NELNET INC

10-Ks and 10-Qs

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

WASHINGTON, D.C. 20549

FORM 10-Q

(Mark One)

|

ý

|

QUARTERLY REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934

|

For the quarterly period ended

September 30, 2018

or

|

¨

|

TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934

|

For the transition period from

to

.

Commission File Number: 001-31924

NELNET, INC.

(Exact name of registrant as specified in its charter)

|

NEBRASKA

(State or other jurisdiction of incorporation or organization)

|

84-0748903

(I.R.S. Employer Identification No.)

|

|

121 SOUTH 13TH STREET

SUITE 100

LINCOLN, NEBRASKA

(Address of principal executive offices)

|

68508

(Zip Code)

|

(402) 458-2370

(Registrant’s telephone number, including area code)

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes [X] No [ ]

Indicate by check mark whether the registrant has submitted electronically every Interactive Data File required to be submitted pursuant to Rule 405 of Regulation S-T (§232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit such files). Yes [X] No [ ]

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, a smaller reporting company, or an emerging growth company. See the definitions of “large accelerated filer,” “accelerated filer,” “smaller reporting company,” and "emerging growth company" in Rule 12b-2 of the Exchange Act.

Large accelerated filer [X] Accelerated filer [ ]

Non-accelerated filer [ ] Smaller reporting company [ ]

Emerging growth company [ ]

If an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided pursuant to Section 13(a) of the Exchange Act. [ ]

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act). Yes[ ] No[X]

As of

October 31, 2018

, there were

29,257,880

and

11,468,587

shares of Class A Common Stock and Class B Common Stock, par value $0.01 per share, outstanding, respectively (excluding a total of

11,305,731

shares of Class A Common Stock held by wholly owned subsidiaries).

NELNET, INC.

FORM 10-Q

INDEX

September 30, 2018

|

|

|||

|

|

Item 1.

|

||

|

|

Item 2.

|

||

|

|

Item 3.

|

||

|

|

Item 4.

|

||

|

|

|

|

|

|

|

|||

|

Item 1.

|

|||

|

|

Item 1A.

|

||

|

|

Item 2.

|

||

|

|

Item 6.

|

||

|

|

|

|

|

|

|

|||

|

NELNET, INC. AND SUBSIDIARIES

|

||||||

|

CONSOLIDATED BALANCE SHEETS

|

||||||

|

(Dollars in thousands, except share data)

|

||||||

|

(unaudited)

|

||||||

|

|

As of

|

|

As of

|

|||

|

|

September 30, 2018

|

|

December 31, 2017

|

|||

|

Assets:

|

|

|

||||

|

Loans receivable (net of allowance for loan losses of $60,217 and $54,590, respectively)

|

$

|

22,528,362

|

|

21,814,507

|

|

|

|

Cash and cash equivalents:

|

|

|

|

|

||

|

Cash and cash equivalents - not held at a related party

|

10,766

|

|

6,982

|

|

||

|

Cash and cash equivalents - held at a related party

|

72,771

|

|

59,770

|

|

||

|

Total cash and cash equivalents

|

83,537

|

|

66,752

|

|

||

|

Investments and notes receivable

|

246,815

|

|

240,538

|

|

||

|

Restricted cash

|

723,338

|

|

688,193

|

|

||

|

Restricted cash - due to customers

|

188,591

|

|

187,121

|

|

||

|

Loan accrued interest receivable

|

624,259

|

|

430,385

|

|

||

|

Accounts receivable (net of allowance for doubtful accounts of $2,426 and $1,436, respectively)

|

76,899

|

|

37,863

|

|

||

|

Goodwill

|

153,802

|

|

138,759

|

|

||

|

Intangible assets, net

|

95,660

|

|

38,427

|

|

||

|

Property and equipment, net

|

339,730

|

|

248,051

|

|

||

|

Other assets

|

41,889

|

|

73,021

|

|

||

|

Fair value of derivative instruments

|

2,043

|

|

818

|

|

||

|

Total assets

|

$

|

25,104,925

|

|

23,964,435

|

|

|

|

Liabilities:

|

|

|

|

|

||

|

Bonds and notes payable

|

$

|

22,251,433

|

|

21,356,573

|

|

|

|

Accrued interest payable

|

60,658

|

|

50,039

|

|

||

|

Other liabilities

|

272,891

|

|

198,252

|

|

||

|

Due to customers

|

188,591

|

|

187,121

|

|

||

|

Fair value of derivative instruments

|

4,224

|

|

7,063

|

|

||

|

Total liabilities

|

22,777,797

|

|

21,799,048

|

|

||

|

Commitments and contingencies

|

|

|

|

|

||

|

Equity:

|

||||||

|

Nelnet, Inc. shareholders' equity:

|

|

|

|

|

||

|

Preferred stock, $0.01 par value. Authorized 50,000,000 shares; no shares issued or outstanding

|

—

|

|

—

|

|

||

|

Common stock:

|

||||||

|

Class A, $0.01 par value. Authorized 600,000,000 shares; issued and outstanding 29,341,791 shares and 29,341,517 shares, respectively

|

293

|

|

293

|

|

||

|

Class B, convertible, $0.01 par value. Authorized 60,000,000 shares; issued and outstanding 11,468,587 shares

|

115

|

|

115

|

|

||

|

Additional paid-in capital

|

4,908

|

|

521

|

|

||

|

Retained earnings

|

2,307,573

|

|

2,143,983

|

|

||

|

Accumulated other comprehensive earnings

|

3,975

|

|

4,617

|

|

||

|

Total Nelnet, Inc. shareholders' equity

|

2,316,864

|

|

2,149,529

|

|

||

|

Noncontrolling interests

|

10,264

|

|

15,858

|

|

||

|

Total equity

|

2,327,128

|

|

2,165,387

|

|

||

|

Total liabilities and equity

|

$

|

25,104,925

|

|

23,964,435

|

|

|

|

Supplemental information - assets and liabilities of consolidated education lending variable interest entities:

|

||||||

|

Student loans receivable

|

$

|

22,536,434

|

|

21,909,476

|

|

|

|

Restricted cash

|

683,211

|

|

641,994

|

|

||

|

Loan accrued interest receivable and other assets

|

625,122

|

|

431,934

|

|

||

|

Bonds and notes payable

|

(22,337,987

|

)

|

(21,702,298

|

)

|

||

|

Accrued interest payable and other liabilities

|

(214,554

|

)

|

(168,637

|

)

|

||

|

Net assets of consolidated education lending variable interest entities

|

$

|

1,292,226

|

|

1,112,469

|

|

|

See accompanying notes to consolidated financial statements.

