UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 20-F

¨

REGISTRATION STATEMENT PURSUANT TO SECTION 12(b) OR (g) OF THE SECURITIES EXCHANGE ACT OF 1934

OR

x

ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934

For the fiscal year ended December 31, 2010

OR

¨

TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934

OR

¨

SHELL COMPANY REPORT PURSUANT TO SECTION 23 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934

Date of event requiring this shell company report_______________________________ .

For the transition period from _____________to__________ .

Commission file number

33-65728

SOCIEDAD QUIMICA Y MINERA DE CHILE S.A.

(Exact name of registrant as specified in its charter)

CHEMICAL AND MINING COMPANY OF CHILE INC.

(Translation of registrant's name into English)

CHILE

(Jurisdiction of incorporation or organization)

El Trovador 4285, 6

th

Floor, Santiago, Chile +56 2 425-2000

(Address of principal executive offices)

Securities registered or to be registered pursuant to Section 12(b) of the Act.

|

Title of each class

|

Name of each exchange on which registered

|

|

|

Series B shares, in the form of American Depositary Shares

|

New York Stock Exchange

|

Securities registered or to be registered pursuant to Section 12(g) of the Act.

NONE

Securities for which there is a reporting obligation pursuant to Section 15(d) of the Act.

NONE

Indicate the number of outstanding shares of each of the issuer's classes of capital or common stock as of the close of the period covered by the annual report.

Series A shares 142,819,552

Series B shares 120,376,972

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in rule 405 of the Securities Act:

x

YES

¨

NO

If this report is an annual or transition report, indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or 15(d) of the Securities Exchange act of 1934:

¨

YES

x

NO

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days.

x

YES

¨

NO

Indicate by check mark whether the registrant has submitted electronically and posted on its corporate Web site, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T (

§

232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files).

¨

YES

¨

NO

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, or a non accelerated filer. See definition of “accelerated filer and large accelerated filer” in rule 12b-2 of the Exchange Act.

x

Large accelerated filer

¨

Accelerated filer

¨

Non- accelerated filer

Indicate by check mark which basis of accounting the registrant has used to prepare the financial statements included in this filing:

¨

U.S. GAAP

x

International Financial Reporting Standards as issued by the International Accounting Standards Board

¨

Other

If “Other” has been checked in response to the previous question, indicate by check mark which financial statement item the registrant has elected to follow.

Indicate by check mark which financial statement item the registrant has elected to follow.

¨

Item 17

x

Item 18

If this is an annual report, indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act):

¨

YES

x

NO

TABLE OF CONTENTS

|

Page

|

||||||

|

PRESENTATION OF INFORMATION

|

iii

|

|||||

|

GLOSSARY

|

iii

|

|||||

|

CAUTIONARY STATEMENT REGARDING FORWARD-LOOKING STATEMENTS

|

vi

|

|||||

|

PART I

|

2 | |||||

|

ITEM 1.

|

IDENTITY OF DIRECTORS, SENIOR MANAGEMENT AND ADVISERS

|

2 | ||||

|

ITEM 2.

|

OFFER STATISTICS AND EXPECTED TIMETABLE

|

2 | ||||

|

ITEM 3.

|

KEY INFORMATION

|

2 | ||||

|

ITEM 4.

|

INFORMATION ON THE COMPANY

|

15 | ||||

|

ITEM 5.

|

OPERATING AND FINANCIAL REVIEW AND PROSPECTS

|

54 | ||||

|

ITEM 6.

|

DIRECTORS, SENIOR MANAGEMENT AND EMPLOYEES

|

71 | ||||

|

ITEM 7.

|

MAJOR SHAREHOLDERS AND RELATED PARTY TRANSACTIONS

|

84 | ||||

|

ITEM 8.

|

FINANCIAL INFORMATION

|

87 | ||||

|

ITEM 9.

|

THE OFFER AND LISTING

|

90 | ||||

|

ITEM 10.

|

ADDITIONAL INFORMATION

|

93 | ||||

|

ITEM 11.

|

QUANTITATIVE AND QUALITATIVE DISCLOSURES ABOUT MARKET RISK

|

106 | ||||

|

ITEM 12.

|

DESCRIPTION OF SECURITIES OTHER THAN EQUITY SECURITIES

|

108 | ||||

|

PART II

|

109 | |||||

|

ITEM 13.

|

DEFAULTS, DIVIDEND ARREARAGES AND DELINQUENCIES

|

109 | ||||

|

ITEM 14.

|

MATERIAL MODIFICATIONS TO THE RIGHTS OF SECURITY HOLDERS AND USE OF PROCEEDS

|

109 | ||||

|

ITEM 15.

|

CONTROLS AND PROCEDURES

|

109 | ||||

|

ITEM 16.

|

RESERVED

|

110 | ||||

|

ITEM 16.a.

|

AUDIT COMMITTEE FINANCIAL EXPERT

|

110 | ||||

|

ITEM 16.B.

|

CODE OF ETHICS

|

110 | ||||

|

ITEM 16.C

|

PRINCIPAL ACCOUNTANT FEES AND SERVICES

|

111 | ||||

|

ITEM 16.D

|

EXEMPTIONS FROM THE LISTING STANDARDS FOR AUDIT COMMITTEES

|

111 | ||||

|

ITEM 16.E

|

PURCHASES OF EQUITY SECURITIES BY THE ISSUERS AND AFFILIATED PURCHASERS.

|

111 | ||||

|

ITEM 16.F

|

CHANGE IN REGISTRANT'S CERTIFYING ACCOUNTANT.

|

112 | ||||

|

ITEM 16.G

|

CORPORATE GOVERNANCE.

|

112 | ||||

|

PART III

|

113 | |||||

|

ITEM 17.

|

FINANCIAL STATEMENTS

|

113 | ||||

|

ITEM 18.

|

FINANCIAL STATEMENTS

|

113 | ||||

|

ITEM 19.

|

EXHIBITS

|

113 | ||||

|

SIGNATURES

|

114 | |||||

|

CONSOLIDATED FINANCIAL STATEMENTS

|

115 | |||||

|

EXHIBIT 1.1

|

||||||

|

EXHIBIT 8.1

|

||||||

|

EXHIBIT 12.1

|

||||||

|

EXHIBIT 12.2

|

||||||

|

EXHIBIT 13.1

|

||||||

|

EXHIBIT 13.2

|

||||||

|

EXHIBIT 15.1

|

||||||

ii

PRESENTATION OF INFORMATION

In this Annual Report on Form 20-F, unless the context requires otherwise, all references to "

we

", "

us

", "

Company

" or "

SQM

" are to Sociedad Química y Minera de Chile S.A., an open stock corporation (

sociedad anónima abierta

) organized under the laws of the Republic of Chile, and its consolidated subsidiaries.

All references to "

$

," "

US$

," "

U.S. dollars,

" “USD” and "

dollars

" are to United States dollars, references to "

pesos,

" “CLP” and "

Ch$

" are to Chilean pesos, references to ThUS$ are to thousands of United States dollars, references to ThCh$ are to thousands of Chilean pesos and references to "

UF

" are to

Unidades de Fomento

. The UF is an inflation-indexed, peso-denominated unit that is linked to, and adjusted daily to reflect changes in, the previous month's Chilean consumer price index. As of May 31, 2011, UF 1.00 was equivalent to US$46.89 and Ch$21,809.84.

