|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

_____________________________________________________

FORM 10-Q

(Mark One)

|

☑ |

QUARTERLY REPORT PURSUANT TO SECTION 13 OR 15(D) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the quarterly period ended : September 30, 2019

OR

|

☐ |

TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(D) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the transition period from ___________ to ___________

Commission file number 1-8625

READING INTERNATIONAL, INC.

(Exact name of Registrant as specified in its charter)

|

NEVADA (State or other jurisdiction of incorporation or organization) |

95-3885184 (IRS Employer Identification No.) |

|

5995 Sepulveda Boulevard, Suite 300 Culver City, CA (Address of principal executive offices) |

90230 (Zip Code) |

Registrant’s telephone number, including area code: (213) 235-2240

Securities registered pursuant to Section 12(b) of the Act:

|

|

|

|

|

|

|

Title of each class |

|

Trading Symbol(s) |

|

Name of each exchange on which registered |

|

Class A Common Stock, $0.01 par value |

|

RDI |

|

The Nasdaq Stock Market LLC |

|

Class B Common Stock, $0.01 par value |

|

RDIB |

|

The Nasdaq Stock Market LLC |

Indicate by check mark whether the registrant: (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding twelve months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes ☑ No ☐

Indicate by check mark whether the registrant has submitted electronically every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T (§ 232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files). Yes ☑ No ☐

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, smaller reporting company, or an emerging growth company. See definitions of “large accelerated filer”, “accelerated filer”, “smaller reporting company,” and “emerging growth company” in Rule 12b-2 of the Exchange Act.

Large accelerated filer ☐ Accelerated filer ☑ Non-accelerated filer ☐ Smaller reporting company ☐ Emerging growth company ☐

If an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided pursuant to Section 13(a) of the Exchange Act. ☐

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act). Yes ☐ No ☑

Indicate the number of shares outstanding of each of the issuer’s classes of common stock, as of the latest practicable date. As of November 8, 2019 there were 20,404,573 shares of Class A Nonvoting Common Stock, $0.01 par value per share and 1,680,590 shares of Class B Voting Common Stock, $0.01 par value per share outstanding.

1

READING INTERNATIONAL , INC. AND SUBSIDIARIES

TABLE OF CONTENTS

|

|

Page |

| 3 | |

| 3 | |

| 3 | |

| 4 | |

|

Consolidated Statements of Comprehensive Income (Unaudited) |

5 |

| 6 | |

| 7 | |

|

Item 2 – Management’s Discussion and Analysis of Financial Condition and Results of Operations |

31 |

|

Item 3 – Quantitative and Qualitative Disclosure about Market Risk |

48 |

| 49 | |

| 50 | |

| 50 | |

| 51 | |

|

Item 2 – Unregistered Sales of Equity Securities and Use of Proceeds |

51 |

| 51 | |

| 51 | |

| 51 | |

| 53 | |

|

Certifications |

|

2

PART 1 – FINANCIAL INFORMATION

READING INTERNATIONAL, INC.

(U.S. dollars in thousands, except share information)

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

September 30, |

|

December 31, |

||

|

|

|

2019 |

|

2018 |

||

|

ASSETS |

|

(unaudited) |

|

|

|

|

|

Current Assets: |

|

|

|

|

|

|

|

Cash and cash equivalents |

|

$ |

8,708 |

|

$ |

13,127 |

|

Receivables |

|

|

4,363 |

|

|

8,045 |

|

Inventory |

|

|

1,195 |

|

|

1,419 |

|

Prepaid and other current assets |

|

|

10,831 |

|

|

7,667 |

|

Total current assets |

|

|

25,097 |

|

|

30,258 |

|

Operating property, net |

|

|

248,100 |

|

|

257,667 |

|

Operating lease right-of-use assets |

|

|

216,963 |

|

|

— |

|

Investment and development property, net |

|

|

107,292 |

|

|

86,804 |

|

Investment in unconsolidated joint ventures |

|

|

4,721 |

|

|

5,121 |

|

Goodwill |

|

|

19,913 |

|

|

19,445 |

|

Intangible assets, net |

|

|

3,607 |

|

|

7,369 |

|

Deferred tax asset, net |

|

|

25,959 |

|

|

26,235 |

|

Other assets |

|

|

6,164 |

|

|

6,129 |

|

Total assets |

|

$ |

657,816 |

|

$ |

439,028 |

|

LIABILITIES AND STOCKHOLDERS' EQUITY |

|

|

|

|

|

|

|

Current Liabilities: |

|

|

|

|

|

|

|

Accounts payable and accrued liabilities |

|

$ |

24,318 |

|

$ |

26,154 |

|

Film rent payable |

|

|

6,430 |

|

|

8,661 |

|

Debt - current portion |

|

|

34,374 |

|

|

30,393 |

|

Derivative financial instruments - current portion |

|

|

105 |

|

|

41 |

|

Taxes payable - current |

|

|

611 |

|

|

1,710 |

|

Deferred current revenue |

|

|

6,406 |

|

|

9,264 |

|

Operating lease liabilities - current portion |

|

|

19,579 |

|

|

— |

|

Other current liabilities |

|

|

9,339 |

|

|

9,305 |

|

Total current liabilities |

|

|

101,162 |

|

|

85,528 |

|

Debt - long-term portion |

|

|

131,681 |

|

|

106,286 |

|

Derivative financial instruments - non-current portion |

|

|

291 |

|

|

145 |

|

Subordinated debt, net |

|

|

26,255 |

|

|

26,061 |

|

Noncurrent tax liabilities |

|

|

11,647 |

|

|

11,530 |

|

Operating lease liabilities - non-current portion |

|

|

210,737 |

|

|

— |

|

Other liabilities |

|

|

12,330 |

|

|

28,931 |

|

Total liabilities |

|

|

494,103 |

|

|

258,481 |

|

Commitments and contingencies (Note 13) |

|

|

|

|

|

|

|

Stockholders’ equity: |

|

|

|

|

|

|

|

Class A non-voting common stock, par value $0.01 , 100,000,000 shares authorized, |

|

|

|

|

|

|

|

32,963,489 issued and 20,404,573 outstanding at September 30, 2019 and 33,112,337 issued and 21,194,748 outstanding at December 31, 2018 |

|

|

231 |

|

|

232 |

|

Class B voting common stock, par value $0.01 , 20,000,000 shares authorized and |

|

|

|

|

|

|

|

1,680,590 issued and outstanding at September 30, 2019 and December 31, 2018 |

|

|

17 |

|

|

17 |

|

Nonvoting preferred stock, par value $0.01 , 12,000 shares authorized and no issued |

|

|

|

|

|

|

|

or outstanding shares at September 30, 2019 and December 31, 2018 |

|

|

— |

|

|

— |

|

Additional paid-in capital |

|

|

148,236 |

|

|

147,452 |

|

Retained earnings |

|

|

48,859 |

|

|

47,616 |

|

Treasury shares |

|

|

(36,541) |

|

|

(25,222) |

|

Accumulated other comprehensive income |

|

|

(1,288) |

|

|

6,115 |

|

Total Reading International, Inc. stockholders’ equity |

|

|

159,514 |

|

|

176,210 |

|

Noncontrolling interests |

|

|

4,199 |

|

|

4,337 |

|

Total stockholders’ equity |

|

|

163,713 |

|

|

180,547 |

|

Total liabilities and stockholders’ equity |

|

$ |

657,816 |

|

$ |

439,028 |

See accompanying Notes to the Unaudited Consolidated Financial Statements.

3

READING INTERNATIONAL, INC.