2

|

NELNET, INC. AND SUBSIDIARIES

|

||||||||||||

|

CONSOLIDATED STATEMENTS OF INCOME

|

||||||||||||

|

(Dollars in thousands, except share data)

|

||||||||||||

|

(unaudited)

|

||||||||||||

|

|

Three months ended

|

Nine months ended

|

||||||||||

|

|

September 30,

|

September 30,

|

||||||||||

|

|

2018

|

2017

|

2018

|

2017

|

||||||||

|

Interest income:

|

|

|

||||||||||

|

Loan interest

|

$

|

232,320

|

|

193,087

|

|

653,414

|

|

564,173

|

|

|||

|

Investment interest

|

7,628

|

|

3,800

|

|

18,581

|

|

9,616

|

|

||||

|

Total interest income

|

239,948

|

|

196,887

|

|

671,995

|

|

573,789

|

|

||||

|

Interest expense:

|

|

|

||||||||||

|

Interest on bonds and notes payable

|

180,175

|

|

121,650

|

|

487,174

|

|

341,787

|

|

||||

|

Net interest income

|

59,773

|

|

75,237

|

|

184,821

|

|

232,002

|

|

||||

|

Less provision for loan losses

|

10,500

|

|

6,700

|

|

18,000

|

|

10,700

|

|

||||

|

Net interest income after provision for loan losses

|

49,273

|

|

68,537

|

|

166,821

|

|

221,302

|

|

||||

|

Other income:

|

|

|

||||||||||

|

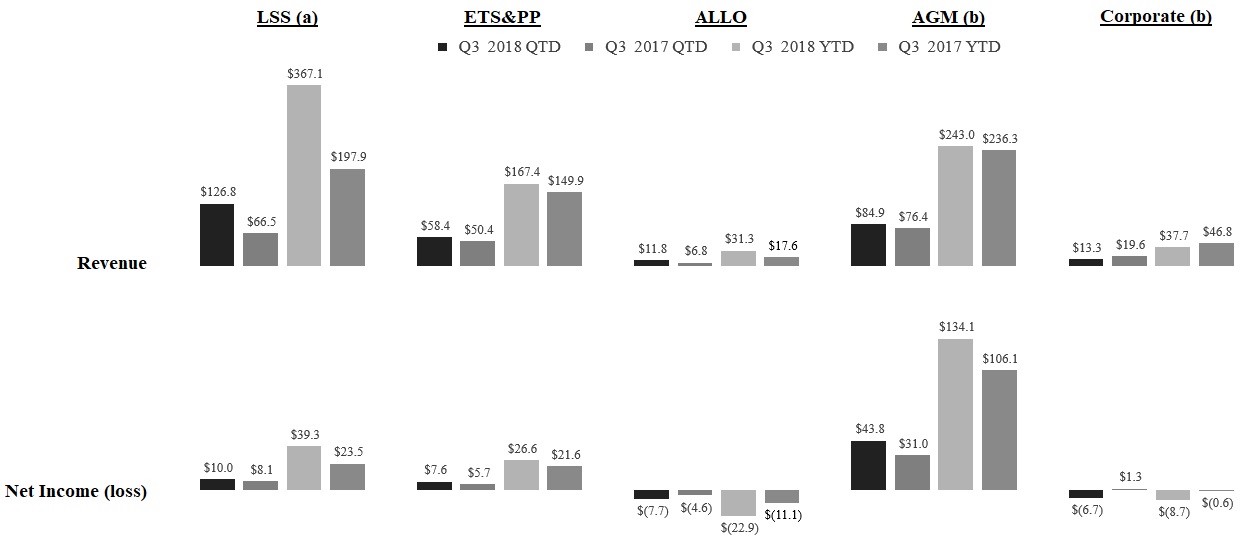

Loan servicing and systems revenue

|

112,579

|

|

55,950

|

|

327,265

|

|

167,079

|

|

||||

|

Education technology, services, and payment processing revenue

|

58,409

|

|

50,358

|

|

167,372

|

|

149,862

|

|

||||

|

Communications revenue

|

11,818

|

|

6,751

|

|

31,327

|

|

17,577

|

|

||||

|

Other income

|

16,673

|

|

19,756

|

|

44,449

|

|

44,874

|

|

||||

|

Gain from debt repurchases

|

—

|

|

116

|

|

359

|

|

5,537

|

|

||||

|

Derivative market value and foreign currency transaction adjustments and derivative settlements, net

|

17,098

|

|

7,173

|

|

100,927

|

|

(25,568

|

)

|

||||

|

Total other income

|

216,577

|

|

140,104

|

|

671,699

|

|

359,361

|

|

||||

|

Cost of services:

|

||||||||||||

|

Cost to provide education technology, services, and payment processing services

|

19,087

|

|

15,151

|

|

44,087

|

|

37,456

|

|

||||

|

Cost to provide communications services

|

4,310

|

|

2,632

|

|

11,892

|

|

6,789

|

|

||||

|

Total cost of services

|

23,397

|

|

17,783

|

|

55,979

|

|

44,245

|

|

||||

|

Operating expenses:

|

|

|

|

|

||||||||

|

Salaries and benefits

|

114,172

|

|

74,193

|

|

321,932

|

|

220,684

|

|

||||

|

Depreciation and amortization

|

22,992

|

|

10,051

|

|

62,943

|

|

27,687

|

|

||||

|

Loan servicing fees

|

3,087

|

|

8,017

|

|

9,428

|

|

19,670

|

|

||||

|

Other expenses

|

45,194

|

|

29,500

|

|

119,020

|

|

81,923

|

|

||||

|

Total operating expenses

|

185,445

|

|

121,761

|

|

513,323

|

|

349,964

|

|

||||

|

Income before income taxes

|

57,008

|

|

69,097

|

|

269,218

|

|

186,454

|

|

||||

|

Income tax expense

|

13,882

|

|

25,562

|

|

63,369

|

|

70,349

|

|

||||

|

Net income

|

43,126

|

|

43,535

|

|

205,849

|

|

116,105

|

|

||||

|

Net (income) loss attributable to noncontrolling interests

|

(199

|

)

|

2,768

|

|

438

|

|

8,960

|

|

||||

|

Net income attributable to Nelnet, Inc.

|

$

|

42,927

|

|

46,303

|

|

206,287

|

|

125,065

|

|

|||

|

Earnings per common share:

|

||||||||||||

|

Net income attributable to Nelnet, Inc. shareholders - basic and diluted

|

$

|

1.05

|

|

1.11

|

|

5.04

|

|

2.97

|

|

|||

|

Weighted average common shares outstanding - basic and diluted

|

40,988,965

|

|

41,553,316

|

|

40,942,177

|

|

42,054,532

|

|

||||

See accompanying notes to consolidated financial statements.