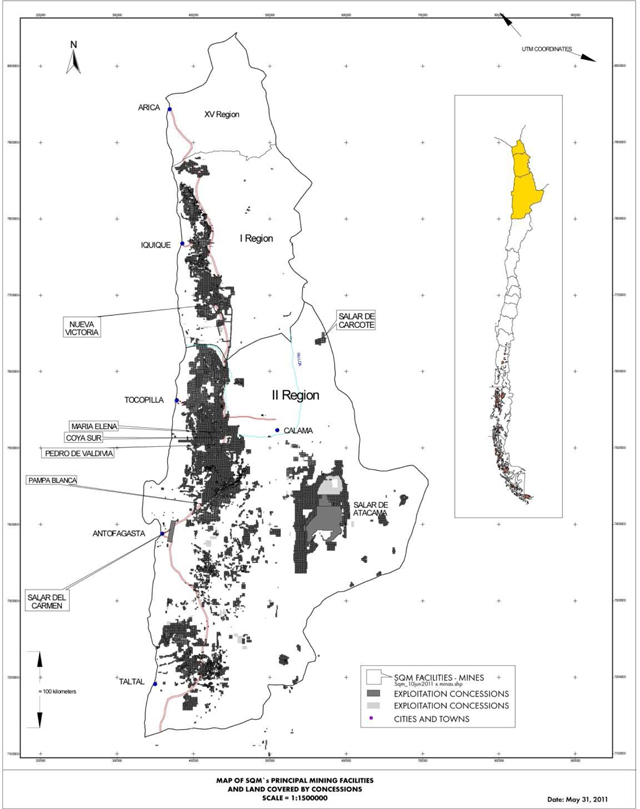

The Republic of Chile is governed by a democratic government, organized in fourteen regions plus the Metropolitan Region (surrounding and including Santiago, the capital of Chile). Our production operations are concentrated in northern Chile, specifically in the Tarapacá Region and in the Antofagasta Region.

Our fiscal year ends on December 31.

We use the metric system of weights and measures in calculating our operating and other data. The United States equivalent units of the most common metric units used by us are as shown below:

1 kilometer equals approximately 0.6214 miles

1 meter equals approximately 3.2808 feet

1 centimeter equals approximately 0.3937 inches

1 hectare equals approximately 2.4710 acres

1 metric ton (“MT”) equals 1,000 kilograms or approximately 2,205 pounds.

We are not aware of any independent, authoritative source of information regarding sizes, growth rates or market shares for most of our markets. Accordingly, the market size, market growth rate and market share estimates contained herein have been developed by us using internal and external sources and reflect our best current estimates. These estimates have not been confirmed by independent sources.

Percentages and certain amounts contained herein have been rounded for ease of presentation. Any discrepancies in any figure between totals and the sums of the amounts presented are due to rounding.

GLOSSARY

"

assay values

" Chemical result or mineral component amount that contains the sample.

"

average global metallurgical recoveries

" Percentage that measures the metallurgical treatment effectiveness based on the quantitative relationship between the initial product contained in the mine-extracted material and the final product produced in the plant.

"

average mining exploitation factor

" Index or ratio that measures the mineral exploitation effectiveness, based on the quantitative relationship between (in-situ mineral minus exploitation losses) / in-situ mineral.

“cash and cash equivalents”

The International Accounting Standards Board (IASB) defines cash and cash equivalents as short-term, highly liquid investments that are readily convertible to known amounts of cash and which are subject to an insignificant risk of changes in value.

“Controller Group

” A person or company or group of persons or companies that have executed a joint performance agreement, that have a direct or indirect share in a company’s ownership and have the power to influence the decisions of the company’s management.

"

Corfo

" Production Development Corporation (

Corporación de Fomento de la Producción

), formed in 1939, a national organization in charge of promoting Chile's manufacturing productivity and commercial development.

"

cut-off grade

" The minimal assay value or chemical amount of some mineral component above which exploitation is economical.

iii

"

dilution

" Loss of mineral grade because of contamination with barren material (or waste) incorporated in some exploited ore mineral.

"

exploitation losses

" Amounts of ore mineral that have not been extracted in accordance with exploitation designs.

"

fertigation

" The process by which plant nutrients are applied to the ground using an irrigation system.

"

geostatistical analysis

" Statistical tools applied to mining planning, geology and geochemical data that allow estimation of averages, grades and quantities of mineral resources and reserves.

"

heap leaching

" A process whereby minerals are leached from a heap, or pad, of crushed ore by leaching solutions percolating down through the heap and collected from a sloping, impermeable liner below the pad.

"

horizontal layering

" Rock mass (stratiform seam) with generally uniform thickness that conform to the sedimentary fields (mineralized and horizontal rock in these cases).

"

hypothetical resources

" Mineral resources that have limited geochemical reconnaissance, based mainly on geological data and samples assay values spaced between 500–1000 meters.

"

Indicated Mineral Resource

" See "Resources—Indicated Mineral Resource."

"

Inferred Mineral Resource

" See "Resources—Inferred Mineral Resource."

"

industrial crops

" Refers to crops that require processing after harvest in order to be ready for consumption or sale. Tobacco, tea and seed crops are examples of industrial crops.

“Kriging Method”

A technique used to estimate ore reserves, in which the spatial distribution of continuous geophysical variables is estimated using control points where values are known.

"LIBOR"

London Inter Bank Offered Rate.

"

limited reconnaissance

" Low or limited level of geological knowledge.

"

Measured Mineral Resource

" See "Resources—Measured Mineral Resource."

"

metallurgical treatment

" A set of chemical and physical processes applied to rocks to extract their useful minerals (or metals).

"

ore depth

" Depth of the mineral that may be economically exploited.

"

ore type

" Main mineral having economic value contained in the caliche ore (sodium nitrate or iodine).

"

ore

" A mineral or rock from which a substance having economic value may be extracted.

"

Probable Mineral Reserve

" See "Reserves—Probable Mineral Reserve."

"

Proved Mineral Reserve

" See "Reserves—Proved Mineral Reserve."

"

Reserves—Probable Mineral Reserve

"* The economically mineable part of an Indicated Mineral Resource and, in some circumstances, Measured Mineral Resource. The calculation of the reserves includes diluting of materials and allowances for losses which may occur when the material is mined. Appropriate assessments, which may include feasibility studies, have been carried out and include consideration of and modification by realistically assumed mining, metallurgical, economic, marketing, legal, environmental, social and governmental factors. These assessments demonstrate at the time of reporting that extraction is reasonably justified. A Probable Mineral Reserve has a lower level of confidence than a Proved Mineral Reserve.

"

Reserves—Proved Mineral Reserve

"* The economically mineable part of a Measured Mineral Resource. The calculation of the reserves includes diluting materials and allowances for losses which may occur when the material is mined. Appropriate assessments, which may include feasibility studies, have been carried out and include consideration of and modification by realistically assumed mining, metallurgical, economic, marketing, legal, environmental, social and governmental factors. These assessments demonstrate at the time of reporting that extraction is reasonably justified.

"

Resources—Indicated Mineral Resource

"* That part of a Mineral Resource for which tonnage, densities, shape, physical characteristics, grade and mineral content can be estimated with a reasonable level of confidence. The calculation is based on exploration, sampling and testing information gathered through appropriate techniques from locations such as outcrops, trenches, pits, workings, and drill holes. The locations are too widely or inappropriately spaced to confirm geological continuity and/or grade continuity but are spaced closely enough for continuity to be assumed. An Indicated Mineral Resource has a lower level of confidence than that applying to a Measured Mineral Resource, but has a higher level of confidence than that applying to an Inferred Mineral Resource.

iv

A deposit may be classified as an Indicated Mineral Resource when the nature, quality, amount and distribution of data are such as to allow the Competent Person determining the Mineral Resource to confidently interpret the geological framework and to assume continuity of mineralization. Confidence in the estimate is sufficient to allow the appropriate application of technical and economic parameters and to enable an evaluation of economic viability.