CONSOLIDATED STATEMENTS OF INCOME

( Unaudited; U.S. dollars in thousands, except per share data)

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Quarter Ended |

|

Nine Months Ended |

||||||||

|

|

|

September 30, |

|

September 30, |

||||||||

|

|

|

2019 |

|

2018 |

|

2019 |

|

2018 |

||||

|

Revenue |

|

|

|

|

|

|

|

|

|

|

|

|

|

Cinema |

|

$ |

66,733 |

|

|

70,671 |

|

$ |

197,101 |

|

$ |

223,109 |

|

Real estate |

|

|

3,723 |

|

|

3,590 |

|

|

11,001 |

|

|

11,286 |

|

Total revenue |

|

|

70,456 |

|

|

74,261 |

|

|

208,102 |

|

|

234,395 |

|

Costs and expenses |

|

|

|

|

|

|

|

|

|

|

|

|

|

Cinema |

|

|

(53,709) |

|

|

(54,929) |

|

|

(158,273) |

|

|

(170,183) |

|

Real estate |

|

|

(2,225) |

|

|

(2,475) |

|

|

(7,108) |

|

|

(7,408) |

|

Depreciation and amortization |

|

|

(5,704) |

|

|

(5,829) |

|

|

(16,870) |

|

|

(16,705) |

|

General and administrative |

|

|

(5,908) |

|

|

(6,489) |

|

|

(18,426) |

|

|

(21,250) |

|

Total costs and expenses |

|

|

(67,546) |

|

|

(69,722) |

|

|

(200,677) |

|

|

(215,546) |

|

Operating income (loss) |

|

|

2,910 |

|

|

4,539 |

|

|

7,425 |

|

|

18,849 |

|

Interest expense, net |

|

|

(1,871) |

|

|

(1,748) |

|

|

(5,924) |

|

|

(5,132) |

|

Gain (loss) on sale of assets |

|

|

(1) |

|

|

— |

|

|

(1) |

|

|

— |

|

Other income (expense) |

|

|

141 |

|

|

(130) |

|

|

190 |

|

|

(273) |

|

Income (loss) before income tax expense and equity earnings of unconsolidated joint ventures |

|

|

1,179 |

|

|

2,661 |

|

|

1,690 |

|

|

13,444 |

|

Equity earnings of unconsolidated joint ventures |

|

|

220 |

|

|

80 |

|

|

581 |

|

|

667 |

|

Income (loss) before income taxes |

|

|

1,399 |

|

|

2,741 |

|

|

2,271 |

|

|

14,111 |

|

Income tax benefit (expense) |

|

|

(547) |

|

|

(1,482) |

|

|

(1,159) |

|

|

(4,618) |

|

Net income (loss) |

|

$ |

852 |

|

$ |

1,259 |

|

$ |

1,112 |

|

$ |

9,493 |

|

Less: net income (loss) attributable to noncontrolling interests |

|

|

(50) |

|

|

(38) |

|

|

(103) |

|

|

88 |

|

Net income (loss) attributable to Reading International, Inc. common shareholders |

|

$ |

902 |

|

$ |

1,297 |

|

$ |

1,215 |

|

$ |

9,405 |

|

Basic earnings (loss) per share attributable to Reading International, Inc. shareholders |

|

$ |

0.04 |

|

$ |

0.06 |

|

$ |

0.05 |

|

$ |

0.41 |

|

Diluted earnings (loss) per share attributable to Reading International, Inc. shareholders |

|

$ |

0.04 |

|

$ |

0.06 |

|

$ |

0.05 |

|

$ |

0.41 |

|

Weighted average number of shares outstanding–basic |

|

|

22,546,827 |

|

|

23,006,040 |

|

|

22,791,530 |

|

|

22,988,227 |

|

Weighted average number of shares outstanding–diluted |

|

|

22,688,230 |

|

|

23,197,924 |

|

|

22,952,838 |

|

|

23,185,021 |

See accompanying Notes to the Unaudited Consolidated Financial Statements .

4

READING INTERNATIONAL, INC.

C ONSOLIDATED STATEMENTS OF COMPREHENSIVE INCOME

( Unaudited; U.S. dollars in thousands)

|

|

||||||||||||

|

|

|

Quarter Ended |

|

Nine Months Ended |

||||||||

|

|

|

September 30, |

|

September 30, |

||||||||

|

|

|

2019 |

|

2018 |

|

2019 |

|

2018 |

||||

|

Net income (loss) |

|

$ |

852 |

|

$ |

1,259 |

|

$ |

1,112 |

|

$ |

9,493 |

|

Foreign currency translation gain (loss) |

|

|

(6,598) |

|

|

(3,547) |

|

|

(7,355) |

|

|

(12,318) |

|

Gain (loss) on cash flow hedges |

|

|

(20) |

|

|

— |

|

|

(211) |

|

|

— |

|

Other |

|

|

51 |

|

|

53 |

|

|

159 |

|

|

155 |

|

Comprehensive income (loss) |

|

|

(5,715) |

|

|

(2,235) |

|

|

(6,295) |

|

|

(2,670) |

|

Less: net income (loss) attributable to noncontrolling interests |

|

|

(50) |

|

|

(38) |

|

|

(103) |

|

|

88 |

|

Less: comprehensive income (loss) attributable to noncontrolling interests |

|

|

(2) |

|

|

(5) |

|

|

(2) |

|

|

(15) |

|

Comprehensive income (loss) attributable to Reading International, Inc. |

|

$ |

(5,663) |

|

|

(2,192) |

|

$ |

(6,190) |

|

$ |

(2,743) |

See accompanying Notes to the Unaudited Consolidated Financial Statements .

5

READING INTERNATIONAL, INC.

CON SOLIDATED STATEMENTS OF CASH FLOWS

( Unaudited; U.S. dollars in thousands)

|

|

||||||

|

|

Nine Months Ended |

|||||

|

|

September 30, |

|||||

|

|

2019 |

2018 |

||||

|

Operating Activities |

||||||

|

Net income (loss) |

$ |

1,112 |

$ |

9,493 | ||

|

Adjustments to reconcile net income (loss) to net cash provided by operating activities: |

||||||

|

Equity earnings of unconsolidated joint ventures |

(581) | (667) | ||||

|

Distributions of earnings from unconsolidated joint ventures |

760 | 532 | ||||

|

Amortization of operating leases |

15,719 |

— |

||||

|

Amortization of finance leases |

121 |

— |

||||

|

Change in operating lease liabilities |

(15,209) |

— |

||||

|

Interest on hedged derivatives |

1 |

— |

||||

|

Change in net deferred tax assets |

272 | (888) | ||||

|

Depreciation and amortization |

16,870 | 16,705 | ||||

|

Other amortization |

1,088 | 7 | ||||

|

Stock based compensation expense |

1,097 | 1,066 | ||||

|

Net changes in operating assets and liabilities: |

||||||

|

Receivables |

3,393 | 4,492 | ||||

|

Prepaid and other assets |

(4,757) | (545) | ||||

|

Payments for accrued pension |

(513) | (2,655) | ||||

|

Accounts payable and accrued expenses |

(3,165) | 411 | ||||

|

Film rent payable |

(2,129) | (6,366) | ||||

|

Taxes payable |

(1,091) | (877) | ||||

|

Deferred revenue and other liabilities |

(2,191) | (1,636) | ||||

|

Net cash provided by (used in) operating activities |

10,797 | 19,072 | ||||

|

Investing Activities |

||||||

|

Insurance recoveries relating to property damage and demolition costs |

168 |

— |

||||

|

Purchases of and additions to operating and investment properties |

(33,205) | (50,118) | ||||

|

Acquisition of business combinations |

(1,380) |

— |

||||

|

Change in restricted cash |

1,334 | (1,556) | ||||

|

Net cash provided by (used in) investing activities |

(33,083) | (51,674) | ||||

|

Financing Activities |

||||||

|

Repayment of long-term borrowings |

(31,692) | (29,546) | ||||

|

Repayment of finance lease principal |

(120) |

— |

||||

|

Proceeds from borrowings |

58,677 | 65,213 | ||||

|

Capitalized borrowing costs |

(502) |

— |

||||

|

Repurchase of Class A Nonvoting Common Stock |

(7,800) | (397) | ||||

|

(Cash paid) proceeds from the settlement of employee share transactions |

(315) | 340 | ||||

|

Noncontrolling interest contributions |

55 | 75 | ||||

|

Noncontrolling interest distributions |

(42) | (117) | ||||

|

Net cash provided by (used in) financing activities |

18,261 | 35,568 | ||||

|

Effect of exchange rate changes on cash and cash equivalents |

(394) | (920) | ||||

|

Net decrease in cash and cash equivalents |

(4,419) | 2,046 | ||||

|

Cash and cash equivalents at January 1 |

13,127 | 13,668 | ||||

|

Cash and cash equivalents at September 30 |

$ |

8,708 |

$ |

15,714 | ||

|

Supplemental Disclosures |

||||||

|

Interest paid |

$ |

8,134 |

$ |

5,762 | ||

|

Income taxes paid |

5,669 | 6,365 | ||||

|

Non-Cash Transactions |

||||||

|

Additions to operating and investing properties through accrued expenses |

5,768 | 2,911 | ||||

See accompanying Notes to the Unaudited Consolidated Financial Statements .