3

|

NELNET, INC. AND SUBSIDIARIES

|

||||||||||||

|

CONSOLIDATED STATEMENTS OF COMPREHENSIVE INCOME

|

||||||||||||

|

(Dollars in thousands)

|

||||||||||||

|

(unaudited)

|

||||||||||||

|

Three months ended

|

Nine months ended

|

|||||||||||

|

September 30,

|

September 30,

|

|||||||||||

|

2018

|

2017

|

2018

|

2017

|

|||||||||

|

Net income

|

$

|

43,126

|

|

43,535

|

|

205,849

|

|

116,105

|

|

|||

|

Other comprehensive income (loss):

|

||||||||||||

|

Available-for-sale securities:

|

||||||||||||

|

Unrealized holding losses arising during period, net

|

2,438

|

|

405

|

|

964

|

|

383

|

|

||||

|

Reclassification adjustment for gains recognized in net income, net of losses

|

(765

|

)

|

(504

|

)

|

(817

|

)

|

(1,244

|

)

|

||||

|

Income tax effect

|

(402

|

)

|

35

|

|

(46

|

)

|

318

|

|

||||

|

Total other comprehensive income (loss)

|

1,271

|

|

(64

|

)

|

101

|

|

(543

|

)

|

||||

|

Comprehensive income

|

44,397

|

|

43,471

|

|

205,950

|

|

115,562

|

|

||||

|

Comprehensive (income) loss attributable to noncontrolling interests

|

(199

|

)

|

2,768

|

|

438

|

|

8,960

|

|

||||

|

Comprehensive income attributable to Nelnet, Inc.

|

$

|

44,198

|

|

46,239

|

|

206,388

|

|

124,522

|

|

|||

See accompanying notes to consolidated financial statements.

4

|

NELNET, INC. AND SUBSIDIARIES

|

|||||||||||||||||||||||||||||||||

|

CONSOLIDATED STATEMENTS OF SHAREHOLDERS' EQUITY

|

|||||||||||||||||||||||||||||||||

|

(Dollars in thousands, except share data)

|

|||||||||||||||||||||||||||||||||

|

(unaudited)

|

|||||||||||||||||||||||||||||||||

|

|

Nelnet, Inc. Shareholders

|

||||||||||||||||||||||||||||||||

|

|

Preferred stock shares

|

Common stock shares

|

Preferred stock

|

Class A common stock

|

Class B common stock

|

Additional paid-in capital

|

Retained earnings

|

Accumulated other comprehensive (loss) earnings

|

Noncontrolling interests

|

Total equity

|

|||||||||||||||||||||||

|

|

Class A

|

Class B

|

|||||||||||||||||||||||||||||||

|

Balance as of June 30, 2017

|

—

|

|

30,373,691

|

|

11,476,932

|

|

$

|

—

|

|

304

|

|

115

|

|

366

|

|

2,110,158

|

|

4,251

|

|

15,215

|

|

2,130,409

|

|

||||||||||

|

Issuance of noncontrolling interests

|

—

|

|

—

|

|

—

|

|

—

|

|

—

|

|

—

|

|

—

|

|

—

|

|

—

|

|

6,901

|

|

6,901

|

|

|||||||||||

|

Net income (loss)

|

—

|

|

—

|

|

—

|

|

—

|

|

—

|

|

—

|

|

—

|

|

46,303

|

|

—

|

|

(2,768

|

)

|

43,535

|

|

|||||||||||

|

Other comprehensive loss

|

—

|

|

—

|

|

—

|

|

—

|

|

—

|

|

—

|

|

—

|

|

—

|

|

(64

|

)

|

—

|

|

(64

|

)

|

|||||||||||

|

Distribution to noncontrolling interests

|

—

|

|

—

|

|

—

|

|

—

|

|

—

|

|

—

|

|

—

|

|

—

|

|

—

|

|

(759

|

)

|

(759

|

)

|

|||||||||||

|

Cash dividend on Class A and Class B common stock - $0.14 per share

|

—

|

|

—

|

|

—

|

|

—

|

|

—

|

|

—

|

|

—

|

|

(5,766

|

)

|

—

|

|

—

|

|

(5,766

|

)

|

|||||||||||

|

Issuance of common stock, net of forfeitures

|

—

|

|

10,125

|

|

—

|

|

—

|

|

—

|

|

—

|

|

278

|

|

—

|

|

—

|

|

—

|

|

278

|

|

|||||||||||

|

Compensation expense for stock based awards

|

—

|

|

—

|

|

—

|

|

—

|

|

—

|

|

—

|

|

1,042

|

|

—

|

|

—

|

|

—

|

|

1,042

|

|

|||||||||||

|

Repurchase of common stock

|

—

|

|

(947,794

|

)

|

—

|

|

—

|

|

(10

|

)

|

—

|

|

(1,326

|

)

|

(43,800

|

)

|

—

|

|

—

|

|

(45,136

|

)

|

|||||||||||

|

Balance as of September 30, 2017

|

—

|

|

29,436,022

|

|

11,476,932

|

|

$

|

—

|

|

294

|

|

115

|

|

360

|

|

2,106,895

|

|

4,187

|

|

18,589

|

|

2,130,440

|

|

||||||||||

|

Balance as of June 30, 2018

|

—

|

|

29,331,002

|

|

11,468,587

|

|

$

|

—

|

|

293

|

|

115

|

|

2,586

|

|

2,271,171

|

|

2,704

|

|

9,834

|

|

2,286,703

|

|

||||||||||

|

Issuance of noncontrolling interests

|

—

|

|

—

|

|

—

|

|

—

|

|

—

|

|

—

|

|

—

|

|

—

|

|

—

|

|

326

|

|

326

|

|

|||||||||||

|

Net income

|

—

|

|

—

|

|

—

|

|

—

|

|

—

|

|

—

|

|

—

|

|

42,927

|

|

—

|

|

199

|

|

43,126

|

|

|||||||||||

|

Other comprehensive income

|

—

|

|

—

|

|

—

|

|

—

|

|

—

|

|

—

|

|

—

|

|

—

|

|

1,271

|

|

—

|

|

1,271

|

|

|||||||||||

|

Distribution to noncontrolling interests

|

—

|

|

—

|

|

—

|

|

—

|

|

—

|

|

—

|

|

—

|

|

—

|

|

—

|

|

(95

|

)

|

(95

|

)

|

|||||||||||

|

Cash dividend on Class A and Class B common stock - $0.16 per share

|

—

|

|

—

|

|

—

|

|

—

|

|

—

|

|

—

|

|

—

|

|

(6,525

|

)

|

—

|

|

—

|

|

(6,525

|

)

|

|||||||||||

|

Issuance of common stock, net of forfeitures

|

—

|

|

14,086

|

|

—

|

|

—

|

|

—

|

|

—

|

|

580

|

|

—

|

|

—

|

|

—

|

|

580

|

|

|||||||||||

|

Compensation expense for stock based awards

|

—

|

|

—

|

|

—

|

|

—

|

|

—

|

|

—

|

|

1,934

|

|

—

|

|

—

|

|

—

|

|

1,934

|

|

|||||||||||

|

Repurchase of common stock

|

—

|

|

(3,297

|

)

