SYNCHRONY FINANCIAL

10-Ks and 10-Qs

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 10-K

(Mark One)

|

x

|

ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934

|

For the fiscal year ended

December 31, 2016

OR

|

o

|

TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934

|

For the transition period from to

001-36560

(Commission File Number)

SYNCHRONY FINANCIAL

(Exact name of registrant as specified in its charter)

|

Delaware

|

|

51-0483352

|

|

(State or Other Jurisdiction of

Incorporation or Organization)

|

|

(I.R.S. Employer

Identification No.)

|

|

777 Long Ridge Road

|

|

|

|

Stamford, Connecticut

|

06902

|

|

|

(Address of principal executive offices)

|

|

(Zip Code)

|

(Registrant’s telephone number, including area code) (203) 585-2400

Securities Registered Pursuant to Section 12(b) of the Act:

|

Title of each class

|

|

Name of each exchange on which registered

|

|

Common stock, par value $0.001 per share

|

|

New York Stock Exchange

|

Securities Registered Pursuant to Section 12(g) of the Act:

|

Title of class

|

||

|

None

|

||

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. Yes

ý

No

¨

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Act. Yes

¨

No

ý

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes

ý

No

¨

Indicate by check mark whether the registrant has submitted electronically and posted on its corporate Web site, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files). Yes

ý

No

¨

Indicate by check mark if disclosure of delinquent filers pursuant to Item 405 of Regulation S-K is not contained herein, and will not be contained, to the best of registrant’s knowledge, in definitive proxy or information statements incorporated by reference in Part III of this Form 10-K or any amendment to this Form 10-K.

ý

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, or a smaller reporting company. See the definitions of “large accelerated filer,” “accelerated filer” and “smaller reporting company” in Rule 12b-2 of the Exchange Act. (Check one):

|

Large accelerated filer

|

ý

|

Accelerated filer

|

o

|

|

Non-accelerated filer

|

o

(Do not check if a smaller reporting company)

|

Smaller reporting company

|

o

|

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Act). Yes

¨

No

ý

The aggregate market value of the outstanding common equity of the registrant held by non-affiliates as of the last business day of the registrant’s most recently completed second fiscal quarter was $21,081,515,270.

The number of shares of the registrant’s common stock, par value $0.001 per share, outstanding as of

February 16, 2017

was 810,786,641.

DOCUMENTS INCORPORATED BY REFERENCE

The definitive proxy statement relating to the registrant’s Annual Meeting of Stockholders, to be held May 18, 2017, is incorporated by reference into Part III to the extent described therein.

Synchrony Financial

Table of Contents

|

Page

|

||

3

Certain Defined Terms

Except as the context may otherwise require in this report, references to:

|

•

|

“we,” “us,” “our” and the “Company” are to SYNCHRONY FINANCIAL and its subsidiaries;

|

|

•

|

“Synchrony” are to SYNCHRONY FINANCIAL only;

|

|

•

|

“GE” are to General Electric Company and its subsidiaries;

|

|

•

|

“GECC” are to General Electric Capital Corporation (a subsidiary of GE) and its subsidiaries;

|

|

•

|

the “Bank” are to Synchrony Bank (a subsidiary of Synchrony);

|

|

•

|

the “Bank Term Loan” are to the term loan agreement, dated as of July 30, 2014, among Synchrony, as borrower, JPMorgan Chase Bank, N.A., as administrative agent, and the lenders from time to time party thereto, as amended;

|

|

•

|

the “Board of Directors” are to Synchrony’s board of directors;

|

|

•

|

the “GECC Term Loan” are to the term loan agreement, dated as of July 30, 2014, among Synchrony, as borrower, GECC, as administrative agent, and the other Lenders party thereto, as amended;

|

|

•

|

“FICO” score are to a credit score developed by Fair Isaac & Co., which is widely used as a means of evaluating the likelihood that credit users will pay their obligations; and

|

|

•

|

“EMV” are to new security technology that utilizes embedded security chips in our credit cards.

|

We provide a range of credit products through programs we have established with a diverse group of national and regional retailers, local merchants, manufacturers, buying groups, industry associations and healthcare service providers, which, in our business and in this report, we refer to as our “partners.” The terms of the programs all require cooperative efforts between us and our partners of varying natures and degrees to establish and operate the programs. Our use of the term “partners” to refer to these entities is not intended to, and does not, describe our legal relationship with them, imply that a legal partnership or other relationship exists between the parties or create any legal partnership or other relationship. The “average length of our relationship” with respect to a specified group of partners or programs is measured on a weighted average basis by interest and fees on loans for the year ended

December 31, 2016

for those partners or for all partners participating in a program, based on the date each partner relationship or program, as applicable, started. Information with respect to partner “locations” in this report is given at

December 31, 2016

. “Open accounts” represents credit card or installment loan accounts that are not closed, blocked or more than 60 days delinquent.

Unless otherwise indicated, references to “loan receivables” do not include loan receivables held for sale.

For a description of certain other terms we use, including “active account” and “purchase volume,” see the notes to “

Item 7. Management’s Discussion and Analysis

—

Other Financial and Statistical Data

.” There is no standard industry definition for many of these terms, and other companies may define them differently than we do.

“Synchrony” and its logos and other trademarks referred to in this report, including, CareCredit®, Quickscreen®, Dual Card™ and eQuickscreen™ belong to us. Solely for convenience, we refer to our trademarks in this report without the ™ and ® symbols, but such references are not intended to indicate that we will not assert, to the fullest extent under applicable law, our rights to our trademarks. Other service marks, trademarks and trade names referred to in this report are the property of their respective owners.

On our website at www.synchronyfinancial.com, we make available under the "Investors-SEC Filings" menu selection, free of charge, our Annual Reports on Form 10-K, Quarterly Reports on Form 10-Q, Current Reports on Form 8-K, and amendments to these reports filed or furnished pursuant to Section 13(a) or 15(d) of the Exchange Act as soon as reasonably practicable after such reports or amendments are electronically filed with, or furnished to, the SEC. Materials that we file or furnish to the SEC may also be read and copied at the SEC's Public Reference Room at 100 F Street, N.E., Washington, DC 20549. Information on the operation of the Public Reference Room may be obtained by calling the SEC at 1-800-SEC-0330. Also, the SEC maintains an Internet site at www.sec.gov that contains reports, proxy and information statements, and other information that we file electronically with the SEC.

Industry and Market Data

This report contains various historical and projected financial information concerning our industry and market. Some of this information is from industry publications and other third-party sources, and other information is from our own

4

data and market research that we commission. All of this information involves a variety of assumptions, limitations and methodologies and is inherently subject to uncertainties, and therefore you are cautioned not to give undue weight to it. Although we believe that those industry publications and other third-party sources are reliable, we have not independently verified the accuracy or completeness of any of the data from those publications or sources. Statements in this report that we are the largest provider of private label credit cards in the United States (based on purchase volume and receivables) are based on issue number 1,087 of “The Nilson Report,” a subscription-based industry newsletter, dated May 2016 (based on 2015 data).

Non-GAAP Measures

We present certain capital ratios for the Company at December 31, 2016 and 2015. These capital ratios include common equity Tier 1 capital ("CET1") as calculated under the U.S. Basel III capital rules on a fully phased-in basis, which is not currently required by our regulators to be disclosed and, as such, is considered to be a non-GAAP measure. We believe these capital ratios are useful measures to investors because they are widely used by analysts and regulators to assess the capital position of financial services companies, although these ratios may not be comparable to similarly titled measures reported by other companies. For a reconciliation of the components of these capital ratios to their nearest comparable GAAP component, see “

Item 7. —Management’s Discussion and Analysis of Financial Condition and Results of Operations—Capital

.”

