|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 10-K

|

ý |

|

ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

|

For the fiscal year ended December 31, 2012 |

||

|

OR |

||

|

o |

|

TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

|

For the transition period from to |

||

Commission File Number 001-35169

RLJ LODGING TRUST

(Exact Name of Registrant as Specified in Its Charter)

| Maryland | 27-4706509 | |

| (State or Other Jurisdiction of Incorporation or Organization) | (I.R.S. Employer Identification No.) | |

|

3 Bethesda Metro Center, Suite 1000 |

|

|

| Bethesda, Maryland | 20814 | |

| (Address of Principal Executive Offices) | (Zip Code) |

(301) 280-7777

(Registrant's Telephone Number, Including Area Code)

Securities registered pursuant to Section 12(b) of the Act:

| Title of Each Class | Name of Each Exchange on Which Registered | |

|---|---|---|

| Common Shares, $0.01 par value | New York Stock Exchange |

Securities registered pursuant to Section 12(g) of the Act: None

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. Yes ý No o

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or 15(d) of the Act. Yes o No ý

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. ý Yes o No

Indicate by check mark whether the registrant has submitted electronically and posted on its corporate Web site, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T (§232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files). ý Yes o No

Indicate by check mark if disclosure of delinquent filers pursuant to Item 405 of Regulation S-K (§ 229.405 of this chapter) is not contained herein, and will not be contained, to the best of registrant's knowledge, in definitive proxy or information statements incorporated by reference in Part III of this Form 10-K or any amendment to this Form 10-K. o

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, or a smaller reporting company. See the definitions of "large accelerated filer," "accelerated filer" and "smaller reporting company" in Rule 12b-2 of the Exchange Act.

| Large accelerated filer ý | Accelerated filer o |

Non-accelerated filer

o

(do not check if a smaller reporting company) |

Smaller reporting company o |

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act). o Yes ý No

The aggregate market value of the 102,481,816 common shares of beneficial interest held by non-affiliates of the Registrant was approximately $1,857,995,324 based on the closing price of $18.13 as reported on the New York Stock Exchange for such common shares of beneficial interest on June 29, 2012.

As of February 20, 2013, 106,540,971 common shares of beneficial interest of the Registrant, $0.01 par value per share, were outstanding.

Documents Incorporated by Reference

Portions of the Definitive Proxy Statement for our 2013 Annual Meeting of Shareholders are incorporated by reference into Part III of this report. We expect to file our proxy statement within 120 days after December 31, 2012.

RLJ Lodging Trust

1

SPECIAL NOTE ABOUT FORWARD-LOOKING STATEMENTS

Certain statements in this Annual Report on Form 10-K, other than purely historical information, including estimates, projections, statements relating to our business plans, objectives and expected operating results, and the assumptions upon which those statements are based, are "forward-looking statements" within the meaning of the Private Securities Litigation Reform Act of 1995, Section 27A of the Securities Act of 1933, as amended and Section 21E of the Securities Exchange Act of 1934, as amended. These forward-looking statements generally are identified by the use of the words "believe," "project," "expect," "anticipate," "estimate," "plan," "may," "will," "will continue," "intend," "should," "may" or similar expressions. Although we believe that the expectations reflected in such forward-looking statements are based upon reasonable assumptions, beliefs and expectations, such forward-looking statements are not predictions of future events or guarantees of future performance and our actual results could differ materially from those set forth in the forward-looking statements. Some factors that might cause such a difference include the following: the current global economic uncertainty, increased direct competition, changes in government regulations or accounting rules, changes in local, national and global real estate conditions, declines in the lodging industry, seasonality of the lodging industry, risks related to natural disasters, such as earthquakes and hurricanes, hostilities, including future terrorist attacks or fear of hostilities that affect travel, our ability to obtain lines of credit or permanent financing on satisfactory terms, changes in interest rates, access to capital through offerings of our common and preferred shares of beneficial interest, or debt, our ability to identify suitable acquisitions, our ability to close on identified acquisitions and integrate those businesses and inaccuracies of our accounting estimates. A discussion of these and other risks and uncertainties that could cause actual results and events to differ materially from such forward-looking statements is included in "Risk Factors" and "Management's Discussion and Analysis of Financial Condition and Results of Operations" of this Annual Report on Form 10-K. Given these uncertainties, undue reliance should not be placed on such statements. Except as required by law, we undertake no obligation to update or revise publicly any forward-looking statements, whether as a result of new information, future events or otherwise. Except where the context suggests otherwise, we define certain terms in this Annual Report on Form 10-K as follows:

- •

-

"our company," "we," "us" and "our" refer to RLJ Lodging Trust, a Maryland real estate investment trust, together with its

consolidated subsidiaries, including RLJ Lodging Trust, L.P., a Delaware limited partnership, which we refer to as "our operating partnership";

- •

-

"our predecessor" collectively refers to RLJ Development, LLC, or RLJ Development, and two lodging-focused private

equity funds that were sponsored and managed by RLJ Development, RLJ Lodging Fund II, L.P. (and its parallel fund), or collectively, Fund II, and RLJ Real Estate Fund III, L.P. (and its

parallel fund), or collectively, Fund III, all of which were entities under the common control of Robert L. Johnson, our Executive Chairman;

- •

-

"our hotels" refers to the 145 hotels owned by us as of December 31, 2012;

- •

-

"our formation transactions" refers to a series of transactions in which, among other things, (1) our company was

formed, (2) our operating partnership was formed, (3) each of Fund II and Fund III were merged with and into our company, with investors in each of Fund II and Fund III receiving common

shares as consideration, and (4) RLJ Development contributed substantially all of its assets and liabilities to our operating partnership in exchange for units of limited partnership interest

in our operating partnership, or OP units;

- •

- a "compact full-service hotel" typically refers to any hotel with (1) less than 300 guestrooms and less than 12,000 square feet of meeting space or (2) more than 300 guestrooms where, unlike traditional full-service hotels, the operations focus primarily on the rental of guestrooms such that a significant majority of its total revenue is generated from room rentals rather than other sources, such as food and beverage;

2

- •

-

a "focused-service hotel" typically refers to any hotel where the operations focus primarily on the rental of guestrooms

and that offers services and amenities to a lesser extent than a typical full-service or compact full-service hotel. For example, a focused-service hotel may have a restaurant,

but, unlike a restaurant in a typical full-service or compact full-service hotel, it may not offer three meals per day and may not offer room service. In addition, a

focused-service hotel differs from a compact full-service hotel in that it typically has less than 2,000 square feet of meeting space, if any at all; and

- •

-

"TRSs" refers to our taxable REIT subsidiaries that are wholly-owned, directly or indirectly, by our operating partnership

and any disregarded subsidiaries of our TRSs.

- •

- "RevPAR penetration index" of our hotels is the measure of each hotel's revenue per available room, or RevPAR, in relation to the average RevPAR of that hotel's competitive set. Each hotel's competitive set consists of a small group of hotels in the relevant market that we and the third-party hotel management company that manages the hotel believe are comparable for purposes of benchmarking the performance of such hotel.

Our Company

We are a self-advised and self-administered Maryland real estate investment trust, or REIT, that acquires primarily premium-branded, focused-service and compact full-service hotels. We are one of the largest U.S. publicly-traded lodging REITs in terms of both number of hotels and number of rooms. Our hotels are concentrated in urban and dense suburban markets that we believe exhibit multiple demand generators and high barriers to entry. We believe focused-service and compact full-service hotels with these characteristics generate high levels of RevPAR, strong operating margins and attractive returns.