"

Resources—Inferred Mineral Resource

"* That part of a Mineral Resource for which tonnage, grade and mineral content can be estimated with a low level of confidence, by inferring them on the basis of geological evidence and assumed but not verified geological and/or grade continuity. The estimate is based on information gathered through appropriate techniques from locations such as outcrops, trenches, pits, workings and drill holes, and this information is of limited or uncertain quality and/or reliability. An Inferred Mineral Resource has a lower level of confidence than that applying to an Indicated Mineral Resource.

"

Resources—Measured Mineral Resource

"* The part of a Mineral Resource for which tonnage, densities, shape, physical characteristics, grade and mineral content can be estimated with a high level of confidence. The estimate is based on detailed and reliable exploration, sampling and testing information gathered through appropriate techniques from locations such as outcrops, trenches, pits, workings, and drill holes. The locations are spaced closely enough to confirm geological and/or grade continuity.

A deposit may be classified as a Measured Mineral Resource when the nature, quality, amount and distribution of data are such as to leave no reasonable doubt, in the opinion of the Competent Person determining the Mineral Resource, that the tonnage and grade of the deposit can be estimated within close limits and that any variation from the estimate would not significantly affect potential economic viability. This category requires a high level of confidence in, and understanding of, the geology and controls of the mineral deposit. Confidence in the estimate is sufficient to allow the appropriate application of technical and economic parameters and to enable an evaluation of economic viability.

“vat leaching”

A process whereby minerals are extracted from crushed ore by placing the ore in large vats containing leaching solutions.

"

waste

" Rock or mineral which is not economical for metallurgical treatment.

"

Weighted Average Age

" The sum of the product of the age of each fixed asset at a given facility and its current gross book value as of December 31, 2010 divided by the total gross book value of the Company's fixed assets at such facility as of December 31, 2010.

|

*

|

The definitions we use for resources and reserves are based on those provided by the “

Instituto de Ingenieros de Minas de Chile

” (Chilean Institute of Mining Engineers).

|

|

**

|

The definition of a Controller Group that has been provided is the one that applies to the Company. Chilean law provides for a broader definition of a Controller Group.

|

SQM will provide a copy of any or all of the documents incorporated herein by reference (other than exhibits, unless such exhibits are specifically incorporated by reference in such documents), upon written or oral request. Written requests for such copies should be directed to Sociedad Química y Minera de Chile S.A., El Trovador 4285, 6

th

Floor, Santiago, Chile, Attention: Investor Relations Department. Requests may also be made by telephone (562-425-2000), facsimile (562-425-2493) or e-mail (ir@sqm.com).

v

CAUTIONARY STATEMENT REGARDING FORWARD-LOOKING STATEMENTS

This Form 20-F contains statements that are or may constitute forward-looking statements within the meaning of the Private Securities Litigation Reform Act of 1995. These statements are not based on historical facts and reflect our expectations for future events and results. Words such as "believe," "expect," "predict," "anticipate," "intend," "estimate," "should," "may," "could" or similar expressions may identify forward-looking information. These statements appear throughout this Form 20-F and include statements regarding the intent, belief or current expectations of the Company and its management, including but not limited to any statements concerning:

|

|

·

|

the Company's capital investment program and development of new products;

|

|

|

·

|

trends affecting the Company's financial condition or results of operations;

|

|

|

·

|

level of production, quality of the ore and brines, and production levels and yields;

|

|

|

·

|

the future impact of competition; and

|

|

|

·

|

regulatory changes

|

Such forward-looking statements are not guarantees of future performance and involve risks and uncertainties. Actual results may differ materially from those described in such forward-looking statements included in this Form 20-F, including, without limitation, the information under Item 4. Information on the Company and Item 5. Operating and Financial Review and Prospects. Factors that could cause actual results to differ materially include, but are not limited to:

|

|

·

|

SQM's ability to implement its capital expenditures, including its ability to arrange financing when required;

|

|

|

·

|

the nature and extent of future competition in SQM's principal markets;

|

|

|

·

|

political, economic and demographic developments in the emerging market countries of Latin America and Asia where SQM conducts a large portion of its business;

|

|

|

·

|

volatility of global prices for SQM’s products;

|

|

|

·

|

changes in production capacities;

|

|

|

·

|

changes in raw material and energy prices;

|

|

|

·

|

currency and interest rate fluctuations; and

|

|

|

·

|

additional factors discussed below under Item 3. Key Information—Risk Factors.

|

vi

Not Applicable.

Not Applicable.

3.A.

Selected Financial Data

The following table presents selected financial data as of December 31, 2010 and the previous year. The selected financial data should be read in conjunction with the Audited Consolidated Financial Statements and notes thereto, “Item 5. Operating and Financial Review and Prospects” and other financial information included herein.

Since January 1, 2010, the Company’s consolidated financial statements are and will be prepared in accordance with the International Financial Reporting Standards as published by the International Accounting Standards Board (IASB).

The Company’s consolidated financial information as of and for the year ended December 31, 2009 included in the Company’s annual consolidated financial statements was restated in accordance with IFRS. See Note 2 to the Audited Consolidated Financial Statements of the Company.

|

Year ended December 31,

|

||||||||

|

2010

|

2009

|

|||||||

|

Income Statement Data

|

(in millions of US$)

(1)

|

|||||||

|

I.F.R.S

|

||||||||

|

Sales

|

1,830.4 | 1,438.7 | ||||||

|

Cost of sales

|

(1,204.4 | ) | (908.5 | ) | ||||

|

Gross profit

|

626.0 | 530.2 | ||||||

|

Administrative expenses

|

(78.8 | ) | (75.5 | ) | ||||

|

Operating Income

|

547.2 | 454.7 | ||||||

|

Net finance costs

|

(22.1 | ) | (17.5 | ) | ||||

|

Foreign currency transactions

|

(5.8 | ) | (7,6 | ) | ||||

|

Equity in gains (losses) of associates and joint ventures accounted for using the equity method

|

10.7 | 4.5 | ||||||

|

Other gains(losses), net

|

(36.7 | ) | (18.5 | ) | ||||

|

Profit before income tax expense

|

493.3 | 415.6 | ||||||

|

Income Tax expense

|

(106.0 | ) | (75.8 | ) | ||||

|

Profit (loss)

|

387.3 | 339.8 | ||||||

|

Equity holders of the parent

|

382.1 | 338.3 | ||||||

|

Non-controlling interest

|

5.2 | 1.5 | ||||||

|

Basic earnings per share (2)

|

1.45 | 1.29 | ||||||

|

Basic earnings per ADR (2) (3)

|

1.45 | 1.29 | ||||||

|

Dividend per share (4) (5)

|

0.73 | 0.66 | ||||||

|

Weighted average shares outstanding (000s) (2)

|

263,197 | 263,197 | ||||||

2

|

Year ended December 31,

|

As of

January 1,

|

|||||||||||

|

2010

|

2009

|

2009

|

||||||||||

|

Balance Sheet Data

|

(in millions of US$)

|

|||||||||||

|

I.F.R.S

|

||||||||||||

|

Total assets

|

3,372.8 | 3,141.8 | 2,484.0 | |||||||||

|

Total Liabilities

|

1,702.0 | 1,677.4 | 1,083.8 | |||||||||

|

Total Equity

|

1,670.8 | 1,464.5 | 1,400.2 | |||||||||

|

Equity attributable to the owners of the controlling entity

|

1,622.8 | 1,418.8 | 1,353.7 | |||||||||

|

Equity attributable to non-controlling interest

|

48.0 | 45.7 | 46.5 | |||||||||

|

Capital stock

|

477.4 | 477.4 | 477.4 | |||||||||

(1) Except shares outstanding, dividend and net earnings per share and net earnings per ADR.

(2) There are no authoritative pronouncements related to the calculation of earnings per share in accordance with IFRS.