Cautionary Note Regarding Forward-Looking Statements:

Various statements in this Annual Report on Form 10-K may contain “forward-looking statements” as defined in Section 27A of the Securities Act of 1933, as amended, and Section 21E of the Securities Exchange Act of 1934, as amended (the “Exchange Act”), which are subject to the “safe harbor” created by those sections. Forward-looking statements may be identified by words such as “expects,” “intends,” “anticipates,” “plans,” “believes,” “seeks,” “targets,” “outlook,” “estimates,” “will,” “should,” “may” or words of similar meaning, but these words are not the exclusive means of identifying forward-looking statements.

Forward-looking statements are based on management’s current expectations and assumptions, and are subject to inherent uncertainties, risks and changes in circumstances that are difficult to predict. As a result, actual results could differ materially from those indicated in these forward-looking statements. Factors that could cause actual results to differ materially include global political, economic, business, competitive, market, regulatory and other factors and risks, such as: the impact of macroeconomic conditions and whether industry trends we have identified develop as anticipated; retaining existing partners and attracting new partners, concentration of our revenue in a small number of Retail Card partners, promotion and support of our products by our partners, and financial performance of our partners; cyber-attacks or other security breaches; higher borrowing costs and adverse financial market conditions impacting our funding and liquidity, and any reduction in our credit ratings; our ability to securitize our loans, occurrence of an early amortization of our securitization facilities, loss of the right to service or subservice our securitized loans, and lower payment rates on our securitized loans; our ability to grow our deposits in the future; changes in market interest rates and the impact of any margin compression; effectiveness of our risk management processes and procedures, reliance on models which may be inaccurate or misinterpreted, our ability to manage our credit risk, the sufficiency of our allowance for loan losses and the accuracy of the assumptions or estimates used in preparing our financial statements; our ability to offset increases in our costs in retailer share arrangements; competition in the consumer finance industry; our concentration in the U.S. consumer credit market; our ability to successfully develop and commercialize new or enhanced products and services; our ability to realize the value of strategic investments; reductions in interchange fees; fraudulent activity; failure of third parties to provide various services that are important to our operations; disruptions in the operations of our computer systems and data centers; international risks and compliance and regulatory risks and costs associated with international operations; alleged infringement of intellectual property rights of others and our ability to protect our intellectual property; litigation and regulatory actions; damage to our reputation; our ability to attract, retain and motivate key officers and employees; tax legislation initiatives or challenges to our tax positions and state sales tax rules and regulations; a material indemnification obligation to GE under the Tax Sharing and Separation Agreement with GE (the "TSSA") if we cause the split-off from GE or certain preliminary transactions to fail to qualify for tax-free treatment or in the case of certain significant transfers of our stock following the split-off; regulation, supervision, examination and enforcement of our business by governmental authorities, the impact of the Dodd-Frank Wall Street Reform and Consumer Protection Act (the “Dodd-Frank Act”) and the impact of the Consumer Financial Protection Bureau’s (the “CFPB”) regulation of our business; impact of capital adequacy rules and liquidity requirements; restrictions that limit our ability to pay dividends and repurchase our common stock, and restrictions that limit the Bank’s ability to pay dividends to us; regulations relating to privacy, information security and data protection; use of third-party vendors and ongoing third-party business relationships; and failure to comply with anti-money laundering and anti-terrorism financing laws.

5

For the reasons described above, we caution you against relying on any forward-looking statements, which should also be read in conjunction with the other cautionary statements that are included in “

Item 1A. Risk Factors

.” You should not consider any list of such factors to be an exhaustive statement of all of the risks, uncertainties, or potentially inaccurate assumptions that could cause our current expectations or beliefs to change. Further, any forward-looking statement speaks only as of the date on which it is made, and we undertake no obligation to update or revise any forward-looking statement to reflect events or circumstances after the date on which the statement is made or to reflect the occurrence of unanticipated events, except as otherwise may be required by the federal securities laws.

6

Our Company

____________________________________________________________________________________________

We are one of the premier consumer financial services companies in the United States. Our roots in consumer finance trace back to 1932, and today we are the largest provider of private label credit cards in the United States based on purchase volume and receivables. We provide a range of credit products through programs we have established with a diverse group of national and regional retailers, local merchants, manufacturers, buying groups, industry associations and healthcare service providers, which we refer to as our “partners.” Through our partners’ over

365,000

locations across the United States and Canada, and their websites and mobile applications, we offer their customers a variety of credit products to finance the purchase of goods and services. During

2016

, we financed

$125.5 billion

of purchase volume, and at

December 31, 2016

, we had

$76.3 billion

of loan receivables and

71.9 million

active accounts. Our active accounts represent a geographically diverse group of both consumers and businesses, with an average FICO score of

714

for active accounts at

December 31, 2016

. For the years ended

December 31, 2016

and

2015

, we had net earnings of

$2.3 billion

and

$2.2 billion

, respectively, representing a return on assets of

2.7%

and

2.9%

, respectively.

Our business benefits from longstanding and collaborative relationships with our partners, including some of the nation’s leading retailers and manufacturers with well-known consumer brands, such as Lowe’s, Walmart, Amazon and Ashley Furniture HomeStore. We believe our partner-centric business model has been successful because it aligns our interests with those of our partners and provides substantial value to both our partners and our customers. Our partners promote our credit products because they generate increased sales and strengthen customer loyalty. Our customers benefit from instant access to credit, discounts and promotional offers. We seek to differentiate ourselves through deep partner integration and our extensive marketing expertise. We have omni-channel (in-store, online and mobile) technology and marketing capabilities, which allow us to offer and deliver our credit products instantly to customers across multiple channels. For example, the purchase volume from our online and mobile channels increased by

26%

for the year ended

December 31, 2016

.

We conduct our operations through a single business segment. Our revenue activities are managed through three sales platforms: Retail Card, Payment Solutions and CareCredit. Retail Card is a leading provider of private label credit cards, and also provides Dual Cards, general purpose co-branded credit cards, and small- and medium-sized business credit products. Payment Solutions is a leading provider of promotional financing for major consumer purchases, offering primarily private label credit cards and installment loans. CareCredit is a leading provider of promotional financing to consumers for health and personal care procedures, products or services, such as dental, veterinary, cosmetic, vision and audiology.

We offer our credit products primarily through our wholly-owned subsidiary, the Bank. Through the Bank, we offer, directly to retail and commercial customers, a range of deposit products insured by the Federal Deposit Insurance Corporation (“FDIC”), including certificates of deposit, individual retirement accounts (“IRAs”), money market accounts and savings accounts. We also take deposits at the Bank through third-party securities brokerage firms that offer our FDIC-insured deposit products to their customers. We have significantly expanded our online direct banking operations in recent years and our deposit base serves as a source of stable and diversified low cost funding for our credit activities. At December 31, 2016, we had

$52.1 billion

in deposits, which represented

72%

of our total funding sources.

7

Ownership and Regulation of Synchrony

____________________________________________________________________________________________

The Company was previously an indirectly wholly-owned subsidiary of General Electric Capital Corporation (“GECC”) until the closing of the initial public offering of our common stock (“IPO”) in 2014, which reduced GECC’s ownership in the Company to approximately 84.6% of our common stock. In November 2015, Synchrony Financial became a stand-alone savings and loan holding company following the completion of GE's exchange offer, in which GE exchanged shares of GE common stock for all the remaining shares of our common stock it owned (the “Separation”).