As of December 31, 2012, we, through wholly-owned subsidiaries, owned 100% of the interests in 144 hotels and a 95% interest in one hotel. Our 145 hotels are made up of 21,617 suites/rooms and are located in 21 states and the District of Columbia.

We elected to be taxed as a REIT, for U.S. federal income tax purposes, when we filed our U.S. federal tax return for the taxable year ended December 31, 2011. Substantially all of our assets are held by, and all of our operations are conducted through, our operating partnership. We are the sole general partner of our operating partnership. As of December 31, 2012, we owned, through a combination of direct and indirect interests, 99.2% of the OP units in our operating partnership.

Our Investment and Growth Strategies

Our objective is to generate strong returns for our shareholders by continuing to acquire primarily premium-branded, focused-service hotels and compact full-service hotels at prices where we believe we can generate attractive returns on investment and long-term value appreciation through proactive asset management. We intend to pursue acquisitions of these hotels in urban and dense suburban markets, and we also intend to selectively dispose of properties when we believe returns have been maximized in order to redeploy capital into more accretive acquisitions and other opportunities. We intend to pursue this objective through the following investment and growth strategies:

- •

- Targeted ownership of premium-branded, focused-service and compact full-service hotels. We believe that premium-branded, focused-service hotels have the potential to generate attractive returns relative to other types of hotels due to their ability to achieve RevPAR levels at or close to those generated by traditional full-service hotels, while achieving higher profit margins due to their

Investment Strategies

3

- •

-

Use of premium hotel brands.

We believe in affiliating

our hotels with premium brands owned by leading international franchisors such as Marriott, Hilton and Hyatt. Within the focused-service category, we target hotels affiliated with premium brands such

as Courtyard by Marriott, Residence Inn by Marriott, Hilton Garden Inn, Homewood Suites by Hilton and Hyatt Place. We believe that utilizing premium brands provides significant advantages because of

their guest loyalty programs, worldwide reservation systems, effective product segmentation, global distribution and strong customer awareness.

- •

- Focus on urban and dense suburban markets. We focus on owning and acquiring hotels in both urban and dense suburban markets that we believe have multiple demand generators and high barriers to entry. As a result, we believe that these hotels generate higher returns on investment.

more efficient operating model and less volatile cash flows. We also may acquire compact full-service hotels which have operating characteristics that resemble those of focused-service hotels.

- •

-

Maximize returns from our hotels.

We believe that our

hotels have the potential to generate significant improvements in RevPAR and earnings before interest, taxes, depreciation and amortization, or EBITDA, as a result of our proactive asset management

and the ongoing economic recovery in the United States. We actively monitor and advise our third-party hotel management companies on most aspects of our hotels' operations, including property

positioning, physical design, capital planning and investment, guest experience and overall strategic direction. We regularly review opportunities to invest in our hotels in an effort to enhance the

quality and attractiveness of our hotels, increase their long-term value and generate attractive returns on investment.

- •

-

Pursue a disciplined hotel acquisition strategy.

We seek

to acquire additional hotels at prices below replacement cost where we believe we can generate attractive returns on investment. We intend to target acquisition opportunities where we can enhance

value by pursuing proactive investment strategies such as renovation, repositioning or rebranding.

- •

- Pursue a disciplined capital recycling program. We intend to continue to pursue a disciplined capital allocation strategy designed to maximize the value of our investments by selectively selling hotels that are no longer consistent with our investment strategy or whose returns appear to have been maximized. To the extent that we sell hotels, we intend to redeploy the capital into acquisition and investment opportunities that we believe will achieve higher returns.

Growth Strategies

Our Hotels

Overview

As of December 31, 2012, we owned a high-quality portfolio of 145 hotels located in 21 states and the District of Columbia comprised of over 21,600 rooms. Including certain pro forma operating information, for the year ended December 31, 2012, the average occupancy rate for our hotels was 72.9%, and the average daily rate, or ADR, and RevPAR of our hotels were $134.05 and $97.71, respectively. No single hotel accounted for more than 7.4% of our total revenue for the year ended December 31, 2012.

We believe that the quality of our portfolio is evidenced by the RevPAR penetration index of 111.2 for our hotels for the year ended December 31, 2012 and portfolio-wide guest satisfaction scores that are consistently higher than the average industry scores for their respective brands.

4

The following table sets forth certain pro forma operating information for our hotels as of and for the years ended December 31, 2012, 2011 and 2010 (excluding hotels that were not open at the end of the applicable period):

|

|

For the year ended December 31, | |||||||||

|---|---|---|---|---|---|---|---|---|---|---|

|

|

2012 | 2011 | 2010 | |||||||

|

Statistical Data(1)(2): |

||||||||||

|

Number of hotels |

144 | 144 | 144 | |||||||

|

Number of rooms |

21,480 | 21,480 | 21,480 | |||||||

|

Occupancy(3) |

72.9 | % | 71.6 | % | 69.8 | % | ||||

|

ADR(3) |

$ | 134.05 | $ | 126.55 | $ | 120.46 | ||||

|

RevPAR(3) |

$ | 97.71 | $ | 90.56 | $ | 84.09 | ||||

- (1)

-

The

table includes unaudited pro forma financial information that excludes discontinued operations and is not necessarily indicative of what actual results

of operations of the hotels would have been had we owned them for the entirety of all periods presented.

- (2)

-

The

132-room Hotel Indigo New Orleans Garden District was closed for substantially all of the periods presented and, therefore, is not reflected

in the table.

- (3)

- For a more detailed explanation of the terms occupancy, ADR and RevPAR and a discussion of how we use these metrics to evaluate the operating performance of our business, see "Management's Discussion and Analysis of Financial Condition and Results of Operations—Key Indicators of Our Operating Performance."

Brand Affiliations

Our hotels operate under strong, premium brands, with approximately 96% of our hotels operating under existing relationships with Marriott, Hilton or Hyatt. The following table sets forth the brand affiliations of our hotels as of December 31, 2012:

|

Brand Affiliations

|

Number of

hotels |

Percentage of

total |

Number of

rooms |

Percentage of

total |

|||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

|

Marriott |

|||||||||||||

|

Courtyard by Marriott |

34 | 23.4 | % | 4,625 | 21.4 | % | |||||||

|

Fairfield Inn & Suites by Marriott |

14 | 9.7 | % | 1,433 | 6.6 | % | |||||||

|

Marriott |

6 | 4.1 | % | 1,834 | 8.5 | % | |||||||

|

Renaissance |

3 | 2.1 | % | 782 | 3.6 | % | |||||||

|

Residence Inn by Marriott |

34 | 23.4 | % | 3,794 | 17.6 | % | |||||||

|

SpringHill Suites by Marriott |

11 | 7.6 | % | 1,354 | 6.2 | % | |||||||

|

Subtotal |

102 | 70.3 | % | 13,822 | 63.9 | % | |||||||

|

Hilton |

|||||||||||||

|

Doubletree |

2 | 1.4 | % | 916 | 4.2 | % | |||||||

|

Embassy Suites |

6 | 4.1 | % | 1,419 | 6.6 | % | |||||||

|

Hampton Inn/Hampton Inn & Suites |

9 | 6.2 | % | 1,115 | 5.2 | % | |||||||

|

Hilton |

2 | 1.4 | % | 462 | 2.1 | % | |||||||

|

Hilton Garden Inn |

10 | 6.9 | % | 1,993 | 9.2 | % | |||||||

|

Homewood Suites |

2 | 1.4 | % | 301 | 1.4 | % | |||||||

|

Subtotal |

31 | 21.4 | % | 6,206 | 28.7 | % | |||||||

|

Hyatt |

|||||||||||||

|

Hyatt House |

6 | 4.1 | % | 828 | 3.8 | % | |||||||

|

Subtotal |

6 | 4.1 | % | 828 | 3.8 | % | |||||||

|

Other Brand Affiliation |

6 | 4.2 | % | 761 | 3.6 | % | |||||||

|

Total |

145 | 100.0 | % | 21,617 | 100.0 | % | |||||||

5

Asset Management

We have a dedicated team of asset management professionals that proactively work with our third-party hotel management companies to maximize profitability at each of our hotels. Our asset management team monitors the performance of our hotels on a daily basis and holds frequent ownership meetings with personnel at the hotels. Our asset management team works closely with our third-party hotel management companies on key aspects of each hotel's operation, including, among others, revenue management, market positioning, cost structure, capital and operational budgeting as well as the identification of return on investment initiatives and overall business strategy. In addition, we retain approval rights on key staffing positions at many of our hotels, such as the hotel's general manager and director of sales. We believe that our strong asset management process helps to ensure that each hotel is being operated to our and our franchisors' standards, that our hotels are being adequately maintained in order to preserve the value of the asset and the safety of the hotel to customers, and that our hotel management companies are maximizing revenue and enhancing operating margins.

Competition

The U.S. lodging industry is highly competitive. Our hotels compete with other hotels for guests in each of their markets on the basis of several factors, including, among others, location, quality of accommodations, convenience, brand affiliation, room rates, service levels and amenities, and level of customer service. Competition is often specific to the individual markets in which our hotels are located and includes competition from existing and new hotels operated under premium brands in the focused-service and full-service segments. We believe that hotels, such as our hotels, that are affiliated with leading national brands, such as the Marriott, Hilton or Hyatt brands, will enjoy the competitive advantages associated with operating under such brands. Increased competition could harm our occupancy and revenues and may require us to provide additional amenities or make capital improvements that we otherwise would not have to make, which may materially and adversely affect our operating results and liquidity.

We face competition for the acquisition of hotels from institutional pension funds, private equity funds, REITs, hotel companies and others who are engaged in the acquisition of hotels. Some of these competitors may have substantially greater financial and operational resources and access to capital than we have and may have greater knowledge of the markets in which we seek to invest. This competition may reduce the number of suitable investment opportunities offered to us and decrease the attractiveness of the terms on which we may acquire our targeted hotel investments, including the cost thereof.

Seasonality

The lodging industry is seasonal in nature, which can be expected to cause quarterly fluctuations in our revenues. Our quarterly earnings may be adversely affected by factors outside our control, including weather conditions and poor economic factors in certain markets in which we operate. For example, our hotels in the Chicago, Illinois metropolitan area experience lower revenues and profits during the winter months of December through March while our hotels in Florida generally have higher revenues in the months of January through April. This seasonality can be expected to cause periodic fluctuations in a hotel's room revenues, occupancy levels, room rates, operating expenses and cash flows.

Our Financing Strategy

We expect to continue to maintain a prudent capital structure by limiting our net debt-to-EBITDA to a ratio of 5.0x or below. We define net debt as total indebtedness minus cash and cash equivalents. Over time, we intend to finance our long-term growth with equity issuances and debt financing having

6

staggered maturities. We will seek to primarily utilize unsecured debt (with the ultimate goal of achieving an investment grade credit rating) and a greater percentage of fixed rate and hedged floating rate debt relative to unhedged floating rate debt. Our debt currently is comprised of both unsecured debt and mortgage debt secured by our hotels. We have a mix of fixed and floating rate debt; however, the majority of our debt either bears interest at fixed rates or effectively bears interest at fixed rates due to interest rate hedges on the debt.

As of December 31, 2012, we had approximately $997.7 million of outstanding mortgage debt and $400.0 million in outstanding unsecured term loans. In addition, on November 20, 2012, we, through our operating partnership, entered into a four-year, $300.0 million unsecured revolving credit facility, or our unsecured revolving credit facility, to fund future acquisitions, as well as for hotel redevelopments, capital expenditures and general corporate purposes. As of December 31, 2012, $16.0 million was drawn on our unsecured revolving credit facility. For more information regarding our indebtedness, see "Management's Discussion and Analysis of Financial Condition and Results of Operations—Liquidity and Capital Resources—Our Outstanding Mortgage Indebtedness."

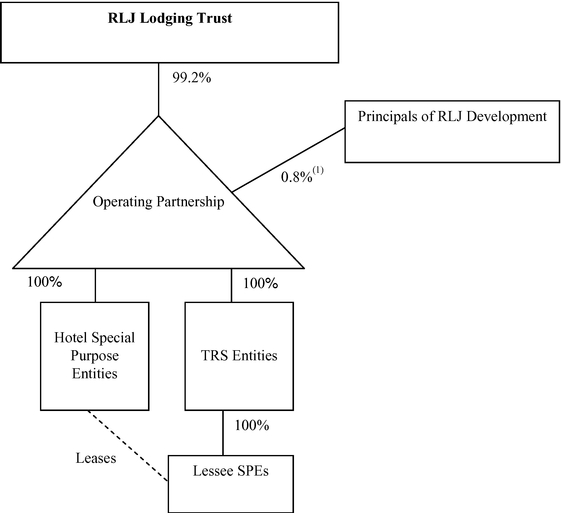

Organizational Structure

We were formed as a Maryland real estate investment trust in January 2011. We conduct our business through a traditional umbrella partnership real estate investment trust, or UPREIT, in which our hotels are indirectly owned by our operating partnership, RLJ Lodging Trust, L.P., through limited partnerships, limited liability companies or other subsidiaries. We are the sole general partner of our operating partnership and as of December 31, 2012, we owned 99.2% of the OP units in our operating partnership. In the future, we may issue OP units from time to time in connection with acquisitions of hotels or for financing, compensation or other reasons.

In order for the income from our hotel operations to constitute "rents from real property" for purposes of the gross income tests required for REIT qualification, we cannot directly or indirectly operate any of our hotels. Accordingly, we lease each of our hotels, and intend to lease any hotels we acquire in the future, to subsidiaries of our TRSs, or TRS lessees, which are wholly-owned by us, and our TRS lessees have engaged, or will engage, third-party hotel management companies to manage our hotels, and any hotels we acquire in the future, on market terms. Our TRS lessees pay rent to us that we intend to treat as "rents from real property," provided that the third-party hotel management companies engaged by our TRS lessees to manage our hotels are deemed to be "eligible independent contractors" and certain other requirements are met. Our TRSs are subject to U.S. federal, state and local income taxes applicable to corporations.

7

The following chart generally depicts our corporate structure as of December 31, 2012:

- (1)

- Reflects OP units issued to RLJ Development, an entity in which each of Messrs. Johnson, Baltimore and Bierkan hold an equity interest, as consideration for substantially all of RLJ Development's assets and liabilities, which were contributed to us in connection with our formation transactions.

Regulation

General

Our hotels are subject to various U.S. federal, state and local laws, ordinances and regulations, including regulations relating to common areas and fire and safety requirements. We believe that each of our hotels has the necessary permits and approvals to operate its business.