6

READING INTERNATIONAL, INC.

NOTES TO CONSOLIDATED FINANCIAL STATEMENTS (Unaudited)

Note 1 – Description of Business and Segment Reporting

The Company

Reading International, Inc., a Nevada corporation (“RDI” and collectively with our consolidated subsidiaries and corporate predecessors, the “Company”, “Reading” and “we”, “us”, or “our”), was incorporated in 1999. Our businesses consist primarily of:

|

|

· |

|

the operation, development and ownership of multiplex cinemas in the United States, Australia, and New Zealand; and, |

|

|

· |

|

the development, ownership, operation and/or rental of retail, commercial and live venue real estate assets in Australia, New Zealand, and the United States. |

Business Segments

Reported below are the operating segments of the Company for which separate financial information is available and evaluated regularly by the Chief Executive Officer, the chief operating decision-maker of the Company. As part of our real estate activities, we hold undeveloped land in urban and suburban centers in Australia, New Zealand, and the United States.

The table below summarizes the results of operations for each of our business segments for the quarter and nine months ended September 30, 2019 and 2018 , respectively. Operating expense includes costs associated with the day-to-day operations of the cinemas and the management of rental properties, including our live theater assets.

|

|

||||||||||||

|

|

Quarter Ended |

Nine Months Ended |

||||||||||

|

|

September 30, |

September 30, |

||||||||||

|

(Dollars in thousands) |

2019 |

2018 |

2019 |

2018 |

||||||||

|

Revenue: |

||||||||||||

|

Cinema exhibition |

$ |

66,733 |

$ |

70,671 |

$ |

197,101 |

$ |

223,109 | ||||

|

Real estate |

5,531 | 5,771 | 16,525 | 18,204 | ||||||||

|

Inter-segment elimination |

(1,808) | (2,181) | (5,524) | (6,918) | ||||||||

|

|

$ |

70,456 |

$ |

74,261 |

$ |

208,102 |

$ |

234,395 | ||||

|

Segment operating income (loss): |

||||||||||||

|

Cinema exhibition |

$ |

6,021 |

$ |

8,202 |

$ |

17,931 |

$ |

30,983 | ||||

|

Real estate |

1,485 | 1,260 | 3,987 | 4,896 | ||||||||

|

|

$ |

7,506 |

$ |

9,462 |

$ |

21,918 |

$ |

35,879 | ||||

A reconciliation of segment operating income to income before income taxes is as follows:

|

|

||||||||||||

|

|

Quarter Ended |

Nine Months Ended |

||||||||||

|

|

September 30, |

September 30, |

||||||||||

|

(Dollars in thousands) |

2019 |

2018 |

2019 |

2018 |

||||||||

|

Segment operating income (loss) |

$ |

7,506 |

$ |

9,462 |

$ |

21,918 |

$ |

35,879 | ||||

|

Unallocated corporate expense |

||||||||||||

|

Depreciation and amortization expense |

(103) | (92) | (288) | (313) | ||||||||

|

General and administrative expense |

(4,493) | (4,831) | (14,205) | (16,717) | ||||||||

|

Interest expense, net |

(1,871) | (1,748) | (5,924) | (5,132) | ||||||||

|

Equity earnings of unconsolidated joint ventures |

220 | 80 | 581 | 667 | ||||||||

|

Gain (loss) on sale of assets |

(1) |

— |

(1) |

— |

||||||||

|

Other income (expense) |

141 | (130) | 190 | (273) | ||||||||

|

Income (loss) before income tax expense |

$ |

1,399 |

$ |

2,741 |

$ |

2,271 |

$ |

14,111 | ||||

Note 2 – Summary of Significant Accounting Policies

Basis of Consolidation

The accompanying consolidated financial statements include the accounts of the Company’s wholly-owned subsidiaries as well as majority-owned subsidiaries that the Company controls, and should be read in conjunction with the Company’s Annual Report on Form 10-K as of and for the year ended December 31, 2018 (“ 2018 Form 10-K”). All significant intercompany balances and transactions have been eliminated on consolidation. These consolidated financial statements were prepared in accordance with accounting principles generally accepted in the United States of America (“U.S. GAAP”) for interim reporting with the instructions for Form 10-Q and Rule 10-01 of Regulation S-X of the Securities and Exchange Commission (“SEC”). As such, they do not include

7

all information and footnotes required by U.S. GAAP for complete financial statements. We believe that we have included all normal and recurring adjustments necessary for a fair presentation of the results for the interim period.

Operating results for the quarter and nine months ended September 30, 2019 are not necessarily indicative of the results that may be expected for the year ending December 31, 2019 .

Use of Estimates

The preparation of consolidated financial statements in conformity with U.S. GAAP requires management to make estimates and assumptions that affect the amounts reported in the consolidated financial statements and footnotes thereto. Significant estimates include (i) projections we make regarding the recoverability and impairment of our assets (including goodwill and intangibles), (ii) valuations of our derivative instruments, (iii) recoverability of our deferred tax assets, (iv) estimation of breakage and redemption experience rates, which drive how we recognize breakage on our gift card and gift certificates, and revenue from our customer loyalty program, and (v) allocation of insurance proceeds to various recoverable components. Actual results may differ from those estimates.

Recently Adopted and Issued Accounting Pronouncements

Adopted:

|

|

1) |

|

Accounting Standards Update (“ASU”) 2016-02 Leases: In February 2016, the Financial Accounting Standards Board (“FASB”) issued a new accounting standard, Accounting Standards Codification (“ ASC ”) 842 Leases , to increase transparency and comparability among organizations by requiring the recognition of right-of-use assets and lease liabilities on the balance sheet. Leases will be classified as either finance or operating, with classification affecting the pattern of expense recognition in the income statement. A modified retrospective transition approach is required for lessees with capital and operating leases existing at, or entered into after, the beginning of the earliest comparative period presented in the financial statements, with certain practical expedients available. |

On January 1, 2019, we adopted the new accounting standard ASC 842 Leases using the modified retrospective method. We recognized the cumulative effect of initially applying the new leasing standard as an adjustment to the opening balance of retained earnings. The comparative information has not been restated and continues to be reported under the accounting standards in effect for those periods. The standard had a material impact on our consolidated balance sheets, but not on our consolidated income statements or statements of cash flow.