As a savings and loan holding company, the Company is subject to regulation, supervision and examination by the Federal Reserve Board. In addition, as a large provider of consumer financial services, the Company is subject to regulation, supervision and examination by the CFPB.

The Bank is a federally chartered savings association and therefore is subject to regulation, supervision and examination by the Office of the Comptroller of the Currency of the U.S. Treasury (the “OCC”), which is its primary regulator, and by the CFPB. In addition, the Bank, as an insured depository institution, is supervised by the FDIC.

For a discussion of the regulation of the Company and the Bank, see “

—Regulation

.”

Our Sales Platforms

____________________________________________________________________________________________

We offer our credit products through three sales platforms: Retail Card, Payment Solutions and CareCredit. Set forth below is a summary of certain information relating to our Retail Card, Payment Solutions and CareCredit platforms:

Retail Card

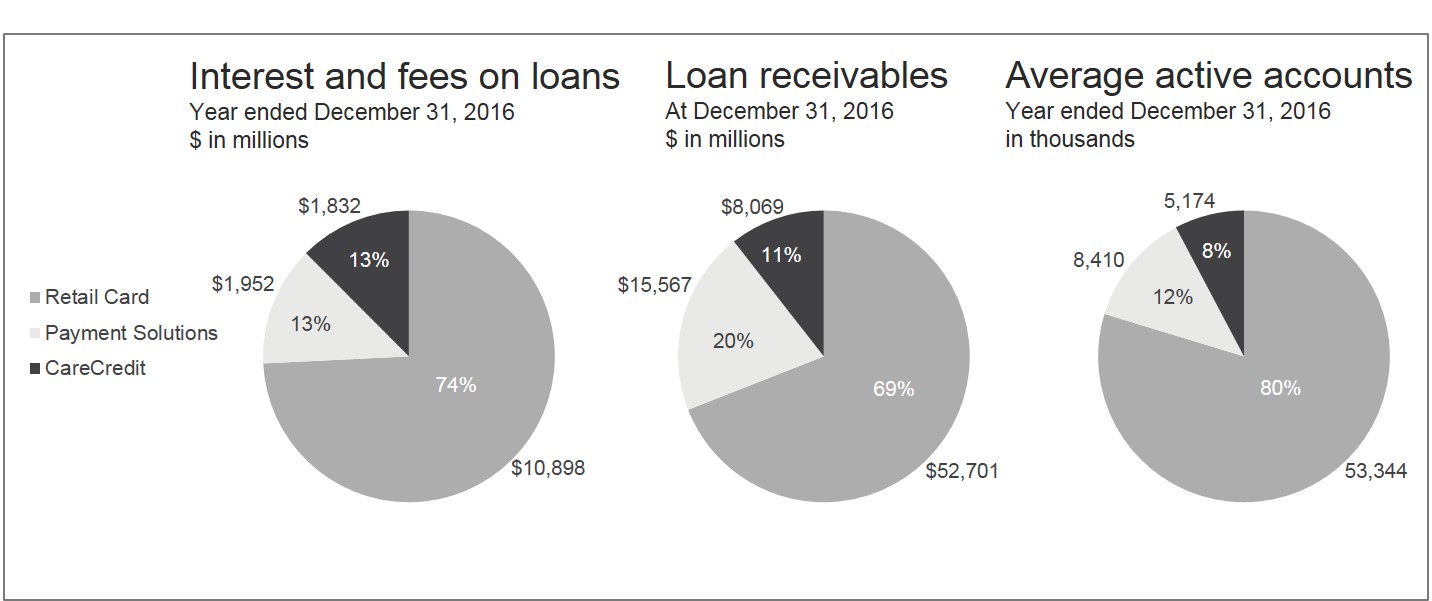

Retail Card is a leading provider of private label credit cards, and also provides Dual Cards, general purpose co-branded credit cards and small- and medium-sized business credit products. Retail Card accounted for

$10.9 billion

, or

74%

, of our total interest and fees on loans for the year ended

December 31, 2016

. Substantially all of the credit extended in this platform is on standard (i.e., non-promotional) terms.

Retail Card’s revenue consists of interest and fees on our loan receivables. Other income earned by the Retail Card sales platform primarily consists of interchange fees earned when our Dual Card or co-brand cards are used outside of our partners’ sales channels and fees paid to us by customers who purchase our debt cancellation products, less loyalty program payments.

8

Retail Card Partners

We have ongoing Retail Card programs with

26

national and regional retailers, which have approximately

45,000

retail locations and include department stores, specialty retailers, mass merchandisers, e-retailers (multi-channel and online retailers) and oil and gas retailers. The average length of our relationship with our ongoing Retail Card partners is

19

years.

During the year ended December 31, 2016, we added the following new Retail Card partners:

|

Programs commenced in 2016:

|

Programs expected to commence in 2017:

|

|

|

Citgo

|

Nissan

|

|

|

Marvel

|

At Home

|

|

|

Google Store

|

Cathay Pacific

|

|

|

Fareportal

|

||

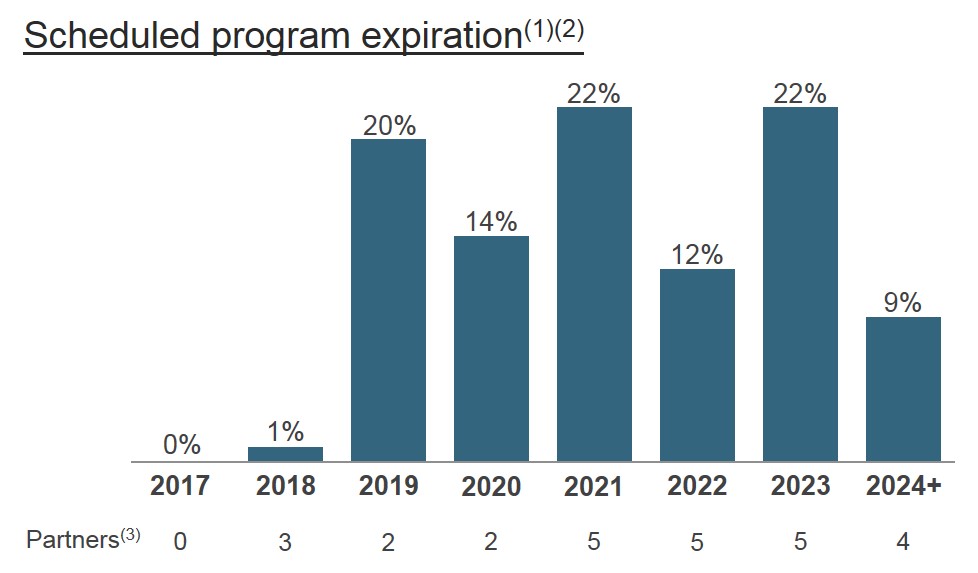

We also extended our program agreements with TJX Companies and Stein Mart during the year ended December 31, 2016. Program agreements accounting for

99%

of Retail Card interest and fees on loans for the year ended December 31, 2016 currently have an expiration date in 2019 or beyond. Set forth below is certain information regarding the current scheduled expiration dates of our ongoing

26

Retail Card partner programs:

9

______________________

|

(1)

|

Percentages stated as a proportion of total Retail Card interest and fees on loans for the year ended December 31, 2016.

|

|

(2)

|

Existing partners as of December 31, 2016 and also reflects the renewal of the Belk program in January 2017.

|

|

(3)

|

Excludes certain credit card portfolios that were sold, have not been renewed, or expire in 2017, which represent less than 1% of our total Retail Card interest and fees on loans for the year ended December 31, 2016.

|

Our five largest programs are with Retail Card partners: Gap, JCPenney, Lowe’s, Sam’s Club and Walmart. These programs accounted in aggregate for 54% of our total interest and fees on loans for the year ended December 31, 2016 and

50%

of loan receivables at December 31, 2016. Our programs with JCPenney, Lowe's and Walmart each accounted for more than 10% of our total interest and fees on loans for the year ended

December 31, 2016

. Sam’s Club is a subsidiary of Walmart that is a separate contracting entity with its own program agreement with us, which we report separately from the Walmart program. For purposes of the information provided in this paragraph with respect to Walmart, the interest and fees on loans from the Sam's Club program have not been included.