Americans with Disabilities Act

Our hotels must comply with applicable provisions of the Americans with Disabilities Act of 1990, or ADA, to the extent that such hotels are "public accommodations" as defined by the ADA. The ADA may require removal of structural barriers to access by persons with disabilities in certain public areas of our hotels where such removal is readily achievable. We believe that our hotels are in substantial compliance with the ADA and that we will not be required to make substantial capital expenditures to address the requirements of the ADA. However, non-compliance with the ADA could

8

result in imposition of fines or an award of damages to private litigants. The obligation to make readily achievable accommodations is an ongoing one, and we will continue to assess our hotels and to make alterations as appropriate in this respect.

Environmental Matters

Under various laws relating to the protection of the environment, a current or previous owner or operator (including tenants) of real estate may be subject to liability related to contamination resulting from the presence or discharge of hazardous or toxic substances at that property and may be required to investigate and clean up such contamination at that property or emanating from that property. These costs could be substantial and liability under these laws may attach without regard to whether the owner or operator knew of, or was responsible for, the presence of the contaminants, and the liability may be joint and several. The presence of contamination or the failure to remediate contamination at our hotels may expose us to third-party liability for cleanup costs, property damage or bodily injury, natural resource damages and costs or expenses related to liens or property use restrictions and materially and adversely affect our ability to sell, lease or develop the real estate or to incur debt using the real estate as collateral. Furthermore, persons who sent waste to a waste disposal facility, such as a landfill or an incinerator, may be liable for costs associated with cleanup of that facility.

Our hotels are subject to various federal, state, and local environmental, health and safety laws and regulations that address a wide variety of issues, including, but not limited to, storage tanks, air emissions from emergency generators, storm water and wastewater discharges, lead-based paint, mold and mildew and waste management. Our hotels incur costs to comply with these laws and regulations and could be subject to fines and penalties for non-compliance. The costs of complying with environmental, health and safety laws could increase as new laws are enacted and existing laws are modified.

Some of our hotels contain asbestos-containing building materials. We believe that the asbestos is appropriately contained, in accordance with current environmental regulations and that we have no need for any immediate remediation or current plans to remove the asbestos. Environmental laws require that owners or operators of buildings with asbestos-containing building materials properly manage and maintain these materials, adequately inform or train those who may come into contact with asbestos and undertake special precautions, including removal or other abatement, in the event that asbestos is disturbed during building renovation or demolition. These laws may impose fines and penalties on building owners or operators for failure to comply with these requirements. In addition, third parties may seek recovery from owners or operators for personal injury associated with exposure to asbestos-containing building materials.

Some of our hotels may contain or develop harmful mold or suffer from other adverse conditions, which could lead to liability for adverse health effects and costs of remediation. The presence of significant mold or other airborne contaminants at any of our hotels could require us to undertake a costly remediation program to contain or remove the mold or other airborne contaminants from the affected hotel or increase indoor ventilation. In addition, the presence of significant mold or other airborne contaminants could expose us to liability from guests or employees at our hotels and others if property damage or health concerns arise.

Insurance

We carry comprehensive general liability, fire, extended coverage, business interruption, rental loss coverage and umbrella liability coverage on all of our hotels and earthquake, wind, flood and hurricane coverage on hotels in areas where we believe such coverage is warranted, in each case with limits of liability that we deem adequate. Similarly, we are insured against the risk of direct physical damage in amounts we believe to be adequate to reimburse us, on a replacement basis, for costs incurred to repair

9

or rebuild each hotel, including loss of rental income during the reconstruction period. We have selected policy specifications and insured limits which we believe to be appropriate given the relative risk of loss, the cost of the coverage and industry practice. We do not carry insurance for generally uninsured losses, including, but not limited to losses caused by riots, war or acts of God. In the opinion of our management, our hotels are adequately insured.

Employees

As of December 31, 2012 we had 53 employees.

Corporate Information

Our principal executive offices are located at 3 Bethesda Metro Center, Suite 1000, Bethesda, Maryland 20814. Our telephone number is (301) 280-7777. Our website is located at www.rljlodgingtrust.com. The information that is found on or accessible through our website is not incorporated into, and does not form a part of, this Annual Report on Form 10-K or any other report or document that we file with or furnish to the SEC. We have included our website address in this Annual Report on Form 10-K as an inactive textual reference and do not intend it to be an active link to our website.

We make available on our website, free of charge, our Annual Report on Form 10-K, Quarterly Reports on Form 10-Q, Current Reports on Form 8-K and amendments to those reports filed or furnished pursuant to Section 13(a) or 15(d) of the Exchange Act as soon as reasonably practicable after we electronically file such material with, or furnish it to, the SEC. We also make our Code of Business Conduct and Ethics for our trustees, officers and employees available on our website on the Corporate Governance page under the Investor Relations section of our website.

This Annual Report on Form 10-K and other reports filed with the SEC can be read or copied at the SEC's Public Reference Room at 100 F Street, NE, Washington, D.C. 20549. Information on the operation of the Public Reference Room can be obtained by calling the SEC at 1-800-SEC-0330. The SEC maintains a website that contains reports, proxy and information statements, and other information regarding issuers that file electronically with the SEC; the website address is www.sec.gov.

Set forth below are the risks that we believe are material to our shareholders. You should carefully consider the following risks in evaluating our Company and our business. The occurrence of any of the following risks could materially adversely impact our financial condition, results of operations, cash flow, the market price of our common shares and our ability to, among other things, satisfy our debt service obligations and to make distributions to our shareholders, which in turn could cause our shareholders to lose all or a part of their investment. Some statements in this report including statements in the following risk factors constitute forward-looking statements. Please refer to the section entitled "Special Note About Forward-Looking Statements" at the beginning of our Annual Report on Form 10-K.

Risks Related to Our Business and Properties

We will continue to be significantly influenced by the economies and other conditions in the specific markets in which we operate, particularly in the metropolitan areas where we have high concentrations of hotels.

Our hotels located in the New York, New York, Chicago, Illinois, Austin, Texas, Denver-Boulder, Colorado, Louisville, Kentucky, and the Baltimore, Maryland-Washington, D.C. metropolitan areas accounted for approximately 15.8%, 12.1%, 10.5%, 8.8%, 6.5%, and 5.8%, respectively, of our total revenue for the fiscal year ended December 31, 2012. As a result, we are particularly susceptible to adverse market conditions in these areas, including industry downturns, relocation of businesses and

10

any oversupply of hotel rooms or a reduction in lodging demand. Adverse economic developments in the markets in which we have a concentration of hotels, or in any of the other markets in which we operate, or any increase in hotel supply or decrease in lodging demand resulting from the local, regional or national business climate, could materially and adversely affect us.

We are dependent on the performance of the third-party hotel management companies that manage the operations of each of our hotels and could be materially and adversely affected if such third-party managers do not manage our hotels in our best interests.

Because federal income tax laws restrict REITs and their subsidiaries from operating or managing hotels, we do not operate or manage our hotels. Instead, we lease all of our hotels to subsidiaries of our TRSs, and our TRS lessees retain third-party managers to operate our hotels pursuant to management agreements. We have entered into individual hotel management agreements for our hotels, 104 of which are with White Lodging Services, or WLS. We could be materially and adversely affected if any of our third-party managers fail to provide quality services and amenities, fail to maintain a quality brand name or otherwise fail to manage our hotels in our best interest. In addition, from time to time, disputes may arise between us and our third-party managers regarding their performance or compliance with the terms of the hotel management agreements, which in turn could adversely affect our results of operations. We generally will attempt to resolve any such disputes through discussions and negotiations; however, if we are unable to reach satisfactory results through discussions and negotiations, we may choose to terminate our management agreement, litigate the dispute or submit the matter to third-party dispute resolution, the outcome of which may be unfavorable to us.