|

—

|

|

—

|

|

—

|

|

—

|

|

(192

|

)

|

—

|

|

—

|

|

—

|

|

(192

|

)

|

|||||||||||

|

Balance as of September 30, 2018

|

—

|

|

29,341,791

|

|

11,468,587

|

|

$

|

—

|

|

293

|

|

115

|

|

4,908

|

|

2,307,573

|

|

3,975

|

|

10,264

|

|

2,327,128

|

|

||||||||||

|

Balance as of December 31, 2016

|

—

|

|

30,628,112

|

|

11,476,932

|

|

$

|

—

|

|

306

|

|

115

|

|

420

|

|

2,056,084

|

|

4,730

|

|

9,270

|

|

2,070,925

|

|

||||||||||

|

Issuance of noncontrolling interests

|

—

|

|

—

|

|

—

|

|

—

|

|

—

|

|

—

|

|

—

|

|

—

|

|

—

|

|

19,553

|

|

19,553

|

|

|||||||||||

|

Net income (loss)

|

—

|

|

—

|

|

—

|

|

—

|

|

—

|

|

—

|

|

—

|

|

125,065

|

|

—

|

|

(8,960

|

)

|

116,105

|

|

|||||||||||

|

Other comprehensive loss

|

—

|

|

—

|

|

—

|

|

—

|

|

—

|

|

—

|

|

—

|

|

—

|

|

(543

|

)

|

—

|

|

(543

|

)

|

|||||||||||

|

Distribution to noncontrolling interests

|

—

|

|

—

|

|

—

|

|

—

|

|

—

|

|

—

|

|

—

|

|

—

|

|

—

|

|

(1,274

|

)

|

(1,274

|

)

|

|||||||||||

|

Cash dividends on Class A and Class B common stock - $0.42 per share

|

—

|

|

—

|

|

—

|

|

—

|

|

—

|

|

—

|

|

—

|

|

(17,569

|

)

|

—

|

|

—

|

|

(17,569

|

)

|

|||||||||||

|

Issuance of common stock, net of forfeitures

|

—

|

|

171,481

|

|

—

|

|

—

|

|

2

|

|

—

|

|

3,359

|

|

—

|

|

—

|

|

—

|

|

3,361

|

|

|||||||||||

|

Compensation expense for stock based awards

|

—

|

|

—

|

|

—

|

|

—

|

|

—

|

|

—

|

|

3,213

|

|

—

|

|

—

|

|

—

|

|

3,213

|

|

|||||||||||

|

Repurchase of common stock

|

—

|

|

(1,363,571

|

)

|

—

|

|

—

|

|

(14

|

)

|

—

|

|

(6,632

|

)

|

(56,685

|

)

|

—

|

|

—

|

|

(63,331

|

)

|

|||||||||||

|

Balance as of September 30, 2017

|

—

|

|

29,436,022

|

|

11,476,932

|

|

$

|

—

|

|

294

|

|

115

|

|

360

|

|

2,106,895

|

|

4,187

|

|

18,589

|

|

2,130,440

|

|

||||||||||

|

Balance as of December 31, 2017

|

—

|

|

29,341,517

|

|

11,468,587

|

|

$

|

—

|

|

293

|

|

115

|

|

521

|

|

2,143,983

|

|

4,617

|

|

15,858

|

|

2,165,387

|

|

||||||||||

|

Issuance of noncontrolling interests

|

—

|

|

—

|

|

—

|

|

—

|

|

—

|

|

—

|

|

—

|

|

—

|

|

—

|

|

847

|

|

847

|

|

|||||||||||

|

Net income (loss)

|

—

|

|

—

|

|

—

|

|

—

|

|

—

|

|

—

|

|

—

|

|

206,287

|

|

—

|

|

(438

|

)

|

205,849

|

|

|||||||||||

|

Other comprehensive income

|

—

|

|

—

|

|

—

|

|

—

|

|

—

|

|

—

|

|

—

|

|

—

|

|

101

|

|

—

|

|

101

|

|

|||||||||||

|

Distribution to noncontrolling interests

|

—

|

|

—

|

|

—

|

|

—

|

|

—

|

|

—

|

|

—

|

|

—

|

|

—

|

|

(351

|

)

|

(351

|

)

|

|||||||||||

|

Cash dividends on Class A and Class B common stock - $0.48 per share

|

—

|

|

—

|

|

—

|

|

—

|

|

—

|

|

—

|

|

—

|

|

(19,539

|

)

|

—

|

|

—

|

|

(19,539

|

)

|

|||||||||||

|

Issuance of common stock, net of forfeitures

|

—

|

|

319,365

|

|

—

|

|

—

|

|

3

|

|

—

|

|

4,662

|

|

—

|

|

—

|

|

—

|

|

4,665

|

|

|||||||||||

|

Compensation expense for stock based awards

|

—

|

|

—

|

|

—

|

|

—

|

|

—

|

|

—

|

|

4,526

|

|

—

|

|

—

|

|

—

|

|

4,526

|

|

|||||||||||

|

Repurchase of common stock

|

—

|

|

(319,091

|

)

|

—

|

|

—

|

|

(3

|

)

|

—

|

|

(4,801

|

)

|

(11,716

|

)

|

—

|

|

—

|

|

(16,520

|

)

|

|||||||||||

|

Impact of adoption of new accounting standards

|

—

|

|

—

|

|

—

|

|

—

|

|

—

|

|

—

|

|

—

|

|

2,007

|

|

(743

|

)

|

—

|

|

1,264

|

|

|||||||||||

|

Acquisition of noncontrolling interest

|

—

|

|

—

|

|

—

|

|

—

|

|

—

|

|

—

|

|

—

|

|

(13,449

|

)

|

—

|

|

(5,652

|

)

|

(19,101

|

)

|

|||||||||||

|

Balance as of September 30, 2018

|

—

|

|

29,341,791

|

|

11,468,587

|

|

$

|

—

|

|

293

|

|

115

|

|

4,908

|

|

2,307,573

|

|

3,975

|

|

10,264

|

|

2,327,128

|

|

||||||||||

See accompanying notes to consolidated financial statements.