The length of our relationship with each of these five Retail Card partners is over

17

years, and in the case of Lowe's, 37 years. All of these program agreements have been renewed in recent years and expire in 2019 or beyond.

Retail Card Program Agreements

Our Retail Card programs are governed by program agreements that are each negotiated separately with our partners. Although the terms of the agreements are partner-specific, and may be amended from time to time, under a typical program agreement our partner agrees to support and promote the program to its customers, but we control credit criteria and issue credit cards to customers who qualify under those criteria. We own the underlying accounts and all loan receivables generated under the program from the time of origination. Other key provisions in the Retail Card program agreements include:

Term

Retail Card program agreements typically have contract terms ranging from approximately five to ten years. Many program agreements have renewal clauses that provide for automatic renewal for one or more years until terminated by us or our partner. We typically seek to renew the program agreements well in advance of their termination dates.

10

Exclusivity

The program agreements typically are exclusive for the products we offer and limit our partners’ ability to originate or promote other private label or co-branded credit cards during the term of the agreement.

Retailer share arrangements

Most of our Retail Card program agreements contain retailer share arrangements that provide for payments to our partner if the economic performance of the program exceeds a contractually-defined threshold. Economic performance for the purposes of these arrangements is typically measured based on agreed upon program revenues (including interest income and certain other income) less agreed upon program expenses (including interest expense, provision for loan losses, retailer payments and operating expenses). We may also provide other economic benefits to our partners such as royalties on purchase volume or payments for new accounts, in some cases instead of retailer share arrangements (for example, on our co-branded credit cards). All of these arrangements align our interests and provide an additional incentive to our partners to promote our credit products.

Other economic terms

In addition to the retailer share arrangements, the program agreements typically provide that the parties will develop a marketing plan to support the program, and they set the terms by which a joint marketing budget is funded, the basic terms of the rewards program linked to the use of our product (such as opportunities to receive double rewards points for purchases made on a Retail Card product), and the allocation of costs related to the rewards program.

Termination

The program agreements set forth the circumstances in which a party may terminate the agreement prior to expiration. Our program agreements generally permit us and our partner to terminate the agreement prior to its scheduled termination date for various reasons, including if the other party materially breaches its obligations. Some program agreements also permit our partner to terminate the program if we fail to meet certain service levels or change certain key cardholder terms or our credit criteria, we fail to achieve certain approval rate targets with respect to approvals of new customers, we elect not to increase the program size when the outstanding loan receivables under the program reach certain thresholds, we are not adequately capitalized, certain force majeure events occur or certain changes in our ownership occur. Certain program agreements are also subject to early termination by a party if the other party has a material adverse change in its financial condition. Historically, these rights have not typically been triggered or exercised. Some of our program agreements provide that, upon termination or expiration, our partner may purchase or designate a third party to purchase the accounts and loan receivables generated with respect to its program at fair market value or a stated price, including all related customer data.

Payment Solutions

Payment Solutions is a leading provider of promotional financing for major consumer purchases, offering private label credit cards and installment loans. Payment Solutions accounted for

$2.0 billion

, or

13%

, of our total interest and fees on loans for the year ended

December 31, 2016

. Substantially all of the credit extended in Payment Solutions is promotional financing.

Payment Solutions’ revenue primarily consists of interest and fees on our loan receivables, including “merchant discounts,” which are fees paid to us by our partners in almost all cases to compensate us for all or part of the foregone interest income associated with promotional financing. The types of promotional financing we offer include: deferred interest (interest accrues during a promotional period and becomes payable if the full purchase amount is not paid off during the promotional period), no interest (no interest on a promotional purchase) and reduced interest (interest is assessed monthly at a promotional interest rate during the promotional period). As a result, during the promotional period we do not generate interest income or generate it at a lower rate, although we continue to generate fee income relating to late fees on required minimum payments.

11

Payment Solutions Partners

In Payment Solutions, we create customized credit programs for national and regional retailers, local merchants, manufacturers, buying groups, industry associations and our own individually-branded industry programs, which are available to local merchants, participating merchants, dealers and retail outlets to provide financing offers to their customers.

At

December 31, 2016

, our Payment Solutions partners had approximately

120,000

retail locations. Payment Solutions is diversified by program, with no one Payment Solutions program accounting for more than 1.2% of our total interest and fees on loans for the year ended

December 31, 2016

. At December 31, 2016, the average length of our relationships with our ten largest Payment Solutions programs was 12 years.

_____________________

|

(1)

|

Based on interest and fees on loans for the year ended December 31, 2016.

|

|

(2)

|

Length of relationship based on Sleepy's, which was subsequently acquired by Mattress Firm.

|

In Payment Solutions, we generally partner with sellers of “big-ticket” products or services (generally priced from $500 to $25,000) to consumers where our financing products provide strong incremental value to our partners and their customers. We also promote all of our programs to sellers through direct marketing activities such as industry trade publications, trade shows and sales efforts by dedicated internal and external sales teams, leveraging our existing partner network or through endorsements from manufacturers, buying groups and industry associations. Our broad array of point of sale technologies and quick enrollment process allow us to quickly and cost-effectively integrate new partners.

During the year ended December 31, 2016, we launched new programs with Mattress Firm and The Container Store, and also extended our program agreements associated with some of our key partner relationships, including Ashley Furniture HomeStore, hhgregg, La-Z-Boy, Nationwide Marketing Group and Suzuki.

12

Payment Solutions Program Agreements

National and Regional Retailers and Manufacturers

The terms of our program agreements with national and regional retailers and manufacturers are typically similar to the terms of our Retail Card program agreements in that we are the exclusive program provider of financing for the national or regional retailer or manufacturer with respect to the financing products that we offer. Some program agreements, however, allow the merchant to use a second source lender after an application has been submitted to us and declined, or in the case of some of our programs, may allow the manufacturer to have several primary lenders. The term of the program agreements generally run from three to five years and are subject to termination prior to the scheduled termination date by us or our partner for various reasons, including if the other party materially breaches its obligations. Some of these programs also permit our partner to terminate the program if we change certain key cardholder terms, exceed certain pricing thresholds, certain force majeure events occur, certain changes in our ownership occur, or there is a material adverse change in our financial condition. A few of these programs also may be terminated at will by the partner on specified notice to us (e.g., several months). Many of these program agreements have renewal clauses which allow the program agreement to be renewed for successive one or more year terms until terminated by us or our partner. We typically negotiate with program participants to renew the program agreements well in advance of their termination dates.