|

(Dollars in thousands) |

Balance at

|

Adjustments

|

Balance at

|

||||||

|

Assets |

|||||||||

|

Operating property, net |

$ |

257,667 |

$ |

370 |

$ |

258,037 | |||

|

Operating lease right-of-use assets |

— |

232,319 | 232,319 | ||||||

|

Intangible assets, net |

7,369 | (3,542) | 3,827 | ||||||

|

Deferred tax asset, net |

26,235 | 82 | 26,317 | ||||||

|

Liabilities |

|||||||||

|

Operating lease liabilities |

$ |

— |

$ |

245,280 |

$ |

245,280 | |||

|

Other non-current liabilities |

28,931 | (16,033) | 12,898 | ||||||

|

Stockholders' Equity |

|||||||||

|

Non-controlling interest |

$ |

4,337 |

$ |

(46) |

$ |

4,291 | |||

|

Retained earnings |

47,616 | 28 | 47,644 | ||||||

8

|

|

|

Quarter Ended September 30, 2019 |

|

Nine Months Ended September 30, 2019 |

||||||||||||||

|

(Dollars in thousands) |

|

As Reported, September 30, 2019 |

|

Balances Without Adoption of ASC 842 |

|

Effect of

|

|

As Reported, September 30, 2019 |

|

Balances

|

|

Effect of

|

||||||

|

Cinema costs and expenses |

|

$ |

53,709 |

|

$ |

53,746 |

|

$ |

(37) |

|

$ |

158,273 |

|

$ |

158,357 |

|

$ |

(84) |

|

Depreciation and amortization |

|

|

5,704 |

|

|

5,665 |

|

|

39 |

|

|

16,870 |

|

|

16,749 |

|

|

121 |

|

General and administrative |

|

|

5,908 |

|

|

5,949 |

|

|

(41) |

|

|

18,426 |

|

|

18,554 |

|

|

(128) |

|

Interest expense, net |

|

|

1,871 |

|

|

1,867 |

|

|

4 |

|

|

5,924 |

|

|

5,914 |

|

|

10 |

|

Income tax (benefit) expense |

|

|

547 |

|

|

535 |

|

|

12 |

|

|

1,159 |

|

|

1,132 |

|

|

27 |

|

Net income (loss) |

|

$ |

852 |

|

$ |

829 |

|

$ |

23 |

|

$ |

1,112 |

|

$ |

1,058 |

|

$ |

54 |

|

|

|

|

|

|

|

|

|

|

|

|

(Dollars in thousands) |

|

As Reported,

|

|

Balances

|

|

Effect of

|

|||

|

Assets |

|

|

|

|

|

|

|

|

|

|

Operating property, net |

|

$ |

248,100 |

|

$ |

247,939 |

|

$ |

161 |

|

Intangible assets |

|

|

3,607 |

|

|

6,894 |

|

|

(3,287) |

|

Operating lease right-of-use assets |

|

|

216,963 |

|

|

— |

|

|

216,963 |

|

Deferred tax asset, net |

|

|

25,959 |

|

|

25,904 |

|

|

55 |

|

Liabilities |

|

|

|

|

|

|

|

|

|

|

Other current liabilities |

|

$ |

9,339 |

|

$ |

9,459 |

|

$ |

(120) |

|

Operating lease liabilities, current |

|

|

19,579 |

|

|

— |

|

|

19,579 |

|

Other non-current liabilities |

|

|

12,330 |

|

|

28,727 |

|

|

(16,397) |

|

Operating lease liabilities, non-current |

|

|

210,737 |

|

|

— |

|

|

210,737 |

|

Stockholders' Equity |

|

|

|

|

|

|

|

|

|

|

Retained earnings |

|

$ |

48,859 |

|

$ |

48,805 |

|

$ |

54 |

|

|

2) |

|

ASU 2014-09 Revenue from Contracts with Customers: On January 1, 2018, we adopted the new accounting standard ASC 606 Revenue from Contracts with Customers using the modified retrospective method. We recognized the cumulative effect of initially applying the new revenue standard as an adjustment to the opening balance of retained earnings. The comparative information was not restated. Adoption of this standard has no material effect on our consolidated financial statements. |

|

|

3) |

|

On January 1, 2018, we adopted ASU 2016-18, Statement of Cash Flows ( Topic 230 ) : Restricted Cash, a consensus of the FASB Emerging Issues Task Force . This standard requires that amounts generally described as restricted cash and cash equivalents be combined with unrestricted cash and cash equivalents when reconciling the beginning and end of period balances on the statement of cash flows. Adoption of this standard has no material effect on our consolidated statement of cash flows. |

|

|

4) |

|

On January 1, 2018, we adopted ASU 2 016-15, Statement of Cash Flows (Topic 230): Classification of Certain Cash Receipts and Cash Payments. The standard applies to eight (8) specific cash flow classification issues, reducing the current and potential future diversity in the presentation of certain cash flows. Adoption of this standard has no material effect on our consolidated statement of cash flows. |

|

|

5) |

|

On January 1, 2018, we adopted ASU 2017-07, Compensation—Retirement Benefits (Topic 715): Improving the Presentation of Net Periodic Pension Cost and Net Periodic Postretirement Benefit Cost . This standard (i) requires that an employer disaggregate the service cost component from the other components of net benefit cost, and (ii) specifies how to present the service cost component and the other components of net benefit cost in the income statement and (iii) allows only the service cost component of net benefit cost to be eligible for capitalization. Adoption of this standard has no material impact on our consolidated financial statements. |

|

|

6) |

|

On January 1, 2018, we adopted ASU 2017-01, Business Combinations (Topic 805): Clarifying the Definition of a Business . This ASU provides that when substantially all of the fair value of the gross assets acquired (or disposed of) is concentrated in a single identifiable asset or a group of similar identifiable assets, the asset is not a “business”, thus reducing the number of transactions that need further evaluation for business combination. The standard has no material impact on our current consolidated financial statements, and we do not expect it to be applicable to our consolidated financial statements in the near term unless we enter into a definitive business acquisition transaction. |

9

Issued:

|

|

v |

|

ASUs Effective 2019 and Beyond |

|

|

· |

|

Goodwill Impairment Simplification ( ASU 2017-04, Intangibles – Goodwill and Other (Topic 350): Simplifying the Test for Goodwill Impairment) |

Issued by FASB in January 2017, this standard removes the second step of the two-step impairment test for measuring goodwill and is to be applied on a prospective basis only. The new standard is effective for the Company on January 1, 2020, including interim periods within the year of adoption. Early adoption is permitted for interim or annual goodwill impairment tests performed on testing dates after January 1, 2017. Early adoption is not being contemplated. It is not anticipated that adoption of this standard will have any material impact on our consolidated financial statements.

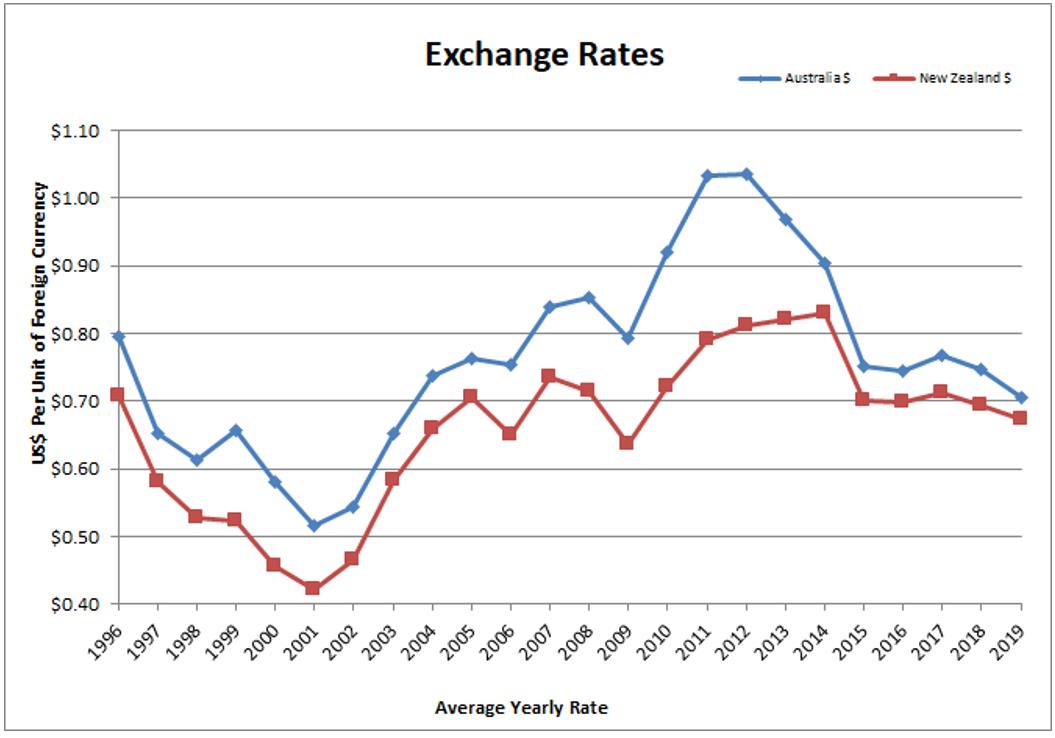

Note 3 – Operations in Foreign Currency

We have significant assets in Australia and New Zealand. Historically, we have conducted our Australian and New Zealand operations (collectively “foreign operations”) on a self-funding basis where we use cash flows generated by our foreign operations to pay for the expense of foreign operations. Our Australian and New Zealand assets and liabilities are translated from their functional currencies of Australian dollar (“AU$”) and New Zealand dollar (“NZ$”), respectively, to the U.S. dollar based on the exchange rate as of September 30, 2019 . The carrying value of the assets and liabilities of our foreign operations fluctuates as a result of changes in the exchange rates between the functional currencies of the foreign operations and the U.S. dollar. The translation adjustments are accumulated in the Accumulated Other Comprehensive Income in the Consolidated Balance Sheets.