5

|

NELNET, INC. AND SUBSIDIARIES

|

||||||

|

CONSOLIDATED STATEMENTS OF CASH FLOWS

|

||||||

|

(Dollars in thousands)

|

||||||

|

(unaudited)

|

||||||

|

|

Nine months ended

|

|||||

|

September 30,

|

||||||

|

|

2018

|

2017

|

||||

|

Net income attributable to Nelnet, Inc.

|

$

|

206,287

|

|

125,065

|

|

|

|

Net loss attributable to noncontrolling interests

|

(438

|

)

|

(8,960

|

)

|

||

|

Net income

|

205,849

|

|

116,105

|

|

||

|

Adjustments to reconcile net income to net cash provided by operating activities, net of acquisition:

|

|

|

|

|

||

|

Depreciation and amortization, including debt discounts and loan premiums and deferred origination costs

|

136,816

|

|

99,826

|

|

||

|

Loan discount accretion

|

(31,315

|

)

|

(32,820

|

)

|

||

|

Provision for loan losses

|

18,000

|

|

10,700

|

|

||

|

Derivative market value adjustment

|

(49,909

|

)

|

(22,381

|

)

|

||

|

Unrealized foreign currency transaction adjustment

|

—

|

|

45,635

|

|

||

|

Proceeds from clearinghouse - initial and variation margin, net

|

46,418

|

|

58,900

|

|

||

|

Gain from debt repurchases

|

(359

|

)

|

(5,537

|

)

|

||

|

Gain from equity securities, net of losses

|

(8,280

|

)

|

—

|

|

||

|

Deferred income tax expense (benefit)

|

23,574

|

|

(15,012

|

)

|

||

|

Non-cash compensation expense

|

4,781

|

|

3,370

|

|

||

|

Impairment expense

|

3,907

|

|

—

|

|

||

|

Other

|

(856

|

)

|

3,451

|

|

||

|

Increase in loan accrued interest receivable

|

(193,926

|

)

|

(5,572

|

)

|

||

|

Increase in accounts receivable

|

(15,328

|

)

|

(19,209

|

)

|

||

|

Decrease (increase) in other assets

|

49,255

|

|

(8,660

|

)

|

||

|

Increase in accrued interest payable

|

10,619

|

|

2,147

|

|

||

|

(Decrease) increase in other liabilities

|

(7,159

|

)

|

20,548

|

|

||

|

Increase (decrease) in due to customers

|

1,470

|

|

(14,403

|

)

|

||

|

Net cash provided by operating activities

|

193,557

|

|

237,088

|

|

||

|

Cash flows from investing activities, net of acquisition:

|

|

|

|

|

||

|

Purchases of loans

|

(3,231,956

|

)

|

(183,466

|

)

|

||

|

Net proceeds from loan repayments, claims, capitalized interest, and other

|

2,484,596

|

|

2,520,197

|

|

||

|

Proceeds from sale of loans

|

23,712

|

|

—

|

|

||

|

Purchases of available-for-sale securities

|

(38,064

|

)

|

(109,666

|

)

|

||

|

Proceeds from sales of available-for-sale securities

|

58,594

|

|

141,206

|

|

||

|

Purchases of investments and issuance of notes receivable

|

(49,216

|

)

|

(21,823

|

)

|

||

|

Proceeds from investments and notes receivable

|

21,461

|

|

6,174

|

|

||

|

Purchases of property and equipment

|

(96,480

|

)

|

(106,656

|

)

|

||

|

Business acquisition, net of cash acquired

|

(109,152

|

)

|

—

|

|

||

|

Net cash (used in) provided by investing activities

|

(936,505

|

)

|

2,245,966

|

|

||

|

Cash flows from financing activities:

|

|

|

|

|

||

|

Payments on bonds and notes payable

|

(2,149,449

|

)

|

(3,679,592

|

)

|

||

|

Proceeds from issuance of bonds and notes payable

|

3,004,848

|

|

1,178,027

|

|

||

|

Payments of debt issuance costs

|

(10,953

|

)

|

(4,411

|

)

|

||

|

Dividends paid

|

(19,539

|

)

|

(17,569

|

)

|

||

|

Repurchases of common stock

|

(16,520

|

)

|

(63,331

|

)

|

||

|

Proceeds from issuance of common stock

|

993

|

|

457

|

|

||

|

Acquisition of noncontrolling interest

|

(13,449

|

)

|

—

|

|

||

|

Issuance of noncontrolling interests

|

768

|

|

19,475

|

|

||

|

Distribution to noncontrolling interests

|

(351

|

)

|

(1,274

|

)

|

||

|

Net cash provided by (used in) financing activities

|

796,348

|

|

(2,568,218

|

)

|

||

|

Net increase (decrease) in cash, cash equivalents, and restricted cash

|

53,400

|

|

(85,164

|

)

|

||

|

Cash, cash equivalents, and restricted cash, beginning of period

|

942,066

|

|

1,170,317

|

|

||

|

Cash, cash equivalents, and restricted cash, end of period

|

$

|

995,466

|

|

1,085,153

|

|

|

6

|

NELNET, INC. AND SUBSIDIARIES

|

||||||

|

CONSOLIDATED STATEMENTS OF CASH FLOWS (Continued)

|

||||||

|

(Dollars in thousands)

|

||||||

|

(unaudited)

|

||||||

|

Nine months ended

|

||||||

|

September 30,

|

||||||

|

2018

|

2017

|

|||||

|

Supplemental disclosures of cash flow information:

|

||||||

|

Cash disbursements made for interest

|

$

|

425,782

|

|

287,265

|

|

|

|

Cash (refunds received) disbursements made for income taxes, net

|

$

|

(6,491

|

)

|

71,431

|

|

|

Supplemental disclosures of noncash operating and investing activities regarding the Company's business acquisition during the

nine months ended September 30, 2018

are contained in note 7.

The following table provides a reconciliation of cash, cash equivalents, and restricted cash reported in the consolidated balance sheets to the total of the amounts reported in the consolidated statements of cash flows.

|

As of

|

As of

|

As of

|

As of

|

|||||||||

|

September 30, 2018

|

December 31, 2017

|

September 30, 2017

|

December 31, 2016

|

|||||||||

|

Total cash and cash equivalents

|

$

|

83,537

|

|

66,752

|

|

254,391

|

|

69,654

|

|

|||

|

Restricted cash

|

723,338

|

|

688,193

|

|

725,463

|

|

980,961

|

|

||||

|

Restricted cash - due to customers

|

188,591

|

|

187,121

|

|

105,299

|

|

119,702

|

|

||||

|

Cash, cash equivalents, and restricted cash

|

$

|

995,466

|

|

942,066

|

|

1,085,153

|

|

1,170,317

|

|

|||

See accompanying notes to consolidated financial statements.

7

NELNET, INC. AND SUBSIDIARIES

NOTES TO CONSOLIDATED FINANCIAL STATEMENTS

(Dollars in thousands, except per share amounts, unless otherwise noted)

(unaudited)

1. Basis of Financial Reporting

The accompanying unaudited consolidated financial statements of Nelnet, Inc. and subsidiaries (the “Company”) as of

September 30, 2018

and for the

three and nine

months ended

September 30, 2018 and 2017

have been prepared on the same basis as the audited consolidated financial statements for the year ended

December 31, 2017

and, in the opinion of the Company’s management, the unaudited consolidated financial statements reflect all adjustments, consisting of normal recurring adjustments, necessary for a fair presentation of results of operations for the interim periods presented. The preparation of financial statements in conformity with U.S. generally accepted accounting principles requires management to make estimates and assumptions that affect the amounts reported in the consolidated financial statements and accompanying notes. Actual results could differ from those estimates. Operating results for the

three and nine

months ended

September 30, 2018

are not necessarily indicative of the results for the year ending

December 31, 2018

. The unaudited consolidated financial statements should be read in conjunction with the Company’s Annual Report on Form 10-K for the year ended

December 31, 2017

(the "

2017

Annual Report").