(3) The Series A ADRs were delisted from the New York Stock Exchange on March 27, 2008. The ratio of ordinary shares to Series B ADRs changed from 10:1 to 1:1 on March 28, 2008. The calculation of earnings per ADR is based on the ratio of 1:1.

(4) Dividends per share are calculated based on 263,196,524 shares for the periods ended December 31, 2009 and 2010.

(5) Dividends may only be paid from net income as determined in accordance with IFRS; see Item 8.A.8. Dividend Policy. For dividends in Ch$ see Item 8.A.8.Dividend Policy — Dividends.

EXCHANGE RATES

Chile has two currency markets, the

Mercado Cambiario Formal

, or the "Formal Exchange Market," and the

Mercado Cambiario Informal

, or the "Informal Exchange Market." The Formal Exchange Market comprises banks and other entities authorized by the Banco Central de Chile (the "Chilean Central Bank"). The Informal Exchange Market comprises entities that are not expressly authorized to operate in the Formal Exchange Market, such as certain foreign exchange houses and travel agencies, among others. The Chilean Central Bank is empowered to determine that certain purchases and sales of foreign currencies be carried out on the Formal Exchange Market.

Both the Formal Exchange Market and the Informal Exchange Market are driven by free market forces. Current regulations require that the Chilean Central Bank be informed of certain transactions and that these transactions be effected through the Formal Exchange Market.

The

dólar observado

, or "Observed Exchange Rate," which is reported by the Chilean Central Bank and published daily in the Chilean newspapers, is computed by taking the weighted average of the previous business day's transactions on the Formal Exchange Market. Nevertheless, the Chilean Central Bank has the power to intervene by buying or selling foreign currency on the Formal Exchange Market to attempt to maintain the Observed Exchange Rate within a desired range.

On January 3, 2011, the Chilean Central Bank decided to intervene in the Formal Exchange Market by increasing the level of international reserves by US$12 billion, the biggest-ever exchange rate intervention aimed at suppressing the rising peso. This plan was implemented in January 2011 and is scheduled to end in December 2011.

3

The Informal Exchange Market reflects transactions carried out at an informal exchange rate, or the "Informal Exchange Rate." There are no limits imposed on the extent to which the rate of exchange in the Informal Exchange Market can fluctuate above or below the Observed Exchange Rate.

The Federal Reserve Bank of New York does not report a noon buying rate for Chilean pesos.

| Ch$ per US$ | ||||||||||||||||

|

Year/Month

|

Low (1)

|

High (1)

|

Average (1)(2)

|

Year/Month

End(3) |

||||||||||||

|

2005

|

509.70 | 592.75 | 559.86 | 512.50 | ||||||||||||

|

2006

|

511.44 | 549.63 | 530.26 | 532.39 | ||||||||||||

|

2007

|

493.14 | 548.67 | 522.69 | 496.89 | ||||||||||||

|

2008

|

431.22 | 676.75 | 521.79 | 636.45 | ||||||||||||

|

2009

|

491.09 | 643.87 | 559.15 | 507.10 | ||||||||||||

|

2010

|

468.01 | 549.17 | 510.22 | 468.01 | ||||||||||||

|

Dec.

|

468.01 | 485.34 | 473.83 | 468.01 | ||||||||||||

|

2011

|

||||||||||||||||

|

Jan.

|

466.05 | 499.03 | 490.21 | 484.14 | ||||||||||||

|

Feb.

|

468.94 | 481.56 | 475.24 | 475.21 | ||||||||||||

|

Mar.

|

472.74 | 485.37 | 479.84 | 479.46 | ||||||||||||

|

Apr.

|

460.04 | 479.90 | 470.35 | 460.09 | ||||||||||||

|

May

|

461.65 | 474.19 | 467.96 | 465.13 | ||||||||||||

Source: Central Bank of Chile

|

|

(1)

|

Observed exchange rates are the actual high and low on a day-to-day basis, for each period.

|

|

|

(2)

|

The monthly average rate is calculated on a day-to-day basis for each month.

|

|

|

(3)

|

The Year/Month End exchange rate is based on transactions observed during the last day of the month/year.

|

Not applicable.

3.C.

Reasons for the Offer and Use of Proceeds

Not applicable.

3.D.

Risk Factors

Our operations are subject to certain risk factors that may affect SQM's financial condition or results of operations. In addition to other information contained in this Annual Report on Form 20-F, you should consider carefully the risks described below. These risks are not the only ones we face. Additional risks not currently known to us or that are known but we currently believe are not significant may also affect our business operations. Our business, financial condition or results of operations could be materially affected by any of these risks.

4

Risks Relating to our Business

Our sales to emerging markets expose us to risks related to economic conditions and trends in those countries

We sell our products in more than 100 countries around the world. In 2010, 48% of our sales were made in emerging market countries: 12% in Central and South America (excluding Chile); 9% to Africa and the Middle East; 13% in Chile; and 13% in Asia (excluding Japan). We expect to expand our sales in these and other emerging markets in the future. The results of and prospects of our operations in these regions and in other countries in which we establish operations will depend, in part, on the general level of political stability and economic activity and policies in those countries. Future developments in the political systems or economies of these countries or the implementation of future governmental policies in those countries, including the imposition of withholding and other taxes, restrictions on the payment of dividends or repatriation of capital, the imposition of import duties or other restrictions, the imposition of new environmental regulations or price controls or changes in relevant laws or regulations could have a material adverse effect on our sales or operations in those countries.

Volatility of world fertilizer and chemical prices and changes in production capacities could affect our business, financial condition and results of operations

The prices of our products are determined principally by world prices, which, in some cases, have been subject to substantial volatility in recent years. World fertilizer and chemical prices vary depending upon the relationship between supply and demand at any given time. Supply and demand dynamics for our products are tied to a certain extent to global economic cycles, and have been impacted by current global economic conditions. Furthermore, the supply of certain fertilizers or chemical products, including certain products that we provide, varies principally depending on the production of the major producers, including SQM, and their respective business strategies.

During 2008, world prices of potassium-based fertilizers (including some of our specialty plant nutrients and potassium chloride) increased significantly during the first nine months of the year. Towards the end of 2008, fertilizer prices generally fell as a result of the global economic and financial slowdown. During 2009, volatility in prices continued to affect commodity markets around the world. During 2010, prices of potassium-based fertilizers stabilized after the conclusion of important contract negotiations between major producers and buyers at the end of 2009. During the first few months of 2011, we have observed consolidation in the industry on the part of producers and the settlement of important supply contracts between China and major potash producers at higher prices, which we expect will support positive price momentum. We have also observed positive price trends in the Brazilian market in the first months of 2011. However, we cannot assure you that prices will not decline in the future.

Iodine prices have followed an upward trend since late 2003, reaching an average price of approximately US$28 per kilogram in 2010. In October 2008, we announced an increase of iodine prices by 25%, and as a result prices increased during 2009. Sales volumes of iodine and its derivatives may be affected by general decreases in the use of applications that are sensitive to economic growth. We cannot assure that prices and sales volumes will not decline in the future.

We started production of lithium carbonate from the brines extracted from Salar de Atacama in October 1996 and started selling lithium carbonate commercially in January 1997. Our entry into the market created an oversupply of lithium carbonate, resulting in a drop in prices from over US$3,000 per ton before our entry to less than US$2,000 per ton. At the end of 2008, prices were approximately US$6,000 per ton and remained at this level until the fourth quarter of 2009 when prices declined to approximately US$5,000 per ton. Before the global economic slowdown, the increase in prices was the result of market dynamics reflecting sustained growth in demand in the past few years and supply that grew only enough to match demand, and we believed this price increase was due mainly to high growth in demand, which had not been fully balanced by the supply of lithium carbonate. As a result of events in global markets during 2009, demand for lithium carbonate declined and, as expected, lithium prices and sales volumes for 2009 were lower compared to the previous year. In September 2009, we announced a 20% price cut for lithium carbonate and lithium hydroxide as a measure to stimulate demand. In 2010, we observed demand recovery in the lithium market. We cannot assure you that this upward trend will continue in the future. Potential decreases in sales volumes of lithium carbonate could have a material adverse effect on our business, financial condition and results of operations.