Due to the natural- hedge nature of our funding policy, we have not historically used derivative financial instruments to hedge against the risk of foreign currency exposure. However, in certain circumstances, we move funds between jurisdictions where circumstances encouraged us to do so from an overall economic standpoint. Going forward, particularly in light of recent tax law changes, we intend to take a more global view of our financial resources, and to be more flexible in making use of resources from one jurisdiction in other jurisdictions.

Presented in the table below are the currency exchange rates for Australia and New Zealand:

|

|

|||||||||

|

|

Foreign Currency / USD |

||||||||

|

|

As of and

|

As of and for the nine months ended |

As of and

|

As of and

|

As of and for the nine months ended |

||||

|

|

September 30, 2019 |

December 31, 2018 |

September 30, 2018 |

||||||

|

Spot Rate |

|||||||||

|

Australian Dollar |

0.6746 |

0.7046 |

0.7238 |

||||||

|

New Zealand Dollar |

0.6262 |

0.6711 |

0.6635 |

||||||

|

Average Rate |

|||||||||

|

Australian Dollar |

0.6856 |

0.6993 |

0.7479 |

0.7311 |

0.7580 |

||||

|

New Zealand Dollar |

0.6486 |

0.6643 |

0.6930 |

0.6685 |

0.7002 |

||||

Note 4 – Earnings Per Share

Basic earnings per share (“EPS”) is calculated by dividing the net income attributable to the Company’s common stockholders by the weighted average number of common shares outstanding during the period. Diluted EPS is calculated by dividing the net income attributable to the Company’s common stockholders by the weighted average number of common and common equivalent shares outstanding during the period and is calculated using the treasury stock method for equity-based compensation awards .

10

The following table sets forth the computation of basic and diluted EPS and a reconciliation of the weighted average number of common and common equivalent shares outstanding:

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Quarter Ended |

|

Nine Months Ended |

||||||||

|

|

|

September 30, |

|

September 30, |

||||||||

|

(Dollars in thousands, except share data) |

|

2019 |

|

2018 |

|

2019 |

|

2018 |

||||

|

Numerator: |

|

|

|

|

|

|

|

|

|

|

|

|

|

Net income (loss) attributable to RDI common stockholders |

|

$ |

902 |

|

$ |

1,297 |

|

$ |

1,215 |

|

$ |

9,405 |

|

Denominator: |

|

|

|

|

|

|

|

|

|

|

|

|

|

Weighted average number of common stock – basic |

|

|

22,546,827 |

|

|

23,006,040 |

|

|

22,791,530 |

|

|

22,988,227 |

|

Weighted average dilutive impact of awards |

|

|

141,403 |

|

|

191,884 |

|

|

161,308 |

|

|

196,794 |

|

Weighted average number of common stock – diluted |

|

|

22,688,230 |

|

|

23,197,924 |

|

|

22,952,838 |

|

|

23,185,021 |

|

Basic earnings (loss) per share attributable to RDI common stockholders |

|

$ |

0.04 |

|

$ |

0.06 |

|

$ |

0.05 |

|

$ |

0.41 |

|

Diluted earnings (loss) per share attributable to RDI common stockholders |

|

$ |

0.04 |

|

$ |

0.06 |

|

$ |

0.05 |

|

$ |

0.41 |

|

Awards excluded from diluted earnings (loss) per share |

|

|

516,010 |

|

|

276,681 |

|

|

516,010 |

|

|

126,840 |

Our weighted average number of common stock - basic decrea sed, primarily as a result of the repurchase of shares of Class A Non-Voting Common Stock pursuant to our current stock repurchase program offset by the issuance of shares due to the exercise of share options and vesting of restricted stock units. During the first nine months of 2019, we repurchased 856,563 shares of Class A Non-Voting Common Stock at an average price of $13.20 per share.

Note 5 – Property and Equipment

Operating Property, net

As of September 30, 2019 and December 31, 2018 , property associated with our operating activities is summarized as follows:

|

|

||||||

|

|

September 30, |

December 31, |

||||

|

(Dollars in thousands) |

2019 |

2018 |

||||

|

Land |

$ |

73,675 |

$ |

75,689 | ||

|

Building and improvements |

143,408 | 149,734 | ||||

|

Leasehold improvements |

55,867 | 55,299 | ||||

|

Fixtures and equipment |

172,687 | 167,943 | ||||

|

Construction-in-progress |

7,032 | 3,478 | ||||

|

Total cost |

452,669 | 452,143 | ||||

|

Less: accumulated depreciation |

(204,569) | (194,476) | ||||

|

Operating property, net |

$ |

248,100 |

$ |

257,667 | ||

Depreciation expense for operating property was $5.5 million and $16.3 million for the quarter and nine months ended September 30, 2019 and $5.4 million and $15.6 million for the quarter and nine months ended September 30, 2018 , respectively.

Investment and Development Property, net

As of September 30, 2019 and December 31, 2018 , our investment and development property is summarized below:

|

|

||||||

|

|

September 30, |

December 31, |

||||

|

(Dollars in thousands) |

2019 |

2018 |

||||

|

Land |

$ |

23,392 |

$ |

24,371 | ||

|

Building |

1,900 | 1,900 | ||||

|

Construction-in-progress (including capitalized interest) |

82,000 | 60,533 | ||||

|

Investment and development property |

$ |

107,292 |

$ |

86,804 | ||

11

Construction-in-Progress – Operating and Investing Properties

Construction-in-Progress balances are included in both our operating and development properties. The balances of our major projects along with the movements for the nine months ended September 30, 2019 are shown below:

|

|

|||||||||||||||

|

(Dollars in thousands) |

Balance,

|

Additions during the period (1) |

Completed

|

Foreign

|

Balance, September 30, 2019 |

||||||||||

|

Union Square development |

$ |

55,634 |

$ |

21,098 |

$ |

— |

$ |

— |

$ |

76,732 | |||||

|

Courtenay Central development |

5,571 | 611 | (40) | (411) | 5,731 | ||||||||||

|

Cinema developments and improvements |

1,664 | 13,470 | (9,931) | (75) | 5,128 | ||||||||||

|

Other real estate projects |

1,142 | 717 | (338) | (80) | 1,441 | ||||||||||

|

Total |

$ |

64,011 |

$ |

35,896 |

$ |

(10,309) |

$ |

(566) |

$ |

89,032 | |||||

|

|

(1) |

|

Includes capitalized interest of $2.2 million and $4.9 million for the quarter and nine months ended September 30, 2019 . |

Real Estate Transactions

Purchase of Income Producing Property at Auburn/Redyard, Australia – On June 29, 2018, we added 20,870 square feet of land, improved with a 16,830 square foot office building, to our Auburn/Redyard entertainment-themed center (“ ETC ”) . The property was acquired at auction for $3.5 million ( AU$4.5 million) and is bordered by our existing ETC on three sides. The property is leased to Telstra through July 2022. This lease will allow us time to plan for the efficient integration of the property into our ETC. With this acquisition, Auburn/Redyard now represents approximately 519,992 square feet ( 48,309 square meters) of land, with approximately 1,620 feet ( 498 meters) of uninterrupted frontage to Parramatta Road, a major Sydney arterial motorway .