Reporting Segment Name Changes

During the first quarter of 2018, the Company changed the name of the Tuition Payment Processing and Campus Commerce operating segment to Education Technology, Services, and Payment Processing to better describe the evolution of services this operating segment provides. In addition, the Loan Systems and Servicing segment was retitled as Loan Servicing and Systems. As a result, the line items "tuition payment processing, school information, and campus commerce revenue" and "loan systems and servicing revenue" on the consolidated statements of income were changed to "education technology, services, and payment processing revenue" and "loan servicing and systems revenue," respectively.

Reclassifications

Certain amounts previously reported within the Company's consolidated balance sheet, statements of income, and statements of cash flows have been reclassified to conform to the current period presentation. These reclassifications include:

|

•

|

Reclassifying certain non-customer receivables, which were previously included in "accounts receivable," to "other assets."

|

|

•

|

Reclassifying direct costs to provide services for education technology, services, and payment processing, which were previously included in "other expenses," to "cost to provide education technology, services, and payment processing services."

|

|

•

|

Reclassifying the line item "cost to provide communications services" on the consolidated statements of income from part of "operating expenses" and presenting such costs as part of "cost of services."

|

|

•

|

Reclassifying consumer loan activity on the consolidated statements of income, which was previously included in "investment interest" and "other expenses," to "loan interest" and "provision for loan losses" and "loan servicing fees," respectively, and reclassifying consumer loan activity on the consolidated statements of cash flows as appropriate. This did not result in a change in the Company's previously reported net cash provided by operating or investing activities.

|

Accounting Standards Adopted in 2018

In the first quarter of 2018, the Company adopted the following new accounting standards and other guidance:

Revenue Recognition

In May 2014, the Financial Accounting Standards Board ("FASB") issued Accounting Standards Codification Topic 606,

Revenue from Contracts with Customers

("ASC Topic 606"). Under the standard, revenue is recognized when a customer obtains control of promised goods or services in an amount that reflects the consideration the entity expects to receive in exchange for those goods or services. In addition, the standard requires disclosure of the nature, amount, timing, and uncertainty of revenue and cash flows arising from contracts with customers.

8

The Company adopted the standard effective January 1, 2018, using the full retrospective method, which required it to restate each prior reporting period presented. As a result, the Company changed its accounting policy for revenue recognition as detailed in note 2, “Summary of Significant Accounting Policies and Practices.”

The most significant impact of the standard relates to identifying the Company's fee-based Education Technology, Services, and Payment Processing operating segment as the principal in its payment services transactions. As a result of this change, the Company presents the payment services revenue gross, with the direct costs to provide these services presented separately. The Company’s other fee-based operating segments will recognize revenue consistent with historical revenue recognition patterns. The majority of the Company's revenue earned in its non-fee-based Asset Generation and Management operating segment, including loan interest and derivative activity, is explicitly excluded from the scope of the new standard.

Impacts to Previously Reported Results

Adoption of the revenue recognition standard impacted the Company’s previously reported results on the consolidated statements of income as follows:

|

Three months ended September 30, 2017

|

||||||||||

|

As previously reported

|

Impact of adoption

|

As restated

|

||||||||

|

Education technology, services, and payment processing revenue

|

$

|

35,450

|

|

14,908

|

|

50,358

|

|

|||

|

Cost to provide education technology, services, and payment processing services

|

—

|

|

14,908

|

|

14,908

|

|

(a)

|

|||

|

Nine months ended September 30, 2017

|

||||||||||

|

As previously reported

|

Impact of adoption

|

As restated

|

||||||||

|

Education technology, services, and payment processing revenue

|

$

|

113,293

|

|

36,569

|

|

149,862

|

|

|||

|

Cost to provide education technology, services, and payment processing services

|

—

|

|

36,569

|

|

36,569

|

|

(a)

|

|||

|

(a)

|

In addition to the impact of adopting the new revenue recognition standard, as discussed above, the Company reclassified other direct costs to provide education technology, services, and payment processing services which were previously reported as part of "other expenses" to "cost to provide education technology, services, and payment processing services."

|

Adoption of the new revenue recognition standard had no impact to the consolidated balance sheets or cash provided by or used in operating, investing, or financing activities on the consolidated statements of cash flows.

Equity Investments

In January 2016, the FASB issued new accounting guidance related to the recognition and measurement of financial assets and financial liabilities. The guidance, including a related clarifying update, requires equity investments with readily determinable fair values to be measured at fair value, with changes in the fair value recognized through net income (other than those equity investments accounted for under the equity method of accounting or those that result in consolidation of the investee). An entity may choose to measure equity investments without readily determinable fair values at fair value or use the measurement alternative of cost minus impairment, if any, plus or minus changes resulting from observable price changes in orderly transactions for the identical or a similar investment of the same issuer. In addition, the impairment assessment is simplified by requiring a qualitative assessment to identify impairment.

The guidance requires a cumulative-effect adjustment to retained earnings as of the beginning of the reporting period of adoption to reclassify the cumulative change in fair value of equity securities with readily determinable fair values previously recognized in accumulated other comprehensive income, and was adopted by the Company as of January 1, 2018. Upon adoption, the Company recorded an immaterial cumulative-effect adjustment to retained earnings, accumulated other comprehensive earnings, and investments and notes receivable. Subsequent to the adoption, the Company is accounting for the majority of its equity investments without readily determinable fair values using the measurement alternative.

9

Other Comprehensive Income

In February 2018, the FASB issued guidance which allows a reclassification from accumulated other comprehensive earnings to retained earnings for stranded tax effects resulting from the Tax Cuts and Jobs Act, which became effective on January 1, 2018. This guidance is effective for fiscal years beginning after December 15, 2018, but early adoption is permitted. The Company elected to early adopt this guidance as of January 1, 2018. Upon adoption, the Company recorded an immaterial reclassification between accumulated other comprehensive earnings and retained earnings.