5

We expect that prices for the products we manufacture will continue to be influenced, among other things, by worldwide supply and demand and the business strategies of major producers. Some of the major producers (including SQM) have increased or have the ability to increase production. As a result, the prices of our products may be subject to substantial volatility. High volatility or a substantial decline in the prices, or in volume demand, of one or more of our products could have a material adverse effect on our business, financial condition and results of operations.

Our inventory levels may increase because of the global economic situation

In general, the global economic slowdown experienced during 2008 and 2009 had an impact on our inventories. Demand decreased during 2009 and, as a result, inventories increased significantly. Higher inventories carry a financial risk due to increased need for cash to fund working capital. Higher inventory levels could also imply increased risk of loss of product. We cannot assure you that these changes in inventory levels will not occur in the future. These factors could have a material adverse effect on our business, financial condition and results of operations.

Our level of and exposure to unrecoverable accounts receivable may significantly increase

The potentially negative effects of the global economic crisis of 2008 and 2009 on the financial condition of our customers may include the extension of the payment terms of our accounts receivable and may increase our exposure to bad debt. While we are taking measures, such as using credit insurance, letters of credits and prepayment for a portion of sales, to minimize this risk, the increase in our accounts receivable coupled with the financial condition of customers may result in losses that could have a material adverse effect on our business, financial condition and results of operations.

New production of lithium carbonate from new competitors

Potential new production of lithium carbonate from new competitors in the markets in which we operate could adversely affect prices. There is limited information on the status of new lithium carbonate production capacity expansion projects being developed by current and potential competitors and, as such, we cannot make accurate projections regarding the capacities of possible new entrants into the market and the dates on which they could become operational. If these potential projects are completed in the short term, they could adversely affect market prices and our market share, which in turn could adversely affect our business, financial position and results of operations.

We have an ambitious capital expenditure program that is subject to significant risks and uncertainties

Our business is capital intensive. Specifically, the exploration and exploitation of reserves, mining and processing costs, the maintenance of machinery and equipment and compliance with applicable laws and regulations require substantial capital expenditures. We must continue to invest capital to maintain or to increase our exploitation levels and the amount of finished products we produce. We require environmental permits for our new projects. Obtaining permits in certain cases may cause significant delays in the execution and implementation of new projects and, consequently, may require us to reassess the related risks and economic incentives. We cannot assure you that we will be able to maintain our production levels or generate sufficient cash flow, or that we will have access to sufficient investments, loans or other financing alternatives, to continue our exploration, exploitation and refining activities at or above present levels, or that we will be able to implement our projects or receive the necessary permits required for them in time. Any or all of these factors may have a material adverse impact on our business, financial condition and results of operations.

6

We transact a significant portion of our business in U.S. dollars, and the U.S. dollar is the currency of the primary economic environment in which we operate. In addition, the U.S. dollar is our functional currency for financial statement reporting purposes. A significant portion of our costs, however, is related to the Chilean peso. Therefore, an increase or decrease in the exchange rate between the Chilean peso and the U.S. dollar would affect our costs of production. The Chilean peso has been subject to large devaluations and revaluations in the past and may be subject to significant fluctuations in the future. As of December 31, 2010, the Chilean peso to U.S. dollar exchange rate was Ch$468.01 per U.S. dollar, while as of December 31, 2009, the Chilean peso to U.S. dollar exchange rate was Ch$507.01 per U.S. dollar. As a result, the U.S. dollar depreciated approximately 8% compared to the peso during 2010.

As an international company operating in several other countries, we also transact business and have assets and liabilities in other non-U.S. dollar currencies, such as, among others, the euro, the South African rand and the Mexican peso. As a result, fluctuations in the exchange rates of such foreign currencies to the U.S. dollar may affect our business, financial condition and results of operations.

Interest rate fluctuations may have a material impact on our financial performance

We have outstanding short- and long-term debt that bears interest based on the London Interbank Offered Rate, or "LIBOR," plus a spread. As we do not have derivative instruments to hedge LIBOR, we are subject to fluctuations in this rate. As of December 31, 2010, approximately 20% of our financial debt had LIBOR-based pricing. Thus, significant increases in the rate could impact our financial condition and results of operations.

High raw materials and energy prices could increase our production costs and cost of goods sold

We rely on certain raw materials and various sources of energy (diesel, electricity, natural gas, fuel oil and others) to manufacture our products. Purchases of raw materials that we do not produce and energy constitute an important part of our cost of sales (17.6% in 2010). To the extent we are unable to pass on increases in raw materials and energy prices to our customers, our business, financial condition and results of operations could be materially adversely affected.

Our reserves estimates could be subject to significant changes

Our mining reserves estimates are prepared by our own geologists. Estimation methods involve numerous uncertainties as to the quantity and quality of the reserves, and reserve estimates could change upwards or downwards. In addition, our reserve estimates are not subject to review by external geologists or an external auditing firm. A downward change in the quantity and/or quality of our reserves could affect future volumes and costs of production and therefore have a material adverse effect on our business, financial condition and results of operations.

Quality standards in markets in which we sell our products could become stricter over time

In the markets in which we do business, customers may impose quality standards on our products and/or governments may enact or are enacting stricter regulations for the distribution and/or use of our products. As a result, we may not be able to sell our products if we cannot meet such new standards. In addition, our cost of production may increase in order to meet any such newly promulgated standards. Failure to sell our products in one or more markets or to important customers could materially adversely affect our business, financial condition and results of operations.

7

Chemical and physical properties of our products could adversely affect its commercialization

Since our products are derived from natural resources, they contain inorganic impurities that may not meet certain client and government standards. As a result, we may not be able to sell our products if we cannot meet such requirements. In addition, our cost of production may increase in order to meet such standards. Failure to meet such standards could materially adversely affect our business, financial condition and results of operations.

Our business is subject to many operating and other risks for which we may not be fully covered under our insurance policies

Our facilities and business operations in Chile and abroad are insured against losses, damages or other risks by insurance policies that are standard for the industry and that would reasonably be expected to be sufficient by prudent and experienced persons engaged in businesses similar to ours.

We may be subject to certain events that may not be covered under our insurance policies, and that could have a material adverse effect on our business, financial condition and results of operations. Additionally, as a result of the major earthquake in Chile in February 2010 and other natural disasters worldwide, conditions in the insurance market may change, and as a result we may face higher premiums and reduced coverage.

We face significantly higher energy costs as a result of a natural gas shortage in Chile

As part of a cost reduction effort, in 2001 we connected our facilities to a natural gas network. This natural gas, which originates in Argentina and is subject to a 10-year agreement terminating in 2011, is used mainly for heat generation at our industrial facilities. Due to energy shortages in Argentina, in 2004 local authorities began to restrict exports of natural gas to Chile in order to increase the supply to their domestic markets. Additionally, even though we have long-term price agreements related to natural gas, the Argentinean government has increased taxes on gas exports, which could lead our suppliers to demand pricing changes, and we cannot assure you that they will not do so again in the future.

