NATIONAL RETAIL PROPERTIES, INC.

10-Ks and 10-Qs

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D. C. 20549

FORM 10-K

(Mark One)

x

ANNUAL REPORT PURSUANT TO SECTION 13 OR 15 (d) OF THE SECURITIES EXCHANGE ACT OF 1934.

For the fiscal year ended

December 31, 2017

OR

¨

TRANSITION REPORT PURSUANT TO SECTION 13 OR 15 (d) OF THE SECURITIES EXCHANGE ACT OF 1934.

For the transition period from to .

Commission file number 001-11290

NATIONAL RETAIL PROPERTIES, INC.

(Exact name of registrant as specified in its charter)

|

Maryland

(State or other jurisdiction of

incorporation or organization)

|

56-1431377

(I.R.S. Employer Identification No.)

|

450 South Orange Avenue, Suite 900

Orlando, Florida 32801

(Address of principal executive offices, including zip code)

Registrant’s telephone number, including area code: (407) 265-7348

Securities registered pursuant to Section 12(b) of the Act:

|

Title of each class:

Common Stock, $0.01 par value

5.700% Series E Preferred Stock, $0.01 par value

5.200% Series F Preferred Stock, $0.01 par value

|

Name of exchange on which registered:

New York Stock Exchange

New York Stock Exchange

New York Stock Exchange

|

Securities registered pursuant to section 12(g) of the Act:

None

(Title of class)

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. Yes

x

No

¨

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Act Yes

¨

No

x

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes

x

No

¨

Indicate by check mark whether the registrant has submitted electronically and posted on its corporate website, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T (§ 232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files). Yes

x

No

¨

Indicate by check mark if disclosure of delinquent filers pursuant to Item 405 of Regulation S-K is not contained herein, and will not be contained, to the best of registrant’s knowledge, in definitive proxy or information statements incorporated by reference in Part III of this Form 10-K or any amendment to this Form 10-K.

¨

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer or a smaller reporting company. See definition of “large accelerated filer,” “accelerated filer” and “smaller reporting company” in Rule 12b-2 of the Exchange Act. (Check one):

|

Large accelerated filer

x

|

|

Accelerated filer

¨

|

|

Non-accelerated filer

¨

|

|

Smaller reporting company

¨

|

|

Emerging growth company

¨

|

||||||

If an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided pursuant to Section 13(a) of the Exchange Act.

¨

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Act). Yes

¨

No

x

The aggregate market value of voting common stock held by non-affiliates of the registrant as of June 30,

2017

was $5,781,786,000.

The number of shares of common stock outstanding as of January 31,

2018

was 153,578,881.

.

DOCUMENTS INCORPORATED BY REFERENCE:

Registrant incorporates by reference into Part III (Items 10, 11, 12, 13 and 14) of this Annual Report on Form 10-K portions of National Retail Properties, Inc.’s definitive Proxy Statement for the 2018 Annual Meeting of Stockholders to be filed with the Securities and Exchange Commission (the “Commission”) pursuant to Regulation 14A. The definitive Proxy Statement will be filed with the Commission not later than 120 days after the end of the fiscal year covered by this Annual Report on Form 10-K.

TABLE OF CONTENTS

|

|

|

PAGE

REFERENCE

|

|

Part I

|

||

|

Item 1.

|

||

|

Item 1A.

|

||

|

Item 1B.

|

||

|

Item 2.

|

||

|

Item 3.

|

||

|

Item 4.

|

||

|

Part II

|

||

|

Item 5.

|

||

|

Item 6.

|

||

|

Item 7.

|

||

|

Item 7A.

|

||

|

Item 8.

|

||

|

Item 9.

|

||

|

Item 9A.

|

||

|

Item 9B.

|

||

|

Part III

|

||

|

Item 10.

|

||

|

Item 11.

|

||

|

Item 12.

|

||

|

Item 13.

|

||

|

Item 14.

|

||

|

Part IV

|

||

|

Item 15.

|

||

Unless the context otherwise requires, references in this Annual Report on Form 10-K to the terms “registrant” or “NNN” or the “Company” refer to National Retail Properties, Inc. and all of its consolidated subsidiaries. NNN may elect to treat certain subsidiaries as taxable real estate investment trust subsidiaries. These subsidiaries and their majority owned and controlled subsidiaries are collectively referred to as the “TRS.” At the close of business on December 31, 2015, NNN elected to revoke its election to classify the TRS as taxable REIT subsidiaries.

Statements contained in this Annual Report on Form 10-K, including the documents that are incorporated by reference, that are not historical facts are forward-looking statements within the meaning of Section 27A of the Securities Act of 1933 and Section 21E of the Securities Exchange Act of 1934 (the “Exchange Act”). Also, when NNN uses any of the words “anticipate,” “assume,” “believe,” “estimate,” “expect,” “intend,” or similar expressions, NNN is making forward-looking statements. Although management believes that the expectations reflected in such forward-looking statements are based upon present expectations and reasonable assumptions, NNN’s actual results could differ materially from those set forth in the forward-looking statements. Certain factors that could cause actual results or events to differ materially from those NNN anticipates or projects are described in “Item 1A. Risk Factors” of this Annual Report on Form 10-K.

Given these uncertainties, readers are cautioned not to place undue reliance on such statements, which speak only as of the date of this Annual Report on Form 10-K or any document incorporated herein by reference. NNN undertakes no obligation to publicly release any revisions to these forward-looking statements that may be made to reflect events or circumstances after the date of this Annual Report on Form 10-K.

|

Item 1.

|

Business

|

The Company

NNN, a Maryland corporation, is a fully integrated real estate investment trust (“REIT”) formed in 1984. NNN's assets are primarily real estate assets. NNN's consolidated financial statements are included in Item 8 of this Annual Report on Form 10-K.

Real Estate Assets

NNN acquires, owns, invests in and develops properties that are leased primarily to retail tenants under long-term net leases and are primarily held for investment ("Properties" or "Property Portfolio," or individually a "Property"). NNN owned

2,764

Properties with an aggregate gross leasable area of approximately

29,093,000

square feet, located in

48

states, with a weighted average remaining lease term of

11.5

years as of

December 31, 2017

. Approximately

99

percent of the Properties were leased as of

December 31, 2017

.

Competition

NNN generally competes with numerous other REITs, commercial developers, real estate limited partnerships and other investors including but not limited to insurance companies, pension funds and financial institutions that own, manage, finance or develop retail and net leased properties.

Employees

As of January 31, 2018

, NNN employed

66

associates.

Other Information

NNN’s executive offices are located at 450 S. Orange Avenue, Suite 900, Orlando, Florida 32801, and its telephone number is (407) 265-7348. NNN has a website at

www.nnnreit.com

where NNN’s filings with the Securities and Exchange Commission (the "Commission") can be downloaded free of charge.

The common shares of National Retail Properties, Inc. are traded on the New York Stock Exchange (the "NYSE") under the ticker symbol "NNN." National Retail Properties, Inc. has two series of preferred shares outstanding which are traded on the NYSE in the form of depositary shares: the depositary shares, each representing a 1/100

th

of a share of 5.700% Series E Cumulative Redeemable Preferred Stock, par value $0.01 per share (“Series E Preferred Stock”), are traded on the NYSE under the ticker symbol "NNNPRE" and the depositary shares, each representing a 1/100

th

of a share of 5.200%

1

Series F Cumulative Redeemable Preferred Stock, par value $0.01 per share (“Series F Preferred Stock”), are traded on the NYSE under the symbol "NNNPRF."