We control credit criteria and issue credit cards or provide installment loans to customers who qualify under those credit criteria. We own the underlying accounts and all loan receivables generated under the program from the time of origination. Our Payment Solutions program agreements set forth the program’s economic terms, including the merchant discount applicable to each promotional finance offering. We typically do not pay fees to our Payment Solutions partners pursuant to any retailer share arrangements, but in some cases we pay a sign-up fee to a partner or provide volume-based rebates on the merchant discount paid by the partner. In addition to the credit programs, we also process general purpose card transactions for some merchants and dealers under programs with manufacturers as their acquiring bank within most of the credit card network associations, for which we receive an interchange fee.

Buying Groups and Industry Associations

The programs we have established with buying groups and industry associations, such as the Home Furnishings Association, Jewelers of America and MEGA Group USA, are governed by program agreements under which we make our credit products available to their respective members or dealers, but these agreements generally do not require the members or dealers to offer our products to their customers. Under the terms of the program agreements, buying groups and industry associations generally agree to support and promote the respective programs. These arrangements may include sign-up fees and volume-based incentives paid by us to the groups and their members.

Individually-Branded Programs

Our individually-branded programs are focused on specific industries, where we create either company-branded or company and partner-branded private label credit cards that are usable across all participating locations within the industry-specific network. For example, our Synchrony Car Care program, comprised of merchants selling automotive parts, repair services and tires, covers over

27,000

locations across the United States, and cards issued may be dual branded with Synchrony Car Care and partners such as Midas, Michelin Tires or Pep Boys. Under the terms of these programs, we establish merchant discounts applicable to each financing offer, and, in some cases, the fees we charge partners for their membership in the network.

Dealer Agreements

For the programs we have established with manufacturers, buying groups, industry associations and individually-branded programs described above, we enter into individual agreements with the merchants and dealers that offer our credit products under these programs. These agreements generally are not exclusive and some parties who offer our financing products also offer financing from our competitors. Our agreements generally continue until terminated by either party, with termination typically available to either party at will upon 15 days’ written notice. Our dealer agreements set forth the economic terms associated with the program, including the fees charged to dealers to offer promotional financing, and in some cases allow us to periodically change the fees we charge.

13

CareCredit

CareCredit is a leading provider of promotional financing to consumers for health and personal care procedures, products or services. CareCredit accounted for

$1.8 billion

, or

13%

, of our total interest and fees on loans for the year ended

December 31, 2016

. Substantially all of the credit extended in CareCredit is promotional financing.

We offer customers a CareCredit-branded private label credit card that may be used across our network of CareCredit providers. We generate revenue in CareCredit primarily from interest and fees on our loan receivables and from merchant discounts paid by providers to compensate us for all or part of the foregone interest income associated with promotional financing. We also process general purpose card transactions for some providers as their acquiring bank within most of the credit card network associations, for which we obtain an interchange fee.

CareCredit Partners

The vast majority of our partners are individual and small groups of independent healthcare providers, which includes networks of healthcare practitioners that provide elective and other procedures that generally are not fully covered by insurance. The remainder are primarily national and regional healthcare providers and health-focused retailers, including Rite Aid.

During

2016

, over 185,000 locations either processed a CareCredit application or made a sale on a CareCredit credit card. No one CareCredit partner accounted for more than

0.3%

of our total interest and fees on loans for the year ended

December 31, 2016

.

We enter into provider agreements with individual healthcare providers who become part of our CareCredit network. These provider agreements are similar to the dealer agreements that govern our relationships with the merchants and dealers offering our Payment Solutions products in that the agreements are not exclusive and typically may be terminated at will upon 15 days’ notice. Multi-year agreements are in place for larger multi-location relationships across all markets. There are typically no retailer share arrangements with partners in CareCredit.

At

December 31, 2016

, we had relationships with over

100

professional and other associations (including the American Dental Association and the American Animal Hospital Association), manufacturers and buying groups, which endorse and promote our credit products to their members. Of these relationships, over

60

were paid endorsements linked to member enrollment in, and volume under, the relevant program.

14

We screen potential partners using a variety of criteria, including whether the potential provider specializes in one of our approved specialties, carries the appropriate licensing and certifications, and meets our underwriting criteria. We also screen potential partners for reputational issues. We work with professional and other associations, manufacturers, buying groups, industry associations and healthcare consultants to educate their constituents about the products and services we offer. We believe our ability to attract new partners is aided by our customer satisfaction rate, which our research in

2016

showed is

91%

. We also approach individual healthcare service providers through direct mail and advertising, and at trade shows.

During the year ended

December 31, 2016

, we renewed VCA Animal Hospitals in our network of providers and renewed our CareCredit endorsement relationships with the American Dental Association and American Society of Plastic Surgeons.

Our Customers

____________________________________________________________________________________________

Acquiring and Marketing to Retail Card & Payment Solutions Customers

We work directly with our partners using their distribution network, communication channels and customer interactions to market our products to their customers and potential customers. We believe our presence at our partners’ points of sale and our ability to make credit decisions instantly for a customer that is already predisposed to make a purchase enables us to acquire new customer accounts at significantly lower costs than general purpose card issuers, who typically market directly to consumers through mass mailings and advertising.

To acquire new customers, we collaborate with our partners and leverage our marketing expertise to create marketing programs that promote our products to creditworthy customers. Frequently, our partners market the availability of credit as part of (and with little incremental cost to) the advertising for their goods and services. Our marketing programs include marketing offers (e.g., 10% off the customer’s first purchase) and consumer communications that are delivered through a variety of channels, including in-store signage, online advertising, retailer website placement, associate communication, emails, text messages, direct mail campaigns, advertising circulars, and outside marketing via television, radio and print. We also employ our proprietary Quickscreen and eQuickscreen acquisition methods to make targeted pre-approved credit offers at the point-of-sale both in-store and online. Our Quickscreen and eQuickscreen technology allows us to run customer information that we have obtained from our partners through our risk models in advance so that when these customers seek to make payment for goods and services at our partners in-store or online point of sale, we can make a credit offer instantly, if appropriate. Based on our experience, due to the personalized and immediate nature of the offer, Quickscreen and eQuickscreen significantly outperform traditional direct-to-consumer pre-approved channels, such as direct mail or email, in response rate and dollar spending.

Acquiring and Marketing to CareCredit Customers

We market our products through our provider network by training our network providers on the advantages of CareCredit products and by making marketing materials available for providers to use to promote the program and educate customers. Our training helps our providers learn to discuss payment options during the pre-treatment consultation phase, including the option to apply for a CareCredit credit card and the offer of promotional credit. According to a 2016 survey of our CareCredit customers,

47%

indicated that they would have postponed or reduced the scope of treatment if financing was not offered by their provider. Consumers can apply for our CareCredit products in the provider’s office and/or online via the web or mobile device.

We also market our products to potential and existing customers directly through our web-based partner locator, which allows customers to search for healthcare service providers that accept the CareCredit credit card by desired geography and provider type. According to our records, our CareCredit partner locator averaged over

850,000

hits per month during the year ended

December 31, 2016

. We believe our partners recognize the locator as an important source of new customer acquisition.

15

Enterprise Customer Engagement ("ECE") / Analytics

After a customer obtains one of our products, our marketing programs encourage card utilization by continuing to communicate our products’ value propositions (such as, depending on the program, promotional financing offers, cardholder events, product discounts, dollar-off certificates, account holder sales, reward points and offers, new product announcements and previews, and free or reduced cost gift wrapping, alteration or delivery services) through our partners’ and our distribution channels.