Under the terms of the hotel management agreements, our ability to participate in operating decisions regarding our hotels is limited to certain matters, including approval of the annual operating budget, and we do not have the authority to require any hotel to be operated in a particular manner (for instance, setting room rates). While our TRS lessees closely monitor the performance of our third-party managers, our general recourse under the hotel management agreements is limited to termination upon sixty days' notice if we believe our third-party managers are not performing adequately. For example, we have a right to terminate a management agreement with WLS, our largest provider of management services, if WLS fails to achieve certain hotel performance criteria measured over any two consecutive fiscal years, as outlined in each WLS management agreement. However, even if WLS fails to perform under the terms of a management agreement, it has the option (exercisable a maximum of three times per hotel) to avoid a performance termination by paying a performance deficit fee as specified in the management agreement.

In the event that we terminate any of our management agreements, we can provide no assurances that we could find a replacement manager or that our franchisors will consent to a replacement manager in a timely manner, or at all, or that any replacement manager will be successful in operating our hotels. Furthermore, if WLS, as our largest provider of management services, is financially unable or unwilling to perform its obligations pursuant to our management agreements, our ability to find a replacement manager or managers for our WLS-managed hotels could be challenging and time consuming, depending on the number of WLS-managed hotels affected, and could cause us to incur significant costs to obtain new management agreements for the affected hotels. Accordingly, if we lose a significant number of our WLS management agreements, we could be materially and adversely affected. In addition, many of our existing franchise agreements provide the franchisor with a right of first offer in the event of certain sales or transfers of a hotel and provide that the franchisor has the right to approve any change in the hotel management company engaged to manage the hotel. If any of the foregoing were to occur, it could have a material adverse effect on us.

11

Restrictive covenants in certain of our hotel management and franchise agreements contain provisions limiting or restricting the sale or financing of our hotels, which could have a material adverse effect on us.

Hotel management and franchise agreements typically contain restrictive covenants that limit or restrict our ability to sell or refinance a hotel without the consent of the hotel management company or franchisor. Many of our franchise agreements provide the franchisor with a right of first offer in the event of certain sales or transfers of a hotel and provide that the franchisor has the right to approve any change in the hotel management company engaged to manage the hotel. Generally, we may not agree to sell, lease or otherwise transfer particular hotels unless the transferee is not a competitor of the hotel management company or franchisor and the transferee assumes the related hotel management and franchise agreements. For example, substantially all of our management agreements with WLS provide that any sale of a hotel to a purchaser who does not meet all of the requirements under the applicable franchise agreement associated with such hotel must be first approved by WLS. If the hotel management company or franchisor does not consent to the sale or financing of our hotels, we may be prohibited from taking actions that would otherwise be in our and our shareholders' best interests.

Substantially all of our hotels operate under either Marriott or Hilton brands; therefore, we are subject to risks associated with concentrating our portfolio in just two brand families.

133 of the 145 hotels that we owned as of December 31, 2012 utilize brands owned by Marriott or Hilton. As a result, our success is dependent in part on the continued success of Marriott and Hilton and their respective brands. We believe that building brand value is critical to increase demand and build customer loyalty. Consequently, if market recognition or the positive perception of Marriott and/or Hilton is reduced or compromised, the goodwill associated with the Marriott- and Hilton-branded hotels in our portfolio may be adversely affected. Furthermore, if our relationship with Marriott or Hilton were to deteriorate or terminate as a result of disputes regarding the management of our hotels or for other reasons, Marriott and/or Hilton could, under certain circumstances, terminate our current franchise licenses with them or decline to provide franchise licenses for hotels that we may acquire in the future. If any of the foregoing were to occur, it could have a material adverse effect on us.

Our long-term growth depends in part on successfully identifying and consummating acquisitions of additional hotels and the failure to make such acquisitions could materially impede our growth.

We can provide no assurances that we will be successful in identifying attractive hotels or that, once identified, we will be successful in consummating an acquisition. We face significant competition for attractive investment opportunities from other well-capitalized investors, some of which have greater financial resources and a greater access to debt and equity capital to acquire hotels than we do. This competition increases as investments in real estate become increasingly attractive relative to other forms of investment. As a result of such competition, we may be unable to acquire certain hotels that we deem attractive or the purchase price may be significantly elevated or other terms may be substantially more onerous. In addition, we expect to finance future acquisitions through a combination of borrowings under our unsecured revolving credit facility, the use of retained cash flows, and offerings of equity and debt securities, which may not be available on advantageous terms, or at all. Any delay or failure on our part to identify, negotiate, finance on favorable terms, consummate and integrate such acquisitions could materially impede our growth.

The departure of any of our key personnel who have significant experience and relationships in the lodging industry, including Robert L. Johnson, Thomas J. Baltimore, Jr. and Ross H. Bierkan, could materially and adversely affect us.

We depend on the experience and relationships of our senior management team, especially Robert L. Johnson, Executive Chairman of our board of trustees, Thomas J. Baltimore, Jr., our

12

President and Chief Executive Officer and a member of our board of trustees, and Ross H. Bierkan, our Chief Investment Officer, to manage our day-to-day operations and strategic business direction. Messrs. Johnson, Baltimore and Bierkan have 19, 24 and 27 years of experience in the lodging industry, respectively, during which time they have established an extensive network of lodging industry contacts and relationships, including relationships with global and national hotel brands, hotel owners, financiers, operators, commercial real estate brokers, developers and management companies. We can provide no assurances that any of our key personnel will continue their employment with us, even though all of the members of our senior management team have entered employment agreements with us. The loss of services of Messrs. Johnson, Baltimore or Bierkan, or of the services of other members of our senior management team, or any difficulty attracting and retaining other talented and experienced personnel, could adversely affect our ability to source potential investment opportunities, our relationship with global and national hotel brands and other industry participants and the execution of our business strategy. Further, such a loss could be negatively perceived in the capital markets, which could reduce the market value of our common shares.

Our business strategy depends on achieving revenue and net income growth from anticipated increases in demand for hotel rooms; accordingly, any delay or a weaker than anticipated economic recovery could materially and adversely affect us and our growth prospects.

Our hotels experienced declining operating performance across various U.S. markets during the most recent economic recession. Our business strategy depends on achieving revenue and net income growth from anticipated improvement in demand for hotel rooms as part of the continued economic recovery. As a result, any delay or a weaker than anticipated continued economic recovery could materially and adversely affect us and our growth prospects. Furthermore, even if the economy continues to recover, we cannot provide any assurances that demand for hotel rooms will increase from current levels. If demand does not increase in the near future, or if demand weakens, our future results of operations and our growth prospects could be materially and adversely affected.

The ongoing need for capital expenditures at our hotels could have a material adverse effect on us.

Our hotels have an ongoing need for renovations and other capital improvements, including replacements, from time to time, of furniture, fixtures and equipment. The franchisors of our hotels also require periodic capital improvements as a condition of maintaining the franchise licenses. In addition, our lenders will likely require that we set aside annual amounts for capital improvements to our hotels. The costs of these capital improvements could materially and adversely affect us.