Purchase of Land at Cannon Park in Townsville, Australia – On June 13, 2018, we acquired a 163,000 square foot ( 15,150 square meter) parcel of land at our Cannon Park ETC, in connection with the restructuring of our relationship with the adjacent land owner. Prior to the restructuring, this parcel was commonly owned by us and the adjoining land owner. In the restructuring, the adjoining land owner conveyed to us its interest in the parcel for AU$1 . We granted the adjoining land owner certain access rights with respect to that parcel.

Exercise of Option to Acquire Ground Lessee’s interest in Ground Lease and Improvements Constituting the Village East Cinema – On August 28, 2019, we exercised our option to acquire the ground lessee’s interest in the 13 year ground lease underlying and the real property assets constituting our Village East Cinema in Manhattan. The purchase price under the option is $5.9 million. It is anticipated that the transaction will close on or about May 31, 2020 .

Note 6 – Investments in Unconsolidated Joint Ventures

Our investments in unconsolidated joint ventures are accounted for under the equity method of accounting.

The table below summarizes our active investment holdings in two (2) unconsolidated joint ventures as of September 30, 2019 and December 31, 2018 :

|

|

||||||||

|

|

September 30, |

December 31, |

||||||

|

(Dollars in thousands) |

Interest |

2019 |

2018 |

|||||

|

Rialto Cinemas |

50.0% |

$ |

1,112 |

$ |

1,260 | |||

|

Mt. Gravatt |

33.3% |

3,609 | 3,861 | |||||

|

Total investments |

$ |

4,721 |

$ |

5,121 | ||||

For the quarter and nine months ended September 30, 2019 and 2018 , the recognized share of equity earnings from our investments in unconsolidated joint ventures are as follows:

|

|

||||||||||||

|

|

Quarter Ended |

Nine Months Ended |

||||||||||

|

|

September 30, |

September 30, |

||||||||||

|

(Dollars in thousands) |

2019 |

2018 |

2019 |

2018 |

||||||||

|

Rialto Cinemas |

$ |

64 |

$ |

— |

$ |

78 |

$ |

152 | ||||

|

Mt. Gravatt |

156 | 80 | 503 | 515 | ||||||||

|

Total equity earnings |

$ |

220 |

$ |

80 |

$ |

581 |

$ |

667 | ||||

12

Note 7 – Goodwill and Intangible Assets

The table below summarizes goodwill by business segment as of September 30, 2019 and December 31, 2018 .

|

|

|||||||||

|

(Dollars in thousands) |

Cinema |

Real Estate |

Total |

||||||

|

Balance at December 31, 2018 |

$ |

14,221 |

$ |

5,224 |

$ |

19,445 | |||

|

Change in goodwill due to a purchase of a business combination |

1,225 |

— |

1,225 | ||||||

|

Foreign currency translation adjustment |

(757) |

— |

(757) | ||||||

|

Balance at September 30, 2019 |

$ |

14,689 |

$ |

5,224 |

$ |

19,913 | |||

The Company is required to test goodwill and other intangible assets for impairment on an annual basis and, if current events or circumstances require, on an interim basis. Our next annual evaluation of goodwill and other intangible assets is scheduled during the fourth quarter of 2019 . To test the impairment of goodwill, the Company compares the fair value of each reporting unit to its carrying amount, including the goodwill, to determine if there is potential goodwill impairment. A reporting unit is generally one level below the operating segment. As of September 30, 2019 , we were not aware that any events indicating potential impairment of goodwill had occurred.

The tables below summarize intangible assets other than goodwill, as of September 30, 2019 and December 31, 2018 , respectively.

|

|

||||||||||||

|

|

As of September 30, 2019 |

|||||||||||

|

(Dollars in thousands) |

Beneficial

|

Trade

|

Other

|

Total |

||||||||

|

Gross carrying amount |

$ |

14,973 |

$ |

7,258 |

$ |

2,262 |

$ |

24,493 | ||||

|

Less: Accumulated amortization |

(14,388) | (5,389) | (1,109) | (20,886) | ||||||||

|

Net intangible assets other than goodwill |

$ |

585 |

$ |

1,869 |

$ |

1,153 |

$ |

3,607 | ||||

|

|

||||||||||||

|

|

As of December 31, 2018 |

|||||||||||

|

(Dollars in thousands) |

Beneficial

|

Trade

|

Other

|

Total |

||||||||

|

Gross carrying amount |

$ |

28,592 |

$ |

7,254 |

$ |

1,951 |

$ |

37,797 | ||||

|

Less: Accumulated amortization |

(24,145) | (5,207) | (1,076) | (30,428) | ||||||||

|

Net intangible assets other than goodwill |

$ |

4,447 |

$ |

2,047 |

$ |

875 |

$ |

7,369 | ||||

Beneficial leases were amortized over the life of the lease up to 30 years up until January 1, 2019. Under ASC 842 they are now incorporated into the relevant right-of-use asset. Trade names are amortized based on the accelerated amortization method over their estimated useful life of 30 years, and other intangible assets are amortized over their estimated useful lives of up to 30 years (except for transferrable liquor licenses, which are indefinite-lived assets). The table below summarizes the amortization expense of intangible assets for the quarter and nine months ended September 30, 2019 .

|

|

||||||||||||

|

|

Quarter Ended |

Nine Months Ended |

||||||||||

|

|

September 30, |

September 30, |

||||||||||

|

(Dollars in thousands) |

2019 |

2018 |

2019 |

2018 |

||||||||

|

Beneficial lease amortization |

$ |

60 |

$ |

284 |

$ |

224 |

$ |

783 | ||||

|

Other amortization |

106 | 380 | 311 | 285 | ||||||||

|

Total intangible assets amortization |

$ |

166 |

$ |

664 |

$ |

535 |

$ |

1,068 | ||||

13

Note 8 – Prepaid and Other Assets

Prepaid and other assets are summarized as follows:

|

|

||||||

|

|

September 30, |

December 31, |

||||

|

(Dollars in thousands) |

2019 |

2018 |

||||

|

Prepaid and other current assets |

||||||

|

Prepaid expenses |

$ |

2,887 |

$ |

1,761 | ||

|

Prepaid rent |

895 | 930 | ||||

|

Prepaid taxes |

632 | 646 | ||||

|

Income taxes receivable |

6,148 | 2,704 | ||||

|

Deposits |

218 | 242 | ||||

|

Investment in marketable securities |

44 | 42 | ||||

|

Restricted cash |

7 | 1,342 | ||||

|

Total prepaid and other current assets |

$ |

10,831 |

$ |

7,667 | ||

|

Other non-current assets |

||||||

|

Straight-line rent |

4,184 | 4,150 | ||||

|

Other non-cinema and non-rental real estate assets |

1,134 | 1,134 | ||||

|

Investment in Reading International Trust I |

838 | 838 | ||||

|

Long-term deposits |

8 | 7 | ||||

|

Total other non-current assets |

$ |

6,164 |

$ |

6,129 | ||

Note 9 – Income Taxes

The interim provision for income taxes is different from the amount determined by applying the U.S. federal statutory rate to consolidated income before taxes. The differences are attributable to foreign tax rate differential, unrecognized tax benefits, and foreign tax credit. Our effective tax rate was 51.1% and 32.7% for the nine months ended September 30, 2019 and 2018, respectively. The change between 2019 and 2018 is primarily due to lower pretax income and accrued interest related to uncertain tax benefits.