Through our ECE and data analytics teams, we track cardholder responsiveness to our marketing programs and use this research to target marketing messages and promotional offers to cardholders based on their individual characteristics, such as length of relationship and spending pattern. For example, if a cardholder responds positively to a coupon sent by text message, we will tailor future marketing messages so that they are delivered by text message. Our ability to target marketing messages and promotions is enhanced for Dual Card and general purpose co-branded credit card programs because we receive, collect and analyze data on in-network and all other spending.

Our extensive marketing activities targeted to existing customers have yielded high levels of re-use across both our Payment Solutions and CareCredit sales platforms. During the year ended

December 31, 2016

,

27%

and

51%

of purchase volume across our Payment Solutions platform and CareCredit network, respectively, resulted from repeat use at one or more retailers or providers.

Digital and mobile capabilities

We continue to develop our digital capabilities to help drive an improved mobile and online experience for our customers. Our mobile applications deliver customized features, including rewards, retail offers, and alerts. We also have enhanced the digital capabilities of our online banking experience, which, among other things, allows customers to access their accounts from any device. In 2016, we launched SyPi™, a fully-integrated Synchrony plug-in credit feature for our retailers’ apps, which allows credit card holders to easily shop, redeem rewards, and securely manage and make payments on their accounts via their mobile device. SyPi is also inclusive of our proprietary digital card product, which offers customers an easy way to complete transactions in our retailers’ stores without a physical card. We also launched new digital solutions including Pay My Provider™, a post-care bill payment application for CareCredit, and several new digital credit acquisition platforms including tablet applications for our field sales team and our home improvement partners to take credit applications in-stores and in-home. Additionally, we developed a new dApply application for consumers to apply for credit from any device.

We continue to invest in upgrading our digital customer experience with the launch of a fully redesigned Consumer Center for online account servicing for our Payment Solutions and CareCredit customers, and the continued rollout of our revamped eService for our Retail Card partners. We also continue to expand the use of our credit cards within various mobile wallets, such as Apple Pay and Samsung Pay, in order to further enhance the user experience for our customers.

Loyalty Programs

The retail loyalty programs we manage typically provide cardholders with rewards in the form of merchandise discounts that are earned by achieving a pre-set spending level on their private label credit card, Dual Card or general purpose co-branded credit card. The merchandise discounts can be mailed to the cardholder, accessed digitally, or may be immediately redeemable at the partner’s store. Other programs provide cash back or reward points, which are redeemable for a variety of products or awards. These loyalty programs are designed to generate incremental purchase volume per customer, while reinforcing the value of the card to the customer and strengthening customer loyalty. We continue to provide loyalty programs to customers that utilize non-credit payment types such as cash, debit or check. These multi-tender loyalty programs will allow our partners to market to an expanded customer base, and allow us access to additional prospective cardholders.

16

Commercial Customers

In addition to our efforts to acquire consumer cardholders, we are increasing our focus on small to mid-sized commercial customers. We offer these customers private label credit cards and Dual Cards that can be used primarily at our Retail Card partners and are similar to our consumer offerings. We are also increasing our focus on marketing our commercial pay-in-full accounts receivable product that supports a wide range of business customers.

Our Credit Products

____________________________________________________________________________________________

Through our platforms, we offer three principal types of credit products: credit cards, commercial credit products and consumer installment loans. We also offer a debt cancellation product.

The following table sets forth each credit product by type and indicates the percentage of our total loan receivables that are under standard terms only or pursuant to a promotional financing offer at

December 31, 2016

.

|

Promotional Offer

|

|||||||||||

|

Credit Product

|

Standard Terms Only

|

Deferred Interest

|

Other Promotional

|

Total

|

|||||||

|

Credit cards

|

67.1

|

%

|

16.5

|

%

|

12.8

|

%

|

96.4

|

%

|

|||

|

Consumer installment loans

|

—

|

|

—

|

|

1.8

|

|

1.8

|

|

|||

|

Commercial credit products

|

1.7

|

%

|

—

|

|

—

|

|

1.7

|

|

|||

|

Other

|

0.1

|

|

—

|

|

—

|

|

0.1

|

|

|||

|

Total

|

68.9

|

%

|

16.5

|

%

|

14.6

|

%

|

100.0

|

%

|

|||

Credit Cards

Our credit card products are loans we extend through open-ended revolving credit card accounts. We offer the following principal types of credit cards:

Private Label Credit Cards

Private label credit cards are partner-branded credit cards (e.g., Lowe’s or Amazon) or program-branded credit cards (e.g., Synchrony Car Care or CareCredit) that are used primarily for the purchase of goods and services from the partner or within the program network. In addition, in some cases, cardholders may be permitted to access their credit card accounts for cash advances.

Credit under a private label credit card typically is extended either on standard terms only in our Retail Card sales platform, which means accounts are assessed periodic interest charges using an agreed non-promotional fixed and/or variable interest rate, or pursuant to a promotional financing offer in our Payment Solutions and CareCredit sales platforms, involving deferred interest, no interest or reduced interest during a set promotional period. Promotional periods typically range between six and 48 months, but we may agree to longer terms with the partner. In almost all cases we receive a merchant discount from our partners to compensate us for all or part of the foregone interest income associated with promotional financing. The terms of these promotions vary by partner, but generally the longer the deferred interest, reduced interest or interest-free period, the greater the partner’s merchant discount. Some offers permit customers to pay for a purchase in equal monthly payments with no interest or at a reduced interest rate, rather than deferring or delaying interest charges. For our deferred interest products, approximately

75%

to

80%

of customer transactions are typically paid off before interest is assessed. In CareCredit, standard rate financing generally applies to charges under $200.

17

We typically do not charge interchange or other fees to our partners when a customer uses a private label credit card to purchase our partners’ goods and services through our payment system.

Most of our private label credit card business is in the United States. For some of our partners who have locations in Canada, we also support the issuance and acceptance of private label credit cards at their locations in Canada and from customers in Canada.

Dual Cards

and General Purpose Co-Brand Cards

Our patented Dual Cards are credit cards that function as private label credit cards when used to make purchases of goods or services from our partners, and as general purpose credit cards when used to make purchases from other retailers wherever cards from those card networks are accepted or for cash advance transactions. We currently issue Dual Cards for use on the MasterCard and Visa networks and we currently have the ability to issue Dual Cards for use on the American Express and Discover networks.

We have been granted two U.S. patents relating to the process by which our Dual Cards function as a private label credit card when used to make purchases from our partners and function as a general purpose credit card when used on the systems of other credit card associations.

We also offer general purpose co-branded credit cards that do not also function as private label credit cards.

Credit extended under our Dual Cards and general purpose co-branded credit cards typically is extended on standard terms only. Currently, only Retail Card offers Dual Cards and general purpose co-branded credit cards. At

December 31, 2016

, we offered Dual Card or general purpose co-branded credit cards through

18

of our

26

ongoing Retail Card programs, of which the majority are Dual Cards. We expect to continue to increase the number of partner programs that offer Dual Cards or general purpose co-branded credit cards and seek to increase the portion of our loan receivables attributable to these products.

Charges using a Dual Card or general purpose co-branded credit card generate interchange income for us in connection with purchases made by cardholders other than in-store or online from that partner.

We currently do not issue Dual Cards or general purpose co-branded credit cards in Canada.

Terms and Conditions

As a general matter, the financial terms and conditions governing our credit card products vary by program and product type and change over time, although we seek to standardize the non-financial provisions consistently across all products. The terms and conditions of our credit card products are governed by a cardholder agreement and applicable laws and regulations.