Restricted Cash

In November 2016, the FASB issued accounting guidance related to restricted cash. The new guidance requires that the statement of cash flows present the change during the period in total cash, cash equivalents, and amounts generally described as restricted cash or restricted cash equivalents, and a reconciliation of such total to amounts on the balance sheet. The Company adopted the standard effective January 1, 2018 using the retrospective transition method. Adoption of this standard impacted the Company's previously reported amounts on the consolidated statements of cash flows as follows:

|

Nine months ended September 30, 2017

|

|||||||||

|

As previously reported

|

Impact of adoption

|

As restated

|

|||||||

|

Decrease in due to customers

|

$

|

—

|

|

(14,403

|

)

|

(14,403

|

)

|

||

|

Proceeds from clearinghouse - initial and variation margin, net

|

37,744

|

|

21,156

|

|

58,900

|

|

|||

|

Net cash provided by operating activities

|

230,335

|

|

6,753

|

|

237,088

|

|

|||

|

Decrease in restricted cash, net

|

276,654

|

|

(276,654

|

)

|

—

|

|

|||

|

Net cash provided by investing activities

|

2,522,620

|

|

(276,654

|

)

|

2,245,966

|

|

|||

2. Summary of Significant Accounting Policies and Practices

Except for the changes below, no significant changes have been made to the Company’s significant accounting policies and practices disclosed in note 3, Summary of Significant Accounting Policies and Practices, in the 2017 Annual Report.

Revenue Recognition

The Company applies the provisions of ASC Topic 606 to its fee-based operating segments. The majority of the Company’s revenue earned in its Asset Generation and Management operating segment, including loan interest and derivative activity, is explicitly excluded from the scope of ASC Topic 606. The Company recognizes revenue under the core principle of ASC Topic 606 to depict the transfer of control of products and services to the Company’s customers in an amount reflecting the consideration to which the Company expects to be entitled. In order to achieve that core principle, the Company applies the following five-step approach: (1) identify the contract with a customer, (2) identify the performance obligations in the contract, (3) determine the transaction price, (4) allocate the transaction price to the performance obligations in the contract, and (5) recognize revenue when a performance obligation is satisfied. Additional information related to the Company's revenue recognition of specific items is provided below.

The Company’s contracts with customers often include promises to transfer multiple products and services to a customer. Determining whether products and services are considered distinct performance obligations that should be accounted for separately versus together may require significant judgment.

Loan servicing and systems revenue

- Loan servicing and systems revenue consists of the following items:

|

•

|

Loan servicing revenue

- Loan servicing revenue consideration is determined from individual contracts with customers and is calculated monthly based on the dollar value of loans, number of loans, number of borrowers serviced for each customer, or number of transactions. Loan servicing requires a significant level of integration and the individual components are not considered distinct. The Company will perform various services, including, but not limited to, (i) application processing, (ii) monthly servicing, (iii) conversion processing, and (iv) fulfillment services, during each distinct service period. Even though the mix and quantity of activities that the Company performs each period may differ, the nature of the activities are substantially the same. Revenue is allocated to the distinct service period, typically a month, and recognized as control transfers as customers simultaneously receive and consume benefits.

|

10

|

•

|

Software services revenue

- Software services revenue consideration is determined from individual contracts with customers and includes license and maintenance fees associated with loan software products, generally in a remote hosted environment, and computer and software consulting. Usage-based revenue from remote hosted licenses is allocated to the distinct service period, typically a month, and recognized as control transfers as customers simultaneously receive and consume benefits. Revenue from any non-refundable up-front fee is recognized ratably over the contract period, as the fee relates to set-up activities that provide no incremental benefit to the customers. Computer and software consulting is also capable of being distinct and accounted for as a separate performance obligation. Revenue allocated to computer and software consulting is recognized as services are provided.

|

|

•

|

Outsourced services revenue

- Outsourced services revenue consideration is determined from individual contracts with customers and is calculated monthly based on the volume of services. Revenue is allocated to the distinct service period, typically a month, and recognized as control transfers as customers simultaneously receive and consume benefits.

|

The following table provides disaggregated revenue by service offering:

|

|

Three months ended September 30,

|

Nine months ended September 30,

|

||||||||||

|

|

2018

|

2017

|

2018

|

2017

|

||||||||

|

Government servicing - Nelnet

|

$

|

38,907

|

|

38,594

|

|

118,015

|

|

117,409

|

|

|||

|

Government servicing - Great Lakes (a)

|

45,671

|

|

—

|

|

122,107

|

|

—

|

|

||||

|

FFELP servicing

|

7,422

|

|

3,979

|

|

24,259

|

|

11,693

|

|

||||

|

Private education and consumer loan servicing

|

10,007

|

|

7,596

|

|

31,990

|

|

20,535

|

|

||||

|

Software services

|

8,201

|

|

4,430

|

|

24,461

|

|

13,093

|

|

||||

|

Outsourced services and other

|

2,371

|

|

1,351

|

|

6,433

|

|

4,349

|

|

||||

|

Loan servicing and systems revenue

|

$

|

112,579

|

|

55,950

|

|

327,265

|

|

167,079

|

|

|||

|

(a)

|

Great Lakes Educational Loan Services, Inc. ("Great Lakes") was acquired by the Company on February 7, 2018. For additional information about the acquisition, see note 7.

|

Education technology, services, and payment processing revenue

- Education technology, services, and payment processing revenue consists of the following items:

|

•

|

Tuition payment plan services

- Tuition payment plan services consideration is determined from individual plan agreements, which are governed by plan service agreements, and includes access to a remote hosted environment and management of payment processing. The management of payment processing is considered a distinct performance obligation when sold with the remote hosted environment. Revenue for each performance obligation is allocated to the distinct service period, the academic school term, and recognized ratably over the service period as customers simultaneously receive and consume benefits.

|

|

•

|

Payment processing

- Payment processing consideration is determined from individual contracts with customers and includes electronic transfer and credit card processing, reporting, virtual terminal solutions, and specialized integrations to business software for education and non-education markets. Volume-based revenue from payment processing is allocated and recognized to the distinct service period, based on when each transaction is completed, and recognized as control transfers as customers simultaneously receive and consume benefits.

|

|

•

|

Education technology and services

- Education technology and services consideration is determined from individual contracts with customers and is based on the services selected by the customer. Services in K-12 private and faith based schools include (i) assistance with financial needs assessment, (ii) automating administrative processes such as admissions, online applications and enrollment services, scheduling, student billing, attendance, and grade book management, and (iii) professional development and educational instruction services. Revenue for these services is recognized for the consideration the Company has a right to invoice, the amount of which corresponds directly with the value provided to the customer based on the performance completed. Services provided to the higher education market include innovative education-focused technologies, services, and support solutions to help schools with the everyday challenges of collecting and processing commerce data. These services are considered distinct performance obligations. Revenue for each performance obligation is allocated to the distinct service period, typically a month or based on when each transaction is completed, and recognized as control transfers as customers simultaneously receive and consume benefits.

|

11

The following table provides disaggregated revenue by service offering:

|

|

Three months ended September 30,

|

Nine months ended September 30,

|

||||||||||

|

|

2018

|

2017

|

2018

|

2017

|

||||||||

|

Tuition payment plan services

|

$

|

19,771

|

|

17,885

|

|

63,209

|

|

58,543

|

|

|||

|

Payment processing

|

26,956

|

|

22,541

|

|

62,908

|

|

55,371

|

|

||||

|

Education technology and services

|

11,419

|

|

9,831

|

|

40,411

|

|

35,804

|

|

||||

|

Other

|

263

|

|

101

|

|

844

|

|

144

|

|

||||

|

Education technology, services, and payment processing revenue

|

$

|

58,409

|

|

50,358

|

|

167,372

|

|

149,862

|

|

|||

Cost to provide education technology, services, and payment processing services is primarily associated with providing payment processing services. Interchange and payment network fees are charged by the card associations or payment networks. Depending upon the transaction type, the fees are a percentage of the transaction’s dollar value, a fixed amount, or a combination of the two methods. Other items included in cost to provide education technology, services, and payment processing services include salaries and benefits and third-party professional service costs directly related to providing professional development and educational instruction services to teachers, school leaders, and students.

