and Securities borrowed 2: |

||||||||||||||||||||||||

|

U.S. |

141,806 | 934 | 2.7 | 124,172 | 309 | 1.0 | ||||||||||||||||||

|

Non-U.S. |

77,256 | 13 | 0.1 | 87,581 | (94 | ) | (0.4) | |||||||||||||||||

|

Trading assets, net of Trading liabilities 3: |

||||||||||||||||||||||||

|

U.S. |

74,152 | 631 | 3.5 | 53,488 | 487 | 3.7 | ||||||||||||||||||

|

Non-U.S. |

11,861 | 82 | 2.8 | 5,059 | 53 | 4.2 | ||||||||||||||||||

|

Customer receivables and Other 4: |

||||||||||||||||||||||||

|

U.S. |

63,649 | 697 | 4.4 | 74,118 | 542 | 3.0 | ||||||||||||||||||

|

Non-U.S. |

55,142 | 263 | 1.9 | 50,080 | 201 | 1.6 | ||||||||||||||||||

|

Total |

$ | 635,470 | $ | 4,290 | 2.7 | % | $ | 579,437 | $ | 2,860 | 2.0 % | |||||||||||||

|

Interest bearing liabilities |

||||||||||||||||||||||||

|

Deposits 1 |

$ | 181,017 | $ | 462 | 1.0 | % | $ | 159,948 | $ | 159 | 0.4 % | |||||||||||||

|

Borrowings 1, 5 |

189,181 | 1,380 | 3.0 | 194,558 | 1,138 | 2.4 | ||||||||||||||||||

|

Securities sold under agreements to repurchase and Securities loaned 6: |

||||||||||||||||||||||||

|

U.S. |

26,615 | 450 | 6.9 | 25,009 | 286 | 4.6 | ||||||||||||||||||

|

Non-U.S. |

32,350 | 150 | 1.9 | 40,675 | 116 | 1.2 | ||||||||||||||||||

|

Customer payables and Other 7: |

||||||||||||||||||||||||

|

U.S. |

117,932 | 554 | 1.9 | 121,438 | 49 | 0.2 | ||||||||||||||||||

|

Non-U.S. |

65,498 | 280 | 1.7 | 69,646 | 137 | 0.8 | ||||||||||||||||||

|

Total |

$ | 612,593 | $ | 3,276 | 2.2 | % | $ | 611,274 | $ | 1,885 | 1.3 % | |||||||||||||

|

Net interest income and net interest rate spread |

$ | 1,014 | 0.5 | % | $ | 975 | 0.7 % | |||||||||||||||||

| 1. |

Amounts include primarily U.S. balances. |

| 2. |

Includes fees paid on Securities borrowed. |

| 3. |

Excludes non-interest earning assets and non-interest bearing liabilities, such as equity securities. |

| 4. |

Includes interest from Customer receivables and Cash and cash equivalents. Prior period amounts have been revised to conform to the current presentation. |

| 5. |

Includes structured notes, whose interest expense is considered part of its value and therefore is recorded within Trading revenues. |

| 6. |

Includes fees received on Securities loaned. The annualized average rate was calculated using (a) interest expense incurred on all securities sold under agreements to repurchase and securities loaned transactions, whether or not such transactions were reported in the balance sheets and (b) net average on-balance sheet balances, which exclude certain securities-for-securities transactions. |

| 7. |

Includes fees received from prime brokerage customers for stock loan transactions entered into to cover customers’ short positions. |

| March 2019 Form 10-Q | 72 |

Table of Contents

Table of Contents

Glossary of Common Acronyms

| March 2019 Form 10-Q | 74 |

Table of Contents

Table of Contents

Unregistered Sales of Equity Securities and Use of Proceeds

The following table sets forth the information with respect to purchases made by or on behalf of the Firm of its common stock during the current quarter ended March 31, 2019.