We suffered partial shortages of natural gas during 2004, 2005 and 2006, and from 2007 through 2010 we received practically no natural gas. We believe this situation will continue and that during 2011 we will likely receive little to no natural gas from Argentina. Most of our industrial equipment that uses natural gas can also operate on fuel oil, and the remaining equipment can operate on diesel. However, the cost of fuel oil and diesel is significantly higher than the cost of natural gas, and therefore we have recently faced significantly higher energy costs. We expect this situation to continue, and, as such, we expect the reduction in our natural gas supply to continue to have a material adverse effect on our business, financial condition and results of operations.

Decline in the supply of natural gas could negatively affect the supply of electricity and our electricity contracts

The natural gas supply crisis discussed above has placed Chile's northern power grid (Sistema Interconectado del Norte Grande) under significant stress. Continued stress on the northern power grid could lead to a system failure that would then affect the supply of electricity. Restrictions on our electricity consumption could materially adversely affect our operations, potentially decreasing our production volumes and increasing our production costs. During 2010, purchases of electricity represented approximately 4% of our cost of sales.

As the supply of natural gas continues to be uncertain, we are faced with the potential early termination, partial amendment or temporary suspension of our long-term electricity supply contracts. We maintain contracts with two main utilities in Chile, Electroandina S.A. and Norgener S.A., and in the past both have sought relief from the terms of their electricity supply agreements, asserting that unforeseen events have restricted the supply and increased the price of gas from Argentina. As a result of these requests, we entered into negotiations resulting in new tariffs that have had a negative effect on our results of operations. Further increases in the cost of energy could prompt these companies to once again seek to modify, terminate or suspend these contracts. If that were to happen, and these companies were to prevail in any resulting judicial proceedings, our business, financial condition and results of operations could be materially adversely affected.

8

Changes in technology or other developments could result in preferences for substitute products

Our products, particularly iodine, lithium and their derivatives, are preferred raw materials for certain industrial applications, such as rechargeable batteries and LCD screens. Changes in technology, the development of substitute raw materials or other developments could adversely affect demand for these and other products which we produce.

We are exposed to labor strikes and liabilities that could impact our production levels and costs

Approximately 69% of our permanent employees in Chile is represented by 27 labor unions. As a result, we are exposed to labor strikes that could impact our production levels. If a strike occurs and continues for a sustained period of time, we could be faced with increased costs and even disruption in our product flow that could have a material adverse effect on our business, financial condition and results of operations.

Chilean Law No. 20,123, known as the Ley de Subcontratación ("Law on Subcontracting"), provides that when a serious accident in the workplace occurs, a company must halt work at the site where the accident took place until authorities from the National Geology and Mining Service inspect the site and prescribe the measures such company must take to prevent future risks. Work may not be resumed until such company has taken the prescribed measures, and the period of time before work may be resumed may last for a number of hours, days, or longer. The effects of this law could have a material adverse effect on our business, financial condition and results of operations.

Lawsuits and arbitrations could adversely impact us

We are party to a range of lawsuits and arbitrations involving different matters as described in Note 20 to our consolidated financial statements. Although we intend to defend our positions vigorously, our defense of these actions may not be successful. Judgments or settlements in these lawsuits may have a material adverse effect on our business, financial condition and results of operations. In addition, our strategy of being a world leader includes entering into commercial and production alliances, joint ventures and acquisitions to improve our global competitive position. As these operations increase in complexity and are carried out in different jurisdictions, we might be subject to legal proceedings that, if settled against us, could have a material adverse effect on our business, financial condition and results of operations.

The Chilean labor code has recently established new procedures for labor matters which include oral trials conducted by specialized judges. The majority of these oral trials have found in favor of the employee. These new procedures could increase the probability of adverse judgments which could have a material adverse effect on our business, financial condition and results of operations.

We have operations in multiple jurisdictions with differing regulatory, tax and other regimes

We operate in multiple jurisdictions with complex regulatory environments subject to different interpretations by companies and respective governmental authorities. These jurisdictions may each have their own tax codes, environmental regulations, labor codes and legal framework, which could complicate efforts to comply with these regulations which could have a material adverse effect on our business, financial condition and results of operations.

9

Risks Relating to Chile

As we are a company based in Chile, we are exposed to Chilean political risks

Our business, results of operations, financial condition and prospects could be affected by changes in policies of the Chilean government, other political developments in or affecting Chile, and regulatory and legal changes or administrative practices of Chilean authorities, over which we have no control.

Changes in regulations regarding, or any revocation or suspension of, our concessions could negatively affect our business

Any adverse changes to our concession rights, or a revocation or suspension of our concessions, could have a material adverse effect on our business, financial condition and results of operations.

Changes in mining or port concessions could affect our operating costs

We conduct our mining (including brine extraction) operations under exploitation and exploration concessions granted in accordance with provisions of the Chilean constitution and related laws and statutes. Our exploitation concessions essentially grant a perpetual right to conduct mining operations in the areas covered by the concessions, provided that we pay annual concession fees (with the exception of the Salar de Atacama rights, for which we have a lease until 2030). Our exploration concessions permit us to explore for mineral resources on the land covered thereby for a specified period of time and to subsequently request a corresponding exploitation concession.

We also operate port facilities at Tocopilla, Chile for the shipment of our products and the delivery of certain raw materials, pursuant to concessions granted by Chilean regulatory authorities. These concessions are renewable provided that we use such facilities as authorized and pay annual concession fees.

Any significant changes to any of these concessions could have a material adverse effect on our business, financial condition and results of operations.

Changes in water rights laws could affect our operating costs

We hold water rights that are key to our operations. These rights were obtained from the Chilean water authority for supply of water from rivers and wells near our production facilities, which we believe are sufficient to meet current operating requirements. However, the Chilean water rights code (the "Water Code") is subject to changes, which could have a material adverse impact on our business, financial condition and results of operations. For example, an amendment published on June 16, 2005 modified the Water Code, allowing under certain conditions, the granting of permanent water rights of up to two liters per second for each well built prior to June 30, 2004, in the locations where we conduct our mining operations, without considering the availability of water, or how the new rights may affect holders of existing rights. Therefore, the amount of water we can effectively extract based on our existing rights could be reduced if these additional rights are exercised. In addition, we must pay annual concession fees to maintain water rights we are not exercising. These and potential future changes to the Water Code could have a material adverse effect on our business, financial condition and results of operations.

Our water supply could be affected by geological changes

Our access to water may be impacted by changes in geology or other natural factors, such as wells drying up, that we cannot control, and which may have a material adverse effect on our business, financial condition and results of operations.

The Chilean government could levy additional taxes on corporations operating in Chile

In 2005, the Chilean Congress approved Law No. 20,026 (also known as the "Royalty Law"), establishing a royalty tax to be applied to mining activities developed in Chile.

10

After the earthquake in February 2010 in the south of Chile, the government approved changes to both the Royalty Law and the corporate tax rate that raised tax rates in order to partially fund the recovery effort.

We cannot assure you that the manner in which the Royalty Law is interpreted and applied will not change in the future. In addition, the Chilean government may decide to levy additional taxes on mining companies or other corporations in Chile. Such changes could have a material adverse effect on our business, financial condition and results of operations.

Environmental laws and regulations could expose us to higher costs, liabilities, claims and failure to meet current and future production targets

Our operations in Chile are subject to national and local regulations relating to environmental protection. We are required to conduct environmental impact studies of any future projects or activities (or significant modifications thereto) that may affect the environment. The National Environmental Commission (the Comisión Nacional del Medio Ambiente, or "CONAMA") currently evaluates environmental impact studies submitted for its approval and oversees the implementation of projects, and private citizens, public agencies or local authorities may challenge projects that may adversely affect the environment, either before these projects are executed or once they are already operating. Enforcement remedies available include fines and temporary or permanent closure of facilities.