Business Strategies and Policies

The following is a discussion of NNN’s operating strategy and certain of its investment, financing and other policies. These strategies and policies have been set by management and the Board of Directors and, in general, may be amended or revised from time to time by management and the Board of Directors without a vote of NNN’s stockholders.

Operating Strategies

NNN’s strategy is to invest primarily in retail real estate that is typically well located within each local market for its tenants’ retail lines of trade. Management believes that these types of properties, generally leased pursuant to triple-net leases, provide attractive opportunities for stable current returns and the potential for increased returns and capital appreciation. Triple-net leases typically require the tenant to pay property operating expenses such as insurance, utilities, repairs, maintenance, capital expenditures and real estate taxes and assessments. Initial lease terms are generally 10 to 20 years.

NNN holds each real estate asset until it determines that the sale of such an asset is advantageous in view of NNN’s investment objectives. In deciding whether to sell a real estate asset, factors NNN may consider may include but are not limited to potential capital appreciation, net cash flow, tenant credit quality, tenant's line of trade, portfolio composition, market lease rates, local market conditions, potential use of sale proceeds and federal income tax considerations.

NNN’s management team focuses on certain key indicators to evaluate the financial condition and operating performance of NNN. These key indicators include the composition of the Property Portfolio (such as tenant, geographic and line of trade diversification), the occupancy rate of the Property Portfolio, certain financial performance ratios and profitability measures, industry trends, and industry performance compared to NNN.

The operating strategies employed by NNN have allowed NNN to increase the annual dividend (paid quarterly) per common share for

28

consecutive years. NNN is one of only three publicly traded REITs to increase its annual dividend per common share for

28

or more consecutive years.

Investment in Real Estate or Interests in Real Estate

NNN’s management believes that single tenant, freestanding net lease retail properties will continue to provide attractive investment opportunities and that NNN is well suited to take advantage of these opportunities because of its experience in accessing capital markets, and its ability to source, underwrite and acquire such properties.

In evaluating a particular acquisition, management may consider a variety of factors, including but not limited to:

|

•

|

the location, visibility and accessibility of the property,

|

|

•

|

the geographic area and demographic characteristics of the community,

|

|

•

|

the local real estate market conditions, including potential for growth, market rents, and existing or potential competing properties or retailers,

|

|

•

|

the size, age and title status of the property,

|

|

•

|

the quality of construction and design and the current physical condition of the property,

|

|

•

|

the potential for, and current extent of, any environmental problems,

|

|

•

|

the purchase price,

|

|

•

|

the non-financial terms of the proposed acquisition,

|

|

•

|

the availability of funds or other consideration for the proposed acquisition and the cost thereof,

|

|

•

|

the compatibility of the property with NNN’s existing Property Portfolio,

|

|

•

|

the property-level operating history,

|

|

•

|

the financial and other characteristics of the existing tenant,

|

|

•

|

the tenant’s business plan, operating history and management team,

|

|

•

|

the tenant’s industry,

|

|

•

|

the terms of any lease,

|

|

•

|

the rent to be paid by the tenant, and

|

2

|

•

|

any existing indebtedness encumbering the property which may be assumed in connection with acquiring or refinancing these investments.

|

NNN intends to engage in future investment activities in a manner that is consistent with the maintenance of its status as a REIT for federal income tax purposes. Additionally, NNN does not intend to engage in activities that will make NNN an investment company under the Investment Company Act of 1940, as amended.

Investments in Real Estate Mortgages and Securities of or Interests in Persons Engaged in Real Estate Activities

While NNN’s primary business objectives emphasize retail properties, NNN may invest in (i) a wide variety of property and tenant types, (ii) leases, mortgages and other types of real estate interests, (iii) loans secured by personal property, (iv) loans secured by partnership or membership interests in partnerships or limited liability companies, respectively, or (v) securities of other REITs, or other issuers, including for the purpose of exercising control over such entities.

Financing Strategy

NNN’s financing objective is to manage its capital structure effectively in order to provide sufficient capital to execute its operating strategies while servicing its debt requirements and providing value to its stockholders. NNN generally utilizes debt and equity security offerings, bank borrowings, proceeds from the sale of properties, and to a lesser extent, internally generated funds to meet its capital needs.

NNN typically funds its short-term liquidity requirements including investments in additional properties with advances from its

$900,000,000

unsecured revolving credit facility ("Credit Facility"). As of

December 31, 2017

,

$120,500,000

was outstanding and

$779,500,000

was available for future borrowings under the Credit Facility, excluding undrawn letters of credit totaling

$230,000

.

As of

December 31, 2017

, NNN’s ratio of total debt to total gross assets (before accumulated depreciation and amortization) was approximately

35

percent and the ratio of secured indebtedness to total gross assets was less than

one

percent. The ratio of total debt to total market capitalization was approximately

27

percent. Certain financial agreements contain covenants that limit NNN’s ability to incur additional debt under certain circumstances.

NNN anticipates it will be able to obtain additional financing for short-term and long-term liquidity requirements as further described in "Item 7. Management’s Discussion and Analysis of Financial Condition and Results of Operations – Liquidity." However, there can be no assurance that additional financing or capital will be available, or that the terms will be acceptable or advantageous to NNN.

The organizational documents of NNN do not limit the absolute amount or percentage of indebtedness that NNN may incur. Additionally, NNN may change its financing strategy at any time.

Strategies and Policy Changes

Any of NNN’s strategies or policies described above may be changed at any time by NNN without notice to or a vote of NNN’s stockholders.

Property Portfolio

As of

December 31, 2017

, NNN owned

2,764

Properties with an aggregate gross leasable area of approximately

29,093,000

square feet, located in

48

states, with a weighted average remaining lease term of

11.5

years. Approximately

99

percent of total Properties were leased as of

December 31, 2017

.

The following table summarizes the Property Portfolio at

December 31, 2017

(in thousands):

|

|

Size

(1)

|

Total Dollars Invested

(2)

|

||||||||||||||||||

|

High

|

Low

|

Average

|

High

|

Low

|

Average

|

|||||||||||||||

|

Land

|

3,733

|

|

2

|

|

102

|

|

$

|

8,882

|

|

$

|

5

|

|

$

|

846

|

|

|||||

|

Building

|

142

|

|

1

|

|

11

|

|

45,286

|

|

19

|

|

1,846

|

|

||||||||

|

(1)

|

Approximate square feet.

|

|

(2)

|

Costs vary depending upon size, improvements, local market conditions and other factors.

|

3

As of

December 31, 2017

, NNN has committed to fund construction commitments on

27

Properties. The improvements on such Properties are estimated to be completed within 12 months. These construction commitments, at

December 31, 2017

, are outlined in the table below (dollars in thousands):

|

Total commitment

(1)

|

$

|

129,925

|

|

|

|

Amount funded

|

67,719

|

|

||

|

Remaining commitment

|

62,206

|

|

||

|

(1)

|

Includes land, construction costs, tenant improvements, lease costs, and capitalized interest.

|

Leases

The following is a summary of the general structure of the leases in the Property Portfolio, although the specific terms of each lease can vary significantly. Generally, the Property leases provide for initial terms of 10 to 20 years. As of

December 31, 2017

, the weighted average remaining lease term of the Property Portfolio was approximately

11.5

years. The Properties are generally leased under net leases, pursuant to which the tenant typically bears responsibility for substantially all property costs and expenses associated with ongoing maintenance, repair, replacement and operation of the property, including utilities, property taxes and insurance. NNN's leases provide for annual base rental payments (generally payable in monthly installments) ranging from $6,000 to $3,714,000 (average of $215,000), and generally provide for increases in rent as a result of (i) increases in the Consumer Price Index ("CPI"), (ii) fixed increases, or, to a lesser extent, (iii) increases in the tenant’s sales volume.