|

Issuer Purchases of Equity Securities

|

||||||||||||||||

| $ in millions, except per share data |

Total Number of

Shares Purchased |

Average Price Paid Per Share |

Total Number of

Shares Purchased as Part of Publicly Announced Plans or Programs 1 |

Approximate

Dollar Value of Shares that May Yet be Purchased Under the Plans or Programs |

||||||||||||

|

Month #1 (January 1, 2019—January 31, 2019) |

||||||||||||||||

|

Share Repurchase Program 2 |

4,408,695 | $ | 42.54 | 4,408,695 | $ | 2,172 | ||||||||||

|

Employee transactions 3 |

10,089,356 | $ | 42.52 | — | — | |||||||||||

|

Month #2 (February 1, 2019—February 28, 2019) |

||||||||||||||||

|

Share Repurchase Program 2 |

8,886,000 | $ | 41.83 | 8,886,000 | $ | 1,801 | ||||||||||

|

Employee transactions 3 |

709,539 | $ | 42.18 | — | — | |||||||||||

|

Month #3 (March 1, 2019—March 31, 2019) |

||||||||||||||||

|

Share Repurchase Program 2 |

14,672,111 | $ | 42.31 | 14,672,111 | $ | 1,180 | ||||||||||

|

Employee transactions 3 |

156,953 | $ | 42.01 | — | — | |||||||||||

|

Quarter ended at March 31, 2019 |

||||||||||||||||

|

Share Repurchase Program 2 |

27,966,806 | $ | 42.19 | 27,966,806 | $ | 1,180 | ||||||||||

|

Employee transactions 3 |

10,955,848 | $ | 42.49 | — | — | |||||||||||

| 1. |

Share purchases under publicly announced programs are made pursuant to open-market purchases, Rule 10b5-1 plans or privately negotiated transactions (including with employee benefit plans) as market conditions warrant and at prices the Firm deems appropriate and may be suspended at any time. On April 18, 2018, the Firm entered into a sales plan with Mitsubishi UFJ Financial Group, Inc. (“MUFG”) and Morgan Stanley & Co. LLC (“MS&Co.”) whereby MUFG sold shares of the Firm’s common stock to the Firm, through the Firm’s agent MS&Co., as part of the Company’s Share Repurchase Program (as defined below). The sales plan is only intended to maintain MUFG’s ownership percentage below 24.9% in order to comply with MUFG’s passivity commitments to the Board of Governors of the Federal Reserve System (the “Federal Reserve”) and has no impact on the strategic alliance between MUFG and the Firm, including the joint ventures in Japan. |

| 2. |

The Firm’s Board of Directors has authorized the repurchase of the Firm’s outstanding stock under a share repurchase program (the “Share Repurchase Program”). The Share Repurchase Program is a program for capital management purposes that considers, among other things, business segment capital needs, as well as equity-based compensation and benefit plan requirements. The Share Repurchase Program has no set expiration or termination date. Share repurchases by the Firm are subject to regulatory approval. On June 28, 2018, the Federal Reserve published summary results of CCAR and the Firm received a conditional non-objection to its 2018 Capital Plan, where the only condition was that the Firm’s capital distributions not exceed the greater of the actual distributions it made over the previous four calendar quarters or the annualized average of actual distributions over the previous eight calendar quarters. As a result, the Firm’s 2018 Capital Plan includes a share repurchase of up to $4.7 billion of its outstanding common stock during the period beginning July 1, 2018 through June 30, 2019. During the quarter ended March 31, 2019, the Firm repurchased approximately $1.2 billion of the Firm’s outstanding common stock as part of its Share Repurchase Program. For further information, see “Liquidity and Capital Resources—Capital Management.” |

| 3. |

Includes shares acquired by the Firm in satisfaction of the tax withholding obligations on stock-based awards granted under the Firm’s stock-based compensation plans. |

| March 2019 Form 10-Q | 76 |

Table of Contents

| 77 | March 2019 Form 10-Q |

Table of Contents

Morgan Stanley

Quarter Ended March 31, 2019

| Exhibit No. | Description | |||

| 15 | ||||

| 23 |

Consent of Shearman & Sterling LLP, as Special Tax Counsel for Certain Structured Product Issuances. |

|||

| 31.1 | ||||

| 31.2 | ||||

| 32.1 | ||||

| 32.2 | ||||

| 101 |

Interactive data files pursuant to Rule 405 of Regulation S-T (unaudited): (i) the Consolidated Income Statements—Three Months Ended March 31, 2019 and 2018, (ii) the Consolidated Comprehensive Income Statements—Three Months Ended March 31, 2019 and 2018, (iii) the Consolidated Balance Sheets—Unaudited at March 31, 2019 and at December 31, 2018, (iv) the Consolidated Statements of Changes in Total Equity—Three Months Ended March 31, 2019 and 2018, (v) the Consolidated Cash Flow Statements—Three Months Ended March 31, 2019 and 2018, and (vi) Notes to Consolidated Financial Statements. |

|||

E-1

Table of Contents

Pursuant to the requirements of the Securities Exchange Act of 1934, the Registrant has duly caused this report to be signed on its behalf by the undersigned thereunto duly authorized.

|

MORGAN STANLEY (Registrant) |

||

|

By: |

/ S / J ONATHAN P RUZAN | |

|

Jonathan Pruzan Executive Vice President and Chief Financial Officer |

||

|

By: |

/ S / P AUL C. W IRTH | |

|

Paul C. Wirth Deputy Chief Financial Officer |

||

Date: May 3, 2019

S-1