Any difficulties in obtaining capital necessary to make required periodic capital expenditures and renovation of our hotels could materially and adversely affect our financial condition and results of operations.

Our hotels require periodic capital expenditures and renovation to remain competitive. In addition, acquisitions or redevelopment of additional hotels will require significant capital expenditures. We may not be able to fund capital improvements on our hotels or acquisitions of new hotels solely from cash provided from our operating activities because we must distribute annually at least 90% of our REIT taxable income, determined without regard to the deduction for dividends paid and excluding net capital gain, to maintain our qualification as a REIT, and we are subject to tax on any retained income and gain. As a result, our ability to fund capital expenditures, acquisitions or hotel redevelopment through retained earnings is very limited. Consequently, we expect to rely upon the availability of debt or equity capital to fund capital improvements and acquisitions. If we are unable to obtain the capital necessary to make required periodic capital expenditures and renovate our hotels on favorable terms, or at all, our financial condition, liquidity and results of operations could be materially and adversely affected.

13

Adverse global market and economic conditions and dislocations in the markets could cause us to recognize impairment charges, which could materially and adversely affect our business, financial condition and results of operations.

We continually monitor events and changes in circumstances, including those resulting from the recent economic downturn that could indicate that the carrying value of the real estate and related intangible assets in which we have an ownership interest may not be recoverable. When circumstances indicate that the carrying value of real estate and related intangible assets may not be recoverable, we assess the recoverability of these assets by determining whether the carrying value will be recovered through the undiscounted future operating cash flows expected from the use of the asset and its eventual disposition. In the event that such expected undiscounted future cash flows do not exceed the carrying value, we adjust the real estate and related intangible assets to the fair value and recognize an impairment loss. Because our predecessor acquired many of our hotels in the last five years, when prices for hotels in many markets were at or near their peaks, we may be particularly susceptible to future non-cash impairment charges as compared to companies that have carrying values well below current market values, which could materially and adversely affect our business, financial condition and results of operations. During the fiscal year ended December 31, 2012, we recognized an impairment charge on the Fairfield Inn Memphis of $0.9 million.

Projections of expected future cash flows require management to make assumptions to estimate future occupancy, hotel operating expenses, and the number of years the hotel is held for investment, among other factors. The subjectivity of assumptions used in the future cash flow analysis, including discount rates, could result in an incorrect assessment of the hotel's fair value and, therefore, could result in the misstatement of the carrying value of our real estate and related intangible assets on our balance sheet and our results of operations. Ongoing adverse market and economic conditions and market volatility will likely continue to make it difficult to value the hotels owned by us, as well as the value of our intangible assets. As a result of adverse market and economic conditions, there may be significant uncertainty in the valuation, or in the stability of, the cash flows, discount rates and other factors related to such assets that could result in a substantial decrease in their value.

Competition from other hotels in the markets in which we operate could adversely affect occupancy levels and/or ADRs, which could have a material adverse effect on us.

We face significant competition from owners and operators of other hotels. These competitors may have an operating model that enables them to offer rooms at lower rates than we can, which could result in those competitors increasing their occupancy at our expense and adversely affecting our ADRs. Given the importance of occupancy and ADR at focused-service and compact full-service hotels, this competition could adversely affect our ability to attract prospective guests, which could materially and adversely affect our results of operations.

The RevPAR penetration index may not accurately reflect our hotels' respective market shares.

We use the RevPAR penetration index, which measures a hotel's RevPAR in relation to the average RevPAR of that hotel's competitive set, as an indicator of a hotel's market share in relation to its competitive set. However, as a particular hotel's competitive set is selected by us and the hotel management company that manages such hotel, no assurance can be given that a competitive set consisting of different hotels would not lead to a more accurate measure of such hotel's market share. As such, the RevPAR penetration index may not accurately reflect our hotels' respective market shares.

14

At December 31, 2012, we had approximately $1.4 billion of debt outstanding, which may materially and adversely affect our operating performance and put us at a competitive disadvantage.

Required repayments of debt and related interest may materially and adversely affect our operating performance. At December 31, 2012, we had approximately $1.4 billion of outstanding debt, approximately $643.0 million of which bears interest at variable rates. Increases in interest rates on our existing or future variable rate debt would increase our interest expense, which could adversely affect our cash flows and our ability to pay distributions to shareholders.

Because we anticipate that our internally generated cash will be adequate to repay only a portion of our debt at maturity, we expect that we will be required to repay debt through debt refinancings and/or offerings of our securities. The amount of our outstanding debt may adversely affect our ability to refinance our debt.

If we are unable to refinance our debt on acceptable terms, or at all, we may be forced to dispose of one or more of our hotels on disadvantageous terms, which may result in losses to us and may adversely affect cash available for distributions to our shareholders. In addition, if then-prevailing interest rates or other factors at the time of refinancing result in higher interest rates upon refinancing, our interest expense would increase, which would adversely affect our future operating results and liquidity.

Our substantial outstanding debt may harm our business, financial condition, liquidity, EBITDA, Funds from Operations, or FFO, and results of operations, including:

- •

-

requiring us to use a substantial portion of our cash flows to pay principal and interest, which would reduce the cash

available for distributions to our shareholders;

- •

-

placing us at a competitive disadvantage compared to our competitors that have less debt;

- •

-

making us vulnerable to the ongoing economic recovery, particularly if the recovery were to slow or stall and reduce our

flexibility to respond to difficult economic conditions; and

- •

- limiting our ability to borrow more money for operations, capital or to finance future acquisitions.

The use of debt to finance future acquisitions could restrict operations, inhibit our ability to grow our business and revenues, and negatively affect our business and financial results.

We may incur additional debt in connection with future hotel acquisitions. We may, in some instances, borrow under our unsecured revolving credit facility or borrow new funds to acquire hotels. In addition, we may incur mortgage debt by obtaining loans secured by a portfolio of some or all of the hotels that we own or acquire. If necessary or advisable, we also may borrow funds to make distributions to our shareholders in order to maintain our qualification as a REIT for U.S. federal income tax purposes. To the extent that we incur debt in the future and do not have sufficient funds to repay such debt at maturity, it may be necessary to refinance the debt through debt or equity financings, which may not be available on acceptable terms or at all and which could be dilutive to our shareholders. If we are unable to refinance our debt on acceptable terms or at all, we may be forced to dispose of hotels at inopportune times or on disadvantageous terms, which could result in losses. To the extent we cannot meet our future debt service obligations, we will risk losing to foreclosure some or all of our hotels that may be pledged to secure our obligations.

For tax purposes, a foreclosure of any of our hotels would be treated as a sale of the hotel for a purchase price equal to the outstanding balance of the debt secured by the mortgage. If the outstanding balance of the debt secured by the mortgage exceeds our tax basis in the hotel, we would recognize taxable income on foreclosure, but we would not receive any cash proceeds, which could hinder our ability to meet the REIT distribution requirements imposed by the Internal Revenue Code

15

of 1986, as amended, or the Code. In addition, we may give full or partial guarantees to lenders of mortgage debt on behalf of the entities that own our hotels. When we give a guarantee on behalf of an entity that owns one of our hotels, we will be responsible to the lender for satisfaction of the debt if it is not paid by such entity. If any of our hotels are foreclosed on due to a default, our ability to pay cash distributions to our shareholders will be limited.

Our organizational documents have no limitation on the amount of indebtedness we may incur. As a result, we may become highly leveraged in the future, which could materially and adversely affect us.