Generally, NNN's leases provide the tenant with one or more multi-year renewal options subject to generally the same terms and conditions provided under the initial lease term. Some of the leases also provide that in the event NNN wishes to sell the Property subject to that lease, NNN first must offer the lessee the right to purchase the Property on the same terms and conditions as any offer which NNN intends to accept for the sale of the Property.

The following table summarizes the lease expirations, assuming none of the tenants exercise renewal options, of the Property Portfolio for each of the next 10 years and then thereafter in the aggregate as of

December 31, 2017

:

|

% of

Annual

Base

Rent

(1)

|

# of

Properties

|

Gross

Leasable

Area

(2)

|

% of

Annual

Base

Rent

(1)

|

# of

Properties

|

Gross

Leasable

Area

(2)

|

||||||||||

|

2018

|

2.0%

|

61

|

787,000

|

|

2024

|

2.2%

|

50

|

833,000

|

|

||||||

|

2019

|

2.7%

|

75

|

1,081,000

|

|

2025

|

4.7%

|

128

|

1,123,000

|

|

||||||

|

2020

|

3.5%

|

127

|

1,559,000

|

|

2026

|

5.6%

|

184

|

1,854,000

|

|

||||||

|

2021

|

4.1%

|

121

|

1,320,000

|

|

2027

|

8.7%

|

197

|

2,766,000

|

|

||||||

|

2022

|

6.4%

|

125

|

1,697,000

|

|

Thereafter

|

57.5%

|

1,566

|

14,540,000

|

|

||||||

|

2023

|

2.6%

|

99

|

1,143,000

|

|

|||||||||||

|

(1)

|

Based on annualized base rent for all leases in place as of

December 31, 2017

.

|

|

(2)

|

Approximate square feet.

|

4

The following table summarizes the diversification of the Property Portfolio based on the top 10 lines of trade:

|

|

|

% of Annual Base Rent

(1)

|

||||||

|

|

Top 10 Lines of Trade

|

2017

|

2016

|

2015

|

||||

|

1.

|

Convenience stores

|

18.1%

|

16.9%

|

16.7%

|

||||

|

2.

|

Restaurants - full service

|

12.1%

|

11.8%

|

11.0%

|

||||

|

3.

|

Restaurants - limited service

|

7.6%

|

7.5%

|

7.2%

|

||||

|

4.

|

Automotive service

|

6.9%

|

6.6%

|

7.0%

|

||||

|

5.

|

Family entertainment centers

|

6.4%

|

5.8%

|

5.6%

|

||||

|

6.

|

Health and fitness

|

5.6%

|

5.7%

|

3.8%

|

||||

|

7.

|

Theaters

|

4.8%

|

4.9%

|

5.2%

|

||||

|

8.

|

Automotive parts

|

3.6%

|

3.9%

|

4.2%

|

||||

|

9.

|

Recreational vehicle dealers, parts and accessories

|

3.4%

|

3.4%

|

3.6%

|

||||

|

10.

|

Banks

|

2.5%

|

3.1%

|

3.4%

|

||||

|

Other

|

29.0%

|

30.4%

|

32.3%

|

|||||

|

100.0%

|

100.0%

|

100.0%

|

||||||

|

(1)

|

Based on annualized base rent for all leases in place as of December 31 of the respective year.

|

The following table summarizes the diversification of the Property Portfolio by state as of

December 31, 2017

:

|

State

|

# of

Properties

|

% of

Annual

Base Rent

(1)

|

||||

|

1.

|

Texas

|

457

|

18.2%

|

|||

|

2.

|

Florida

|

211

|

8.7%

|

|||

|

3.

|

Illinois

|

132

|

5.4%

|

|||

|

4.

|

Ohio

|

168

|

5.3%

|

|||

|

5.

|

North Carolina

|

154

|

5.1%

|

|||

|

6.

|

Georgia

|

127

|

4.3%

|

|||

|

7.

|

Tennessee

|

131

|

4.0%

|

|||

|

8.

|

Virginia

|

119

|

3.9%

|

|||

|

9.

|

Indiana

|

123

|

3.9%

|

|||

|

10.

|

Alabama

|

128

|

3.1%

|

|||

|

Other

|

1,014

|

38.1%

|

||||

|

2,764

|

100.0%

|

|||||

|

(1)

Based on annualized base rent for all leases in place as of December 31, 2017.

|

||||||

As of

December 31, 2017

, NNN did not have any tenant that accounted for ten percent or more of its rental income.

5

Governmental Regulations Affecting Properties

Property Environmental Considerations.

Subject to a determination of the level of risk and potential cost of remediation, NNN may acquire a property where some level of environmental contamination may exist. Investments in real property create a potential for substantial environmental liability for the owner of such property from the presence or discharge of hazardous materials on the property or the improper disposal of hazardous materials emanating from the property, regardless of fault. In order to mitigate exposure to environmental liability, NNN maintains an environmental insurance policy which provides some coverage for substantially all of the properties. Such policy expires in August 2018. As a part of its acquisition due diligence process, NNN obtains an environmental site assessment for each property. In such cases where NNN intends to acquire a property where some level of contamination may exist, NNN generally requires the seller or tenant to (i) remediate the problem, (ii) indemnify NNN for environmental liabilities, and/or (iii) agree to other arrangements deemed appropriate by NNN, including, under certain circumstances, the purchase of environmental insurance to address environmental conditions at the property. NNN may incur costs if the tenant does not comply with these requests.

As of

February 6, 2018

, NNN has

77

Properties currently under some level of environmental remediation and/or monitoring. In general, the seller, a previous owner, the tenant or an adjacent land owner is responsible for the cost of the environmental remediation for each of these Properties.

Americans with Disabilities Act of 1990.

The Properties, as commercial facilities, are required to comply with Title III of the Americans with Disabilities Act of 1990 and similar state and local laws and regulations (collectively, the "ADA"). The tenants will typically have primary responsibility for complying with the ADA, but NNN may incur costs if the tenant does not comply. As of

February 6, 2018

, NNN has not been notified by any governmental authority of, nor is NNN’s management aware of, any non-compliance with the ADA that NNN’s management believes would have a material adverse effect on its business, financial position or results of operations.

Other Regulations.

State and local fire, life-safety and similar entities regulate the use of the Properties. NNN’s leases generally require each tenant to undertake primary responsibility for complying with regulations, but failure to comply could result in fines by governmental authorities, awards of damages to private litigants, or restrictions on the ability to conduct business on such properties.

|

Item 1A.

|

Risk Factors

|

Carefully consider the following risks and all of the other information set forth in this Annual Report on Form 10-K, including the consolidated financial statements and the notes thereto. If any of the events or developments described below were actually to occur, NNN’s business, financial condition or results of operations could be adversely affected.

Financial and economic conditions may have an adverse impact on NNN, its tenants, and commercial real estate in general.

Financial and economic conditions can be challenging and volatile and any worsening of such conditions, including any disruption in the capital markets, could adversely affect NNN’s business and results of operations. Such conditions could also affect the financial condition of NNN’s tenants, developers, borrowers, lenders or the institutions that hold NNN’s cash balances and short-term investments, which may expose NNN to increased risks of default by these parties.