Note 10 – Debt

The Company’s borrowings at September 30, 2019 and December 31, 2018 , net of deferred financing costs and including the impact of interest rate derivatives on effective interest rates, are summarized below:

|

|

|||||||||||||||

|

|

As of September 30, 2019 |

||||||||||||||

|

(Dollars in thousands) |

Maturity Date |

Contractual

|

Balance,

|

Balance,

|

Stated

|

Effective

|

|||||||||

|

Denominated in USD |

|||||||||||||||

|

Trust Preferred Securities (USA) |

April 30, 2027 |

$ |

27,913 |

$ |

27,913 |

$ |

26,228 |

6.27% |

6.27% |

||||||

|

Bank of America Credit Facility (USA) |

October 1, 2020 |

55,000 | 27,000 | 26,959 |

4.79% |

4.79% |

|||||||||

|

Bank of America Line of Credit (USA) |

October 1, 2020 |

5,000 | 5,000 | 5,000 |

5.04% |

5.04% |

|||||||||

|

Banc of America digital projector loan (USA) |

December 28, 2019 |

706 | 706 | 706 |

5.00% |

5.00% |

|||||||||

|

Cinemas 1, 2, 3 Term Loan (USA) |

December 1, 2019 |

18,767 | 18,767 | 18,597 |

3.25% |

3.25% |

|||||||||

|

Minetta & Orpheum Theatres Loan (USA) (2) |

November 1, 2023 |

8,000 | 8,000 | 7,880 |

4.15% |

5.15% |

|||||||||

|

U.S. Corporate Office Term Loan (USA) |

January 1, 2027 |

9,320 | 9,320 | 9,210 |

4.64% / 4.44% |

4.61% |

|||||||||

|

Purchase Money Promissory Note |

September 18, 2024 |

3,519 | 3,519 | 3,519 |

5.00% |

5.00% |

|||||||||

|

Union Square Construction Financing (USA) |

December 29, 2019 |

50,000 | 32,350 | 31,915 |

6.27% |

6.27% |

|||||||||

|

Denominated in foreign currency ("FC") (3) |

|||||||||||||||

|

NAB Corporate Term Loan (AU) |

December 31, 2023 |

80,952 | 54,977 | 54,782 |

1.91% |

1.91% |

|||||||||

|

Westpac Bank Corporate (NZ) |

December 31, 2023 |

20,038 | 7,514 | 7,514 |

3.05% |

3.05% |

|||||||||

|

|

$ |

279,215 |

$ |

195,066 |

$ |

192,310 | |||||||||

|

|

(1) |

|

Net of deferred financing costs amounting to

$2.8

million.

|

|

|

(2) |

|

The interest rate derivative associated with the Minetta & Orpheum loan provides for an effective fixed rate of 5.15% . |

|

|

(3) |

|

The contractual facilities a nd outstanding balances of the foreign currency denominated borrowings were translated into U.S. dollars based on the applicable exchange rates as of September 30, 2019 . |

14

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

As of December 31, 2018 |

|||||||||||||

|

(Dollars in thousands) |

|

Maturity Date |

|

Contractual

|

|

Balance,

|

|

Balance, Net (1) |

|

Stated

|

|

Effective Interest Rate |

|||

|

Denominated in USD |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Trust Preferred Securities (USA) (2) |

|

April 30, 2027 |

|

$ |

27,913 |

|

$ |

27,913 |

|

$ |

26,061 |

|

6.52% |

|

6.52% |

|

Bank of America Credit Facility (USA) (2) |

|

May 1, 2020 |

|

|

55,000 |

|

|

25,000 |

|

|

25,000 |

|

5.02% |

|

5.02% |

|

Bank of America Line of Credit (USA) |

|

October 31, 2019 |

|

|

5,000 |

|

|

— |

|

|

— |

|

5.48% |

|

5.48% |

|

Banc of America digital projector loan (USA) |

|

December 28, 2019 |

|

|

2,604 |

|

|

2,604 |

|

|

2,604 |

|

5.00% |

|

5.00% |

|

Cinemas 1, 2, 3 Term Loan (USA) |

|

September 1, 2019 |

|

|

19,086 |

|

|

19,086 |

|

|

18,838 |

|

3.25% |

|

3.25% |

|

Minetta & Orpheum Theatres Loan (USA) |

|

November 1, 2023 |

|

|

8,000 |

|

|

8,000 |

|

|

7,857 |

|

4.88% |

|

4.88% |

|

U.S. Corporate Office Term Loan (USA) |

|

January 1, 2027 |

|

|

9,495 |

|

|

9,495 |

|

|

9,373 |

|

4.64% / 4.44% |

|

4.61% |

|

Union Square Construction Financing (USA) |

|

December 29, 2019 |

|

|

57,500 |

|

|

27,182 |

|

|

25,280 |

|

6.76% / 12.51% |

|

8.35% |

|

Denominated in foreign currency ("FC") (3) |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

NAB Corporate Loan Facility (AU) |

|

December 31, 2023 |

|

|

46,856 |

|

|

37,696 |

|

|

37,660 |

|

3.05% |

|

3.05% |

|

Westpac Corporate Credit Facility (NZ) |

|

December 31, 2023 |

|

|

21,475 |

|

|

10,067 |

|

|

10,067 |

|

3.80% |

|

3.80% |

|

|

|

|

|

$ |

252,929 |

|

$ |

167,043 |

|

$ |

162,740 |

|

|

|

|

|

|

(1) |

|

Net of deferred financing costs amounting to $4.3 million. |

|

|

(2) |

|

The interest rate derivatives associated with the Trust Preferred Securities and the Bank of America Credit Facility expired in October 2017 so the effective interest rate no longer applie d as of December 31, 2018. |

|

|

(3) |

|

The contractual facilities and outstanding balances of the foreign currency denominated borrowings were translated into U.S. dollars based on the applicable exchange rates as of December 31, 2018 . |

Our loan arrangements are presented, net of the deferred financing costs, on the face of our consolidated balance sheet as follows:

|

|

||||||

|

|

September 30, |

December 31, |

||||

|

Balance Sheet Caption |

2019 |

2018 |

||||

|

Debt - current portion |

$ |

34,374 |

$ |

30,393 | ||

|

Debt - long-term portion |

131,681 | 106,286 | ||||

|

Subordinated debt |

26,255 | 26,061 | ||||

|

Total borrowings |

$ |

192,310 |

$ |

162,740 | ||

Bank of America Credit Facility

On March 3, 2016, we amended our $55.0 million credit facility with Bank of America to permit real property acquisition loans. This amendment reduces the applicable consolidated leverage ratio covenant by 0.25% and modifies the term of the facility based on the earlier of the eighteen months from the date of such borrowing or the maturity date of the credit agreement. Such modification was not considered substantial in accordance with U.S. GAAP. On March 5, 2019, this Credit Facility was extended for six (6) months to May 1, 2020 . On August 8, 2019, this Credit Facility was extended by an additional four months to September 1, 2020 . On November 5, 2019, this Credit Facility was further extended by an additional one month to October 1, 2020.

Bank of America Line of Credit

In October 2016, the term of this $5.0 million line of credit was extended to October 31, 2019 . Such modification was not considered to be substantial under US GAAP. On August 8, 2019, this Line of Credit was extended an additional ten months to September 1, 2020 . On November 5, 2019, this Line of Credit was further extended by an additional one month to October 1, 2020.

Minetta and Orpheum Theatres Loan

On October 12, 2018, we refinanced our $7.5 million loan with Santander Bank, which is secured by our Minetta and Orpheum Theatres, with a loan for a five year term of $8.0 million. Such modification was not considered to be substantial under US GAAP.

Banc of America Digital Projector Loan

On February 5, 2018, we purchased our U.S. digital cinema projectors, which had previously been held on operating leases, using a $4.6 million loan from Banc of America. We made further U.S. digital projector purchases, of projectors similarly held on other operating leases, in March and April 2018, increasing this loan to $4.9 million. This loan carries an interest rate of 5% and is due and payable December 28, 2019.

15

44 Union Square Construction Financing

On December 29, 2016, we closed on our new construction finance facilities totaling $57.5 million to fund the non-equity portion of the anticipated construction costs of the redevelopment of our property at 44 Union Square in New York City. The combined facilities consisted of $50.0 million in aggregate loans (comprised of three loan tranches) from Bank of the Ozarks, and a $7.5 million mezzanine loan from Tammany Mezz Investor, LLC, an affiliate of Fisher Brothers. At December 31, 2016, Bank of the Ozarks advanced $8.0 million to repay the then existing $8.0 million loan with East West Bank. As of September 30, 2019 , an additional $24.4 million had been advanced under the senior loan facility. On August 8, 2019, we repaid in full the $7.5 million mezzanine loan from Tammany Mezz Investor, LLC.