We assign each card account a credit limit when the account is initially opened. Thereafter, we may increase or decrease individual credit limits from time to time, at our discretion, based primarily on our evaluation of the customer’s creditworthiness and ability to pay.

For the vast majority of accounts, periodic interest charges are calculated using the daily balance method, which results in daily compounding of periodic interest charges, subject to, at times, a grace period on new purchases. Cash advances are not subject to a grace period, and some credit card programs do not provide a grace period for promotional purchases. In addition to periodic interest charges, we may impose other charges and fees on credit card accounts, including, as applicable and provided in the cardholder agreement, cash advance transaction fees and late fees where a customer has not paid at least the minimum payment due by the required due date.

Typically, each customer with an outstanding debit balance on his or her credit card account must make a minimum payment each month. A customer may pay the total amount due at any time without penalty. We also may enter into arrangements with delinquent customers to extend or otherwise change payment schedules and to waive interest charges and/or fees.

18

Commercial Credit Products

We offer private label cards and Dual Cards for commercial customers that are similar to our consumer offerings. We also offer a commercial pay-in-full accounts receivable product to a wide range of business customers. We offer commercial credit products primarily through our Retail Card platform to the commercial customers of our Retail Card partners.

Installment Loans

In Payment Solutions, we originate installment loans to consumers (and a limited number of commercial customers) in the United States, primarily in the power products market. Installment loans are closed-end credit accounts where the customer pays down the outstanding balance in installments. The terms of our installment loans are governed by customer agreements and applicable laws and regulations.

Installment loans are assessed periodic interest charges using fixed interest rates. In addition to periodic interest charges, we may impose other charges and fees on loan accounts, including late fees where a customer has not made the required payment by the required due date and returned payment fees.

We offer a debt cancellation product to our credit card customers online and, on a limited basis, by direct mail. Customers who choose to purchase this product are charged a monthly fee based on their ending balance on each billing statement. In return, the Bank will cancel all or a portion of a customer’s credit card balance in the event of certain qualifying life events.

Direct Banking

__________________________________________________________________________________________

Through the Bank, we offer our customers a range of FDIC-insured deposit products. The Bank also takes deposits through third-party securities brokerage firms that offer our FDIC-insured deposit products to their customers. At

December 31, 2016

, we had

$52.1 billion

in deposits,

$37.9 billion

of which were direct deposits (which includes deposits from banks and financial institutions) and

$14.2 billion

of which were brokered deposits. During 2016, direct deposits were received from approximately

300,000

customers that had a total of over

535,000

accounts. Retail customers accounted for

99%

of our direct deposits (by volume) at

December 31, 2016

. The Bank had a

91%

retention rate on certificates of deposit balances up for renewal for the year ended

December 31, 2016

. FDIC insurance is provided for our deposit products up to applicable limits.

We have significantly expanded our online direct banking operations in recent years and our deposit base serves as a source of stable and diversified low cost funding for our credit activities. Our online platform is highly scalable allowing us to expand without having to rely on a traditional “brick and mortar” branch network. We expect the continued growth in our direct banking platform to come primarily from retail deposits.

We are growing our direct banking operations and believe we are well-positioned to benefit from the consumer-driven shift from branch banking to direct banking. According to the 2016 American Bankers Association survey, the percentage of customers who prefer to do their banking via direct channels (internet, mail, phone and mobile) was

80%

, while those who prefer branch banking was only

14%

.

Our deposit products include certificates of deposit, IRAs, money market accounts and savings accounts. We market our deposit products through multiple channels including digital and print. Customers can apply for, fund, and service their deposit accounts at our branch in Bridgewater, NJ, online or via phone. We have dedicated banking representatives within our call centers to service deposit accounts.

To attract new deposits and retain existing ones, we intend to introduce new deposit products and enhancements to our existing products. These new and enhanced products may include the introduction of checking accounts, overdraft protection lines of credit, a bill payment and person-to-person payment features, and Synchrony-branded debit cards. Our focus on deposit-taking and related branding efforts will also enable us to offer other branded direct-banking products more efficiently in the future.

19

During 2016, we transitioned the core banking and deposit services provided by Fidelity National Information Services, Inc. to Fiserv, Inc. ("Fiserv"). Fiserv provides our platform for online retail deposits including a customer-facing account opening and servicing platform.

We seek to differentiate our deposit product offerings from our competitors on the basis of brand, reputation, convenience, customer service and value. Our deposit products emphasize reliability, trust, security, convenience and attractive rates. We

offer rewards to customers based on their tenure or balance amounts, including reduced fees, travel offers and concierge telephone support.

Credit Risk Management

____________________________________________________________________________________________

Credit risk management is a critical component of our management and growth strategy. Credit risk refers to the risk of loss arising from customer default when customers are unable or unwilling to meet their financial obligations to us. Our credit risk arising from credit products is generally highly diversified across over

125 million

open accounts at

December 31, 2016

, without significant individual exposures. We manage credit risk primarily according to customer segments and product types.

Customer Account Acquisition

We have developed programs to promote credit with each of our partners and have developed varying credit decision guidelines for the different partners. We originate credit accounts through several different channels, including in-store, mail, internet, mobile, telephone and pre-approved solicitations. In addition, we have, and may in the future acquire, accounts that were originated by third parties in connection with establishing programs with new partners.

Regardless of the channel, in making the initial credit approval decision to open a credit card or other account or otherwise grant credit, we follow a series of credit risk and underwriting procedures. In most cases, when applications are made in-store or by internet or mobile, the process is fully automated and applicants are notified of our credit decision immediately. We generally obtain certain information provided by the applicant and obtain a credit bureau report from one of the major credit bureaus. The credit report information we obtain is electronically transmitted into industry scoring models and our proprietary scoring models developed to calculate a credit score. The risk management team determines in advance the qualifying credit scores and initial credit line assignments for each portfolio and product type. We periodically analyze performance trends of accounts originated at different score levels as compared to projected performance, and adjust the minimum score or the opening credit limit to manage risk. Different scoring models may be used depending upon bureau type and account source.

We also apply additional application screens based on various inputs, including credit bureau information, to help identify potential fraud and prior bankruptcies before qualifying the application for approval. We compare applicants’ names against the Specially Designated Nationals list maintained by the Office of Foreign Assets Control of the U.S. Department of the Treasury (“OFAC”), as well as screens that account for adherence to USA PATRIOT Act of 2001 (the “Patriot Act”) and Credit Card Accountability Responsibility and Disclosure Act of 2009 (the “CARD Act”) requirements, including ability to pay requirements.

We also use pre-approved account solicitations for certain programs. Potential applicants are pre-screened using information provided by our partner or obtained from outside lists, and qualified individuals receive a pre-approved credit offer by mail or email.

20

Acquired Portfolio Evaluation

Our risk management team evaluates each portfolio that we acquire in connection with establishing programs with new partners to ensure the portfolio satisfies our credit risk guidelines. As part of this review, we receive data on the third-party accounts and loans, which allows us to assess the portfolio on the basis of certain core characteristics, such as historical performance of the assets and distributions of credit and loss information. In addition, we benchmark potential portfolio acquisitions against our existing programs to assess relative current and projected risks. Finally, our risk management team must approve the acquisition, taking into account the results of our risk assessment process. Once assets are migrated to our systems, our account management protocols will apply immediately as described below under “

—Customer Account Management

,” “

—Credit Authorizations of Individual Transactions

” and “

—Collections

.”