There can be no assurance that actions of the United States Government, the Federal Reserve or other government and regulatory bodies intended to stabilize the economy or financial markets will achieve their intended effect. Additionally, some of these actions may adversely affect financial institutions, capital providers, retailers, consumers, NNN’s financial condition, NNN's results of operations or the trading price of NNN’s shares.

6

Potential consequences of challenging and volatile financial and economic conditions include:

|

•

|

the financial condition of NNN’s tenants may be adversely affected, which may result in tenant defaults under the leases due to bankruptcy, lack of liquidity, operational failures or for other reasons,

|

|

•

|

the ability to borrow on terms and conditions that NNN finds acceptable may be limited or unavailable, which could reduce NNN’s ability to pursue acquisition and development opportunities and refinance existing debt, reduce NNN’s returns from acquisition and development activities, reduce NNN’s ability to make cash distributions to its stockholders and increase NNN’s future interest expense,

|

|

•

|

the recognition of impairment charges on or reduced values of the Properties, may adversely affect NNN's results of operations,

|

|

•

|

reduced values of the Properties may limit NNN's ability to dispose of assets at attractive prices and reduce the availability of buyer financing, and

|

|

•

|

the value and liquidity of NNN’s short-term investments and cash deposits could be reduced as a result of (i) a deterioration of the financial condition of the institutions that hold NNN’s cash deposits or the institutions or assets in which NNN has made short-term investments, (ii) the dislocation of the markets for NNN’s short-term investments, (iii) increased volatility in market rates for such investments or (iv) other factors.

|

NNN may be unable to obtain debt or equity capital on favorable terms, if at all.

NNN may be unable to obtain capital on favorable terms, if at all, to further its business objectives or meet its existing obligations. Nearly all of NNN’s debt, including the Credit Facility, is subject to balloon principal payments due at maturity. These maturities range between 2021 and 2027. NNN's ability to make these scheduled principal payments may be adversely impacted by NNN’s inability to extend or refinance the Credit Facility, the inability to dispose of assets at an attractive price or the inability to obtain additional debt or equity capital. Capital that may be available may be materially more expensive or available under terms that are materially more restrictive which would have an adverse impact on NNN’s business, financial condition and results of operations.

Loss of rent from tenants would reduce NNN’s cash flow.

NNN's tenants encounter significant macroeconomic, governmental and competitive forces. Adverse changes in consumer spending or consumer preferences for particular goods, services or store based retailing could severely impact their ability to pay rent. Shifts from in-store to online shopping could increase due to changing consumer shopping patterns as well as the increase in consumer adoption and use of mobile electronic devices. This expansion of e-commerce could have an adverse impact on NNN's tenants' ongoing viability. The default, financial distress, bankruptcy or liquidation of one or more of NNN’s tenants could cause substantial vacancies in the Property Portfolio. Vacancies reduce NNN’s revenues, increase property expenses and could decrease the value of each such vacant Property. Upon the expiration of a lease, the tenant may choose not to renew the lease and NNN may not be able to re-lease the vacant Property at a comparable lease rate. Furthermore, NNN may incur additional expenditures in connection with such renewal or re-leasing.

A significant portion of the source of the Property Portfolio annual base rent is concentrated in specific industry classifications, tenants and geographic locations.

As of

December 31, 2017

, approximately,

|

•

|

51.1% of the Property Portfolio annual base rent is generated from tenants in five retail lines of trade, including convenience stores (18.1%) and full-service and limited-service restaurants (19.7%),

|

|

•

|

20.6% of the Property Portfolio annual base rent is generated from five tenants, Sunoco (5.1%), Camping World (4.2%), Mister Car Wash (4.1%), LA Fitness (3.8%), AMC Theatres (3.4%), and

|

|

•

|

42.7% of the Property Portfolio annual base rent is generated from properties located in five states, including Texas (18.2%) and Florida (8.7%).

|

Any financial hardship and/or economic changes in these lines of trade, tenants or states could have an adverse effect on NNN’s results of operations.

7

Owning real estate and indirect interests in real estate carries inherent risks.

NNN’s economic performance and the value of its real estate assets are subject to the risk that if the Properties do not generate revenues sufficient to meet its operating expenses, including debt service, NNN’s cash flow and ability to pay distributions to its stockholders will be adversely affected. As a real estate company, NNN is susceptible to the following real estate industry risks, which are beyond its control:

|

•

|

changes in national, regional and local economic conditions and outlook,

|

|

•

|

decreases in consumer spending and retail sales or adverse changes in consumer preferences for particular goods, services or store based retailing,

|

|

•

|

economic downturns in the areas where the Properties are located,

|

|

•

|

adverse changes in local real estate market conditions, such as an oversupply of space, reduction in demand for space, loss of a large employer, intense competition for tenants, or a demographic change,

|

|

•

|

changes in tenant or consumer preferences that reduce the attractiveness of the Properties to tenants,

|

|

•

|

changes in zoning, regulatory restrictions, or tax laws, and

|

|

•

|

changes in interest rates or availability of financing.

|

All of these factors could result in decreases in market rental rates and increases in vacancy rates, which could adversely affect NNN’s results of operations.

NNN’s real estate investments are illiquid.

Because real estate investments are relatively illiquid, NNN’s ability to adjust the portfolio promptly in response to economic or other conditions is limited. Certain significant expenditures generally do not change in response to economic or other conditions, including: (i) debt service (if any), (ii) real estate taxes, and (iii) operating and maintenance costs. This combination of variable revenue and relatively fixed expenditures may result, under certain market conditions, in reduced earnings and could have an adverse effect on NNN’s financial condition.

Costs of complying with changes in governmental laws and regulations may adversely affect NNN’s results of operations.

NNN cannot predict what laws or regulations will be enacted in the future, how future laws or regulations will be administered or interpreted, or how future laws or regulations will affect NNN or its Properties, including, but not limited to environmental laws and regulations. Compliance with new laws or regulations, or stricter interpretation of existing laws, may require NNN, its retail tenants, or consumers to incur significant expenditures, impose significant liability, restrict or prohibit business activities and could cause a material adverse effect on NNN’s results of operation.

NNN may be subject to known or unknown environmental liabilities and hazardous materials on Properties owned by NNN.

There may be known or unknown environmental liabilities associated with Properties owned or acquired in the future by NNN. Certain particular uses of some Properties may also have a heightened risk of environmental liability because of the hazardous materials used in performing services on those Properties, such as convenience stores with underground petroleum storage tanks or auto parts and auto service businesses using petroleum products, paint and machine solvents. Some of the Properties may contain asbestos or asbestos-containing materials, or may contain or may develop mold or other bio-contaminants. Asbestos-containing materials must be handled, managed and removed in accordance with applicable governmental laws, rules and regulations. Mold and other bio-contaminants can produce airborne toxins, may cause a variety of health issues in individuals and must be remediated in accordance with applicable governmental laws, rules and regulations.

As part of its due diligence process, NNN generally obtains an environmental site assessment for each Property it acquires. In cases where NNN intends to acquire real estate where evidence of some level of known contamination may exist, NNN generally requires the seller or tenant to (i) remediate the contamination in accordance with applicable laws, rules and regulations, (ii) indemnify NNN for environmental liabilities, and/or (iii) agree to other arrangements deemed appropriate by NNN, including, under certain circumstances, the purchase of environmental insurance. Although sellers or tenants may be contractually responsible for remediating hazardous materials on a property and may be responsible for indemnifying NNN for any liability resulting from the use of a Property and for any failure to comply with any applicable environmental laws, rules or regulations, NNN has no assurance that sellers or tenants shall be able to meet their remediation and indemnity obligations to NNN. A tenant or seller may not have the financial ability to meet its remediation and indemnity obligations to NNN when required. Furthermore, NNN may have strict liability to governmental agencies or

8

third parties as a result of the existence of hazardous materials on Properties, whether or not NNN knew about or caused such hazardous materials to exist.