Our business strategy contemplates the use of both non-recourse secured and unsecured debt to finance long-term growth. In addition, our organizational documents contain no limitations on the amount of debt that we may incur, and our board of trustees may change our financing policy at any time without shareholder notice or approval. As a result, we may be able to incur substantial additional debt, including secured debt, in the future. Incurring debt could subject us to many risks, including the risks that:

- •

-

our cash flows from operations may be insufficient to make required payments of principal and interest;

- •

-

our debt may increase our vulnerability to adverse economic and industry conditions;

- •

-

we may be required to dedicate a substantial portion of our cash flows from operations to payments on our debt, thereby

reducing cash available for distribution to our shareholders, funds available for operations and capital expenditures, future business opportunities or other purposes;

- •

-

the terms of any refinancing may not be in the same amount or on terms as favorable as the terms of the existing debt

being refinanced; and

- •

- the use of leverage could adversely affect our ability to raise capital from other sources or to make distributions to our shareholders and could adversely affect the market price of our common shares.

If we violate covenants in future agreements relating to indebtedness that we may incur, we could be required to repay all or a portion of our indebtedness before maturity at a time when we might be unable to arrange financing for such repayment on attractive terms, if at all. In addition, future indebtedness agreements may require that we meet certain covenant tests in order to make distributions to our shareholders.

Disruptions in the financial markets could adversely affect our ability to obtain sufficient third-party financing for our capital needs, including expansion, acquisition and other activities, on favorable terms or at all, which could materially and adversely affect us.

In recent years, the U.S. stock and credit markets have experienced significant price volatility, dislocations and liquidity disruptions, which have caused market prices of many stocks to fluctuate substantially and the spreads on prospective debt financings to widen considerably. These circumstances have materially impacted liquidity in the financial markets, making terms for certain financings less attractive, and in some cases have resulted in the unavailability of financing, even for companies which otherwise are qualified to obtain financing. In addition, several banks and other institutions that historically have been reliable sources of financing have gone out of business, which has reduced significantly the number of lending institutions and the availability of credit. Continued volatility and uncertainty in the stock and credit markets may negatively impact our ability to access additional financing for our capital needs, including expansion, acquisition activities and other purposes, on favorable terms or at all, which may negatively affect our business. Additionally, due to this uncertainty, we may in the future be unable to refinance or extend our debt, or the terms of any refinancing may

16

not be as favorable as the terms of our existing debt. If we are not successful in refinancing our debt when it becomes due, we may be forced to dispose of hotels on disadvantageous terms, which might adversely affect our ability to service other debt and to meet our other obligations. A prolonged downturn in the financial markets may cause us to seek alternative sources of potentially less attractive financing and may require us to further adjust our business plan accordingly. These events also may make it more difficult or costly for us to raise capital through the issuance of new equity capital or the incurrence of additional secured or unsecured debt, which could materially and adversely affect us.

Hedging against interest rate exposure may adversely affect us.

Subject to maintaining our qualification as a REIT, we may manage our exposure to interest rate volatility by using interest rate hedging arrangements, such as cap agreements and swap agreements. These agreements involve the risks that these arrangements may fail to protect or adversely affect us because, among other things:

- •

-

interest rate hedging can be expensive, particularly during periods of rising and volatile interest rates;

- •

-

available interest rate hedges may not correspond directly with the interest rate risk for which protection is sought;

- •

-

the duration of the hedge may not match the duration of the related liability;

- •

-

the credit quality of the hedging counterparty owing money on the hedge may be downgraded to such an extent that it

impairs our ability to sell or assign our side of the hedging transaction; and

- •

- the hedging counterparty owing money in the hedging transaction may default on its obligation to pay.

As a result of any of the foregoing, our hedging transactions, which are intended to limit losses, could have a material adverse effect on us.

Our failure to comply with all covenants in our existing or future debt agreements could materially and adversely affect us.

The mortgages on our hotels, and hotels that we may acquire in the future likely will, contain customary covenants such as those that limit our ability, without the prior consent of the lender, to further mortgage the applicable hotel or to discontinue insurance coverage. In addition, our continued ability to borrow under our unsecured revolving credit facility is subject to compliance with our financial and other covenants, including covenants relating to debt service coverage ratios and leverage ratios, and our ability to meet these covenants will be adversely affected if U.S. lodging fundamentals do not continue to improve to the extent that we expect. In addition, any credit facility or secured loans that we enter into in the future likely will contain customary financial covenants, restrictions, requirements and other limitations with which we must comply. Our failure to comply with covenants in our existing or future indebtedness, as well as our inability to make required payments, could cause a default under the applicable debt agreement, which could result in the acceleration of the debt and require us to repay such debt with capital obtained from other sources, which may not be available to us or may be available only on unattractive terms. Furthermore, if we default on secured debt, lenders can take possession of the hotel or hotels securing such debt. In addition, debt agreements may contain specific cross-default provisions with respect to specified other indebtedness, giving the lenders the right to declare a default on its debt and to enforce remedies, including acceleration of the maturity of such debt upon the occurrence of a default under such other indebtedness. If we default on several of our debt agreements or any significant debt agreement, we could be materially and adversely affected.

17

Covenants applicable to future debt could restrict our ability to make distributions to our shareholders and, as a result, we may be unable to make distributions necessary to maintain our qualification as a REIT, which could materially and adversely affect us and the market price of our common shares.

We intend to continue to operate in a manner so as to maintain our qualification as a REIT for U.S. federal income tax purposes. In order to qualify as a REIT, we generally are required to distribute at least 90% of our REIT taxable income, determined without regard to the dividends paid deduction and excluding net capital gain, each year to our shareholders. To the extent that we satisfy this distribution requirement, but distribute less than 100% of our REIT taxable income, we will be subject to U.S. federal corporate income tax on our undistributed taxable income. In addition, we will be subject to a 4% nondeductible excise tax if the actual amount that we distribute to our shareholders in a calendar year is less than a minimum amount specified under the Code. In order to meet the REIT requirements, we may be required to issue common shares of beneficial interest in lieu of cash distributions. If, as a result of covenants applicable to our future debt, we are restricted from making distributions to our shareholders, we may be unable to make distributions necessary for us to avoid U.S. federal corporate income and excise taxes and maintain our qualification as a REIT, which could materially and adversely affect us and the market price of our shares.

We may change the distribution policy for our common shares of beneficial interest in the future.

Our management and Board of Trustees will continue to evaluate our distribution policy on a quarterly basis as they monitor the capital markets, the impact of the economy on our operations and other factors. Future distributions will be declared and paid at the discretion of our board of trustees and will depend upon a number of factors, including our actual and projected financial condition, liquidity, EBITDA, FFO and results of operations, the revenue we actually receive from our properties, our operating expenses, our debt service requirements, our capital expenditures, prohibitions and other limitations under our financing arrangements, our REIT taxable income, the annual REIT distribution requirements, applicable law and such other factors as our board of trustees deems relevant. Any change in our distribution policy could have a material adverse effect on the market price of our common shares.

Costs associated with, or failure to maintain, franchisor operating standards may materially and adversely affect us.