Chilean environmental regulations have become increasingly stringent in recent years, both with respect to the approval of new projects and in connection with the implementation and development of projects already approved. This trend is likely to continue. Furthermore, recently implemented environmental regulations have created uncertainty because rules and enforcement procedures for these regulations have not been fully developed. Given public interest in environmental enforcement matters, these regulations or their application may also be subject to political considerations that are beyond our control.

We continuously monitor the impact of our operations on the environment and have, from time to time, made modifications to our facilities to minimize any adverse impacts. We believe we are currently in compliance in all material respects with applicable environmental regulations in Chile. The only exception is for particulate matter levels that have exceeded permissible levels at the María Elena facilities. We believe that we are complying with current regulations at these facilities; however, we must complete a three-year monitoring period which ends in 2011. Future developments in the creation or implementation of environmental requirements, or in their interpretation, could result in substantially increased capital, operation or compliance costs or otherwise adversely affect our business, financial condition and results of operations.

In connection with our current investments at the Salar de Atacama, we have obtained approval for an environmental impact assessment study that allows us to increase brine and water extraction, subject to a rigorous environmental monitoring system. The success of these investments is dependent on the behavior of the ecosystem variables being monitored over time. If the behavior of these variables in future years does not meet environmental requirements, our operation may be subject to important restrictions by the authorities on the maximum allowable amounts of brine and water extraction.

In connection with our future investments in nitrate and iodine operations, we have submitted and expect to submit several environmental impact assessment studies. The success of these investments is dependent on the approval of such submissions by the pertinent governmental authorities.

Our future development also depends on our ability to sustain future production levels, which requires additional investments and the submission of the corresponding environmental impact assessment studies. If we fail to obtain approval, our ability to maintain production at specified levels will be seriously impaired, thus having a material adverse effect on our business, financial condition and results of operations.

11

In addition, our worldwide operations are subject to international environmental regulations. Since laws and regulations in the different jurisdictions in which we operate may change, we cannot guarantee that future laws, or changes to existing laws, will not materially adversely impact our business, financial condition and results of operations.

Ratification of the International Labor Organization's Convention 169 concerning indigenous and tribal peoples might affect our development plans

In 2008, Chile, a member of the International Labor Organization ("ILO"), ratified the ILO's Convention 169 (the "Indigenous Rights Convention") concerning indigenous and tribal peoples. The Indigenous Rights Convention established several rights for indigenous individuals and communities. Among other rights, the Indigenous Rights Convention outlines that (i) indigenous groups be notified of and consulted prior to the development of any project on land deemed indigenous (right to veto was not included); and (ii) indigenous groups have, to the extent possible, a stake in benefits resulting from the exploitation of natural resources in alleged indigenous land. The extent of these benefits has not been defined by the government. The new rights outlined in the Indigenous Rights Convention could affect the development of our investment projects in alleged indigenous lands which could have a material adverse effect on our business, financial condition and results of operations.

Chile is located in a seismically active region

Although a major earthquake affected parts of southern Chile in February 2010, SQM operations were not impacted. Chile is prone to earthquakes because it is located along major fault lines. A major earthquake could have significant negative consequences for our operations and for the general infrastructure, such as roads, rail, and access to goods, in Chile. Even though we maintain insurance policies standard for this industry with earthquake coverage we cannot assure you that a future seismic event will not have a material adverse effect on our business, financial condition and results of operations.

Risks related to our shares and to our ADRs

The price of our ADRs and the U.S. dollar value of any dividends will be affected by fluctuations in the U.S. dollar/Chilean peso exchange rate

Chilean trading in the shares underlying our ADRs is conducted in Chilean pesos. The depositary will receive cash distributions that we make with respect to the shares in pesos. The depositary will convert such pesos to U.S. dollars at the then prevailing exchange rate to make dividend and other distribution payments in respect of ADRs. If the value of the peso falls relative to the U.S. dollar, the value of the ADRs and any distributions to be received from the depositary will decrease.

Developments in other emerging markets could materially affect the value of our ADRs

The Chilean financial and securities markets are, to varying degrees, influenced by economic and market conditions in other emerging market countries or regions of the world. Although economic conditions are different in each country or region, investor reaction to developments in one country or region can have significant effects on the securities of issuers in other countries and regions, including Chile and Latin America. Events in other parts of the world may have an adverse effect on Chilean financial and securities markets and on the value of our ADRs.

The volatility and low liquidity of the Chilean securities markets could affect the ability of our shareholders to sell our ADRs

The Chilean securities markets are substantially smaller, less liquid and more volatile than the major securities markets in the United States. The volatility and low liquidity of the Chilean markets could increase the price volatility of our ADRs and may impair the ability of a holder to sell our ADRs into the Chilean market in the amount and at the price and time he wishes to do so.

12

Our share price may react negatively to future acquisitions and investments

As world leaders in our core businesses, part of our strategy is to constantly look for opportunities that will allow us to consolidate and strengthen our competitive position. Pursuant to this strategy, we may from time to time, evaluate and eventually carry out acquisitions relating to any of our businesses or to new businesses in which we believe we may have sustainable competitive advantages. Depending on our capital structure at the time of such acquisitions, we may need to raise significant debt and/or equity which will affect our financial condition and future cash flows. Any change in our financial condition could affect our results of operations, negatively impacting our share price.

You may be unable to enforce rights under U.S. Securities Laws

Because we are a Chilean company subject to Chilean law, the rights of our shareholders may differ from the rights of shareholders in companies incorporated in the United States, and you may not be able to enforce or may have difficulty enforcing rights currently in effect under U.S. Federal or State securities laws.

Our Company is a "

sociedad anónima abierta

" (open stock corporation) incorporated under the laws of the Republic of Chile. Most of SQM's directors and officers reside outside the United States, principally in Chile. All or a substantial portion of the assets of these persons are located outside the United States. As a result, if any of our shareholders, including holders of our ADRs, were to bring a lawsuit against our officers or directors in the United States, it may be difficult for them to effect service of legal process within the United States upon these persons. Likewise, it may be difficult for them to enforce judgments obtained in United States courts based upon the civil liability provisions of the federal securities laws of the United States against them in United States courts.

In addition, there is no treaty between the United States and Chile providing for the reciprocal enforcement of foreign judgments. However, Chilean courts have enforced judgments rendered in the United States, provided that the Chilean court finds that the United States court respected basic principles of due process and public policy. Nevertheless, there is doubt as to whether an action could be brought successfully in Chile in the first instance on the basis of liability based solely upon the civil liability provisions of the United States federal securities laws.

As preemptive rights may be unavailable for our ADR holders, they have the risk of their holdings being diluted if we issue new stock

Chilean laws require companies to offer their shareholders preemptive rights whenever selling new shares of capital stock. Preemptive rights permit holders to maintain their existing ownership percentage in a company by subscribing for additional shares. If we increase our capital by issuing new shares, a holder may subscribe for up to the number of shares that would prevent dilution of the holder's ownership interest.

If we issue preemptive rights, United States holders of ADRs would not be able to exercise their rights unless a registration statement under the Securities Act were effective with respect to such rights and the shares issuable upon exercise of such rights or an exemption from registration were available. We cannot assure holders of ADRs that we will file a registration statement or that an exemption from registration will be available. We may, in our absolute discretion, decide not to prepare and file such a registration statement. If our holders were unable to exercise their preemptive rights because SQM did not file a registration statement, the depositary bank would attempt to sell their rights and distribute the net proceeds from the sale to them, after deducting the depositary's fees and expenses. If the depositary could not sell the rights, they would expire and holders of ADRs would not realize any value from them. In either case, ADR holders' equity interest in SQM would be diluted in proportion to the increase in SQM's capital stock.