As of

February 6, 2018

, NNN has

77

Properties currently under some level of environmental remediation and/or monitoring. In general, the seller, a previous owner, the tenant or an adjacent land owner is responsible for the cost of the environmental remediation for each of these Properties.

If NNN is responsible for hazardous materials located on its Properties, NNN’s liability may include investigation and remediation costs, property damage to third parties, personal injury to third parties, and governmental fines and penalties. Furthermore, the presence of hazardous materials on a Property may adversely impact the Property value or NNN’s ability to sell the Property. Significant environmental liability could impact NNN’s results of operations, ability to make distributions to stockholders, and its ability to meet its debt obligations.

In order to mitigate exposure to environmental liability, NNN maintains an environmental insurance policy which provides some coverage for substantially all of its Properties. That policy expires in August 2018. However, the policy is subject to exclusions and limitations and does not cover all of the Properties owned by NNN. For those Properties covered under the policy, insurance may not fully compensate NNN for any environmental liability. NNN has no assurance that the insurer on its environmental insurance policy will be able to meet its obligations under the policy. NNN may not desire to renew the environmental insurance policy in place upon expiration or a replacement policy may not be available at a reasonable cost, if at all.

NNN may not be able to successfully execute its acquisition or development strategies.

NNN may not be able to implement its investment strategies successfully. Additionally, NNN cannot assure that its Property Portfolio will expand at all, or if it will expand at any specified rate or to any specified size. In addition, investment in additional real estate assets is subject to a number of risks. Because NNN expects to invest in markets other than the ones in which its current Properties are located or properties which may be leased to tenants other than those to which NNN has historically leased properties, NNN will also be subject to the risks associated with investment in new markets, new lines of trade or with new tenants that may be relatively unfamiliar to NNN’s management team.

NNN’s development activities are subject to, without limitation, risks relating to the availability and timely receipt of zoning and other regulatory approvals, the cost and timely completion of construction (including risks from factors beyond NNN’s control, such as weather or labor conditions or material shortages), the risk of finding tenants for the properties and the ability to obtain both construction and permanent financing on favorable terms. These risks could result in substantial unanticipated delays or expenses and, under certain circumstances, could prevent completion of development activities once undertaken or provide a tenant the opportunity to reduce rent or terminate a lease. Any of these situations may delay or eliminate proceeds or cash flows NNN expects from these projects, which could have an adverse effect on NNN’s financial condition.

NNN may not be able to dispose of properties consistent with its operating strategy.

NNN may be unable to sell Properties targeted for disposition due to adverse market conditions or possible prohibitive income tax liability. This may adversely affect, among other things, NNN’s ability to sell under favorable terms, execute its operating strategy, achieve target earnings or returns, retire or repay debt or pay dividends.

NNN may suffer a loss in the event of a default of or bankruptcy of a tenant or a borrower.

As of

December 31, 2017

, NNN had

no

outstanding mortgages and notes receivable. If a borrower defaults on a mortgage or other loan made by NNN, and does not have sufficient assets to satisfy the loan, NNN may suffer a loss of principal and interest. In the event of the bankruptcy of a borrower, NNN may not be able to recover against all or any of the assets of the borrower, or the collateral may not be sufficient to satisfy the balance due on the loan. In addition, certain of NNN’s loans may be subordinate to other debt of a borrower. These investments are typically loans secured by a borrower’s pledge of its ownership interests in the entity that owns the real estate or other assets and are typically subordinated to senior loans encumbering the underlying real estate or assets. Subordinated positions are generally subject to a higher risk of nonpayment of principal and interest than the more senior loans. If a borrower defaults on the debt senior to NNN’s loan, or in the event of the bankruptcy of a borrower, NNN’s loan will be satisfied only after the borrower’s senior creditors’ claims are satisfied. Where debt senior to NNN’s loans exists, the presence of intercreditor arrangements may limit NNN’s ability to amend loan documents, assign the loans, accept prepayments, exercise remedies and control decisions made in bankruptcy proceedings relating to borrowers. Bankruptcy proceedings and litigation can significantly increase the time

9

needed for NNN to acquire underlying collateral, if any, in the event of a default, during which time the collateral may decline in value. In addition, there are significant costs and delays associated with the foreclosure process.

Certain provisions of NNN’s leases or loan agreements may be unenforceable.

NNN’s rights and obligations with respect to its leases, mortgage loans or other loans are governed by written agreements. A court could determine that one or more provisions of such an agreement are unenforceable, such as a particular remedy, a master lease covenant, a loan prepayment provision or a provision governing NNN’s security interest in the underlying collateral of a borrower or lessee. NNN could be adversely impacted if this were to happen with respect to an asset or group of assets.

Property ownership through joint ventures and partnerships could limit NNN’s control of those investments.

Joint ventures or partnerships involve risks not otherwise present for direct investments by NNN. It is possible that NNN’s co-venturers or partners may have different interests or goals than NNN at any time and they may take actions contrary to NNN’s requests, policies or objectives, including NNN’s policy with respect to maintaining its qualification as a REIT. Other risks of joint venture or partnership investments include impasses on decisions because in some instances no single co-venturer or partner has full control over the joint venture or partnership, respectively, or the co-venturer or partner may become insolvent, bankrupt or otherwise unable to contribute to the joint venture or partnership, respectively. Further, disputes may develop with a co-venturer or partner over decisions affecting the property, joint venture or partnership that may result in litigation, arbitration or some other form of dispute resolution.

Competition from numerous other REITs, commercial developers, real estate limited partnerships and other investors may impede NNN’s ability to grow.

NNN may not complete suitable property acquisitions or developments on advantageous terms, if at all, due to competition for such properties with others engaged in real estate investment activities or lack of properties for sale on terms deemed acceptable to NNN. NNN’s inability to successfully acquire or develop new properties may affect NNN’s ability to achieve anticipated return on investment or realize its investment strategy, which could have an adverse effect on its results of operations.

NNN's loss of key management personnel could adversely affect performance and the value of its securities.

NNN is dependent on the efforts of its key management. Competition for senior management personnel can be intense and NNN may not be able to retain its key management. Although NNN believes qualified replacements could be found for any departures of key management, the loss of their services could adversely affect NNN's performance and the value of its securities.

Uninsured losses may adversely affect NNN’s operating results and asset values.

The Properties are generally covered by comprehensive liability, fire, and extended insurance coverage. NNN believes that the insurance carried on its Properties is adequate and in accordance with industry standards. There are, however, types of losses (such as from hurricanes, floods, earthquakes or other types of natural disasters or wars or other acts of violence) which may be uninsurable, self-insured by tenants, or the cost of insuring against these losses may not be economically justifiable in the opinion of tenants or NNN. If an uninsured loss occurs or a loss exceeds policy limits, NNN could lose both its invested capital and anticipated revenues from the property, thereby reducing NNN’s cash flow and asset value.

Acts of violence, terrorist attacks or war may affect the markets in which NNN operates and NNN’s results of operations.