Customer Account Management

We regularly assess the credit risk exposure of our customer accounts. This ongoing assessment includes information relating to the customer’s performance with respect to its account with us, as well as information from credit bureaus relating to the customer’s broader credit performance. To monitor and control the quality of our loan portfolio (including the portion of the portfolio originated by third parties), we use behavioral scoring models that we have developed to score each active account on its monthly cycle date. Proprietary risk models, together with the FICO scores obtained on each active account no less than quarterly, are an integral part of our credit decision-making process. Depending on the duration of the customer’s account, risk profile and other performance metrics, the account may be subject to a range of account actions, including limits on transaction authorization and increases or decreases in purchase and cash credit limits.

Credit Authorizations of Individual Transactions

Once an account has been opened, when a credit card is used to make a purchase in-store at one of our partners’ locations or online, point-of-sale terminals or online sites have an online connection with our credit authorization system, which allows for real-time updating of accounts. Each potential sales transaction is passed through a transaction authorization system, which takes into account a variety of behavior and risk factors to determine whether the transaction should be approved or declined, and whether a credit limit adjustment is warranted.

Fraud Investigation

We provide follow up and research with respect to different types of fraud such as fraud rings, new account fraud and transactional fraud. We have developed a proprietary fraud model to identify new account fraud and deployed tools that help identify transaction purchase behavior outside a customer’s established pattern. Our proprietary model is also complemented by externally sourced models and tools used across the industry to better identify fraud and protect our customers. We also are continuously implementing new and improved technologies to detect and prevent fraud such as utilizing embedded security chips ("EMV") for our active Dual Card and general purpose co-branded credit card products with all of our retail partners.

Collections

All monthly billing statements of accounts with past due amounts include a request for payment of these amounts. Collections personnel generally initiate contact with customers within 30 days after any portion of their balance becomes past due. The nature and the timing of the initial contact, typically a personal call, e-mail, text message or letter, are determined by a review of the customer’s prior account activity and payment habits.

We re-evaluate our collection efforts and consider the implementation of other techniques, including internal collection activities, use of external vendors and the sale of debt to third-party buyers, as a customer becomes increasingly delinquent. We limit our exposure to delinquencies through controls within the transaction authorization processes, the imposition of credit limits and criteria-based account suspension and revocation processes. In certain situations, we may enter into arrangements to extend or otherwise change payment schedules, decrease interest rates and/or waive fees to aid customers experiencing financial difficulties in their efforts to become current on their obligations to us.

21

Customer Service

____________________________________________________________________________________________

Customer service is an important feature of our relationship with our partners. Our customers can contact us via phone, mail, email, eService and eChat. During the year ended

December 31, 2016

, we handled approximately

260 million

calls.

We assign a dedicated toll-free customer service phone number to each of our Retail Card programs. Our Payment Solutions customers access customer service through one general purpose toll-free customer service phone number (except for a few large Payment Solutions programs, which have dedicated toll-free numbers). Our CareCredit platform has its own, dedicated toll-free customer service phone number. We also have dedicated toll-free customer service phone numbers for our deposit business.

We service all programs through our ten domestic and two off-shore call centers. We also provide phone-based customer service through a third-party vendor. Our off-shore facilities are located in Hyderabad, India and Manila, Philippines. We blend domestic and off-shore locations as an important part of our servicing strategy, to maintain service availability beyond normal work hours in the U.S. and to seek optimal costs. Customer service for cards issued to customers in Canada is supported through agents based in the United States.

Given the nature of our business and the high volume of calls, we maintain several centers of excellence to ensure the quality of our customer service across all of our sites. These centers of excellence consist of quality assurance, customer experience, training, workforce and capacity planning, surveillance and process control, tactical operations center, business solutions and technology support.

Production Services

____________________________________________________________________________________________

Our production services organization oversees a number of services, including:

|

•

|

payment processing (more than

605 million

paper and electronic payments in

2016

);

|

|

•

|

embossing and mailing credit cards (more than

55 million

cards in

2016

);

|

|

•

|

printing and mailing and eService delivery of credit card statements (more than

720 million

paper and electronic statements in

2016

); and

|

|

•

|

other letters mailed or sent electronically (more than

80 million

in

2016

).

|

All United States customer payments received by mail are processed at one of two centers located in Atlanta, Georgia and Longwood, Florida, both of which are operated by the Bank. United States credit card statement printing and mailing, card embossing and mailing and letter production and mailing for customers are provided through outsourced services with First Data Corporation (“First Data”). While these services are outsourced, we monitor and maintain oversight of these other services. First Data also produces our statements and other mailings for deposit customers.

Card production embossing, mailing, statement printing and mailing services related to cards issued to customers in Canada are outsourced to Canadian suppliers.

22

Technology and Data Security

____________________________________________________________________________________________

Products and Services

We leverage information technology and deliver products and services that meet the needs of our partners and enable us to operate our business efficiently. The integration of our technology with our partners is at the core of our value proposition, enabling, among other things, customers to “apply and buy” at the point of sale, and many of our partners to settle transactions directly with us without an interchange fee. A key part of our strategic focus is the continued development of innovative, efficient, flexible technology and operational platforms to support marketing, risk management, account acquisition and account management, customer service, and new product development. We believe that the continued investment in and development of these platforms is an important part of our efforts to increase our competitive capabilities, reduce costs, improve quality and provide faster, more flexible technology services. Therefore, we continuously review capabilities and develop or acquire systems, processes and competencies to meet our business needs.

As part of our continuous efforts to enhance our technologies, we may either develop these capabilities internally or in partnership with third-party providers. We rely on third-party providers to help us deliver systems and operational infrastructure based on strategies and, in some cases, architecture, designed by us. These relationships include: First Data for our credit card transaction processing and production and Fiserv for retail banking.

Data Security

The protection and security of financial and personal information of our consumers is one of our highest priorities. We have implemented a comprehensive information security program that includes administrative, technical and physical safeguards and provides an appropriate level of protection to maintain the confidentiality, integrity, and availability of our Company's and our customers' information. This includes protecting against any known or evolving threats to the security or integrity of customer records and information, and against unauthorized access to or use of customer records or information.

Our information security program is intelligence-led, focused on continuously adapting to an evolving landscape of emerging threats and available technology. Through data gathering and evaluation of emerging threats from internal and external incidents and technology investment, security controls are adjusted on a continuous basis. We work directly with our partners on an ongoing basis to expand our intelligence ecosystem and facilitate awareness and communications of events outside of the Company.

We have developed a security strategy and implemented multiple layers of controls embedded throughout our technology environment that establish multiple control points between threats and our assets. Our security program is designed to provide oversight of third parties who store, process or have access to sensitive data, and we require the same level of protection from such third-party service providers. We evaluate the effectiveness of the key security controls through ongoing assessment and measurement.

In addition, we identify risks that may threaten customer information and perform a variety of vulnerability and penetration testing on the platforms, systems and applications used to provide our products and services. We employ backup and disaster recovery procedures for all the systems that are used for storing, processing and transferring customer information, and we periodically test and validate our disaster recovery plans. We are compliant with the Payment Card Industry (PCI) program.

In connection with the Separation, we have completed the migration of the majority of the transitional services relating to technology and business processes provided by GE. The exit of these remaining services includes the migration of very limited portions of our technology operating environment. As a stand-alone company, our corporate infrastructure is more focused and simplified, creating greater security and resiliency for our clients, partners and customers.

23

Competition

____________________________________________________________________________________________