If the Company were classified as a Passive Foreign Investment Company there could be adverse consequences for U.S. investors

We believe that we were not classified as a passive foreign investment company, or PFIC, for 2010. Characterization as a PFIC could result in adverse U.S. tax consequences to you if you are a U.S. investor in our shares or ADRs. For example, if we (or any of our subsidiaries) are a PFIC, our U.S. investors may become subject to increased tax liabilities under U.S. tax laws and regulations and will become subject to burdensome reporting requirements. The determination of whether or not we (or any of our subsidiaries or portfolio companies) are a PFIC is made on an annual basis and will depend on the composition of our (or their) income and assets from time to time. See Item 10.E Taxation – United States Tax Considerations.

13

Changes in Chilean tax regulations could have adverse consequences for U.S. investors

Currently cash dividends paid by the Company to foreign shareholders are subject to a 35% Chilean withholding tax. If the Company has paid corporate income tax (the "First Category Tax") on the income from which the dividend is paid, a credit for the First Category Tax effectively reduces the rate of Withholding Tax. Changes in current Chilean tax regulations could have adverse consequences for U.S. investors.

14

4.A.

History and Development of the Company

Historical Background

Sociedad Química y Minera de Chile S.A. "SQM" is an open stock corporation (

sociedad anónima abierta

) organized under the laws of the Republic of Chile. The Company was constituted by public deed issued on June 17, 1968 by the Notary Public of Santiago, Mr. Sergio Rodríguez Garcés. Its existence was approved by Decree No. 1.164 of June 22, 1968 of the Ministry of Finance, and it was registered on June 29, 1968 in the Registry of Commerce of Santiago, on page 4.537 No. 1.992. SQM's headquarters are located at El Trovador 4285, Fl. 6, Las Condes, Santiago, Chile. The Company's telephone number is +56 2 425-2000.

Commercial exploitation of the caliche ore deposits in northern Chile began in the 1830s, when sodium nitrate was extracted from the ore for use in the manufacturing of explosives and fertilizers. By the end of the nineteenth century, nitrate production had become the leading industry in Chile and the country was the world's leading supplier of nitrates. The accelerated commercial development of synthetic nitrates in the 1920s and the global economic depression in the 1930s caused a serious contraction of the Chilean nitrate business, which did not recover significantly until shortly before the Second World War. After the war, the widespread commercial production of synthetic nitrates resulted in a further contraction of the natural nitrate industry in Chile, which continued to operate at depressed levels into the 1960s.

SQM was formed in 1968 through a joint venture between Compañía Salitrera Anglo Lautaro S.A. (“Anglo Lautaro”) and

Corporación de Fomento de la Producción

(“Production Development Corporation” or “Corfo”), a Chilean government entity. Three years after our formation, in 1971, Anglo Lautaro sold all of its shares to Corfo, and we were wholly owned by the Chilean Government until 1983. In 1983, Corfo began a process of privatization by selling our shares to the public and subsequently listing such shares on the Santiago Stock Exchange. By 1988, all of our shares were publicly owned. Our Series B ADRs have traded on the NYSE under the ticker symbol “SQM” since 1993.

Since its inception, in addition to producing nitrates, the Company has produced iodine, which is also found in the caliche ore deposits in northern Chile.

Between the years 1994 and 1999, we invested approximately US$300 million in the development of the Salar de Atacama project in northern Chile. The project involved the construction of a potassium chloride plant, a lithium carbonate plant, a potassium sulfate plant, and a boric acid plant.

To help finance the above projects, we accessed the international capital markets by issuing additional Series B ADRs on the New York Stock Exchange in 1995. In 1999 we issued additional Series A shares, which were also listed on the New York Stock Exchange as ADRs. Effective March 27, 2008, the Company voluntarily delisted its Series A ADR (“SQM-A”) from the New York Stock Exchange.

During the period from 2000 through 2004 we principally consolidated the investments carried out in the preceding five years. We focused on reducing costs and improving efficiencies throughout the organization.

Since 2005, we have strengthened our leadership in our main businesses by increasing our capital expenditure program and making appropriate acquisitions and divestitures. During this period we acquired Kefco in Dubai and the iodine business of DSM. We also sold (i) Fertilizantes Olmeca, our Mexican subsidiary, (ii) our butyllithium plant located in Houston, Texas and (iii) our stake in Impronta S.R.L., our Italian subsidiary. These sales allowed SQM to concentrate its efforts on its core products. In 2007, we completed the construction of a new prilling and granulating plant. In 2008, we completed our lithium carbonate capacity expansion and began work on the engineering stage of a new potassium nitrate plant. During 2009 and 2010, we continued expansion of potassium-based products in the Salar de Atacama. During the first quarter of 2011, we completed the construction of a new potassium nitrate facitly in Coya Sur.

15

Capital Expenditure Program

We are constantly reviewing different opportunities to improve our production methods, reduce costs, increase production capacity of existing products and develop new products and markets. Additionally, significant capital expenditures are required every year in order to sustain our production capacity. We are focused on developing new products in response to identified customer demand, as well as new products that can be derived as part of our existing production or other products that could fit our long-term development strategy. Our capital expenditures during the past five years were mainly related to the acquisition of new assets, construction of new facilities and renewal of plant and equipment.

SQM’s capital expenditures in the 2008-2010 period were the following:

|

(in millions of US$)

|

2010

|

2009

|

2008

|

|||||||||

|

Capital Expenditures (1)

|

336.0 | 376.2 | 286.6 | |||||||||

|

|

(1)

|

For purposes of this item, capital expenditures include investments aimed at sustaining, improving or increasing production levels, including acquisitions and investments in related companies.

|

We have developed a capital expenditure program calling for investments totalling approximately US$540 million for 2011. This amount may increase or decrease depending on market conditions. The main purpose of our capital expenditure program is to increase the production capacities of several of our products, including expansions in potassium-based products from the Salar de Atacama, iodine and natural nitrates. In addition, part of this investment plan is intended to modernize production processes in order to improve our operating efficiency.

During 2010, we had total capital expenditures of US$336.0 million, primarily due to:

|

|

·

|

continued construction of a new potassium nitrate production facility at Coya Sur;

|

|

|

·

|

investments related to increase production capacity of potassium-based products at the Salar de Atacama;

|

|

|

·

|

upgrade of our railroad system to handle expanded production capacity; and

|

|

|

·

|

various projects designed to maintain production capacity, increase yields and reduce costs.

|

We have budgeted for 2011 total capital expenditures of approximately US$540 million, primarily relating to:

|

|

·

|

investments related to increase production capacity of potassium-based products at the Salar de Atacama;

|

|

|

·

|

increase capacity and efficiencies at nitrate and iodine facilities;

|

|

|

·

|

optimization railroad system;

|

|

|

·

|

various projects designed to maintain production capacity, increase yields and reduce costs.

|

No external financing is needed to finance the capital expenditure program for the 2011 period. Investments made during this period will be concentrated in the Tarapacá and Antofagasta Regions of Chile.

16

4.B.

Business Overview

The Company

We believe that we are the world’s largest integrated producer of potassium nitrate, iodine and lithium carbonate. We also produce other specialty plant nutrients, iodine and lithium derivatives, potassium chloride and certain industrial chemicals (including industrial nitrates). Our products are sold in over 100 countries through our worldwide distribution network, with more than 85% of our sales derived from countries outside Chile in 2010.

Our products are mainly derived from mineral deposits found in northern Chile. We mine and process caliche ore and brine deposits. The caliche ore in northern Chile contains the only known nitrate and iodine deposits in the world and is the world’s largest commercially exploited source of natural nitrates. The brine deposits of the Salar de Atacama, a salt-encrusted depression within the Atacama desert in northern Chile, contain high concentrations of lithium and potassium as well as significant concentrations of sulfate and boron.