Terrorist attacks or other acts of violence may negatively affect NNN’s operations. There can be no assurance that there will not be terrorist attacks against businesses within the United States. These attacks may directly or indirectly impact NNN’s physical facilities or the businesses or the financial condition of its tenants, developers, borrowers, lenders or financial institutions with which NNN has a relationship. The United States is engaged in armed conflict, which could have an impact on these parties. The consequences of armed conflict are unpredictable, and NNN may not be able to foresee events that could have an adverse effect on its business or be insured for such.

More generally, any of these events or threats of these events could cause consumer confidence and spending to decrease or result in increased volatility in the United States and worldwide financial markets and economies. They also could result in,

10

or cause a deepening of, economic recession in the United States or abroad. Any of these occurrences could have an adverse impact on NNN’s financial condition or results of operations.

Vacant properties or bankrupt tenants or borrowers could adversely affect NNN’s business or financial condition.

As of

December 31, 2017

, NNN owned

24

vacant, un-leased Properties, which accounted for approximately

one

percent of total Properties held in the Property Portfolio. NNN is actively marketing these Properties for sale or lease but may not be able to sell or lease these Properties on favorable terms or at all. The lost revenues and increased property expenses resulting from the rejection by any bankrupt tenant of any of their respective leases with NNN could have a material adverse effect on the liquidity and results of operations of NNN if NNN is unable to re-lease the Properties at comparable rental rates and in a timely manner. As of

January 31, 2018

, less than

one

percent of total Properties held in the Property Portfolio was leased to two tenants that each filed a petition for bankruptcy under Chapter 11 of the U.S. Bankruptcy Code. As a result, these tenants have the right to reject or affirm their leases with NNN.

The amount of debt NNN has and the restrictions imposed by that debt could adversely affect NNN’s business and financial condition.

As of

December 31, 2017

, NNN had outstanding debt including mortgages payable of

$13,300,000

, total unsecured notes payable of

$2,446,407,000

and

$120,500,000

outstanding on the Credit Facility. NNN’s organizational documents do not limit the level or amount of debt that it may incur. If NNN incurs additional indebtedness and permits a higher degree of leverage, debt service requirements would increase and could adversely affect NNN’s financial condition and results of operations, as well as NNN’s ability to pay principal and interest on the outstanding indebtedness or cash dividends to its stockholders. In addition, increased leverage could increase the risk that NNN may default on its debt obligations.

The amount of debt outstanding at any time could have important consequences to NNN’s stockholders. For example, it could:

|

•

|

require NNN to dedicate a substantial portion of its cash flow from operations to payments on its debt, thereby reducing funds available for operations, real estate investments and other business opportunities that may arise in the future,

|

|

•

|

increase NNN’s vulnerability to general adverse economic and industry conditions,

|

|

•

|

limit NNN’s ability to obtain any additional financing it may need in the future for working capital, debt refinancing, capital expenditures, real estate investments, development or other general corporate purposes,

|

|

•

|

make it difficult to satisfy NNN’s debt service requirements,

|

|

•

|

limit NNN’s ability to pay dividends in cash on its outstanding common and preferred stock,

|

|

•

|

limit NNN’s flexibility in planning for, or reacting to, changes in its business and the factors that affect the profitability of its business, and

|

|

•

|

limit NNN’s flexibility in conducting its business, which may place NNN at a disadvantage compared to competitors with less debt or debt with less restrictive terms.

|

NNN’s ability to make scheduled payments of principal or interest on its debt, or to retire or refinance such debt will depend primarily on its future performance, which to a certain extent is subject to the creditworthiness of its tenants, competition, and economic, financial, and other factors beyond its control. There can be no assurance that NNN’s business will continue to generate sufficient cash flow from operations in the future to service its debt or meet its other cash needs. If NNN is unable to generate sufficient cash flow from its business, it may be required to refinance all or a portion of its existing debt, sell assets or obtain additional financing to meet its debt obligations and other cash needs.

NNN cannot assure stockholders that any such refinancing, sale of assets or additional financing would be possible or, if possible, on terms and conditions, including but not limited to the interest rate, which NNN would find acceptable or would not result in a material decline in earnings.

11

NNN is obligated to comply with financial and other covenants in its debt instruments that could restrict its operating activities, and the failure to comply with such covenants could result in defaults that accelerate the payment of such debt.

As of

December 31, 2017

, NNN had approximately

$2,580,207,000

of outstanding indebtedness, of which approximately

$13,300,000

was secured indebtedness. NNN’s unsecured debt instruments contain various restrictive covenants which include, among others, provisions restricting NNN’s ability to:

|

•

|

incur or guarantee additional debt,

|

|

•

|

make certain distributions, investments and other restricted payments,

|

|

•

|

enter into transactions with certain affiliates,

|

|

•

|

create certain liens,

|

|

•

|

consolidate, merge or sell NNN’s assets, and

|

|

•

|

pre-pay debt.

|

NNN’s secured debt instruments generally contain customary covenants, including, among others, provisions:

|

•

|

requiring the maintenance of the property securing the debt,

|

|

•

|

restricting its ability to sell, assign or further encumber the properties securing the debt,

|

|

•

|

restricting its ability to incur additional debt on the property securing the debt,

|

|

•

|

restricting modifications to property improvements,

|

|

•

|

restricting its ability to amend or modify existing leases on the property securing the debt, and

|

|

•

|

establishing certain prepayment restrictions.

|

In addition, NNN’s debt instruments may contain cross-default provisions, in which case a default of NNN under one debt instrument will be a default of NNN under multiple or all debt instruments of NNN.

NNN’s ability to meet some of its debt covenants, including covenants related to the condition of the property or payment of real estate taxes, may be dependent on the performance by NNN’s tenants under their leases.

In addition, certain covenants in NNN’s debt instruments, including its Credit Facility, require NNN, among other things, to:

|

•

|

limit certain leverage ratios,

|

|

•

|

maintain certain minimum interest and debt service coverage ratios, and

|

|

•

|

limit investments in certain types of assets.

|

NNN’s failure to comply with certain of its debt covenants could result in defaults that accelerate the payment under such debt and limit the dividends paid to NNN’s common and preferred stockholders which would likely have a material adverse impact on NNN’s financial condition and results of operations. In addition, these defaults could impair its access to the debt and equity markets.

The market value of NNN’s equity and debt securities is subject to various factors that may cause significant fluctuations or volatility.

As with other publicly traded securities, the market price of NNN’s equity and debt securities depends on various factors, which may change from time-to-time and/or may be unrelated to NNN’s financial condition, operating performance or prospects that may cause significant fluctuations or volatility in such prices. These factors, among others, include:

|

•

|

general economic and financial market conditions,

|

|

•

|

level and trend of interest rates,

|

|

•

|

changes in government taxation or regulatory authorities,

|

|

•

|

NNN’s ability to access the capital markets to raise additional capital,

|

|

•

|

the issuance of additional equity or debt securities,

|

|

•

|

changes in NNN’s funds from operations or earnings estimates,

|

|

•

|

changes in NNN’s debt ratings or analyst ratings,

|

|

•

|

NNN’s financial condition and performance,

|

|

•

|

market perception of NNN compared to other REITs, and

|

12

|

•

|

market perception of REITs compared to other investment sectors.

|

NNN’s failure to qualify as a REIT for federal income tax purposes could result in significant tax liability.