U.S. Corporate Office Term Loan

On December 13, 2016, we obtained a ten -year $8.4 million mortgage loan on our new Los Angeles Corporate Headquarters at a fixed annual interest rate of 4.64% . This loan provided for a second loan upon completion of certain improvements. On June 26, 2017, we obtained a further $1.5 million under this provision at a fixed annual interest rate of 4.44% .

Cinemas 1,2,3 Term Loan

On August 31, 2016, Sutton Hill Properties LLC (“SHP”), a 75% subsidiary of RDI, refinanced its $15.0 million Santander Bank term loan with a new lender, Valley National Bank. This new $20.0 million loan is collateralized by our Cinemas 1,2,3 property and bears an interest rate of 3.25% per annum, with principal installments and accruing interest paid monthly. The new loan matured on September 1, 2019 , with a one -time option to extend maturity date for another year. On August 8, 2019, this maturity date was extended to December 1, 2019, with the one-time option to extend the maturity date for another year preserved. Such modification was not considered to be substantial under US GAAP.

Purchase Money Promissory Note

On September 18, 2019, we purchased 407,000 Company shares in a privately negotiated transaction under our Share Repurchase Program for $5.5 million . Of this amount, $3.5 million was paid by the issuance of a Purchase Money Promissory Note, which bears an interest rate of 5.0% per annum , payable in equal quarterly payments of principal plus accrued interest. The Purchase Money Promissory Note matures on September 18, 2024 .

Westpac Bank Corporate Credit Facility (NZ)

On December 20, 2018, we restructured our Westpac Corporate Credit Facilities. The maturity of the 1 st tranche (general/non-construction credit line) was extended to December 31, 2023 , with the available facility being reduced from NZ$35.0 million to NZ$32.0 million. The facility bears an interest rate of 1.75% above the Bank Bill Bid Rate on the drawn down balance and a 1.1% line of credit charge on the entire facility. The 2 nd tranche (construction line) with a facility of NZ$18.0 million was not renewed.

Australian NAB Corporate Term Loan (AU)

On March 15, 2019, we amended our Revolving Corporate Markets Loan Facility with National Australia Bank (“NAB”) from a facility comprised of (i) a AU$66.5 million loan facility with an interest rate of 0.95% above the Bank Bill Swap Bid Rate (“BBSY”) and a maturity date of June 30, 2019 and (ii) a bank guarantee of AU$5.0 million at a rate of 1.90% per annum into a (i) AU$120.0 million Corporate Loan facility at rates of 0.85% - 1.30% above BBSY depending on certain ratios with a due date of December 31, 2023 , of which AU$80.0 million is revolving and AU$40.0 million is core and (ii) a Bank Guarantee Facility of AU$5.0 million at a rate of 1.85% per annum. Such modifications of this particular term loan were not considered to be substantial under US GAAP.

16

Note 11 – Other Liabilities

Other liabilities are summarized as follows:

|

|

||||||

|

|

September 30, |

December 31, |

||||

|

(Dollars in thousands) |

2019 |

2018 |

||||

|

Current liabilities |

||||||

|

Lease liability |

$ |

5,900 |

$ |

5,900 | ||

|

Liability for demolition costs |

2,548 | 2,630 | ||||

|

Accrued pension |

684 | 684 | ||||

|

Security deposit payable |

83 | 84 | ||||

|

Finance lease liabilities |

117 |

— |

||||

|

Other |

7 | 7 | ||||

|

Other current liabilities |

$ |

9,339 |

$ |

9,305 | ||

|

Other liabilities |

||||||

|

Straight-line rent |

$ |

— |

$ |

16,362 | ||

|

Lease make-good provision |

5,930 | 5,614 | ||||

|

Accrued pension |

4,571 | 4,670 | ||||

|

Environmental reserve |

1,656 | 1,656 | ||||

|

Deferred revenue - real estate |

— |

32 | ||||

|

Acquired leases |

38 | 91 | ||||

|

Finance lease liabilities |

128 |

— |

||||

|

Other |

7 | 506 | ||||

|

Other liabilities |

$ |

12,330 |

$ |

28,931 | ||

On August 29, 2014, the Supplemental Executive Retirement Plan (“SERP”) that has been effective since March 1, 2007, was ended and replaced in accordance with the terms of a pension annuity. As a result of the termination of the SERP program, the accrued pension liability of $7.6 million was reversed and replaced with this pension annuity liability of $7.5 million. The valuation of the liability is based on the present value of $10.2 million discounted at a rate of 4.25% over a 15 -year term, resulting in a monthly payment of $57,000 . The discounted value of $2.7 million (which is the difference between the estimated payout of $10.2 million and the present value of $7.5 million) as of August 29, 2014 will be amortized and expensed based on the 15-year term. In addition, the accumulated actuarial loss of $3.1 million recorded, as part of other comprehensive income will also be amortized based on the 15 - year term.

In February 2018, we made a payment of $2.4 million relating to the annuity representing payments for the 42 months outstanding at the time. Monthly ongoing payments of $57,000 are now being made.

As a result of the above, included in our current and non-current liabilities are accrued pension costs of $5.3 million at September 30, 2019 . The benefits of our pension plan are fully vested and therefore no service costs were recognized for the quarter and nine months ended September 30, 2019 and 2018 . Our pension plan is unfunded.

During the quarter and nine months ended September 30, 2019 , the interest cost was $70,000 and $414,000 respectively, and the actuarial loss was $52,000 and $155,000 respectively. During the quarter and nine months ended September 30, 2018 , the interest cost was $45,000 and $135,000 respectively, and the actuarial loss was $52,000 and $156,000 respectively.

17

Note 12 – Accumulated Other Comprehensive Income

The following table summarizes the changes in each component of accumulated other comprehensive income attributable to RDI:

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

(Dollars in thousands) |

Foreign

|

|

Unrealized

|

|

Accrued

|

|

Hedge Accounting Reserve |

|

Total |

|||||

|

Balance at January 1, 2019 |

$ |

8,687 |

|

$ |

3 |

|

$ |

(2,438) |

|

$ |

(137) |

|

$ |

6,115 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Change related to derivatives |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Total change in hedge fair value recorded in Other Comprehensive Income |

|

— |

|

|

— |

|

|

— |

|

|

(253) |

|

|

(253) |

|

Amounts reclassified from accumulated other comprehensive income |

|

— |

|

|

— |

|

|

— |

|

|

42 |

|

|

42 |

|

Net change related to derivatives |

|

— |

|

|

— |

|

|

— |

|

|

(211) |

|

|

(211) |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Net current-period other comprehensive income (loss) |

|

(7,351) |

|

|

4 |

|

|

155 |

|

|

(211) |

|

|

(7,403) |

|

Balance at September 30, 2019 |

$ |

1,336 |

|

$ |

7 |

|

$ |

(2,283) |

|

$ |

(348) |

|

$ |

(1,288) |

Note 13 – Commitments and Contingencies

Litigation General

We are currently involved in certain legal proceedings and, as required, have accrued estimates of probable and estimable losses for the resolution of these claims, including legal costs.

|

|

· |

|

Where we are a plaintiff , we accrue legal fees as incurred on an on-going basis and make no provision for any potential settlement amounts until received. In Australia, the prevailing party is usually entitled to recover its attorneys’ fees, which recoveries typically work out to be approximately 60% of the amounts actually spent where first-class legal counsel is engaged at customary rates. Where we are a plaintiff, we have likewise made no provision for the liability for the defendant’s attorneys' fees in the event we are determined not to be the prevailing party. |

|

|

· |

|

Where we are a defendant , we accrue for probable damages that insurance may not cover as they become known and can be reasonably estimated, as permitted under ASC 450-20 Loss Contingencies . In our opinion, any claims and litigation in which we are currently involved are not reasonably likely to have a material adverse effect on our business, results of operations, financial position, or liquidity. I t is possible, however, that future results of the operations for any particular quarterly or annual period could be materially affected by the ultimate outcome of the legal proceedings. From time-to-time, we are involved with claims and lawsuits arising in the ordinary course of our business that may include contractual obligations, insurance claims, tax claims, employment matters, and anti-trust issues, among other matters. |