Under the terms of our franchise license agreements, we are required to meet specified operating standards and other terms and conditions. We expect that our franchisors will periodically inspect our hotels to ensure that we and the hotel management companies follow brand standards. Failure by us, or any hotel management company that we engage, to maintain these standards or other terms and conditions could result in a franchise license being canceled or the franchisor requiring us to undertake a costly property improvement program. If a franchise license is terminated due to our failure to make required improvements or to otherwise comply with its terms, we also may be liable to the franchisor for a termination payment, which will vary by franchisor and by hotel. Furthermore, under certain circumstances, a franchisor may require us to make capital expenditures, even if we do not believe the capital improvements are necessary or desirable or will result in an acceptable return on our investment. If the funds required to maintain franchisor operating standards are significant, or if a franchise license is terminated, we could be materially and adversely affected.

If we were to lose a franchise license at one or more of our hotels, the value of the affected hotels could decline significantly and we could incur significant costs to obtain new franchise licenses, which could have a material adverse effect on us.

If we were to lose a franchise license, we would be required to re-brand the affected hotel(s). As a result, the underlying value of a particular hotel could decline significantly from the loss of associated

18

name recognition, marketing support, participation in guest loyalty programs and the centralized system provided by the franchisor, which could require us to recognize an impairment on the hotel. Furthermore, the loss of a franchise license at a particular hotel could harm our relationship with the franchisor, which could impede our ability to operate other hotels under the same brand, limit our ability to obtain new franchise licenses from the franchisor in the future on favorable terms, or at all, and cause us to incur significant costs to obtain a new franchise license for the particular hotel. Accordingly, if we lose one or more franchise licenses, we could be materially and adversely affected.

Applicable REIT laws may restrict certain business activities.

As a REIT, we are subject to various restrictions on our income, assets and activities. Business activities that could be impacted by applicable REIT laws include, but are not limited to, activities such as developing alternative uses of real estate, including the development and/or sale of timeshare or condominium units. Due to these restrictions, we anticipate that we will continue to conduct certain business activities, including those mentioned above, in one or more of our TRSs. Our TRSs are taxable as regular C corporations and are subject to federal, state, local, and, if applicable, foreign taxation on their taxable income. In addition, neither we, nor our TRSs can directly manage or operate hotels, making us entirely dependent on unrelated third-party operators/managers.

Federal income tax provisions applicable to REITs may restrict our business decisions regarding the potential sale of a hotel.

The federal income tax provisions applicable to REITs provide that any gain realized by a REIT on the sale of property held as inventory or other property held primarily for sale to customers in the ordinary course of business is treated as income from a "prohibited transaction" that is subject to a 100% excise tax. Under existing law, whether property, including hotels, is held as inventory or primarily for sale to customers in the ordinary course of business is a question of fact that depends upon all of the facts and circumstances with respect to the particular transaction. We intend to hold our hotels for investment with a view to long-term appreciation, to engage in the business of acquiring and owning hotels and to make occasional sales of hotels consistent with our investment objectives. There can be no assurance, however, that the Internal Revenue Service, or the IRS, might not contend that one or more of these sales are subject to the 100% excise tax. Moreover, the potential application of this penalty tax could deter us from selling one or more hotels even though it otherwise would be in the best interests of us and our shareholders for us to do so. There is a statutory safe harbor available for a limited number of sales in a single taxable year of properties that have been owned by a REIT for at least two years, but that safe harbor likely would not apply to all sales transactions that we might otherwise consider. As a result, we may not be able to vary our portfolio promptly in response to economic or other conditions or on favorable terms, which may adversely affect us.

Joint venture investments that we make could be adversely affected by our lack of sole decision-making authority, our reliance on joint venture partners' financial condition and liquidity and disputes between us and our joint venture partners.

We own the Doubletree Metropolitan Hotel New York City through a joint venture with an affiliate of the hotel's property manager. In addition, we may enter into joint ventures in the future to acquire, develop, improve or partially dispose of hotels, thereby reducing the amount of capital required by us to make investments and diversifying our capital sources for growth. Such joint venture investments involve risks not otherwise present in a wholly-owned hotel or a redevelopment project, including the following:

- •

- we may not have exclusive control over the development, financing, leasing, management and other aspects of the hotel or joint venture, which may prevent us from taking actions that are in our best interest but opposed by our partners;

19

- •

-

joint venture agreements often restrict the transfer of a partner's interest or may otherwise restrict our ability to sell

the interest when we desire or on advantageous terms;

- •

-

joint venture agreements may contain buy-sell provisions pursuant to which one partner may initiate procedures

requiring the other partner to choose between buying the other partner's interest or selling its interest to that partner;

- •

-

we may not be in a position to exercise sole decision-making authority regarding the hotel or joint venture, which could

create the potential risk of creating impasses on decisions, such as acquisitions or sales;

- •

-

a partner may, at any time, have economic or business interests or goals that are, or that may become, inconsistent with

our business interests or goals;

- •

-

a partner may be in a position to take action contrary to our instructions, requests, policies or objectives, including

our current policy with respect to maintaining our qualification as a REIT;

- •

-

a partner may fail to fund its share of required capital contributions or may become bankrupt, which would mean that we

and any other remaining partners generally would remain liable for the joint venture's liabilities;

- •

-

relationships with joint-venture partners are contractual in nature and may be terminated or dissolved under the terms of

the applicable joint venture agreements and, in such event, we may not continue to own or operate the interests or assets underlying such relationship or may need to purchase such interests or assets

at a premium to the market price to continue ownership;

- •

-

disputes between us and a partner may result in litigation or arbitration that would increase our expenses and prevent our

officers and trustees from focusing their time and efforts on our business and could result in subjecting the hotels owned by the joint venture to additional risk; or

- •

- we may, in certain circumstances, be liable for the actions of a partner, and the activities of a partner could adversely affect our ability to qualify as a REIT, even though we do not control the joint venture.

Any of the above might subject a hotel to liabilities in excess of those contemplated and adversely affect the value of our current and future joint venture investments.

Risks Related to the Lodging Industry

Our ability to make distributions to our shareholders may be adversely affected by various operating risks common to the lodging industry, including competition, over-building and dependence on business travel and tourism.

The hotels that we own have different economic characteristics than many other real estate assets. A typical office property, for example, has long-term leases with third-party tenants, which provides a relatively stable long-term stream of revenue. Hotels, on the other hand, generate revenue from guests that typically stay at the hotel for only a few nights, which causes the room rate and occupancy levels at each of our hotels to change every day, and results in earnings that can be highly volatile.

In addition, our hotels are subject to various operating risks common to the lodging industry, many of which are beyond our control, including, among others, the following:

- •

-

competition from other hotels in the markets in which we operate;

- •

- over-building of hotels in the markets in which we operate, which results in increased supply and will adversely affect occupancy and revenues at our hotels;

20

- •

-

dependence on business and commercial travelers and tourism;

- •

-

labor strikes, disruptions or lockouts that may impact operating performance;

- •

-

increases in energy costs and other expenses affecting travel, which may affect travel patterns and reduce the number of

business and commercial travelers and tourists;

- •

-

requirements for periodic capital reinvestment to repair and upgrade hotels;

- •

-

increases in operating costs due to inflation and other factors that may not be offset by increased room rates;

- •

-

changes in interest rates;

- •

-

changes in the availability, cost and terms of financing;

- •

-

changes in governmental laws and regulations, fiscal policies and zoning ordinances and the related costs of compliance

with laws and regulations, fiscal policies and ordinances;

- •

-

adverse effects of international, national, regional and local economic and market conditions;

- •

-

unforeseen events beyond our control, such as terrorist attacks, travel-related health concerns, including pandemics and