NNN intends to operate in a manner that will allow NNN to continue to qualify as a REIT. NNN believes it has been organized as, and its past and present operations qualify NNN as a REIT. However, the Internal Revenue Service (“IRS”) could successfully assert that NNN is not qualified as such. In addition, NNN may not remain qualified as a REIT in the future. Qualification as a REIT involves the application of highly technical and complex provisions of the Internal Revenue Code of 1986, as amended (the “Code”) for which there are only limited judicial or administrative interpretations and involves the determination of various factual matters and circumstances not entirely within NNN’s control. Furthermore, new tax legislation, administrative guidance or court decisions, in each instance potentially with retroactive effect, could make it more difficult or impossible for NNN to qualify as a REIT or avoid significant tax liability.

If NNN fails to qualify as a REIT, it would not be allowed a deduction for dividends paid to stockholders in computing taxable income and would become subject to federal income tax at regular corporate rates. In this event, NNN could be subject to potentially significant tax liabilities and penalties. Unless entitled to relief under certain statutory provisions, NNN would also be disqualified from treatment as a REIT for the four taxable years following the year during which the qualification was lost.

Even if NNN remains qualified as a REIT, NNN faces other tax liabilities that reduce operating results and cash flow.

Even if NNN remains qualified for taxation as a REIT, NNN is subject to certain federal, state and local taxes on its income and assets, including taxes on any undistributed income, tax on income from some activities conducted as a result of a foreclosure, and state or local income, property and transfer taxes. Any increase of these taxes would decrease earnings and cash available for distribution to stockholders. In addition, in order to meet certain REIT qualification requirements, NNN has owned some of its assets in the TRS.

Adverse legislative or regulatory tax changes could reduce NNN’s earnings and cash flow and the market value of NNN’s securities.

At any time, the federal and state income tax laws or the administrative interpretations of those laws may change. Any such changes may have current and retroactive effects, and could adversely affect NNN or its stockholders. Legislation could cause shares in non-REIT corporations to be a more attractive investment to individual investors than shares in REITs, and could have an adverse effect on the value of NNN’s securities.

Compliance with REIT requirements, including distribution requirements, may limit NNN’s flexibility and may negatively affect NNN’s operating decisions.

To maintain its status as a REIT for U.S. federal income tax purposes, NNN must meet certain requirements on an on-going basis, including requirements regarding its sources of income, the nature and diversification of its assets, the amounts NNN distributes to its stockholders and the ownership of its shares. NNN may also be required to make distributions to its stockholders when it does not have funds readily available for distribution or at times when NNN’s funds are otherwise needed to fund expenditures or debt service requirements. NNN generally will not be subject to federal income taxes on amounts distributed to stockholders, so long as it distributes 100 percent of its REIT taxable income and meets certain other requirements for qualifying as a REIT. For each of the years in the three-year period ended

December 31, 2017

, NNN believes it has qualified as a REIT. Notwithstanding NNN’s qualification for taxation as a REIT, NNN is subject to certain state taxes on its income and real estate.

Changes in accounting pronouncements could adversely impact NNN’s or NNN’s tenants’ reported financial performance.

Accounting policies and methods are fundamental to how NNN records and reports its financial condition and results of operations. From time to time the Financial Accounting Standards Board (“FASB”) and the Commission, who create and interpret appropriate accounting standards, may change the financial accounting and reporting standards or their interpretation and application of these standards that govern the preparation of NNN’s financial statements. These changes could have a material impact on NNN’s reported financial condition and results of operations. In some cases, NNN could be required to apply a new or revised standard retroactively, resulting in restating prior period financial statements. Similarly, these changes could have a material impact on NNN’s tenants’ reported financial condition or results of operations and affect their preferences regarding leasing real estate.

13

NNN’s failure to maintain effective internal control over financial reporting could have a material adverse effect on its business, operating results and the market value of NNN's securities.

Section 404 of the Sarbanes-Oxley Act of 2002 requires annual management assessments of the effectiveness of the Company’s internal control over financial reporting. If NNN fails to maintain the adequacy of its internal control over financial reporting, as such standards may be modified, supplemented or amended from time to time, NNN may not be able to ensure that it can conclude on an ongoing basis that it has effective internal control over financial reporting in accordance with Section 404 of the Sarbanes-Oxley Act of 2002. Moreover, effective internal control over financial reporting, particularly those related to revenue recognition, are necessary for NNN to produce reliable financial reports and to maintain its qualification as a REIT and are important in helping to prevent financial fraud. If NNN cannot provide reliable financial reports or prevent fraud, its business and operating results could be harmed, REIT qualification could be jeopardized, investors could lose confidence in the Company’s reported financial information, the company's access to capital could be impaired, and the trading price of NNN’s shares could drop significantly.

NNN’s ability to pay dividends in the future is subject to many factors.

NNN’s ability to pay dividends may be impaired if any of the risks described in this section were to occur. In addition, payment of NNN’s dividends depends upon NNN’s earnings, financial condition, maintenance of NNN’s REIT status and other factors as NNN’s Board of Directors may deem relevant from time to time.

Cybersecurity risks and cyber incidents could adversely affect NNN's business, disrupt operations and expose NNN to liabilities to tenants, employees, capital providers, and other third parties.

Cyber incidents can result from deliberate attacks or unintentional events. These incidents can include, but are not limited to, gaining unauthorized access to digital systems for purposes of misappropriating assets or sensitive information, corrupting data, or causing operational disruption. The result of these incidents could include, but are not limited to, disrupted operations, misstated financial data, liability for stolen assets or information, increased cybersecurity protection costs, litigation and reputational damage adversely affecting customer or investor confidence. These cyber incidents could negatively impact NNN, NNN's tenants and/or the capital markets.

Future investment in international markets could subject NNN to additional risks.

If NNN expands its operating strategy to include investment in international markets, NNN could face additional risks, including foreign currency exchange rate fluctuations, operational risks due to local economic and political conditions and laws and policies of the U.S. affecting foreign investment.

|

Item 1B.

|

Unresolved Staff Comments

|

None.

|

Item 2.

|

Properties

|

Please refer to Item 1. “Business.”

|

Item 3.

|

Legal Proceedings

|

In the ordinary course of its business, NNN is a party to various legal actions that management believes are routine in nature and incidental to the operation of the business of NNN. Management does not believe that any of these proceedings are material.

|

Item 4.

|

Mine Safety Disclosures

|

None.

14

|

Item 5.

|

Market for Registrant’s Common Equity, Related Stockholder Matters and Issuer Purchases of Equity Securities

|

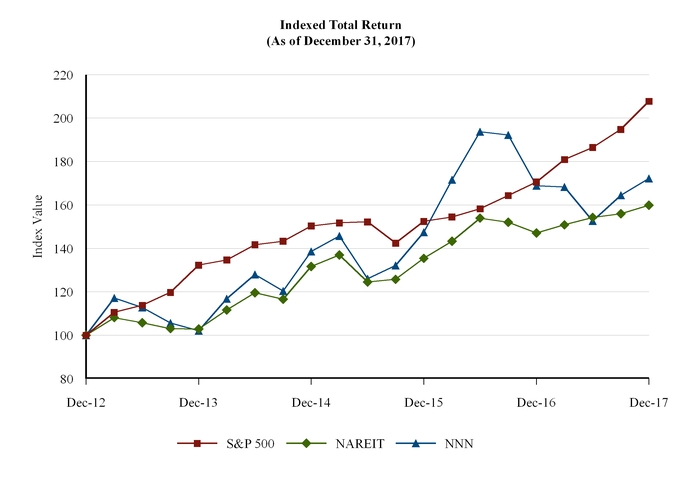

The common stock of NNN currently is traded on the NYSE under the symbol “NNN.” Set forth below is a line graph comparing the cumulative total stockholder return on NNN’s common stock, based on the market price of the common stock and assuming reinvestment of dividends, with the FTSE National Association of Real Estate Investment Trusts Equity Index (“NAREIT”) and the S&P 500 Index (“S&P”) for the five-year period commencing

December 31, 2012

and ending

December 31, 2017

. The graph assumes an investment of $100 on

December 31, 2012

.