Communications revenue

-

Communications revenue is derived principally from internet, television, and telephone services and is billed as a flat fee in advance of providing the service. Revenues for usage-based services, such as access charges billed to other telephone carriers for originating and terminating long-distance calls on the Company's network, are billed in arrears. These are each considered distinct performance obligations. Revenue is recognized monthly for the consideration the Company has a right to invoice, the amount of which corresponds directly with the value provided to the customer based on the performance completed. The Company recognizes revenue from these services in the period the services are rendered rather than billed. Revenue received or receivable in advance of the delivery of services is included in deferred revenue. Earned but unbilled usage-based services are recorded in accounts receivable.

The following table provides disaggregated revenue by service offering and customer type:

|

Three months ended September 30,

|

Nine months ended September 30,

|

|||||||||||

|

2018

|

2017

|

2018

|

2017

|

|||||||||

|

Internet

|

$

|

6,456

|

|

3,205

|

|

16,547

|

|

7,978

|

|

|||

|

Television

|

3,385

|

|

2,115

|

|

9,250

|

|

5,498

|

|

||||

|

Telephone

|

1,957

|

|

1,413

|

|

5,471

|

|

4,018

|

|

||||

|

Other

|

20

|

|

18

|

|

59

|

|

83

|

|

||||

|

Communications revenue

|

$

|

11,818

|

|

6,751

|

|

31,327

|

|

17,577

|

|

|||

|

Residential revenue

|

$

|

8,896

|

|

4,680

|

|

23,367

|

|

11,851

|

|

|||

|

Business revenue

|

2,861

|

|

2,013

|

|

7,779

|

|

5,525

|

|

||||

|

Other

|

61

|

|

58

|

|

181

|

|

201

|

|

||||

|

Communications revenue

|

$

|

11,818

|

|

6,751

|

|

31,327

|

|

17,577

|

|

|||

Cost to provide communications services is primarily associated with television programming costs. The Company has various contracts to obtain television programming from programming vendors whose compensation is typically based on a flat fee per customer. The cost of the right to exhibit network programming under such arrangements is recorded in the month the programming is available for exhibition. Programming costs are paid each month based on calculations performed by the Company and are subject to periodic audits performed by the programmers. Other items in cost to provide communications services include connectivity, franchise, and other regulatory costs directly related to providing internet and telephone services.

12

Other income

-

The following table provides the components of "other income" on the consolidated statements of income:

|

Three months ended September 30,

|

Nine months ended September 30,

|

|||||||||||

|

2018

|

2017

|

2018

|

2017

|

|||||||||

|

Realized and unrealized gains on investments, net

|

$

|

1,288

|

|

2,201

|

|

11,505

|

|

3,818

|

|

|||

|

Borrower late fee income

|

3,253

|

|

2,731

|

|

8,994

|

|

9,098

|

|

||||

|

Investment advisory fees

|

1,183

|

|

5,852

|

|

4,169

|

|

11,661

|

|

||||

|

Management fee revenue

|

1,756

|

|

—

|

|

4,673

|

|

—

|

|

||||

|

Peterson's revenue

|

—

|

|

3,402

|

|

—

|

|

9,282

|

|

||||

|

Other

|

9,193

|

|

5,570

|

|

15,108

|

|

11,015

|

|

||||

|

Other income

|

$

|

16,673

|

|

19,756

|

|

44,449

|

|

44,874

|

|

|||

|

•

|

Borrower late fee income

- Late fee income is earned by the education lending subsidiaries. Revenue is allocated to the distinct service period, based on when each transaction is completed.

|

|

•

|

Investment advisory fees

- Investment advisory services are provided by the Company through an SEC-registered investment advisor subsidiary under various arrangements. The Company earns monthly fees based on the monthly outstanding balance of investments and certain performance measures, which are recognized monthly as the uncertainty of the transaction price is resolved.

|

|

•

|

Management fee revenue

- Management fee revenue is earned for technology and certain administrative support services provided to Great Lakes' former parent company. Revenue is allocated to the distinct service period, based on when each transaction is completed.

|

|

•

|

Peterson's revenue

- The Company earned revenue related to digital marketing and content solution products and services under the brand name Peterson's. These products and services included test preparation study guides, school directories and databases, career exploration guides, on-line courses and test preparation, scholarship search and selection data, career planning information and guides, and on-line information about colleges and universities. Several content solutions services included services to connect students to colleges and universities, and were sold based on subscriptions. Revenue from sales of subscription services was recognized ratably over the term of the contract as it was earned. Subscription revenue received or receivable in advance of the delivery of services was included in deferred revenue. Revenue from the sale of print products was generally earned and recognized, net of estimated returns, upon shipment or delivery. All other digital marketing and content solutions revenue was recognized over the period in which services were provided to customers. On December 31, 2017, the Company sold Peterson's. The Company applied a practical expedient allowed for the retrospective comparative period which does not require the Company to restate revenue from contracts that began and were completed within the same annual reporting period.

|

Contract Balances

-

The following table provides information about liabilities from contracts with customers:

|

As of September 30, 2018

|

As of December 31, 2017

|

|||||

|

Deferred revenue, which is included in "other liabilities" on the consolidated balance sheets

|

$

|

42,831

|

|

32,276

|

|

|

Timing of revenue recognition may differ from the timing of invoicing to customers. The Company records deferred revenue when revenue is received or receivable in advance of the delivery of service. For multi-year contracts, the Company generally invoices customers annually at the beginning of each annual coverage period. Payment terms and conditions vary by contract type, although terms generally include a requirement of payment within 30 to 60 days. In instances where the timing of revenue recognition differs from the timing of invoicing, the Company has determined its contracts do not include a significant financing component.

13

Activity in the deferred revenue balance is shown below:

|

Three months ended September 30,

|

Nine months ended September 30,

|

|||||||||||

|

2018

|

2017

|

2018

|

2017

|

|||||||||

|

Balance, beginning of period

|

$

|

25,660

|

|

25,954

|

|

32,276

|

|

33,141

|

|

|||

|

Deferral of revenue

|

45,174

|

|

38,705

|

|

97,726