Comparison to Five-Year Cumulative Total Return

15

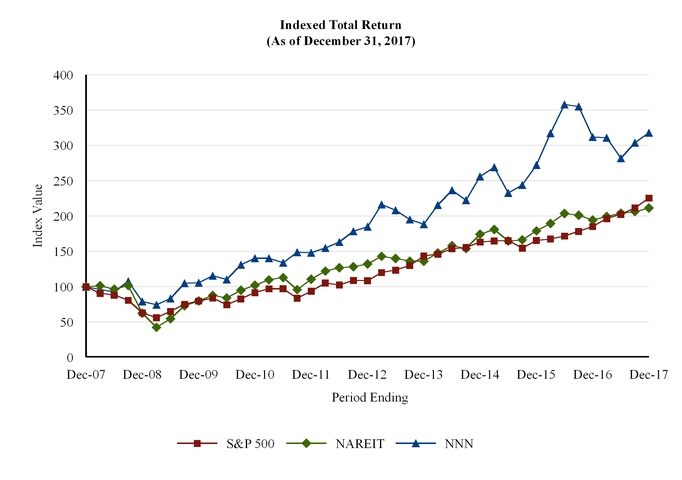

Set forth below is a line graph comparing the cumulative total stockholder return on NNN’s common stock, based on the market price of the common stock and assuming reinvestment of dividends, with the FTSE National Association of Real Estate Investment Trusts Equity Index (“NAREIT”) and the S&P 500 Index (“S&P”) for the ten-year period commencing December 31, 2007 and ending

December 31, 2017

. The graph assumes an investment of $100 on December 31, 2007.

Comparison to Ten-Year Cumulative Total Return

16

For each calendar quarter and year indicated, the following table reflects respective high, low and closing sales prices for the common stock as quoted by the NYSE and the dividends paid per share in each such period.

|

2017

|

First

Quarter

|

Second

Quarter

|

Third

Quarter

|

Fourth

Quarter

|

Year

|

|||||||||||||||

|

High

|

$

|

46.34

|

|

$

|

45.63

|

|

$

|

43.41

|

|

$

|

43.90

|

|

$

|

46.34

|

|

|||||

|

Low

|

41.91

|

|

36.45

|

|

37.45

|

|

38.97

|

|

36.45

|

|

||||||||||

|

Close

|

43.62

|

|

39.10

|

|

41.66

|

|

43.13

|

|

43.13

|

|

||||||||||

|

Dividends paid per share

|

0.455

|

|

0.455

|

|

0.475

|

|

0.475

|

|

1.860

|

|

||||||||||

|

2016

|

|

|

|

|

|

|||||||||||||||

|

High

|

$

|

46.86

|

|

$

|

51.72

|

|

$

|

53.60

|

|

$

|

51.26

|

|

$

|

53.60

|

|

|||||

|

Low

|

38.29

|

|

43.52

|

|

47.76

|

|

39.86

|

|

38.29

|

|

||||||||||

|

Close

|

46.20

|

|

51.72

|

|

50.85

|

|

44.20

|

|

44.20

|

|

||||||||||

|

Dividends paid per share

|

0.435

|

|

0.435

|

|

0.455

|

|

0.455

|

|

1.780

|

|

||||||||||

The following table presents the characterizations for tax purposes of such common stock dividends for the years ended December 31:

|

|

2017

|

2016

|

|||||||||||

|

Ordinary dividends

|

$

|

1.559781

|

|

83.8592

|

%

|

$

|

1.513705

|

|

85.0396

|

%

|

|||

|

Capital gain

|

0.035041

|

|

1.8839

|

%

|

—

|

|

—

|

|

|||||

|

Unrecaptured Section 1250 Gain

|

0.012194

|

|

0.6556

|

%

|

—

|

|

—

|

|

|||||

|

Nontaxable distributions

|

0.252984

|

|

13.6013

|

%

|

0.266295

|

|

14.9604

|

%

|

|||||

|

$

|

1.860000

|

|

100.0000

|

%

|

$

|

1.780000

|

|

100.0000

|

%

|

||||

NNN intends to pay regular quarterly dividends to its stockholders, although all future distributions will be declared and paid at the discretion of the Board of Directors and will depend upon cash generated by operating activities, NNN’s financial condition, capital requirements, annual distribution requirements under the REIT provisions of the Code and such other factors as the Board of Directors deems relevant.

In January 2018

, NNN declared dividends payable to its stockholders of

$72,733,000

, or

$0.475

per share, of common stock.

On January 31, 2018, there were 1,767 registered holders of record of NNN's common stock.

17

|

Item 6.

|

Selected Financial Data

|

Historical Financial Highlights

(dollars in thousands, except per share data)

|

2017

|

2016

|

2015

|

2014

|

2013

|

|||||||||||||||

|

Gross revenues

(1)

|

$

|

585,255

|

|

$

|

533,817

|

|

$

|

483,025

|

|

$

|

435,278

|

|

$

|

397,008

|

|

||||

|

Earnings from continuing operations

|

228,716

|

|

212,324

|

|

187,511

|

|

179,777

|

|

154,006

|

|

|||||||||

|

Net earnings

|

265,371

|

|

239,506

|

|

197,961

|

|

191,170

|

|

160,085

|

|

|||||||||

|

Net earnings attributable to NNN

|

264,973

|

|

239,500

|

|

197,836

|

|

190,601

|

|

160,145

|

|

|||||||||

|

Total assets

|

6,560,534

|

|

6,334,151

|

|

5,460,044

|

|

4,915,551

|

|

4,445,308

|

|

|||||||||

|

Total debt

|

2,580,207

|

|

2,311,689

|

|

1,975,944

|

|

1,729,891

|

|

1,560,844

|

|

|||||||||

|

Total stockholders’ equity of NNN

|

3,840,593

|

|

3,916,799

|

|

3,342,134

|

|

3,082,515

|

|

2,777,045

|

|

|||||||||

|

Cash dividends declared to:

|

|||||||||||||||||||

|

Common stockholders

|

277,120

|

|

257,007

|

|

228,699

|

|

204,157

|

|

189,107

|

|

|||||||||

|

Series D preferred stockholders

|

3,598

|

|

19,047

|

|

19,047

|

|

19,047

|

|

19,047

|

|

|||||||||

|

Series E preferred stockholders

|

16,387

|

|

16,387

|

|

16,387

|

|

16,387

|

|

8,876

|

|

|||||||||

|

Series F preferred stockholders

|

17,940

|

|

3,189

|

|

—

|

|

—

|

|

—

|

|

|||||||||

|

Weighted average common shares:

|

|||||||||||||||||||

|

Basic

|

149,111,188

|

|

144,176,224

|

|

133,998,674

|

|

124,257,558

|

|

118,204,148

|

|

|||||||||

|

Diluted

|

149,432,641

|

|

144,660,633

|

|

134,489,416

|

|

124,710,226

|

|

119,864,824

|

|

|||||||||

|

Per share information:

|

|||||||||||||||||||

|

Earnings from continuing operations:

|

|||||||||||||||||||

|

Basic

|

$

|

1.45

|

|

$

|

1.39

|

|

$

|

1.21

|

|

$

|